Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

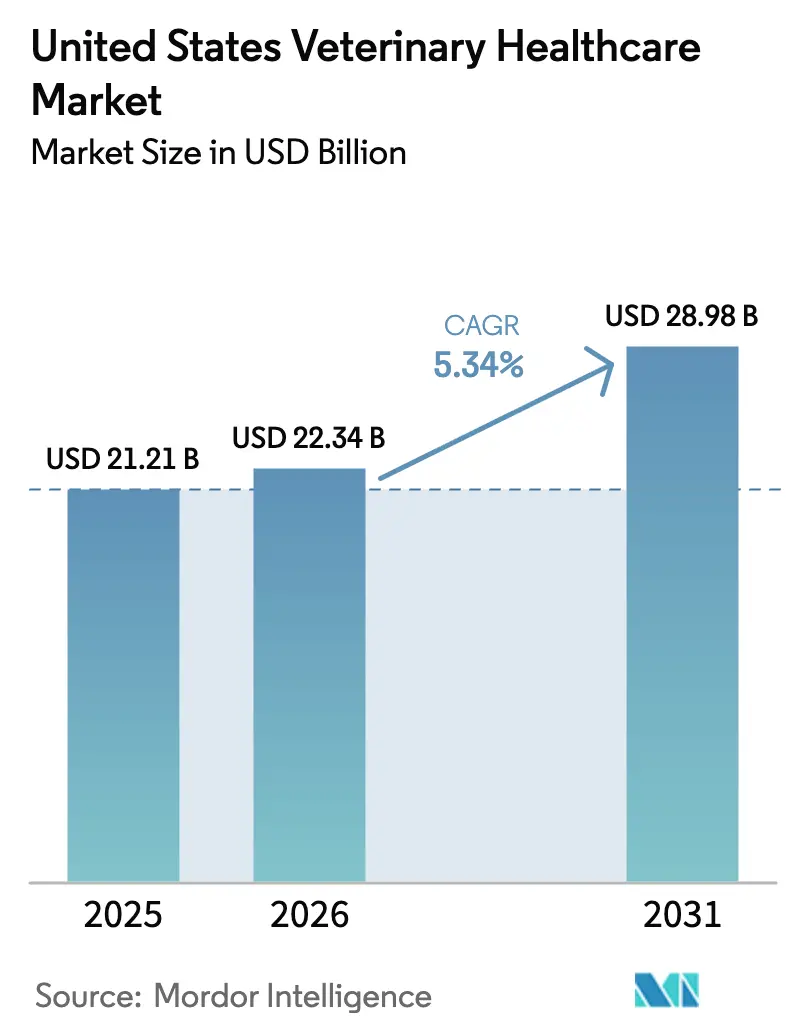

| Base Year Market Size (2025) | USD 21.21 Billion |

| Market Size (2026) | USD 22.34 Billion |

| Market Size (2031) | USD 28.98 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

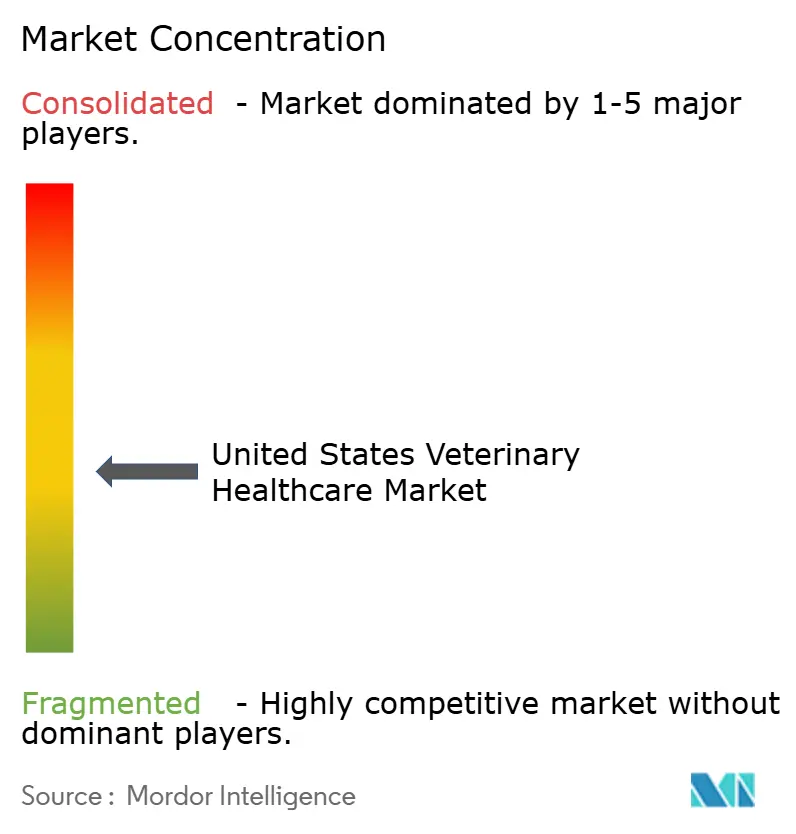

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Veterinary Healthcare Market Analysis by Mordor Intelligence

The United States veterinary healthcare market size is projected to expand from USD 21.21 billion in 2025 and USD 22.34 billion in 2026 to USD 28.98 billion by 2031, registering a CAGR of 5.34% between 2026 to 2031. Growth rides on rising pet humanization, productivity pressures in large-scale livestock operations, and a regulatory environment that favors fast-track pathways for innovative therapeutics and diagnostics. Companion-animal owners increasingly accept prices that mirror human healthcare as they seek chronic-disease management, while livestock producers focus on feed-conversion efficiency and zoonotic-risk reduction. The 2024 restructuring of the FDA Center for Veterinary Medicine into discrete companion- and production-animal divisions tightens this focus by aligning review standards with each sub-market’s economic logic. Competitive advantage hinges on ecosystem lock-in: platform strategies that bind hardware, software, and reference-lab services drive recurring revenue, and artificial intelligence (AI) tools embedded in imaging and molecular platforms narrow the diagnostic gap between primary-care practitioners and specialists. Workforce shortages, biologics supply vulnerabilities, and elongated approval timelines temper growth but also amplify returns for firms able to navigate these hurdles.

Key Report Takeaways

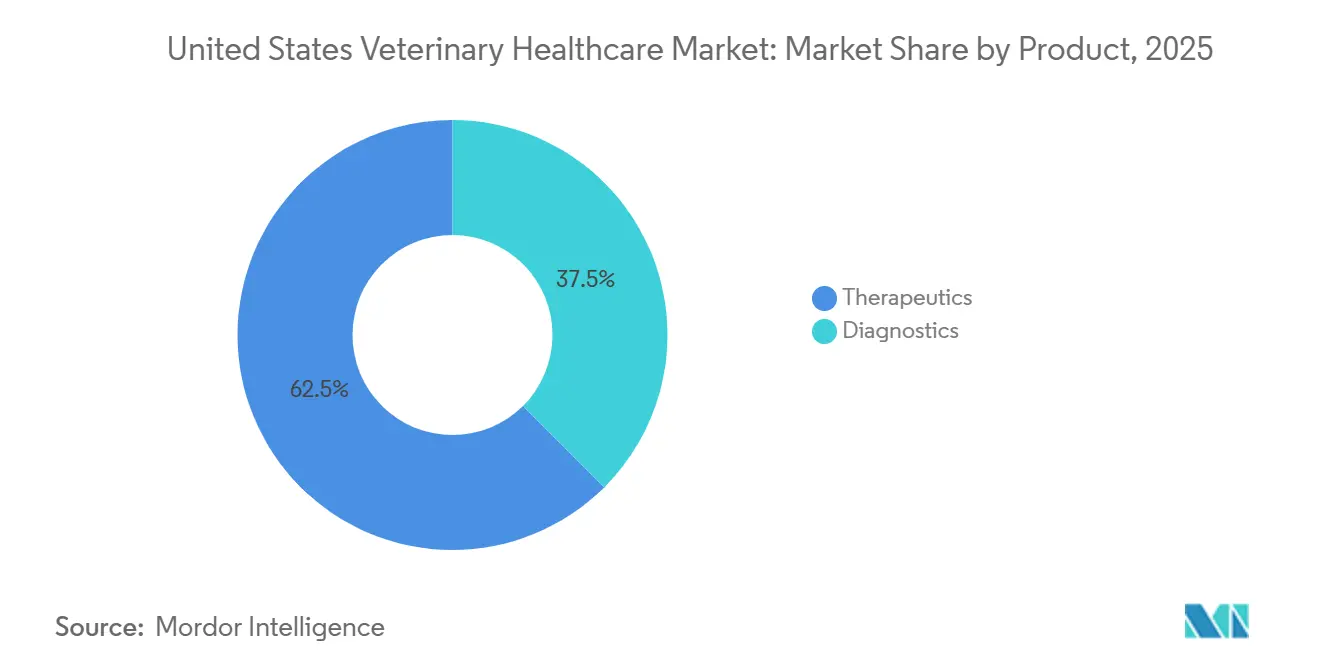

- By product, therapeutics held 62.46% of United States veterinary healthcare market share in 2025, while diagnostics are on track for the fastest 6.76% CAGR through 2031.

- By animal type, dogs and cats contributed 49.26% of 2025 revenue, whereas poultry is forecast to advance at a 6.67% CAGR to 2031, reflecting biosecurity investment after 2024 HPAI outbreaks.

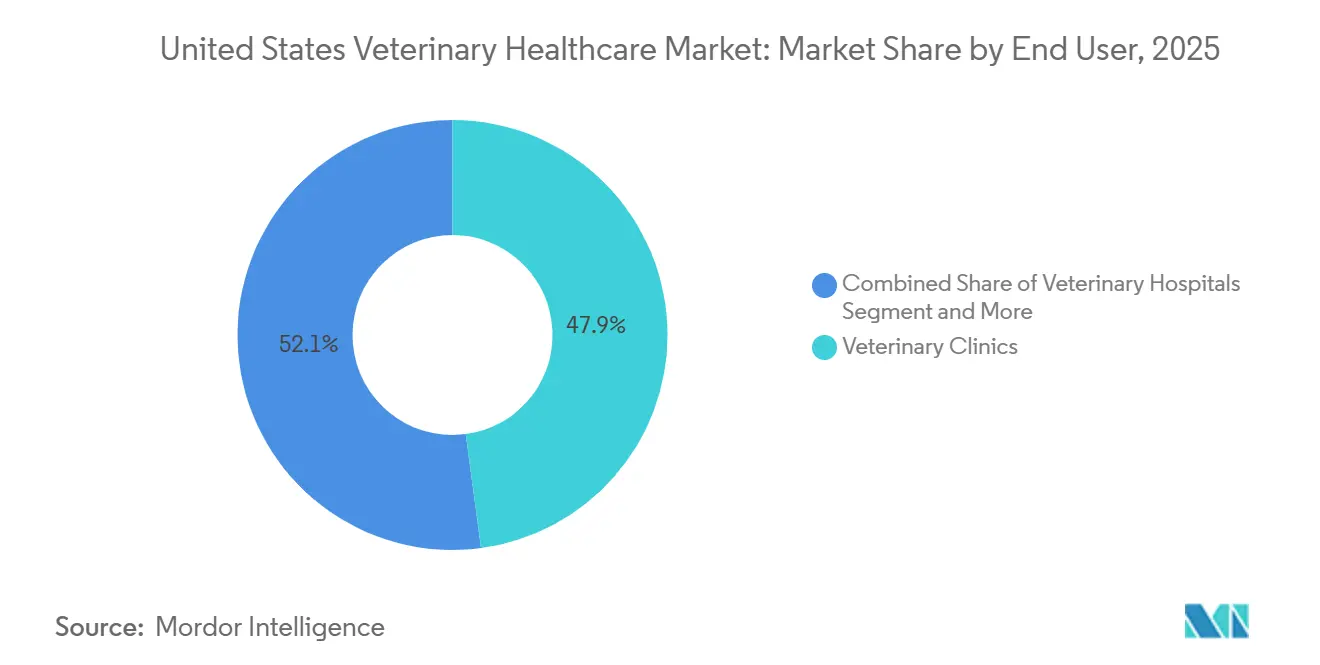

- By end user, veterinary clinics captured 47.89% share in 2025, yet reference laboratories are poised for a 6.81% CAGR through 2031, supported by consolidation and next-generation sequencing roll-outs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Veterinary Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pet ownership & expenditure | +1.2% | National, with concentration in urban metros and suburban clusters | Medium term (2-4 years) |

| Advanced technology & innovation in animal healthcare | +1.5% | National, with early adoption in specialty referral centers and academic veterinary hospitals | Long term (≥ 4 years) |

| Government & animal-welfare initiatives | +0.6% | National, with targeted programs in underserved rural regions | Medium term (2-4 years) |

| Productivity pressures increasing zoonotic risk | +0.8% | National, with acute focus in Midwest livestock corridors and poultry-dense Southeast | Short term (≤ 2 years) |

| AI-driven predictive diagnostics adoption | +0.9% | National, with rapid uptake in corporate veterinary chains and reference laboratories | Medium term (2-4 years) |

| Gene-edited therapeutics pipeline momentum | +0.4% | National, pending FDA regulatory clarity and commercial-scale manufacturing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Pet Ownership & Expenditure

American households owned 89.7 million dogs and 73.8 million cats in 2024, spending USD 598 and USD 529 per household respectively on veterinary care, a pattern that normalizes preventive plans and chronic-disease protocols.[3]American Veterinary Medical Association, “U.S. Pet Ownership Statistics,” AVMA.org Limited pet-insurance penetration below 5% leaves most owners paying out of pocket, yet millennials and Gen Z increasingly regard pets as family members, sustaining demand for oncology, cardiology, and orthopedic services. Digital-first engagement preferences fuel telemedicine sign-ups and at-home monitoring adoption, broadening the care continuum beyond episodic clinic visits. The willingness to finance high-acuity interventions lifts average transaction values and offsets pricing elasticity concerns. These trends collectively support premium diagnostic and biologic uptake even when macroeconomic conditions tighten.

Advanced Technology & Innovation in Animal Healthcare

The FDA’s January 2025 approval of Librela, the first monoclonal antibody for canine osteoarthritis, validated a biologics pathway and created repeat-visit revenue models for clinics equipped with cold-chain storage. Point-of-care molecular tests now deliver PCR-grade sensitivity in under 20 minutes, allowing same-visit therapeutic starts and reducing abandonment. IDEXX’s Inovu DX embeds AI trained on 4 million radiographs, lowering diagnostic error rates in general practice and reinforcing platform lock-in. Gene-edited PRRS-resistant pigs signal similar innovation for production animals, although widespread adoption awaits trade and consumer-acceptance resolution. Taken together, these advances compress diagnostic windows, elevate standard-of-care expectations, and expand addressable revenue per visit.

Government & Animal-Welfare Initiatives

Priority Zoonotic Animal Drug designations enacted in 2024 shorten review timelines for cross-species pathogen solutions, reducing development risk for smaller biotech firms. USDA’s National Animal Health Monitoring System now integrates real-time genomic sequencing, supporting predictive modeling that guides vaccine strain updates months ahead of traditional surveillance. Twelve states relaxed telemedicine restrictions in 2024, enabling veterinarians to form client-patient relationships by video visit, which expands access in rural areas. These policy shifts collectively decrease geographic care disparities, catalyze data-driven product development, and attract venture funding for niche therapeutics.

Productivity Pressures Increasing Zoonotic Risk

Concentrated animal feeding operations house 95% of poultry and 80% of swine, magnifying the economic fallout from outbreaks such as the 2024 HPAI episode that forced depopulation of 17 million birds. Integrators now embed predictive analytics and automated environmental sensors to detect subtle behavioral changes before clinical signs emerge. Elanco’s 2024 acquisition of a microbiome analytics platform illustrates the pivot toward precision livestock management where interventions target specific herd profiles. Producers show rising willingness to purchase rapid diagnostics and vaccines that safeguard throughput and contract fulfillment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High costs of veterinary testing & treatment | -0.9% | National, with acute affordability constraints in rural and lower-income urban areas | Short term (≤ 2 years) |

| Stringent regulatory approval timelines | -0.5% | National, affecting all product categories but disproportionately impacting small-molecule generics | Medium term (2-4 years) |

| Veterinary workforce shortage | -0.7% | National, with critical gaps in rural regions and production-animal specialties | Long term (≥ 4 years) |

| Biologics-input supply-chain vulnerabilities | -0.3% | National, with dependencies on European adjuvant suppliers and Asian API manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Costs of Veterinary Testing & Treatment

The Consumer Price Index for veterinary services rose 10% yearly from 2020 to 2024, far outpacing general inflation, driving emergency visit bills to USD 1,500-3,000 and MRI scans to USD 2,000-3,500. Only 4.4% of U.S. pets had insurance in 2024, forcing owners to finance care via credit products that charge interest rates above 20%, which causes deferred or foregone treatments. This affordability ceiling suppresses volume growth, particularly in chronic disease where lifetime costs accumulate. Rural and low-income populations seek telehealth or online pharmacies as substitutes, eroding full-service clinic revenue in those areas.

Stringent Regulatory Approval Timelines

Full reviews run 18 months for novel molecules and 12 months for generics, extending to 24 months when food-safety data packages are complex. Conditional approvals trim six months but add USD 2-5 million in postmarket study costs, burdening startups without diversified cashflow. These timelines create windows for competitors to leapfrog with next-generation molecules, discouraging small sponsors from filing unless patents are exceptionally strong.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Diagnostics Outpace Therapeutics Growth

Diagnostics revenue is projected to climb at a 6.76% CAGR through 2031, surpassing therapeutics and lifting the United States veterinary healthcare market size for this segment to USD 11.2 billion by the end of the forecast period. Therapeutics retained a 62.46% share in 2025, but information-rich point-of-care assays now compress diagnostic cycles to minutes, compelling practices to preface treatment with evidence rather than empirical protocols. The United States veterinary healthcare market share advantage for therapeutics is therefore narrowing as diagnostics command a larger share of the clinical workflow.

Vaccines and parasiticides dominate companion-animal spending, while feed additives and anti-infectives drive production-animal uptake. Zoetis’s Simparica Trio reduced owner pill burden and captured incremental share, whereas monoclonal antibodies such as Librela inaugurate recurring injection models. Catalyst One and ProCyte One analyzers yield full blood work within 10 minutes, delivering lab-grade accuracy chairside. As AI augments imaging reads, general practitioners confidently perform advanced diagnostics without specialist referrals, deepening in-house revenue capture and cementing platform loyalty.

By Animal Type: Companion Animals Lead as Poultry Accelerates

Dogs and cats delivered 49.26% of 2025 revenue, anchoring the United States veterinary healthcare market size for companion animals at USD 11.0 billion. Poultry, though smaller in absolute terms, is projected for a 6.67% CAGR, the swiftest among livestock groups, driven by biosecurity investments that defend integrated supply chains against HPAI shocks. The United States veterinary healthcare market share for poultry therapeutics and diagnostics will therefore expand by more than 100 basis points by 2031.

Companion-animal owners fund advanced oncology, orthopedic, and cardiology services that parallel human care pathways. In poultry and swine, vertical integrators deploy predictive analytics and rapid diagnostics to safeguard throughput. Gene-edited pigs resistant to PRRS await commercialization once trade barriers resolve, while ruminant segments adapt to antimicrobial-use restrictions that elevate veterinarian oversight and shift purchasing authority. Equine spending concentrates in performance horses where regenerative therapies command price premiums despite limited clinical evidence.

By End User: Reference Laboratories Capture Growth

Reference laboratories are on track for a 6.81% CAGR to 2031, elevating their portion of United States veterinary healthcare market revenue as centralized platforms amortize high-throughput sequencing and mass spectrometry across millions of tests. Veterinary clinics still hold 47.89% share as of 2025, but capacity constraints in imaging and molecular tests push complex cases to labs that guarantee sensitivity and specificity levels unattainable in-house.

Corporate chains funnel samples to captive labs, tightening lock-in while small independent clinics leverage subscription models that bundle equipment leases with reagent contracts. Livestock producers buy through integrator contracts prioritizing cost per pound gained, encouraging pharmaceutical firms to append consulting and data-analytics services to product bids. Home-care and tele-veterinary users emerged after 2024 regulatory relaxations allowed remote prescribing, with Chewy’s subscription model undercutting traditional advice channels and widening the market’s digital front door.

Geography Analysis

The southern United States hosts dense poultry and swine operations that amplify disease-spread risk and spur early adoption of on-farm diagnostics and biosecurity hardware, positioning the region as the growth engine for the United States veterinary healthcare market. Midwestern corridors where beef and dairy cattle dominate exhibit steady demand tied to Veterinary Feed Directive compliance, driving purchases of antimicrobial alternatives and herd-health analytics. The Northeast and West Coast record the nation’s highest per-pet household spending, underpinned by affluent urban centers where pet health mirrors human wellness trends.

Corporate veterinary chains concentrate clinics in coastal metros, funneling high volumes of samples to centralized labs and accelerating AI algorithm refinement. Rural western states face acute workforce shortages that curb service penetration despite sizable livestock inventories. Telemedicine adoption partially bridges this gap, but connectivity barriers persist in sparsely populated counties. The presence of major veterinary schools in the Midwest fosters translational research partnerships that pilot novel gene-edited livestock and precision dairy platforms. Climate variability in the Southwest influences vector-borne disease patterns, increasing demand for year-round parasiticides.

Regulatory initiatives such as state-level telehealth legislation diffuse fastest in western states with vast catchment areas, driving experimentation in hybrid care models. Federal surveillance efforts headquartered in Iowa and Georgia channel funding toward local contract laboratories, seeding new reference capacities that later scale nationally. Across regions, pet insurance enrollment rises fastest in metros with large millennial populations, reflecting digital-first product distribution and employer-sponsored benefit adoption. Collectively, these regional dynamics diversify revenue drivers while sustaining the unified growth trajectory of the United States veterinary healthcare market.

Competitive Landscape

Zoetis remains the largest single player, leveraging cross-category bundling to deepen account penetration, while IDEXX dominates diagnostics with a 60% stake anchored in its integrated hardware-software-lab ecosystem. Boehringer Ingelheim amplifies parasiticide production capacity with a USD 150 million Georgia plant expansion that fortifies supply security. Elanco’s microbiome analytics acquisition reinforces a pivot toward precision livestock offerings that embed data services into product packages.

Platform lock-in rather than price competition defines strategic positioning. IDEXX’s AI interpretation tools prompt automatic treatment pathways that incline clinicians toward its reagents. Zoetis extends its Petcare Rewards program to rebate diagnostics when paired with Simparica Trio, elevating lifetime customer value and thwarting generic encroachment. Mars Veterinary Health integrates Banfield clinics with Antech labs, capturing margin at multiple value-chain nodes and standardizing practice protocols across 3,000 locations.

Disruptors arise from adjacent segments. Pumpkin Insurance complements policies with embedded virtual visits, vertically integrating risk management and care delivery. Chewy’s telehealth subscription commoditizes basic consultations, siphoning low-complexity cases from brick-and-mortar clinics. Patent cliffs looming for blockbuster parasiticides between 2027 and 2029 may compress margins for incumbents, redirecting R&D spend toward biologics and gene therapies with durable exclusivity. Start-ups targeting niche segments such as aquaculture therapeutics exploit regulatory pathways left unserved by large firms, fragmenting the market at the edges while core categories remain consolidated.

United States Veterinary Healthcare Industry Leaders

Elanco Animal Health

Merck & Co. Inc.

Idexx Laboratories

Zoetis, Inc.

Boehringer Ingelheim International GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Zoetis received FDA approval for Librela, the first monoclonal antibody therapy for canine osteoarthritis pain, inaugurating a monthly injection model for companion-animal biologics.

- October 2024: The FDA reorganized its Center for Veterinary Medicine into separate companion- and production-animal divisions to streamline review processes.

- September 2024: IDEXX launched Inovu DX, an imaging platform that marries radiography hardware with AI interpretation trained on 4 million images.

- August 2024: Elanco acquired Prevtec Microbia’s microbiome analytics platform, bolstering precision livestock offerings.

United States Veterinary Healthcare Market Report Scope

As per the scope of the report, veterinary healthcare can be defined as the science associated with the diagnosis, treatment, and prevention of diseases in animals. The veterinary healthcare market comprises therapeutic and diagnostic products and solutions for companion and farm animals. Companion animals can be tamed or adopted for companionship or as house/office guards, and farm animals are raised for meat and milk-related products. Companion animals include canines, felines, and equines. Farm animals include bovine, poultry, and porcine. The United States Veterinary Healthcare Market is segmented by Product (Therapeutics and Diagnostics), Animal Type (Dogs and Cats, Horses, Ruminants, Swine, Poultry, and Other Animals). The report offers the value (in USD million) for the above segments.

By Product

| Therapeutics | Vaccines |

| Parasiticides | |

| Anti-infectives | |

| Medical Feed Additives | |

| Other Therapeutics | |

| Diagnostics | Immunodiagnostic Tests |

| Molecular Diagnostics | |

| Diagnostic Imaging | |

| Clinical Chemistry | |

| Other Diagnostics |

By Animal Type

| Dogs and Cats |

| Horses |

| Ruminants |

| Swine |

| Poultry |

| Other Animals |

By End User

| Veterinary Clinics |

| Veterinary Hospitals |

| Reference Laboratories |

| Livestock Producers |

| Home-care / Tele-veterinary Users |

| Others |

| By Product | Therapeutics | Vaccines |

| Parasiticides | ||

| Anti-infectives | ||

| Medical Feed Additives | ||

| Other Therapeutics | ||

| Diagnostics | Immunodiagnostic Tests | |

| Molecular Diagnostics | ||

| Diagnostic Imaging | ||

| Clinical Chemistry | ||

| Other Diagnostics | ||

| By Animal Type | Dogs and Cats | |

| Horses | ||

| Ruminants | ||

| Swine | ||

| Poultry | ||

| Other Animals | ||

| By End User | Veterinary Clinics | |

| Veterinary Hospitals | ||

| Reference Laboratories | ||

| Livestock Producers | ||

| Home-care / Tele-veterinary Users | ||

| Others | ||

Key Questions Answered in the Report

What is the current valuation of the United States veterinary healthcare market?

The market is valued at USD 22.34 billion in 2026, with forecasts pointing to USD 28.98 billion by 2031.

How fast is the market expected to grow through 2031?

It is projected to register a 5.34% CAGR through the forecast period.

Which product category shows the fastest growth?

Diagnostics are set to grow at a 6.76% CAGR, outpacing therapeutics.

Why is poultry the fastest-growing animal segment?

Biosecurity investments after the 2024 HPAI outbreaks are driving poultry to a 6.67% CAGR.

Which end-user segment is gaining share fastest?

Reference laboratories will expand at a 6.81% CAGR thanks to centralized high-throughput testing.

What key restraint could limit market expansion?

Rising treatment costs, which outpace general inflation, could dampen demand, especially in lower-income areas.

Page last updated on: