Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

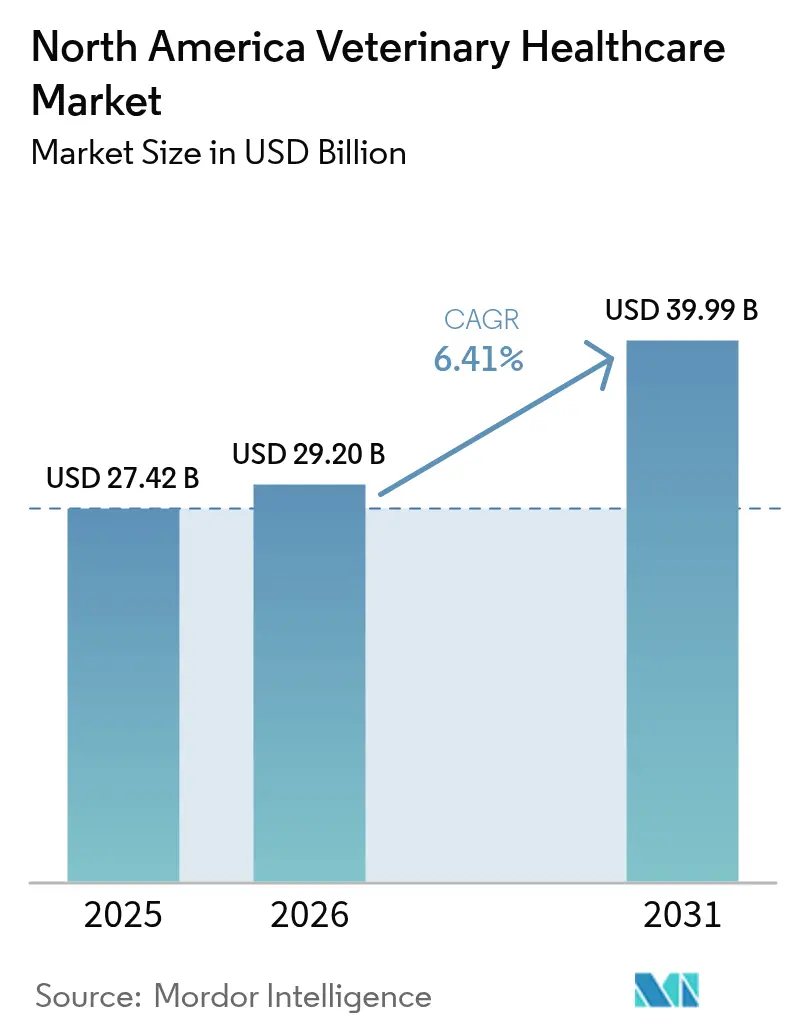

| Base Year Market Size (2025) | USD 27.42 Billion |

| Market Size (2026) | USD 29.20 Billion |

| Market Size (2031) | USD 39.99 Billion |

| Growth Rate (2026 - 2031) | 6.41% CAGR |

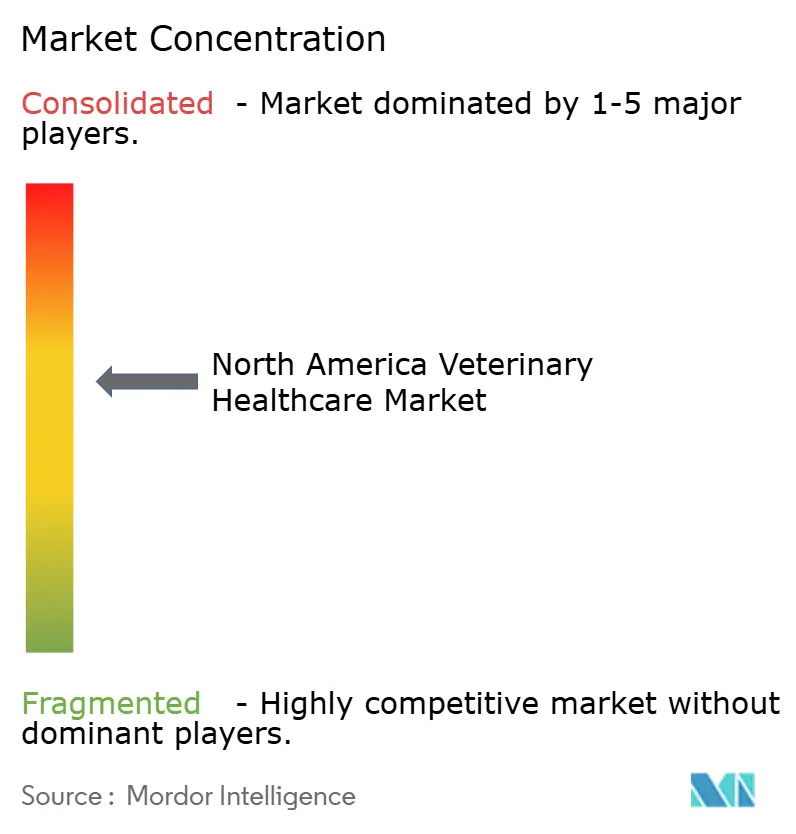

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Veterinary Healthcare Market Analysis by Mordor Intelligence

The North America Veterinary Healthcare Market size is projected to expand from USD 27.42 billion in 2025 and USD 29.20 billion in 2026 to USD 39.99 billion by 2031, registering a CAGR of 6.41% between 2026 to 2031.

Corporate consolidation is shifting pricing power toward a handful of hospital chains, while point-of-care (POC) diagnostics are decentralizing routine testing away from reference laboratories, squeezing incumbent margins while opening avenues for equipment-driven recurring revenues. Rising pet insurance uptake is broadening demand for higher-acuity procedures, though affordability gaps persist for uninsured households, which still dominate the population. Therapeutic innovation, particularly monoclonal antibodies such as Zoetis’ Librela, continues to blur the line between human and veterinary standards of care, creating premium niches that support above-average margins. At the same time, regulators are tightening antimicrobial stewardship rules, channeling R&D toward alternatives such as probiotics, phage therapy, and vaccine platforms.

Key Report Takeaways

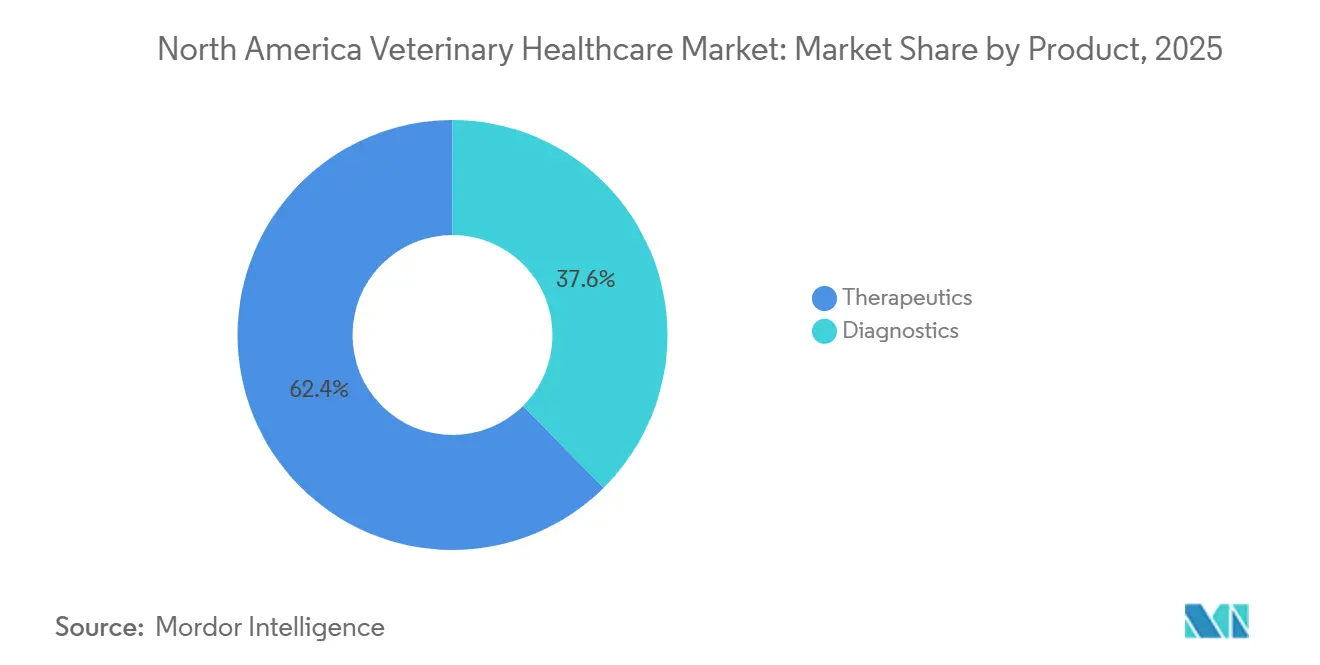

- By product, therapeutics accounted for 62.43% of the North America veterinary healthcare market share in 2025, whereas diagnostics are forecast to advance at a 6.43% CAGR through 2031.

- By animal type, dogs and cats accounted for 45.78% of revenue in 2025; poultry is projected to record the fastest growth at a 6.66% CAGR through 2031.

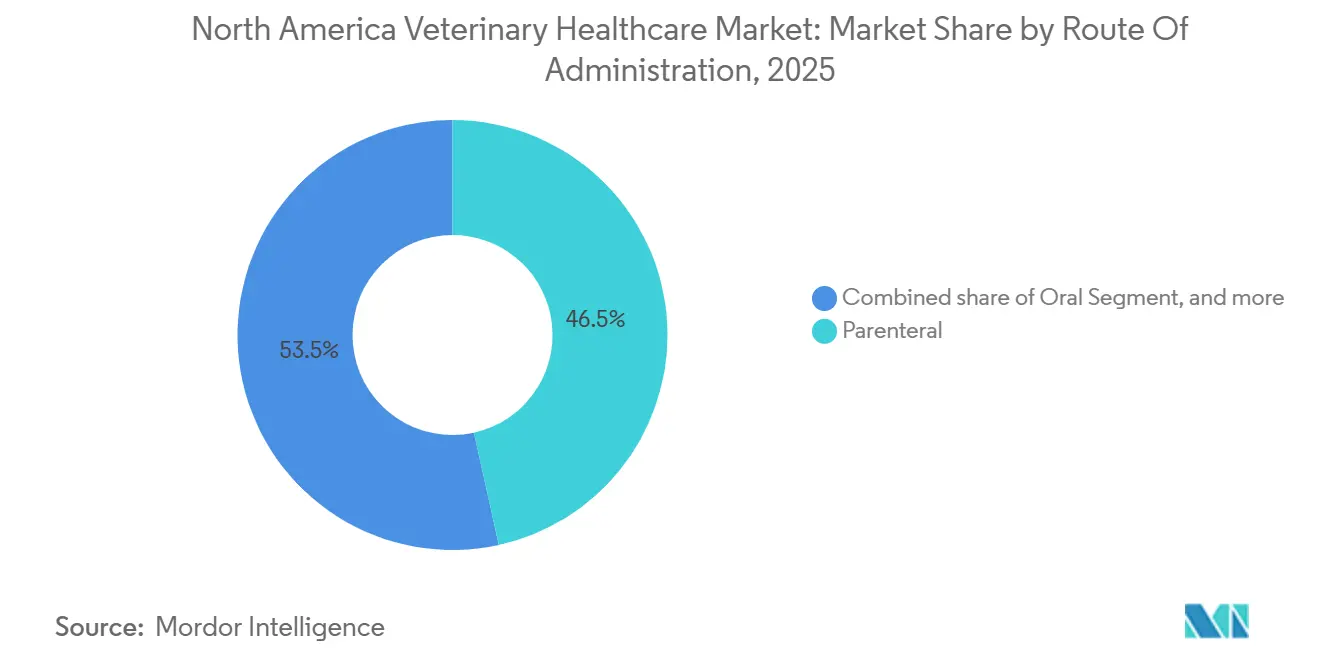

- By route of administration, parenteral formulations led with 46.54% of the North American veterinary healthcare market in 2025, while oral formulations are expected to expand at a 6.12% CAGR over 2026-2031.

- By end user, veterinary hospitals and clinics captured 58.65% of the revenue share in 2025; POC and in-house testing settings are set to grow at a 7.12% CAGR to 2031.

- By geography, the United States accounted for 78.54% of 2025 revenue, whereas Mexico is forecast to post the highest growth rate at a 7.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Veterinary Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in Companion Animal Ownership | +1.2% | United States, Canada, Mexico | Medium term (2-4 years) |

| Increasing Pet Healthcare Expenditure | +1.5% | United States, Canada | Short term (≤ 2 years) |

| Advancements in Veterinary Diagnostics and Therapeutics | +1.8% | Global, led by North America | Long term (≥ 4 years) |

| Rising Adoption of Pet Insurance | +0.9% | United States, Canada | Medium term (2-4 years) |

| Expansion of Corporate Veterinary Chains | +1.3% | United States, Canada | Short term (≤ 2 years) |

| Supportive Government Animal Health Policies | +0.7% | Region-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Companion Animal Ownership

Pet-owning households continue to climb, reaching 70 million in the United States in 2024 and 7.9 million in Canada, with Mexico showing 70% household penetration[1]American Veterinary Medical Association, “Pet Ownership Statistics 2025,” avma.org. Younger owners increasingly adopt multiple pets at once, compressing routine-care cycles and straining under-staffed clinics. This intensifies demand for efficiency-enhancing POC diagnostics that deliver results during the same visit. Scheduling backlogs, particularly for wellness appointments, are steering corporate groups to extend weekend hours and to offer teletriage options that direct non-urgent cases to virtual platforms.

Increasing Pet Healthcare Expenditure

U.S. veterinary-care outlays grew from USD 39.8 billion in 2024 to USD 41.4 billion in 2025, while Canada allocated CAD 2.1 billion to veterinary services in 2023. Corporate groups segment offerings into tiered wellness packages versus high-acuity specialties, capturing both price-sensitive and premium spend without cannibalization. Although pet insurance premiums reached USD 4.7 billion in 2024, 94% of veterinarians still cite cost as a barrier to recommended care, signaling that coverage skews toward affluent clients[2]North American Pet Health Insurance Association, “2025 Industry Report,” naphia.org.

Advancements in Veterinary Diagnostics and Therapeutics

POC hematology analyzers such as IDEXX ProCyte One and Heska Element HT5 now deliver CBCs in minutes, eliminating three-day laboratory waits. Next-generation sequencing panels frequently identify actionable mutations in 90% of canine and feline oncology specimens, accelerating the uptake of targeted therapy. Therapeutic pipelines are likewise advancing; FDA approval of Zoetis’ Librela in 2025 marked the first monoclonal antibody to modify the progression of canine osteoarthritis. Multi-agent oral parasiticides, such as Elanco’s Credelio Quattro, address owner compliance by replacing multi-product regimens with single chewables.

Rising Adoption of Pet Insurance

Policies covered 6.3 million U.S. pets in 2024, yet penetration remains under 7%. Insured clients approve higher-margin imaging, oncology, and surgical cases at greater rates, shifting clinic case-mix toward revenue-dense procedures. However, coverage continues to cluster in suburban and urban regions; rural areas lag due to lower average income and limited insurer marketing.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Veterinary Professionals | -1.1% | United States, Canada, Mexico | Long term (≥ 4 years) |

| High Cost of Advanced Veterinary Care | -0.8% | Region-wide | Medium term (2-4 years) |

| Stringent Regulatory Compliance Requirements | -0.5% | United States (FDA-CVM), Canada (VDD), Mexico (SENASICA) | Short term (≤ 2 years) |

| Concerns Over Antimicrobial Resistance | -0.4% | North America livestock and companion-animal sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Veterinary Professionals

The AVMA projects a 15,000-veterinarian deficit by 2030, while Canada anticipates a 1,500-practitioner shortfall. Debt-to-income imbalance discourages graduates from rural practice ownership, concentrating talent in urban centers and raising wait times for elective care. Corporate consolidators are bidding up salaries with sign-on bonuses and loan-repayment packages, but the measures mostly re-shuffle existing clinicians rather than expand total supply. Burnout, driven by moral distress and long hours, further erodes retention.

High Cost of Advanced Veterinary Care

Emergency visits average USD 1,000-2,000 in the United States, while specialty oncology consults can exceed USD 5,000. Insurance scarcity leaves owners to self-fund high-ticket procedures, producing case deferrals that undermine clinic profitability. In Mexico, annual dog maintenance runs 15,000-35,000 MXN (USD 800-1,900), with inflation at 8.15% as of September 2025, intensifying price sensitivity. Low-cost entrants such as Farmacias Similares’ SimiPet Care demonstrate that sub-USD 10 consultations can unlock latent demand when traditional fees exceed household budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Diagnostics Gain Share as Therapeutics Plateau

Diagnostics revenue is poised to climb at a 6.43% CAGR, eclipsing therapeutic growth as practices embrace in-clinic molecular platforms that accelerate decision-making and generate consumable pull-through. SNAP immunoassays for heartworm and tick-borne panels are now featured in 80% of U.S. wellness visits, anchoring recurring kit sales that bolster the North American veterinary healthcare market for diagnostic consumables. Therapeutics continue to dominate absolute value; however, antimicrobial resistance constraints and heightened regulatory oversight temper volume expansion. Combination parasiticides, such as Simparica Trio and Credelio Quattro, demonstrate that convenience drives owner adherence, mitigating revenue leakage from missed doses. Within vaccines, livestock operators favor multivalent formulations that reduce handling stress, while companion-animal updates now incorporate chimeric technologies for broader strain coverage.

By Animal Type: Companion Animals Dominate, Poultry Drives Growth

Companion animals retain 45.78% revenue in 2025, reflecting entrenched pet-humanization behaviors that propel specialty referrals and chronic-disease management. Nevertheless, poultry health spending will outpace all other categories, expanding at 6.66% CAGR on the back of post-HPAI biosecurity upgrades and stricter export certification rules. Diagnostic laboratories report a surge in avian PCR panels, while vaccine suppliers ramp production to meet flock-wide prophylaxis mandates. Ruminant uptake remains constrained by commodity-price volatility; however, screwworm-related trade disruptions are spurring cattle operators to integrate parasiticides and serology screens to regain U.S. market access.

By Route of Administration: Oral Gains on Compliance

Parenteral products represented 46.54% revenue in 2025, but oral formats are set to climb at 6.12% CAGR through 2031, leveraging owner preference for at-home dosing convenience. Chewable parasiticides and flavored analgesics now command merchandising space at hospital checkout counters, directly boosting pharmacy-front sales. Practices benefit from reduced injection labor, yet the heightened non-compliance risk necessitates follow-up reminder systems to ensure dose completion, safeguard therapeutic outcomes, and minimize resistance development.

By End User: Point-of-Care Disrupts Reference Labs

Veterinary hospitals and clinics continue to anchor demand, yet POC and in-house testing settings will grow fastest at 7.12% CAGR. Analyzers financed via reagent-rental models lower upfront CAPEX, enticing mid-volume practices to internalize chemistry, hematology, and serology workflows. Reference labs respond with a broader menu and courier service guarantees, reserving complex histopathology and endocrinology assays for cases where economies of scale remain decisive. Hybrid testing models—IDEXX’s SDMA kidney biomarker, available both in-house and through labs—offer practices flexibility between turnaround time and breadth.

Geography Analysis

The United States accounted for 78.54% of 2025 revenue, underpinned by USD 41.4 billion in veterinary care spend and USD 4.7 billion in pet insurance premiums. FDA-mandated stewardship of antibiotics rechannels demand toward vaccines and POC pathogen screens, while workforce shortages elevate clinician salaries and incentivize telemedicine adoption for triaging routine follow-ups.

Canada’s share trails at roughly 14%, yet household pet ownership at 58% fuels steady clinic traffic, and CAD 2.1 billion in veterinary services underscores the country’s alignment with U.S. care standards[3]. Veterinary school capacity constraints and an aging practitioner base sustain vacancy rates, encouraging cross-border recruiting and licensing harmonization initiatives.

Mexico, expanding at 7.21% CAGR, emerges as the fastest-growing geography despite sub-1% insurance penetration. The screwworm-driven cattle export ban sharpened focus on biosecurity compliance, accelerating uptake of parasiticides and lab diagnostics. Farmacias Similares’ rollout of low-cost SimiPet Care clinics—charging 100 MXN for consultations—confirms latent demand among middle-income households that have been historically priced out of premium operators. Multinational investment, exemplified by Mars’ MXN 3,500 million plant expansion, validates the long-term growth thesis.

Regulatory Landscape

North American veterinary healthcare is shaped by drug, biologics, and animal movement and import controls that affect time-to-market and commercialization costs. In the United States, USDA APHIS Center for Veterinary Biologics (CVB) oversees veterinary biologics (including inspection and compliance expectations), while federal import rules (for example, restrictions in 9 CFR Part 94 for animal products) interact with disease-driven trade measures. In June 2026, USDA APHIS issued updated import restrictions for specific avian zones in Alberta and Saskatchewan tied to HPAI, underscoring the operational importance of zone-based compliance for poultry and related diagnostics.

Regulatory processes are also moving toward digital-first submissions and lifecycle oversight. USDA APHIS published NCAH Portal user guides in January 2026 to support veterinary biologics submissions and licensing procedures, and CVB continued publishing updated catalog and organizational materials in April 2026. In Canada, Health Canada implemented a policy-based terms and conditions (T&Cs) approach for veterinary drugs in February 2025 to enable conditional market access for critical therapies, and opened a public consultation in December 2025 on revised draft guidance (concluding February 2026), indicating more structured use of conditional authorization pathways alongside evolving submission requirements.

Value Chain Analysis

The value chain covers discovery and formulation (innovator pharma and specialty biotech), regulated manufacturing and quality control, cold-chain dependent logistics (notably for vaccines and other biologics), wholesale distribution, and dispensing through veterinary hospitals, clinics, and emerging point-of-care and retail-service channels. Large manufacturers such as Zoetis, Elanco, Merck Animal Health, and Boehringer Ingelheim supply a mix of therapeutics and diagnostics that flows through value-added distributors and practice networks, while procurement scale is increasingly concentrated as corporate groups standardize formularies and testing menus across multi-site footprints.

Distribution and channel execution are becoming differentiators as consolidators seek predictable availability and negotiated pricing across thousands of sites. Covetrus renewed its distribution partnership with National Veterinary Associates in January 2024, supporting supply to more than 1,000 NVA hospitals in the United States and illustrating how contracted distribution supports on-shelf continuity for in-clinic products and consumables. Upstream, partnerships such as Elanco and Medgene (February 2025) to commercialize an HPAI vaccine platform for U.S. dairy cattle, and Longhorn Vaccines and Diagnostics with Promega (July 2025) for integrated molecular testing workflows, show how co-development and co-marketing are used to shorten commercialization cycles and expand access to specialized testing and prevention tools. Across the chain, reliance on globally sourced APIs and equipment increases exposure to tariff and transport disruptions, while cold-chain integrity remains a key operational constraint for biologics.

Competitive Landscape

The top five suppliers, Zoetis, Boehringer Ingelheim, Elanco, Merck Animal Health, and IDEXX, control roughly 40-45% of the North American veterinary healthcare market, indicating moderate concentration. Zoetis reported USD 2.36 billion in Q3 2024 revenue, buoyed by the launches of Simparica Trio and Librela, while IDEXX generated USD 968 million, leveraging its 5,000+ lab network and analyzer placements. Mars Veterinary Health’s vertical integration across hospitals, diagnostics (Antech), and nutrition reinforces bargaining leverage over manufacturers. Heska’s Q3 2024 revenue of USD 67.7 million highlights niche growth among mid-tier practices seeking POC differentiation. M&A momentum persists as private-equity-backed consolidators snap up independent clinics, drawing antitrust scrutiny amid owner concerns over fee escalation.

North America Veterinary Healthcare Industry Leaders

Boehringer Ingelheim International GmbH

Merck & Co Inc

Zoetis Inc

Idexx Laboratories

Elanco Animal Health Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are concentrating around three clear whitespace areas: (1) faster diagnosis and workflow automation inside clinics, (2) scalable access models for routine care, and (3) differentiated alternatives to traditional antimicrobials. On the diagnostics side, Zoetis entered an agreement in July 2026 to acquire VitalRADS, a veterinary teleradiology platform, which aligns with the move toward distributed specialist capacity as case volumes rise and clinician time tightens. It also complements the shift toward point-of-care and in-house testing, where analyzer placements support recurring consumables pull-through and reduce dependence on reference laboratory turnaround for routine cases.

Service delivery expansion is also creating openings for suppliers that can support standardized protocols, integrated pharmacy fulfillment, and subscription-like preventive care bundles across large footprints. Tractor Supply Company acquired VIP Petcare from PetIQ in May 2026 to bring mobile in-store veterinary clinic operations in-house, and Bond Vet and Small Door Veterinary finalized a merger in July 2026 to form a network of more than 55 premium clinics, reflecting continued investment in scaled, tech-enabled care models. On the therapeutics side, FDA CVM actions in early 2026, including approvals of first generics (for example, robenacoxib tablets for cats) and emergency authorizations for specific animal health needs, point to a market environment where pricing tiers widen and where rapid-response regulatory mechanisms can accelerate access for high-impact disease events.

Recent Industry Developments

- July 2026: Zoetis entered an agreement to acquire VitalRADS, a veterinary teleradiology platform, to expand AI-assisted diagnostic capabilities. The deal expands clinic access to specialist interpretation for imaging-heavy caseloads and supports workflow automation as point-of-care and in-house diagnostics grow.

- December 2025: Elanco Animal Health received conditional approval from the U.S. FDA for Credelio Quattro-CA1 for the treatment of New World screwworm larvae (myiasis) in dogs. The authorization broadened the companion-animal toolkit for an escalating parasitic threat and reinforced the role of conditional pathways in shortening time-sensitive veterinary therapeutics to market.

- January 2024: Covetrus renewed its strategic distribution partnership with National Veterinary Associates to supply in-clinic products to more than 1,000 NVA hospitals across the United States. The agreement supports centralized procurement and more consistent product availability across a large corporate network, highlighting how distributor execution and inventory reliability affect practice economics.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the North America veterinary healthcare market is defined as spending on animal health therapeutics and diagnostics used by veterinary service providers and animal owners across the United States, Canada, and Mexico.

Scope exclusions: Human healthcare, pet food and treats, grooming and boarding services, and non-medical pet accessories are excluded from this market sizing.

Segmentation Overview

- By Product

- Therapeutics

- Vaccines

- Parasiticides

- Anti-Infectives

- Medical Feed Additives

- Other Therapeutics

- Diagnostics

- Immunodiagnostic Tests

- Molecular Diagnostics

- Diagnostic Imaging

- Clinical Chemistry

- Other Diagnostics

- Therapeutics

- By Animal Type

- Dogs & Cats

- Horses

- Ruminants

- Swine

- Poultry

- Other Animal Types

- By Route Of Administration

- Oral

- Parenteral

- Topical

- Other Routes

- By End User

- Veterinary Hospitals & Clinics

- Reference Laboratories

- Point-Of-Care / In-House Settings

- Academic & Research Institutes

- By Country

- United States

- Canada

- Mexico

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the core fact base for animal populations, disease and parasite prevalence, and the regulatory and trade backdrop that shapes veterinary product demand. We referenced public sources such as USDA and CDC publications, Statistics Canada releases, Mexico health and agriculture statistics, and animal health guidance from bodies such as the WOAH, alongside peer-reviewed veterinary journals that help validate treatment patterns.

On the commercial side, we reviewed public company filings and investor presentations to understand revenue exposure by animal health lines, product launches, and pricing commentary. Where it helped tighten assumptions, we used paid subscriptions for company financials and intelligence, patent databases, and an import and export shipment-level database to sense-check cross-border flows of selected product categories. These desk inputs are not exhaustive, and many other public sources were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with veterinary clinic and hospital decision-makers, distributors, and product-side experts who track therapeutics and diagnostics demand across North America. We used these conversations to confirm what is actually used in day-to-day practice, pressure-test pricing and mix shifts, and close gaps where public statistics do not break out veterinary-specific lines cleanly.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 13% | |

| Mid tier: 42% | Functional/Unit leaders: 36% | |

| Smaller Players: 22% | Managers: 51% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up model, where North America demand was first reconstructed from animal population pools and care intensity, then cross-checked with supplier and channel signals. On the top-down side, we translated treated-animal volumes into value by applying realistic therapy and diagnostic utilization rates, followed by average selling price (ASP) bands that vary by product type and country.

Key inputs that shaped the model included companion versus farm animal population trends, vaccination and parasite prevention adoption, diagnostic testing frequency, clinic visit intensity, and typical pricing progression for therapeutics and imaging-based diagnostics. Where public data was not granular, gaps were handled by using informed ranges from interviews and then calibrating to observable anchors such as reported regional revenue exposure, product mix commentary, and shipment directionality for select categories.

For forecasting, we used scenario analysis supported by a simple multivariate view of the drivers that move spend, especially pet ownership trends, preventive care uptake, and price and mix changes in higher-value diagnostics. Assumptions were reviewed with primary respondents so that growth rates stayed consistent with what clinics and suppliers expect to see in real purchasing cycles.

Data Validation & Update Cycle

Outputs were triangulated across multiple checks so that one data source did not overly influence the final number. We compared implied per-animal spend, product mix splits, and country-level growth patterns against independent signals, then reviewed any sharp jumps that did not match known regulatory, pricing, or disease-cycle explanations.

Before sign-off, the model goes through multi-step internal review, and analysts re-contact sources when a key assumption shifts or when large variances show up across inputs. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery refresh pass so clients receive the most current view.

Mordor Intelligence's North America Veterinary Healthcare Market Market Size Measured Against Other Published Estimates

Published market values for North America veterinary healthcare can look far apart because each study draws the boundary differently and then updates its assumptions on a different timetable. Differences usually come from what is counted as veterinary healthcare (products only versus products plus services), how fast ASPs are allowed to rise, and whether country-level currency timing is handled consistently.

In our refresh-led workflow, price and mix assumptions are rechecked using recent clinic purchasing feedback and public financial disclosures, and currency conversion is aligned to a consistent year convention, which is why the latest estimate in Mordor Intelligence can land below broader scopes that bundle in service revenues or apply more aggressive ASP progression.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 27.42 B (2025) | |

| Regional Consultancy A | USD 37.97 B (2024) | This figure uses an earlier base year and a wider commercial definition that typically includes veterinary service delivery and related spend alongside products, which lifts the total versus a therapeutics-plus-diagnostics scope. |

| Industry Publisher B | USD 11.01 B (2024) | This estimate appears to apply a narrower coverage boundary, likely focusing on selected product categories or a reduced set of end users, which compresses the market when diagnostics and full therapeutic breadth are not fully captured. |

The spread across sources is mainly explained by scope choices and how pricing and currency are timed in the model. By keeping the counted basket tied to measurable product and diagnostic demand, then validating it through repeated checks from clinic-side and supply-side signals, the final number stays traceable to clear inputs and can be updated in a repeatable way as conditions change.

Key Questions Answered in the Report

How large is the North America veterinary healthcare market in value terms?

The market reached USD 27.68 billion in 2025 and is projected to climb to USD 39.99 billion by 2031, growing at a 6.49% CAGR over 2026-2031.

Which product category is expanding fastest?

Diagnostics are forecast to advance at a 6.43% CAGR, outpacing therapeutics as clinics adopt rapid in-house molecular and immunoassay platforms.

What segment of pet owners drives market growth?

Younger households increasingly adopt multiple pets simultaneously, boosting demand for preventive care and compressing the interval between wellness visits.

Why is poultry healthcare spend rising sharply?

Post-outbreak biosecurity mandates and vaccination campaigns are lifting poultry health expenditures at a 6.66% CAGR through 2031.

What is the chief bottleneck facing clinics?

A projected shortage of 15,000 U.S. veterinarians by 2030 is lengthening wait times and constraining elective procedure volumes.

Page last updated on: