Veterinary Surgical Instruments Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

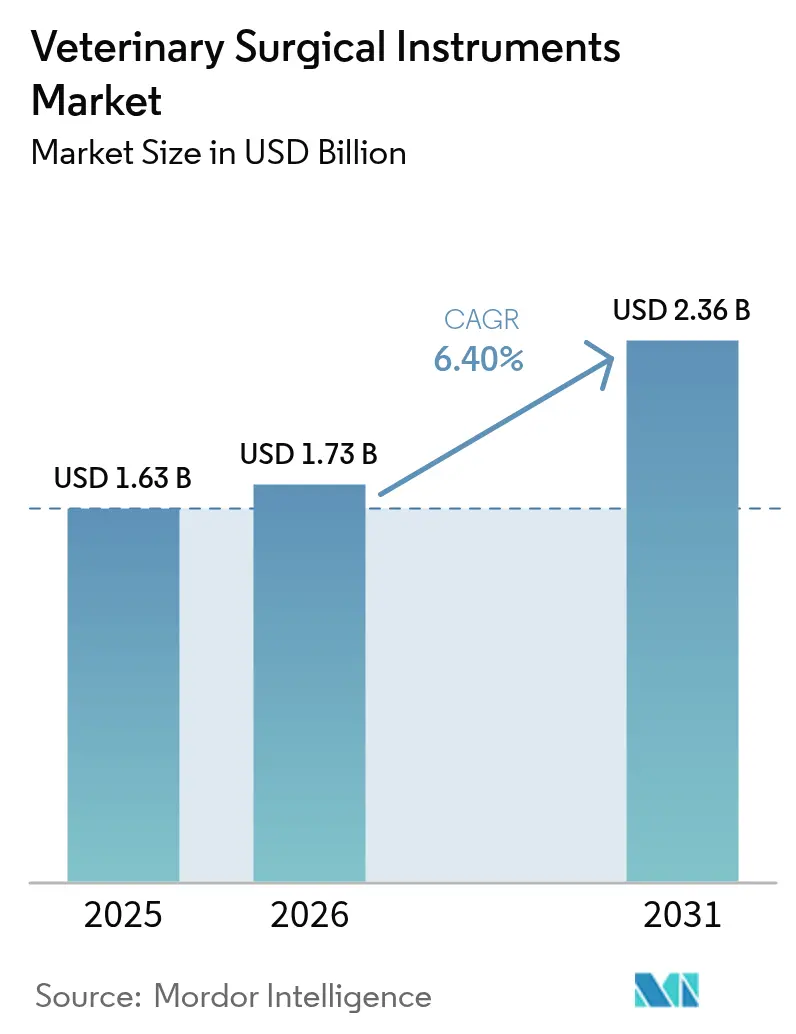

| Market Size (2026) | USD 1.73 Billion |

| Market Size (2031) | USD 2.36 Billion |

| Growth Rate (2026 - 2031) | 6.40% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

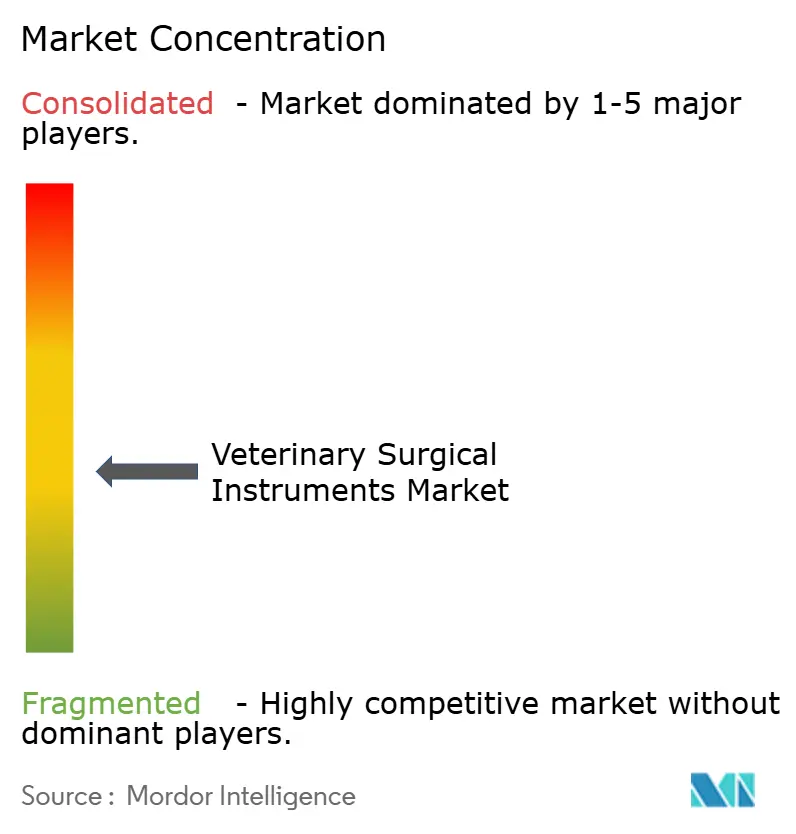

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Surgical Instruments Market Analysis by Mordor Intelligence

The veterinary surgical instruments market size is expected to grow from USD 1.63 billion in 2025 to USD 1.73 billion in 2026 and is forecast to reach USD 2.36 billion by 2031 at 6.40% CAGR over 2026-2031. Companion-animal demand, rapid innovations in electrosurgery, and expanding pet insurance coverage are propelling revenue. Precision-based protocols, particularly minimally invasive surgery, are pushing clinics to upgrade to high-definition visualization, bipolar electrosurgery, and 3D-printed orthopedic implants. Asia-Pacific shows the strongest momentum thanks to rising disposable income, government-led infrastructure programs, and a growing urban pet population. Orthopedic surgery is emerging as the next growth engine, supported by custom implants and AI-guided planning. Still, high capital costs and a global shortfall of board-certified surgeons threaten adoption rates, underscoring the importance of training and flexible financing for new equipment.

Key Report Takeaways

- By animal type, companion animals commanded 68.45% of the veterinary surgical instruments market share in 2025, while farm animals trailed at 31.55%.

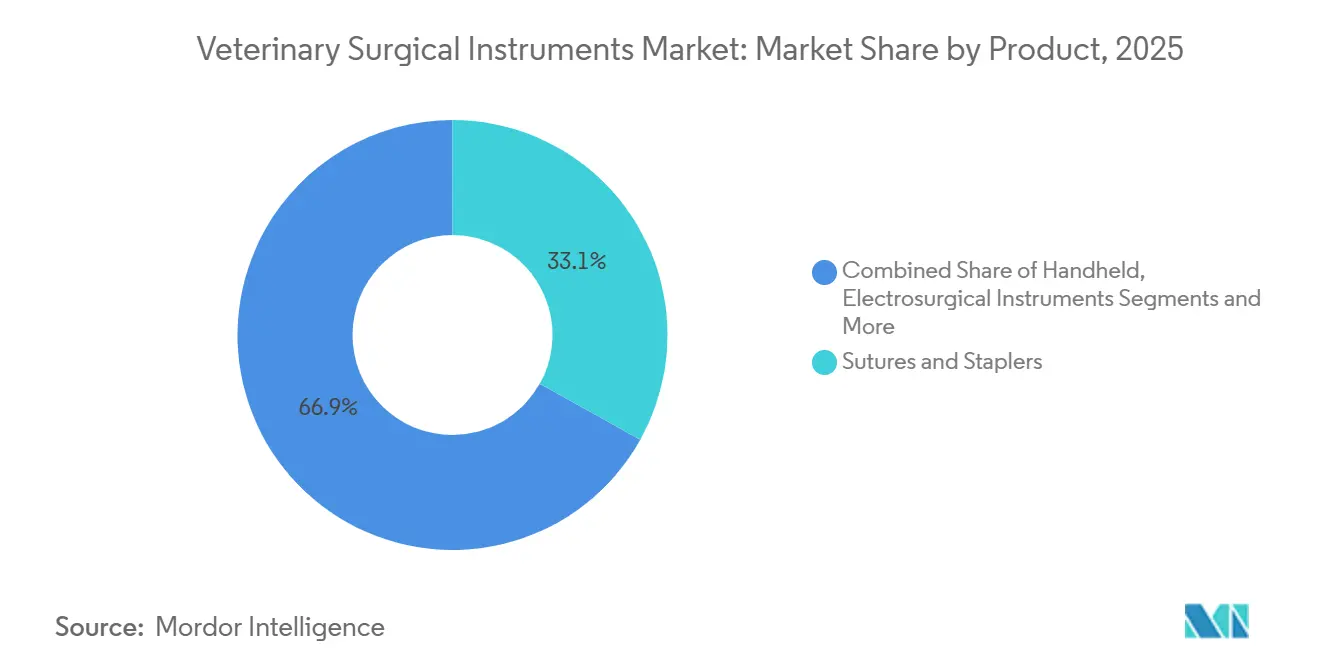

- By product category, sutures and staplers led with 33.10% revenue share in 2025; electrosurgery instruments are projected to expand at a 9.60% CAGR to 2031.

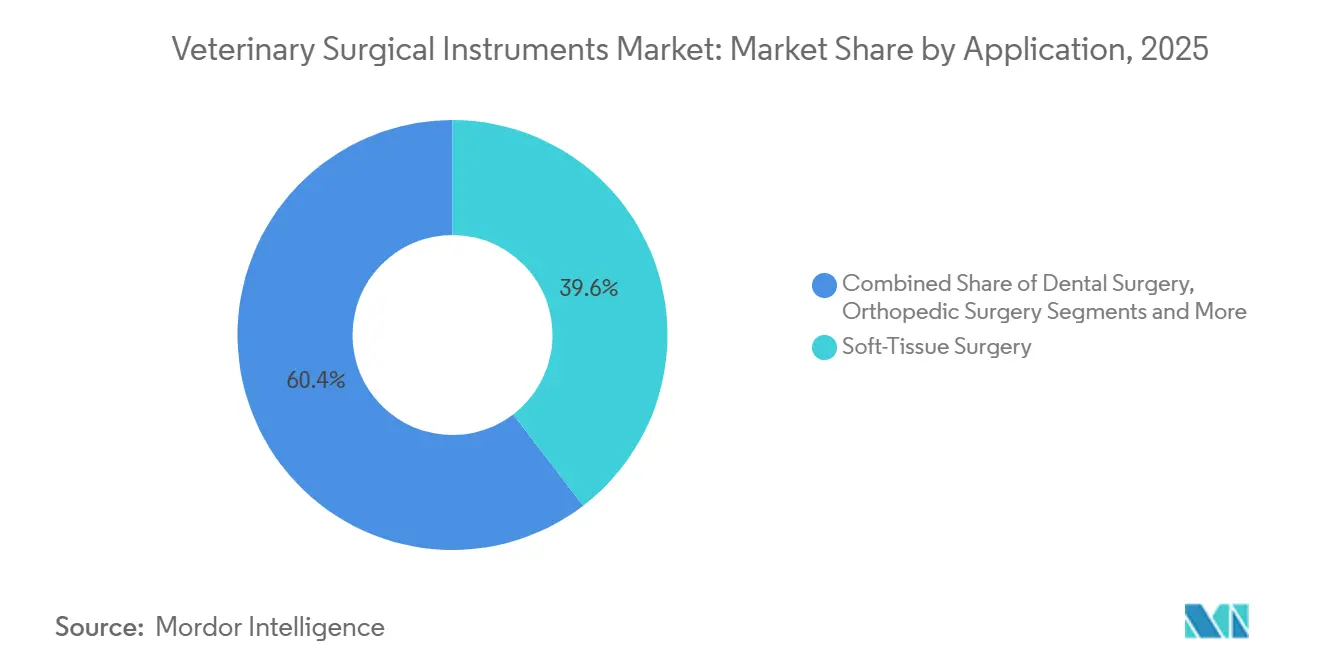

- By application, soft-tissue surgery accounted for a 39.60% share of the veterinary surgical instruments market size in 2025, whereas orthopedic surgery is advancing at an 8.33% CAGR through 2031.

- By geography, North America generated 37.40% of 2025 revenue; Asia-Pacific is forecast to grow at 10.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Veterinary Surgical Instruments Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Minimally-invasive surgery trend in animals | +1.30% | North America & Western Europe (core); APAC spill-over via referral hospitals in Australia, Japan, South Korea | Medium term (2–4 years) |

| Rising pet ownership and pet insurance penetration | +1.50% | Global; strongest in North America, UK, Germany, Australia; accelerating in Brazil, China | Short term (≤ 2 years) |

| Rising animal disease burden and spay/neuter programs boosting surgical volumes | +1.10% | Global; municipal program intensity highest in India, Mexico, Turkey, and across Latin America | Short term (≤ 2 years) |

| Increasing R&D expenditure and product innovation for animal healthcare | +0.80% | North America & EU (R&D origin); global adoption lag of 2–4 years in MEA and Southeast Asia | Long term (≥ 4 years) |

| Expansion of veterinary healthcare infrastructure coupled with government initiatives and animal welfare regulations | +0.70% | APAC core (China, India); spill-over to MEA (GCC, South Africa) and Eastern Europe | Long term (≥ 4 years) |

| Clinic corporatization unlocking budgets for premium instruments | +0.60% | North America (most advanced consolidation), UK, Germany, Australia; early-stage in France, Spain | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Minimally-invasive surgery trend in animals

Demand for laparoscopic and arthroscopic procedures is transforming the veterinary surgical instruments market. Recovery times fall by up to 65% and complication rates decline when trocars, cannulas, and HD endoscopes replace open techniques. U.S. specialty clinics report 42% MIS adoption for spays, while 56% of orthopedic specialists deploy arthroscopy to refine joint diagnostics. Clinics that market shorter convalescence periods see higher case acceptance, pushing distributors to prioritize MIS-ready kits. Manufacturers respond with ergonomic instrument handles that minimize surgeon fatigue during procedures lasting beyond 90 minutes.

Rising pet ownership and pet-insurance penetration

Ninety-four million U.S. households kept pets in 2024, and 4.4 million of those owners insured their animals, triggering 40% higher veterinary outlays per insured pet[1]American Veterinary Medical Association, “Artificial Intelligence in Clinical Practice,” avma.org. This behavior directly lifts procedure volumes for orthopedic repair, cardiac interventions, and advanced dentistry. Insurers, meanwhile, influence procurement by reimbursing clinics that use certified devices, indirectly accelerating premium instrument purchases. Cities such as London, New York, and Shanghai form dense clusters of high-end demand, allowing suppliers to pilot AI-enabled electrosurgery platforms before wider rollout.

Growing disease burden and spay-neuter programs

Shelter medicine accounts for a rising share of the veterinary surgical instruments industry. SPCA International’s 2025 grant funded sterilizations for 10,000 animals, boosting needs for standardized, durable spay packs[3]SPCA International, “2025 Spay-Neuter Initiative Funding,” spcai.org. High-volume clinics conduct over 5,000 procedures annually and replace instruments every 6-8 months, while mobile units prize portability and rapid autoclave cycles. Conversely, aging companion animals require therapeutic orthopedics and oncology surgeries, creating a dual-track market split between cost-sensitive shelters and premium referral centers.

Intensifying R&D and product innovation

University ties are shortening innovation cycles. The University of California, Davis installed 25 ultra-clean suites in 2025 that support robotic scopes and custom 3D-printed titanium hip implants[2]University of California Davis, “Advanced Veterinary Surgery Center Opens,” vetmed.ucdavis.edu. AI-assisted planning software guides drilling trajectories within 0.5 mm accuracy, reducing operative time. Companies that co-develop prototypes with teaching hospitals secure early-adopter revenue and publish validation studies, positioning their catalogues as the evidence-based option for private clinics.

Restraints Impact Analysis of Veterinary Surgical Instruments Market*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced Surgical Instruments and Procedures | -1.2% | Global, most significant in developing regions and rural areas | Medium to Long term (2-4+ years) |

| Shortage of board-certified veterinary surgeons | -0.9% | Global, most severe in rural areas and developing regions | Long term (≥ 4 years) |

| Stringent Regulatory Approvals | -0.6% | North America and Europe, with increasing impact in Asia-Pacific | Medium term (2-4 years) |

| Limited sterilization infrastructure in smaller clinics curbs adoption of complex reusable surgical tools | -0.5% | Global, most significant in developing regions and rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High costs limiting adoption of advanced instruments

Premium electrosurgery towers can top USD 50,000 when bundled with smoke evacuators and bipolar forceps. Maintenance contracts, tip replacements, and technician training push total cost of ownership far above basic scalpel sets, widening the technology gap between high-end referral hospitals and rural practices. Leasing, pay-per-use, and refurbished options are gaining traction, but uptake remains uneven in India, Brazil, and South-East Asia.

Shortage of board-certified veterinary surgeons

The projected shortfall of 17,000 U.S. veterinarians by 2032 disproportionately affects surgical specialties. Practices equipped with modern towers often defer complex cases due to staffing gaps, slowing capital rotation on new devices. Accredited residency programs expand seats only gradually, making human-resource constraints more persistent than import duties or approval delays.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Veterinary Surgical Instruments Market Segment Analysis

By Product:

Electrosurgery instruments gain tractionSutures and staplers continued to command 33.10% of 2025 sales. Yet electrosurgery systems are the fastest climber with a 9.60% CAGR that will add roughly USD 245 million to the veterinary surgical instruments market size by 2031. The veterinary surgical instruments market benefits from ergonomically contoured handles and foot-switch integration that lessen fatigue during two-hour tumor resections. Handheld scissors, needle holders, and rongeurs remain essential, but demand now centers on premium steel grades and micro-serrated edges that prolong sharpness.

Veterinary teaching hospitals in the United States and Australia have publicized cardiology firsts such as transcatheter mitral-valve repair in dogs, demonstrating electrosurgery’s widening clinical scope. This evidence base nudges private clinics toward mid-range bipolar generators instead of entry-level monopolar units. Suppliers bundle trocar sets and smoke extractors, boosting average sale value per clinic by 28% between 2024 and 2025.

By Animal:

Companion animals sustain premium demandDogs and cats underpin 68.45% of revenue, with the veterinary surgical instruments market share for companion species projected to edge up as procedures shift from curative to wellness-oriented. The veterinary surgical instruments market records an 8.14% CAGR in this segment, fueled by joint replacements, brachycephalic airway surgeries, and advanced dentistry. Urban adoption of wellness packages makes financing elective cruciate repairs more predictable, driving hospitals to stock complete arthroscopy towers.

Farm livestock still requires rugged instruments that tolerate field sterilization. Bovine procedures such as displaced abomasum correction rely on stainless-steel trocars with replaceable cannulas, whereas swine castration sets emphasize low cost per use. Poultry, though high in volume, captures modest equipment revenue, encouraging suppliers to offer bulk packaging and rapid turnaround sharpening services rather than premium innovations.

By Application:

Orthopedic surgery emerges as the growth engineSoft-tissue procedures hold 39.60% of current demand, yet orthopedic interventions outpace at an 8.33% CAGR, reflecting improvements in titanium locking plates and CT-guided osteotomy planning. The veterinary surgical instruments market size for orthopedic kits is forecast to pass USD 623 million by 2031, spurred by 3D-printed implants that match canine femoral geometry.

Referral hospitals invest in low-profile drill guides and variable-angle screw systems that mirror human trauma sets. Dental surgery follows orthopedic as clinics adopt dedicated delivery carts and LED fiber optics. Ophthalmology, though niche, supports high-margin phacoemulsification tips and microsurgical forceps, validating the case for multispecialty portfolios.

Geography Analysis

Midwest and Mountain United States Veterinary Surgical Instruments Market

North America generated 37.40% of global sales in 2025. Early adoption of AI-assisted imaging and a pet-insurance culture enable clinics to upgrade every five to seven years instead of once a decade. Thirty percent of U.S. veterinarians already use some form of artificial intelligence during diagnosis, increasing data capture that feeds back into surgical planning. Nonetheless, the veterinarian shortage is acute in Midwest and Mountain states, stretching case loads and pushing tele-mentoring for general practitioners undertaking complex procedures.

APAC Veterinary Surgical Instruments Market

Asia-Pacific is the fastest-growing territory at 10.05% CAGR. China’s 2025 medical-device fair introduced an AI-integrated orthopedic robot, reinforcing investor appetite for high-precision systems. India’s private chain hospitals are experimenting with subscription-based service contracts to spread equipment costs. Regional governments link zoonotic-disease surveillance with veterinary-hospital expansion, unlocking grants for autoclaves and endoscopes in tier-two cities. These policies are broadening distributor networks and compressing delivery times for critical parts.

EMEA and LATAM Veterinary Surgical Instruments Market

Europe maintains stringent welfare regulations that require certified instrument traceability and sterile reprocessing logs. The CVS Group’s USD 54.7 million spend on upgrades in 2024 underlines the region’s willingness to rotate stock toward high-performance alloys with traceable lot numbers. Meanwhile, Latin America and the Middle East and Africa show accelerating demand as pet ownership climbs. Brazil leads surgical-instrument imports, while Gulf markets prioritize equine surgery, raising requirements for extra-long bone plates and laryngoscopic devices.

Competitive Landscape

The veterinary surgical instruments market houses a mix of global device giants and niche veterinary specialists. No single vendor controls more than 10%-12% of revenue, reflecting a moderately fragmented profile. Players differentiate through procedure-specific kits rather than broad catalogues. GerVetUSA’s customizable dental and spay packs, unveiled at the 2025 Animal Care Expo, target busy urban clinics seeking standardized layouts. Integra LifeSciences leverages its human-neuro portfolio to cross-sell high-precision rongeurs for small-animal neurosurgery.

Digital features form the next battleground. VetOvation partners with human-device makers to adapt smoke evacuation and laparoscopic insufflation for compact spaces. Start-ups offering 3D-printed patient-matched implants challenge incumbents on turnaround speed, while established brands reply with validated fatigue-testing data. Distribution alliances remain critical: regional distributors that stock sterile sets and provide same-day sharpening services secure repeat orders even when price premiums run 15%.

Veterinary Surgical Instruments Industry Leaders

Integra LifeSciences

B. Braun SE

Medtronic

Veterinary Instrumentation (Vi)

Jorgensen Laboratories

- *Disclaimer: Major Players sorted in no particular order

Veterinary Surgical Instruments Market Companies Covered in this Report

- B. Braun

- Medtronic

- Integra LifeSciences

- Jorgensen Laboratories

- Kshama Surgical

- Accesia AB

- GerVetUSA

- Arch Medical Solutions Company (gSource)

- Orthomed (UK) Ltd

- Johnson & Johnson

- Eickemeyer Veterinary Equipment

- World Precision Instruments

- Dentalaire International

- SAI Infusion Technologies

- Granim Healthcare (DRE Veterinary)

- Amerisource Bergen Corporation

- Surgical Holdings

- Aspen Surgical Products, Inc.

- IndoSurgicals Private Limited

- Rajindra Surgical Industries

Recent Industry Developments in Veterinary Surgical Instruments Market

- April 2025: The China International Medical Equipment Fair showcased Longwood Valley MedTech’s ROPA orthopedic robot integrating AI deep learning, signaling imminent cross-over to veterinary use.

- March 2025: University of California, Davis inaugurated a 7,300 sq ft Advanced Veterinary Surgery Center with 25 operating rooms and in-house 3D-printing labs.

- January 2025: Michigan State University secured AO Foundation funding to refine pulse-drilling techniques that reduce thermal necrosis during orthopedic fixation.

- March 2024: AO Foundation released distal femoral osteotomy plates and screw targeting clamps for canine patellar luxation repairs

Veterinary Surgical Instruments Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the veterinary surgical instruments market as all purpose-built handheld devices, powered tools, and electrosurgery units that cut, dissect, cauterize, retract, ligate, or close tissue during surgery on companion and farm animals in clinics, hospitals, and specialty centers. Mordor Intelligence sizes this market at USD 1.63 billion for 2025.

Scope exclusion: instruments intended solely for industrial slaughterhouses and any pharmaceutical, implant, or imaging consumables are outside scope.

Segments Covered in This Report

- By Product

- Sutures and Staplers

- Handheld Instruments

- Scalpels

- Forceps

- Scissors

- Retractors

- Electro-surgery Instruments

- Other Products

- Trocars and Cannulas

- Suction and Irrigation

- By Animal

- Companion Animals

- Dogs

- Cats

- Farm Animals

- Bovine

- Swine

- Poultry

- Companion Animals

- By Application

- Soft-Tissue Surgery

- Dental Surgery

- Orthopedic Surgery

- Ophthalmic Surgery

- Other Applications

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

We interviewed board-certified surgeons, procurement heads at multi-clinic chains, and distributors across North America, Europe, and Asia-Pacific. Their insights refined instrument life cycles, price dispersion, and adoption rates for minimally invasive kits, letting us stress-test early desk findings.

Desk Research

We began by collecting USDA livestock inventories, AVMA pet-ownership surveys, WOAH disease logs, and UN Comtrade shipment codes to anchor animal numbers and procedure triggers. Our analysts then tapped D&B Hoovers and Dow Jones Factiva to track company filings, catalog prices, and plant expansions, grounding our average selling price assumptions. A review of peer-reviewed articles in Veterinary Surgery and policy notes from the European Commission's Animal Health Directorate clarified procedure-mix shifts and regulatory inflection points. These references are illustrative; many other public and paid sources informed evidence gathering.

Market-Sizing & Forecasting

A top-down model converts validated animal counts into surgery volumes through prevalence ratios, multiplies those by replacement cycles and average prices, and then cross-checks totals with selective bottom-up supplier roll-ups. Multivariate regression links forecast growth to pet-insurance penetration, disposable income, clinic density, regulatory approvals, and technology upgrades, while scenario analysis frames upside from faster electrosurgery uptake. Data gaps on niche tools are bridged with weighted averages from adjacent classes.

Data Validation & Update Cycle

Outputs undergo variance tests against customs values and a second-analyst peer review before sign-off. We refresh models each year and issue interim updates when price or policy shifts breach preset thresholds, so clients always receive the latest view.

How Mordor Intelligence's Veterinary Surgical Instruments Market Size Compares to Other Published Estimates

Published estimates often diverge because providers select different product baskets, price escalators, and refresh rhythms.

The widest gaps arise when disposables are bundled, 2022 prices are frozen, or Asia's fast-growing referral centers are underweighted.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.63 B | Mordor Intelligence | - |

| USD 1.78 B | Global Consultancy A | Bundles drapes and generic disposables |

| USD 1.44 B | Trade Journal B | Uses static 2022 prices, omits specialty-center surge |

By pairing a clearly bounded scope with live price tracking and a disciplined update rhythm, we deliver a balanced, transparent baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the veterinary surgical instruments market?

The market is worth USD 1.73 billion in 2026 and is on course to reach USD 2.36 billion by 2031.

Which product category is growing fastest?

Electrosurgery instruments lead growth with a 9.60% CAGR, spurred by rising adoption of bipolar and AI-assisted devices.

Why is Asia-Pacific the most attractive growth region?

Rapid urban pet ownership, government investment in veterinary infrastructure, and rising disposable income drive a 10.05% CAGR in Asia-Pacific.

Which surgical application offers the best long-term opportunity?

Orthopedic surgery, supported by 3D-printed implants and precision drilling tools, is expected to post the highest growth through 2030.

How does the shortage of veterinary surgeons impact equipment demand?

In 2025, the North America accounts for the largest market share in Veterinary Surgical Instruments Market.

Page last updated on: