Urinary Incontinence Treatment Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.9 Billion |

| Market Size (2031) | USD 5.78 Billion |

| Growth Rate (2026 - 2031) | 8.20% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Urinary Incontinence Treatment Devices Market Analysis by Mordor Intelligence

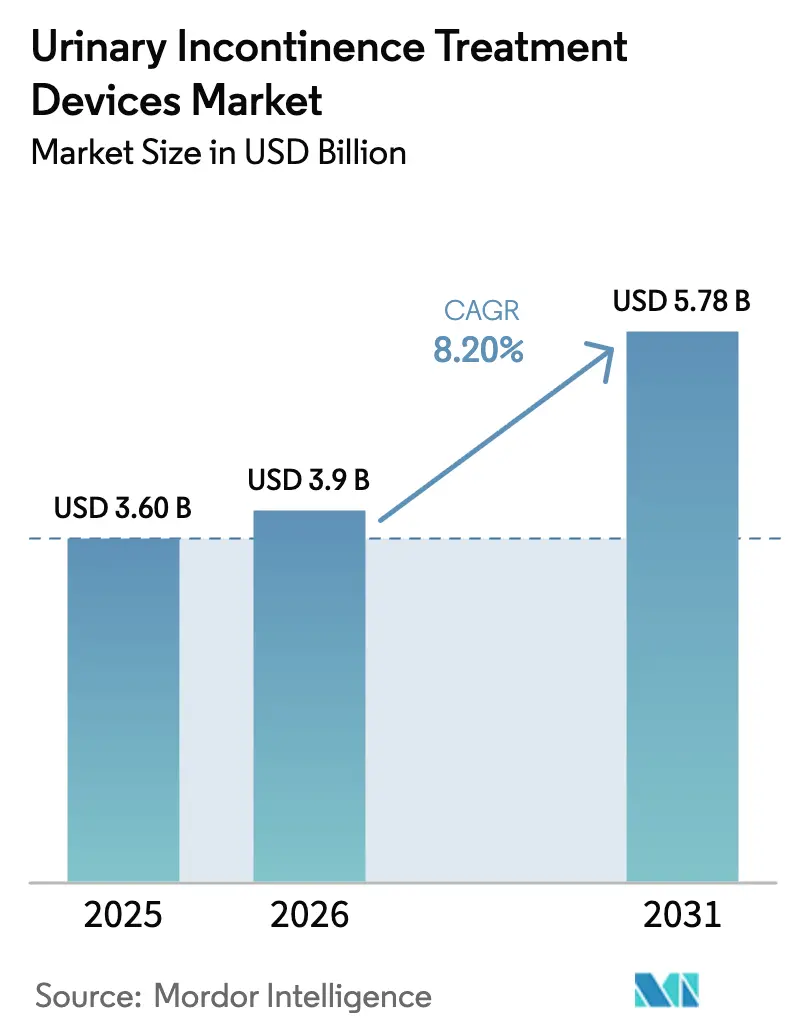

The Urinary Incontinence Treatment Devices Market size is projected to expand from USD 3.60 billion in 2025 and USD 3.9 billion in 2026 to USD 5.78 billion by 2031, registering a CAGR of 8.20% between 2026 to 2031.

Rising life-expectancy, growing awareness of quality-of-life therapies and sustained reimbursement support keep demand for evidence-based continence care on a steady upward track. Device makers now compete on sensor miniaturization, battery longevity and cloud connectivity rather than on basic efficacy alone, positioning the urinary incontinence treatment devices market as a proof-point for digital surgery convergence. Adoption is further lifted by Medicare coverage expansions, new HCPCS codes and Europe’s push to curb the EUR 69 billion (USD 79.84 billion) annual continence burden through earlier intervention. Meanwhile, venture funding accelerates prototype-to-approval timelines, allowing small entrants to leapfrog legacy platforms with AI-enabled, adaptive neuromodulation. Together, these forces re-shape the urinary incontinence treatment devices market into a long-horizon play for integrated patient-management ecosystems.

Key Report Takeaways

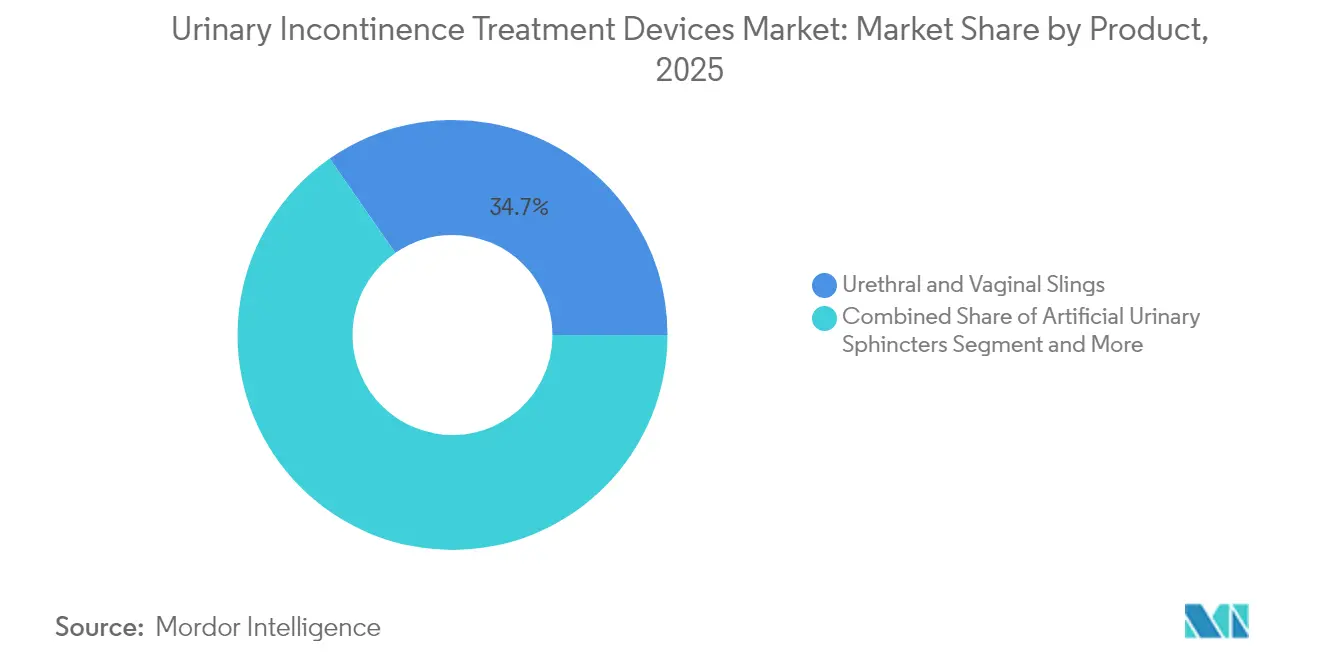

- By product, urethral and vaginal slings held 34.68% of the urinary incontinence treatment devices market share in 2025, while electrical and neuromodulation devices are projected to expand at a 12.08% CAGR through 2031.

- By incontinence type, stress incontinence captured 45.03% revenue in 2025; urge incontinence solutions are set to grow the fastest at an 11.18% CAGR to 2031.

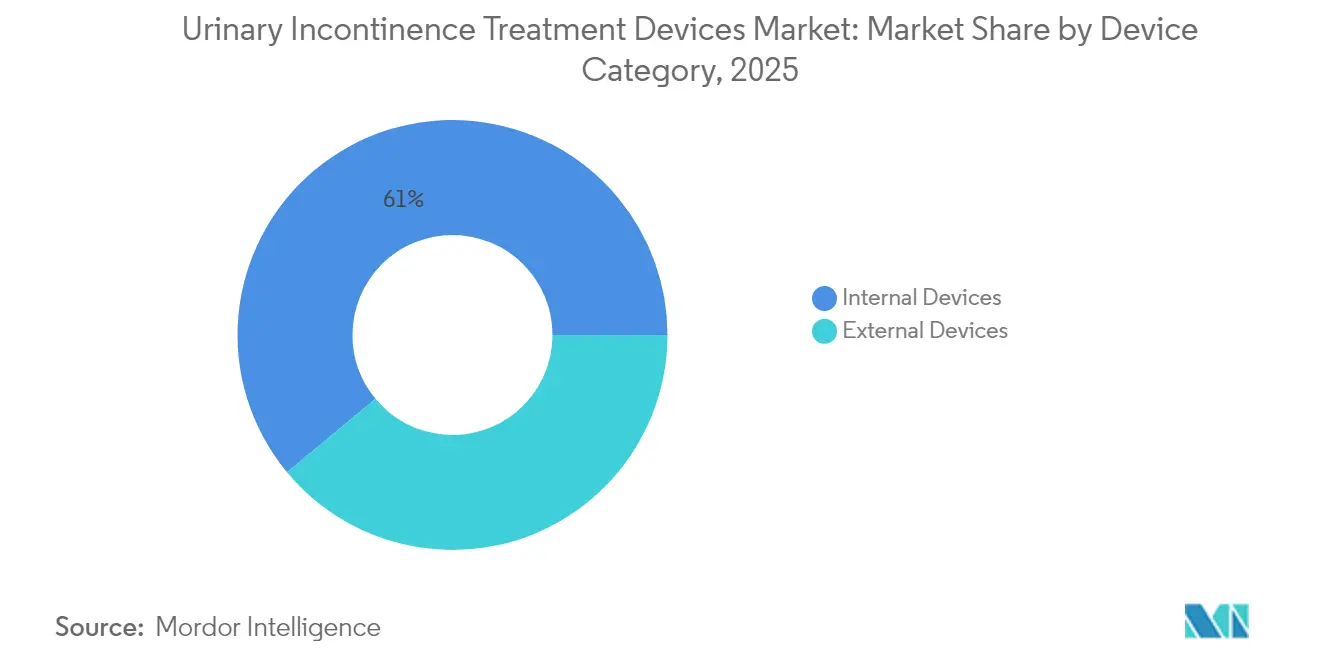

- By device category, internal systems commanded 61.02% of the urinary incontinence treatment devices market size in 2025, whereas external solutions are forecast to rise at a 12.02% CAGR.

- By end user, hospitals accounted for 55.12% share of the urinary incontinence treatment devices market size in 2025; home-care and long-term care settings record the highest projected CAGR at 11.44% to 2031.

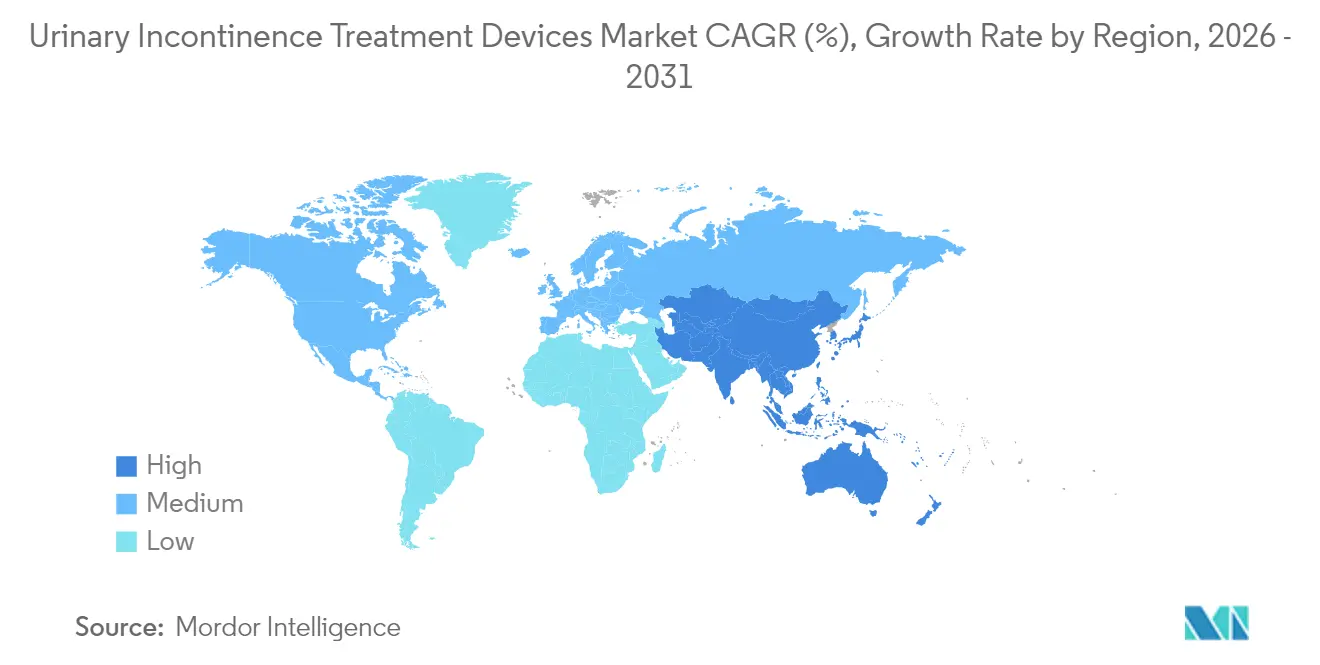

- By geography, North America led with 39.42% share in 2025, but Asia-Pacific is expected to post the fastest 10.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Urinary Incontinence Treatment Devices Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population & prevalence surge | +2.1% | Global, concentrated in North America, Europe, Japan | Long term (≥ 4 years) |

| Demand for minimally-invasive & outpatient procedures | +1.8% | North America & EU, expanding to Asia-Pacific | Medium term (2–4 years) |

| Favourable reimbursement in US & EU | +1.5% | North America & EU | Short term (≤ 2 years) |

| AI-enabled pelvic-floor digital therapeutics adoption | +1.2% | Global, early uptake in developed markets | Medium term (2–4 years) |

| Rapid innovation in neuromodulation & wireless implants | +1.6% | Global, led by North America and Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Ageing Population & Prevalence Surge

One in three women older than 55 now experiences some form of incontinence, and prevalence in residential facilities exceeds 75%[1]Continence Foundation of Australia, “Key Statistics on Incontinence,” continence.org.au. Health systems also report that 11.2% of Medicare beneficiaries carry an incontinence diagnosis, with prevalence jumping to 20.6% in skilled-nursing settings. Because falls, dermatitis and urinary tract infections often follow untreated leakage, clinicians frame devices as preventive investments rather than discretionary aids. This shift shields demand from macro-economic slowdowns, giving the urinary incontinence treatment devices market a recession-resistant profile. For manufacturers, the demographic wave provides a long runway for connected devices that monitor hydration, activity and therapy adherence in real time.

Demand for Minimally-invasive & Outpatient Procedures

Health providers target shorter stays and lower facility fees by moving sacral nerve stimulation and tibial nerve stimulation to office environments. The eCoin device, implanted under local anesthesia, delivers 68% symptom improvement at 48 weeks and eliminates overnight hospitalization. Outpatient neuromodulation cuts direct procedure costs by as much as 40% while preserving outcomes, making payer authorizations faster and broadening patient eligibility. Device vendors therefore engineer quick-fit leads, awake-procedure workflows and training modules for non-surgical specialists. As a result, the urinary incontinence treatment devices market gains access to ambulatory surgery centers and urology offices previously untapped by implantable therapy.

Favourable Reimbursement in US & EU

Medicare’s 2024 decision to list the PureWick external catheter as durable medical equipment covers 80% of cost after deductibles and sets a reimbursement precedent for future external systems. Two new HCPCS codes also create specific billing routes for intravaginal digital therapeutics, stimulating physician prescription in primary-care settings. In Europe, statutory insurance in Germany reimburses prescribed incontinence aids with patient co-payment capped at EUR 10 per month, keeping affordability consistent even for retirees. These policy tailwinds compress the pay-back period for hospitals investing in new platforms, maintaining momentum within the urinary incontinence treatment devices market.

AI-enabled Pelvic-floor Digital Therapeutics Adoption

Convolutional neural networks now identify correct pelvic floor muscle contractions with 98.7% accuracy, turning once-subjective exercises into quantifiable therapy. Smartphone-based coaching lifted adherence during pandemic restrictions and proved as effective as clinic-guided regimens. Ultrasound algorithms that estimate bladder volume within 3% of manual catheterization accuracy further reduce invasive diagnostics. For vendors, integrating analytics dashboards with implant telemetry differentiates offerings and cements recurring revenue from data subscriptions. Patients gain discreet, at-home feedback, making AI platforms complementary to implants rather than substitutes.

Restraints Impact Analysis of Urinary Incontinence Treatment Devices Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited awareness & persisting social stigma | -1.3% | Global, pronounced in developing regions | Long term (≥ 4 years) |

| Post-operative complications & device recalls | -0.9% | Global, regulatory focus in US & EU | Short term (≤ 2 years) |

| Shortage of specialised uro-gyne surgeons in LMICs | -0.7% | Sub-Saharan Africa, rural Asia & Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Awareness & Persisting Social Stigma

Seven of every ten people living with symptoms never discuss them with a clinician, delaying diagnosis and skewing prevalence data. Regional surveys show that 32% of older adults in Shanghai regard leakage as shameful compared with 6% of healthcare professionals, revealing stark communication gaps. Stigma also keeps many women from regular exercise, indirectly raising cardiovascular risk. When clinicians omit routine screening, device adoption lags despite technological progress. Addressing cultural barriers therefore remains central to long-run expansion of the urinary incontinence treatment devices market.

Post-operative Complications & Device Recalls

FDA Class 2 recalls, such as the 2025 action against the InterStim programming module, can stall new implant orders for months[2]U.S. Food and Drug Administration, “Class 2 Device Recall MEDTRONIC INTERSTIM THERAPY SYSTEM FOR URINARY CONTROL,” accessdata.fda.gov. High-profile vaginal mesh litigation, which resulted in USD 302 million in penalties for one manufacturer, amplifies patient hesitation and insurer scrutiny. External catheter adverse-event reports citing dermatitis and infections trigger safety reviews, pressing suppliers to prove skin-friendliness with clinical data. Each incident undermines clinician confidence, trimming near-term sales even in otherwise receptive segments of the urinary incontinence treatment devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Urinary Incontinence Treatment Devices Market Segment Analysis

By Product:

Slings Retain Scale as Neuromodulation Gains PaceSlings contributed 34.68% to the urinary incontinence treatment devices market share in 2025, a share built on surgical familiarity and mature supply chains. Continuous refinements in mesh material and anchoring techniques sustain relevance, yet future volume growth shifts toward electrical and neuromodulation systems posting a 12.08% CAGR. Battery lives exceeding 10 years, wireless re-charging and MRI conditionality reduce lifetime maintenance, making implants practical for younger patients who expect device longevity. Venture investments in closed-loop stimulation add algorithms that auto-adjust amplitude to bladder pressure, raising therapeutic success while limiting manual re-programming. Slings therefore evolve into one component of a broader toolkit rather than the market’s single anchor.

Procedural economics also nudge hospitals toward neuromodulation, because outpatient implantation frees theatre time and yields faster DRG turn-around. Nonetheless, sling revisions still account for a sizeable portion of uro-gynecology caseload, generating predictable consumable demand for specialized surgical instruments. The result is a dual-trajectory product landscape in which low-complexity devices defend existing share while electronics-heavy platforms capture incremental volume. Within this context, the urinary incontinence treatment devices market enjoys diversified revenue streams resilient to reimbursement or technology shocks.

By Incontinence Type:

Stress Dominates but Urge Expands RapidlyStress incontinence captured 45.03% of revenue in 2025, underpinned by well-established mid-urethral sling protocols and favorable long-term efficacy data. Yet urge incontinence therapies are projected to log an 11.18% CAGR as sacral and tibial neuromodulation demonstrate 85% first-year success rates against 49% for oral antimuscarinics. Device makers respond by fine-tuning stimulation algorithms that modulate afferent signaling, thereby addressing overactive detrusor activity without systemic side effects. Cross-over designs now allow the same implant to treat mixed incontinence via firmware updates, letting physicians personalize care without added inventory.

For stress cases, innovation targets less-invasive sling insertion and alternative bulking agents to defer surgery. Meanwhile, overflow and functional categories remain niche yet clinically significant, driving demand for sensors that alert caregivers when voiding assistance is needed. Smart diapers equipped with moisture detectors already reduce dermatitis by supporting timely changes in cognitively impaired patients. Diversifying indications therefore enlarges the urinary incontinence treatment devices market while underscoring the need for modular platforms adaptable across symptom clusters.

By Device Category:

Internal Systems Lead, External Solutions AccelerateInternal implants held 61.02% share of the urinary incontinence treatment devices market size in 2025, thanks to proven efficacy in severe leakage cases and established surgical pathways. Device miniaturization continues, with nickel-sized tibial stimulators lasting 2.8 years on a single battery cycle. Next-generation units add wireless power from wearable transmitters, removing replacement surgeries and extending therapy life indefinitely. Yet patient preference increasingly favors external alternatives that avoid implantation risks, propelling external solutions toward a 12.02% CAGR through 2031.

Medicare coverage of PureWick exemplifies payer acceptance of non-invasive systems, and smart textile sensors that integrate into underwear discreetly track voiding episodes without plumbing attachments. Vendors leverage these textiles to collect longitudinal data, generating analytics that can trigger telehealth interventions before complications arise. Consequently, competition pivots from hardware alone to combined hardware-software value propositions, expanding the addressable base inside the urinary incontinence treatment devices market.

By End User:

Hospitals Anchor Volume as Home-Care Demand SurgesHospitals contributed 55.12% of 2025 revenue as complex revisions, refractory urge therapies and comorbidity management require multidisciplinary teams and 24-hour monitoring. However, the fastest 11.44% CAGR belongs to home-care and long-term care settings, where aging-in-place policies and staffing shortages make remote monitoring and caregiver-friendly devices indispensable. Outpatient surgery centers also gain share because same-day discharge for neuromodulation saves direct costs and frees inpatient beds.

Specialty uro-gyne clinics capitalize on narrowly focused expertise, attracting referrals and streamlining device selection protocols. Nursing homes prioritize infection control and labor efficiency, turning to external urine-collection systems coupled with digital dashboards that flag high-risk residents. Together, these shifts re-allocate therapy delivery across a continuum of sites, reinforcing the need for interoperable platforms within the urinary incontinence treatment devices market.

Geography Analysis

North America Urinary Incontinence Treatment Devices Market

North America held 39.42% of the urinary incontinence treatment devices market share in 2025, buoyed by Medicare Part B covering 80% of approved device costs after deductible thresholds. Leading academic centers in Chicago and Boston adopt smart bladder implants that transmit fullness data to mobile apps, accelerating clinical translation and peer-review dissemination. FDA de novo pathways further facilitate first-in-class approvals, allowing start-ups to navigate stringent quality benchmarks without legacy PMA burdens. Commercial insurers often mirror Medicare policy within one year, shortening payer-adoption lag and maintaining high per-patient revenue within the region.

APAC Urinary Incontinence Treatment Devices Market

Asia-Pacific is the fastest-growing geography with a 10.48% CAGR through 2031, driven by rapid population aging in Japan and infrastructure investments in China and India. Japan’s policy push for home-based care fuels demand for remote-monitored devices, while private hospitals in tier-one Chinese cities open cash-pay opportunities for neuromodulation implants. Nevertheless, specialist shortages outside urban hubs limit procedural throughput, prompting vendors to build training hubs and tele-mentoring platforms. Cultural taboos around discussing bladder symptoms continue to suppress early diagnosis, yet mobile-first health campaigns supported by governments begin to close awareness gaps.

Germany, MEA and South America Urinary Incontinence Treatment Devices Market

Germany reimburses prescribed aids with capped co-payments, but southern markets remain price-sensitive, slowing premium implant uptake. Still, policy makers cite the continent’s EUR 69 billion (USD 79.84 billion) continence burden to advocate preventive coverage for digital therapeutics and early-stage neuromodulation. Middle East, Africa and South America collectively represent under-penetrated territories where cost-effective external devices and mobile support tools may leapfrog resource constraints, gradually enlarging the global urinary incontinence treatment devices market.

Competitive Landscape

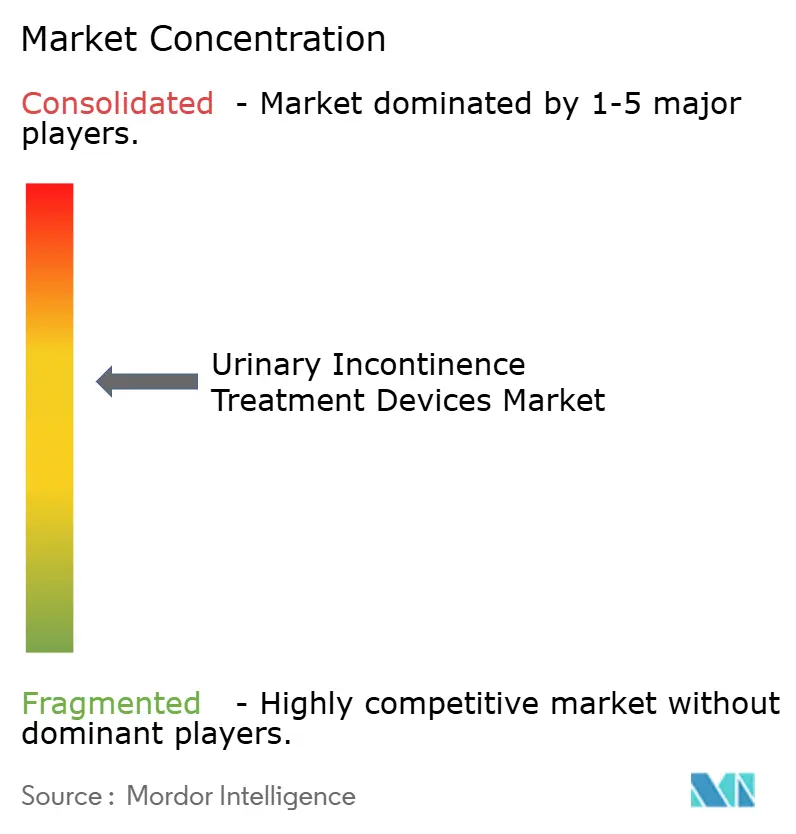

The field displays moderate consolidation, with Boston Scientific, Medtronic, Coloplast, Hollister and Convatec collectively controlling an estimated mid-50s percentage of global revenue. Boston Scientific’s USD 3.7 billion Axonics acquisition blended sacral neuromodulation expertise with an expansive urology sales force, signaling that incumbents favor acquisition over green-field R&D for platform gaps[3]Boston Scientific Corporation, “Boston Scientific Announces Agreement to Acquire Axonics, Inc.,” bostonscientific.com. The combined entity now markets a cradle-to-grave portfolio, from rechargeable SNM implants to pelvic-health digital coaching apps, tightening hospital purchasing-bundle strategies.

Medtronic answered by launching InterStim X, offering 15-year battery life and MRI conditionality, and by pursuing closed-loop algorithms that adjust stimulation based on evoked compound action potentials. Patent disputes over lead anchoring and telemetry protocols underscore the strategic value of intellectual property in defending share. Coloplast and Convatec focus on external devices and ostomy-adjacent platforms, investing in sensor-embedded drainage bags to add data services and lock in consumable revenue.

Start-ups secure sizable venture rounds to challenge incumbents on agility and technology freshness. Amber Therapeutics garnered USD 100 million to advance adaptive neuromodulation for mixed incontinence, while UroMems raised USD 47 million for an automated artificial sphincter that self-regulates cuff pressure. Neuspera’s micro-stimulation system met primary endpoints in 2025, delivering “gold standard” outcomes in less than five cubic centimeters of implant volume. These entrants prioritize adaptive firmware, cloud analytics and smartphone control, aiming to bypass entrenched hardware with service-oriented business models that could reset value capture in the urinary incontinence treatment devices market.

Urinary Incontinence Treatment Devices Industry Leaders

Boston Scientific Corporation

Becton, Dickinson and Company

PROMEDON GmbH

AMI GmbH

Coloplast A/S

- *Disclaimer: Major Players sorted in no particular order

Urinary Incontinence Treatment Devices Market Companies Covered in this Report

- Coloplast

- Boston Scientific

- Beckton Dickinson

- Medtronic

- Johnson & Johnson

- Hollister

- B. Braun

- ConvaTec Group plc

- PROMEDON

- A.M.I.

- Caldera Medical

- Zephyr Surgical Implants

- Teleflex

- Cardinal Health

- UroMems SA

- Neuspera Medical Inc.

- Uroplasty Inc.

- Kimberly-Clark Worldwide

- Essity

Read Analysis of Urinary Incontinence Treatment Devices Companies

Recent Industry Developments in Urinary Incontinence Treatment Devices Market

- February 2025: Neuspera neuromodulation device achieved “gold standard” results in pivotal urinary incontinence trials.

- February 2025: UroMems reported successful six-month outcomes in the first female clinical study of the UroActive smart sphincter for stress incontinence.

Urinary Incontinence Treatment Devices Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the urinary incontinence treatment devices market as all clinically approved implantable or externally worn medical devices that actively prevent, control, or monitor involuntary urine leakage, including urethral or vaginal slings, artificial urinary sphincters, neuromodulation systems, urinary catheters, penile clamps, drainage bags, and pelvic-floor training systems. According to Mordor Intelligence, every value discussed refers to the revenue these devices generate when first sold to healthcare providers or consumers, stated in constant 2024 US dollars.

Scope exclusion: Absorbent hygiene products (pads, adult diapers, briefs) and prescription pharmaceuticals lie outside this market boundary.

Segments Covered in This Report

- By Product

- Urethral & Vaginal Slings

- Artificial Urinary Sphincters

- Electrical / Neuromodulation Devices

- Urinary Catheters

- Penile Clamps & Pessary Devices

- Urinary Drainage Bags & Accessories

- Pelvic Floor Training Systems

- By Incontinence Type

- Stress

- Urge

- Mixed

- Overflow & Functional

- By Device Category

- Internal Devices

- External Devices

- By End User

- Hospitals

- Ambulatory Surgical Centres

- Specialty / Uro-Gyn Clinics

- Home-care & Long-term Care Settings

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed urologists, uro-gynecologists, pelvic-floor physiotherapists, biomedical engineers, and procurement managers across North America, Europe, and Asia-Pacific. These conversations validated therapy pathway assumptions, average selling prices, and regional reimbursement triggers, while short online surveys with device distributors filled volume or replacement-cycle gaps.

Desk Research

We began with government and public health datasets such as WHO Global Health Estimates, the International Continence Society prevalence surveys, US CDC NHANES, Eurostat hospital discharge files, OECD Health Statistics, and national device registries, which quantify patient pools and surgical volumes across age cohorts and geographies. Regulatory databases, notably the US FDA 510(k) and EU MDR notified-body listings, helped us verify commercial availability year by year.

Corporate sources were then mined; annual reports, 10-Ks, investor decks, and product catalogs were retrieved through D&B Hoovers and Dow Jones Factiva, while patent activity around neuromodulation and mini-slings was screened on Questel to flag pipeline impacts. Trade associations such as the European Association of Urology and the Japanese Continence Society supplied guideline updates that shape device uptake. This list is illustrative; many other documents informed data collection, cross-checks, and clarification.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-patient model starts by sizing adult populations living with stress, urge, or mixed incontinence, adjusts for diagnosis and treatment rates, and then links each treatment pathway to its typical device kit. Results are corroborated with selective bottom-up roll-ups drawn from sampled manufacturer revenues, channel checks, and an average selling price × unit calculus, before final alignment. Key variables include age-specific prevalence, sling procedure counts, neuromodulation adoption curves, elective surgery backlogs, per-capita health spending, and average device ASP progression. We forecast with multivariate regression blended with scenario analysis, so macro shifts (aging index, reimbursement reforms) and expert consensus guide growth to 2030. Data voids are bridged with region-specific analogs and clearly logged estimation rules.

Data Validation & Update Cycle

Model outputs pass anomaly checks against independent shipment statistics and public earnings transcripts, followed by a second analyst review. Reports refresh every year, with interim updates when recalls, pivotal approvals, or reimbursement shocks occur. A final analyst pass just before publication ensures clients receive the latest calibrated view.

How Mordor Intelligence's Urinary Incontinence Treatment Devices Market Size Compares to Other Published Estimates

Published market values often diverge because firms choose different device baskets, pricing resets, and refresh cadences. Our readers deserve clarity on those gaps before they rely on any single number.

Key gap drivers include the tendency of some publishers to blend absorbent disposables with therapeutic devices, to extrapolate single-country ASPs globally, or to roll forward pandemic-era procedure deferrals without re-benchmarking 2024 volumes. Mordor's model isolates active treatment hardware only, applies country-level ASP series, and is refreshed annually, so our 2025 base is grounded in recently restored elective surgery data.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.60 B (2025) | Mordor Intelligence | - |

| USD 4.22 B (2024) | Global Consultancy A | Mixes absorbent products and applies uniform 7 % ASP uplift across regions |

| USD 3.10 B (2023) | Trade Journal B | Uses pre-pandemic surgical volumes and excludes neuromodulation implants |

These comparisons show that figures swing when scope or assumptions shift; however, Mordor's disciplined segmentation, variable-level audits, and yearly refresh give decision-makers a transparent, balanced baseline they can trace back to clear inputs and repeatable steps.

Key Questions Answered in the Report

What is the current value of the urinary incontinence treatment devices market?

The market is valued at USD 3.9 billion in 2026 and is projected to reach USD 5.78 billion by 2031.

Which product segment holds the largest share?

Urethral and vaginal slings lead with a 34.68% share, owing to established surgical protocols.

Which region is growing the fastest?

Asia-Pacific is expected to post the highest 10.48% CAGR through 2031, driven by rapid population aging and infrastructure upgrades.

How are reimbursement policies influencing adoption?

Medicare and new HCPCS codes in the United States, along with capped co-payments in Germany, lower patient cost-burden and stimulate clinician uptake.

What technologies are most disruptive today?

Wireless, battery-free neuromodulation implants and AI-enabled pelvic-floor digital therapeutics are redefining patient experience and broadening indication coverage.

What is the primary restraint on market growth?

Persistent social stigma keeps many affected individuals from seeking treatment, delaying diagnosis and device adoption despite available reimbursement.

Page last updated on: