Market Overview

| Study Period | 2020 - 2031 |

|---|---|

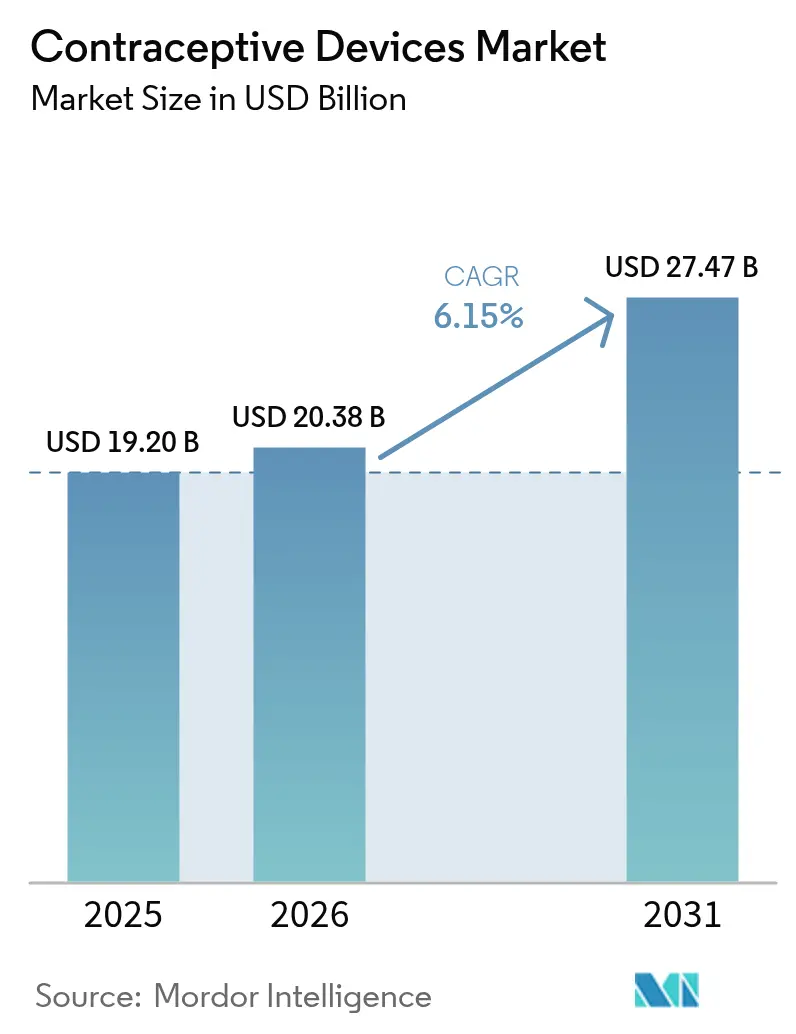

| Market Size (2026) | USD 20.38 Billion |

| Market Size (2031) | USD 27.47 Billion |

| Growth Rate (2026 - 2031) | 6.15% CAGR |

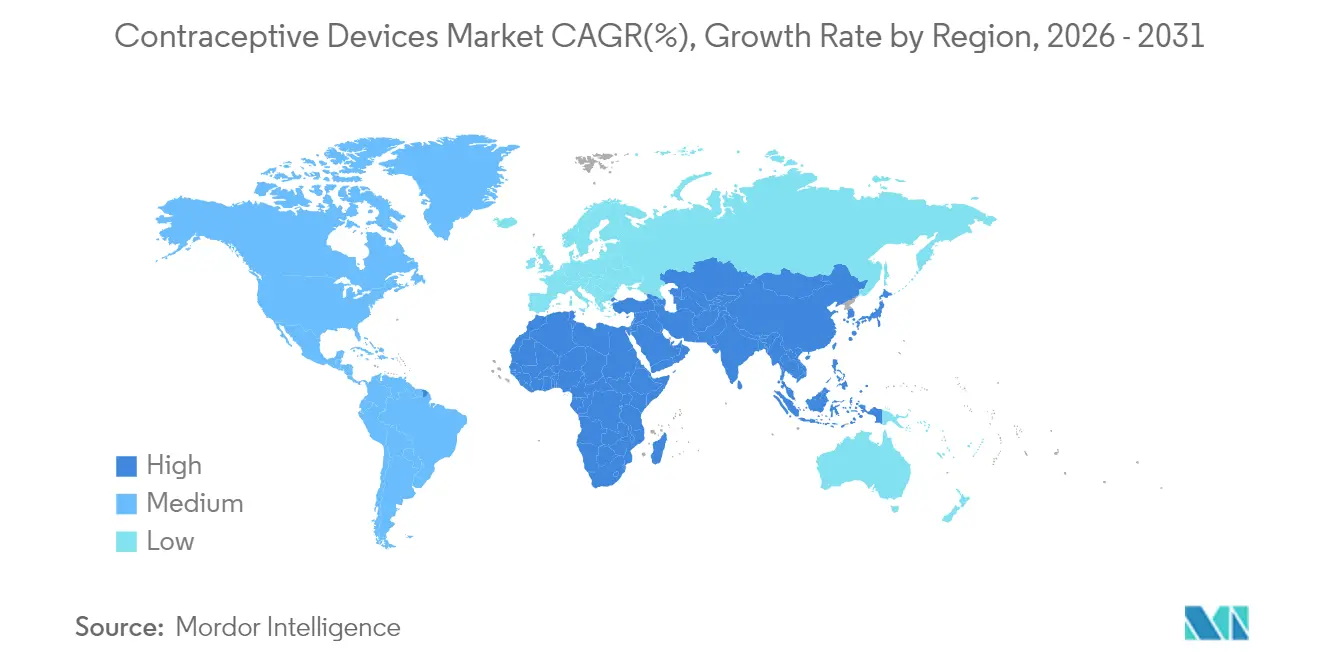

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Contraceptive Devices Market Analysis by Mordor Intelligence

The contraceptive devices market size is expected to grow from USD 19.20 billion in 2025 to USD 20.38 billion in 2026 and is forecast to reach USD 27.47 billion by 2031 at 6.15% CAGR over 2026-2031. Demand gains pace as governments broaden family-planning programs, digital health tools expand access, and dual-protection products answer the twin challenges of unintended pregnancy and sexually transmitted infections. Long-acting reversible contraceptives (LARCs) post robust uptake, online direct-to-consumer models compress time between intent and purchase, and material innovation responds to latex-sensitivity concerns. Technology platforms that integrate wireless control, real-time monitoring, and personalized dosing reshape user expectations, while policy moves that lift cost-sharing hurdles spur broader coverage. Competitive intensity rises as multinational device makers and emerging FemTech firms race to close white spaces in non-hormonal, smart, and multipurpose prevention technologies, elevating product diversity within the contraceptive devices market.

Key Take Aways

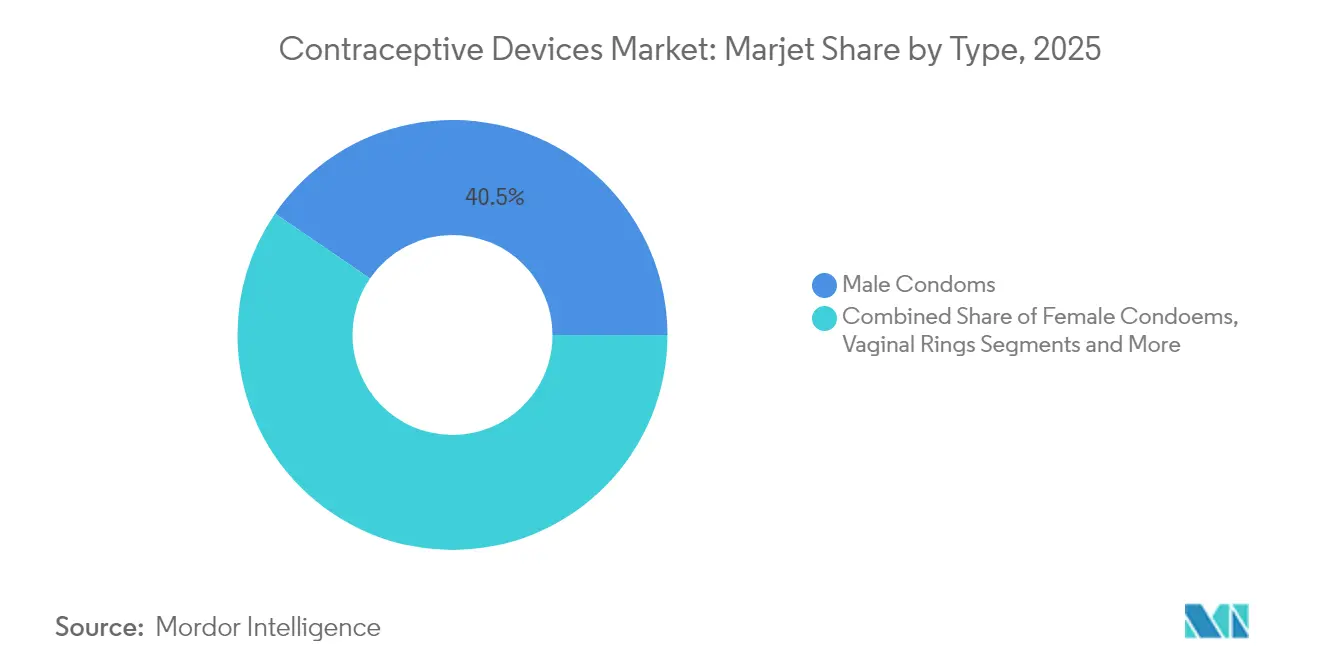

- By type, male condoms led with 40.45% of the contraceptive devices market share in 2025, whereas contraceptive implants are forecast to expand at a 9.34% CAGR to 2031.

- By gender, the male segment held 53.68% share of the contraceptive devices market size in 2025, while the female segment is projected to advance at a 7.18% CAGR through 2031.

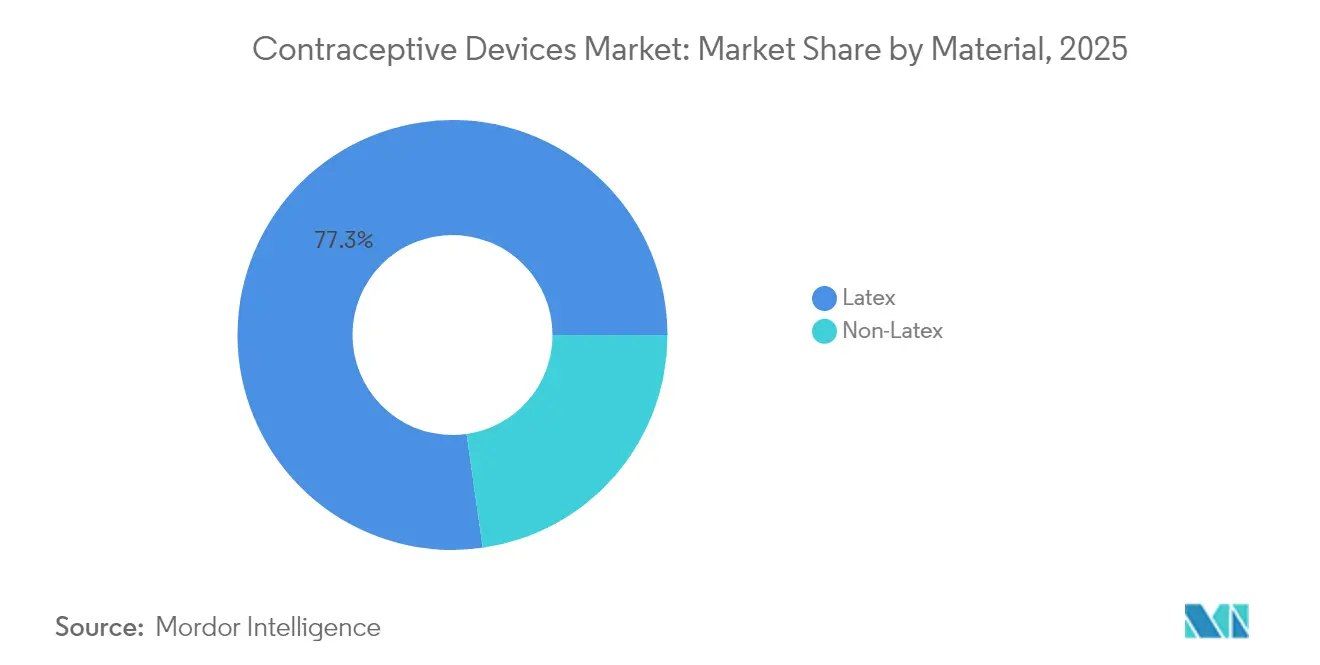

- By material, latex products commanded 77.25% share in 2025; the non-latex segment is expected to grow at a 9.02% CAGR over the same period.

- By distribution channel, retail pharmacies generated 44.43% revenue share in 2025, yet online/direct-to-consumer platforms are set to grow at a 9.92% CAGR up to 2031.

- By geography, Asia-Pacific accounted for 31.55% of the contraceptive devices market share in 2025, whereas the Middle East & Africa region is poised for the fastest growth at an 8.44% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Contraceptive Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Preference for Long-Acting Reversible Contraceptives (LARC) | +1.5% | North America and Europe, with increasing adoption in Asia-Pacific | Medium term (2-4 years) |

| High Burden of Sexually Transmitted Disease (STD) and Rising Awareness About STD | +1.0% | Global, with particular impact in North America, Europe, and urban centers in developing regions | Short term (≤ 2 years) |

| Initiatives Taken By Government and Private Firms | +0.7% | Asia-Pacific, Middle East and Africa, Latin America | Medium term (2-4 years) |

| Technological Advancements and Product Innovation | +1.2% | Global, with initial impact in North America and Europe | Long term (≥ 4 years) |

| High Rate of Unintended Pregnancies and Delayed Family Planning | +0.6% | Global, with significant impact in developing regions | Medium term (2-4 years) |

| Rapid Adoption of Telemedicine & Subscription-Based Direct-to-Consumer Platforms | +0.8% | North America & Europe, with gradual expansion to urban areas in developing regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Preference for Long-Acting Reversible Contraceptives (LARC)

LARC usage in the United States climbed from 2% in 2002 to 16% by 2019 and continues to rise through 2025, reflecting superior efficacy and convenience. Health-system initiatives that authorize nurses to place implants and IUDs in single-visit encounters remove access frictions and lower unintended pregnancy costs. Medicaid reimbursement reforms in 37 states cover same-day insertions, reducing high upfront outlays for low-income users. Training curricula covering counseling and insertion techniques now appear in 65% of medical schools, narrowing provider knowledge gaps. Economic studies suggest that every percentage-point shift from short-acting methods to LARCs yields measurable savings by preventing costly unplanned births. These factors elevate LARC penetration, thereby underpinning revenue expansion within the contraceptive devices market.

High Burden of Sexually Transmitted Disease and Rising Awareness

Surveillance in New York City showed upticks in chlamydia and gonorrhea cases in 2023, most pronounced among Black and Latina youth.[1]NYC Health Department, “STI Surveillance Data 2023,” nyc.govThe epidemiological pattern drives interest in multipurpose prevention technologies that block infection and pregnancy in one device. Prototypes include female condoms imbued with antimicrobial agents and vaginal rings releasing antiviral compounds alongside hormones, now progressing through trials under WHO coordination who.int. Public-health campaigns that spotlight dual-protection benefits boost condom and barrier sales, while research grants stimulate agile startups developing microbicidal coatings. Heightened risk perception therefore accelerates demand, enlarging the contraceptive devices market.

Technological Advancements and Product Innovation

Biomedical microelectromechanical systems enable implantable devices with wireless dose modulation and multi-year lifespans. Daré Bioscience demonstrated proof of concept for its DARE-LARC1 implant in 2024, targeting up to 20 years of contraceptive coverage with external activation control.[2]Daré Bioscience, “DARE-LARC1 Platform Technology Achieves Proof of Concept,” darebioscience.comSmart contraceptive rings pair with mobile applications to log adherence and tailor hormone release profiles, while biodegradable polymers promise “set-and-forget” implants that dissolve after use, eliminating removal visits. These features align with consumer expectations for convenience, personalization, and minimal clinical touchpoints, reinforcing the technology-driven curve of the contraceptive devices market.

Rapid Adoption of Telemedicine & Subscription-Based Direct-to-Consumer Platforms

Prescription contraceptive fulfillment increasingly occurs through virtual clinics that integrate video counseling, e-prescribing, and discreet doorstep delivery. Regulatory clarity around interstate telehealth commerce in the United States and Europe shortens procurement cycles and normalizes online renewal, driving a 10.1% CAGR in digital channel revenues. Subscription services bundle device refills, STI test kits, and educational content, creating predictable recurring revenue streams for suppliers. This distribution shift erodes traditional pharmacy dominance yet broadens reach, especially among younger cohorts. The convenience premium attached to digital pathways translates into incremental sales volume for the contraceptive devices market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cultural & Religious Opposition to Sterile Barrier Methods | -0.7% | Middle East and Africa, South Asia, Latin America | Long term (≥ 4 years) |

| Lower Physician Confidence for Certain Contraceptive Options | -0.5% | Global, with particular impact in developing regions | Medium term (2-4 years) |

| Product Litigation Issues | -0.4% | North America, Europe | Short term (≤ 2 years) |

| Stringent Regulatory Scenario | -0.3% | Global, with significant impact in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cultural and Religious Opposition to Sterile Barrier Methods

Modern contraceptive uptake in Saudi Arabia reached 46% in 2023, yet community norms still discourage barrier methods for married women, limiting condom and diaphragm penetration.[3]World Health Organization, “Contraception Fact Sheet,” who.intRecent legal reforms that prohibit marriage under 18 signal gradual attitudinal shifts, but long-standing beliefs continue to impede adoption across parts of the Middle East & Africa. Faith-based organizations often wield influence over reproductive choices, necessitating culturally tailored advocacy to recalibrate perceptions. Without such engagement, usage gaps persist, tempering growth prospects in these high-population markets within the contraceptive devices market.

Lower Physician Confidence for Certain Contraceptive Options

The 2024 US Medical Eligibility Criteria update reclassified injectable depot medroxyprogesterone acetate for users at elevated thromboembolic risk, raising counseling complexity. Similar guideline shifts worldwide compel clinicians to weigh nuanced risk-benefit profiles, especially for patients with comorbidities. Limited hands-on training in IUD insertions or implant removals curtails method recommendations, a constraint amplified in busy primary-care settings. Studies show that provider endorsement strongly predicts patient uptake; hesitant counseling therefore suppresses potential demand and restrains the contraceptive devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: LARCs Gain Despite Condom Dominance

Male condoms captured 40.45% of the contraceptive devices market share in 2025 thanks to affordability, accessibility, and dual-protection features. Perfect use offers 98% efficacy, but real-world effectiveness drops to 87% due to inconsistent or incorrect application. Nevertheless, rising latex-allergy awareness, interest in enhanced sensation, and digital ordering conveniences sustain steady volume. In parallel, implant sales climb at a 9.34% CAGR to 2031, underpinning a notable slice of the contraceptive devices market size for long-acting methods. Wireless-enabled implants and biodegradable variants reduce clinic visits, encourage first-time adoption, and mitigate removal barriers, reinforcing their growth momentum.

Development pipelines underscore broadening choices. Hormonal IUDs deliver non-contraceptive benefits such as lighter bleeding, bolstering uptake among women who previously avoided device-based options. Single-handed inserters launched in 2024 streamline placement, decreasing procedure time and pain signals. Vaginal rings advance through trials with both hormonal and non-hormonal compositions; the investigational monthly Ovaprene ring demonstrated strong post-coital reductions in motile sperm. Each innovation diversifies method mix, cushioning revenue streams across the contraceptive devices market.

By Gender: Female Segment Accelerating Growth

The male cohort accounted for 53.68% of 2025 sales, yet condom usage among European adolescents slipped to 61% in the latest WHO survey, hinting at plateauing penetration.The female segment is forecast to outpace at a 7.18% CAGR, reflecting greater decision autonomy, discreet options, and device personalization. Smart rings that pair with apps for dosage tracking and biodegradable implants, appealing to long-term planners, broaden method portfolios. Multipurpose prevention devices that marry pregnancy avoidance with antimicrobial protections resonate with women prioritizing holistic sexual health, enlarging the contraceptive devices market size for female-targeted products.

Emergent FemTech solutions enable self-administration and real-time data capture, compelling insurers to recognize patient-generated metrics in coverage decisions. As urbanization and workforce participation rates climb, the convenience value of low-maintenance methods rises, further lifting female segment revenues within the contraceptive devices market.

By Material: Non-Latex Gaining Momentum

Latex still accounts for 77.25% of unit sales and remains the cost-efficient material of choice for condoms. Concerns over allergies, odor, and sensitivity, however, push non-latex categories toward a 9.02% CAGR, with nitrile and polyurethane alternatives capturing attention. Reckitt Benckiser plans Q1 2025 launch of nitrile condoms in Europe, signaling mainstream commercialization after robust Chinese demand. The contraceptive devices market size for non-latex offerings benefits from premium pricing tied to perceived comfort and safety.

Beyond condoms, biodegradable polymers enter implant development pipelines, promising eventual absorption and eliminating removal procedures. Smart rings fabricated from medical-grade silicone enable embedded electronics without compromising flexibility. Manufacturers that integrate material science breakthroughs with user-centric design gain competitive lift in the contraceptive devices market.

By Distribution Channel: Digital Disruption Accelerates

Retail pharmacies retained 44.43% revenue share in 2025 due to broad geographic reach and immediate product availability. Yet the online/D2C channel, rising at a 9.92% CAGR, reshapes purchasing behavior, especially among Gen Z and Millennials who value discretion and doorstep delivery. Telemedicine portals bundle e-consults, device prescriptions, and automatic refills, compressing consultation-to-usage timelines. The contraceptive devices market size for digital distribution scales further as payment platforms integrate flexible spending account compatibility, smoothing transaction friction.

Hospitals and specialty clinics maintain importance for LARCs that need professional insertion. Simplified insertion tools cut chair time, enabling higher throughput. NGO and government programs channel subsidized devices into underserved areas, as evidenced by a 17% rise in contraceptive procurement across 85 lower-income countries between 2022 and 2023. Collectively, these channels balance reach, counseling, and affordability across the contraceptive devices market.

Geography Analysis

Asia-Pacific generated 31.55% of revenues in 2025, propelled by large reproductive-age populations, declining fertility intentions, and strengthened public health budgets. Country programs in China, India, and Indonesia deploy postpartum LARC initiatives, rural outreach, and digital education campaigns, narrowing urban–rural usage gaps. However, disparities linger among adolescents and marginalized groups, creating addressable pockets of unmet need that extend runway for the contraceptive devices market.

The Middle East and Africa region is forecast to grow at an 8.44% CAGR through 2031. Saudi Arabia’s adolescent birth rate fell from 8.65 per 1,000 in 2009 to 8.28 in 2021 after education and youth empowerment investments. Partnerships such as Bayer and UNFPA Egypt target 810,000 women by 2028 with modern devices, illustrating how multilateral funding accelerates adoption. Despite cultural constraints, improving female literacy and employment weave a supportive backdrop for the contraceptive devices market.

North America and Europe exhibit high method diversity, favorable reimbursement, and rapid uptake of innovative devices. FDA approvals of single-handed IUD inserters and ongoing subsidy expansions under the Affordable Care Act elevate accessibility. Latin America faces persistent adolescent pregnancy costs estimated at USD 15.3 billion per year, catalyzing national health ministries to promote LARC usage among teenagers. Region-wide campaigns that highlight over-99% efficacy of IUDs and implants aim to curb unintended births, bolstering the contraceptive devices market.

Competitive Landscape

The contraceptive devices market remains moderately fragmented. Bayer AG, Cooper Surgical, and Reckitt Benckiser anchor their positions through scale, brand recognition, and multiregional distribution. Cooper Surgical’s 2024 launch of a single-handed Paragard inserter simplifies procedure workflows, reinforcing its IUD niche. Reckitt Benckiser leverages supply-chain depth to introduce nitrile condoms in Europe, aligning product roadmaps with allergy-aware consumers.

Mid-tier companies pursue innovation in non-hormonal and smart platforms. Daré Bioscience’s wireless-controlled implant targets decades of coverage, a leap beyond current ten-year products. FemTech startups package remote prescription services with device delivery, challenging incumbents to accelerate their digital pivot. Strategic collaborations with NGOs and global health agencies open subsidized channels in emerging economies, as evidenced by Bayer’s expanding UNFPA partnership valued at EUR 170,000 in cumulative funding.

Patent portfolios, manufacturing know-how, and regulatory agility serve as core differentiators, yet user experience and privacy assurances increasingly drive brand loyalty. Firms that integrate real-time data, smartphone interfaces, and discreet shipping position themselves to capture elastic demand segments across the contraceptive devices market. As consolidation pressures surface, acquisitions of technology-rich startups by diversified healthcare conglomerates appear probable.

Contraceptive Devices Industry Leaders

Cooper Surgical Inc.

Reckitt Benckiser Group PLC

Bayer AG

Karex Berhad

Church & Dwight Co. Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Bayer expanded its partnership with UNFPA Egypt with an additional EUR 100,000 funding, aiming to reach 810,000 women with family planning services and ensure 540,000 women receive modern contraceptive methods by 2028.

- February 2025: Daré Bioscience and Theramex entered a co-development and licensing deal for Casea S, a biodegradable contraceptive implant now in Phase 1 trials.

- January 2025: Daré Bioscience announced technological proof of concept for its DARE-LARC1 wireless-controlled long-acting implant platform.

- November 2024: The US Department of Health & Human Services issued the HIPAA Privacy Rule Final Rule that enhances privacy protections for reproductive health care.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global contraceptive devices market as all barrier and long-acting reversible products, condoms, diaphragms, cervical caps, sponges, vaginal rings, intra-uterine devices, and sub-dermal implants, supplied new for human birth-control use. Values are expressed in USD at manufacturer selling price.

Scope exclusion: Hormonal pills, injectables, topical gels, fertility drugs, and any aftermarket accessories are not covered.

Segmentation Overview

- Non-Latex (Polyurethane, Poly-isoprene and others)

- Female Condoms

- Intra-Uterine Devices (IUD)

- Hormonal IUD

- Copper IUD

- Contraceptive Implants

- Vaginal Rings

- Diaphragms and Cervical Caps

- Contraceptive Sponges

- By Gender

- Male

- Female

- By Material

- Latex

- Non-Latex

- By Distribution Channel

- Hospital and Specialty Clinics

- Retail Pharmacies and Drug Stores

- Online Pharmacies and D2C Platforms

- NGO and Government Programmes

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts then interview public-health program managers, procurement officers, gynecologists, retail pharmacy buyers, and device distributors across Africa, Asia, the Americas, and Europe. These conversations validate usage trends, average selling prices, unmet need pockets, and upcoming tenders that secondary data alone cannot surface.

Desk Research

We first collect multi-year volume and value data from trusted public sources such as UNFPA's contraceptive procurement database, WHO's FP2020 dashboards, national health statistics portals, and customs shipment records. Additional context is drawn from peer-reviewed journals, trade association briefs, patent filings via Questel, and company 10-Ks. These inputs anchor historical demand, pricing corridors, and regulatory timelines. The sources listed illustrate our approach and are not exhaustive; many other open datasets enrich the evidence pool.

Market-Sizing & Forecasting

A top-down model starts with country-level modern contraceptive prevalence rates and reproductive-age female populations, which are then matched with public and private device distribution volumes to rebuild 2024 demand. Select bottom-up cross-checks, supplier shipment roll-ups and sampled ASP × units, calibrate totals. Key variables include mCPR movement, commodity donation flows, average device replacement cycles, regulatory approvals of next-generation LARCs, and e-commerce share gains. Forecasts to 2030 rely on multivariate regression blended with scenario analysis, letting birth-rate elasticity, government funding shifts, and GDP per capita trajectories drive outlook ranges. Data gaps, when encountered, are bridged through weighted regional proxies vetted in follow-up calls.

Data Validation & Update Cycle

Every output passes a two-step peer review and an automated variance check against independent indicators such as latex import volumes and NGO distribution reports. We refresh the model annually; material events, large tenders, landmark approvals, and policy changes trigger interim revisions before client delivery.

Why Our Contraceptive Devices Baseline Commands Reliability

Published estimates differ because firms apply distinct device baskets, price assumptions, and refresh cadences.

According to Mordor Intelligence, careful scope discipline and yearly updates reduce those swings.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 19.20 B (2025) | Mordor Intelligence | - |

| USD 10.54 B (2024) | Global Consultancy A | Excludes implants and NGO channel volumes; covers 12 major countries only |

| USD 21.39 B (2024) | Industry Association B | Bundles fertility-tracking devices and mixed drug-device kits, inflating totals |

These comparisons show that when device scope is narrowly defined or overly broad, figures skew low or high. Our balanced mix of public data, frontline interviews, and timely revisions therefore provides decision-makers with a dependable, transparent baseline.

Key Questions Answered in the Report

What is the current size of the contraceptive devices market?

The contraceptive devices market is valued at USD 20.38 billion in 2026.

How fast is the contraceptive devices market expected to grow?

It is forecast to expand at a 6.15% CAGR, reaching USD 27.47 billion by 2031.

Which product category is growing the quickest?

Contraceptive implants are set to grow at a 9.34% CAGR, the fastest among device types.

Why is Asia-Pacific leading the contraceptive devices market?

Asia-Pacific accounted for 31.55% of the contraceptive devices market share in 2025 over the forecast period (2026-2031).

How are digital channels influencing sales?

Online and direct-to-consumer platforms are registering a 9.92% CAGR as telemedicine streamlines prescriptions and discreet delivery

What materials are gaining popularity beyond latex?

Nitrile and polyurethane condoms, along with biodegradable polymers for implants, are growing at a 9.02% CAGR due to allergy and sustainability considerations.

Page last updated on: