Uterine Serous Carcinoma Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

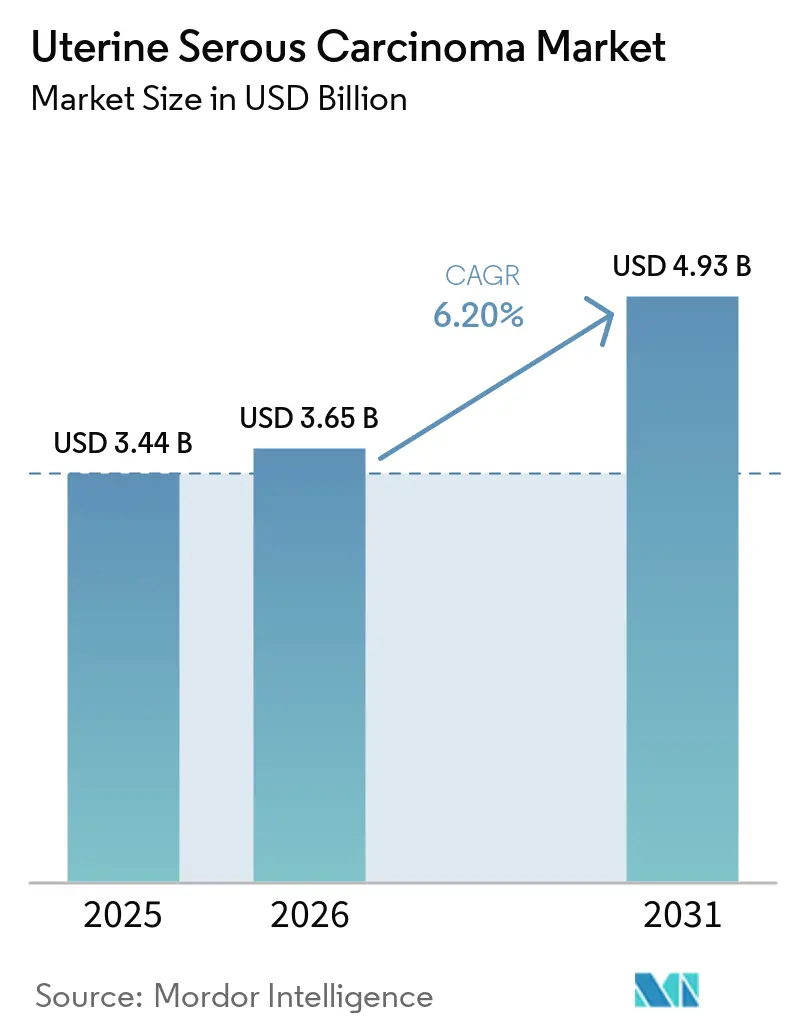

| Market Size (2026) | USD 3.65 Billion |

| Market Size (2031) | USD 4.93 Billion |

| Growth Rate (2026 - 2031) | 6.20% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Uterine Serous Carcinoma Market Analysis by Mordor Intelligence

The Uterine Serous Carcinoma Market size is projected to expand from USD 3.44 billion in 2025 and USD 3.65 billion in 2026 to USD 4.93 billion by 2031, registering a CAGR of 6.20% between 2026 to 2031.

Checkpoint-inhibitor doublets, which extend progression-free survival, are being rapidly adopted. Additionally, trastuzumab deruxtecan, approved for broader HER2-positive eligibility, is gaining traction with its tumor-agnostic approval. In the United States, Canada, Germany, and Australia, payer reforms now support reimbursement for comprehensive genomic profiling. Regulators are prioritizing combination endpoints over single-agent response rates, accelerating pipeline momentum and reducing development timelines by 18 to 24 months. Simultaneously, the introduction of low-cost pembrolizumab biosimilars in Asia is reducing price premiums previously limited to North America while increasing access in markets that have traditionally relied on generic chemotherapy. These factors are shaping a competitive global landscape, requiring manufacturers to balance innovation and affordability to maintain or capture market share in uterine serous carcinoma.

Key Report Takeaways

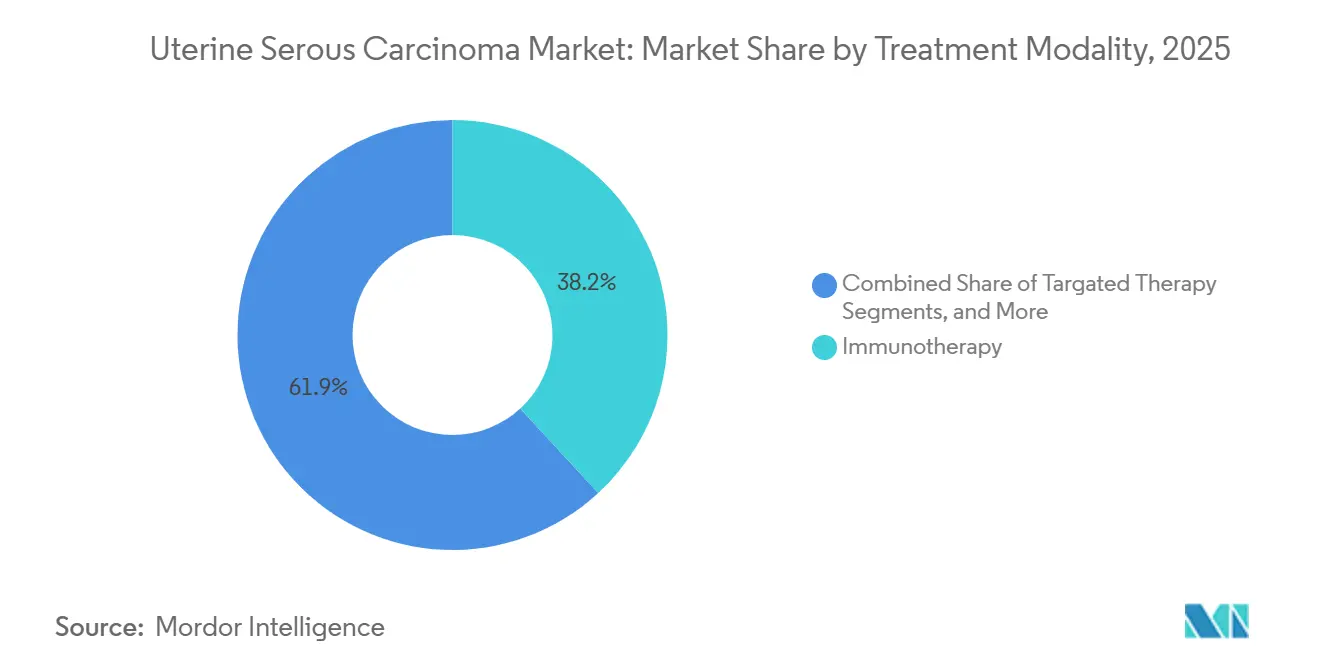

- By treatment modality, immunotherapy led with 38.15% of the uterine serous carcinoma market share in 2025, while immunotherapy is advancing at the fastest CAGR of 7.34% through 2031.

- By drug class, immune checkpoint inhibitors captured 35.45% of revenue in 2025, but HER2-targeted monoclonal antibodies are projected to post the highest 6.75% CAGR to 2031 on the strength of trastuzumab deruxtecan’s tumor-agnostic label.

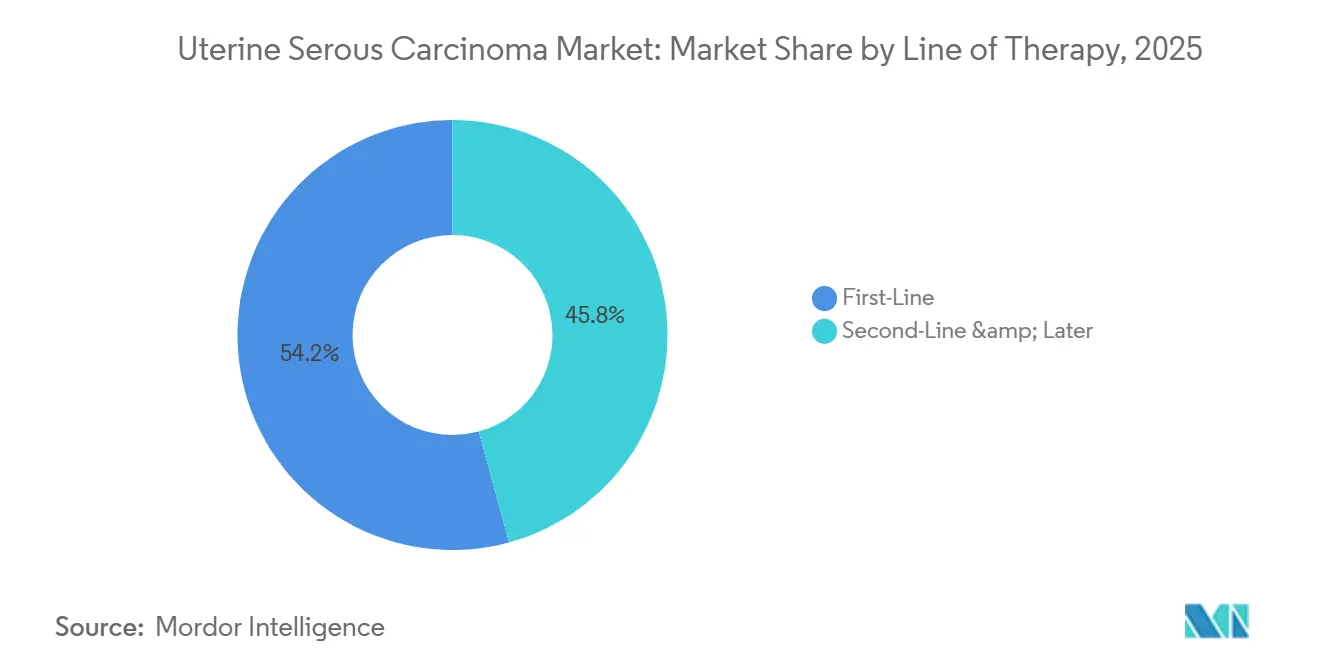

- By line of therapy, the first-line segment is forecast to expand at 7.15% from 2026-2031, narrowing the historical dominance of second-line and later therapy that still commanded 54.23% of spending in 2025.

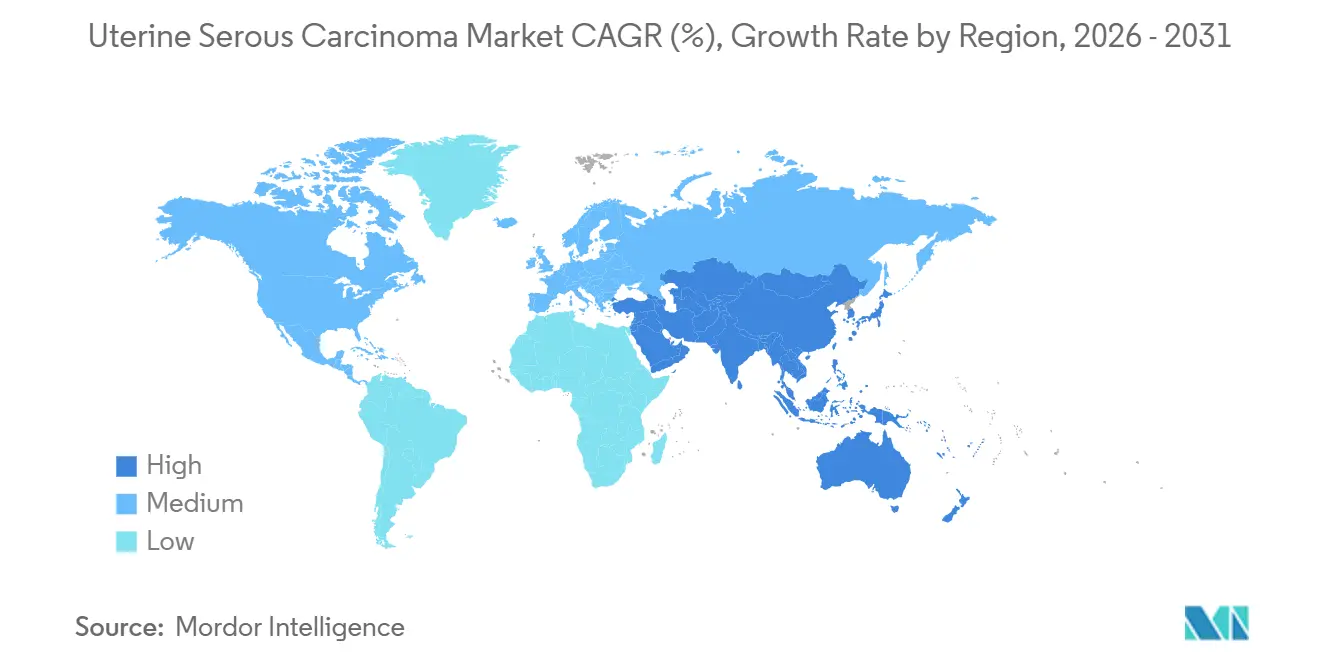

- By geography, North America retained 43.13% uterine serous carcinoma market share in 2025, but Asia-Pacific is the fastest-growing region at a 6.98% CAGR, thanks to rapid approvals of locally manufactured checkpoint inhibitors and widespread biosimilar uptake.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Uterine Serous Carcinoma Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising incidence linked to aging & obesity | +1.2% | Global, concentrated in North America, Europe, Gulf Cooperation Council states | Long term (≥ 4 years) |

| Regulatory approvals for immuno-oncology combinations | +1.5% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Uptake of molecular profiling & HER2 testing | +0.9% | North America, Western Europe, urban centers in China, Japan, South Korea | Medium term (2-4 years) |

| Expansion of investigator-sponsored trials & EAPs | +0.7% | North America, select European Union countries | Short term (≤ 2 years) |

| Companion-diagnostic reimbursement incentives (OECD) | +0.8% | OECD member states, early adoption in Australia, Canada, Germany | Medium term (2-4 years) |

| Fast-track synthetic-lethality pipeline inflection | +0.6% | North America, Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence Linked to Aging & Obesity

The global rise in metabolic syndrome is driving a steady increase in endometrial cancer diagnoses, with a pronounced shift toward serous histology among women over 60. Obesity-related inflammation elevates peripheral estrogen levels, encouraging TP53 mutations that typify the serous subtype and shorten the interval from stage I to metastatic disease. Japan, Italy, and South Korea face a triple burden of aging populations, delayed first pregnancies, and reduced parity, all of which extend lifetime estrogen exposure. Consequently, the addressable patient pool is expanding faster than historical averages, stimulating sustained demand for first-line immune-checkpoint doublets and salvage antibody-drug conjugates through 2031. Health ministries are already signaling higher budget allocations for gynecologic oncology, locking in multiyear procurement contracts that underpin volume certainty for drug makers.

Regulatory Approvals for Immuno-Oncology Combinations

The FDA’s June 2024 accelerated approval of pembrolizumab plus carboplatin-paclitaxel for newly diagnosed advanced disease cut the standard four-year bench-to-bedside interval in half, encouraging sponsors to file combination biologics earlier in development.[1]U.S. Food and Drug Administration, “FDA Grants Accelerated Approval to Pembrolizumab for Endometrial Carcinoma,” fda.gov The European Commission’s conditional nod four months later enabled pan-EU reimbursement negotiations and prompted several national payers to waive sequential chemotherapy prerequisites. Regulators in Japan, South Korea, and Australia rapidly adopted comparable review pathways, reducing the lag between U.S. and Asia-Pacific launches to under one year. These synchronized approvals compress time-to-revenue and push manufacturers to initiate global pivotal trials from day one to secure a wider uterine serous carcinoma market footprint.

Uptake of Molecular Profiling & HER2 Testing

Medicare’s 2024 decision to cover FoundationOne CDx and Guardant360 CDx sliced patient out-of-pocket costs from USD 5,800 to below USD 100, triggering a 40% spike in test volumes at National Cancer Institute-designated centers.[2]Centers for Medicare & Medicaid Services, “Medicare Coverage Database: Companion Diagnostics,” cms.gov Reflex HER2 testing identifies 15-30% of uterine serous carcinoma tumors as targetable, funneling thousands of patients toward trastuzumab deruxtecan and next-generation antibody-drug conjugates. Germany’s bundled reimbursement model, which rolls genomic testing into drug payment, is now being reviewed by several U.S. Medicare Advantage plans, suggesting imminent diffusion of the approach. Diagnostic vendors are responding with automated IHC algorithms that deliver same-day HER2 scores, trimming therapy initiation lag by two weeks in high-volume institutions.

Companion-Diagnostic Reimbursement Incentives

OECD health agencies now link premium pricing to mandatory biomarker utilization, rewarding manufacturers that co-develop diagnostics and drugs. Australia and Canada offer additional fee-for-service payments to pathologists who perform HER2 or mismatch-repair testing within 72 hours of biopsy receipt, driving double-digit adoption gains. Germany’s Federal Joint Committee recently codified outcome-based rebates that penalize manufacturers if companion diagnostic penetration falls below 80%, creating a powerful stick-and-carrot mechanism.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High cost & reimbursement hurdles for IO agents | -0.9% | Global, acute in Latin America, Eastern Europe, Middle East & Africa | Medium term (2-4 years) |

| Low biomarker-testing penetration in LMICs | -0.6% | Sub-Saharan Africa, South Asia, Southeast Asia, Central America | Long term (≥ 4 years) |

| Patient-pool limitations slowing trial recruitment | -0.4% | Global, most pronounced in rare-subtype trials | Short term (≤ 2 years) |

| Safety concerns over TKI + checkpoint blockade combos | -0.3% | North America, Europe, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Costs & Reimbursement Hurdles for IO Agents

In the United States, checkpoint inhibitors are priced between USD 150,000 and 200,000 annually per patient, resulting in prior-authorization requirements that can delay treatment by up to a month.[3]Merck & Co., “Form 10-K 2025,” merck.com Fourteen Medicaid programs in the United States mandate chemotherapy failure before approving immunotherapy, restricting its use as a first-line treatment. In Latin America, public insurers negotiate confidential rebates of 30-50%. However, budget caps limit drug availability to major academic centers. Private payers in the Gulf Cooperation Council require biomarker evidence and impose annual spending limits, often causing interruptions to therapy mid-cycle. These challenges collectively reduce the global market's compound annual growth rate for uterine serous carcinoma by nearly one percentage point.

Limited Biomarker-Testing in LMICs

Sub-Saharan Africa and Southeast Asia face a lack of next-generation sequencing and IHC capabilities. With fewer than 40 accredited molecular pathology labs serving populations exceeding 300 million, shipping tissue samples to reference centers in Singapore or Australia adds an additional USD 2,000 to costs. This process also extends turnaround times to six weeks, increasing the risk of disease progression before results are available. The Union for International Cancer Control has introduced a pilot hub-and-spoke model, but it currently covers less than 5% of eligible patients and depends heavily on donor funding, which is vulnerable to geopolitical instability. Due to the absence of robust diagnostic infrastructure, many oncologists default to platinum-based chemotherapy, limiting the adoption of advanced targeted and immuno-oncology treatments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Modality: Immunotherapy Leads Multi-Modal Integration

Immunotherapy accounted for a 38.15% share of the uterine serous carcinoma market size in 2025 and is projected to grow at a 7.34% CAGR through 2031. Pembrolizumab, combined with carboplatin-paclitaxel, advanced to first-line therapy following its FDA approval in June 2024, quickly replacing chemotherapy-only regimens at NCCN-designated centers. Dostarlimab monotherapy has become a preferred option for mismatch-repair-deficient tumors, achieving objective response rates exceeding 40%. Surgery continues to be the standard for early-stage disease, but neoadjuvant immunotherapy is reducing tumor volume in bulky stage III cases, improving resectability. Radiation therapy is now primarily used for palliating symptomatic pelvic relapse or brain metastases, reflecting a shift toward systemic control.

By Drug Class: HER2-Targeted Agents Disrupt Checkpoint Inhibitor Dominance

Immune checkpoint inhibitors captured 35.45% of revenue in 2025, but HER2-targeted antibodies are growing at a 6.75% CAGR, potentially closing the gap by 2031. The tumor-agnostic approval of trastuzumab deruxtecan in April 2024 generated immediate off-label demand among oncologists treating HER2-positive uterine serous carcinoma, a biomarker present in up to 30% of cases. DESTINY-Endometrial01, launched in June 2025, is evaluating the agent against physician’s-choice chemotherapy; positive results could establish antibody-drug conjugates as the standard second-line therapy. Meanwhile, early-stage bispecifics targeting HER2 and CD3 are entering Phase I trials, aiming to deliver localized cytotoxicity while sparing healthy tissue.

By Line of Therapy: First-Line Gains Compress Salvage Market

Second-line and later therapies represented 54.23% of 2025 spending, reflecting the aggressive progression of uterine serous carcinoma. However, first-line regimens are expected to grow at a 7.15% CAGR as immunotherapy-chemotherapy combinations extend median progression-free survival from 6.5 months with chemotherapy alone to 13.1 months. This improved durability delays recurrence and reduces near-term demand for salvage agents, compressing the second-line revenue pool. Paradoxically, patients who eventually fail first-line checkpoint inhibitors often present with immune-refractory disease characterized by MHC class I loss, prompting developers to innovate next-generation mechanisms such as TIGIT or LAG-3 blockade. As a result, the uterine serous carcinoma market is transitioning from volume-driven salvage cycles to higher-value first-line interventions supported by robust biomarker selection.

Geography Analysis

In 2025, North America held a dominant 43.13% share of the uterine serous carcinoma market, attributed to Medicare's efficient reimbursement process. Medicare reimburses drugs such as pembrolizumab, dostarlimab, and trastuzumab deruxtecan for FDA-approved indications without requiring prior authorization. Starting January 2026, the Inflation Reduction Act allows Medicare to negotiate prices for oncology drugs. This initiative is expected to reduce net costs by 25-40% for the highest-spending drugs. While this measure ensures continued patient access, it also moderates revenue growth, prompting manufacturers to explore opportunities in Asia to increase volumes.

Asia-Pacific is the fastest-growing region, advancing at a 6.98% CAGR. China's rapid approval of sintilimab and tislelizumab for MSI-high tumors, along with Japan's expedited designation for trastuzumab deruxtecan, has reduced the time-to-launch to less than nine months after first-in-class approvals. In South Korea and Australia, checkpoint inhibitors are reimbursed within 60 days of regulatory approval, making these countries early contributors to revenue.

Europe holds a stable share but displays heterogeneity. Germany and France reimburse immune-checkpoint combinations promptly, whereas Italy and Spain impose budget caps that delay adoption at the hospital level. Eastern European countries negotiate significant rebates but primarily restrict access to urban tertiary centers. In the Middle East and Africa, the uterine serous carcinoma market accounts for less than 5% of the total size due to systemic therapy penetration remaining low. Challenges such as limited cold-chain infrastructure, currency volatility, and insufficient local biologic manufacturing capacity hinder drug availability, emphasizing the need for international funding initiatives.

Competitive Landscape

Market concentration remains moderate, with Merck, GSK, Daiichi Sankyo, Pfizer (following its acquisition of Seagen), and Eisai collectively commanding around 65% of global revenue. They achieve this dominance through proprietary checkpoint inhibitors and antibody-drug conjugates. Merck leads in combination trial breadth, conducting 47 active studies on pembrolizumab in gynecologic oncology. These studies include innovative strategies like the TIGIT and LAG-3 triplet approaches, aimed at overcoming acquired resistance. GSK has expanded its Phase III portfolio for dostarlimab, strategically focusing on chemotherapy backbones to secure a leading position in first-line treatments. On another front, Pfizer is utilizing Seagen’s linker-payload technology. This move is set to accelerate the development of the next generation of HER2-directed antibody-drug conjugates, emphasizing enhanced bystander killing capabilities.

In the realm of diagnostics, innovation is emerging as a competitive differentiator. Companies like Guardant Health and Foundation Medicine are introducing liquid-biopsy platforms. Their technology can identify circulating tumor DNA within a swift seven-day window, allowing for timely therapy adjustments ahead of any radiographic progression. Moreover, strategic partnerships are linking these advanced diagnostics with established drug brands. This synergy is creating comprehensive treatment ecosystems, fostering strong loyalty among prescribers. Chinese innovators Innovent Biologics and Zai Lab are leveraging reduced trial expenses and expedited domestic pathways. They have introduced checkpoint inhibitors at prices 40-50% lower than their Western counterparts. With an eye on global expansion, they are positioning themselves to venture beyond Asia, especially as biosimilar regulations begin to relax in Europe and Latin America.

Uterine Serous Carcinoma Industry Leaders

AstraZeneca PLc

Merck & Co.

Pfizer Inc.

Eli Lilly & Co.

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Aprea Therapeutics completed a USD 30 million private placement to advance its WEE1 inhibitor APR-1051, resuming capital-market activity after earlier clinical setbacks.

- January 2026: Acrivon Therapeutics reported interim Phase IIb data showing a 52% confirmed ORR for CHK1/CHK2 inhibitor ACR-368 in platinum-resistant ovarian or endometrial serous cancer, and will expand the trial into Europe during Q1 2026.

- January 2026: Early proof-of-concept from the ongoing ACESOT-1051 trial revealed a partial response in a patient with PPP2R1A-mutated uterine serous carcinoma treated with APR-1051 at 150 mg, with dose escalation ongoing.

- November 2025: Zentalis Pharmaceuticals prioritized azenosertib for Cyclin E1-positive PROC and signaled that further uterine serous carcinoma work depends on partnerships or new capital allocation.

Global Uterine Serous Carcinoma Market Report Scope

As per the scope of the report, uterine serous carcinoma (USC) is a rare, highly aggressive form of endometrial (uterine lining) cancer, accounting for about 10% of cases but a disproportionate 40% of deaths. It is a Type II, high-grade cancer that typically affects postmenopausal women, often arising from atrophic endometrium rather than estrogen-driven hyperplasia. It is known for early, rapid metastasis and poor prognosis.

The uterine serous carcinoma market is segmented by treatment modality, drug class, line of therapy, and geography. By treatment modality, the market includes surgery, chemotherapy, radiotherapy, immunotherapy, and targeted therapy. By drug class, the market is segmented into immune checkpoint inhibitors, tyrosine-kinase inhibitors, HER2-targeted monoclonal antibodies, hormonal agents, and cytotoxic agents. By line of therapy, the market is categorized into first-line, second-line, and later. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Surgery |

| Chemotherapy |

| Radiotherapy |

| Immunotherapy |

| Targeted Therapy |

| Immune Checkpoint Inhibitors |

| Tyrosine-Kinase Inhibitors |

| HER2-targeted Monoclonal Antibodies |

| Hormonal Agents |

| Cytotoxic Agents |

| First-Line |

| Second-Line & Later |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Modality | Surgery | |

| Chemotherapy | ||

| Radiotherapy | ||

| Immunotherapy | ||

| Targeted Therapy | ||

| By Drug Class | Immune Checkpoint Inhibitors | |

| Tyrosine-Kinase Inhibitors | ||

| HER2-targeted Monoclonal Antibodies | ||

| Hormonal Agents | ||

| Cytotoxic Agents | ||

| By Line of Therapy | First-Line | |

| Second-Line & Later | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the uterine serous carcinoma market in 2026?

The uterine serous carcinoma market size stands at USD 3.65 billion in 2026 and is projected to reach USD 4.93 billion by 2031, growing at a 6.20% CAGR.

Which treatment modality holds the largest revenue share?

Immunotherapy leads, capturing 38.15% uterine serous carcinoma market share in 2025, and remains the fastest-growing modality through 2031.

What segment is expanding fastest by drug class?

HER2-targeted monoclonal antibodies are registering a 6.75% CAGR between 2026-2031 due to trastuzumab deruxtecans tumor-agnostic approval.

Which region shows the highest growth?

Asia-Pacific is advancing at a 6.98% CAGR through 2031, propelled by rapid approvals of local checkpoint inhibitors and biosimilar uptake.

What is the outlook for first-line therapy?

First-line regimens integrating pembrolizumab are projected to grow at 7.15% CAGR, steadily compressing the salvage-therapy segment by delaying recurrence.

Page last updated on: