Artificial Intelligence In Hospital Operations Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.29 Billion |

| Market Size (2031) | USD 18.36 Billion |

| Growth Rate (2026 - 2031) | 28.25% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

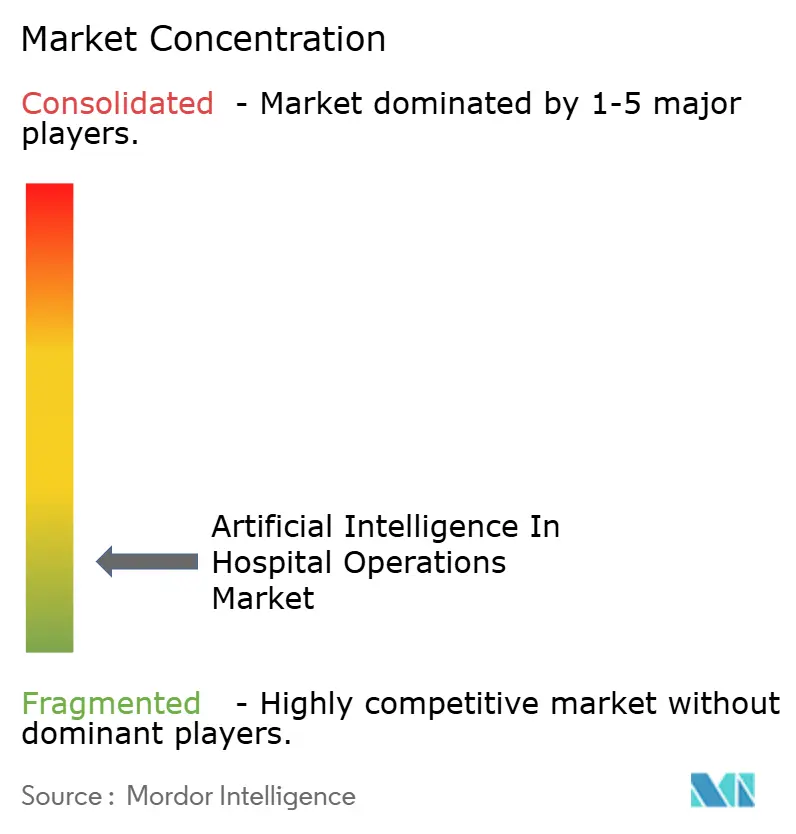

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Artificial Intelligence In Hospital Operations Market Analysis by Mordor Intelligence

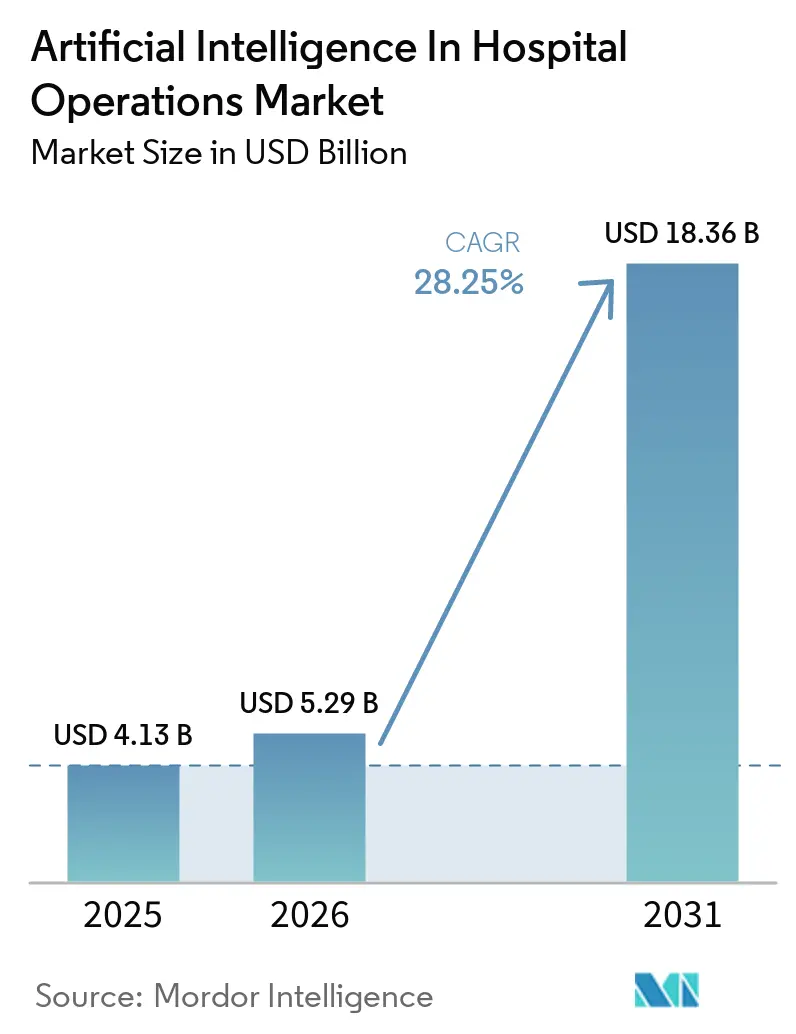

The Artificial Intelligence In Hospital Operations Market size is projected to be USD 4.13 billion in 2025, USD 5.29 billion in 2026, and reach USD 18.36 billion by 2031, growing at a CAGR of 28.25% from 2026 to 2031.

The market is moving into broader deployment because hospital staffing shortages have turned scheduling, documentation support, and administrative automation into operational priorities rather than optional pilots, with Duke Health reporting 95% staffing forecast accuracy up to 14 days in advance and a 50% reduction in temporary labor after deploying predictive staffing tools. The Artificial Intelligence in Hospital Operations market is also benefiting from payment reform, as the CMS Transforming Episode Accountability Model began on January 1, 2026 and now places 745 hospitals across 188 markets under bundled-payment accountability for selected surgical episodes, which raises immediate demand for discharge coordination and post-acute management tools. The Artificial Intelligence in Hospital Operations market is becoming easier to access for mid-size health systems because cloud-based operational platforms and hybrid command-center models are reducing the technical burden tied to deployment, retraining, and cross-site visibility. Competitive pressure is rising as large EHR vendors push deeper into workflow orchestration while focused vendors defend their position through faster deployment, deeper integration, and outcome-based delivery models. The main constraint remains execution, since high implementation costs, uneven organizational readiness, and growing cyber exposure still favor vendors that can phase deployment and support stronger governance from day 1.

Key Report Takeaways

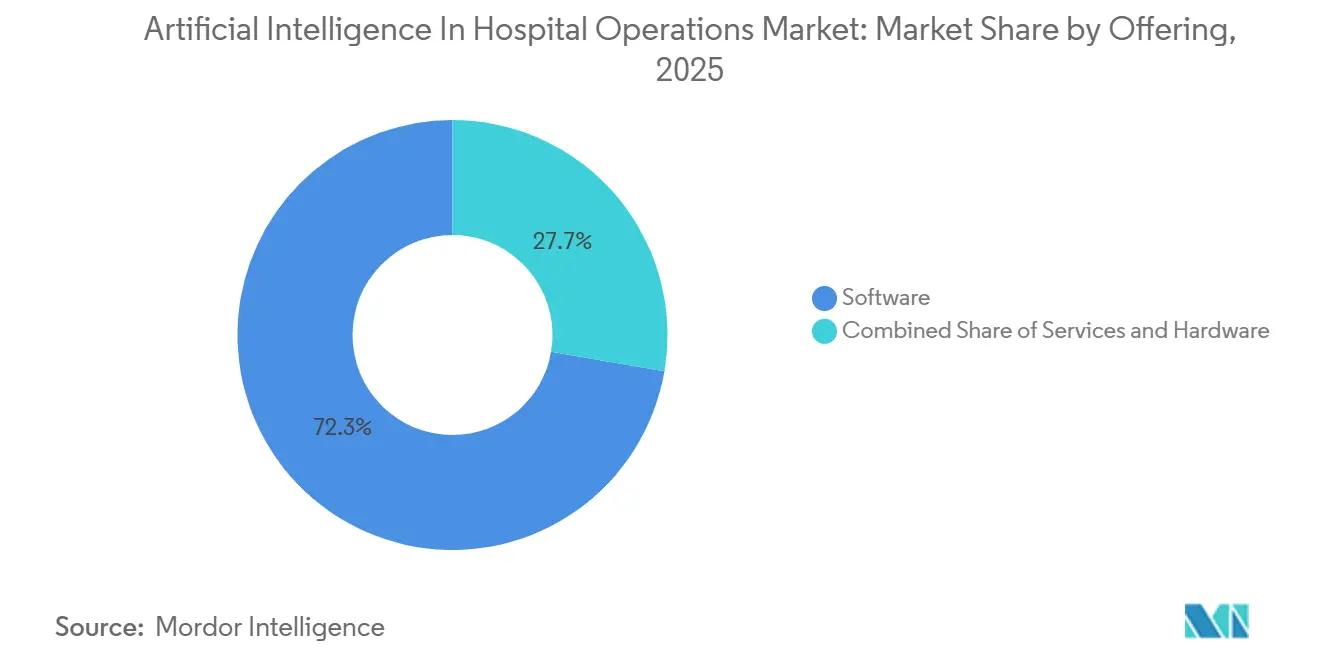

- By offering, software held 72.31% of the Artificial Intelligence in Hospital Operations market share in 2025, while services is forecast to expand at a 29.38% CAGR through 2031.

- By use case, Revenue Cycle and Administrative Automation accounted for 25.24% of the Artificial Intelligence in Hospital Operations market size in 2025, while Command Center and Operational Decision Support is projected to advance at a 29.52% CAGR through 2031.

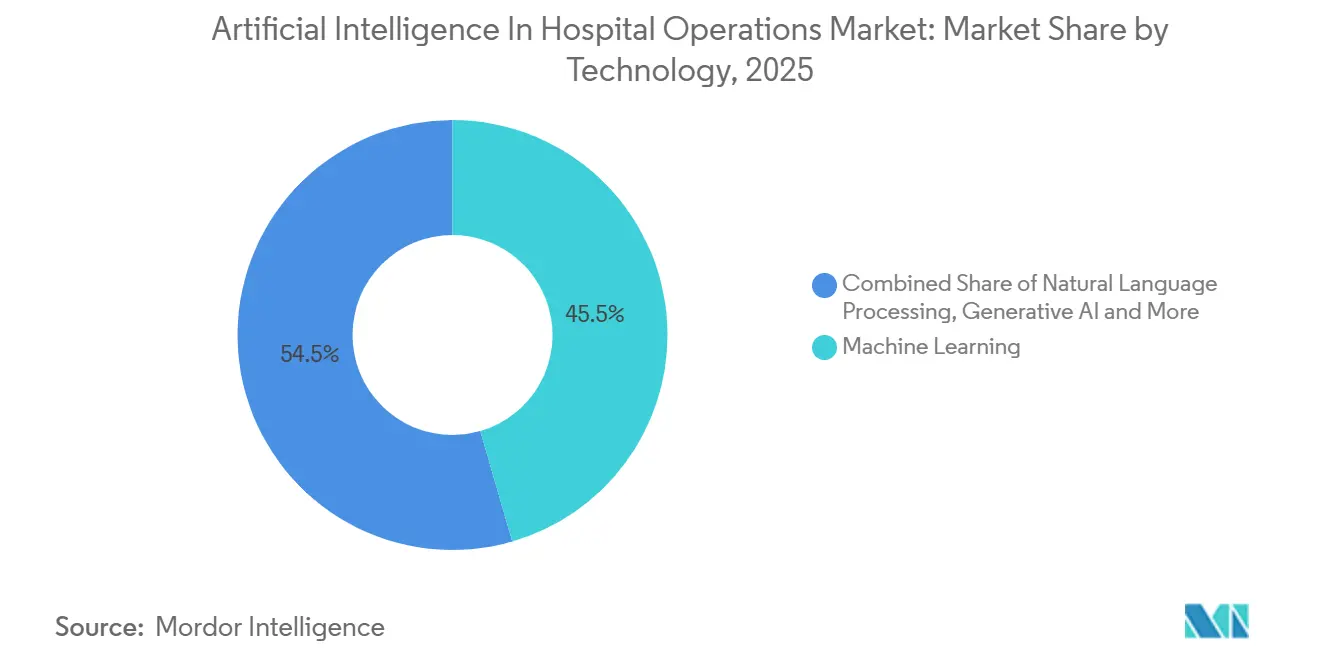

- By technology, machine learning led with a 45.52% share in 2025, while Natural Language Processing is forecast to grow at a 29.25% CAGR through 2031.

- By deployment model, cloud accounted for a 61.24% share in 2025 and is also projected to record the fastest CAGR at 30.83% through 2031.

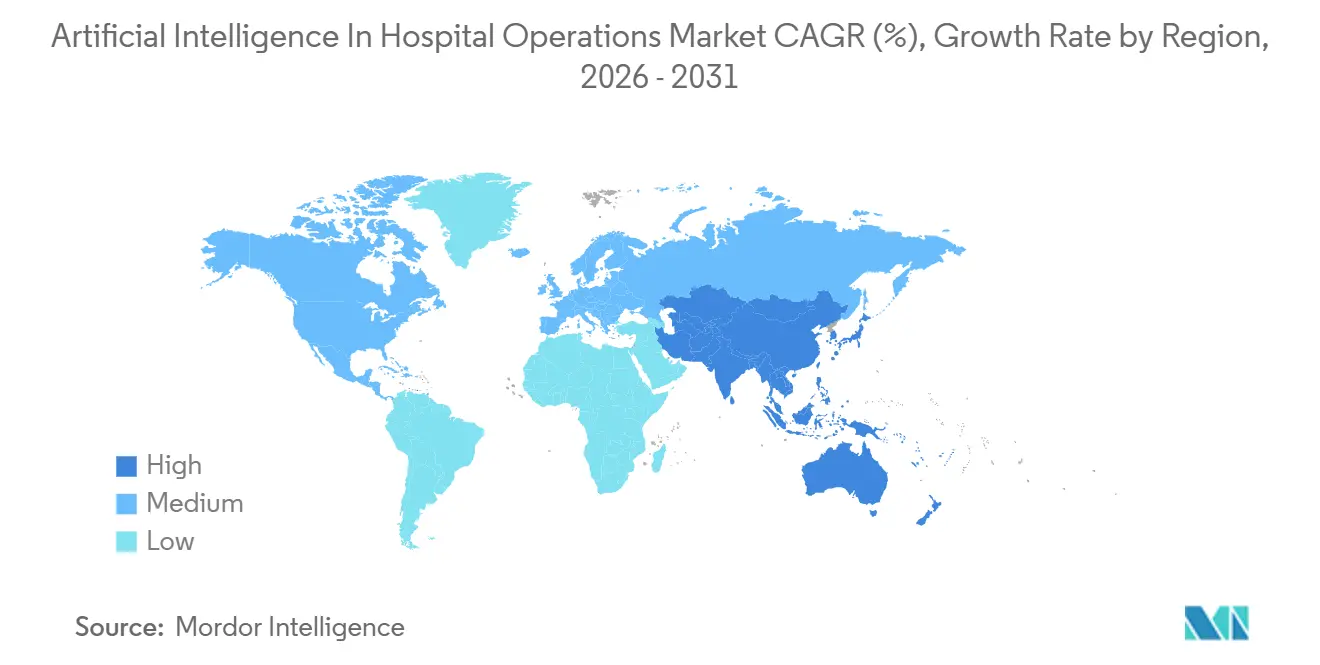

- By geography, North America held 43.24% of Artificial Intelligence in Hospital Operations market share in 2025, while Asia-Pacific is set to expand at a 29.53% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Artificial Intelligence In Hospital Operations Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Workforce Shortages and Administrative Burden Push Automation | +6.0% | Global, concentrated in North America, UK, and Australia | Short term (≤ 2 years) |

| Pressure to Improve Patient Flow, Bed Turnover, and ED Throughput | +4.0% | Global, strongest intensity in North America and Europe | Short term (≤ 2 years) |

| Value-Based Care and Margin Pressure Raise ROI for Predictive Operations AI | +4.5% | North America and Europe core, spill-over to APAC premium segments | Medium term (2-4 years) |

| Cloud, Interoperability, and Command-Center Digitization Improve Implementation Feasibility | +3.5% | Global, accelerating in APAC and MEA | Medium term (2-4 years) |

| TEAM Bundled-Payment Rollout Raises Demand for Discharge and Episode Orchestration | +3.0% | United States | Short term (≤ 2 years) |

| Tightening Staffing-Governance Pressure Boosts AI Scheduling and Virtual Nursing | +3.5% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Workforce Shortages and Administrative Burden Push Automation

The Artificial Intelligence in Hospital Operations market is gaining support from chronic workforce strain, which is pushing hospitals to automate staffing, scheduling, and routine administrative work with a clearer return tied to patient safety and labor stability. Duke Health, using GE HealthCare command-center staffing tools, achieved 95% forecasting accuracy for staffing needs up to 14 days in advance and cut temporary labor use by 50%, which created capacity for 500 additional patients each year without adding physical space. This has changed how providers judge operational AI, because tools are now being measured against retention, overtime, and workload balance rather than only against throughput. A 2025 study in Systems found that an AI-enabled rostering system used within a participatory governance model reduced nursing turnover pressure and shift-allocation conflict, which supports the view that deployment quality matters as much as algorithm quality. As a result, hospitals entering the Artificial Intelligence in Hospital Operations market are treating governance readiness, workflow redesign, and staff acceptance as core procurement criteria.

Pressure to Improve Patient Flow, Bed Turnover, and ED Throughput

The Artificial Intelligence in Hospital Operations market is also being lifted by the cost of poor patient flow, because emergency departments, inpatient units, and discharge teams all depend on earlier visibility into bottlenecks. A 2025 study in JMIR Medical Informatics showed that machine learning models could forecast emergency department waiting counts with a mean absolute error as low as 2.45, which gives hospitals more time to adjust staffing and bed allocation before congestion builds[1]JMIR Medical Informatics, “An AI-Based Framework for Predicting Emergency Department Overcrowding,” JMIR Medical Informatics, jmir.org. A 2025 digital-twin study presented at the IEOM Society Paris conference reported a 53.7% reduction in total bed requirements and a 63.9% decline in patient waiting times when pooled-resource strategies replaced compartmentalized bed management. These results matter because they show that hospitals are no longer using AI only to improve scheduling at the margin, they are using it to redesign how beds, staff, and patient movement are coordinated across the enterprise. In high-occupancy systems, this is also shifting vendor focus toward tools that shorten length of stay and accelerate discharge decisions, since the next limit is often bed scarcity rather than weak planning.

TEAM Bundled-Payment Rollout Raises Demand for Discharge and Episode Orchestration

The Artificial Intelligence in Hospital Operations market has a direct regulatory tailwind from the CMS TEAM model, which started on January 1, 2026 and covers 745 hospitals in 188 selected markets for 30-day surgical episode accountability. The model begins with upside-only participation in 2026, but hospitals will face greater financial exposure from 2027, when up to 20% of the designated reimbursement target can be at risk across the covered procedures. This matters because hospitals now need near-real-time visibility into discharge timing, post-acute utilization, follow-up activity, and readmission risk, and those tasks are difficult to manage consistently with manual processes. The mandatory design also separates this cycle from earlier bundled-payment programs, since health systems can no longer delay participation by opting out. That is why the Artificial Intelligence in Hospital Operations market is seeing stronger demand for episode tracking, care-transition monitoring, and interoperable audit trails tied to reimbursement performance.

Cloud, Interoperability, and Command-Center Digitization Improve Implementation Feasibility

The Artificial Intelligence in Hospital Operations market is becoming more deployable because command-center platforms, cloud analytics, and stronger interoperability are reducing the friction that once limited operational AI to only the largest health systems. Oracle introduced AI-driven EHR workflows in 2025 with voice-first functionality and plans to extend those capabilities into acute care in 2026, which reflects a broader move toward embedded tools inside existing hospital systems rather than separate analytics environments. GE HealthCare’s command-center model also shows how hybrid architectures can connect live hospital data with centralized operational analytics across multiple facilities. This lowers the technical threshold for mid-size and multi-site providers, because they can adopt AI inside familiar workflows instead of building entirely new digital operating layers from scratch. It also explains why the Artificial Intelligence in Hospital Operations market is converging toward cloud-first and hybrid-ready deployments rather than splitting cleanly between cloud and on-premise models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation and Maintenance Cost | -2.5% | Global, acutest in MEA, South America, and rural North America | Medium term (2-4 years) |

| Cybersecurity, Privacy, and Governance Risk | -1.5% | Global, regulatory complexity highest in EU and U.S. | Long term (≥ 4 years) |

| Data Quality and Workflow Fragmentation Weaken Model Trust | -2.0% | Global, concentrated in mixed-EHR ecosystems | Medium term (2-4 years) |

| Frontline Resistance to Centralized Command-Center Workflows | -1.0% | North America and EU, less pronounced in greenfield APAC deployments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Implementation and Maintenance Cost

The Artificial Intelligence in Hospital Operations market still faces a meaningful adoption barrier because hospitals must fund software, integration, data preparation, training, and workflow redesign before benefits appear at scale. A 2025 study in the Journal of Medical Artificial Intelligence found that hospital AI adoption can remain net-value negative for 4 to 5 years before turning net-value positive, which compresses decision making for providers already under financial strain[2]Journal of Medical Artificial Intelligence, “The Financial Challenges of Artificial Intelligence Integration in Healthcare,” Journal of Medical Artificial Intelligence, amegroups.org. A 2025 JAMIA study covering 43 health systems found that 47% named financial concerns as one of the top 2 barriers to AI tool development or deployment, second only to tool maturity at 77%. This slows adoption most in community, rural, and safety-net settings, where the margin for multiyear payback is narrower and implementation teams are smaller. It also favors vendors in the Artificial Intelligence in Hospital Operations market that can offer phased rollouts, measurable milestones, and lower-risk deployment pathways.

Cybersecurity, Privacy, and Governance Risk

The Artificial Intelligence in Hospital Operations market is also constrained by the fact that AI deployment expands the number of systems, vendors, and data flows connected to hospital operations. IBM’s 2025 Cost of a Data Breach Report found that 13% of organizations experienced breaches involving AI models or applications, and 97% of those affected lacked proper AI-specific access controls at the time of compromise. A 2025 MDPI study on integrated EHR environments found that hospitals using third-party tracking technologies were 46% more likely to experience a data breach, which is especially relevant for command-center settings that rely on many interconnected tools. These risks raise the burden tied to access control, auditability, vendor review, and model governance across both the United States and Europe. The result is that buyers in the Artificial Intelligence in Hospital Operations market are placing more weight on secure architecture, compliance history, and clear accountability for integrated data environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Dominance Masks an Accelerating Services Imperative

Software accounted for 72.31% of the Artificial Intelligence in Hospital Operations market in 2025, while services is projected to expand at a 29.38% CAGR through 2031, which shows that the revenue base is still platform-led even as deployment support gains importance. Subscription software remains the core buying model because hospitals prefer lower upfront capital needs, faster rollout, and pre-built integration with existing EHR and workflow systems. Qventus reported in 2026 that willingness among health systems to wait for an EHR vendor to build a needed feature fell from 52% in 2025 to 22% in 2026, which suggests that independent software vendors still have a meaningful window if they can deliver value faster than the large platforms. That keeps software at the center of the Artificial Intelligence in Hospital Operations market, but it also raises the standard for usability, integration speed, and measurable workflow gains.

Services is growing faster because hospitals have learned that operational AI rarely performs well when the tool is installed without process redesign, training, and change management. This is one area where the Artificial Intelligence in Hospital Operations industry is shifting from simple software procurement toward broader operating model work. Providers increasingly need implementation partners that can redesign staffing workflows, build escalation rules, clean fragmented data, and align local teams around new command-center processes. That need becomes stronger when hospitals want AI to manage patient flow, discharge sequencing, perioperative coordination, or revenue cycle workflows across multiple departments at once. Hardware remains the smallest offering layer in strategic importance, but it should benefit from wider use of edge devices, room sensors, and real-time location infrastructure as virtual nursing and smart-room deployments scale beyond pilot programs.

By Use Case: Revenue Cycle Anchors Share While Command-Center Logic Redefines Operational Architecture

Revenue Cycle and Administrative Automation held 25.24% of the Artificial Intelligence in Hospital Operations market size in 2025, which reflects the scale of billing complexity, coding volume, denial management, and prior authorization burden inside hospitals. This use case has matured earlier than others because coding and claims workflows generate structured, repetitive tasks that fit natural language processing and rules-driven automation well. Optum’s 2025 launch of Integrity One, powered by Clinical Language Intelligence, shows how vendors are building integrated revenue cycle platforms that automate work from point of care through final coding rather than optimizing one narrow task at a time. That is why revenue cycle remains the default entry point for many organizations entering the Artificial Intelligence in Hospital Operations market.

Command Center and Operational Decision Support is the fastest-growing use case, with a 29.52% CAGR projected through 2031, because hospitals increasingly want a single operational layer that can coordinate staffing, bed management, throughput, and discharge activity at the same time. GE HealthCare reported that its command-center platform now operates in nearly 500 hospitals globally and can deliver up to a 12x ROI and USD 40 million in savings by reducing operational inefficiency. Patient Flow and Bed Capacity Management and Workforce Management and Staffing Optimization remain among the largest adjacent use cases because both depend on live operational visibility and rapid intervention. Perioperative and Procedural Operations is also gaining momentum as providers extend AI from operating room block utilization into pre-surgical coordination and clinic scheduling. LeanTaaS supported that shift in 2025 when it launched iQueue for Surgical Clinics to connect upstream clinic workflows with downstream surgical coordination.

By Technology: Machine Learning Holds the Base While NLP Captures the Workflow Layer

Machine learning led the technology mix with a 45.52% share in 2025, which reflects its deep use across staffing forecasting, readmission modeling, bed allocation, patient flow prediction, and capacity planning. A 2025 London Business School study found that robust machine learning-based bed assignment reduced off-service placements by 24% and emergency department boarding delays by 35% while keeping hospital occupancy stable, which shows why hospitals continue to treat ML as core operational infrastructure. The Artificial Intelligence in Hospital Operations market still relies on ML as its decision engine because so many hospital operating problems depend on forecast quality, prioritization, and dynamic allocation rather than simple automation. That foundation keeps machine learning central even as newer interfaces receive more public attention.

Natural Language Processing is projected to grow at a 29.25% CAGR through 2031 because it sits directly inside documentation, coding, summarization, and prior authorization workflows where hospitals can see immediate labor savings. Optum’s Integrity One launch in 2025 illustrates that NLP is now being positioned as a production layer for revenue cycle work instead of a narrow supporting feature. Generative and agentic tools are drawing strategic attention in 2026 because hospitals want systems that can convert guidelines, workflow rules, and task logic into executable actions across departments. Computer vision and ambient intelligence are also scaling through smart-room, virtual nursing, and monitoring environments, while rules-based optimization and simulation remain important for perioperative planning, capacity testing, and environments that require tighter validation. Taken together, these layers show that the Artificial Intelligence in Hospital Operations industry is not replacing ML, it is adding NLP and workflow orchestration on top of the installed predictive base.

By Deployment Model: Cloud's Self-Reinforcing Growth Narrows the On-Premise Rationale

Cloud accounted for 61.24% of the Artificial Intelligence in Hospital Operations market in 2025 and is projected to record the fastest CAGR at 30.83% through 2031, which indicates that the dominant model is also still strengthening. Cloud adoption is rising because vendors can retrain models faster, aggregate data across sites more easily, and push updates without heavy local infrastructure burdens. This makes cloud especially attractive for multi-hospital systems that want one operational view across staffing, patient flow, and revenue cycle processes. It also helps explain why the Artificial Intelligence in Hospital Operations market is converging toward cloud-first architectures instead of maintaining a stable balance between delivery models.

On-premise deployment still matters in tightly regulated settings and in hospitals with strong data residency, latency, or internal control requirements. Hybrid models therefore remain important where providers want local system control but still need centralized analytics, remote management, and rapid model improvement. GE HealthCare reported that The Queen’s Health Systems achieved a 0.7-day reduction in patient length of stay using its Command Center, which combined on-premise EHR data with cloud analytics across multiple facilities. That outcome shows why hybrid-capable design is increasingly a procurement requirement rather than a temporary bridge. Over time, cloud should keep taking share in the Artificial Intelligence in Hospital Operations market, but hybrid support will remain essential where security, compliance, and operational continuity must coexist.

Geography Analysis

North America held 43.24% of the Artificial Intelligence in Hospital Operations market share in 2025, which keeps the region as the main revenue base for global vendors. The United States drives this position because it combines large-scale hospital digitization with payment models that reward operational visibility and cost control. The strongest near-term catalyst is the CMS TEAM program, which now places 745 hospitals across 188 selected markets under episode accountability and directly raises demand for discharge, post-acute, and care-transition orchestration[3]Centers for Medicare & Medicaid Services, “TEAM Frequently Asked Questions,” Centers for Medicare & Medicaid Services, cms.gov. This environment supports earlier scaling of command-center, workforce, and revenue cycle AI than in most other regions. Canada continues to move through cloud-based patient flow and workforce tools, while Mexico remains earlier in the digitization curve because hospital IT capacity is less consistent across providers.

Europe remains the second-largest regional cluster for the Artificial Intelligence in Hospital Operations market, with the United Kingdom and Germany acting as the leading adoption centers. WHO Europe reported in 2026 that EU health systems showed clear momentum in AI readiness, supported by the EU AI Act and national strategies, while also facing large regional disparities and increasing dependence on non-EU suppliers in strategic domains. That combination means European adoption is moving forward, but it is doing so under tighter governance expectations and stronger scrutiny of infrastructure control. For vendors, Europe offers meaningful demand but also requires more discipline around transparency, validation, and data governance than many other regions.

Asia-Pacific is the fastest-growing region in the Artificial Intelligence in Hospital Operations market, with a 29.53% CAGR forecast for 2026-2031, supported by greenfield hospital construction in China and India that allows more AI-native design choices. Australia already shows this command-center expansion, with GE HealthCare launching its ORA Command Center across 3 Melbourne hospitals in March 2026. The region is not growing for one single reason, since some countries are building new hospital infrastructure while others are layering AI onto expanding private health networks and large tertiary systems. In the Middle East and Africa, adoption is earlier overall, but sovereign AI investment in the Gulf is creating faster pockets of uptake, illustrated by the 2025 Oracle, Cleveland Clinic, and G42 partnership to build a global AI-based healthcare delivery platform anchored in the UAE. South America remains the smallest regional base, though Brazil is beginning to show proof points, including Rede Mater Dei de Saúde’s use of 12 AI agents in revenue cycle workflows on Amazon Bedrock AgentCore.

Competitive Landscape

The Artificial Intelligence in Hospital Operations market remains fragmented at the vendor level, but the direction of competition is increasingly shaped by a smaller set of integrated platform architectures. Large incumbent vendors are pushing deeper into workflow orchestration because they already sit inside hospital data and daily user workflows. Oracle advanced that position in August 2025 through AI-driven EHR capabilities with voice-first workflows for ambulatory care and stated that acute care functionality is planned for 2026. This gives platform vendors an advantage in integration, distribution, and switching cost, even when specialist vendors still move faster on specific operational pain points. As a result, the Artificial Intelligence in Hospital Operations market is becoming less about isolated algorithms and more about who controls the operating layer through which tasks are routed, monitored, and improved.

Specialist vendors are responding by moving beyond narrow use cases and building broader workflow depth around measurable outcomes. LeanTaaS extended its reach in 2025 with iQueue for Surgical Clinics, which linked upstream clinic coordination with downstream surgical scheduling and supports a wider perioperative value proposition. Symplr also broadened its operational footprint by acquiring Smart Square in July 2025 and then launching new AI-powered contract and credentialing tools at ViVE 2026. Cleveland Clinic and AKASA announced a strategic collaboration in 2025 to launch AI tools for revenue cycle operations, which shows that health systems are still willing to work with focused vendors when the use case is close to clear financial return. These moves indicate that smaller players can still defend space in the Artificial Intelligence in Hospital Operations market if they solve a high-value workflow with faster time to impact.

The next layer of competition comes from infrastructure and compliance strength, not only from application features. Vendors that can support secure hybrid deployment, interoperable data exchange, and auditable workflow decisions should remain better positioned as hospitals tighten oversight of AI operations. That matters because buyers are increasingly balancing speed with governance, especially after more visible concerns around AI-specific access controls and multi-vendor exposure. The competitive field therefore remains broad, but durable advantage in the Artificial Intelligence in Hospital Operations market is likely to come from integration depth, proof of operational outcomes, and compliance maturity rather than from model novelty alone.

Artificial Intelligence In Hospital Operations Industry Leaders

TeleTracking

LeanTaaS

Oracle Health

Qventus

Palantir Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Japan Community Healthcare Organization Osaka Hospital (JCHO Osaka Hospital), Fujitsu Japan Limited, and Fortience Consulting Inc. announced the commencement of a project aimed at establishing a system for the safe utilization of generative AI across all medical operations at JCHO Osaka Hospital.

- February 2026: Union Health Minister of India Inaugurated AI-Enabled E-ICU Command Centre at Yashoda Medicity to Strengthen Technology-Driven Critical Care Services. Union Health Minister Highlighted the Role of AI-Enabled Healthcare in Ensuring Timely Intervention, Diagnostic Precision and Real-Time Monitoring in Critical Care.

Global Artificial Intelligence In Hospital Operations Market Report Scope

As per the scope of the report, artificial intelligence in hospital operations refers to the use of advanced computer algorithms and machine learning techniques to streamline, automate, and enhance various administrative and clinical processes within a hospital.

The segmentation for the artificial intelligence (AI) in hospital operations market is categorized by offering, use case, technology, deployment model, and geography. By offering, the market is divided into software, services, and hardware. By use case, it includes managing patient flow and bed capacity, optimizing workforce management and staffing, automating revenue cycle and administrative tasks, supporting operational decisions with command centers, handling perioperative and procedural operations, and managing assets, rooms, and ancillary operations. By technology, the segmentation covers utilizing machine learning, employing natural language processing, leveraging generative and agentic AI, incorporating computer vision and ambient intelligence, and applying rules-based optimization and simulation. By deployment model, the market is segmented into cloud-based, on-premise, and hybrid. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Software |

| Services |

| Hardware |

| Patient Flow and Bed Capacity Management |

| Workforce Management and Staffing Optimization |

| Revenue Cycle and Administrative Automation |

| Command Center and Operational Decision Support |

| Perioperative and Procedural Operations |

| Asset, Room, and Ancillary Operations |

| Machine Learning |

| Natural Language Processing |

| Generative AI and Agentic AI |

| Computer Vision and Ambient Intelligence |

| Rules-based Optimization and Simulation |

| Cloud |

| On-premise |

| Hybrid |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Offering | Software | |

| Services | ||

| Hardware | ||

| By Use Case | Patient Flow and Bed Capacity Management | |

| Workforce Management and Staffing Optimization | ||

| Revenue Cycle and Administrative Automation | ||

| Command Center and Operational Decision Support | ||

| Perioperative and Procedural Operations | ||

| Asset, Room, and Ancillary Operations | ||

| By Technology | Machine Learning | |

| Natural Language Processing | ||

| Generative AI and Agentic AI | ||

| Computer Vision and Ambient Intelligence | ||

| Rules-based Optimization and Simulation | ||

| By Deployment Model | Cloud | |

| On-premise | ||

| Hybrid | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 outlook for Artificial Intelligence in Hospital Operations?

The Artificial Intelligence in Hospital Operations market is forecast to reach USD 18.36 billion by 2031 from USD 5.29 billion in 2026, rising at a 28.25% CAGR over 2026-2031.

Why are hospitals adopting AI for operations so quickly in 2026?

Staffing shortages, pressure to improve patient flow, and the CMS TEAM bundled-payment model are pushing hospitals to automate scheduling, discharge coordination, and revenue cycle workflows faster.

Which offering leads spending today in hospital operations AI?

Software led with a 72.31% share in 2025, but services is growing faster at a 29.38% CAGR through 2031 because hospitals need workflow redesign, integration, and change management to realize value.

Which use case is most established and which is growing the fastest?

Revenue Cycle and Administrative Automation held the largest share at 25.24% in 2025, while Command Center and Operational Decision Support is projected to grow fastest at a 29.52% CAGR through 2031.

Which region is strongest right now and which region is expanding the fastest?

North America led with 43.24% share in 2025, supported by reimbursement reform and strong digital infrastructure, while Asia-Pacific is projected to grow fastest at a 29.53% CAGR through 2031.

What is the biggest barrier to wider use of AI in hospital operations?

High implementation cost remains a major barrier, especially because benefits can take 4 to 5 years to turn net positive and 47% of health systems cited financial concerns as a top barrier in 2025.

Page last updated on: