United States Veterinary Equipment and Disposables Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

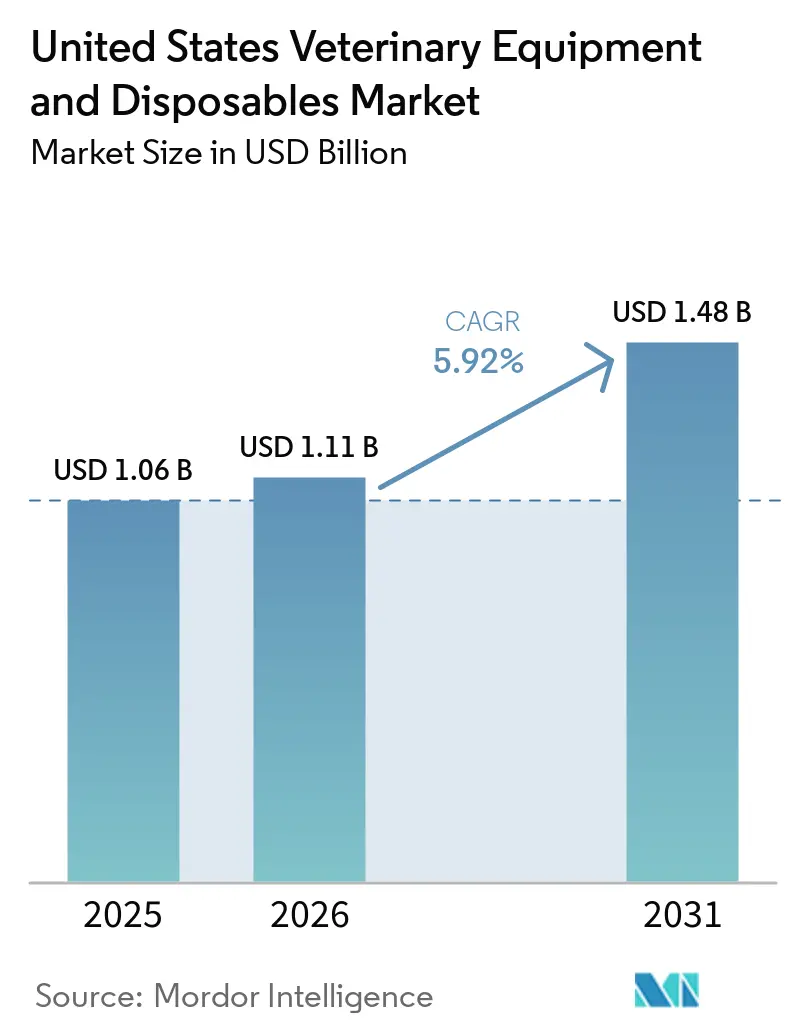

| Base Year Market Size (2025) | USD 1.06 Billion |

| Market Size (2026) | USD 1.11 Billion |

| Market Size (2031) | USD 1.48 Billion |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Veterinary Equipment and Disposables Market Analysis by Mordor Intelligence

The United States Veterinary Equipment And Disposables Market size was valued at USD 1.06 billion in 2025 and is estimated to grow from USD 1.11 billion in 2026 to reach USD 1.48 billion by 2031, at a CAGR of 5.92% during the forecast period (2026-2031).

The United States veterinary equipment and disposables market is being supported by a larger pet care base, with 77.5 million pet-owning households recorded by the American Veterinary Medical Association, and US pet industry spending reaching USD 158 billion in 2025. That stronger attachment to companion animals is increasing procedure volumes, extending treatment pathways, and supporting demand for imaging, anesthesia, monitoring, and high-turn consumables across routine and specialty care settings. The United States veterinary equipment and disposables market is also benefiting from specialty hospital expansion, distributor-led procurement consolidation, and the tax support available for capital equipment purchases under the higher Section 179 deduction threshold. Product demand remains balanced between high-value equipment placements and faster-turn consumables, which gives suppliers multiple ways to grow as clinics and hospitals upgrade their clinical capabilities. High upfront equipment costs and a limited pool of trained technicians still slow adoption at smaller practices, but they do not change the market’s underlying direction through 2031.

Key Report Takeaways

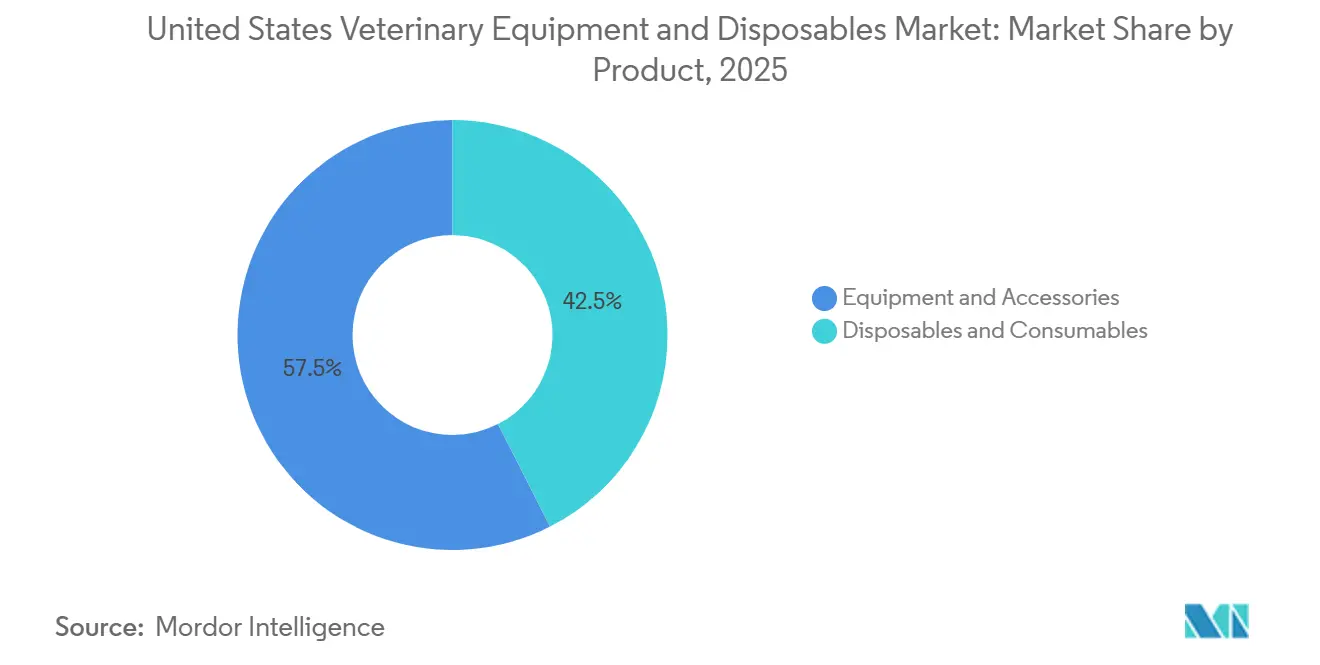

- By product, equipment and accessories held 57.48% of the United States veterinary equipment and disposables market share in 2025, while disposables and consumables are projected to expand at a 7.36% CAGR through 2031.

- By animal type, small animals accounted for 59.17% of the segment in 2025, while large animals are forecast to grow at an 8.87% CAGR through 2031.

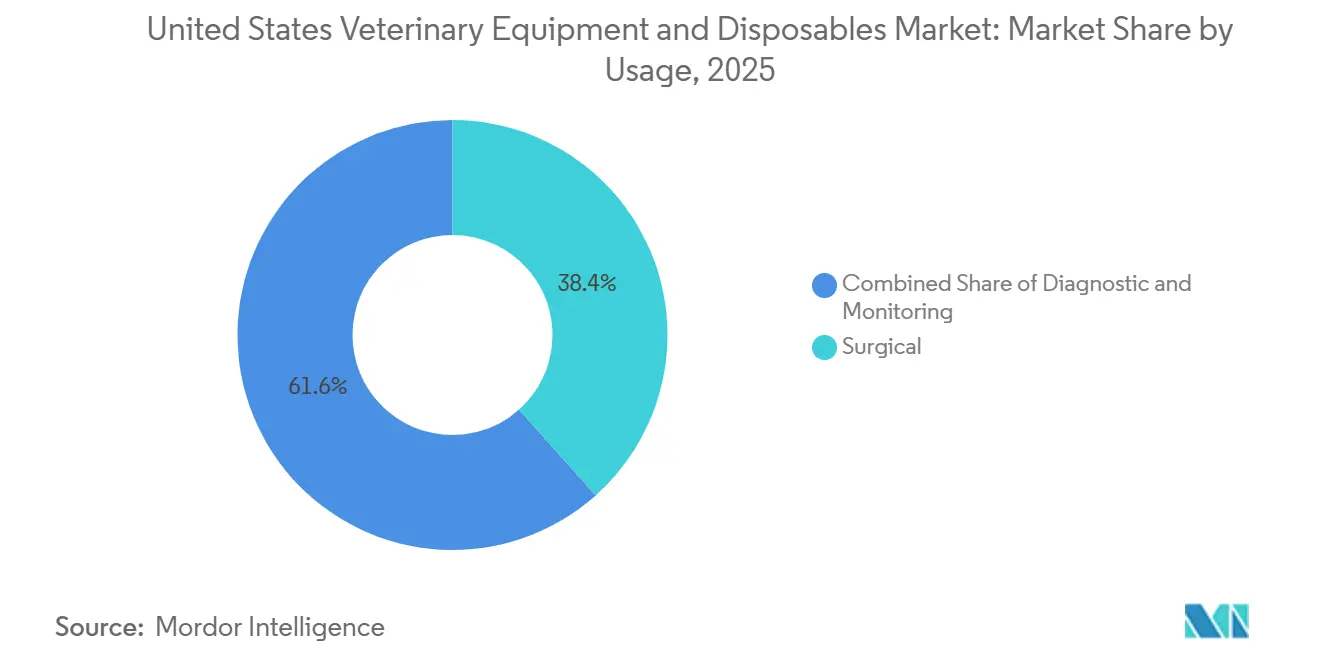

- By usage, surgery represented 38.42% of the segment in 2025, while diagnostics is expected to record the fastest growth at 7.97% through 2031.

- By end use, veterinary clinics held 43.62% of the segment in 2025, while veterinary hospitals are projected to advance at an 8.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Veterinary Equipment and Disposables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Companion Animal Procedural Volume | +2.0% | National, concentrated in high-density metro corridors including NYC, LA, Chicago, Dallas, and Houston | Medium term (2-4 years) |

| Shift Toward Single-Use Infection-Control Consumables | +1.2% | National, with early gains in Sun Belt corporate-chain clinics | Short term (≤ 2 years) |

| Section 179 Supported Capital Equipment Purchases | +0.8% | National, with stronger pull-through in profitable multi-site practices in the Southeast and Southwest | Short term (≤ 2 years) |

| Growth of High-Acuity Referral and Specialty Veterinary Care | +1.5% | National, driven by California, Texas, Florida, and Northeast specialty hospital expansion | Medium term (2-4 years) |

| Expansion of Portable and Point-of-Care Diagnostics | +1.0% | National, with rural and mixed-practice settings accelerating adoption | Medium term (2-4 years) |

| Rising Demand for Workflow-Safe, Low-Labor Clinical Consumables | +0.9% | National, with highest urgency in understaffed independent clinics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Companion Animal Procedural Volume

The United States veterinary equipment and disposables market is being driven first by the scale of companion animal ownership and care activity. The American Pet Products Association reported that 53% of US households owned dogs and 39% owned cats in 2025, while the American Veterinary Medical Association reported 87.3 million owned dogs and 76.3 million owned cats in the country.[1]American Pet Products Association, “The APPA Releases 2025 State of the Industry Report,” APPA, americanpetproducts.org That larger patient pool lifts demand for vaccinations, routine surgeries, dental procedures, imaging, and in-clinic diagnostic tests. The care burden is also becoming more complex because pets are living with more chronic conditions that require repeated monitoring and longer treatment pathways. The American Veterinary Medical Association also stated in 2026 that more than half of US dogs and cats are overweight or obese, which raises anesthesia and perioperative risk and supports wider use of monitoring equipment and critical care consumables.

Shift Toward Single-Use Infection-Control Consumables

The United States veterinary equipment and disposables market is also moving toward single-use sterile products in surgical and critical care settings. High-throughput clinics want faster room turnover, simpler traceability, and lower sterilization burden, which makes syringes, drapes, IV accessories, and other disposable items more attractive. Corporate networks are also standardizing their supply lists, which narrows approved vendor pools and increases the repeat purchase rate for compliant consumables. Covetrus said its VetSuite network delivered more than USD 30 million in realized savings to independent clinics since launch, which shows how group purchasing is making higher-standard consumables easier to adopt at scale. The result is a demand pattern in which consumables growth is becoming less tied to one-time capital cycles and more tied to daily clinical throughput.

Section 179 Supported Capital Equipment Purchases

The United States veterinary equipment and disposables market is receiving near-term support from tax policy. The Internal Revenue Service publication for 2025 reflected the permanent expansion of the Section 179 deduction limit to USD 2.5 million, with the phase-out threshold increased to USD 4 million.[2]Internal Revenue Service, “Publication 225 Farmer’s Tax Guide,” IRS, irs.gov That change allows profitable veterinary practices to expense a larger share of qualifying equipment in the year of purchase rather than spread the benefit over a longer depreciation period. The practical effect is stronger year-end demand for imaging systems, anesthesia machines, and fluid management platforms as practice owners align purchases with tax planning. This support is most useful for multi-site groups and better-capitalized clinics, but it also improves the purchase case for independent practices that have delayed needed upgrades.

Growth of High-Acuity Referral and Specialty Veterinary Care

The United States veterinary equipment and disposables market is gaining from the rapid expansion of specialty and emergency care. The American Veterinary Medical Association reported that specialty practices represented 4.2% of all US veterinary practices in 2024, and that demand for specialty services continues to rise as the relationship between primary and specialty care evolves.[3]American Veterinary Medical Association, “Specialty, Primary Veterinarians Navigate Evolving Relationship as Demand Continues to Grow,” AVMA, avma.org New specialty sites require advanced imaging, ICU monitoring, oncology support equipment, surgical systems, and high-volume consumable inventories from the start. Veritas Veterinary Partners opened a 28,000-square-foot facility in San Rafael in February 2025 with a dedicated ICU, chemotherapy treatment suite, and 128-slice CT system, which shows the size of first-site equipment spending in this care model. As those referral networks expand, general practices also face pressure to improve their own imaging and diagnostic capabilities before transferring complex cases upstream.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Imaging and Surgical Platforms | -0.8% | National, most acute in rural and independent single-site practices | Medium term (2-4 years) |

| Shortage of Credentialed Veterinary Technicians for Advanced Equipment | -0.5% | National, concentrated in rural areas and understaffed suburban practices | Long term (≥ 4 years) |

| Reimbursement Friction and Price Sensitivity Among Pet Owners | -0.6% | National, with highest price sensitivity in non-metro markets | Short term (≤ 2 years) |

| Procurement Delays From Highly Regulated Supply Chains | -0.4% | National, concentrated in products sourced through FDA Class II or III and USDA-regulated channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Of Imaging And Surgical Platforms

The United States veterinary equipment and disposables market still faces a meaningful barrier from the upfront cost of advanced equipment. CT systems, MRI platforms, digital radiography units, and endoscopy towers require capital budgets that many independent and single-site practices cannot support without financing. The American Veterinary Medical Association cited CareCredit survey findings showing that cost was the primary concern for 80% of pet owners considering specialty veterinary care, which makes clinics more cautious about investing in equipment that depends on steady, high-value case flow. Large groups can spread procurement costs across multiple facilities and negotiate stronger supplier terms, while smaller operators carry the full exposure of each purchase. Section 179 support and financing options help the United States veterinary equipment and disposables market, but they do not fully close the gap between corporate networks and independent practices.

Shortage Of Credentialed Veterinary Technicians For Advanced Equipment

The United States veterinary equipment and disposables market is also constrained by limited technician availability and retention pressure. The Bureau of Labor Statistics reported 134,200 veterinary technologists and technicians in the United States in May 2024. The American Animal Hospital Association reported that 30% of veterinary professionals were actively planning to leave their current positions, and compensation remained the leading reason behind attrition in its retention research. Understaffed practices are less willing to buy systems that need trained operators, frequent calibration, or workflow redesign. That restraint pushes some buyers toward more automated analyzers and lower-labor clinical tools rather than traditional multi-step platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Capital Dominates Today, But Consumables Are Closing The Gap

Equipment and accessories captured 57.48% of the United States veterinary equipment and disposables market share in 2025, which reflects the large installed base of anesthesia, monitoring, imaging, and fluid management systems across the country. The United States veterinary equipment and disposables market still leans toward capital equipment because these platforms anchor surgical, emergency, and inpatient workflows in both general and specialty settings. Anesthesia equipment and patient monitors remain central to procedure volume because they are needed across elective surgery, urgent interventions, and ICU care. Research equipment and rescue or resuscitation systems remain smaller categories, but they hold a stable place in referral hospitals, veterinary schools, and teaching facilities.

Disposables and consumables will post the fastest growth, with the United States veterinary equipment and disposables market size for this segment projected to expand at 7.36% CAGR through 2031. This segment benefits from high reorder frequency in syringes and needles, IV accessories, infusion sets, tubes, catheters, drapes, sutures, and wound care materials. Standardization by larger clinic groups is making purchasing more predictable, and that favors vendors with broad product coverage and integrated ordering support. Covetrus said its VetSuite network has delivered savings to independent practices nationwide, which supports the adoption of standardized consumables that previously competed mainly on unit price.

By Animal Type: Small Animals Lead, But Large Animal Demand Is Rising Faster

Small animals accounted for 59.17% of the segment in 2025, which keeps companion animal medicine at the center of the United States veterinary equipment and disposables market. That position is tied to strong household ownership of dogs and cats and to owner willingness to approve more testing, surgery, and preventive care than in the past. In-clinic chemistry systems, hematology analyzers, anesthesia platforms, and monitoring equipment are seeing wider use because general practices are handling a broader range of cases before referral. The United States veterinary equipment and disposables market also benefits from a more wellness-oriented approach in companion animal care, which lifts recurring demand for point-of-care diagnostics and everyday consumables.

Large animals are the fastest-growing segment, and the United States veterinary equipment and disposables market size for this segment is forecast to rise at 8.87% CAGR through 2031. Growth here is supported by a stronger interest in portable ultrasound, point-of-care blood analysis, and field-ready fluid management products that can be used outside fixed clinical infrastructure. Zoetis announced in February 2026 that it would acquire Neogen’s animal genomics business, which points to growing demand for more precise diagnostic and monitoring approaches in livestock health. The American Pet Products Association also reported that 2 million US households own horses, which supports mobile care demand in equine settings where distance and access still shape equipment choice.

By Usage: Surgical Volume Sustains Equipment Spend, While Diagnostics Expands Faster

Surgical usage held 38.42% of the segment in 2025, which made it the largest use case in the United States veterinary equipment and disposables market. This category depends on anesthesia machines, patient monitors, temperature management systems, sterile packs, wound care products, and related consumables that move with procedure volume. The expansion of specialty surgical centers is reinforcing demand for the highest-value equipment categories, especially in referral settings with larger case complexity. Veritas Veterinary Partners opened new California facilities in 2025, including a surgery-only center in Tustin with 5 suites, which reflects the level of focused capital deployment now taking place in advanced surgical care.

Diagnostic is the fastest-growing usage area, and the United States veterinary equipment and disposables market size for this segment is projected to advance at 8% CAGR through 2031. Faster in-clinic turnaround is the core reason, as analyzers with more automation are helping general practices keep more diagnostic work onsite rather than sending it out. That shift improves clinical speed and also increases recurring use of cartridges, test consumables, sample-prep products, and service-linked instrument placements. Monitoring remains a solid third usage area because ICU capability is spreading from large specialty hospitals into more everyday practice settings, especially where hospitals are expanding emergency coverage.

By End Use: Clinics Lead On Breadth, While Hospitals Set The Pace For Upgrades

Veterinary clinics represented 43.62% of the segment in 2025, which gave them the broadest end-user role in the United States veterinary equipment and disposables market. Their purchasing mix is led by high-frequency products such as syringes, wound care items, IV sets, portable monitors, and point-of-care diagnostic supplies. These facilities also remain the main outlet for routine-care equipment because they handle the largest everyday case flow across the country. The United States veterinary equipment and disposables market keeps returning to clinics as its largest volume base because this channel combines a wide national footprint with steady replenishment demand.

Veterinary hospitals will grow the fastest, at 8.03% CAGR, through 2031 within the United States veterinary equipment and disposables market. Emergency and specialty hospitals are investing in imaging suites, ICU monitoring networks, laboratory capacity, and higher-value surgical workflows that go well beyond the procurement needs of most general clinics. MedVet opened 2 new emergency and specialty hospitals in Central Ohio in 2025 with in-house imaging, laboratory services, and round-the-clock ICU monitoring, which shows the kind of integrated buildout now shaping this end-use tier. Research institutes and academic institutions remain smaller but stable buyers, supported by teaching hospital refresh cycles and ongoing animal health research needs.

Geography Analysis

The United States veterinary equipment and disposables market is national in scope, but demand intensity is not evenly distributed across regions. The Sun Belt is seeing the strongest recent buildout in specialty and emergency capacity, especially in California, Texas, Florida, and the Southeast. Veritas Veterinary Partners expanded in California in February 2025, while Arista Advanced Pet Care opened its first specialty and emergency hospital in Atlanta in April 2025 and stated that Dallas would be part of its expansion path. These investments create concentrated procurement events for imaging, monitoring, ICU equipment, and surgical disposables.

The United States veterinary equipment and disposables market also shows a strong growth node in Florida, where expansion is being driven by affluent pet-owner populations and rising care intensity. Lakefield Veterinary Group entered Naples, Florida, in July 2025, which points to continued East Coast specialty and hospital investment. California still leads in installed capital intensity because it has the deepest concentration of board-certified specialists in high-acuity fields such as oncology, neurology, and cardiology. The Northeast remains important because it combines dense practice networks with premium care demand and active referral consolidation. COVE Animal Health expanded in Pennsylvania in June 2025 through a partnership with Hickory Veterinary Hospital, which shows how Northeast networks are combining general practice, boarding, emergency, and specialty services within a linked procurement model.

The Midwest is now part of the same capital expansion story, which makes the United States veterinary equipment and disposables market less concentrated in coastal metros than it was in earlier years. MedVet’s 2025 Ohio expansion showed that specialty hospital investment is now reaching strong mid-market regions with meaningful clinical depth. Rural and agricultural areas remain the clearest whitespace for portable diagnostics and mobile treatment tools because fixed imaging infrastructure is still limited there. That leaves room for field-ready ultrasound, blood analysis, and monitoring systems that can close access gaps without requiring a full hospital footprint.

Competitive Landscape

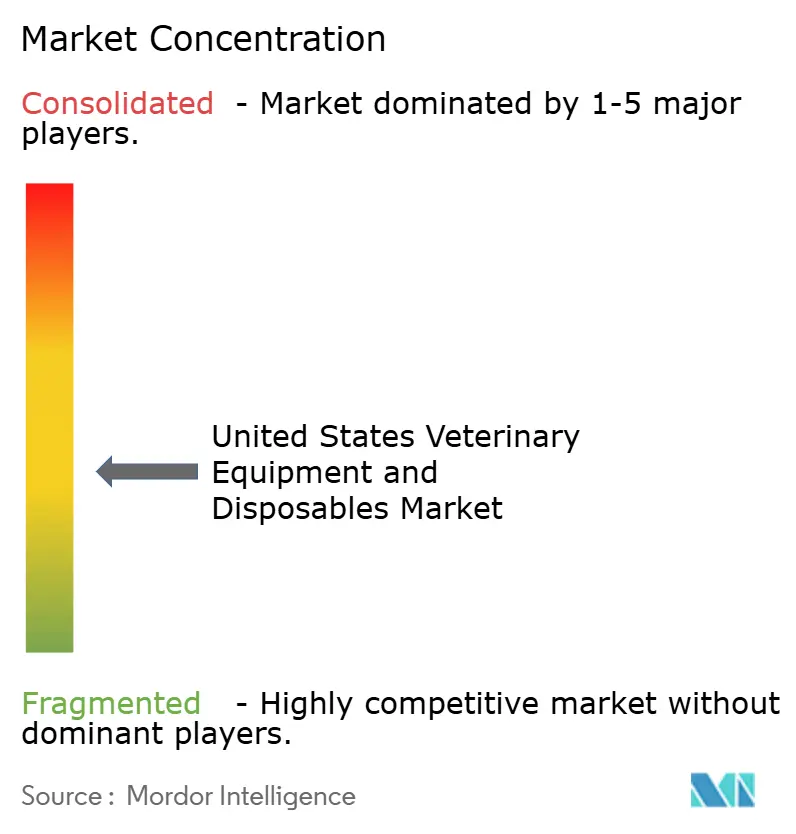

The United States veterinary equipment and disposables market remains moderately fragmented, with competition spread across specialized equipment manufacturers, animal health companies with diagnostics capabilities, human healthcare suppliers with veterinary exposure, and technology-enabled distributors. IDEXX Laboratories, Midmark, Mindray Animal Medical, Avante Animal Health, Vetland Medical, Zoetis, B. Braun Vet Care, STERIS, Covetrus, Henry Schein, and Patterson Companies all compete from different positions in the value chain. This structure means no single company controls the full market, but some firms hold stronger leverage in procurement, software integration, or installed diagnostic systems than others. The result is a market where scale matters, but clinical fit, service reach, and workflow compatibility still shape buying decisions.

Distribution scale is becoming more important in the United States veterinary equipment and disposables market. Covetrus and MWI Animal Health announced a merger under Cencora in February 2026, combining MWI’s supply chain infrastructure with Covetrus’s software and pharmacy assets into a broader animal health platform. That move is likely to strengthen purchasing leverage with suppliers and make it harder for smaller distributors to defend their share with large clinic networks. On the manufacturer side, product ecosystems are becoming stickier as vendors tie instruments to software, consumables, and service workflows. This creates higher switching costs once a practice validates a platform and trains staff around it.

The United States veterinary equipment and disposables market still has room for challengers, where automation and labor reduction are the main value drivers. Bionote USA launched the Vcheck H hematology analyzer in January 2026 and the Vcheck U urinalysis analyzer in February 2026, while HORIBA introduced the Yumivet veterinary diagnostics brand in 2026 with the VH2500 hematology analyzer. Smaller vendors can win in underpenetrated areas such as portable diagnostics, low-labor workflows, and field-ready tools, but it remains difficult to displace entrenched platforms without a clear cost or usability advantage. The competitive position of large suppliers is strengthened further by multi-product contracts, software-linked ordering, and the validation burden that comes with replacing clinical systems once they are embedded in practice routines.

United States Veterinary Equipment and Disposables Industry Leaders

Boehringer Ingelheim Animal Health

Elanco Animal Health Incorporated

Neogen Corporation

IDEXX Laboratories, Inc.

Zoetis Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Covetrus and MWI Animal Health announced a definitive merger agreement under Cencora, combining MWI's distribution capabilities with Covetrus's integrated software and pharmacy platform to form a leading US animal health distribution entity serving companion, equine, and production animal markets. The merger is expected to deliver operational efficiencies and cost savings for veterinary practices nationwide.

- March 2026: Zoetis announced a definitive agreement to acquire Neogen Corporation's animal genomics business, accelerating its precision livestock health strategy with predictive genomic insights for cattle, swine, and other major species. The acquisition is expected to close in H2 2026.

- February 2026: Midmark Corporation launched 2 new veterinary Multiparameter Monitors, a 12-inch and a compact portable 8-inch version, featuring Cardell blood pressure technology and veterinary-specific algorithms designed to support anesthetic procedure management with integrated safety features.

- February 2026: Bionote USA introduced the Vcheck U, an in-clinic urinalysis analyzer combining urine chemistry and sediment analysis in a single automated unit with AI-assisted result interpretation for canine and feline patients.

United States Veterinary Equipment and Disposables Market Report Scope

The United States Veterinary Equipment and Disposables Market encompasses the tools, devices, and single-use consumables utilized to diagnose, monitor, and treat animals in clinics, hospitals, and research facilities.

The Veterinary Equipment and Disposables Market is segmented by product, animal type, usage, and end use. By product, the market is divided into equipment and accessories including anesthesia equipment, temperature management equipment, fluid management equipment, patient monitoring equipment, research equipment, rescue and resuscitation equipment, and other accessories as well as disposables and consumables such as syringes and needles, bandages and wound care products, infusion sets and IV accessories, tubes and catheters, and surgical consumables. By animal type, the market is segmented into small animals and large animals. By usage, products are applied in surgical, diagnostic, and monitoring settings. By end use, adoption is driven by veterinary clinics, veterinary hospitals, veterinary research institutes, and academic institutions.

| Equipment and Accessories | Anesthesia Equipment |

| Temperature Management Equipment | |

| Fluid Management Equipment | |

| Patient Monitoring Equipment | |

| Research Equipment | |

| Rescue and Resuscitation Equipment | |

| Other Equipment and Accessories | |

| Disposables and Consumables | Syringes and Needles |

| Bandages and Wound Care Products | |

| Infusion Sets and IV Accessories | |

| Tubes and Catheters | |

| Surgical Consumables |

| Small Animals |

| Large Animals |

| Surgical |

| Diagnostic |

| Monitoring |

| Veterinary Clinics |

| Veterinary Hospitals |

| Veterinary Research Institutes |

| Academic Institutions |

| By Product | Equipment and Accessories | Anesthesia Equipment |

| Temperature Management Equipment | ||

| Fluid Management Equipment | ||

| Patient Monitoring Equipment | ||

| Research Equipment | ||

| Rescue and Resuscitation Equipment | ||

| Other Equipment and Accessories | ||

| Disposables and Consumables | Syringes and Needles | |

| Bandages and Wound Care Products | ||

| Infusion Sets and IV Accessories | ||

| Tubes and Catheters | ||

| Surgical Consumables | ||

| By Animal Type | Small Animals | |

| Large Animals | ||

| By Usage | Surgical | |

| Diagnostic | ||

| Monitoring | ||

| By End Use | Veterinary Clinics | |

| Veterinary Hospitals | ||

| Veterinary Research Institutes | ||

| Academic Institutions | ||

Key Questions Answered in the Report

What is the 2031 value forecast for United States veterinary equipment and disposables?

The United States veterinary equipment and disposables market is forecast to reach USD 1.48 billion by 2031 from USD 1.11 billion in 2026, growing at a 5.92% CAGR.

Which product category leads spending in the United States?

Equipment and accessories led in 2025 with 57.48% share, supported by anesthesia, monitoring, imaging, and fluid management placements across clinics and hospitals.

Which area is growing fastest by product type?

Disposables and consumables are the fastest-growing product segment and are projected to expand at a 7.36% CAGR through 2031.

Why are veterinary hospitals becoming more important buyers?

Veterinary hospitals are expected to grow at 8.03% CAGR through 2031 because new specialty and emergency facilities need imaging suites, ICU monitoring, laboratory systems, and large consumable inventories.

Which animal segment offers the strongest growth outlook?

Large animals are projected to grow fastest at an 8.87% CAGR through 2031, supported by portable diagnostics, field-based monitoring, and precision livestock health tools.

What are the main risks affecting equipment adoption at smaller practices?

The main constraints are high upfront costs for imaging and surgical platforms and a shortage of veterinary technicians, which reduces confidence in buying systems that require trained operators and workflow changes.

Page last updated on: