Veterinary Orthopedic Implants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 378.11 Million |

| Market Size (2031) | USD 554.28 Million |

| Growth Rate (2026 - 2031) | 7.95% CAGR |

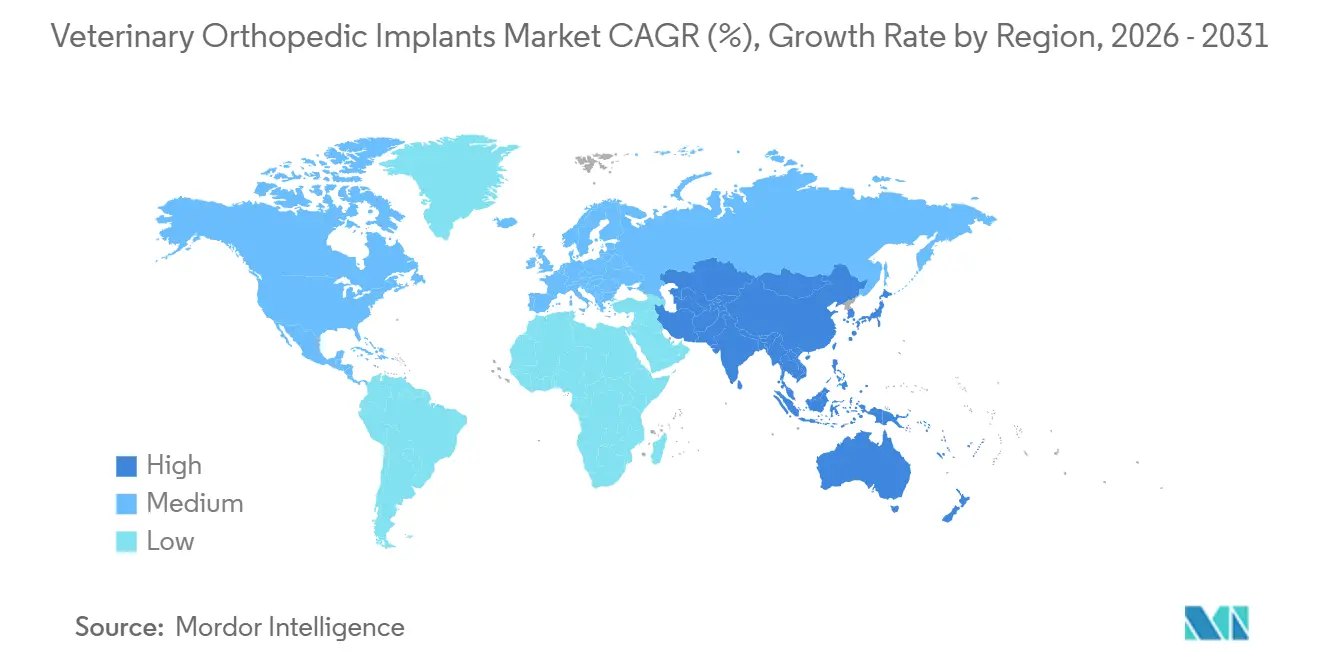

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

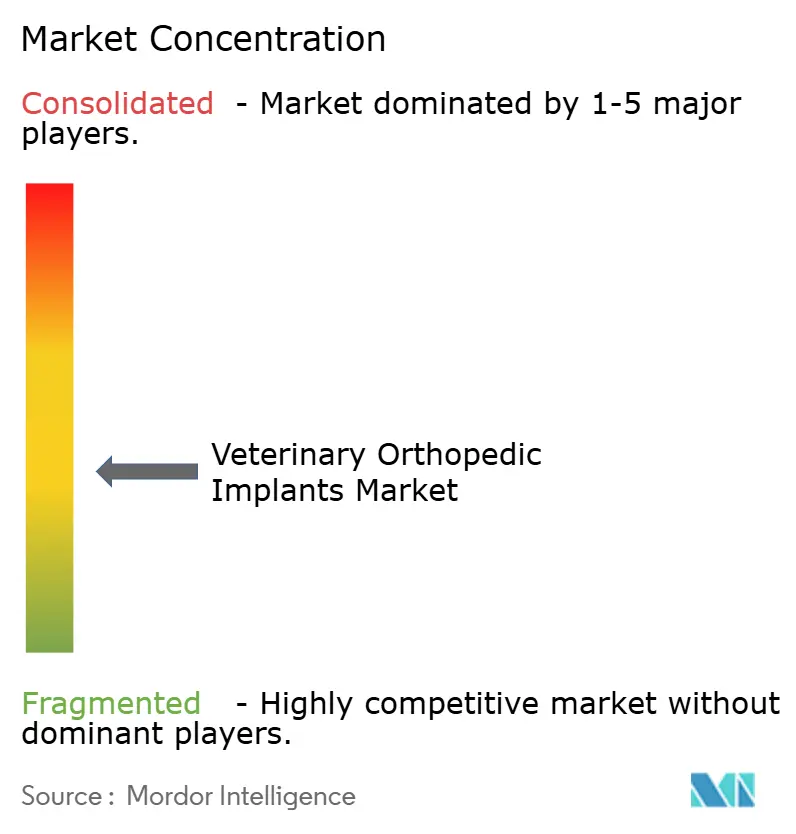

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Orthopedic Implants Market Analysis by Mordor Intelligence

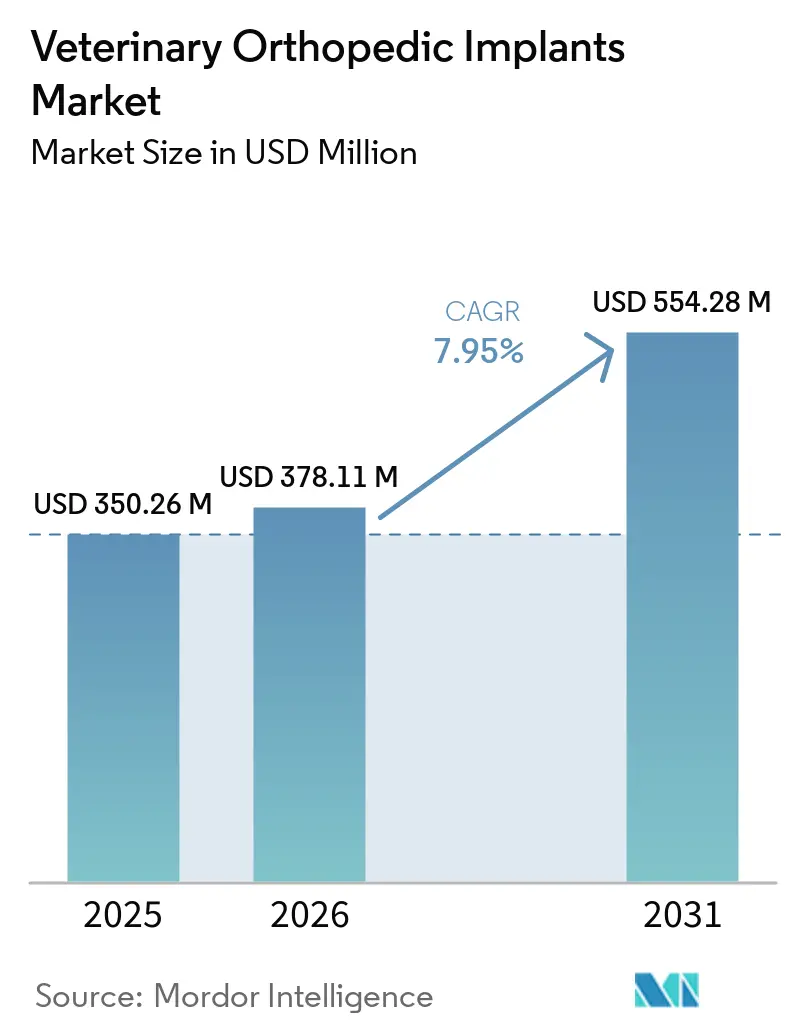

The Veterinary Orthopedic Implants Market size was valued at USD 350.26 million in 2025 and is estimated to grow from USD 378.11 million in 2026 to reach USD 554.28 million by 2031, at a CAGR of 7.95% during the forecast period (2026-2031).

A larger companion animal base is widening the addressable procedure pool, with the American Veterinary Medical Association reporting 87.3 million dogs in the United States and owned cats rising from 58.3 million to 76.3 million over the same period, which supports a broader case base for musculoskeletal care. Pet spending also continues to support procedure demand, with the American Pet Products Association stating that U.S. pet industry expenditures reached USD 158 billion in 2025 and are projected at USD 165 billion in 2026, with veterinary services taking the fastest-growing share. The Veterinary orthopedic implants market is also benefiting from the steady transfer of locking-plate systems, cannulated screws, and patient-specific additive manufacturing from human orthopedics into veterinary practice, which raises the treatment threshold for cases that once remained untreated. Referral expansion, surgeon training, and broader reimbursement support are converting latent biological need into treated volume, which gives the Veterinary orthopedic implants market a wider and more durable demand base. Competition is becoming harder for smaller suppliers as larger platforms pair implants with education, workflow support, and premium outcome positioning, which is raising switching costs across the Veterinary orthopedic implants market.

Key Report Takeaways

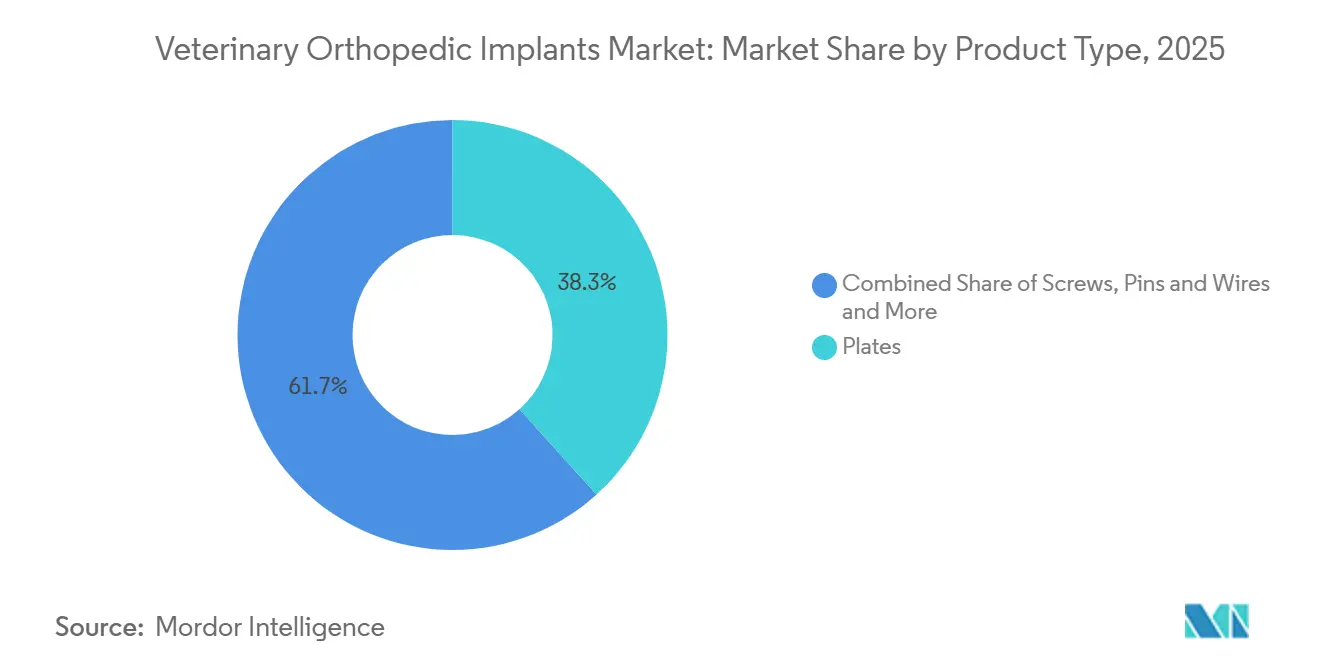

- By product type, plates accounted for 38.31% of revenue in 2025, while screws are projected to expand at a 10.38% CAGR through 2031.

- By animal type, dogs held 67.24% of revenue in 2025, while cats are expected to grow at a CAGR at 9.52% through 2031.

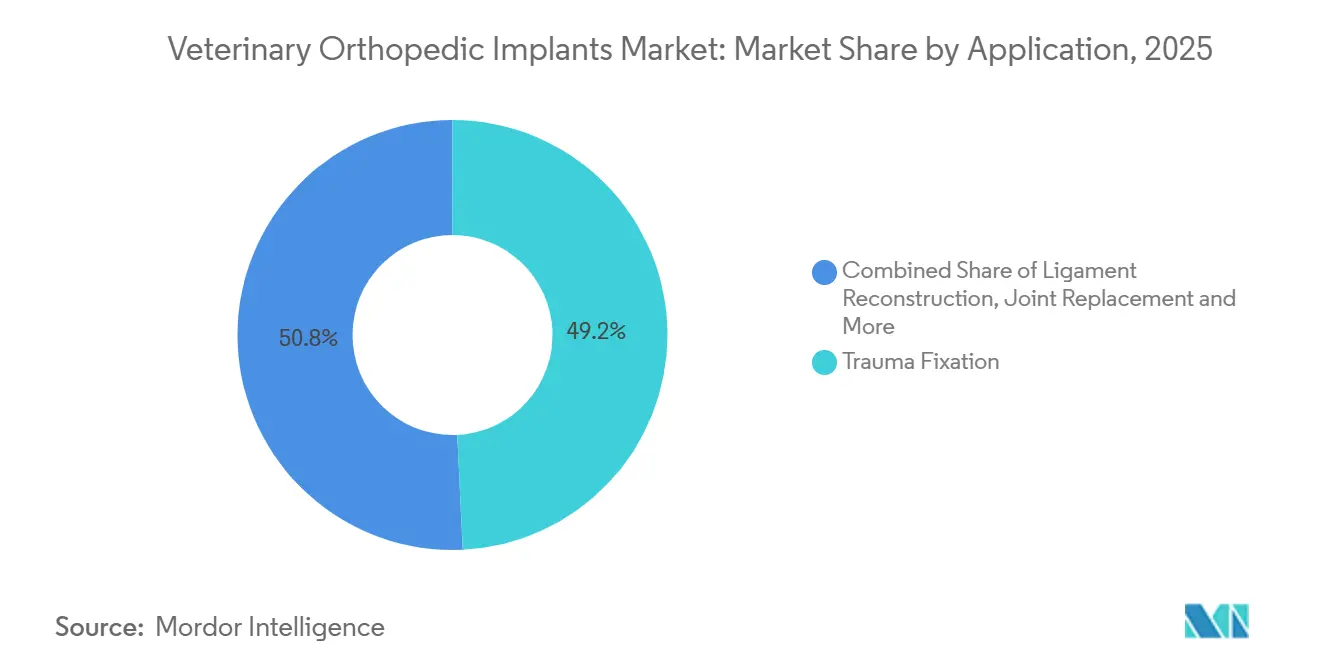

- By application, trauma fixation represented 49.24% of revenue in 2025, while ligament reconstruction is expected to advance at a 9.52% CAGR through 2031.

- By end user, veterinary hospitals captured 60.56% of revenue in 2025, while veterinary surgical centers are expected to grow at an 8.85% CAGR through 2031.

- By material, titanium commanded 78.52% of revenue in 2025, while bioabsorbable polymers are forecast to expand at a 10.25% CAGR through 2031.

- By geography, North America held 41.22% of revenue in 2025, while Asia-Pacific is expected to grow at a 9.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Veterinary Orthopedic Implants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Companion Animal Orthopedic Caseload | +2.5% | Global | Short term (≤ 2 years) |

| Expansion Of Referral-Grade Surgical Capability | +1.8% | North America and Europe, spill-over to APAC | Medium term (2-4 years) |

| 3D Printed Patient-Specific Implants And Guides | +1.2% | North America, Europe, APAC core | Medium term (2-4 years) |

| Growth In Pet Insurance Reimbursement For Orthopedic Care | +1.0% | North America and UK, early gains in Germany, France, Australia | Medium term (2-4 years) |

| Standardization Of Minimally Invasive TPLO And TTA Surgical Protocols | +0.8% | Global, highest concentration in North America and Western Europe | Short term (≤ 2 years) |

| Cross-Border Sourcing Of Veterinary-Grade Implant Systems | +0.7% | APAC, South America, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Companion Animal Orthopedic Caseload

The Veterinary orthopedic implants market is being lifted by a larger companion animal population and by longer pet lifespans that increase the incidence of degenerative musculoskeletal disease. The American Veterinary Medical Association reported that 58.6% of U.S. households owned a pet in 2025, up from 56.8% a decade earlier, and the dog-owning base reached 71 million U.S. households in 2025 after a net addition of 4 million households in 1 year. The same structural expansion matters clinically because a larger household base does not just mean more pets, it also means more animals reaching ages where cruciate disease, dysplasia, and age-related fracture risk become more common.

The Veterinary orthopedic implants market also benefits from the fact that improved routine veterinary care is keeping dogs and cats alive longer, which raises the probability of later-life fixation and reconstruction procedures over each animal’s lifetime. This demand is especially concentrated in medium-to-large breed dogs, where cranial cruciate ligament disease and hip dysplasia continue to generate a high share of elective orthopedic referrals. As the case load expands faster than specialist capacity in several regions, the Veterinary orthopedic implants market is favoring standardized systems that shorten decision time and help surgeons move through a larger caseload with more predictable technique selection.

Expansion Of Referral-Grade Surgical Capability

The Veterinary orthopedic implants market is also advancing because more referral-grade capability is reaching secondary cities and suburban catchments that previously sent many orthopedic cases untreated or managed conservatively. Vimian Group stated in its 2024 Annual Report that only 1 in 3 dogs requiring cruciate ligament surgery currently receives the procedure, which shows that access expansion still has room to convert unmet need into active procedural demand. The same report noted that Movora trained 5,150 veterinary professionals through on-site surgery workshops and supported nearly 4,000 online learners in 2024, which shows how training is being used as a commercial growth tool as well as a clinical enabler[1]Vimian Group AB, “Annual Report 2024,” Vimian Group AB, storage.mfn.se. This education model matters because surgeons who learn standardized methods at referral centers often carry those methods into general or mixed specialty settings, which gradually widens the treated population.

The Veterinary orthopedic implants market gains from that diffusion because it expands the installed base of surgeons comfortable with premium plate, screw, and procedure-specific systems. It also creates lasting vendor preference, since implant design, instrumentation, and training tend to be adopted together rather than as separate buying decisions.

3D Printed Patient-Specific Implants And Guides

Additive manufacturing is changing the value proposition in the Veterinary orthopedic implants market by allowing implants and guides to be matched more closely to individual anatomy and surgical goals. A case series published in Frontiers in Veterinary Science in April 2025 reported that 3D-printed surgical guides and patient-specific external fixator frames reduced operating room time by 1 hour per complex corrective osteotomy case in canine patients, which directly lowers anesthesia burden and operating room pressure. That time saving matters because complex corrective work is often limited not only by implant cost but also by the surgeon time and planning burden required to execute it well.

Research in Frontiers in Bioengineering and Biotechnology also showed that laser powder bed fusion titanium scaffolds supported strong cortico-cancellous osseointegration in a load-bearing ovine femoral model, which strengthens the mechanical case for 3D-printed titanium in demanding reconstructive settings. The Veterinary orthopedic implants market is therefore moving toward a point where patient-specific capability is becoming a practical expectation for advanced surgeons rather than a rare premium add-on. This is raising the bar for suppliers, since vendors now need planning support, design speed, and manufacturing reliability in addition to standard implant quality.

Growth In Pet Insurance Reimbursement For Orthopedic Care

The Veterinary orthopedic implants market is gaining support from wider pet insurance coverage because orthopedic procedures sit among the costliest and most predictable categories of veterinary claims. NAPHIA stated that the U.S. pet insurance market generated USD 4.7 billion in gross written premium in 2024 and projected that it would exceed USD 6 billion by the end of 2026, which points to a larger reimbursable base for high-value surgery. NAPHIA also reported that U.S. penetration stood at 3.9% of the total pet population at year-end 2024, with 5.5% for dogs and 2.0% for cats, which shows that the reimbursement base is still small relative to its long-term room for expansion.

Trupanion reported in Q1 2026 that subscription revenue rose 16% year over year to USD 269.5 million and enrolled pets reached 1.105 million, which confirms continued momentum in the insured population. NAPHIA’s orthopedic procedure benchmarks show TPLO surgery at USD 4,000 to USD 8,000 per procedure and orthopedic surgery for ACL and hip conditions at USD 3,000 to USD 7,000, so reimbursement materially changes owner approval behavior in a category where sticker shock is a major barrier[2]North American Pet Health Insurance Association, “2025 Pet Insurance Industry Annual Statistics Report,” North American Pet Health Insurance Association, naphia.org. As more policies cover these expenses, the Veterinary orthopedic implants market is likely to see stronger demand for premium systems that owners might otherwise decline in self-pay settings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Procedure Cost Relative To The Perceived Economic Value Of The Animal | -1.5% | Global, concentrated in price-sensitive segments of North America, South America, MEA | Long term (≥ 4 years) |

| Limited Specialist Surgeon Availability Outside Major Metropolitan Centres | -1.0% | Global, most acute in rural North America, APAC periphery, MEA | Long term (≥ 4 years) |

| Fragmented And Inconsistent Reimbursement For Veterinary Orthopedic Procedures | -0.8% | North America, Western Europe | Medium term (2-4 years) |

| Import Tariffs And Metal Input Price Volatility Affecting Implant Manufacturing Costs | -0.6% | North America, APAC-sourcing manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Procedure Cost Versus Animal Economic Value

Procedure affordability remains one of the clearest limits on the Veterinary orthopedic implants market because common orthopedic surgeries often cost far more than many owners are prepared to spend without reimbursement support. NAPHIA’s benchmark ranges place TPLO surgery at USD 4,000 to USD 8,000 and orthopedic surgery for ACL and hip conditions at USD 3,000 to USD 7,000, which keeps a large part of demand exposed to out-of-pocket resistance. This cost pressure is sharper in lower-income settings and in cases where owners compare treatment expense with the perceived economic value of the animal, especially outside affluent urban companion animal markets. Vimian Group’s 2024 Annual Report estimated that only 1 in 3 dogs requiring cruciate surgery currently receives treatment, which shows how far realized procedure volume still sits below biological need.

The Veterinary orthopedic implants market therefore loses volume not because clinical solutions are absent, but because owner approval breaks down at the point where benefit, cost, and emotional value are weighed together. Suppliers and hospitals that offer tiered treatment pathways or work more closely with insurers are better placed to unlock that deferred demand without forcing a broad move down the pricing curve.

Limited Specialist Surgeon Availability Outside Major Cities

The Veterinary orthopedic implants market also faces a structural access problem because specialist orthopedic surgeons remain concentrated in metropolitan referral clusters rather than spread evenly across demand centers. The USDA identified 243 rural veterinary shortage areas across 46 U.S. states in 2025 and launched a Rural Veterinary Action Plan in August 2025 that included USD 15 million for its Veterinary Medicine Loan Repayment Program, which shows the scale of geographic workforce imbalance. While that shortage is most visible in food-animal practice, the same geographic concentration affects advanced companion animal surgery because complex orthopedic care is still clustered in urban and suburban referral hospitals. This means many owners remain outside a practical referral radius for procedures that require dedicated imaging, anesthesia support, and surgeon experience. Digital education, telemedicine-assisted planning, and regional wet-lab models are helping the Veterinary orthopedic implants market improve capability, but they do not fully solve the physical access gap in dispersed geographies. Until specialist density broadens, a meaningful share of orthopedic demand will continue to be delayed, redirected, or lost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Screws Outpace Plates as Minimally Invasive Demand Intensifies

Plates accounted for 38.31% of revenue in 2025, giving them the leading position across product categories in the Veterinary orthopedic implants market. Their lead reflects broad utility across fracture fixation, corrective osteotomy, and tibial realignment, where surgeons need predictable fixation across many case types. Locking compression plates and TPLO-specific plate designs continue to anchor a large share of this revenue because they align with procedure standardization and support stable fixation in high-volume canine cases. Within the Veterinary orthopedic implants industry, plates remain the foundational inventory line for hospitals and referral surgeons because they support both routine trauma and more advanced reconstructive work. That installed-base advantage matters because once a team is trained around a plate family and its instrumentation, purchasing behavior tends to remain sticky.

Screws are projected to grow at a 10.38% CAGR through 2031, making them the fastest-growing product type in the Veterinary orthopedic implants market. Demand is being lifted by locking and cannulated variants that fit minimally invasive TPLO and TTA workflows and support lower-profile fixation in increasingly standardized procedures. Surgeons also value screws for their compatibility with closed-reduction methods, which can reduce periosteal disruption and support faster bone consolidation in selected cases. A 2026 study in Veterinary and Comparative Orthopaedics and Traumatology found meaningful variability in tibial plateau angle maintenance and bone healing outcomes when a 3.5 mm TPLO locking compression plate was used in dogs weighing 45 to 70 kg, which underlines the engineering challenge of adapting standard hardware across large-breed anatomy. Beyond the leading lines, pins and wires still hold an important role in small-animal fracture management, while joint replacement implants sit in a premium, lower-volume tier that grows as specialist capability matures.

By Animal Type: Canine Caseloads Dominate but Feline Orthopedics Emerges as Strategic Growth Segment

Dogs contributed 67.24% of revenue by animal type in 2025, which makes them the core demand driver in the Veterinary orthopedic implants market. That dominance is tied to the size of the canine patient pool and to the high orthopedic burden seen in medium-to-large breeds prone to cruciate ligament disease, hip dysplasia, and trauma-related fractures. Dog cases also tend to produce more revenue per treated animal because they more often involve high-value stabilization or reconstruction procedures rather than purely conservative management. The American Veterinary Medical Association reported a U.S. dog population of 87.3 million, which reinforces why the canine base remains the commercial center of the Veterinary orthopedic implants market. Within the Veterinary orthopedic implants industry, canine procedure volume continues to shape product development, training priorities, and inventory planning across almost every major supplier.

Cats are expected to record the fastest CAGR at 9.52% through 2031, which gives feline orthopedics the strongest growth profile among animal types. The American Pet Products Association reported a 23% increase in cat ownership in 2024, and that household shift is widening the patient base for feline fracture repair, stifle stabilization, and patellar luxation treatment. The American Veterinary Medical Association also showed owned cat numbers rising from 58.3 million to 76.3 million, which points to a larger and younger pool of future orthopedic candidates. Growth is also being helped by stronger owner willingness to authorize elective orthopedic work for cats, a category that historically lagged dogs in both recognition and treatment rates. Most current feline implants still adapt canine systems rather than fully purpose-built feline designs, which leaves a clear product gap for companies able to miniaturize without compromising biomechanical stability.

By Material Type: Titanium's Dominance Persists While Bioabsorbable Polymers Open New Clinical Frontiers

Titanium held 78.52% of revenue by material in 2025, which kept it firmly in the lead across the Veterinary orthopedic implants market size. Surgeons continue to favor titanium because it combines biocompatibility, corrosion resistance, osseointegration potential, and high load-bearing strength in a way few alternatives can match across routine and advanced applications. Titanium also aligns well with additive manufacturing, which makes it central to the current move toward patient-specific planning and custom implant design. Research published in Frontiers in Bioengineering and Biotechnology in 2024 found that additively manufactured titanium implants supported robust cortico-cancellous osseointegration in a load-bearing large-animal model, which validates the material’s value in demanding reconstructive settings. This keeps titanium at the center of the Veterinary orthopedic implants market when surgeons prioritize longevity, stability, and premium clinical performance.

Bioabsorbable polymers are projected to grow at a 10.25% CAGR through 2031, which gives them the fastest growth profile among material types. Their appeal is strongest in temporary fixation, pediatric or small-animal cases, and scaffold uses where implant removal would otherwise require a second procedure. A 2025 article indexed in PMC reviewed advances in biodegradable implants in large-animal surgical models, while a 2026 study in the Journal of Polymers and the Environment described 4D-printed polymer devices with programmable self-positioning behavior for personalized arthrodesis, together showing an active innovation pipeline around degradable fixation concepts. At the same time, the FDA’s January 2024 draft guidance on metallic and calcium phosphate coatings on orthopedic devices shows that surface and material characterization standards are becoming more demanding for new submissions. That raises development work for novel systems, but it also supports higher quality thresholds for future entrants into the Veterinary orthopedic implants market. Stainless steel still retains a meaningful role in price-sensitive settings where lower unit cost and broad fabrication availability remain decisive.

By Application: Trauma Fixation Anchors Revenue While Ligament Reconstruction Accelerates

Trauma fixation accounted for 49.24% of revenue in 2025, giving it the largest application position within the Veterinary orthopedic implants market size. This application remains the broadest commercial base because it covers fractures from high-activity injuries, road incidents, and degenerative conditions that require osteotomy or mechanical stabilization. It is also the most common entry point for both general practices and referral facilities, which is why many implant portfolios are built around trauma systems first and specialized lines second. In the Veterinary orthopedic implants industry, trauma fixation supports steady purchasing because the indication set is wide and the instrument familiarity is high across practice types. That makes it the segment that most directly anchors baseline utilization even when more specialized elective procedures fluctuate.

Ligament reconstruction is expected to grow at a 9.52% CAGR through 2031, making it the fastest-growing application in the Veterinary orthopedic implants market. Growth is being driven mainly by wider use of TPLO and TTA in canine cranial cruciate ligament disease, one of the most common and expensive orthopedic conditions seen in dogs. A 2025 review in Animals described TTA as a less invasive alternative to TPLO across different dog sizes, which supports continuing uptake as surgeons balance stability, recovery profile, and procedural familiarity. A 2026 pilot study in Frontiers in Veterinary Science on porous titanium TTA without flange also reported procedural feasibility and early biological integration findings, which supports further normalization of the technique in real-world use. Joint replacement remains a premium application with strong strategic value, while osteoarthritis-related implant intervention is set to widen as companion animals live longer and owners accept more advanced care pathways.

By End User: Veterinary Surgical Centers Gain Ground on Hospitals in the Race for Complex Procedures

Veterinary hospitals held 60.56% of revenue in 2025, which kept them as the leading end-user setting in the Veterinary orthopedic implants market size. Their lead reflects access to advanced imaging, intensive care support, and multidisciplinary teams that are often needed for total joint replacement, corrective osteotomy, and complex trauma repair. Hospitals also remain the default setting for referral inflow because they can absorb case complexity, perioperative monitoring, and longer post-surgical observation. In the Veterinary orthopedic implants market, this makes hospitals the anchor buyers for broad implant portfolios that cover trauma, ligament work, and reconstructive procedures. Their purchasing behavior still sets the tone for premium adoption in many countries because surgeon preference, training, and case volume are concentrated in these environments.

Veterinary surgical centers are projected to grow at an 8.85% CAGR through 2031, which makes them the fastest-growing end-user channel in the Veterinary orthopedic implants market. Growth is being driven by stand-alone specialty facilities that attract board-certified surgeons seeking greater procedural focus and less operational complexity than full-service hospitals. Vimian reported that Movora trained 5,150 veterinary professionals on site and supported nearly 4,000 online learners in 2024, and that education-led model helps spread capability into surgical-center settings as much as into academic hospitals. Veterinary clinics continue to serve the middle of the channel mix by managing routine fracture repair and lower-complexity fixation cases with standardized systems. For suppliers competing below the largest referral hospitals, surgical centers represent an attractive account type because they can deliver high procedure volume per facility with a tighter focus on orthopedics.

Geography Analysis

North America held 41.22% of revenue in 2025, which gave it the leading regional position in the Veterinary orthopedic implants market share. The region benefits from high pet healthcare spending, dense specialist referral networks, and a large insured companion animal base that supports acceptance of high-value surgery. NAPHIA reported USD 4.7 billion in U.S. pet insurance gross written premium in 2024 and projected more than USD 6 billion by the end of 2026, which gives North America a strong reimbursement tailwind for orthopedic procedures. APPA also reported U.S. pet industry expenditures of USD 158 billion in 2025 and USD 165 billion in 2026, with veterinary services capturing the fastest-growing share, which reinforces the region’s spending depth[3]American Pet Products Association, “U.S. Pet Industry Reaches USD 158 Billion in 2025, Poised for Continued Growth in 2026,” American Pet Products Association, americanpetproducts.org. Europe remains the second-largest regional block, while South America is smaller and still constrained by affordability and specialist availability even as urban pet ownership rises.

Europe’s position in the Veterinary orthopedic implants market rests on mature referral pathways and a tighter regulatory environment that increasingly rewards established quality systems. The EU Medical Device Regulation is raising expectations around biocompatibility documentation and post-market surveillance for implants traded across member states, which creates a higher compliance burden for smaller producers and a stronger moat for better-resourced suppliers. The region also benefits from strong veterinary surgery ecosystems in Germany, the United Kingdom, France, and Switzerland, where surgeon-led product development and structured referral channels support premium fixation and reconstruction demand. This makes Europe a market where procedural sophistication and regulatory discipline move together rather than in separate tracks.

Asia-Pacific is projected to expand at a 9.65% CAGR through 2031, giving it the fastest growth profile in the Veterinary orthopedic implants market size. China, Japan, India, Australia, and South Korea remain the core demand centers because they combine rising companion animal spending with ongoing investment in veterinary hospitals and specialist education. Urbanization and middle-class expansion are widening acceptance of advanced orthopedic care, especially in companion animal segments where owners are increasingly willing to pay for mobility-restoring procedures. The Middle East and Africa are developing from a smaller base, but GCC countries are building higher-end hospital capacity around equine medicine and premium pet ownership. India also stands out as a dual opportunity because it offers both expanding domestic demand for affordable fixation systems and a manufacturing base that can support export-oriented supply into neighboring regions.

Competitive Landscape

The Veterinary orthopedic implants market remains moderately fragmented, with no single supplier holding a dominant position across all product lines and geographies. The leading competitive set includes diversified platforms and veterinary-focused specialists, and the balance of power is shaped as much by training reach and procedural support as by raw catalog breadth. Vimian Group, through Movora, has built strong positioning by combining implants with an education ecosystem that trained 5,150 professionals on site and reached nearly 4,000 online learners in 2024. Johnson & Johnson announced in October 2025 that it intends to separate its orthopaedics business, a step that could sharpen focus on adjacency opportunities connected to premium fixation and reconstruction. The Veterinary orthopedic implants market is therefore seeing competition move away from simple product overlap and toward platform strength, surgeon familiarity, and procedural confidence.

Education-led adoption is now one of the clearest competitive levers in the Veterinary orthopedic implants market. Arthrex Vet Systems launched the OrthoPedia Vet digital education platform in February 2026, which supports procedure learning and keeps surgeons inside its implant ecosystem as case complexity rises. In March 2026, Arthrex Vet Systems also launched the OrthoLine Acetabular Plates system, which expanded its veterinary-specific trauma offering for complex pelvic reconstruction. These kinds of moves matter because advanced orthopedic purchasing often follows training pathways, instrumentation familiarity, and outcome trust rather than unit price alone. As a result, companies that support both the implant and the technique are better placed to defend accounts over time.

Technology is the other major source of differentiation in the Veterinary orthopedic implants market, especially in patient-specific titanium implants, surgical guides, bioabsorbable systems, and soft-tissue fixation. Arthrex announced in February 2026 the release of its TightRope SB all-suture implant for ACL fixation, and the company reported nearly 2,000 early U.S. uses, which shows how quickly a targeted innovation can scale when it matches established procedural need. White-space opportunities still exist in feline-specific implant design, where many products remain scaled-down canine systems rather than anatomy-specific solutions. Regulatory expectations are also becoming more relevant to competitive positioning, with the FDA classifying manual surgical instruments for appropriate patient selection for orthopedic implants as Class II in April 2026, which adds structure to device pathways connected to orthopedic workflows. Together, these forces are pushing the Veterinary orthopedic implants market toward higher development standards and a more defensible premium tier for companies that pair engineering with evidence and training.

Veterinary Orthopedic Implants Industry Leaders

BioMedtrix LLC

Movora

B. Braun Vet Care GmbH

Orthomed (UK) Ltd.

DePuy Synthes (Johnson & Johnson)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Arthrex Vet Systems launched the OrthoLine Acetabular Plates system, a pre-contoured plating platform designed for three key acetabular fracture types in companion animals. This launch enhances Arthrex's veterinary pelvic trauma offerings, addressing a gap in complex reconstructions that previously relied on adapted human implant systems.

- July 2025: Movora, a global player in veterinary orthopedic solutions, partnered with the AO Foundation, known for its expertise in medical education and innovation. They have signed a Memorandum of Understanding (MoU) to enhance veterinary education.

Global Veterinary Orthopedic Implants Market Report Scope

As per the scope of the report, veterinary orthopedic implants are medical devices designed specifically for use in animals to stabilize, support, or replace damaged or diseased bones and joints. They are used in veterinary medicine to treat conditions such as fractures, joint instability, or deformities, facilitating proper healing and restoring mobility in animals.

The segmentation of the veterinary orthopedic implants market is categorized by product type, animal type, material type, application, end user, and geography. By product type, the market includes plates (locking compression plates, locking distal plates, dynamic compression plates, reconstruction plates, TPLO plates, and TTA plates), screws (bone screws, cortical screws, cancellous screws, locking screws, and cannulated screws), pins and wires (intramedullary pins and Kirschner wires), implants for total elbow replacement, total hip replacement, and total knee replacement, fixation systems, and other product types. By animal type, the market is segmented into dogs, cats, horses, and other animals. By material type, the categories include titanium, stainless steel, bioabsorbable polymers, and other materials. By application, the market is divided into trauma fixation, joint replacement, ligament reconstruction, osteoarthritis management, and other applications. By end user, the segmentation includes veterinary hospitals, veterinary clinics, veterinary surgical centers, and other end users. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Plates | Locking Compression Plates |

| Locking Distal Plates | |

| Dynamic Compression Plates | |

| Reconstruction Plates | |

| TPLO Plates | |

| TTA Plates | |

| Screws | Bone Screws |

| Cortical Screws | |

| Cancellous Screws | |

| Locking Screws | |

| Cannulated Screws | |

| Pins and Wires | Intramedullary Pins |

| Kirschner Wires | |

| Total Elbow Replacement Implants | |

| Total Hip Replacement Implants | |

| Total Knee Replacement Implants | |

| Fixation Systems | |

| Other Product Types |

| Dog |

| Cat |

| Horses |

| Other Animals |

| Titanium |

| Stainless Steel |

| Bioabsorbable Polymers |

| Other Materials |

| Trauma Fixation |

| Joint Replacement |

| Ligament Reconstruction |

| Osteoarthritis Management |

| Other Applications |

| Veterinary Hospitals |

| Veterinary Clinics |

| Veterinary Surgical Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Plates | Locking Compression Plates |

| Locking Distal Plates | ||

| Dynamic Compression Plates | ||

| Reconstruction Plates | ||

| TPLO Plates | ||

| TTA Plates | ||

| Screws | Bone Screws | |

| Cortical Screws | ||

| Cancellous Screws | ||

| Locking Screws | ||

| Cannulated Screws | ||

| Pins and Wires | Intramedullary Pins | |

| Kirschner Wires | ||

| Total Elbow Replacement Implants | ||

| Total Hip Replacement Implants | ||

| Total Knee Replacement Implants | ||

| Fixation Systems | ||

| Other Product Types | ||

| By Animal Type | Dog | |

| Cat | ||

| Horses | ||

| Other Animals | ||

| By Material Type | Titanium | |

| Stainless Steel | ||

| Bioabsorbable Polymers | ||

| Other Materials | ||

| By Application | Trauma Fixation | |

| Joint Replacement | ||

| Ligament Reconstruction | ||

| Osteoarthritis Management | ||

| Other Applications | ||

| By End User | Veterinary Hospitals | |

| Veterinary Clinics | ||

| Veterinary Surgical Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the Veterinary orthopedic implants market?

The Veterinary orthopedic implants market is generating USD 378.11 million in 2026 and is projected to reach USD 554.28 million by 2031 at a 7.95% CAGR.

Which product category leads revenue in veterinary orthopedic implants?

Plates lead product revenue with a 38.31% share in 2025 because they are used widely in fracture fixation, corrective osteotomy, and tibial realignment.

Which product segment is growing the fastest through 2031?

Screws are the fastest-growing product type with a 10.38% CAGR through 2031, helped by demand for locking and cannulated variants used in minimally invasive TPLO and TTA procedures.

Why do dogs account for most orthopedic implant procedures?

Dogs held 67.24% of revenue in 2025 because the canine caseload is larger and includes many medium-to-large breeds with cruciate disease, hip dysplasia, and trauma-related injuries.

Which region is growing the fastest for veterinary orthopedic implants?

Asia-Pacific is the fastest-growing region with a 9.65% CAGR through 2031, supported by urbanization, rising companion animal spending, and expanding veterinary infrastructure.

What is driving demand for advanced orthopedic procedures in pets?

The main drivers are larger pet populations, longer lifespans, stronger referral capacity, wider insurance reimbursement, and growing use of patient-specific and minimally invasive orthopedic solutions.

Page last updated on: