Veterinary Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

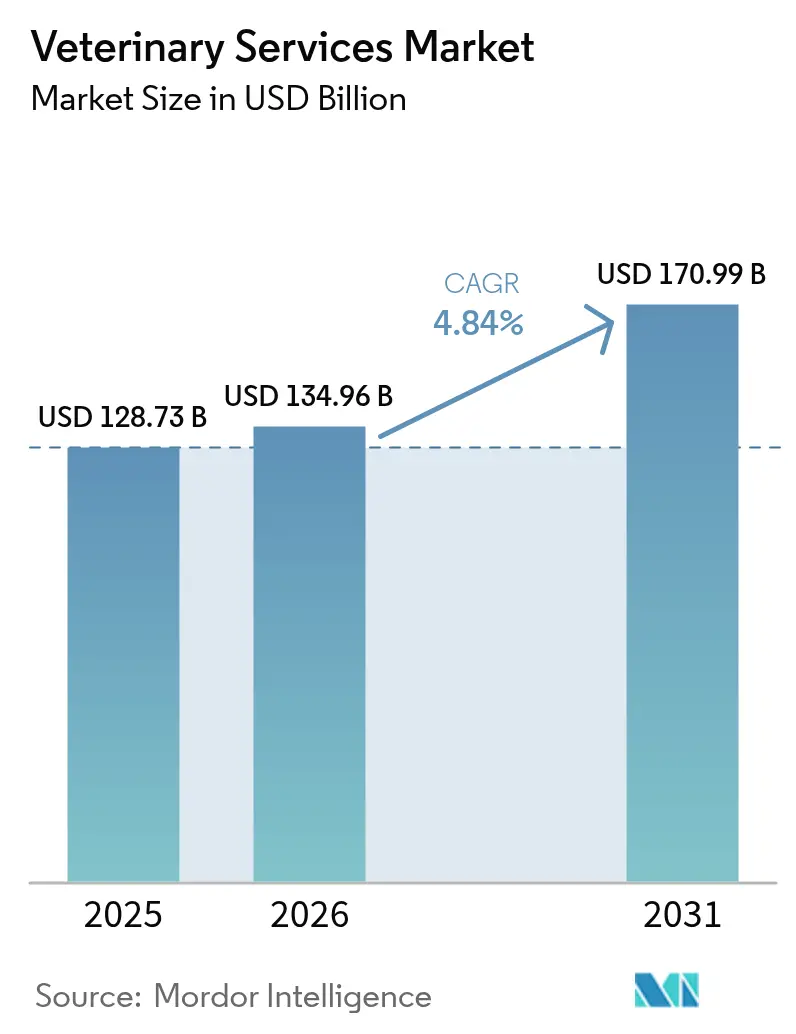

| Market Size (2026) | USD 134.96 Billion |

| Market Size (2031) | USD 170.99 Billion |

| Growth Rate (2026 - 2031) | 4.84% CAGR |

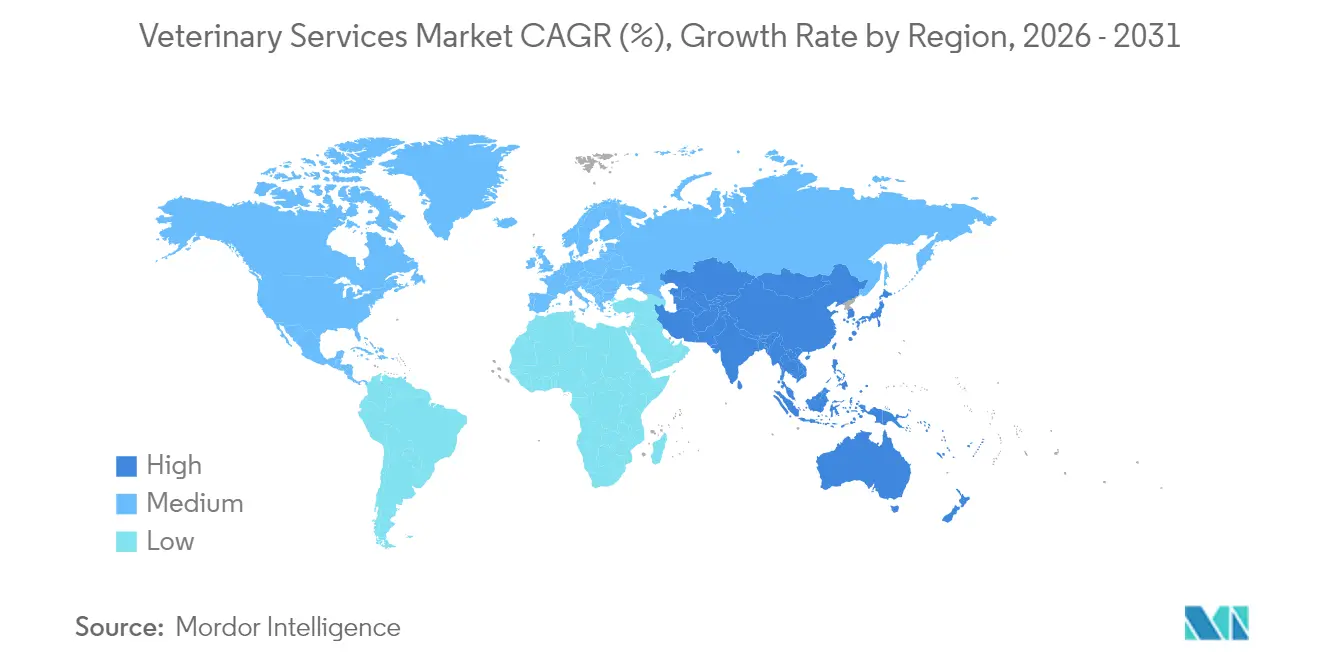

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

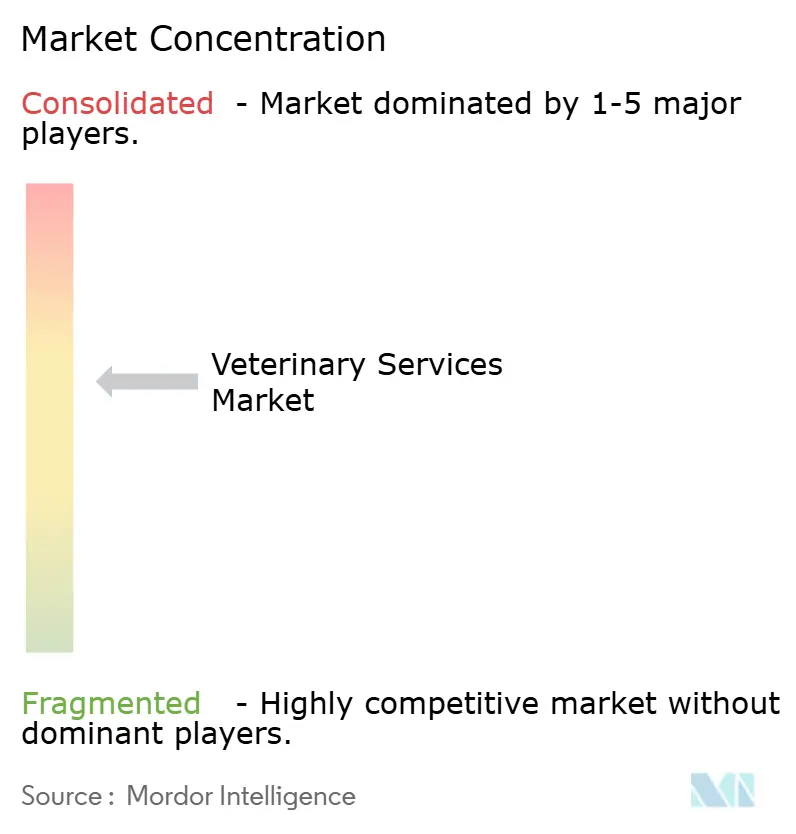

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Services Market Analysis by Mordor Intelligence

The veterinary services market size was valued at USD 128.73 billion in 2025 and estimated to grow from USD 134.96 billion in 2026 to reach USD 170.99 billion by 2031, at a CAGR of 4.84% during the forecast period (2026-2031). Healthy pet-owner spending, rapid technology adoption, and sustained corporate buy-outs keep the veterinary services market on an expansion path. Preventive medicine captures demand as households shift from episodic to continuous care, while artificial intelligence raises diagnostic throughput and supports busy clinicians. Private-equity and strategic buyers accelerate roll-up activity to secure scale economies, data assets, and talent pools. Demand also grows outside companion care: zoonotic-disease surveillance, livestock productivity mandates, and One-Health policy frameworks widen the revenue base of the veterinary services market.

Key Report Takeaways

- By service, preventive and wellness care led with 31.02% revenue share in 2025; tele-health and virtual care are projected to expand at a 6.45% CAGR through 2031.

- By animal type, companion animals accounted for 62.68% of the veterinary services market share in 2025; the same segment is set to post the fastest 6.63% CAGR by 2031.

- By provider ownership, corporate clinic chains held 40.92% of the veterinary services market in 2025, while mobile and house-call practices record the strongest 7.49% CAGR.

- By delivery mode, brick-and-mortar clinics maintained 73.58% share of the veterinary services market size in 2025; tele-consultation platforms will grow at 7.18% CAGR to 2031.

- Geographically, North America controlled 42.01% of the veterinary services market in 2025; Asia-Pacific is the fastest-growing region with a 5.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Services Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Pet Ownership & Humanisation of Animals | +1.8% | North America & Europe (high), APAC (rising) | Long term (≥ 4 years) |

| Increasing Incidence of Zoonotic & Chronic Animal Diseases | +1.2% | Global; heightened focus in APAC & emerging markets | Medium term (2-4 years) |

| Growing Livestock Productivity & Food-Safety Requirements | +0.9% | APAC & South America agricultural hubs | Long term (≥ 4 years) |

| Expansion of Pet-Insurance Reimbursement Models | +0.6% | North America & Western Europe | Medium term (2-4 years) |

| AI-Enabled Triage & Diagnostics Boosting Clinic Capacity | +0.7% | North America & Europe initially, expanding to APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Pet Ownership & Humanisation of Animals

Pet ownership reached 94 million U.S. households in 2025, up from 56 million in 2011, and Generation Z now represents the fastest-growing cohort of new owners[1]American Pet Products Association, “2024–2025 National Pet Owners Survey,” americanpetproducts.org. This demographic expects oncology, cardiology, and behavioural therapies once reserved for human medicine. High-net-worth clients also purchase concierge plans that bundle genomic screening, nutrition counselling, and 24/7 tele-access to specialists. Such premiumisation strengthens cash-flow visibility across the veterinary services market while justifying equipment upgrades and specialist training.

Increasing Incidence of Zoonotic & Chronic Animal Diseases

The 2024 H5N1 influenza episode affected more than 800 U.S. dairy herds, with 66 confirmed human infections traced to animal exposure. Companion pets live longer, which increases chronic conditions: 73% of dogs and 64% of cats were diagnosed with dental disease in 2024. These dual pressures support sustained laboratory, imaging, and bio-security spending within the veterinary services market.

Growing Livestock Productivity & Food-Safety Requirements

USDA surveillance programs safeguard export credibility and detect antimicrobial resistance, reinforcing demand for herd-health consulting and vaccination campaigns. Low-income regions register lower vaccination rates, opening service-outsourcing opportunities for multinational providers. State-funded incentives, such as Virginia’s USD 110,000 grants for rural large-animal practice, aim to correct workforce gaps.

AI-Enabled Triage & Diagnostics Boosting Clinic Capacity

Thirty percent of veterinarians now deploy AI tools for imaging, cytology, and practice-management workflows. Solutions such as Vetscan Imagyst analyse slides in minutes, easing caseload spikes amid clinician shortages. Machine-learning models also forecast local disease outbreaks, allowing clinics to pre-position treatments, an efficiency dividend that strengthens the veterinary services market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global Shortage & Burnout of Veterinarians | -1.4% | Rural North America, APAC, parts of Europe | Medium term (2-4 years) |

| Escalating Cost of Advanced Procedures & Equipment | -0.8% | North America & Europe; urban APAC centers | Short term (≤ 2 years) |

| Regulatory Ambiguity on Cross-Border Tele-Veterinary Care | -0.5% | Europe (intra-EU), North America, APAC | Medium term (2-4 years) |

| Consumer Price-Sensitivity Causing Deferred Care | -0.4% | Global; strongest in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Global Shortage & Burnout of Veterinarians

Forecasts show a deficit of 70,092 veterinarians by 2032 versus only 52,926 graduates, a shortfall aggravated by student debt that averages USD 400,000[2]American Association of Veterinary Medical Colleges, “Workforce Demand Study 2025,” aavmc.org. Burnout exceeds 40%, and suicide risk remains elevated, pressuring clinic rosters in the veterinary services industry. Rural zones suffer most, with 243 U.S. counties classified as shortage areas in 2025.

Escalating Cost of Advanced Procedures & Equipment

Veterinary care prices climbed 7.6% between May 2023 and May 2025, far above general inflation. Capital-intensive MRI or CT units push independent practices toward corporate buyers or referral strategies. Sixty percent of owners cite affordability as the main barrier to care, curbing elective spending in parts of the veterinary services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Preventive Care Dominance Drives Digital Transformation

Preventive and wellness care captured 31.02% of 2025 revenue, anchoring the veterinary services market. Subscription wellness plans and annual health screens generate predictable margins, while pharmacy auto-refills deepen client stickiness. The veterinary services market size for tele-health is set to climb from USD 392.98 million in 2026 to USD 0.54 billion by 2031, a 6.45% CAGR. AI-enhanced imaging lifts throughput and supports surge capacity. Surgical demand stabilises as minimally-invasive techniques cut recovery time. Dental procedures remain lucrative, averaging USD 170-350 per case, and 73% of dogs need at least one intervention during their lifetime.

Diagnostic laboratories enjoy cross-selling with clinics, and e-prescribing platforms streamline drug compliance. Emergency and critical-care centres face labour constraints, prompting corporate groups to open 24-hour hubs linked by tele-ICU dashboards. Rehabilitation, acupuncture, and hydro-therapy gain traction as pets age, extending lifetime spending in the veterinary services market.

By Animal Type: Companion Animals Lead Growth Amid Livestock Surveillance Expansion

Companion animals constituted 62.68% of revenue in 2025 and will post the fastest 6.63% CAGR through 2031. Dogs continue as the largest sub-segment, with oncology and cardiology services mirroring human care protocols. Urban cat ownership rises among millennials and Generation Z, pushing demand for feline-only clinics. Equine medicine remains niche but commands high average transaction values for lameness diagnostics and sports-injury rehabilitation.

Production animals demand service integration after the H5N1 dairy-herd outbreak highlighted public-health risks. Cattle operators now purchase real-time monitoring and vaccine-compliance audits. Swine and poultry producers expand comprehensive bio-security packages, and aquaculture ventures request specialised health plans, both adding breadth to the veterinary services market. Small ruminants gain attention as consumers diversify protein sources, further widening the client base.

By Provider Ownership Structure: Corporate Consolidation Accelerates Amid Independent Innovation

Corporate chains held 40.92% of 2025 revenue. Mars Incorporated alone operates nearly 3,000 clinics worldwide after absorbing VCA for USD 9.1 billion and later acquisitions. National Veterinary Associates split its specialty and general-practice businesses ahead of a possible IPO. Mission Veterinary Partners and Southern Veterinary Partners plan a merger covering 730 sites, a deal currently under antitrust review.

Mobile and house-call practices clock a 7.49% CAGR, appealing to time-pressed owners and clinicians seeking lifestyle balance. The Vets and BetterVet merger extended mobile reach to 30 cities, lifting the segment’s share of the veterinary services market. Universities and referral centres offer advanced modalities, such as interventional radiology, and act as talent incubators while generating premium caseloads.

By Delivery Mode: Traditional Clinics Adapt While Digital Platforms Surge

Brick-and-mortar facilities still account for 73.58% of 2025 spending, supported by the hands-on nature of diagnosis and surgery. Yet the tele-consultation slice of the veterinary services market is growing at 7.18% CAGR. California’s Assembly Bill 1399 and similar rules in Colorado formalised virtual-care protocols and broadened technician duties, unlocking efficiencies. Wearables capture vitals, allowing remote monitoring between visits, and AI triage guides owners to in-person care when warranted.

Farm and mobile services bridge rural gaps, especially in shortage counties. Airvet raised USD 11 million to scale a virtual triage platform, seeking to mitigate an estimated 15,000 veterinarian deficit by 2030. Traditional clinics respond by extending hours, adding curbside drop-off, and embedding cloud practice-management to keep pace with the digital pivot.

Geography Analysis

North America retained 42.01% of global revenue in 2025. Mature insurance penetration, robust e-commerce pharmacy channels, and One-Health policy integration sustain premium-price elasticity. Multinational chains cluster around U.S. urban centres, and Canadian operators observe similar consolidation but tailor offerings to public-health mandates. Mexico’s rising middle class fuels double-digit pet-food growth, a signal of downstream service opportunity.

Europe shows steady uptake. The United Kingdom’s Royal College of Veterinary Surgeons streamlines accreditation, facilitating cross-border clinician mobility. Germany and France invest in surveillance platforms that link animal and human epidemiological data. EQT’s acquisition of VetPartners indicates capital inflows aiming at clinic platform scaling across member states. Regulatory harmonisation for tele-medicine and prescription data interoperability aids clinic groups in capturing operational synergies across the veterinary services market.

Asia-Pacific is the fastest-expanding zone at 5.57% CAGR. China’s pet-medical spend hit 1,062 billion yuan in 2024 and keeps rising despite fragmentation. India’s pet-food market is growing at 15.37% CAGR and pulls ancillary services such as dietetic consults and dermatology. Japan’s super-aging dogs spur demand for geriatric care, while South Korea pioneers AI algorithms for small-animal imaging. Australia’s clinic roll-ups attract European buyers hunting for exposure to a high-compliance market. Collectively, these dynamics enlarge the veterinary services market size for the region.

Competitive Landscape

The veterinary services market shows moderate concentration and rising deal momentum. Mars Incorporated integrates pet food, diagnostics, and clinics, extracting scale benefits and data synergies. Private-equity ownership expanded from 8% of U.S. clinics in 2011 to nearly 50% by 2025, anchoring cost-of-capital advantages for serial acquirers. Covetrus was taken private for USD 4 billion, underscoring investor appetite for technology distributors. PE groups assemble regional networks, invest in AI workflow tools, and upgrade referral centres to protect margins.

White-space niches include mobile veterinary services, specialist dermatology, and rehabilitation, where smaller operators innovate without heavy fixed-asset burdens. The FDA’s Veterinary Innovation Program offers expedited pathways for software-as-a-medical-device, reducing regulatory friction. Corporate acquirers chase these assets to refresh growth and diversify against economic cycles. Despite consolidation, independent clinics still hold 51% of sites, leveraging personalised care and community ties.

The market therefore balances scale benefits with room for disruptors. AI and remote monitoring ease labour strain, but talent scarcity keeps salary inflation high. Consolidators will likely continue to pay premiums for top-tier clinics, sustaining a pipeline of exits for owner-founders and PE sponsors in the veterinary services market.

Veterinary Services Industry Leaders

Mars Inc.

National Veterinary Associates (NVA)

CVS Group PLC

IVC Evidensia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Mars Incorporated acquired Heska for USD 120 per share, expanding its diagnostics portfolio

- October 2024: Animal Dermatology Group bought four specialty practices across four U.S. states.

- October 2024: Tractor Supply purchased Allivet to enter veterinary pharmaceuticals.

- July 2024: Incorporated completed its purchase of Cerba Vet and ANTAGENE diagnostic businesses.

Global Veterinary Services Market Report Scope

As per the scope of the report, veterinary services refer to all kinds of facilities, solutions, systems, and services targeted at animal health welfare, including hospitalization, dentistry, diagnostics, surgery, nursing, medication, medical devices, specialist referral, alternative therapies, and behavioral therapies performed by a veterinarian. The Veterinary Services Market is segmented by Service (Surgery, Diagnostic Tests and Imaging, Physical Health Monitoring, and Other Services), Animal Type (Companion Animal, and Farm Animal), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Surgery |

| Diagnostic Imaging & Laboratory |

| Preventive & Wellness Care |

| Emergency & Critical Care |

| Tele-health & Virtual Care |

| Rehabilitation & Physiotherapy |

| Dentistry |

| Pharmacy & Prescription Management |

| Companion Animals | Dogs |

| Cats | |

| Horses & Equine | |

| Production / Farm Animals | Cattle & Buffalo |

| Swine | |

| Poultry | |

| Small Ruminants | |

| Aquaculture Species |

| Independent Practices |

| Corporate Clinic Chains |

| Mobile / House-call Practices |

| University & Referral Hospitals |

| In-Clinic (Brick & Mortar) |

| Mobile / On-farm |

| Tele-consultation Platforms |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service | Surgery | |

| Diagnostic Imaging & Laboratory | ||

| Preventive & Wellness Care | ||

| Emergency & Critical Care | ||

| Tele-health & Virtual Care | ||

| Rehabilitation & Physiotherapy | ||

| Dentistry | ||

| Pharmacy & Prescription Management | ||

| By Animal Type | Companion Animals | Dogs |

| Cats | ||

| Horses & Equine | ||

| Production / Farm Animals | Cattle & Buffalo | |

| Swine | ||

| Poultry | ||

| Small Ruminants | ||

| Aquaculture Species | ||

| By Provider Ownership Structure | Independent Practices | |

| Corporate Clinic Chains | ||

| Mobile / House-call Practices | ||

| University & Referral Hospitals | ||

| By Delivery Mode | In-Clinic (Brick & Mortar) | |

| Mobile / On-farm | ||

| Tele-consultation Platforms | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the veterinary services market?

The veterinary services market is valued at USD 134.96 billion in 2026.

How fast is the veterinary services market expected to grow?

The market is projected to expand at a 4.84% CAGR, reaching USD 170.99 billion by 2031.

Which service segment holds the largest share?

Preventive and wellness care led with 31.02% of revenue in 2025.

Why is Asia-Pacific the fastest-growing region?

Urbanisation, rising disposable incomes, and shifting cultural attitudes toward companion animals drive a 5.57% CAGR in Asia-Pacific.

How is artificial intelligence influencing veterinary care?

Thirty percent of veterinarians already use AI to accelerate imaging interpretation, cytology analysis, and workflow management, improving capacity amid workforce shortages.

What challenges could slow market growth?

An acute veterinarian shortage and rising treatment costs could limit clinic capacity and suppress demand in certain demographics.

Page last updated on: