Veterinary Wound Cleansers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

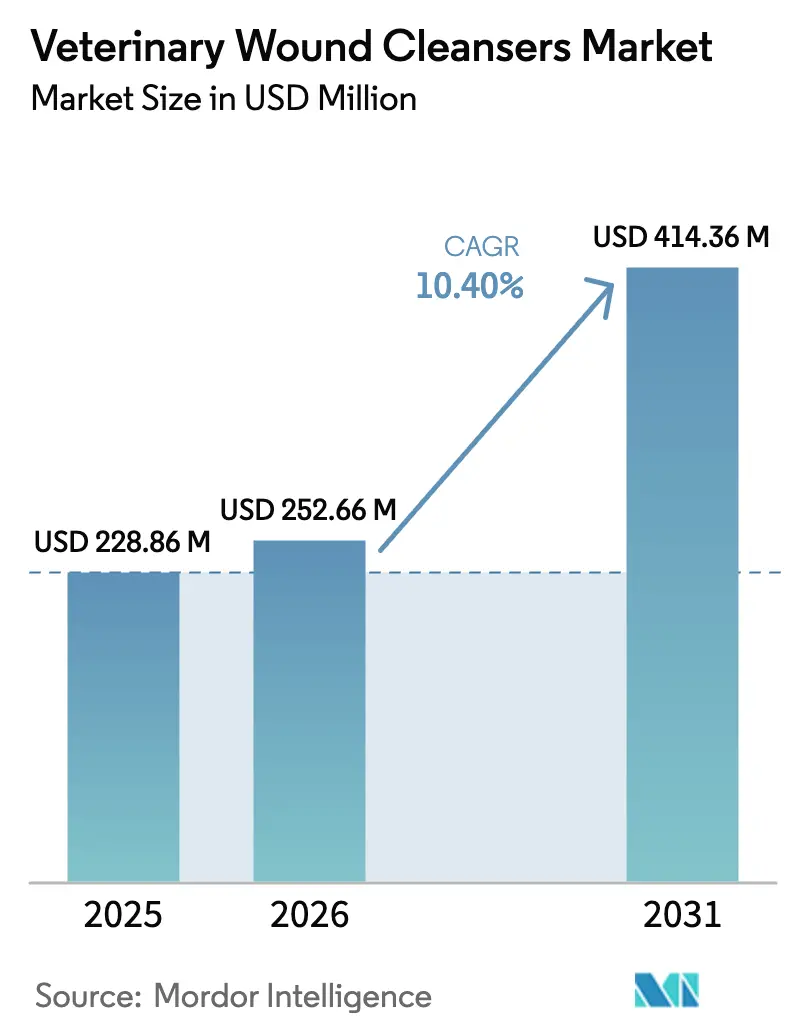

| Market Size (2026) | USD 252.66 Million |

| Market Size (2031) | USD 414.36 Million |

| Growth Rate (2026 - 2031) | 10.40% CAGR |

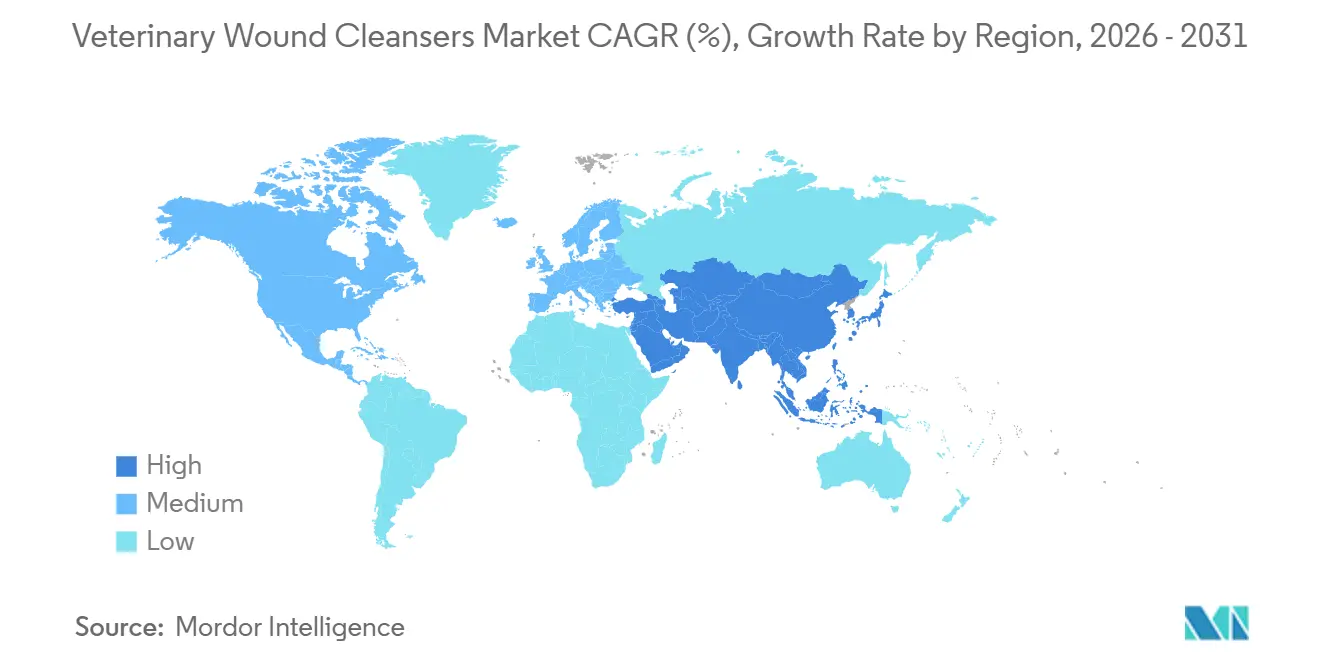

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

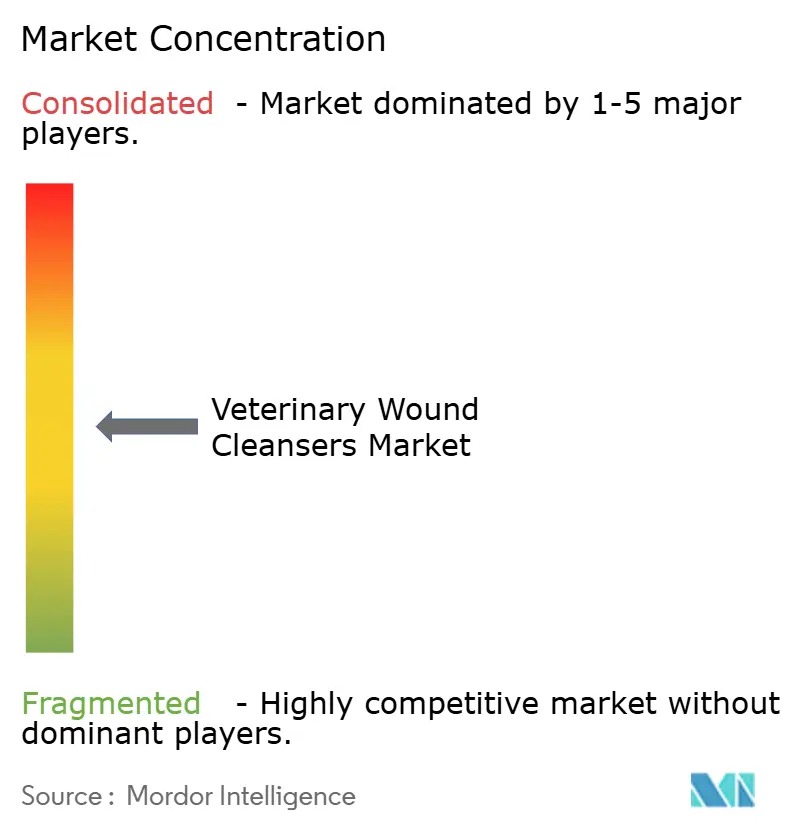

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Wound Cleansers Market Analysis by Mordor Intelligence

The Veterinary Wound Cleansers Market size is projected to expand from USD 228.86 million in 2025 and USD 252.66 million in 2026 to USD 414.36 million by 2031, registering a CAGR of 10.40% between 2026 to 2031.

Increasing companion-animal ownership, stricter livestock biosecurity regulations, and the introduction of low-cytotoxic hypochlorous acid and polyhexanide products are driving a shift among veterinarians from traditional iodine and chlorhexidine solutions. Pet insurance coverage for wound-care consumables is reducing price sensitivity and boosting the adoption of premium sprays and gels. The expansion of mobile veterinary clinics in rural areas is further fueling demand for shelf-stable spray formats that do not require sterile water. Moreover, online retailers are optimizing supply chains, enabling manufacturers to directly provide veterinarian-grade cleansers, packaged for home use, to pet owners.

Key Report Takeaways

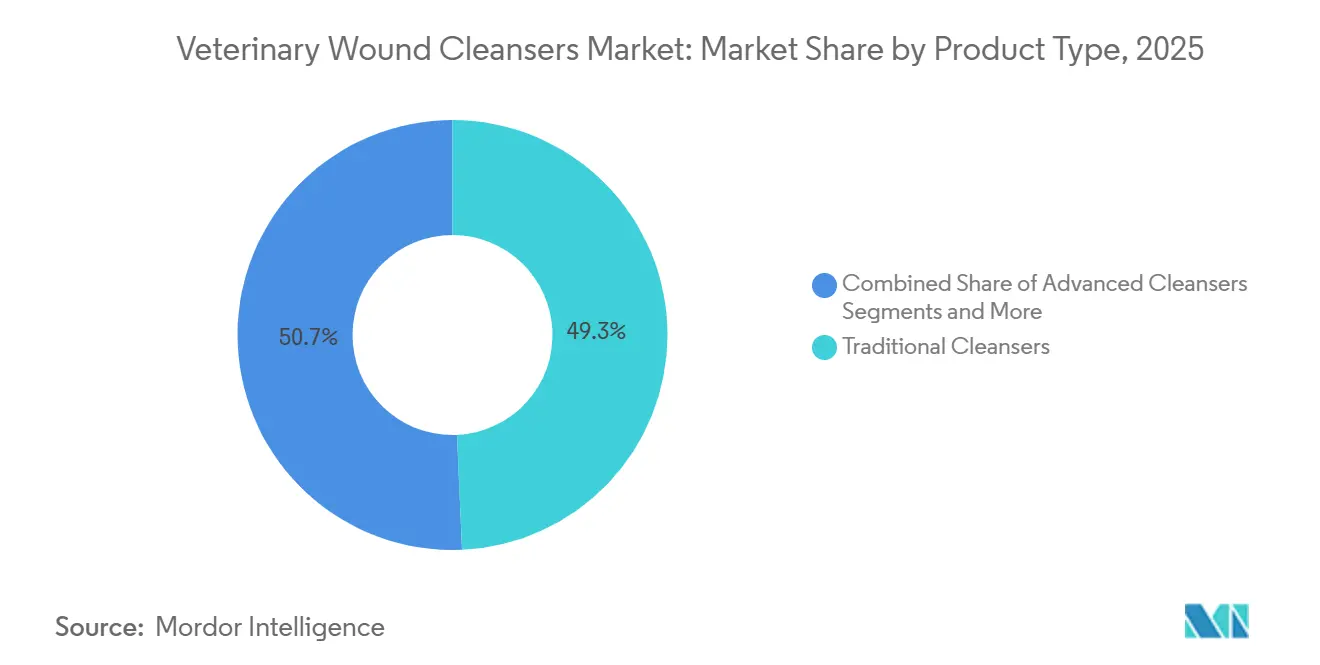

- By product type, traditional cleansers led with 49.30% of the veterinary wound cleanser market share in 2025, while advanced cleansers are slated to grow at a 12.15% CAGR through 2031.

- By form, spray formats accounted for the fastest growth, rising at an 11.87% CAGR compared with solutions that held 38.68% revenue in 2025.

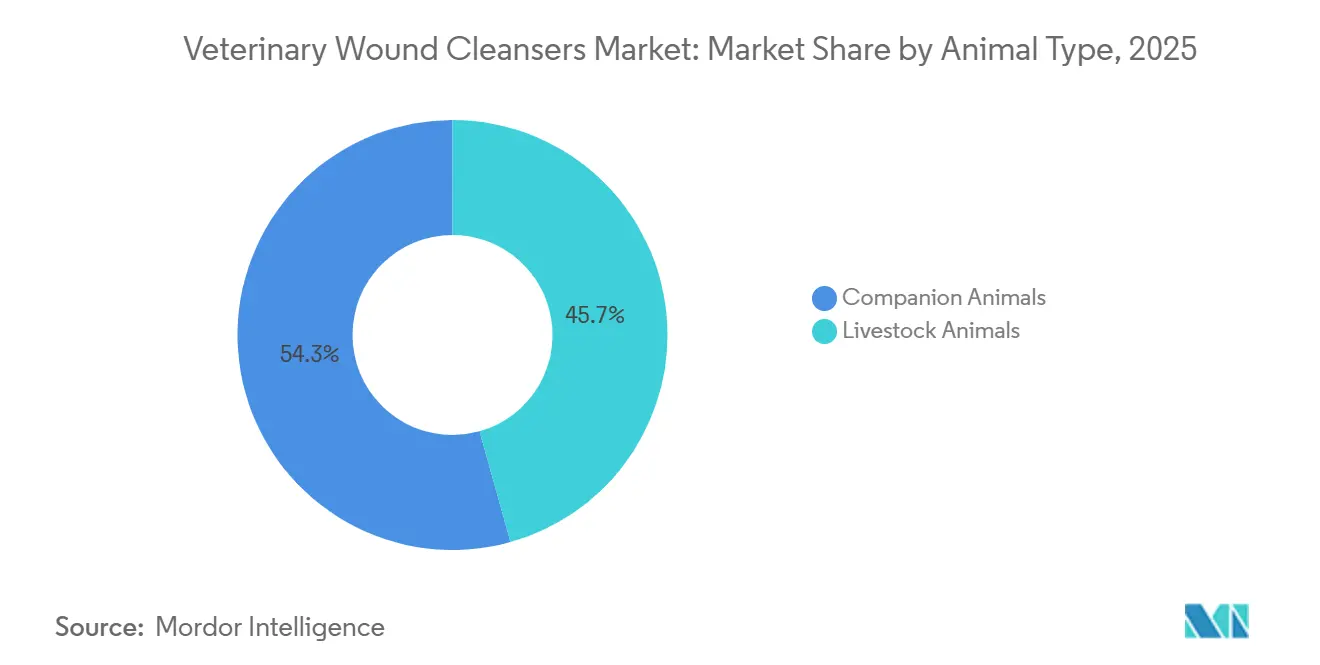

- By animal type, companion animals commanded 54.34% of 2025 revenue and are advancing at a 12.48% CAGR, outpacing livestock applications.

- By end user, home-care channels are expanding at a 12.13% CAGR, although veterinary hospitals & clinics still generated 59.50% of 2025 sales.

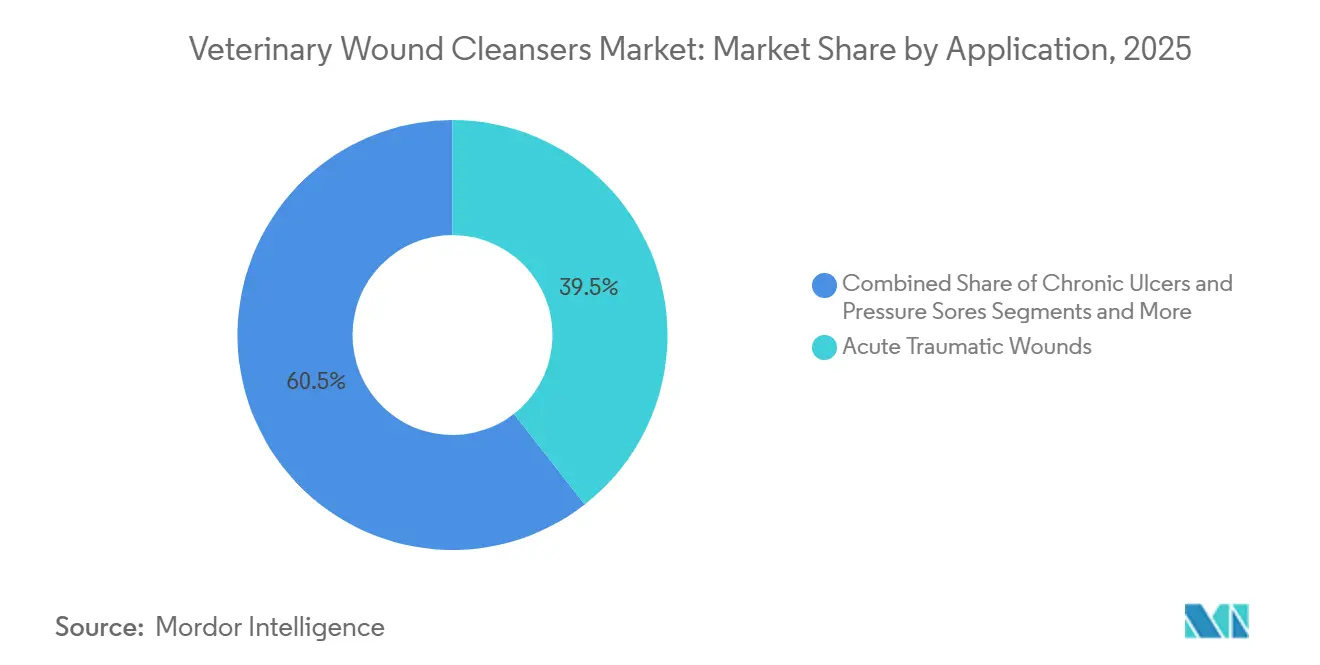

- By application, chronic ulcers & pressure sores are forecast to rise at an 11.65% CAGR, compared with acute traumatic wounds that represented 39.46% of 2025 revenue.

- By geography, North America led with a 39.10% revenue share in 2025; Asia-Pacific is advancing at a 10.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Veterinary Wound Cleansers Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising prevalence of traumatic & surgical wounds in companion animals | 1.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Growth in pet-insurance reimbursement for wound-care consumables | 1.6% | North America, Western Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Expansion of mobile veterinary clinics in underserved rural areas | 1.4% | North America rural corridors, Sub-Saharan Africa, Southeast Asia | Long term (≥ 4 years) |

| Livestock bio-security mandates driving on-farm antiseptic use | 1.2% | Global, acute in Asia-Pacific (China, Vietnam) & Europe | Short term (≤ 2 years) |

| Innovation in hypochlorous-acid & polyhexanide low-cytotoxic cleansers | 1.1% | Global, led by North America & Europe | Medium term (2-4 years) |

| Shift toward natural/plant-based antimicrobial formulations | 0.9% | North America, Europe, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Traumatic & Surgical Wounds in Companion Animals

Post-pandemic adoption surges have driven an increase in visits to U.S. veterinary hospitals for trauma, neoplasia, and abscess drainage. Hospital data indicates that multi-drug-resistant infections are extending patient stays, thereby increasing the demand for low-cytotoxic cleansers that effectively reduce biofilm formation. With average treatment costs now exceeding USD 1,500 per case, veterinarians are increasingly adopting prophylactic cleansers as a cost-management strategy. Urban specialty centers, recognized for their complex orthopedic and oncologic surgeries, have emerged as a lucrative market for premium wound-care products. This trend has resulted in sustained growth in the companion-animal segment of the veterinary wound cleanser market.

Growth in Pet-Insurance Reimbursement for Wound-Care Consumables

In 2023, the U.S. and Canada recorded 5.36 million active pet insurance policies, reflecting a 17.2% annual increase and expanding coverage for wound care products.[1]North American Pet Health Insurance Association, “State of the Industry Report 2023,” naphia.org Reimbursement schedules now include cleansers as part of standard benefits, enabling veterinarians to recommend advanced sprays over generic saline. Insurers in Germany and the U.K. adopted similar models in 2024, reducing out-of-pocket expenses for European pet owners. This shift has allowed manufacturers to set premium prices on hypochlorous-acid products without affecting demand. Additionally, pilot programs linking telemedicine with reimbursements are driving home-care consumption, reducing reliance on in-clinic visits for cleanser sales.

Expansion of Mobile Veterinary Clinics in Underserved Rural Areas

In July 2025, to ensure effective treatment for domestic animals, the Animal Husbandry department (AHD) has launched a mobile veterinary surgery unit in Alappuzha district. These mobile units utilize spray and wipe formats that withstand temperature variations and eliminate the need for sterile irrigation. In regions such as Sub-Saharan Africa and Southeast Asia, similar mobile clinic initiatives funded by development agencies have reported a 30-40% reduction in post-procedure infections when advanced cleansers are used instead of improvised antiseptics. The adoption of single-use packaging minimizes contamination risks and aligns with the limited storage capabilities of field operations. The continued expansion of this model is driving incremental demand in the veterinary wound cleanser market.

Livestock Bio-Security Mandates Driving on-Farm Antiseptic Use

In 2024, outbreaks of African Swine Fever in China and Vietnam led to the implementation of mandatory wound-care protocols on commercial farms. Europe has introduced similar standards under its 2025 Animal Health Law, incorporating cleanser usage into audit checklists. Poultry and swine exporters in Brazil and Argentina have responded by offering traceable, lot-coded products to meet the requirements of importing countries. As compliance becomes a prerequisite for market access, the livestock sector is transitioning from discretionary spending on cleansers to recognizing them as a fixed operational expense, thereby driving overall revenue growth.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Cost & Cold-Chain Burden for Advanced Cleansers | -0.8% | Emerging markets in Asia-Pacific, Sub-Saharan Africa, Latin America | Medium term (2-4 years) |

| Fragmented Regulatory Approvals Across Emerging Markets | -0.6% | India, China, Brazil, Southeast Asia | Long term (≥ 4 years) |

| Poor User Compliance & Limited Owner Education in LMICs | -1.1% | Global, acute in remote regions with limited infrastructure | Short term (≤ 2 years) |

| Competition From Generic Saline & Home Remedies | -1.3% | Europe & China primarily, spillover to other regulated markets Source: | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost & Cold-Chain Burden for Advanced Cleansers

Hypochlorous acid and polyhexanide products are priced at USD 15-30 per 100 ml, approximately 5-10 times higher than saline, limiting their adoption in cost-sensitive livestock operations. Additionally, some stabilized formulations require refrigeration, adding USD 0.50-1.00 per unit in warmer climates where clinics often face unreliable power supply. Consequently, livestock producers frequently opt for more affordable iodine for non-critical wounds. Suppliers are introducing ambient-stable sprays and bulk packaging to lower per-dose costs, but margin compression continues to pose challenges in emerging markets.

Fragmented Regulatory Approvals Across Emerging Markets

Distinct approval processes in India, China, and Brazil extend time-to-market by 18-36 months and often necessitate duplicate clinical trials.[2]Journal of Veterinary Emergency and Critical Care, “Wound Management in Companion Animals,” wiley.com In Brazil, separate registrations for companion-animal and livestock products double regulatory expenses. This lack of harmonization discourages smaller firms from pursuing multi-country launches, concentrating market access among multinational companies with dedicated regulatory teams. As a result, delays in the introduction of new active ingredients constrain short-term growth potential in the veterinary wound cleanser market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Advanced Cleansers Outpace Legacy Solutions

Advanced Cleansers are expected to grow at a strong 12.15% CAGR, while Traditional Cleansers accounted for 49.30% of the veterinary wound cleanser market share in 2025. Hypochlorous acid and polyhexanide platforms are increasingly adopted in specialty referral centers and equine hospitals, where their ability to accelerate healing enhances discharge rates and improves client satisfaction. Regulatory audits requiring lot-traceable products are reducing the price advantage historically held by iodine and chlorhexidine solutions.

Clinics managing chronic pressure sores are shifting toward low-cytotoxic actives that protect granulation tissue, driving the preference for Advanced Cleansers in the veterinary wound cleanser market. Traditional options remain relevant for livestock due to cost considerations, but new biosecurity mandates are limiting the appeal of unlabeled generics. Natural or herbal solutions occupy a niche among organic producers, but their limited clinical validation and shorter shelf life restrict broader adoption.

By Form: Sprays Extend Reach Beyond Surgery Suites

Solutions held a 38.68% revenue share in 2025, but Sprays are advancing at an 11.87% CAGR, representing the fastest growth in the veterinary wound cleanser market. Mobile clinics and home-care settings favor sprays for their ability to dispense without requiring gauze or sterile water, saving time and reducing contamination risks.

Foams are preferred by veterinarians for treating deep or irregular wounds, while wipes are targeted at pet owners managing minor abrasions under telehealth guidance. Gels and ointments are designed for horses and exotic species that require prolonged tissue contact. Field insights indicate that single-use packaging and ambient-stable formulations are driving higher reorder rates across all product forms

By Animal Type: Companion Animals Anchor Premium Demand

Companion Animals accounted for 54.34% of revenue in 2025 and are growing at a 12.48% CAGR, outpacing livestock in the veterinary wound cleanser market. Dogs dominate the segment's revenue due to frequent trauma, orthopedic surgeries, and dermatological conditions requiring extended wound care.

Cat owners are increasingly adopting advanced sprays for abscess drainage and post-spay care, although lower spending levels moderate overall growth. Equine medicine remains a niche but high-value segment, driven by the critical nature of limb wounds in performance horses. The ongoing trend of pet humanization and rising pet insurance coverage continue to fuel demand for companion animals.

By End-User: Home-Care Channels Gain Traction

Veterinary Hospitals and Clinics accounted for 59.50% of sales in 2025, but Home-care channels are expanding at a 12.13% CAGR, driven by the growing adoption of telehealth in the veterinary wound cleanser market. Insurers now reimburse home-applied cleansers, and e-commerce platforms ensure fast delivery, reducing the need for in-clinic pickups.

Research institutes maintain steady, though modest, volumes for antimicrobial-resistance monitoring, with spending remaining stable rather than growing rapidly. The shift toward direct-to-consumer sales is intensifying competition, enabling agile brands to bypass distributor mark-ups and capture market share through subscription delivery models.

By Application: Chronic Wounds Emerge as a Growth Hotspot

Acute Traumatic Wounds accounted for 39.46% of revenue in 2025, but Chronic Ulcers and Pressure Sores are growing at an 11.65% CAGR, driven by aging pets and extended post-operative recovery periods. Surgical Incisions continue to generate consistent volume, as best practices require cleanser use before closure and during bandage changes.

Burn and chemical injuries, though infrequent, demand high-potency, low-cytotoxic products, aligning with the capabilities of advanced hypochlorous formulations. As chronic cases extend treatment durations, repeat purchases are increasing, enhancing the revenue contribution of long-term therapies in the veterinary wound cleanser market.

Geography Analysis

In 2025, North America accounted for 39.10% of the veterinary wound cleanser market revenue, maintaining its leadership due to a dense clinic network and a significant number of insured pets. Regulatory approvals in the region have facilitated the swift launch of innovative sprays and gels. High e-commerce penetration has further driven home-care product volumes as pet owners increasingly purchase cleansers online.

Asia-Pacific is expected to grow at the fastest rate, with a projected CAGR of 10.82%. Rising urban pet ownership in China and India is boosting demand for companion animals, while government subsidies are encouraging livestock producers to adopt biosecurity measures, including wound disinfection. South Korea mirrors North America in its preference for premium formulations, reflecting a growing willingness to invest in high-quality products.

Europe is witnessing steady growth under streamlined regulatory frameworks that simplify cross-border approvals. Germany and the United Kingdom lead in companion-animal sales, while Spain and Italy are seeing increased adoption of cleansers in livestock farms due to disease control measures. In South America, Brazil and Argentina are focusing on traceable cleansers to meet export standards, although high pricing limits broader adoption. Regional growth trends are shaped by disposable income, regulatory enforcement, and disease-control priorities.

Competitive Landscape

The veterinary wound cleanser market is moderately fragmented. Leading players like Zoetis and Elanco bundle cleansers with vaccines and antibiotics, leveraging established sales networks in both companion-animal and livestock channels. Innovacyn and Sonoma Pharmaceuticals dominate the hypochlorous-acid segment with proprietary chemistries offering rapid antimicrobial action without tissue damage. Cresilon’s VETIGEL, designed for emergency hemostasis, enhances trauma care and highlights the growing demand for gel-based formats.

Direct-to-consumer e-commerce is driving significant growth, with start-ups offering ambient-stable sprays in subscription models that bypass distributor mark-ups. Technology advancements focus on bag-on-valve aerosol delivery, single-use droppers, and temperature-resilient formulations to reduce cold-chain costs. Regulatory expertise is a key differentiator, enabling firms to navigate complex requirements in markets like Brazil and India, while smaller competitors often target Europe, benefiting from streamlined EMA processes.

The competitive landscape rewards companies with either global regulatory capabilities or a strong focus on innovative product development. Firms that excel in these areas are better positioned to capture market share and drive growth in this evolving sector.

Veterinary Wound Cleansers Industry Leaders

Axio Biosolutions Pvt Ltd

Virbac.

Innovacyn, Inc.

Zoetis Services LLC

Vetoquinol

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Amferia received FDA De Novo clearance for an antibacterial peptide dressing, opening United States distribution for its Class 2 device targeting advanced wound care.

- May 2025: Zoetis inaugurated a reference laboratory in Louisville to expand nationwide diagnostics.

- May 2025: Dechra secured FDA approval for Otiserene, the first single-dose otic suspension for dogs.

Global Veterinary Wound Cleansers Market Report Scope

As per the scope of the report, veterinary wound cleansers are specialized topical solutions used to remove debris, bacteria, and other contaminants from wounds on animals. Cleansers are important in promoting healing and preventing infections in various situations, from minor cuts and scrapes to surgical incisions and chronic wounds.

The veterinary wound cleansers market is segmented by product type, animal type, end-user, and geography. By product type, the market is segmented into traditional cleansers, advanced cleansers, and natural cleansers. By animal type, the market is segmented into companion animals and livestock animals. By end user, the market is segmented by veterinary hospitals and clinics, home care, and research institutes. By application, the market is segmented into acute traumatic wounds, surgical incisions, chronic ulcers & pressure sores, and burn & chemical wounds. By geography, the market is segmented by North America, Europe, Asia-Pacific, Middle East and Africa, and South America. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Traditional Cleansers |

| Advanced Cleansers |

| Natural / Herbal Cleansers |

| Solutions |

| Sprays |

| Foams |

| Wipes |

| Gels & Ointments |

| Companion Animals | Dogs |

| Cats | |

| Horses | |

| Livestock Animals | Cattle |

| Swine | |

| Poultry |

| Veterinary Hospitals & Clinics |

| Home-care (Pet Owners) |

| Research Institutes |

| Acute Traumatic Wounds |

| Surgical Incisions |

| Chronic Ulcers & Pressure Sores |

| Burn & Chemical Wounds |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Traditional Cleansers | |

| Advanced Cleansers | ||

| Natural / Herbal Cleansers | ||

| By Form | Solutions | |

| Sprays | ||

| Foams | ||

| Wipes | ||

| Gels & Ointments | ||

| By Animal Type | Companion Animals | Dogs |

| Cats | ||

| Horses | ||

| Livestock Animals | Cattle | |

| Swine | ||

| Poultry | ||

| By End User | Veterinary Hospitals & Clinics | |

| Home-care (Pet Owners) | ||

| Research Institutes | ||

| By Application | Acute Traumatic Wounds | |

| Surgical Incisions | ||

| Chronic Ulcers & Pressure Sores | ||

| Burn & Chemical Wounds | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecasted value of global veterinary wound cleansers by 2031?

Revenue is projected to reach USD 414.36 million by 2031, reflecting a 10.4% CAGR since 2026.

Which animal segment is expanding fastest in companion care?

Dogs drive the highest absolute growth, while both dogs and cats together lift companion-animal revenue at a 12.48% CAGR.

Why are hypochlorous-acid products gaining share?

They deliver broad-spectrum antimicrobial activity with low cytotoxicity, accelerating healing compared with iodine or chlorhexidine solutions.

How are mobile clinics influencing product demand?

Rural mobile units favor spray packages that work without sterile water, boosting field consumption and widening geographic reach.

Which region is set to grow quickest?

Asia-Pacific is leading with a projected 10.82% CAGR thanks to rising pet ownership, urbanization, and livestock biosecurity mandates.

What constraints limit adoption in emerging countries?

High unit prices and fragmented regulatory approvals prolong launch timelines and raise distribution costs, slowing penetration in price-sensitive markets.

Page last updated on: