Market Overview

| Study Period | 2020 - 2031 |

|---|---|

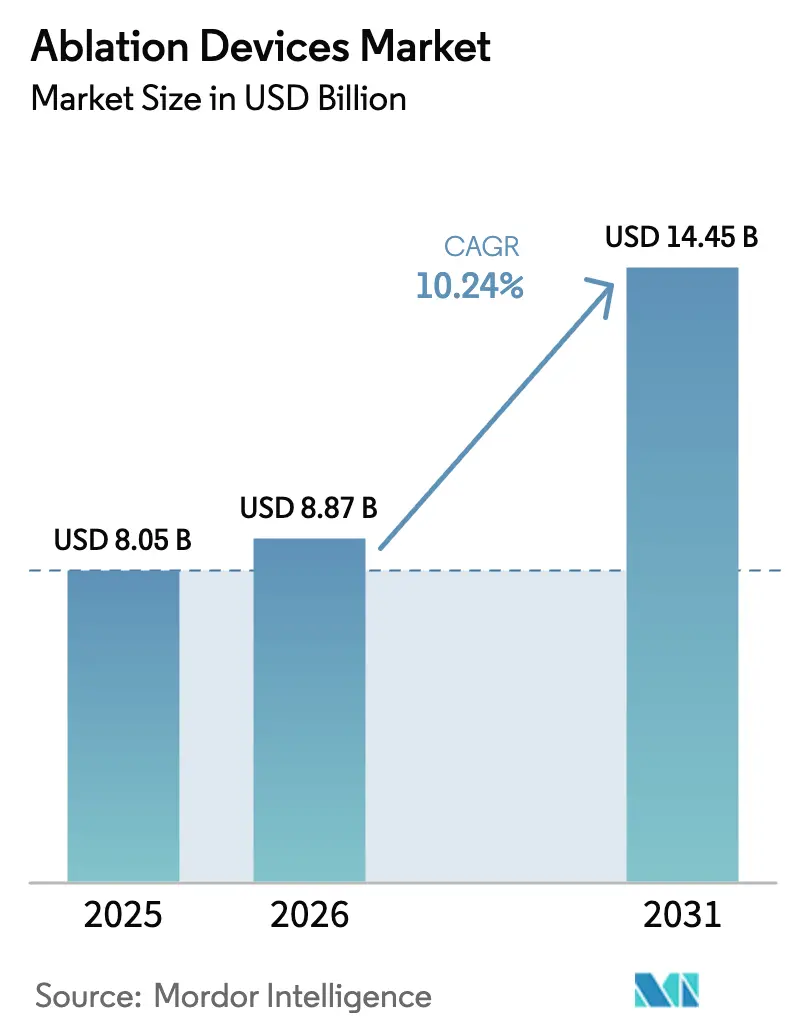

| Market Size (2026) | USD 8.87 Billion |

| Market Size (2031) | USD 14.45 Billion |

| Growth Rate (2026 - 2031) | 10.24% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ablation Devices Market Analysis by Mordor Intelligence

The ablation device market size was valued at USD 8.05 billion in 2025 and estimated to grow from USD 8.87 billion in 2026 to reach USD 14.45 billion by 2031, at a CAGR of 10.24% during the forecast period (2026-2031). Strong demand for minimally invasive care, rapid regulatory clearances for pulsed-field ablation, and the growing burden of chronic diseases sustain this upward curve. Radiofrequency platforms still anchor revenues, yet non-thermal systems gain traction as early data confirm shorter procedures and lower complication risks. Regional growth tilts toward Asia-Pacific, where healthcare modernization widens access to advanced therapies, while North America maintains revenue leadership through premium pricing and steady replacement cycles. Consolidation and aggressive R&D spending sharpen competitive rivalry, but the market continues to reward firms that can pair energy delivery innovations with precise imaging and mapping solutions.

Key Report Takeaways

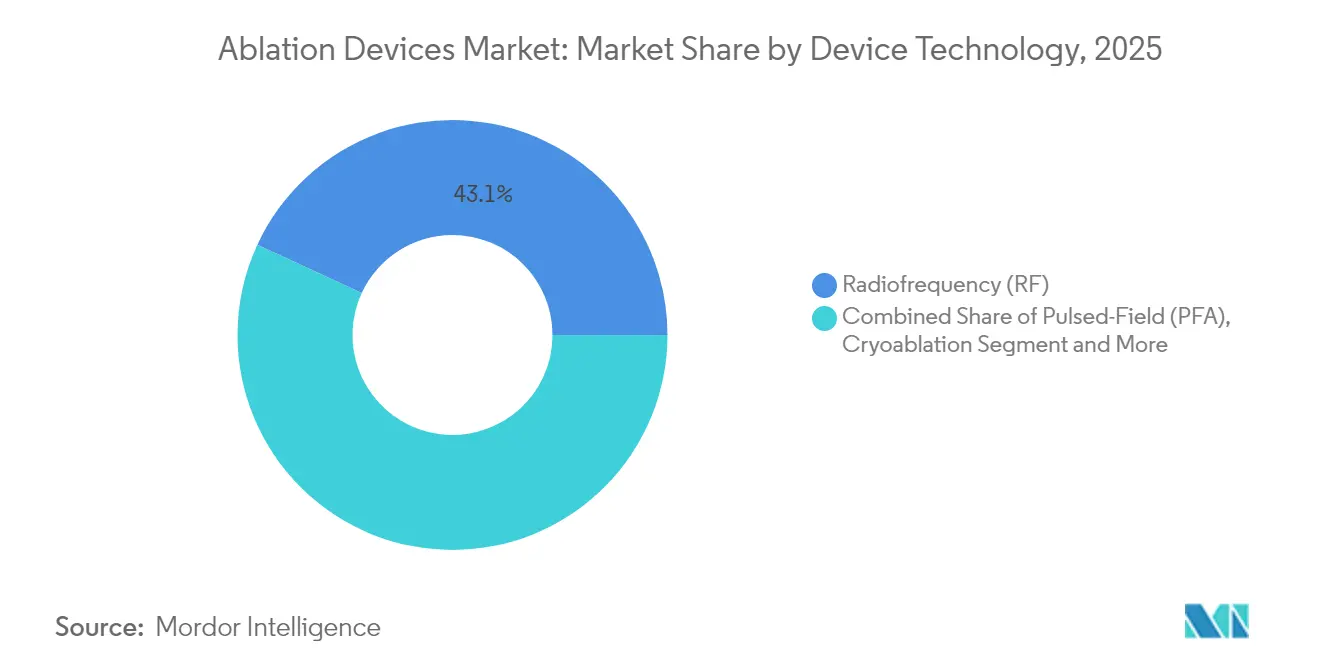

- By device technology, radiofrequency held 43.10% of ablation device market share in 2025, while pulsed-field ablation is projected to expand at a 22.10% CAGR through 2031.

- By application, oncology led with 39.10% revenue share in 2025; cardiovascular procedures are poised to grow at 11.95% CAGR to 2031.

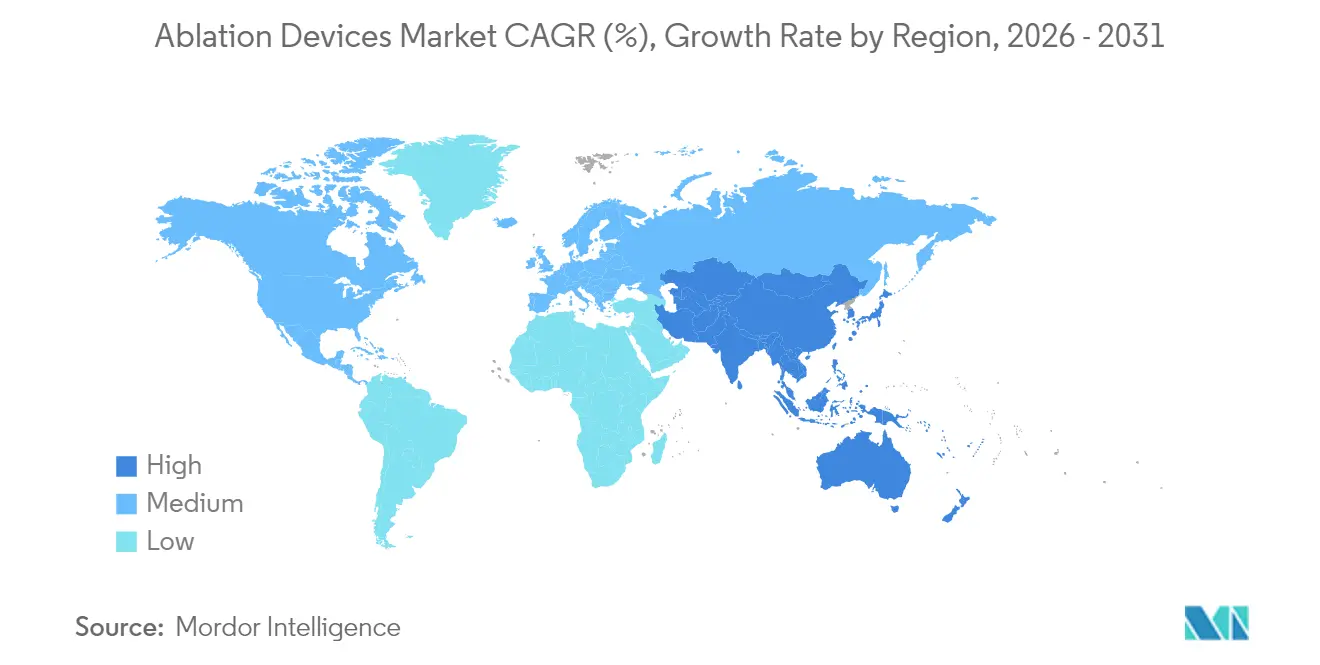

- By geography, North America accounted for 38.40% of the ablation device market in 2025, whereas Asia-Pacific is forecast to grow at 12.10% CAGR.

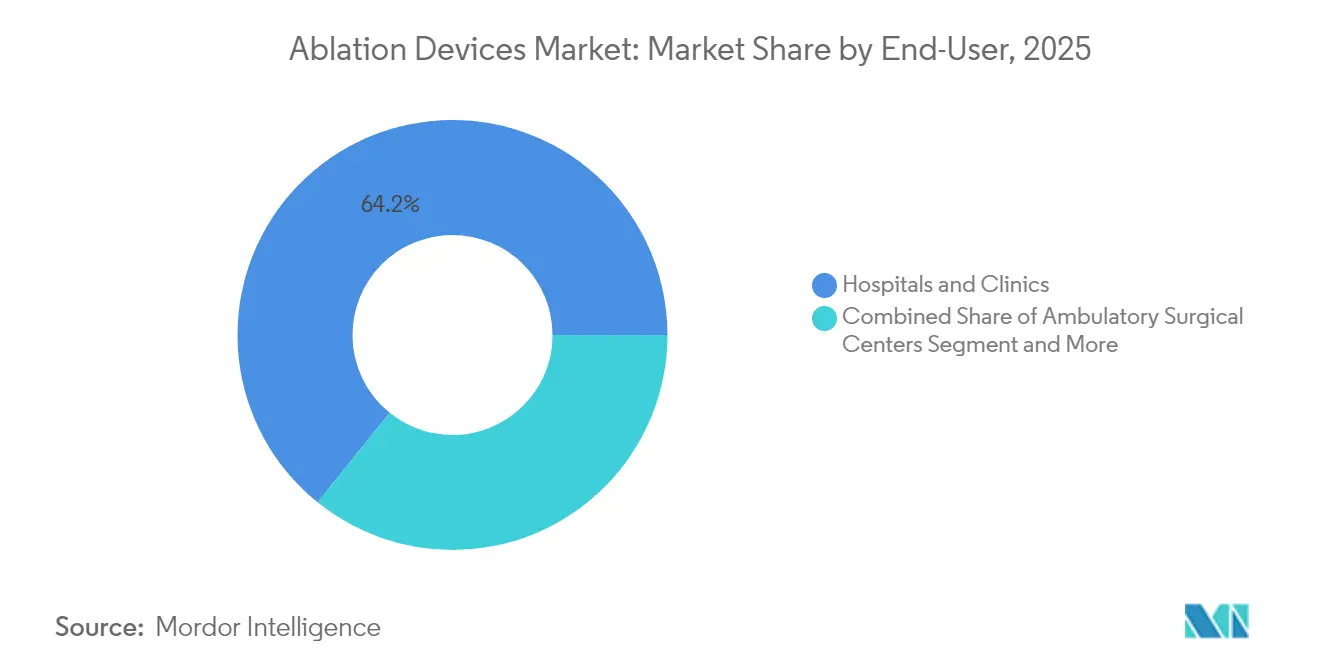

- By end-user, hospitals and clinics commanded 64.20% share of the ablation device market size in 2025, while ambulatory surgical centers are advancing at 12.75% CAGR.

- By mode of procedure, percutaneous techniques represented 59.30% share of the ablation device market size in 2025, and laparoscopic approaches are tracking an 11.40% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ablation Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise In Prevalence Of Chronic Diseases Requiring Surgery | 2.8% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Technological Advancements In Ablation Devices | 3.2% | Global, led by North America, expanding to APAC | Medium term (2-4 years) |

| Surge In Demand For Minimally-Invasive Procedures | 2.1% | Global, accelerated adoption in APAC & Europe | Medium term (2-4 years) |

| Growing Incidence Of Atrial Fibrillation Driving Cardiac Ablation Adoption | 1.9% | North America & Europe core, emerging in APAC | Long term (≥ 4 years) |

| Rapid Commercial Adoption Of Pulsed-Field Ablation (PFA) Systems | 2.5% | North America & Europe, expanding globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Technological Advancements in Ablation Devices

Pulsed-field ablation (PFA) delivers tissue-selective energy that avoids thermal injury to adjacent organs and cuts procedure times nearly in half. In the ADVENT trial, Boston Scientific’s FARAPULSE achieved 81.6% arrhythmia-free survival at 12 months while completing most cases under 60 minutes[1]Boston Scientific, “Boston Scientific Receives FDA Approval for FARAPULSE Pulsed Field Ablation System,” bostonscientific.com. Medtronic’s PulseSelect posted 88% freedom from recurrence and similar time savings, and Abbott’s Volt platform reported 94.5% freedom from repeat ablation. FDA approvals for multiple PFA systems in 2024–2025 signal regulatory confidence and encourage global roll-outs. Broader portfolios that integrate advanced mapping and closed-loop control are expected to further expand the ablation device market.

Rapid Commercial Adoption of PFA Systems

Hospitals justify PFA investment through measurable operating gains. European centers reported per-patient savings of USD 850 versus cryoablation and USD 1,301 against radiofrequency as fewer complications and shorter room times trimmed resource use. More than 200,000 patients have already been treated worldwide with FARAPULSE, and early adopter feedback notes average procedure times near 30 minutes, an efficiency that accelerates learning curves for new users. As physicians gain confidence across paroxysmal and persistent atrial fibrillation, PFA transitions from niche to platform technology, reinforcing growth across the ablation device market.

Surge in Demand for Minimally Invasive Procedures

Payers and patients favor same-day interventions that shrink costs and speed recovery. Ambulatory centers now manage a growing share of ablation cases as device miniaturization and procedural safety enable outpatient workflows. Recent studies show same-day discharge in more than 80% of PFA cases with no rise in readmissions. Robotic catheter systems add precision and reduce radiation, which improves staff safety and supports higher procedural volumes.

Growing Incidence of Atrial Fibrillation

Atrial fibrillation affects roughly 60 million people worldwide and now drives earlier ablation referrals as guidelines shift toward rhythm control. Evidence shows catheter ablation outperforms drug therapy for long-term sinus rhythm maintenance and quality-of-life gains. The FDA recently allowed Medtronic’s Arctic Front cryo-balloon to be used without prior antiarrhythmic failure, reflecting this paradigm change. Rising diagnosis rates in emerging markets widen the global addressable pool, sustaining volume growth for the ablation device market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Ablation Devices & Disposables | -1.8% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| Procedural Risks (Thermal Injury, Arrhythmia Recurrence, Etc.) | -1.2% | Global, varying by technology adoption | Long term (≥ 4 years) |

| Reimbursement Uncertainty For Novel Energy Modalities | -1.5% | North America & Europe, emerging in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Ablation Devices & Disposables

Capital investments above USD 500,000 and single-use catheter prices ranging from USD 3,000 to USD 8,000 deter small facilities from adopting next-generation systems. Annual service contracts add 15–20% to ownership costs. Providers now request value-based pricing that links payments to clinical outcomes, compelling manufacturers to craft shared-savings or pay-per-use models that temper upfront spending.

Reimbursement Uncertainty for Novel Energy Modalities

Policy frameworks lag behind technology approvals. Medicare coverage for PFA remains in evaluation, and temporary local determinations create billing risk for hospitals considering capital commitments. Private insurers vary in prior-authorization requirements, lengthening decision cycles and adding administrative burden. International markets face similar gaps as reimbursement agencies analyze long-term cost-effectiveness data.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Technology: Non-Thermal Platforms Re-Shape Treatment Choices

Radiofrequency ablation retained 43.10% ablation device market share in 2025 through decades of clinical familiarity and efficient reimbursement pathways. However, pulsed-field systems are forecast to post a 22.10% CAGR, the fastest within the ablation device market, as physicians embrace shorter cases and improved safety. Cryoablation remains important for pulmonary vein isolation, while microwave systems gain ground in oncology where larger, uniform ablation zones are prized. Histotripsy recently secured FDA clearance for liver tumors with 85–95% success, signaling broader acceptance of mechanical energy therapies.

The technology mix is also influenced by artificial intelligence that tailors power delivery to patient anatomy, producing consistent lesion sets and reducing operator variability. Laser and high-intensity focused ultrasound are expanding beyond dermatology into pain and gynecology, while integrated mapping plus therapy catheters shorten lab time. As capital budgets migrate toward multi-energy consoles, suppliers able to consolidate modalities on one platform are positioned to capture greater ablation device market opportunity.

By Application: Cardiac Procedures Accelerate

Oncology commanded 39.10% of the ablation device market in 2025 thanks to established protocols for liver, lung, and renal tumors. Cardiovascular ablation is projected to grow at 11.95% CAGR, sharpening competition for share of the ablation device market size among EP labs that increasingly ablate early in atrial fibrillation. Ophthalmology and pain management niche uses expand steadily due to micro-catheters that target delicate tissues without open surgery. In gynecology, minimally invasive fibroid treatment gains traction as fertility-preserving options rise in demand.

Clinical data continue to validate cardiac growth. Durability rates above 90% at 12 months have been reported when advanced 3-D mapping guides lesion placement. AI-driven algorithms further personalize ablation lines, while wearable monitors capture post-procedure rhythm metrics, reinforcing physician confidence and boosting volumes within the ablation device market.

By End-User: Outpatient Settings Scale Quickly

Hospitals and clinics owned 64.20% of the ablation device market in 2025, leveraging intensive care capacity for complex cases. Ambulatory surgical centers are forecast to log a 12.75% CAGR through 2031, reflecting payer pressure for lower costs and patient desire for swift discharge. Device miniaturization supports this shift, and purpose-built consoles fit ASC footprints without major renovations.

ASC growth also spurs demand for disposables optimized for quick turnover, and vendors now offer single-tray kits that reduce set-up time. Specialty cancer centers use focused ablation to complement targeted therapies, expanding total ablation device market size as multidisciplinary teams adopt combined protocols.

By Mode of Procedure: Percutaneous Still Dominant, Laparoscopy Rising

Percutaneous entry captured 59.30% of ablation device market size in 2025 owing to minimal trauma and quick recovery. Laparoscopic methods are tracking an 11.40% CAGR as surgeons exploit high-definition imaging and articulating tools. The Boztosun technique in laparoscopic hysterectomy cut operating times and admissions in recent trials. Robotic assistance further enhances dexterity for hard-to-reach lesions and reduces ergonomic strain.

Hybrid procedures that pair percutaneous energy delivery with laparoscopic visualization blur traditional boundaries. These workflows broaden candidate eligibility, lift success rates, and expand the overall ablation device market.

Geography Analysis

North America accounted for 38.40% of global revenue in 2025. A mature reimbursement system, accelerated FDA approvals, and strong replacement cycles sustain leadership. Boston Scientific treated more than 40,000 patients with FARAPULSE during its first commercial year, underscoring rapid uptake. The region also hosts leading research centers that generate pivotal data supporting new indications, which reinforces confidence across hospitals and ambulatory centers.

Asia-Pacific is the fastest-growing territory, projected at 12.10% CAGR to 2031. National health reforms and expanding device manufacturing in China and India lower procurement costs and improve availability. Japanese regulators authorized FARAPULSE in September 2024, and early hospital demand signals strong appetite for non-thermal technologies. Demographic shifts toward older populations and rising chronic disease prevalence assure continued growth of the ablation device market in the region.

Europe delivers steady expansion under a harmonized Medical Device Regulation framework that still promotes innovation while safeguarding patients. The early CE Mark approval of Abbott’s Volt PFA system in March 2025 illustrates the region’s role as a launchpad for advanced platforms. Academic hospitals continue to lead investigator-initiated studies, especially in oncology and neurologic uses, helping European clinicians refine protocols that ripple worldwide.

Competitive Landscape

Market concentration is moderate. Boston Scientific, Medtronic, Johnson & Johnson, and Abbott form a four-player core, yet a wave of niche rivals and acquisitions shifts positions regularly. Boston Scientific captured early mindshare with FARAPULSE, boosting overall electrophysiology revenues in 2024 – 2025. Medtronic counters with the Affera Sphere-9 catheter that combines mapping and PFA in one device, trimming lab time.

Strategic deals exceed USD 6 billion across 2024-2025. Stryker’s USD 4.9 billion bid for Inari Medical expands its vascular reach, while Boston Scientific’s USD 1.26 billion purchase of Silk Road Medical adds neuro-vascular expertise. Patents covering catheter materials, energy algorithms, and closed-loop control remain critical barriers for late entrants.

R&D investment tops USD 1.28 billion annually among leading firms, targeting AI-guided therapy, smaller generators, and multi-energy consoles. Partnerships with imaging companies and cloud-based data platforms further differentiate offerings. Emerging players keep competitive intensity high as they bring focused innovations to specialty segments such as renal denervation or histotripsy, ensuring the ablation device market continues to evolve at pace.

Ablation Devices Industry Leaders

Medtronic PLC

Johnson and Johnson

Abbott Laboratories

Boston Scientific Corporation

AngioDynamics, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Pulsed-field ablation (PFA) is expanding upgrade cycles in electrophysiology as non-thermal energy shifts from early adoption toward routine purchasing decisions. Recent FDA actions reinforce this direction, including approval activity around Boston Scientific's FARAPULSE PFA catheter in January 2026 and Abbott's Volt PFA system in December 2025, which broaden the set of commercially available PFA options for atrial fibrillation workflows. With more than 200,000 patients treated worldwide with FARAPULSE, vendors that pair ablation catheters with compatible mapping, software, and lab efficiency tools have room to differentiate, rather than competing on energy modality alone.

Care-site expansion is also creating demand signals for device makers and providers, particularly in the United States as ambulatory surgical centers (ASCs) take on a larger share of minimally invasive procedures. Effective January 1, 2026, CMS added cardiac catheter ablation to its list of covered procedures for ASCs, supporting outpatient pathway design and demand for smaller-footprint consoles, streamlined disposable kits, and protocols that enable same-day discharge. In Europe, the combination of the EU Medical Device Regulation (MDR) and the Health Technology Assessment Regulation (HTAR) moving into implementation phases in 2025 and 2026 raises the emphasis on long-term outcomes evidence and coordinated clinical assessment readiness, which tends to favor manufacturers with stronger clinical programs and post-market data infrastructure.

Recent Industry Developments

- June 2026: Boston Scientific announced expansion of Farapulse manufacturing capacity to support growing demand for pulsed-field ablation systems in the United States and Europe. The move is intended to enable broader access for hospitals and ambulatory centers.

- December 2025: Abbott announced FDA approval of its Volt pulsed field ablation system to treat patients with atrial fibrillation. This approval expands the multi-vendor PFA ecosystem and adds more lab workflow options.

- October 2024: Affera received FDA approval of the Mapping and Ablation System with the Sphere-9 catheter. The integrated mapping and ablation approach influences capital purchase decisions and installed-base upgrades in electrophysiology.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the ablation device market covers revenues earned from medical devices that destroy, remove, or modify tissue using energy, including capital generators and the related procedure tools used in hospitals and outpatient settings.

Scope exclusions: We exclude standalone diagnostic mapping systems, service and maintenance contracts, and veterinary-only ablation platforms.

Segmentation Overview

- By Device Technology

- Radiofrequency (RF)

- Cryoablation

- Microwave

- Laser / Light

- Ultrasound / HIFU

- Pulsed-Field (PFA)

- Others

- By Application

- Oncology

- Cardiovascular Disease

- Ophthalmology

- Gynecology

- Urology

- Cosmetic & Dermatology

- Pain Management & Neurology

- By End-User

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Specialty & Cancer Centers

- By Mode of Procedure

- Percutaneous

- Laparoscopic

- Open / Surgical

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the clinical and regulatory context, and to anchor the model to observable procedure and disease signals before we spoke to industry participants. We referenced public sources such as the US FDA device databases and safety communications, CDC and WHO disease burden statistics, OECD health statistics, and national health ministry publications that track service delivery and care access.

To translate this into a usable market model, we also reviewed peer reviewed clinical literature on ablation utilization and outcomes, society and association guidance documents for electrophysiology and oncology pathways, and import and export trade statistics where relevant for cross-checking device flows. Company filings, earnings transcripts, and investor presentations were used to sanity check product mix direction and pricing logic, supported by a paid subscription for company financials and another paid subscription for patent database lookups to understand technology momentum. The sources listed here are illustrative only, and many other public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and structured surveys were used to confirm what gets purchased and what is actually used in ablation procedures, since published utilization numbers often miss local practice patterns. We spoke with a mix of device-side roles, distributors, and clinical stakeholders, and we validated assumptions across Americas, EMEA, and APAC so regional differences in procedure mix and adoption timing were not averaged away.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | APAC: 48% |

| Mid tier: 58% | Functional/Unit leaders: 32% | EMEA: 32% |

| Smaller Players: 14% | Managers: 54% | Americas: 20% |

Market-Sizing & Forecasting

Our sizing model starts from a top-down demand build that reconstructs revenue from procedure volumes by key indications and settings, which are then translated into device and accessory consumption using utilization rates. Since real-world purchasing differs by modality, the model applies separate assumptions for modalities such as radiofrequency, microwave, cryo, ultrasound, laser, and pulsed-field, and then checks that the implied mix is consistent with what interviewees report for their accounts.

Several inputs are tracked because they move the total in a measurable way, including electrophysiology and tumor ablation procedure trends, catheter and probe replacement rates, installed base of generators, average selling price ranges by modality and geography, and the pace of technology shifts like pulsed-field adoption in cardiac workflows. For forecasts, we rely on scenario analysis tied to these drivers, and the adoption and pricing paths are stress-tested using ranges agreed during primary discussions. Bottom-up approximations are used as a control, including selective supplier and channel checks and sampled ASP-to-volume math, and gaps are handled by using proxy utilization rates from comparable procedures when a country series is incomplete.

Data Validation & Update Cycle

Model outputs are triangulated against independent signals, such as publicly reported procedure growth, regulatory approvals timing, and observed pricing bands, and then outliers are investigated before any totals are finalized. If a region shows an unexpected jump, the assumptions behind volumes, mix, and currency are rechecked, followed by a re-contact of selected respondents to confirm whether it reflects a one-time event or a structural change.

Each report goes through multi-step analyst review so calculations, sources, and year alignment are verified, and the final story stays consistent with the data. The study is refreshed annually, and interim updates are made when material events occur, such as major approval waves, reimbursement changes, or large shifts in hospital capital spending. Right before delivery, a final pass is done to ensure the latest public releases and market signals are reflected.

Mordor Intelligence's Ablation Device Market Estimate Compared With Other Published Estimates

Published market estimates for ablation devices often diverge because authors do not always count the same products, and they may anchor demand to different clinical volume indicators. The timing of currency conversion, what gets treated as recurring revenue, and how fast newer modalities are assumed to scale can also change the number noticeably.

The main gap comes from whether procedure tools and single-use accessories are counted alongside capital generators, and how fast pulsed-field adoption is blended into the cardiology mix, which is the point where Mordor Intelligence keeps accessories in-scope only when they are directly tied to ablation energy delivery and validates the adoption curve through procedure and installed base checks.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.87 B (2026) | |

| Industry Publisher A | USD 7.10 B (2024) | Uses an earlier base year and a longer horizon, and the scope can be narrower in how recurring accessories and newer modalities are treated, which can depress the starting value versus a procedure-linked demand build. |

| Research Portal B | USD 10.84 B (2025) | Reports a higher base-year value that can come from broader inclusion of adjacent products, different pricing progression assumptions, and a more aggressive near-term adoption path for newer cardiac technologies. |

The spread across sources is mostly explained by what gets counted as ablation revenue, how procedure demand is translated into device consumption, and how pricing and modality mix are carried forward year to year. By keeping the inputs tied to observable procedure signals and by checking the implied installed base and ASP ranges with industry respondents, the final number stays traceable to clear steps that can be repeated and reviewed.

Key Questions Answered in the Report

What is the current size of the ablation device market?

The market is valued at USD 8.87 billion in 2026 and is projected to reach USD 14.45 billion by 2031.

Which technology segment is growing the fastest?

Pulsed-field ablation is forecast to expand at a 22.10% CAGR through 2031 due to shorter procedures and reduced complications.

Which region will add the most new revenue?

Asia-Pacific shows the highest growth rate at 12.10% CAGR, supported by large patient pools and expanding device manufacturing.

How quickly are ambulatory surgical centers adopting ablation devices?

Procedures in ASCs are advancing at a 12.75% CAGR as payers push for cost-effective outpatient care.

What restrains wider adoption of next-generation ablation systems?

High capital and disposable costs and uncertain reimbursement for novel energy modalities remain key barriers.

Page last updated on: