Veterinary Monitoring Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

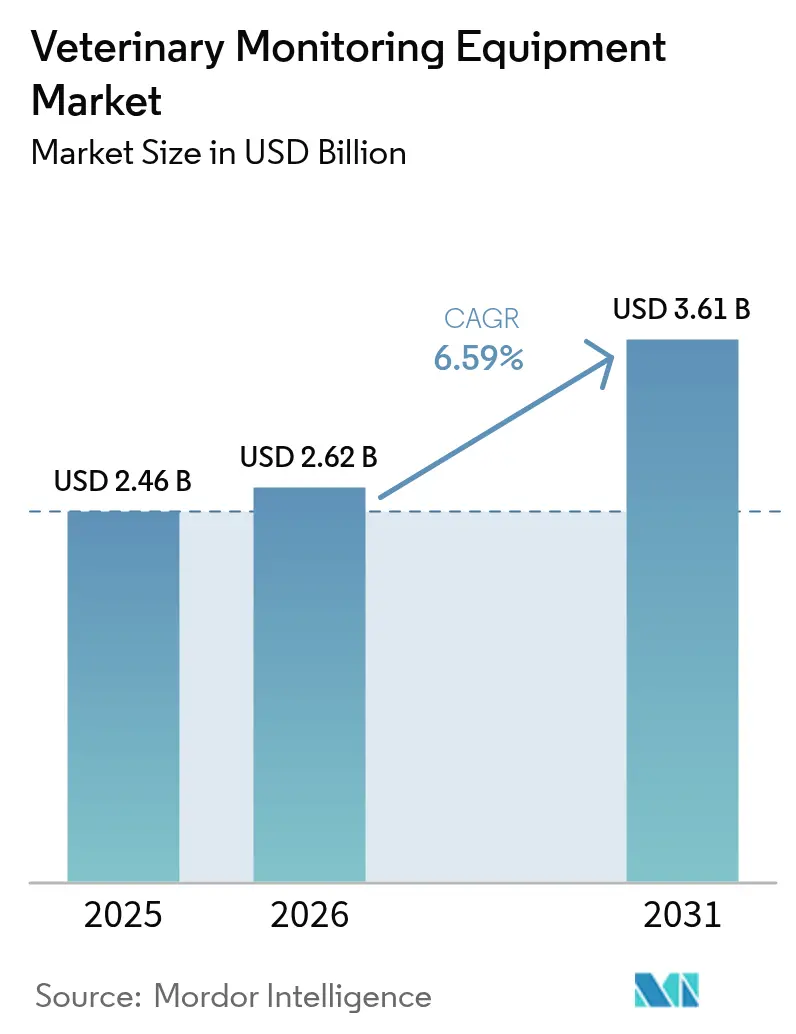

| Market Size (2026) | USD 2.62 Billion |

| Market Size (2031) | USD 3.61 Billion |

| Growth Rate (2026 - 2031) | 6.59% CAGR |

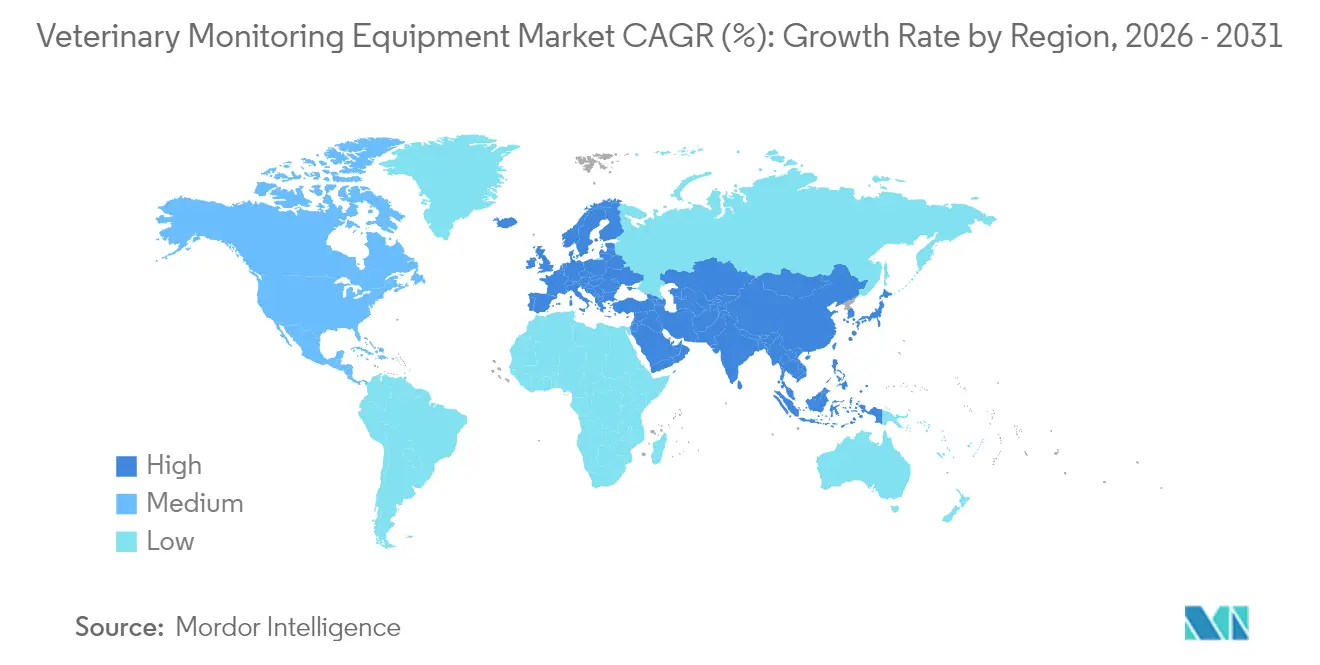

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

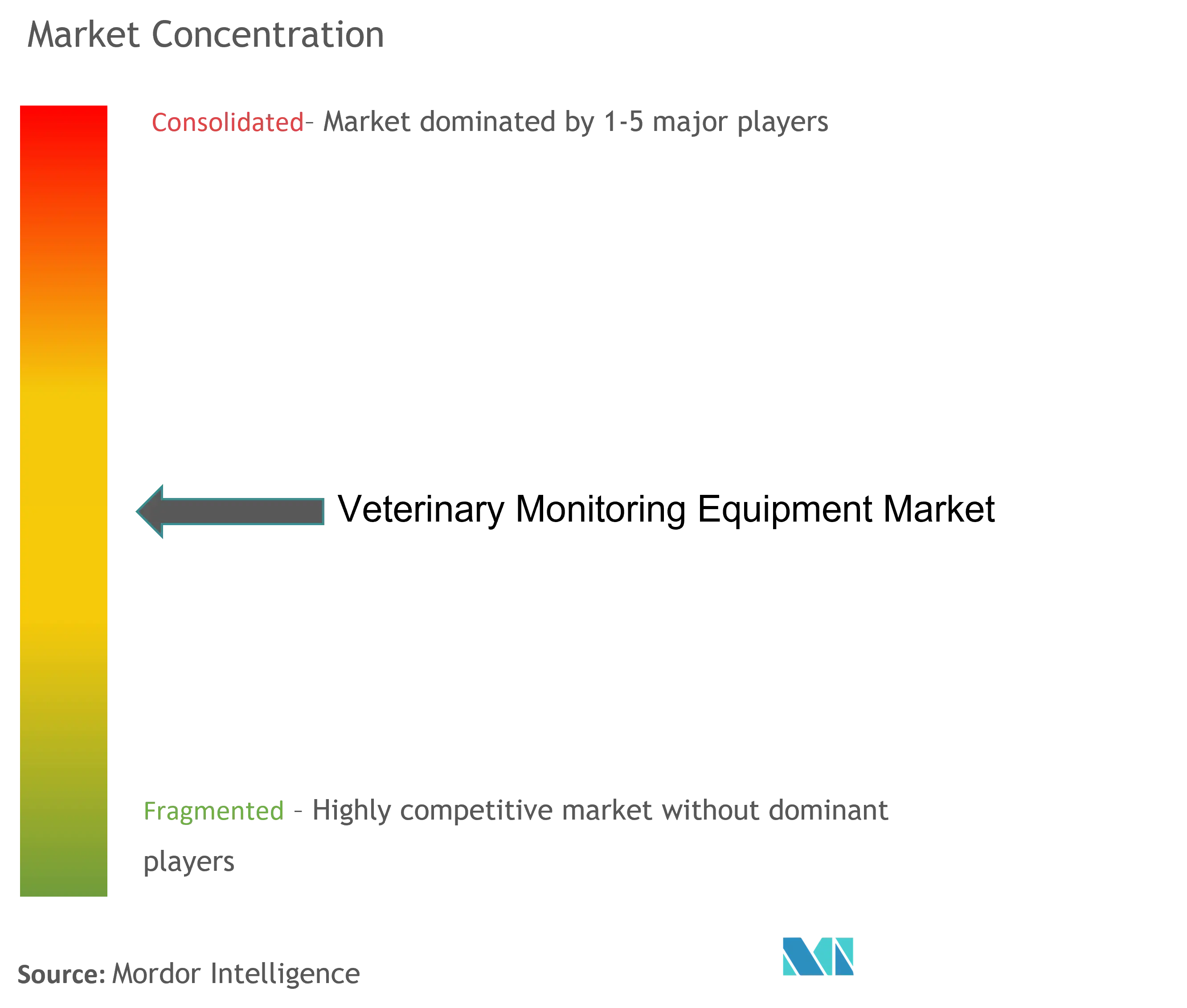

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Monitoring Equipment Market Analysis by Mordor Intelligence

The veterinary monitoring equipment market size is expected to grow from USD 2.46 billion in 2025 to USD 2.62 billion in 2026 and is forecast to reach USD 3.61 billion by 2031 at 6.59% CAGR over 2026-2031. This growth reflects rising pet humanization, livestock productivity targets, and the rapid deployment of AI-enabled diagnostics. Ongoing integration of multi-parameter, wearable, and remote technologies is shifting care from episodic clinic visits toward always-on, data-driven health management. Demand is reinforced by regulatory programs that speed approvals for connected devices and by producers’ need to safeguard food-supply traceability. Competitive intensity remains moderate, yet platform-centric strategies and specialist entrants are redrawing value pools across the veterinary monitoring equipment market.

Key Report Takeaways

- By product type, multi-parameter monitors led with 35.05% of veterinary monitoring equipment market share in 2025, while wearable and remote monitors are projected to expand at a 6.88% CAGR to 2031.

- By animal type, companion animals accounted for 59.10% of the veterinary monitoring equipment market size in 2025; livestock monitoring is forecast to advance at 7.55% CAGR through 2031.

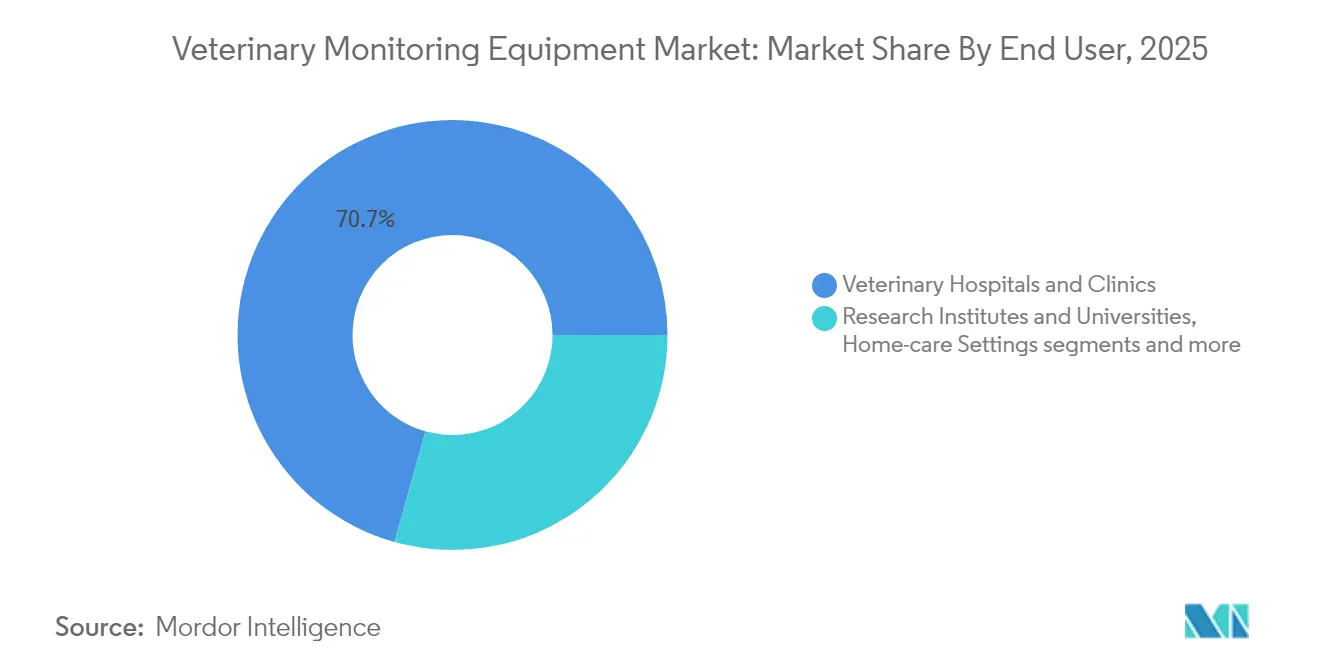

- By end user, veterinary hospitals and clinics held 70.65% revenue share in 2025, whereas the home-care segment is set to grow at 7.84% CAGR to 2031.

- By geography, North America commanded 41.95% of the veterinary monitoring equipment market share in 2025, while APAC is projected to register the fastest 7.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Monitoring Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pet ownership & spending on veterinary care | +1.8% | North America & Europe | Medium term (2-4 years) |

| Increasing prevalence of chronic animal diseases | +1.2% | Developed markets | Long term (≥4 years) |

| Technological advances in multi-parameter & wearable monitors | +2.1% | North America & APAC | Short term (≤2 years) |

| Growth in livestock production & herd-health programs | +0.9% | APAC, Latin America, MEA | Medium term (2-4 years) |

| AI-driven predictive analytics in monitoring devices | +1.4% | North America & Europe, expanding to APAC | Short term (≤2 years) |

| Regulatory push for tele-veterinary remote monitoring | +0.8% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Pet Ownership & Spending on Veterinary Care

Pet owners increasingly view animals as family and demand comprehensive, enabling clinics to position devices as wellness tools rather than episodic diagnostics. Continuous data streams reduce emergency costs and improve life-quality metrics, pushing the veterinary monitoring equipment market toward subscription-based models.

Increasing Prevalence of Chronic Animal Diseases

Diabetes, cardiac disorders, and osteoarthritis now mirror human chronic disease patterns in pets. AI-enabled collars such as PetPace 2.0 track long-term vitals and behavior, giving veterinarians granular trendlines for treatment adjustments. For cattle, early-warning systems lower mortality and feed wastage, creating multi-year device demand within the veterinary monitoring equipment market.

Technological Advances in Multi-Parameter & Wearable Monitors

Compact platforms combine ECG, blood pressure, capnography, and temperature in a single enclosure; SunTech Vet40 exemplifies this shift with ACVIM-validated accuracy. Twenty-five-day battery cycles and kinetic-energy harvesting make continuous monitoring viable for extensive herds, accelerating the veterinary monitoring equipment expansion.

Growth in Livestock Production & Herd-Health Programs

Precision-farming adoption cuts disease-related losses by more than 30% while boosting feed-conversion efficiency. Integrated platforms log environmental and biometric data, satisfying traceability mandates and propelling the veterinary monitoring equipment market in APAC and Latin America.

Restraints Impact Analysis*

| Restarint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced monitoring equipment | -1.6% | Developing markets | Medium term (2-4 years) |

| Limited awareness & adoption in developing regions | -0.8% | MEA, Latin America, rural APAC | Long term (≥4 years) |

| Data-privacy & interoperability concerns | -0.7% | North America & Europe | Short term (≤2 years) |

| Battery-life & durability limits in large-animal wearables | -0.5% | Global livestock operations | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Monitoring Equipment

Practice owners face equipment outlays exceeding USD 50,000 for full multi-parameter platforms and doubling ownership costs once software, maintenance, and training are included. These economics stall penetration across developing economies, tempering near-term growth in the veterinary monitoring equipment market.

Limited Awareness & Adoption in Developing Regions

Fragmented supply chains and limited technical support delay uptake in rural Africa and South Asia, where veterinary infrastructure remains under-resourced [1]Source: Frontiers in Veterinary Science, “Net Economic Benefits to Small-Scale Producers,” frontiersin.org . Device makers must simplify interfaces and leverage community-based animal-health workers to unlock latent demand within the veterinary monitoring equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Multi-Parameter Dominance Faces Wearable Disruption

Multi-parameter systems retained 35.05% veterinary monitoring equipment market share in 2025, owing to their role in anesthesia and critical-care workflows. The segment’s robust clinical validation underpins purchasing, and portable form factors such as the 3-lb LifeWindow One broaden use beyond surgical suites. These platforms now integrate Wi-Fi and cloud dashboards, allowing remote specialists to review waveforms in real time. Procurement remains capital-intensive, yet leasing models and bundled service contracts sustain revenue visibility.

Wearable and remote units are the fastest-growing category at 6.88% CAGR, driving fresh penetration in home-care and extensive-farm settings. AI-driven collars, rumen boluses, and non-contact Doppler devices detect subtle physiological deviations hours before clinical symptoms appear, cutting intervention costs. Embedded telecom modules transmit encrypted data to practice management systems, embedding these devices within preventive-care plans. Battery-life breakthroughs and energy harvesting support multi-year deployment, cementing the segment’s disruptive momentum within the veterinary monitoring equipment market.

By Animal Type: Companion Care Leads While Livestock Accelerates

The veterinary monitoring equipment market size for companion animals reached USD 1.45 billion in 2025. Dogs dominate through smart collars that track cardiac, respiratory, and activity markers. Consumer willingness to pay for preventive insights sustains device subscriptions that generate recurring revenue. Feline solutions are catching up via lightweight tags that overcome cats’ lower wear-tolerance and offer body-temperature, sleep, and activity analytics.

Livestock applications are projected to post 7.55% CAGR, underpinned by dairy, beef, and swine producers’ need to improve feed conversion and lower mortality. Bolus sensors monitor rumen pH and temperature, enabling pre-emptive treatment of bovine respiratory disease. Ear-tag sensors with LoRa connectivity link to cloud dashboards for pen-level analytics, while integrated barn-environment monitors correlate ambient conditions with animal health. Government traceability mandates further standardize sensor usage across the veterinary monitoring equipment market.

By End User: Hospitals Dominate While Home Care Surges

Veterinary hospitals and clinics held 70.65% revenue in 2025, reflecting their central role in surgeries and emergency interventions. Facilities increasingly interface monitors with practice-management software, automating charting and billing and freeing staff for higher-value tasks. Strategic instrument placements by top vendors bolster installed bases and recurring consumables turnover.

Home-care settings are projected to grow at 7.84% CAGR, fueled by pet owner demand for low-stress monitoring and by telemedicine platforms that integrate device feeds into virtual consults. Bluetooth-enabled thermometers and pulse-oximeters that auto-sync with mobile apps simplify owner usage. Veterinarians review data asynchronously, prescribe adjustments, and schedule in-clinic visits only when clinically necessary, embedding remote monitoring as a mainstream service line within the veterinary monitoring equipment market.

Geography Analysis

North America generated 41.95% of 2025 sales, sustained by high pet ownership rates, robust insurance penetration, and streamlined FDA pathways that encourage device launches . Companion-animal spend offsets soft clinical-visit traffic, as reflected in IDEXX’s 7% organic growth and record premium-instrument placements. Canada’s extensive beef and dairy sectors adopt bolus and ear-tag sensors, while Mexico’s emerging middle class fuels companion-animal device uptake.

APAC is forecast to expand at 7.98% CAGR, undergirded by China’s 106.2 billion-yuan pet medical market and rapid livestock modernization. Local manufacturing lowers price points, aiding diffusion across mid-tier clinics and midsize farms. Japan and South Korea advance next-gen sensor R&D, while India’s dairy cooperatives pilot large-scale IoT herd-health systems. Regional governments allocate subsidies for food-safety traceability, reinforcing adoption across the veterinary monitoring equipment market.

Europe exhibits steady uptake, driven by stringent animal-welfare statutes and tele-medicine reimbursements. Germany anchors device manufacturing, the United Kingdom pioneers remote-consult frameworks, and France leverages cloud analytics to streamline dairy herd management. Eastern Europe presents greenfield opportunities as cost-optimized wearables gain traction amongst smallholder farms. Harmonized CE-marking procedures shorten time-to-market relative to other regulated regions.

Regulatory Landscape

Regulation for veterinary monitoring equipment remains jurisdiction-specific. In the United States, oversight for animal devices is mainly handled by the US Food and Drug Administration (FDA) Center for Veterinary Medicine (CVM) under the Federal Food, Drug, and Cosmetic Act, with a focus on misbranding, adulteration, and labeling rather than a formal premarket clearance pathway for animal devices. Quality-system expectations have also tightened for manufacturers that operate in regulated device markets, following the FDA Quality Management System Regulation (QMSR), which became effective on February 2, 2026 and aligns quality management with ISO 13485:2016.

In Europe, veterinary medicinal products operate under a harmonized regime (Regulation (EU) 2019/6, administered through the European Medicines Agency framework), while veterinary medical devices do not have a single EU-wide device framework. This creates compliance fragmentation across member states. Separately, the European Commission updated the harmonized standards environment for medical electrical equipment and biological evaluation through Commission Implementing Decision (EU) 2026/1231 dated June 11, 2026, which influences technical conformity expectations for monitor platforms derived from human medical device standards. In other regions, national requirements continue to evolve, including South Africa, where SAHPRA issued a 2025-2026 regulatory requirements document for veterinary medical devices, reinforcing documentation and compliance readiness for suppliers operating across multiple territories.

Value Chain Analysis

The value chain starts with sensor and electronics component suppliers, including boards, batteries, displays, cables, and medical-grade plastics. It then moves through device design, software and algorithm development, verification and validation, and quality and regulatory documentation before final assembly and test. Manufacturing is carried out either through in-house plants or specialized contract manufacturing partners, followed by configuration, packaging, and post-sale service infrastructure that supports calibration, repairs, and software updates, particularly for multi-parameter monitors and connected wearable systems.

Downstream distribution is led by veterinary-focused channels that combine equipment logistics with practice support and financing, including broadline distributors and platforms such as Covetrus and MWI Animal Health. Specialist suppliers such as Jorgensen Laboratories, Leading Edge Veterinary Equipment, and Globalvets also participate in serving clinics and farm deployments. End customers include veterinary hospitals and clinics, which remain the largest purchasing channel in 2025, as well as a growing set of home-care and farm deployments that need onboarding, connectivity support, and data integration into practice-management or herd-management workflows. Key friction points across the chain include logistics volatility, sourcing constraints for electronics and plastics, and rising tariff-driven input costs for imported supplies, which increases the value of diversified sourcing, distributor-managed inventory, and service-centric contracts that reduce downtime for installed equipment.

Competitive Landscape

The veterinary monitoring equipment market features moderate fragmentation. Top five suppliers collectively control over half of revenue, giving mid-scale innovators room to differentiate. Incumbents such as IDEXX, Masimo, Smiths Medical, and Mindray cross-utilize human-health IP, achieving economies in sensor development and manufacturing scale. Strategic focus has migrated from hardware sales toward integrated ecosystems bundling cloud analytics, consumables, and service contracts.

Platform integration now defines competitive edge. Vendors embed open APIs, enabling seamless data flow into practice-management and telehealth portals. AI modules generate predictive alerts, moving the value proposition upstream from measurement to clinical decision support. In livestock, multinational pharmaceutical companies partner with sensor start-ups to pair therapeutic portfolios with health-monitoring subscriptions, locking in long-term farm relationships.

Market entry barriers ease as component costs fall and regulatory programs favor innovative SMEs. Niche challengers target under-served species or deploy disruptive business models such as device-as-a-service. However, sustaining momentum demands robust distribution and post-sale support. Consequently, alliances, OEM agreements, and selective acquisitions are intensifying as incumbents shore up feature gaps and expand geographic reach.

Veterinary Monitoring Equipment Industry Leaders

Covetrus

Agfa-Gevaert Group

Smiths Medical

Masimo

Midmark Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One opportunity area is the shift from standalone monitoring toward integrated livestock and companion-animal ecosystems that pair sensors with cloud analytics and decision support. Merck Animal Health reported in August 2025 that 2 million cows are monitored globally using its SenseHub dairy technology platform. The market has also continued to see AI-native monitoring expansion, including BioCV Inc.s May 2026 intelligent sow monitoring system, which combines ear-tag hardware with machine learning to detect heat cycles, farrowing, and health issues. These deployments create whitespace for multi-parameter and wearable vendors to integrate telemetry, dashboards, and workflow tools into subscription-based programs used by clinics, corporate practice groups, and large farms.

Adoption pathways for automated monitoring in herd-health programs and welfare-led dairy operations are also improving through clinical and production outcome validation. In July 2026, CattleEye highlighted University of Liverpool trial results reported in the Journal of Dairy Science, where automated AI mobility monitoring reduced severe lameness to 2% compared with 7.9% in control groups, supporting budget allocation for sensor systems that tie monitoring to measurable outcomes. Platform consolidation and adjacency moves are expanding partnership and bundling potential, including dsm-firmenichs July 2026 acquisition of the Verax predictive farm analytics platform to integrate biomarker-driven AI into precision livestock offerings, and Virbacs April 2026 exclusive distribution rights for MACSOs AI-powered respiratory monitoring technology for swine across Europe, Latin America, and Asia. In parallel, the lack of a harmonized EU-wide veterinary device framework and the US emphasis on labeling and post-market controls increase the value of manufacturers and distributors that can package compliance, cybersecurity, and data-governance capabilities alongside hardware.

Recent Industry Developments

- April 2026: Dispomed announced the launch of its Dovria line of veterinary monitors, including Dovria One and Dovria Pro handheld units and the modular Dovria Ultra. The launch expands choice in portable and modular monitoring formats used in anesthesia and critical-care workflows, supporting deployments across both small practices and higher-acuity settings.

- February 2026: Midmark commercially launched new Midmark Multiparameter Monitors, offering 12-inch and 8-inch display configurations. The update strengthens Midmark's monitoring portfolio for clinics seeking integrated vital-sign capture across procedure rooms and recovery areas.

- July 2024: Midmark launched the next generation of its M9 and M11 Steam Sterilizers, increasing rated life to 25,000 cycles. While not a monitor, the upgrade supports procedure throughput and infection-control readiness in veterinary facilities, indirectly enabling greater utilization of anesthesia and monitoring workflows that depend on reliable instrument reprocessing.

Research Methodology Framework and Report Scope

Market Definition and Coverage

We define the veterinary monitoring equipment market as the revenues generated from devices used to track animal vital signs and physiologic parameters during exams, anesthesia, surgery, and critical care, across veterinary clinics, hospitals, and other care settings worldwide.

Scope exclusions: We exclude veterinary consumables and single use sensors, and we also exclude broader diagnostic imaging and therapeutic equipment that is not primarily used for patient monitoring.

Segmentation Overview

- By Product Type (Value)

- Multi-parameter Monitors

- ECG Monitors

- Pulse-Oximeters

- Capnography Devices

- Blood-Pressure Monitors

- Wearable / Remote Monitors

- Other Products

- By Animal Type (Value)

- Companion Animals

- Dogs

- Cats

- Horses

- Others

- Livestock Animals

- Cattle

- Swine

- Poultry

- Sheep & Goats

- Others

- Companion Animals

- By End User (Value)

- Veterinary Hospitals & Clinics

- Research Institutes & Universities

- Home-care Settings

- Others

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- APAC

- China

- Japan

- India

- South Korea

- Australia

- Rest of APAC

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping what gets bought, where it is used, and how purchasing is funded, so the market is not mixed with adjacent equipment categories. We leaned on public health and animal care statistics to set the demand backdrop, and then aligned it to how monitors are used inside veterinary clinics and hospitals.

For grounding data, we referenced sources such as USDA animal health and livestock statistics, AVMA publications on veterinary practice and pet ownership, OIE (WOAH) animal health information, World Bank macro indicators, and UN Comtrade trade flows for relevant medical device categories. We also reviewed public company filings, investor presentations, product brochures, regulatory and standards references, and trusted press to understand pricing direction and product replacement cycles. Where helpful, our internal paid subscriptions were used for company financials and intelligence, news and financials tracking, patent lookups, and selected import export shipment level checks. These desk research sources are not exhaustive, and we reviewed additional public references to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary research focused on confirming what equipment is actually installed and purchased, how often it gets replaced, and what add-ons are treated as part of monitoring in day to day practice. We spoke with a mix of manufacturers, distributors, veterinary clinic and hospital staff, and service partners across APAC, EMEA, and the Americas, which helped finalize gaps on average selling prices, usage patterns, and adoption of connected or wearable monitoring.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 16% | APAC: 42% |

| Mid tier: 44% | Functional/Unit leaders: 30% | EMEA: 31% |

| Smaller Players: 17% | Managers: 54% | Americas: 27% |

Market-Sizing & Forecasting

Our sizing starts from a top down build that reconstructs demand using the veterinary care footprint in each region, and then converts that footprint into monitoring equipment spending through adoption and replacement behavior. To keep the model tied to real purchasing, we anchor assumptions to care settings that routinely monitor patients (for example during anesthesia, critical care, and in-patient recovery), then apply price and mix logic by equipment type.

Key inputs used in the model include the veterinary clinic and hospital base, procedure intensity signals (especially surgeries requiring anesthesia monitoring), the mix of companion animals versus livestock care, replacement cycles for monitors and modules, and average selling price progression by device class such as multi-parameter monitors and capnography and oximetry systems. Where public data is too broad, selective bottom up checks are used, including supplier revenue roll ups, channel checks on typical unit pricing, and sampled ASP times volume calculations to test whether regional totals look realistic. Missing pieces from bottom up checks are handled through conservative gap fills that are only applied after primary feedback confirms typical coverage and utilization.

For forecasting, we mainly used scenario analysis supported by trend smoothing on the core drivers, and the scenarios were reviewed with interviewees to agree on what adoption speed is practical by region. The forecast also reflects expected shifts toward connected monitoring and telemetry, but only where clinics report clear workflow fit and reimbursement support for these upgrades.

Data Validation & Update Cycle

Before finalizing, we run variance checks across regions and device groups, then compare outputs against independent signals such as trade movement direction, procedure growth, and reported clinic expansion trends. Outliers are reviewed in a second pass, and we re contact sources when pricing, replacement timing, or penetration assumptions appear inconsistent with how equipment is purchased in practice.

The model, assumptions, and calculations go through multi step analyst review before sign off, and the full report is refreshed annually so the market view stays current. If there is a material event such as a regulatory change, a major product shift, or a clear pricing reset, we also do an interim update. Right before delivery, an analyst performs a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Global Veterinary Monitoring Equipment Market Sizing Compared With Other Published Estimates

Published market sizes for veterinary monitoring equipment can differ because firms often count different product baskets, apply different price logic, and use different timing for currency conversion and updates. We try to keep the inputs traceable to how clinics and hospitals buy monitors, and then validate the totals with practical checks.

The main gap comes from whether single use sensors and other consumables are included inside the equipment number. Mordor Intelligence counts only durable monitoring devices and excludes routine disposable items even when they are bundled on invoices. Another frequent driver is the treatment of wearable and remote monitoring, since some estimates either treat it as a pet tech category or count only in clinic installs, which shifts volumes and average prices. Differences also show up when one model assumes aggressive ASP declines, or when the region mix is not refreshed after a demand swing in APAC and Europe.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.62 B (2026) | |

| Trade Journal A | USD 0.57 B (2027) | Uses an older base year and a narrower device set that emphasizes basic in clinic monitors, and it appears to undercount multi parameter upgrades and higher ASP modules used in surgical and ICU settings. |

| Industry Research Group B | USD 0.57 B (2020) | Reports an early year value and likely limits coverage to a few device types, and it does not clearly adjust for expansion of companion animal care or the growing mix of connected and wearable monitoring. |

The table shows that the spread mainly comes from scope and timing choices rather than arithmetic differences. By keeping the scope tied to durable monitoring equipment, using region level demand signals, and stress testing prices with channel feedback, we can produce a balanced figure that can be replicated and updated in a repeatable way.

Key Questions Answered in the Report

What segment fuels the fastest revenue growth?

Wearable and remote solutions lead the veterinary monitoring equipment market with a projected 6.88% CAGR because they enable continuous, AI-supported surveillance outside clinic walls.

How do U.S. regulations influence new-device launches?

FDA’s Innovation Agenda streamlines 510(k) reviews for connected sensors, cutting time-to-market and lowering costs for emerging manufacturers.

Why are ownership economics a challenge for small clinics?

Total cost of ownership for full multi-parameter suites can exceed USD 100,000 once maintenance and software subscriptions are included, stretching budgets for independent practices.

Which region displays the highest future growth?

APAC will advance at 7.98% CAGR through 2031, propelled by China’s expanding pet-medical spend and livestock modernization programs.

What competitive strategies define market leaders?

Companies are bundling hardware, cloud analytics, and telemedicine integration to create end-to-end platforms that embed predictive insights into daily workflows.

Page last updated on: