Veterinary Dental Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

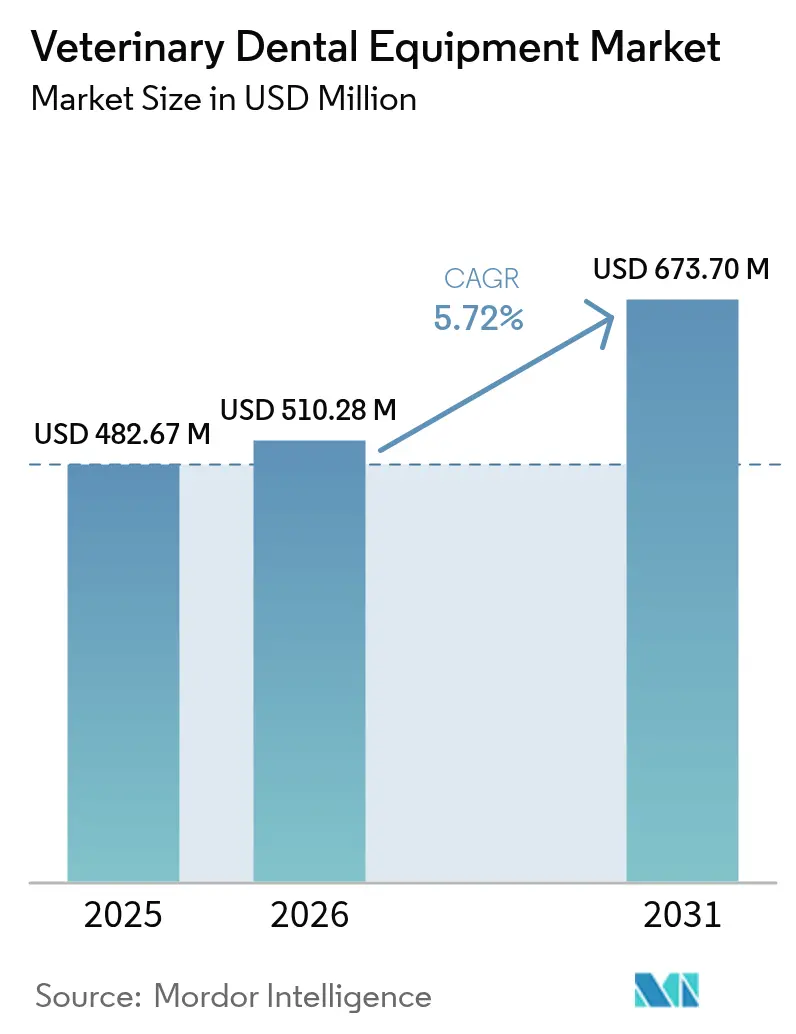

| Market Size (2026) | USD 510.28 Million |

| Market Size (2031) | USD 673.7 Million |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Dental Equipment Market Analysis by Mordor Intelligence

Veterinary Dental Equipment Market size market size in 2026 is estimated at USD 510.28 million, growing from 2025 value of USD 482.67 million with 2031 projections showing USD 673.7 million, growing at 5.72% CAGR over 2026-2031.

Rising pet longevity, growing awareness of periodontal disease, and the normalization of preventive dentistry have created a durable demand funnel that sustains steady equipment sales. Clinics are enlarging chair capacity and adopting workflow-centric layouts, which shortens procedure times and pushes average equipment spend higher. Pet insurance policies that now reimburse cleanings, extractions, and even endodontics are accelerating the replacement cycle for high-value digital radiography and powered handpieces. At the same time, portable field kits aimed at mass vaccination initiatives in emerging markets widen the intake pipeline for first-time buyers.

Key Report Takeaways

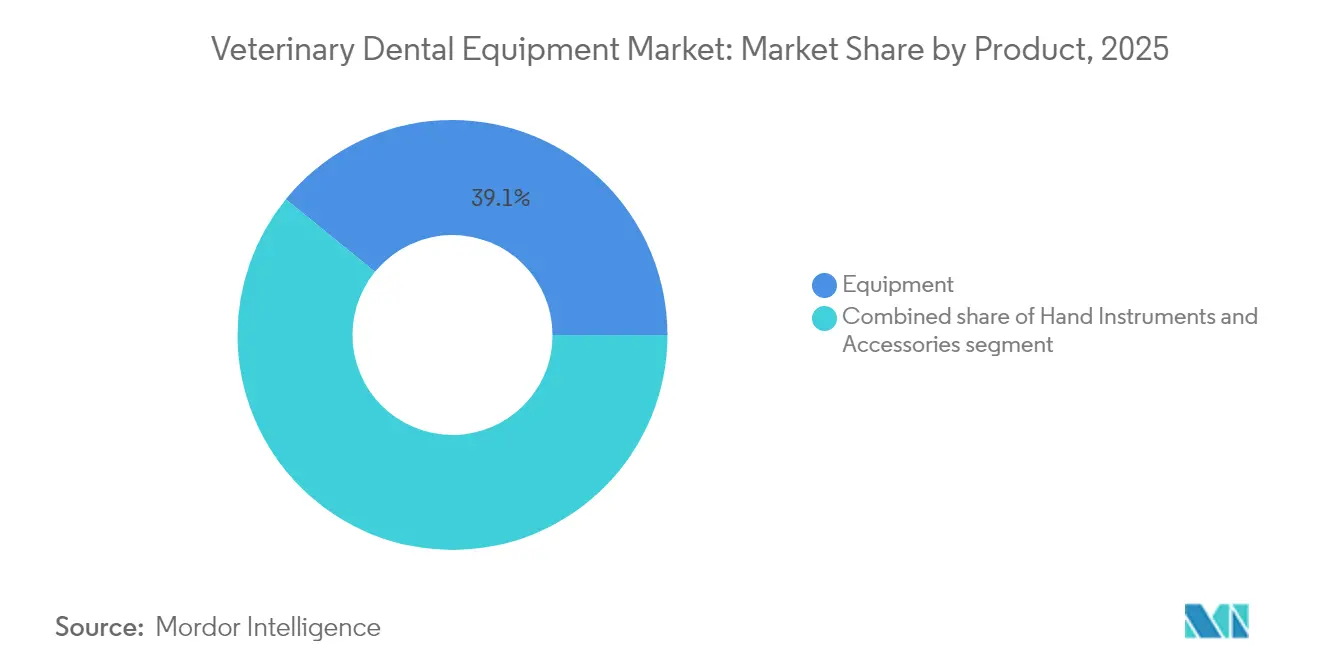

- By product type, hand instruments captured 39.12% of the veterinary dental equipment market share in 2025 and are forecast to grow at a 6.72% CAGR through 2031, outpacing all other categories.

- By procedure, diagnostic imaging commanded 33.45% of the 2025 veterinary dental equipment market size and is projected to expand at 6.21% CAGR to 2031.

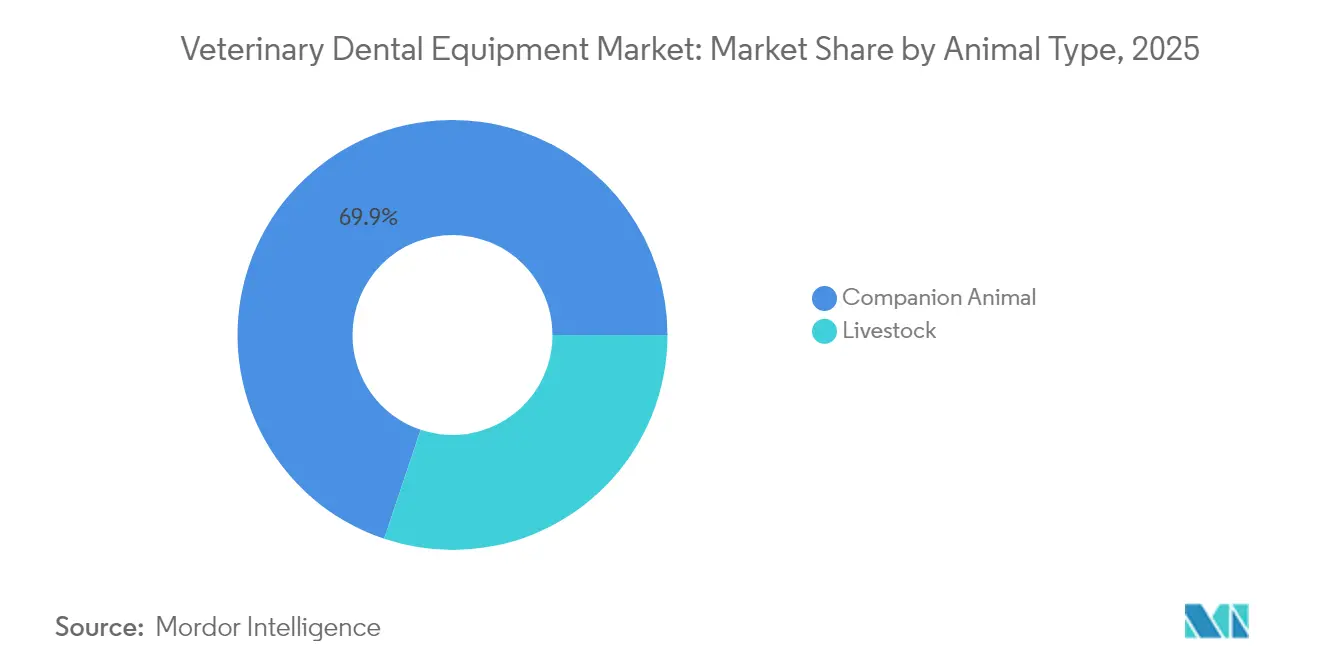

- By animal type, companion animals held 69.85% revenue share of the veterinary dental equipment market in 2025, while the livestock segment is projected to post the fastest growth at 6.45% through 2031.

- By end user, veterinary clinics accounted for 52.55% of the veterinary dental equipment market size in 2025; the “others” category (academia, mobile units, dental-only practices) is expected to advance the quickest at 6.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Veterinary Dental Equipment Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Board-Certified Veterinary Dentistry Practices | +1.2% | North America & Europe | Medium term (2-4 years) |

| Rising Uptake of Digital Dental Radiography in Equine Hospitals | +0.8% | Global, with concentration in North America & Europe | Short term (≤ 2 years) |

| Expansion of Pet Insurance Policies Covering Dental Procedure | +1.5% | North America, Europe, developed APAC | Medium term (2-4 years) |

| Government-Sponsored Mass Rabies Drives Triggering Routine Oral Check-ups | +0.7% | Latin America, Asia-Pacific, Africa | Long term (≥ 4 years) |

| Growth of Tele-Dentistry Triage Platforms for Rural Companion-Animal Clinics | +0.9% | Global, with emphasis on rural regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Board-Certified Veterinary Dentistry Practices

Regional clusters of American Veterinary Dental College diplomates surpassed 220 in 2024, multiplying referral flows that incentivize general practices to upgrade imaging and high-speed instrumentation. Corporate suppliers integrate hands-on workshops with equipment bundles, creating a virtuous loop where clinical mastery fuels hardware demand. The driver’s impact is strongest in secondary cities, where early adopters quickly influence five to seven neighboring clinics to follow suit, gradually lifting the veterinary dental equipment market.

Rising Uptake of Digital Dental Radiography in Equine Hospitals

Direct digital plates engineered for large skulls enable immediate diagnostics and lower retake rates, encouraging equine practices to retire film systems. A 2025 study showed artificial-intelligence software reached high inter-rater agreement with board-certified dentists when identifying common lesions. Although sensitivity still trails human expertise, the technology enriches treatment planning and shortens reading times, raising utilization of digital sensors and consoles within the veterinary dental equipment market.

Expansion of Pet Insurance Policies Covering Dental Procedures

Average dental cleaning costs of USD 170-350 are now routinely reimbursed by North American and Nordic policies, lifting client acceptance of advanced treatments and shrinking payback periods on capital items. Clinics report procedure approval rates climbing 30-40% after policy upgrades, driving a direct uptick in handpiece, suction, and X-ray sales and reinforcing the growth trajectory of the veterinary dental equipment market.

Government-Sponsored Mass Rabies Drives

Canada’s 2025 rabies vaccination guideline recommends full-mouth inspections during each inoculation, formalizing preventive dentistry in public-health settings. Portable LED lights, mouth gags, and battery-run polishers are now adapted for field use, opening incremental channels for suppliers targeting first-time users in emerging economies.

Restraints Impact Analysis of Veterinary Dental Equipment Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front Cost of CBCT & Advanced Imaging in Emerging Markets | -0.9% | Asia-Pacific, Latin America, Middle East & Africa | Medium term (2-4 years) |

| Shortage of Diplomate Veterinary Dentists Beyond Tier-1 Cities | -1.3% | Global, particularly acute in developing regions | Long term (≥ 4 years) |

| Grey-Market Imports & Non-Certified Equipment in Latin America | -0.8% | Latin America, with spillover to other developing regions | Medium term (2-4 years) |

| Limited Reimbursement for Equine Dental Services in the Nordics | -0.4% | Nordic countries (Sweden, Norway, Denmark, Finland) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Diplomate Dentists Beyond Tier-1 Cities

Limited specialist presence outside metropolitan hubs curbs exposure to advanced techniques, slowing adoption of premium units. Research on geographic access indicates significant care gaps that suppress equipment uptake in semi-urban clinics. Suppliers respond with simplified controls and remote coaching, but sustained specialist scarcity still drags on the broader veterinary dental equipment market.

Grey-Market Imports & Non-Certified Equipment

Price discounts of 30-50% entice Latin American buyers toward counterfeit handpieces and cloned sensors, undermining certified vendors. Legitimate manufacturers deploy holograms and online serial checks to protect brand equity. While education campaigns gradually steer customers back, persistent grey-channel leakage moderates growth rates in affected sub-regions of the veterinary dental equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Veterinary Dental Equipment Market Segment Analysis

By Product:

Precision Hand Instruments Extend Clinical ReachHand instruments represent 39.12% of the veterinary dental equipment market and are advancing at a 6.72% CAGR as practitioners adopt color-coded scalers, curettes, and winged elevators for species-specific pathology. Over 80-90% of dogs older than three years present periodontal lesions, making fine-tip instruments indispensable. Vendors now offer ergonomic silicone handles that reduce operator fatigue, prompting clinics to replace legacy sets more frequently. Lighting and magnification tools maintain robust incremental demand due to the migration of microsurgical techniques from human dentistry, while waste-management accessories enjoy regulatory tailwinds as infection-control standards tighten across the veterinary dental equipment market.

Digital X-ray consoles, sensors, and positioning aids comprise roughly one-quarter of revenue and benefit from steady conversion of film users. The shift accelerates where pet insurance and specialist referrals overlap, underscoring the linked nature of procedural complexity and imaging investment. Recent launches of veterinary-specific intra-oral sensors hardened against bite pressure amplify confidence in long-term durability, fostering repeat purchases in the veterinary dental equipment market.

By Procedure:

Imaging-Led Diagnosis Reshapes Care PathwaysDiagnostic imaging accounts for 33.45% of 2025 revenue, with clinics integrating chairside monitors that allow real-time owner consultations. The feedback loop drives higher acceptance of periodontal therapy, which retains the largest case volume because canine prevalence exceeds 80% in adult dogs. Extraction kits featuring power elevators and precision burs deliver less trauma and faster healing, encouraging broader use even among general practitioners. Preventive polishing heads, fluoride gels, and sealants add recurring consumable revenue, anchoring long-term client retention within the veterinary dental equipment market.

Restorative and endodontic procedures, once confined to referral centers, gain traction as training materials demonstrate reliable outcomes. Composite syringes and light-curing handpieces adapted from human dentistry allow tooth-saving therapies that align with owner sentiment. Exotic-animal dentistry underscores the need for specialized micro-burs; a 2024 rabbit study cited 41% complication rates during intra-oral surgeries, highlighting equipment gaps that innovators now target. Each of these sub-segments keeps broadening the scope of services that underpin the veterinary dental equipment market.

By Animal Type:

Companion Animals Dominate, Livestock AccelerateCompanion animals deliver 69.85% of 2025 revenue in the veterinary dental equipment market, reflecting owner willingness to approve elective dental care. Insurance reimbursement and consumer financing reduce price sensitivity, stimulating sales of premium handpieces and implant-grade kits. Pediatric dentistry for brachycephalic breeds is a rising niche that requires fine diamond burs and magnification loops, ensuring repeat purchases.

Livestock and equine applications together capture the remaining share yet exhibit a 6.45% CAGR through 2031. Dental pathologies hamper feed conversion and performance; a 2023 survey found 95% of miniature horses had clinically significant findings, pushing equine practitioners to acquire field-portable power floats. Durable casings, splash-resistant consoles, and battery longevity dominate buying criteria in this cohort of the veterinary dental equipment market.

By End User:

Clinics Anchor Demand, Mobile Units Expand ReachVeterinary clinics hold 52.55% of the veterinary dental equipment market size and treat dentistry as a key revenue driver that raises per-visit spend. Modern design philosophy allocates a dedicated dental table, wall-mounted X-ray generator, and automated suction to maximize throughput. Hospitals and referral centers add anesthesia monitors and separate airflow systems to support longer, specialist-level procedures, reinforcing the high-value end of the veterinary dental equipment market.

Mobile services, dental-only practices, and academic labs collectively form the fastest-growing end-user block. Unit shipments to mobile operators rise as customized vans ship with built-in compressors and handheld radiography devices, allowing access to underserved ZIP codes. Academic institutions refresh high-fidelity models and simulation suites frequently, validating novel tools before they reach commercial channels. This cross-pollination accelerates the diffusion curve across the veterinary dental equipment market.

Geography Analysis

North America Veterinary Dental Equipment Market

North America retains leadership with 41.85% revenue share and records above-average equipment density per practice. Specialist clusters, widespread insurance coverage, and mandatory device certifications create a favorable demand profile. Technician enrollment in dental post-certificates is projected to climb 20% from 2021-2031, adding skilled labor that justifies expanded operatory footprints. Clinics upgrade from single to dual chairs, effectively doubling capacity without enlarging real estate, which boosts capital investment in the veterinary dental equipment market.

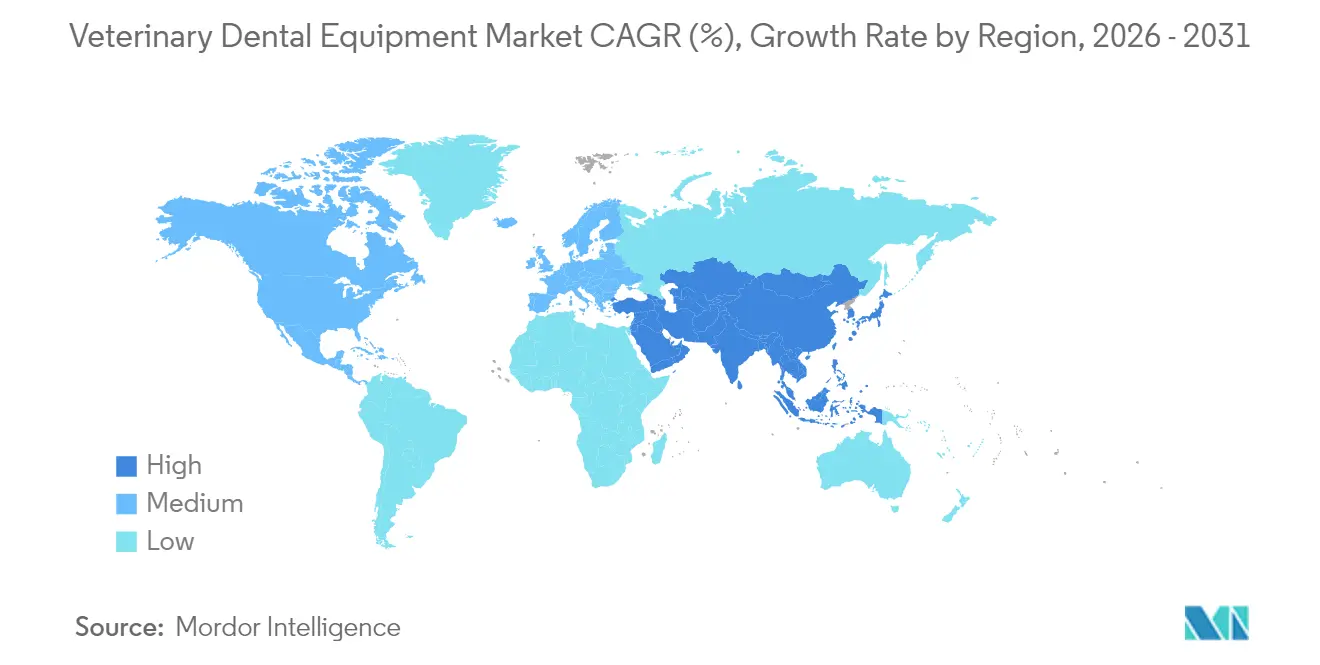

APAC Veterinary Dental Equipment Market

Asia-Pacific posts the fastest growth, at a 7.01% CAGR, propelled by rising disposable incomes and rapid urbanization that concentrates pet ownership in megacities. China, Japan, and South Korea anchor premium purchases, while India and Southeast Asian nations exhibit first-wave adoption of portable kits suited to mixed-practice environments. Government-funded rabies campaigns integrate oral screenings, exposing field veterinarians to equipment benefits. This experience seeds future private-sector demand, expanding the veterinary dental equipment market.

EMEA and LATAM Veterinary Dental Equipment Market

Europe remains a mature yet innovation-oriented region where stringent safety standards favor certified suppliers. Price transparency varies: a 2024 multi-country study recorded wide fee swings, affecting payback models for new hardware. Clinics in higher-fee territories adopt premium imaging sooner, while lower-fee zones phase in gradually. Latin America and the Middle East-Africa collectively hold a modest share but display pockets of high growth in urban hubs. Counterfeit penetration and uneven enforcement temper expansion in Latin America, whereas infrastructure limitations constrain many African sub-markets, though elite owners sustain small clusters of demand. Collectively, these dynamics underscore the varied maturity levels across the global veterinary dental equipment market.

Competitive Landscape

The veterinary dental equipment market shows moderate concentration: the top five suppliers collectively account for more than half of global revenue. Diversified distributors such as Patterson Companies provide financing and broad catalogs, while specialist innovators like iM3 focus exclusively on dental units and training. Midmark’s academy program doubled dental revenue share for participating practices, demonstrating how education augments product pull-through.

Convergence with human dentistry hastens product iterations. Companies transfer sensor patents, LED light technology, and ergonomic handle designs, shortening development timelines within the veterinary dental equipment market. The 2024 acquisition of iM3 by Vimian Group for EUR 87.5 million underscores sustained investor appetite for highly specialized product lines that pair consumable yield with capital uptime.

Artificial-intelligence overlays represent a potential pivot: a 2025 peer-reviewed study shows software achieving human-level accuracy on several lesion types, hinting at subscription-based models that bundle hardware and analytics. Smaller players differentiate through species-specific instrumentation—such as micro-burs for birds and rodents—carving out defensible niches in the wider veterinary dental equipment market.

Veterinary Dental Equipment Industry Leaders

Midmark Corporation

MAI Animal Health

Dentalaire, International

iM3Vet Pty Ltd

Dispomed ltd

- *Disclaimer: Major Players sorted in no particular order

Veterinary Dental Equipment Market Companies Covered in this Report

- iM3 Veterinary Dentistry

- Midmark

- Henry Schein

- Dentalaire International

- Patterson Companies

- Acteon Group Ltd.

- Planmeca

- Integra LifeSciences Holdings Corp.

- Jørgen Kruuse A/S

- Eickemeyer Veterinary Equipment

- B. Braun

- Covetrus

- Dispomed

- Heska

- DRE Veterinary

- Summit Veterinary Pharmacy

- Accesia AB

- Avante Health Solutions

- Cislak

- VetDent

Recent Industry Developments in Veterinary Dental Equipment Market

- February 2025: Midmark launched a dental-imaging training and install program granting on-site positioning tuition valued at USD 1,995 with each digital X-ray bundle purchase.

- December 2024: Patterson Companies agreed to a USD 4.1 billion take-private deal with Patient Square Capital

Global Veterinary Dental Equipment Market Report Scope

As per the scope of the report, veterinary dental equipment is used for the cleaning, extraction, filling, adjustment, repair, and in other aspects of animal oral healthcare.

The veterinary dental equipment market is segmented by Equipment Type (Dental Stations, Dental X-Ray Systems, Dental Powered Units, Dental Lasers, Dental Electrosurgical Units, and Others), Consumables (Dental Supplies, Prophy Products, Others), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above-mentioned segments.

Segmentation Overview

| Equipment | Dental X-ray Systems |

| Dental Stations & Delivery Units | |

| Ultrasonic & Piezo Scalers | |

| High- & Low-Speed Handpieces | |

| Electrosurgical & Laser Units | |

| Other Equipment (Intra-oral Cameras, Compressors) | |

| Hand Instruments | Extractions (Elevators, Luxators) |

| Periodontal Instruments (Scalers, Curettes, Probes) | |

| Restorative Instruments | |

| Orthodontic Instruments | |

| Adjuvants/Accessories | Instrument Cassettes & Sterilization Trays |

| Lighting & Magnification Systems | |

| Waste Management & Suction Accessories |

| Companion Animals | Canines |

| Felines | |

| Equines | |

| Other Companion Animals | |

| Livestock | Bovines |

| Swine |

| Veterinary Hospitals |

| Veterinary Specialty & Referral Centers |

| Veterinary Clinics |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product | Equipment | Dental X-ray Systems |

| Dental Stations & Delivery Units | ||

| Ultrasonic & Piezo Scalers | ||

| High- & Low-Speed Handpieces | ||

| Electrosurgical & Laser Units | ||

| Other Equipment (Intra-oral Cameras, Compressors) | ||

| Hand Instruments | Extractions (Elevators, Luxators) | |

| Periodontal Instruments (Scalers, Curettes, Probes) | ||

| Restorative Instruments | ||

| Orthodontic Instruments | ||

| Adjuvants/Accessories | Instrument Cassettes & Sterilization Trays | |

| Lighting & Magnification Systems | ||

| Waste Management & Suction Accessories | ||

| By Animal Type | Companion Animals | Canines |

| Felines | ||

| Equines | ||

| Other Companion Animals | ||

| Livestock | Bovines | |

| Swine | ||

| By End User | Veterinary Hospitals | |

| Veterinary Specialty & Referral Centers | ||

| Veterinary Clinics | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What drives current demand in the veterinary dental equipment market?

Demand is propelled by preventive-care normalization, expanded pet-insurance coverage for dental work, and technology migration from human dentistry that boosts clinical outcomes.

How is artificial intelligence influencing veterinary dentistry?

AI-based radiographic software now matches human readers on common lesions, cutting interpretation time and enhancing owner communication, thereby encouraging clinics to upgrade to digital imaging.

Which region is growing the fastest?

Asia-Pacific leads with a forecast CAGR of 7.01% thanks to rising urban pet ownership and veterinary-infrastructure build-out.

Why are hand instruments gaining share?

High prevalence of periodontal disease and growing procedure specialization make precision scalers, curettes, and elevators indispensable daily tools. High prevalence of periodontal disease and growing procedure specialization make precision scalers, curettes, and elevators indispensable daily tools.

Page last updated on: