Veterinary Equipment And Disposables Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

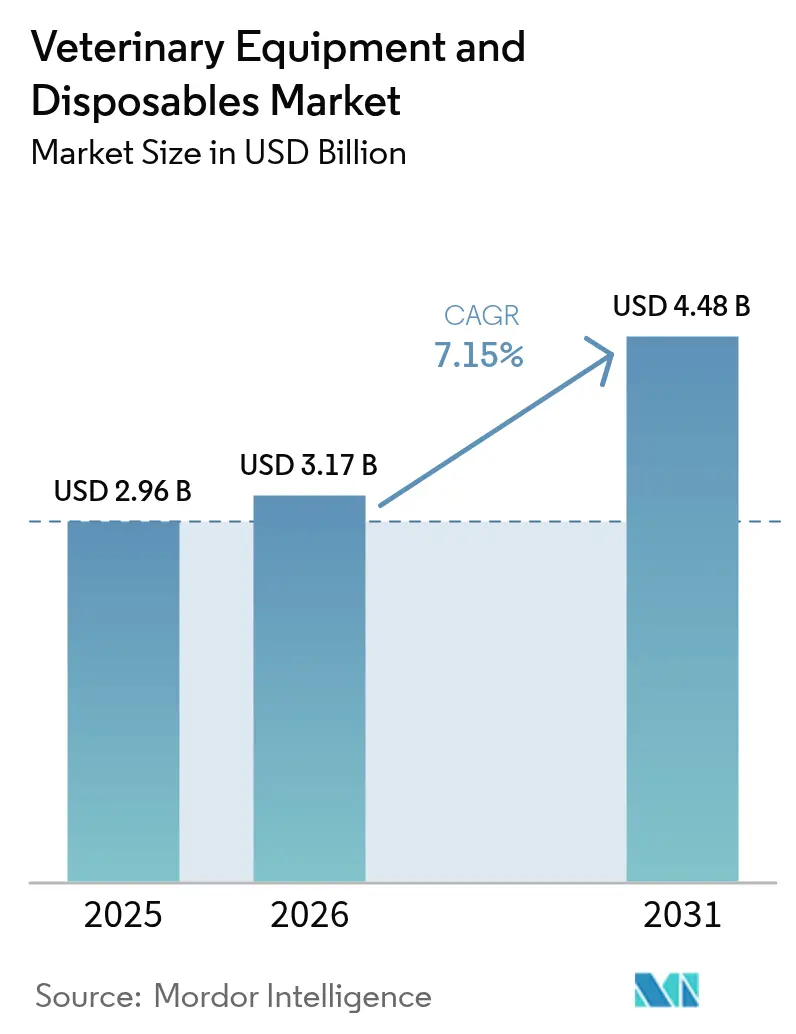

| Market Size (2026) | USD 3.17 Billion |

| Market Size (2031) | USD 4.48 Billion |

| Growth Rate (2026 - 2031) | 7.15% CAGR |

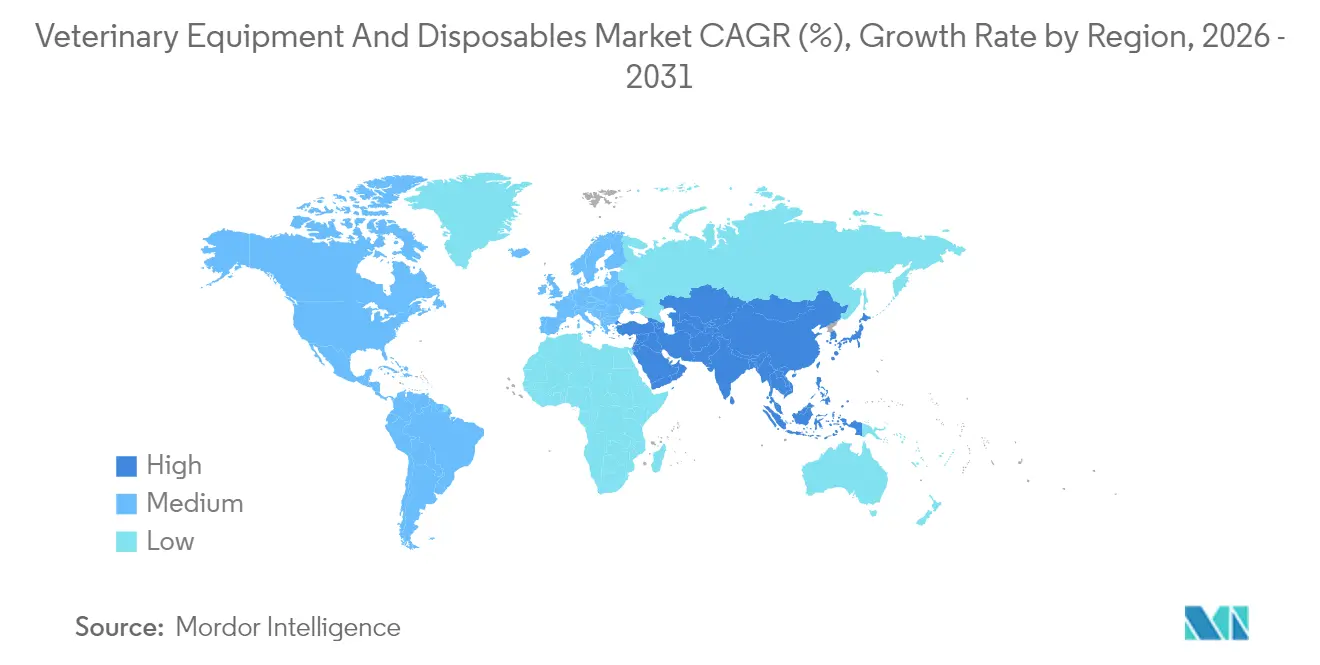

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Equipment And Disposables Market Analysis by Mordor Intelligence

The veterinary equipment and disposables market size is expected to grow from USD 2.96 billion in 2025 to USD 3.17 billion in 2026 and is forecast to reach USD 4.48 billion by 2031 at 7.15% CAGR over 2026-2031. Growth is fuelled by sustained pet humanization that lifts spending on advanced diagnostics, regulatory disease-surveillance mandates within livestock sectors, and a steady pipeline of technology upgrades that shorten equipment replacement cycles. Momentum is reinforced by the spread of pet insurance, which improves client willingness to authorize higher-value procedures, and by rapid uptake of portable, AI-enabled devices that suit both clinic-based and mobile care models. Livestock operators add further demand through compulsory H5N1 testing regimes that require rugged point-of-care analyzers [1]Source: USDA APHIS, “Federal Order Requiring Testing for and Reporting of Highly Pathogenic Avian Influenza (HPAI) in Livestock,” aphis.usda.gov . Competitive rivalry is intensifying as platform players bundle instruments, consumables, cloud software, and AI analytics to create sticky ecosystems, while emerging manufacturers court cost-sensitive buyers with modular, service-light designs. Asia-Pacific’s build-out of private pet hospitals, alongside the consolidation of fragmented chains, positions the region as the most dynamic geography for equipment vendors.

Key Report Takeaways

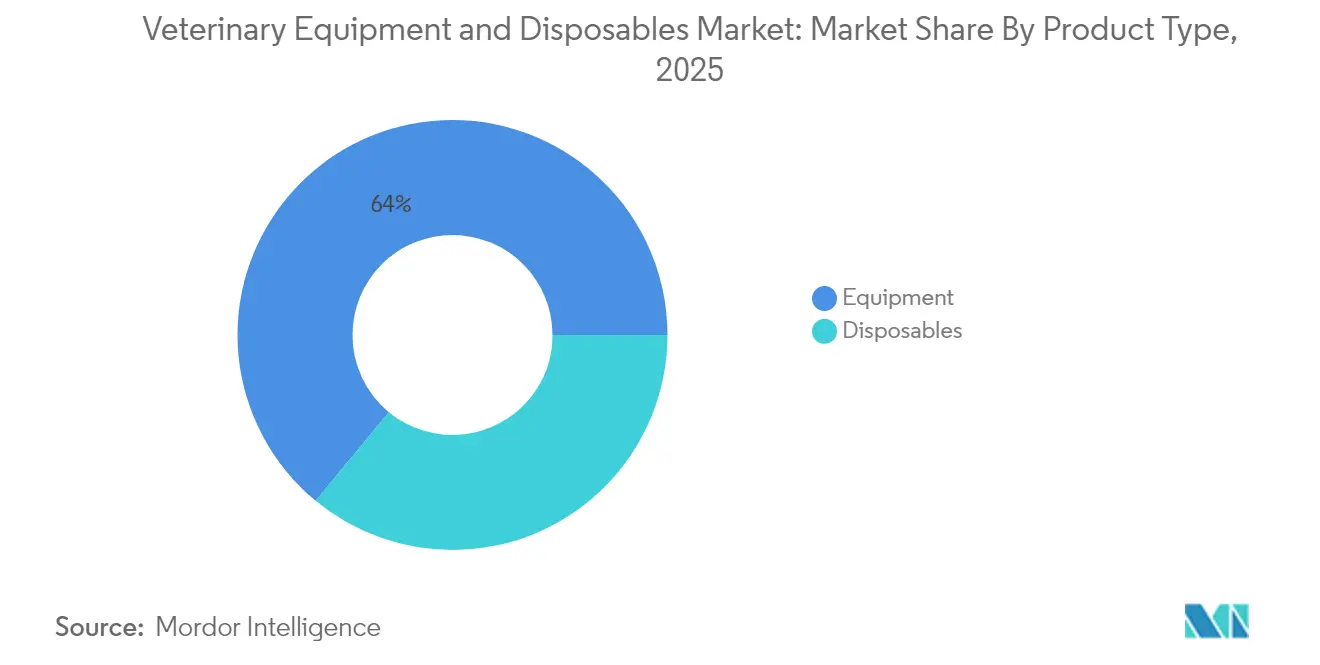

- By product type, equipment led with 64.02% revenue share in 2025, while disposables are forecast to expand at an 7.74% CAGR through 2031.

- By animal type, companion animals held 57.85% of the veterinary equipment and disposables market share in 2025 and are projected to grow at an 8.14% CAGR to 2031.

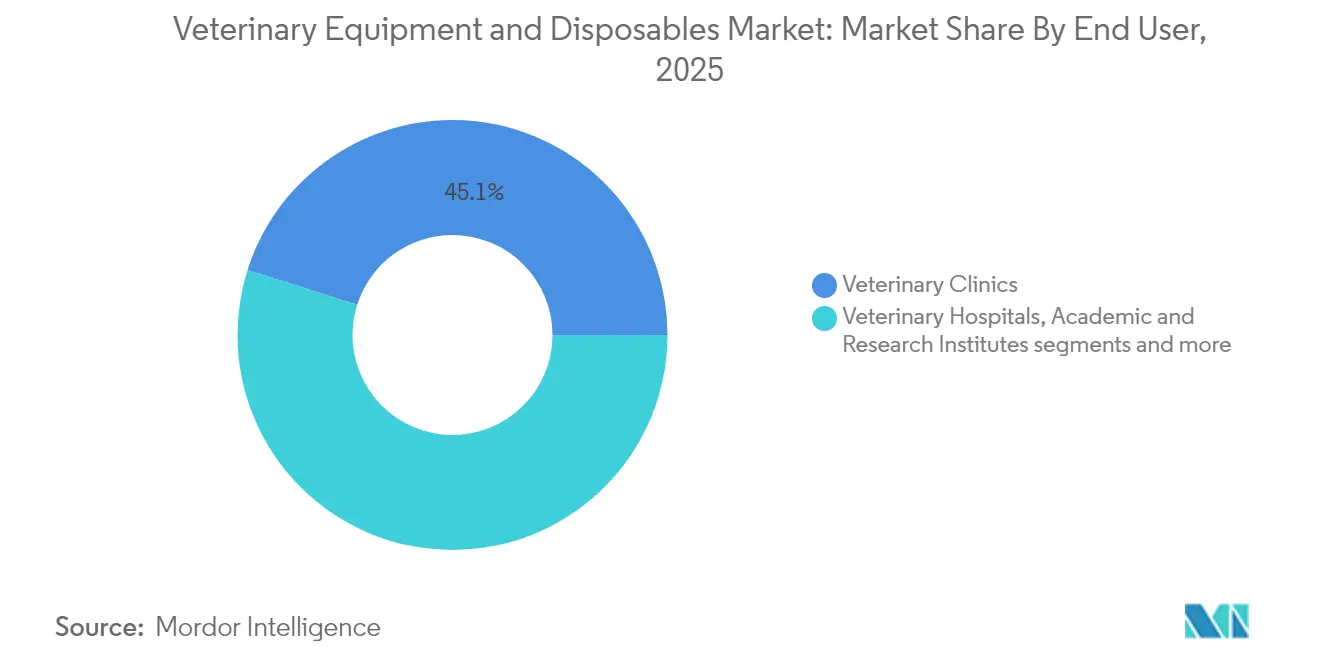

- By end user, veterinary clinics commanded 45.12% share of the veterinary equipment and disposables market size in 2025, whereas mobile and ambulatory services register the strongest 8.61% CAGR to 2031.

- By geography, North America captured 41.05% revenue share in 2025; Asia-Pacific is advancing at a 9.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Equipment And Disposables Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth in pet insurance penetration | +1.20% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Rising livestock disease surveillance mandates | +0.90% | Global, with emphasis on US, EU, and China | Short term (≤ 2 years) |

| Expansion of minimally-invasive surgical tools | +1.10% | North America & Europe, gradual APAC adoption | Medium term (2-4 years) |

| Growth of tele-veterinary diagnostics platforms | +1.30% | Global, accelerated in developed markets | Short term (≤ 2 years) |

| Mainstream adoption of single-use endoscopy | +0.80% | North America & Europe primarily | Medium term (2-4 years) |

| Genetic screening driving preventive equipment demand | +0.70% | North America & Europe, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth in Pet Insurance Penetration

Pet insurance policies are reshaping the veterinary equipment and disposables market by encouraging earlier adoption of high-end imaging and in-house laboratory systems. Insured clients approve advanced diagnostics 2.3 times more often than uninsured owners, which lifts practice revenue and accelerates equipment payback periods. In the United States, policy coverage now exceeds 5.5 million pets, and insurers increasingly require detailed imaging or pathology reports for claim validation, driving clinics to upgrade to digital radiography and CT platforms. Europe mirrors this trajectory, as Nordic countries exceed a 30% penetration rate, prompting widespread modernization of anesthesia monitors and dental suites. Asian providers are launching bundled micro-insurance products that cover outpatient diagnostics, further broadening demand. The cascading effect of higher reimbursement limits supports the placement of premium instruments across corporate chains and independent practices.

Rising Livestock Disease Surveillance Mandates

The USDA Federal Order of April 2024 compels dairy herds to test for H5N1 before interstate transport, immediately boosting orders for on-farm PCR units, handheld blood analyzers, and secure data-logging software. European and Chinese authorities are deploying comparable frameworks that require traceable, rapid diagnostics within poultry, swine, and cattle operations, catalyzing procurement of ruggedized ultrasound and thermal-imaging equipment. Producers utilize these tools to minimize quarantine downtime and maintain export eligibility, resulting in recurring revenue from consumables for manufacturers. The mandates also accelerate laboratory capacity expansion, stimulating sales of centrifuges, biosafety cabinets, and sample-prep robotics. Short-cycle replacement of field-deployed sensors sustains aftermarket growth throughout the forecast window.

Expansion of Minimally-Invasive Surgical Tools

Veterinary surgeons are increasingly favoring laparoscopic, arthroscopic, and endoscopic techniques that reduce postoperative pain and shorten recovery intervals, thereby elevating demand for high-definition cameras, insufflators, and articulating instruments. The utilization of rigid endoscopy has increased by 34% since 2024, with procedures such as urethroscopy and thoracoscopy gaining widespread acceptance. Specialty hospitals invest in 4K visualization towers and advanced energy devices to market premium care packages. At the same time, compact all-in-one scopes make minimally invasive options viable for mid-sized clinics. Disposable accessory kits support infection-control standards and enable predictable case costing. In the medium term, AI-assisted image recognition is expected to enhance lesion detection accuracy, unlocking new revenue streams for software service subscriptions.

Growth of Tele-Veterinary Diagnostics Platforms

Teleconsultation volumes remain above pre-pandemic levels, as clients appreciate the convenience and rural geographies benefit from expert access. Devices like Zoetis’ iSTAT Alinity v deliver electrolyte and blood-gas panels in under three minutes, supporting remote treatment protocols. AI-enabled cytology platforms, such as Vetscan Imagyst, automate result interpretation, which mitigates the shortage of specialist pathologists while enhancing diagnostic consistency. Practices also deploy mobile carts that integrate camera-enabled slit lamps and dermatology scopes, allowing veterinarians to perform comprehensive exams during home visits or farm calls.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost for advanced imaging suites | -1.40% | Global, more pronounced in emerging markets | Medium term (2-4 years) |

| Shortage of skilled veterinary radiologists | -0.80% | North America & Europe primarily | Long term (≥ 4 years) |

| Re-use culture in price-sensitive markets | -1.10% | APAC emerging markets, Latin America, MEA | Medium term (2-4 years) |

| Regulatory ambiguity for novel disposables | -0.60% | Global, with varying regional intensity | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost for Advanced Imaging Suites

Digital radiography units start at around USD 21,000, and full DR suites average USD 29,995; however, lifetime costs double once warranties, service contracts, and software upgrades are factored in. Small clinics postpone purchases or turn to refurbished systems, which slows primary market turnover. In emerging economies, limited access to low-interest financing further deters adoption of CT and MRI platforms. Large corporate chains leverage volume discounts and centralized reading services to dilute per-exam costs, thereby widening the technology gap between consolidated networks and solo practitioners. Government tax incentives, such as US Section 179, provide partial relief but do not fully offset the capital intensity that constrains equipment penetration.

Shortage of Skilled Veterinary Radiologists

North America has fewer than 700 board-certified veterinary radiologists, a shortage that hinders the full utilization of advanced imaging modalities. Europe faces similar imbalances as caseloads per specialist exceed sustainable levels, leading to diagnostic delays and burnout. Academic programs struggle to expand class sizes due to limited training infrastructure, while escalating student debt discourages specialization in specific fields. AI-based image-analysis software helps mitigate routine case backlogs; however, complex studies still require human interpretation, making staffing a persistent bottleneck. Practices therefore hesitate to invest in high-end modalities that may sit idle, thereby moderating the growth trajectory of the veterinary equipment and disposables market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Equipment Dominance Drives Innovation

Equipment represented 64.02% of the veterinary equipment and disposables market in 2025, underscoring the capital-intensive nature of modern practice operations. Diagnostic imaging units are the fastest-growing subcategory, as AI-integrated ultrasound and digital radiography reduce scan times and enhance triage accuracy. Surgical lasers and regenerative therapy devices broaden therapeutic options and carry premium margins. Anesthesia workstations and multiparameter monitors record steady uptake due to stricter procedural safety protocols. The veterinary equipment and disposables market size for disposables is smaller; however, single-use drapes, catheters, and endoscopy consumables are projected to post an 7.74% CAGR, driven by infection-control standards and predictable cost models.

Disposables accounted for a 35.98% share in 2025, but their recurring-revenue profile appeals to suppliers seeking stable cash flows. Syringes and needles dominate the volume; wound dressings and cytology slides are growing, with a focus on preventive dermatology. Single-use endoscopy accessories garner attention where contamination risk is high, although recent studies have found reusable forceps to be non-inferior after repeated sterilization. Cost-benefit debates will shape penetration levels, especially in resource-constrained clinics. Material advances in breathable laminates lower the environmental footprint of disposables and may attract sustainability-minded buyers.

By Animal Type: Companion Animals Lead Growth

Companion animals held a 57.85% share of the veterinary equipment and disposables market in 2025 and are projected to grow at an 8.14% CAGR, supported by urban pet adoption and aging canine and feline populations. Dogs present varied anatomy that motivates clinics to stock a broad range of probes, scopes, and orthopedic implants. Feline-specific calming enclosures and low-noise dental units enhance compliance, thereby increasing equipment utilization. Equine practitioners invest in portable radiography and regenerative therapy systems for sports medicine cases, although volumes remain niche. Exotic pets stimulate demand for miniature endoscopes and microfluidic hematology analyzers.

Livestock animals retained a 42.15% share in 2025, powered by dairy and poultry biosecurity investments. The veterinary equipment and disposables market size for cattle increased after the H5N1 surveillance order prompted farms to purchase mobile PCR readers. Swine producers install automated body-weight cameras and gas-sensor arrays to optimize feed conversion. Poultry integrators use handheld thermography and rapid antigen tests to manage flock health in high-density barns. Goat and sheep segments remain under-equipped, yet present an upside, as small-ruminant meat gains popularity in Africa and Southeast Asia.

By End User: Clinics Dominate, Mobile Services Surge

Veterinary clinics captured 45.12% of the veterinary equipment and disposables market share in 2025, purchasing mid-range digital X-ray, in-house blood analyzers, and dental suites that support routine wellness programs. Corporate groups leverage centralized purchasing to negotiate bundled equipment plus software subscriptions, which fosters stickiness. Independent clinics differentiate themselves through niche services, such as reproductive imaging or laser rehabilitation, spurring the addition of targeted equipment.

Mobile and ambulatory units are the fastest-growing end-user segment, posting a 8.61% CAGR through 2031 as pet owners seek at-home care convenience. Portable ultrasound, battery-powered chemistry analyzers, and wireless otoscopes enable comprehensive field diagnostics. Hospitals retain a 28.45% share, focusing on MRI, CT, and fluoroscopy, which underpin intensive care and specialty surgery. Academic institutions purchase high-fidelity simulators and advanced imaging equipment to meet evolving curricular standards, although budget cycles cause lumpy demand.

Geography Analysis

North America held 41.05% of 2025 revenue, anchored by high pet ownership, favorable insurance penetration, and federal livestock testing directives that stimulate equipment upgrades. The United States clinics are rapidly adopting AI-powered hematology and cytology platforms, while Canada is emphasizing cattle traceability and companion animal dental care. Mexico’s growing middle class drives puppy and kitten wellness programs, leading to increased turnover of small equipment. Although mature, the region still represents a market for replacing battery-powered digital radiography and cloud PACS that streamline workflows.

The Asia-Pacific region is the fastest-growing, with a 9.12% CAGR through 2031. Japan adopts minimally invasive surgical tools to serve an aging pet population. South Korea leads in digital neuro-diagnostics for small dogs prone to IVDD. India’s livestock modernization drives the adoption of portable ultrasound and mastitis-test readers, while Australia upgrades its biosecure poultry inspection systems to maintain export status.

Europe ranks second in share owing to robust welfare regulations and broad companion coverage. Germany mandates radiation safety certification for X-ray operators, driving upgrades to low-dose detectors. The UK Competition and Markets Authority investigation into veterinary pricing could spur transparency-driven procurement of cost-efficient analyzers. France and the Netherlands pilot eco-friendly anaesthesia scavenging systems, aligning with EU Green Deal ambitions. Southern markets such as Spain prioritize multi-species versatility in imaging suites to serve mixed companion-livestock practices.

Competitive Landscape

The veterinary equipment and disposables market is moderately concentrated, with North America leading the way today, while the Asia-Pacific region is the fastest-growing. Competition is split between capital equipment (anesthesia workstations, monitors, imaging, and dental) and high-velocity consumables (needles, IV sets, catheters, and drapes). Platform vendors such as Midmark (dental delivery, sterilizers, and patient monitoring), Mindray Animal Medical (anesthesia, monitoring, and imaging), and B. Braun Vet Care (infusion pumps/lines, and DEHP-free sets) rely on service coverage and OEM parts to create stickiness. Distributors/integrators Covetrus bundle equipment with software, financing, and field support, shaping procurement choices for clinics and corporate groups. Their catalogs span anesthesia, dental, imaging, lab analyzers, and private-label consumables. Regional specialists (e.g., Eickemeyer, Dispomed/Avante) round out the landscape, competing on value, training, and niche SKUs. Diagnostic instrument ecosystems are increasingly influencing capital and consumables pull-through: IDEXX continues to grow its installed base and in-clinic analyzer lineup, reinforcing recurring revenue from reagents and services.

Veterinary Equipment And Disposables Industry Leaders

Mindray Medical International Limited

Medtronic

B. Braun SE

ICU Medical, Inc. (Smiths Medical Inc.)

Midmark Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Zoetis launched enhanced telemedicine features and AI upgrades for the Vetscan Imagyst platform, targeting improved diagnostic accuracy and reduced administrative burden

- January 2025: IDEXX Laboratories commenced commercial rollout of its Cancer Diagnostics screening panel following successful clinical validation.

- November 2024: IDEXX reported nearly 700 pre-orders for the inVue Dx Cellular Analyzer, underscoring a strong appetite for point-of-care cytology.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the veterinary equipment and disposables market as all new, factory-built medical devices, ranging from patient monitors and anesthesia machines to single-use syringes, catheters, drapes, and wound dressings, supplied to licensed animal-health practitioners worldwide. The value reflects direct manufacturer invoice prices, net of intra-company transfers, for companion and livestock animal care across clinics, hospitals, academia, and mobile services.

Scope Exclusion: second-hand or rental units, feed additives, and pharma therapeutics remain outside the present valuation.

Segmentation Overview

- By Product Type

- Equipment

- Therapeutic Equipment

- Diagnostic Imaging

- Anesthesia Machines

- Patient Monitoring

- Dental Equipment

- Disposables

- Syringes & Needles

- Infusion & Transfusion Sets

- Catheters

- Wound Dressings & Bandages

- Surgical Drapes & Gowns

- Equipment

- By Animal Type

- Companion Animals

- Dogs

- Cats

- Horses

- Others

- Livestock Animals

- Cattle

- Swine

- Poultry

- Others

- Companion Animals

- By End User

- Veterinary Clinics

- Veterinary Hospitals

- Academic & Research Institutes

- Mobile/ Ambulatory Services

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with practicing veterinarians, clinic procurement heads, and regional distributors across North America, Europe, and Asia-Pacific to validate surgical volumes, gauge disposable burn rates, and test price elasticity assumptions. Follow-up surveys with farm animal practitioners in Brazil and India filled gaps on bulk infusion sets and monitoring kit turnover that seldom surface in public data.

Desk Research

We began by mapping global pet and herd demographics using sources such as the USDA-APHIS animal census, Eurostat livestock databases, and FAO trade dashboards, which give baseline procedure volumes. Regulatory filings from the FDA-CVM, EMA, and Australia's TGA clarified device clearance pipelines that influence installed-base refresh rates. Company 10-Ks, selected veterinary association fee schedules, and open-access journals (Journal of Veterinary Internal Medicine, Frontiers in Veterinary Science) supplied utilization multipliers and average selling prices. Subscription resources, D&B Hoovers for producer financials and Dow Jones Factiva for shipment news, helped cross-verify revenue splits. This list is illustrative; numerous additional records supported data gathering and sense-checking.

Secondarily, macro inputs such as pet insurance penetration, OECD consumer spend indices, and customs HS code flows were captured to anchor regional demand curves, while Mindray and Midmark patent filings from Questel hinted at technology adoption lags.

Market-Sizing & Forecasting

A top-down build converts recorded veterinary visit volumes into addressable procedure pools, followed by prevalence-to-treated-cohort adjustments. Results are then weighed against selective bottom-up roll-ups of leading supplier revenues and sampled ASP × unit checks, allowing us to fine-tune overlaps. Key variables in our model include 1) annual companion-animal clinic visits, 2) elective surgery incidence, 3) median price of multiparameter monitors, 4) pet insurance claim frequency, 5) livestock disease-screening mandates, and 6) regional currency shifts. Five-year forecasts apply multivariate regression blended with scenario analysis to reflect shifts in insurance uptake and biosecurity rules. Data voids, for example, Asia-Pacific clinic counts, are bridged using growth proxies from veterinary council registration rolls before being re-benchmarked.

Data Validation & Update Cycle

We perform layered variance checks, peer reviews, and anomaly flags between modeled outputs and external signposts such as import value trends or clinic capital budgets. Reports refresh each year, with interim revisions triggered by material recalls, pandemics, or major regulatory approvals, ensuring buyers receive recently validated numbers.

Why Mordor's Veterinary Equipment And Disposables Baseline Commands Credibility

Published market values often diverge because firms pick different device baskets, discount structures, and refresh cadences.

Primary gap drivers include whether disposables tied to imaging are counted, if rental income is embedded, how companion versus livestock demand is split, conversion year for local currencies, and the rigor of primary verification.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| $2.96 B (2025) | Mordor Intelligence | - |

| $3.50 B (2024) | Global Consultancy A | folds rental and service revenue into equipment totals and lacks separate companion-animal calibration |

| $2.70 B (2024) | Trade Journal B | omits anesthesia systems and models only five macro regions without clinic-level primary checks |

Taken together, the comparison shows that while other publishers swing wider on scope or skip validation loops, Mordor's disciplined mix of verified procedure counts, dual-approach modeling, and annual refresh delivers a balanced, transparent baseline stakeholders can retrace and trust.

Key Questions Answered in the Report

What is the size of the veterinary equipment and disposables market in 2026?

The market stands at USD 3.17 billion in 2026 and is projected to reach USD 4.48 billion by 2031 at a 7.15% CAGR.

Which product category holds the largest share of revenue?

Equipment dominates with 64.02% share in 2025, driven by imaging, anesthesia, and surgical systems.

Why is Asia-Pacific the fastest-growing region?

Rapid pet hospital expansion, consolidation opportunities in China, and livestock modernization across India and Southeast Asia push the region to a 9.12% CAGR.

How are mobile veterinary clinics influencing equipment design?

Their 8.61% CAGR growth fuels demand for lightweight, battery-operated analyzers, wireless imaging probes, and cloud-connected tools that work in non-clinical environments.

What barriers limit adoption of high-end imaging suites?

Upfront costs exceeding USD 21,000 for digital X-ray and a shortage of radiologists who can interpret scans curb uptake, especially in emerging markets.

What years does this Veterinary Equipment And Disposables Market cover, and what was the market size in 2025?

In 2025, the Veterinary Equipment And Disposables Market size was estimated at USD 3.17 billion.

Page last updated on: