Veterinary Forceps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

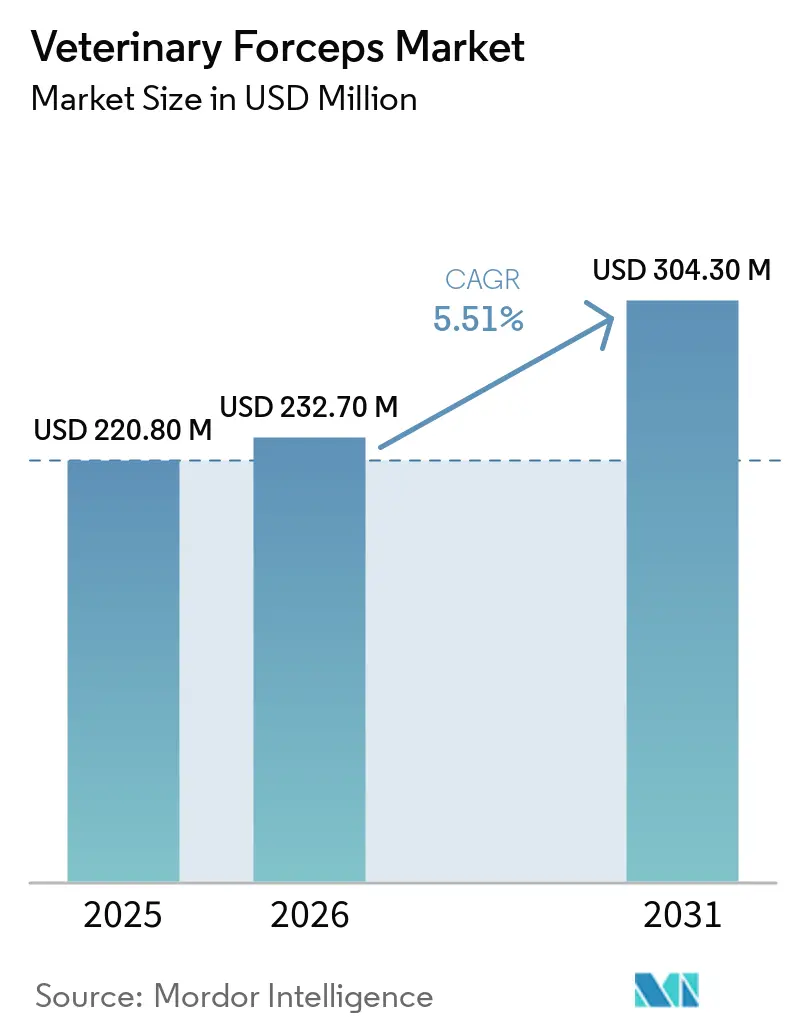

| Market Size (2026) | USD 232.70 Million |

| Market Size (2031) | USD 304.30 Million |

| Growth Rate (2026 - 2031) | 5.51% CAGR |

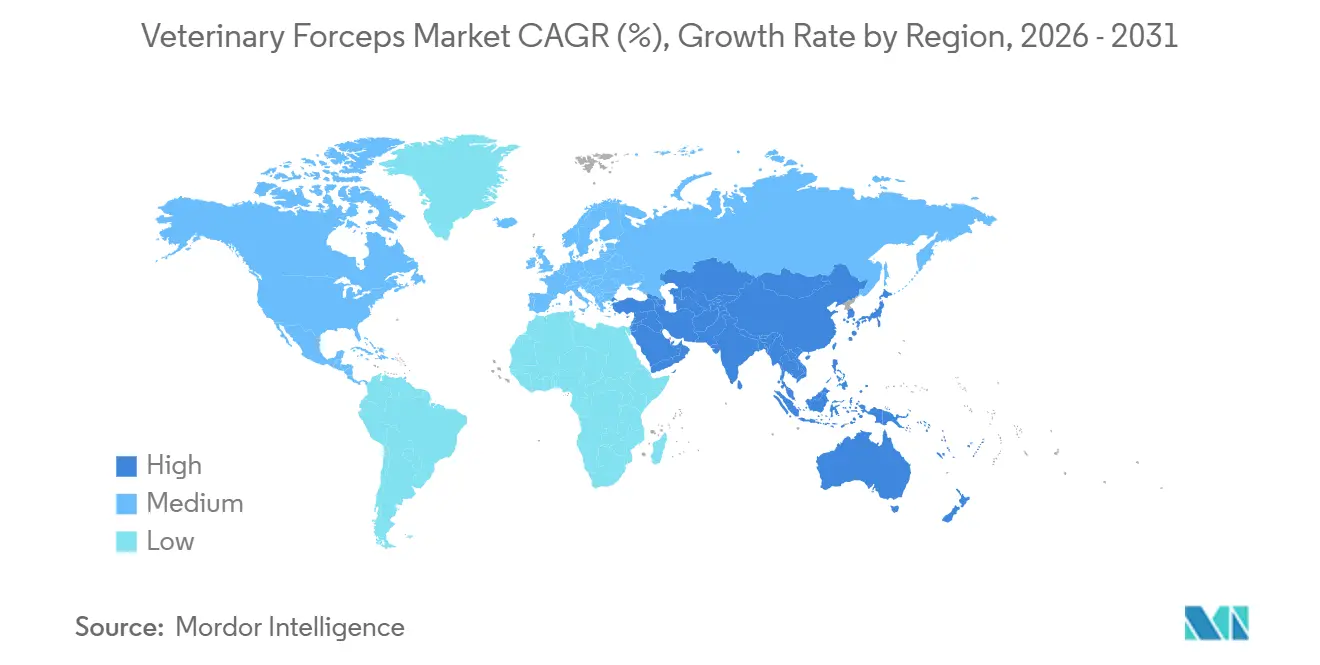

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Forceps Market Analysis by Mordor Intelligence

The Veterinary Forceps Market size is expected to grow from USD 220.80 million in 2025 to USD 232.70 million in 2026 and is forecast to reach USD 304.30 million by 2031 at 5.51% CAGR over 2026-2031.

Corporate consolidation is compressing supplier lists, lifting replacement cycles, and giving scale-ready manufacturers privileged access to multi-site chains [1]Integra LifeSciences Holdings Corporation, “Form 10-Q for the Quarter Ended September 30, 2025,” investor.integralife.com. Growth also reflects expanding dental and orthopedic caseloads, the diffusion of minimally invasive techniques into general practice, and regulatory momentum for traceable sterilization. Tariff pressures and titanium cost inflation are tempering margins but accelerating a pivot toward recycled alloys and sourcing from India or ASEAN. Asia-Pacific remains the fastest-growing geography, underpinned by pet ownership gains and livestock disease-control programs funded by multilateral agencies. Instrument suppliers capable of documenting sterilization cycles, offering just-in-time inventory, and bundling training are best positioned to capture chain-wide agreements.

Key Report Takeaways

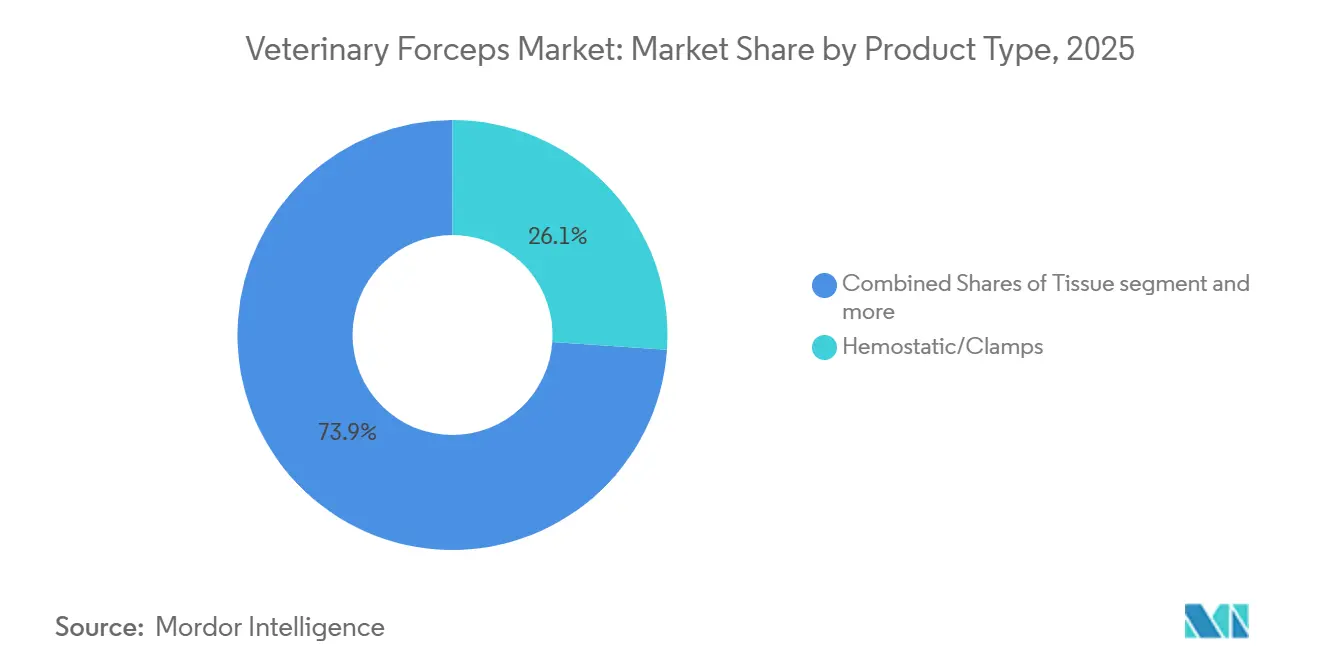

- By product type, hemostatic and clamp forceps led the veterinary forceps market, accounting for 26.10% share in 2025. However, dental extraction forceps are projected to grow at a 6.09% CAGR through 2031.

- By application, soft-tissue surgery accounted for 34.87% of the veterinary forceps market in 2025. However, orthopedic surgery is set to advance at a 5.98% CAGR to 2031.

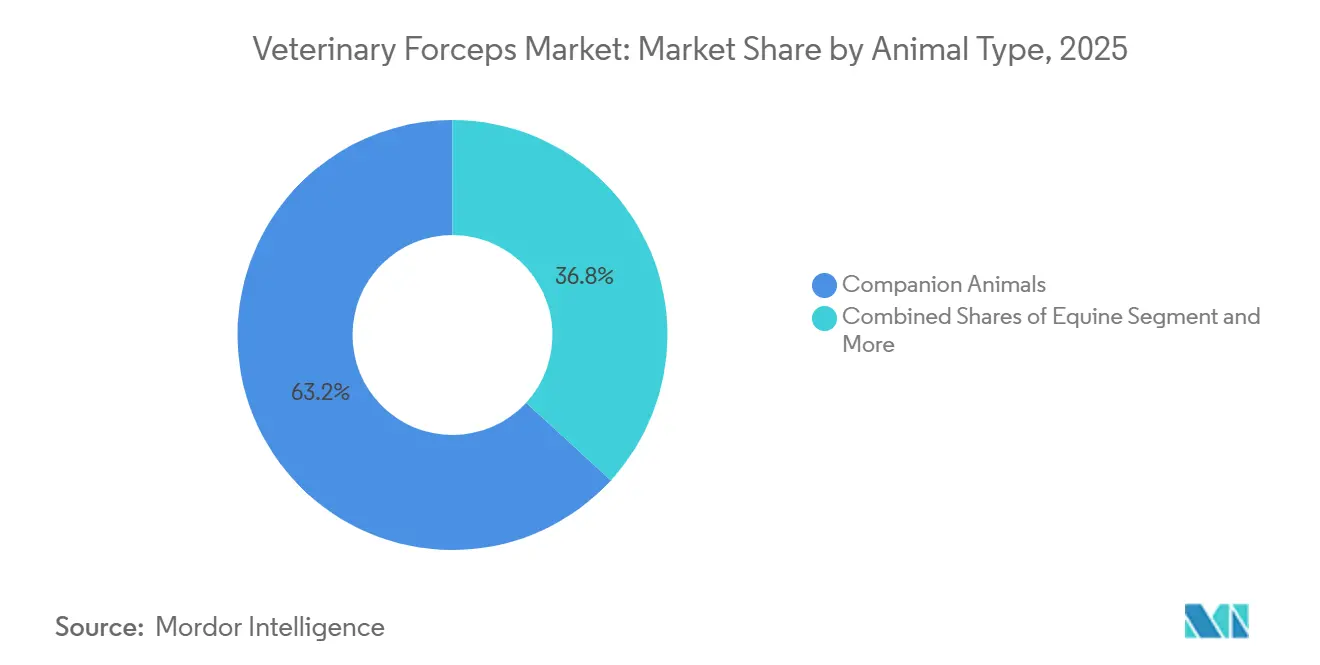

- By animal type, companion animals accounted for 63.18% of revenue in 2025 and is expected to grow with 5.81% CAGR by 2031.

- By end users, veterinary clinics accounted for 58.18% of revenue in 2025 and are projected to grow at a 5.81% CAGR through 2031.

- By geography, North America captured 43.81% share in 2025, while Asia-Pacific is forecast to post a 5.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Veterinary Forceps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Companion animal ownership and pet-health spending lift surgical procedure volumes | +1.2% | Global, strongest in North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| High-volume spay/neuter programs and post-pandemic surgical backlog sustain instrument demand | +0.9% | North America, Latin America, India, China | Short term (≤ 2 years) |

| Expansion of veterinary dental care elevates demand for extraction and tissue forceps | +0.8% | North America, Europe, Australia | Medium term (2-4 years) |

| Growth of minimally invasive and specialty procedures expands forceps use-cases | +1.0% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Procurement standardization by corporate consolidators accelerates SKU adoption and replacement | +0.7% | North America, Europe | Medium term (2-4 years) |

| Infection-control focus raises demand for sterile single-use and reprocessing-traceable forceps | +0.6% | Global, regulatory drivers in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Companion Animal Ownership and Pet-Health Spending Lift Surgical Procedure Volumes

U.S. pet spending climbed to USD 158 billion in 2025, and is projected to reach USD 165 billion in 2026. Rapid insurance uptake lowers cost barriers, prompting owners to approve surgeries that formerly were deferred. Although overall visit counts dipped 3.1% due to staffing shortages, the procedures performed tend to be complex and instrument-intensive, boosting demand for high-margin specialty forceps. Emergency visits rose to 22% of owners in 2025, concentrating surgical volumes at referral hospitals that maintain deeper inventories and tighter replacement cycles. Suppliers that certify traceability and provide quick-turn servicing strengthen their position with these hospitals.

High-Volume Spay/Neuter Programs and Post-Pandemic Surgical Backlog Sustain Instrument Demand

High-volume clinics, typified by PAWS Chicago’s target of 20,000 spay-neuter surgeries in 2025, are addressing a backlog of 261,763 missed procedures accumulated during 2020-2023 lockdowns. Rising throughput favors pre-sterilized or single-use hemostats that bypass autoclave bottlenecks. Yet persistent workforce gaps cap expansion speed, forcing tray standardization and bulk purchasing to curb turnaround delays. Vendors offering kitted solutions and competitive per-procedure economics gain preferred-vendor status.

Expansion of Veterinary Dental Care Elevates Demand for Extraction and Tissue Forceps

Periodontal disease affects the majority of dogs over 3 years old, and typical cleanings cost USD 300–700, prompting general practitioners to add dental suites. GerVetUSA’s 2025 launch of customizable Extraction Kits illustrates the push toward modular instruments that match practitioner skill levels [2]B. Braun Vet Care, “Minimally Invasive Surgery: Small Access, Clear Vision,” bbraun-vetcare.com. Exotic-animal kits with mini handles are designed for rabbits and rodents, underscoring the premium that owners place on specialized oral care. As dentistry migrates from referral centers into general practice, instrument volumes accelerate and average selling prices moderate, rewarding manufacturers that can scale production without sacrificing finish and edge retention.

Growth of Minimally Invasive and Specialty Procedures Expands Forceps Use-Cases

Single-port laparoscopy significantly reduces postoperative pain and nearly halves infection risk, broadening its acceptance among non-specialists. Learning curves plateau after roughly a dozen cases, driving incremental demand for optical, articulating, and vessel-sealing forceps. B. Braun’s Caiman system and DS-Clips facilitate laparoscopic splenectomy and adrenalectomy, while Securos Surgical’s lifetime-warranty clamps appeal to cost-sensitive clinics that autoclave instruments daily. As specialty techniques diffuse, reusable forceps that retain alignment after repeated sterilization command loyalty.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High instrument and sterilization costs constrain clinic CAPEX | -0.8% | Global, acute in emerging markets and independents | Short term (≤ 2 years) |

| Shortage of skilled veterinary surgeons limits surgical throughput | -0.6% | North America, Europe, Australia | Medium term (2-4 years) |

| Input and tariff volatility for surgical-grade steel and titanium pressure prices and margins | -0.5% | Global, acute in U.S. and EU | Short term (≤ 2 years) |

| Research 3Rs and activism reduce lab-animal surgical volumes for micro-forceps | -0.3% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Instrument and Sterilization Costs Constrain Clinic CAPEX

Fixed facility start-ups require USD 433,000–2 million, with roughly USD 70,000 earmarked for surgical and dental gear, leaving little headroom for premium forceps. Working-capital constraints and higher 2025 interest rates prompted many independents to stretch replacement cycles through repair services. Equipment financing demands credit scores above 640 and exposes clinics to rate resets, prompting deferral of non-essential upgrades. Suppliers offering repair kits, sharpening programs, and trade-in rebates can ease budgetary friction.

Shortage of Skilled Veterinary Surgeons Limits Surgical Throughput

Forecast gaps of 15,000–41,000 veterinarians by 2030 curb procedure volumes despite rising pet counts. High-volume centers absorb basic surgeries, concentrating complex cases, and forcing patients to spend more time in referral hospitals. Long learning curves for laparoscopic or neurosurgical tools slow the diffusion of specialized clamps and graspers, tempering upside-down for innovative designs until training capacity expands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dental Extraction Forceps Outpace Hemostatic Clamps

Hemostatic and clamp forceps captured 26.10% veterinary forceps market share in 2025, anchored by universal use across soft-tissue, orthopedic, and emergency trays. Dental extraction forceps are on track for a 6.09% CAGR to 2031, expanding 58 basis points faster than the overall veterinary forceps market. Growth stems from general-practice adoption of dental suites and rising owner awareness of periodontal disease. Tissue, dressing, and orthopedic forceps fill mature niches where sales hinge on replacement rather than first-time installs. Ophthalmic and endoscopic biopsies remain small but price-dense due to precision machining and microtip finishing. GerVetUSA’s titanium dental kits and B. Braun’s BipoJet bipolar clamps exemplify performance-driven innovations commanding price premiums [3]B. Braun Vet Care, “BipoJet Bipolar Program,” bbraun-vetcare.com.

Continued investments in operator ergonomics, such as winged elevators and articulating handles, improve grip security and reduce surgeon fatigue, reinforcing repeat purchasing. The demand for veterinary surgical forceps is expected to surge. Manufacturers pairing extraction forceps with luxating elevators and periosteal lifters deepen lock-in among clinics upgrading entire dental sets at once.

By Application: Soft-Tissue Dominates, Orthopedic Accelerates

Soft-tissue procedures held 34.87% of revenue in 2025, led by spay-neuter, mass removal, and abdominal surgery, yet orthopedic cases are slated for a 5.98% CAGR through 2031, outrunning the veterinary forceps market by 47 basis points. Locking-plate systems that outperform pin-and-wire constructs require specialized reduction grips and bone-holding clamps, pushing per-case instrument outlays higher. As insurers reimburse fracture repair more readily, clinics increase stock of rongeurs, bone plates, and reduction forceps, driving a larger share of the veterinary forceps market size into orthopedic SKUs. Endoscopic neurosurgery and ophthalmic specialties extend portfolio depth at referral hospitals, although volumes remain comparatively modest.

Technological spillover from human orthopedics, such as 3D-printed patient-specific guides, further differentiates forceps offerings. High upfront capital impedes adoption by general practices, but teaching hospitals and corporate referral centers are piloting these systems, reinforcing demand for compatible graspers and reduction clamps. Suppliers that bundle power tools with matching forceps under service contracts gain cross-selling synergy.

By Animal Type: Companion Animals Lead, Livestock Gains Momentum

Companion animals comprised 63.18% of 2025 revenue and will remain the anchor of the veterinary forceps market, supported by urban pet humanization and rising insurance coverage. Livestock lines, however, are forecast to grow at 5.86% CAGR on the back of Asia-Pacific disease-control programs funded by USD 25 million in ADB/FAO grants.

Field-ready, corrosion-resistant clamps tailored for castration and dehorning are in high demand, with rugged designs outweighing premium surface polish. The equine and exotic-animal segments command higher price points per instrument due to their size and torque requirements, but contribute smaller absolute volumes.

Growing ownership of non-traditional pets boosts micro-series forceps. Titanium micro-avian kits reduce surgeon fatigue during prolonged procedures on birds or reptiles and sell at a 20–30% premium to stainless counterparts. As more practitioners pursue exotic certification, the installed base of niche forceps widens, offsetting deceleration in laboratory-animal demand.

By End User: Clinics Consolidate Share, Referral Centers Specialize

Veterinary clinics accounted for 58.18% of revenue in 2025 and are projected to grow at a 5.81% CAGR through 2031. Corporate chains absorb independents at a record pace 532 transactions in 2025—centralizing procurement and standardizing trays. Chains prize consistent quality and automated inventory resupply, favoring manufacturers with ERP integration. Referral hospitals and teaching institutions, while smaller in number, buy a wider spectrum of specialty forceps and replace them more often due to resident turnover and accreditation audits. Research institutes shrink as in vitro alternatives displace animal models; nonetheless, they continue to purchase micro-dissection tools for remaining regulated studies.

Geography Analysis

North America retained a 43.81% share in 2025, driven by USD 157 billion in U.S. pet spending and a dense network of Mars Petcare facilities. Pet insurance penetration of 6.4 million policies lowers decision friction for elective surgery, though clinic staffing shortages capped 2025 visit growth. Tariffs of up to 54% on Chinese forceps elevated landed costs, prompting suppliers to near-shore production or blend recycled titanium to maintain margins.

Asia-Pacific is forecast to advance at a 5.97% CAGR through 2031, driven by China’s urban pet boom and India’s National Animal Disease Control Programme, which underwrites large-scale surgical interventions in livestock. Regulatory clarification by India’s CDSCO in July 2025 eased device imports, inviting foreign brands to tap the veterinary forceps market. Japan and South Korea add premium tailwinds via tech-enabled clinics and willingness to adopt minimally invasive procedures.

Europe presents a fragmented regulatory patchwork; only six member states directly regulate veterinary devices, complicating rollout. Dual-use instruments must comply with MDR 2017/745, thereby inflating compliance costs. Upcoming EU GMP rules effective July 2026 tighten aseptic manufacturing requirements, indirectly raising the bar for forceps sterilization validation. South America and MEA remain smaller but rising; Brazil benefits from increasing companion-animal ownership, while GCC states boost livestock health budgets, together nudging incremental demand for mid-tier forceps lines.

Competitive Landscape

The market is moderately fragmented. Integra LifeSciences, B. Braun Vet Care, and KRUUSE anchor the upper tier, leveraging broad catalog depth and global distribution. Integra’s Codman Specialty Surgical division booked USD 50.2 million from veterinary offices in Q3 2025, although USD 511.4 million in goodwill impairments signaled profitability pressures. B. Braun deepens penetration through exclusive distribution pacts with Movora, adding power-tool ecosystems that dovetail with bone-holding forceps.

Mid-sized specialists GerVetUSA, iM3, and Securos Surgical compete on customization, ergonomic design, and post-sale service. Securos’ lifetime warranty and free sharpening program lowers total cost of ownership, resonating with budget-conscious chains. GerVetUSA’s online configurator lets clinics tailor sets, tightening customer lock-in. New entrants exploit additive manufacturing to produce patient-specific guides but face steep regulatory hurdles and significant capital outlays.

Corporate consolidation reshapes bargaining power. Large chains negotiate multi-year contracts with automatic replenishment, squeezing unit margins yet guaranteeing volume. Suppliers with ISO-certified plants in low-tariff zones and the ability to document cradle-to-grave traceability secure an edge. Meanwhile, independents remain open to niche innovations, providing a testing ground for novel handle geometries and coated jaws.

Veterinary Forceps Industry Leaders

Integra LifeSciences

B. Braun Melsungen AG

KRUUSE

GerVetUSA

iM3

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Dr. Bellows Extraction Kit featured in MVC Midwest Veterinary Conference 2026. The Dr. Bellows Extraction Kit is a complete veterinary dental set featuring GLux luxating straight elevators, Winged elevators, periosteal elevators, Olsen Hegar needle holder scissors, forceps, lip retractor, gum scissors, and more for precise extractions.

- Jul 2025: Movora partnered with dvmGRO to bundle orthopedic products and CE programs across U.S. corporate clinics, expanding reach into standardized procurement channels

- June 2025: KARL STORZ consolidated its Canada, U.S., and Veterinary operations into a North America hub to streamline cross-selling of endoscopic gear into veterinary accounts.

Global Veterinary Forceps Market Report Scope

As per the scope of the report, veterinary medicine, forceps are essential, handheld, hinged instruments designed to provide precision and controlled leverage for grasping, holding, or manipulating tissues, vessels, and various objects during surgical procedures. Functioning on the principle of a lever, these tools allow veterinarians to access confined body cavities and manipulate small structures that are too small or delicate for human fingers.

The veterinary forceps market is segmented by product type, application, animal type, end user, and geography. By product type, the market is segmented into hemostatic/clamps tissue, dressing/sponge, dental extraction, orthopedic, ophthalmic, and endoscopic & biopsy. By applications, the market is segmented into dental surgery, soft tissue surgery, orthopedic surgery, ophthalmic/neurosurgery, and endoscopy. By animal type, the market is segmented into companion animals, equine, livestock, and avian/exotics/small mammals. By end user, the market is segmented into veterinary clinics, veterinary hospitals/referral & teaching centers, research institutes & academic labs.

Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Hemostatic/Clamps |

| Tissue |

| Dressing/Sponge |

| Dental Extraction |

| Orthopedic |

| Ophthalmic |

| Endoscopic & Biopsy |

| Dental Surgery |

| Soft Tissue Surgery |

| Orthopedic Surgery |

| Ophthalmic/Neurosurgery |

| Other Applications |

| Companion Animals |

| Equine |

| Livestock |

| Other Animal Types |

| Veterinary Clinics |

| Veterinary Hospitals/Referral & Teaching Centers |

| Research Institutes & Academic Labs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Hemostatic/Clamps | |

| Tissue | ||

| Dressing/Sponge | ||

| Dental Extraction | ||

| Orthopedic | ||

| Ophthalmic | ||

| Endoscopic & Biopsy | ||

| By Application | Dental Surgery | |

| Soft Tissue Surgery | ||

| Orthopedic Surgery | ||

| Ophthalmic/Neurosurgery | ||

| Other Applications | ||

| By Animal Type | Companion Animals | |

| Equine | ||

| Livestock | ||

| Other Animal Types | ||

| By End User | Veterinary Clinics | |

| Veterinary Hospitals/Referral & Teaching Centers | ||

| Research Institutes & Academic Labs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the veterinary forceps market?

The market was valued at USD 232.7 million in 2026 and is projected to reach USD 304.3 million by 2031.

Which product segment is expanding fastest?

Dental extraction forceps are forecast to grow at a 6.09% CAGR through 2031, outpacing all other product types.

Why are tariffs relevant to forceps pricing?

U.S. tariffs of up to 54% on Chinese medical devices applied in April 2025 raised landed costs, pressuring margins and prompting suppliers to shift sourcing to India and Southeast Asia.

Which region is projected to post the highest growth?

Asia-Pacific is expected to register a 5.97% CAGR between 2026 and 2031, driven by rising companion-animal ownership and government-funded livestock health programs.

Page last updated on: