Myomectomy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

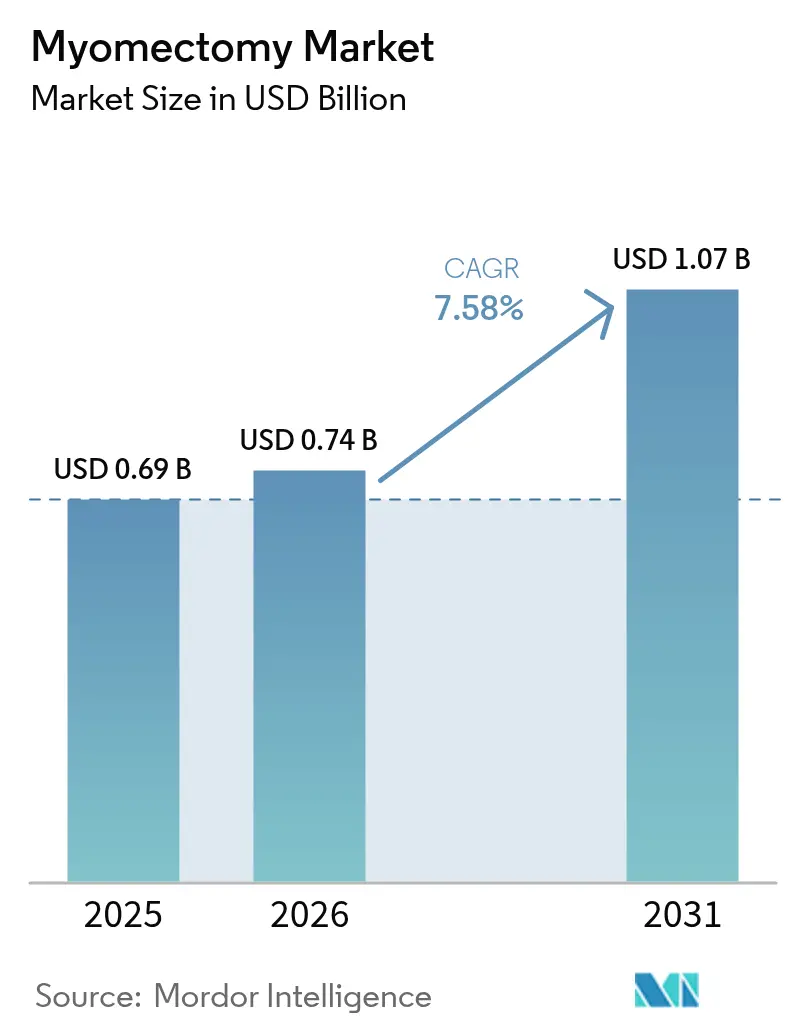

| Market Size (2026) | USD 0.74 Billion |

| Market Size (2031) | USD 1.07 Billion |

| Growth Rate (2026 - 2031) | 7.58% CAGR |

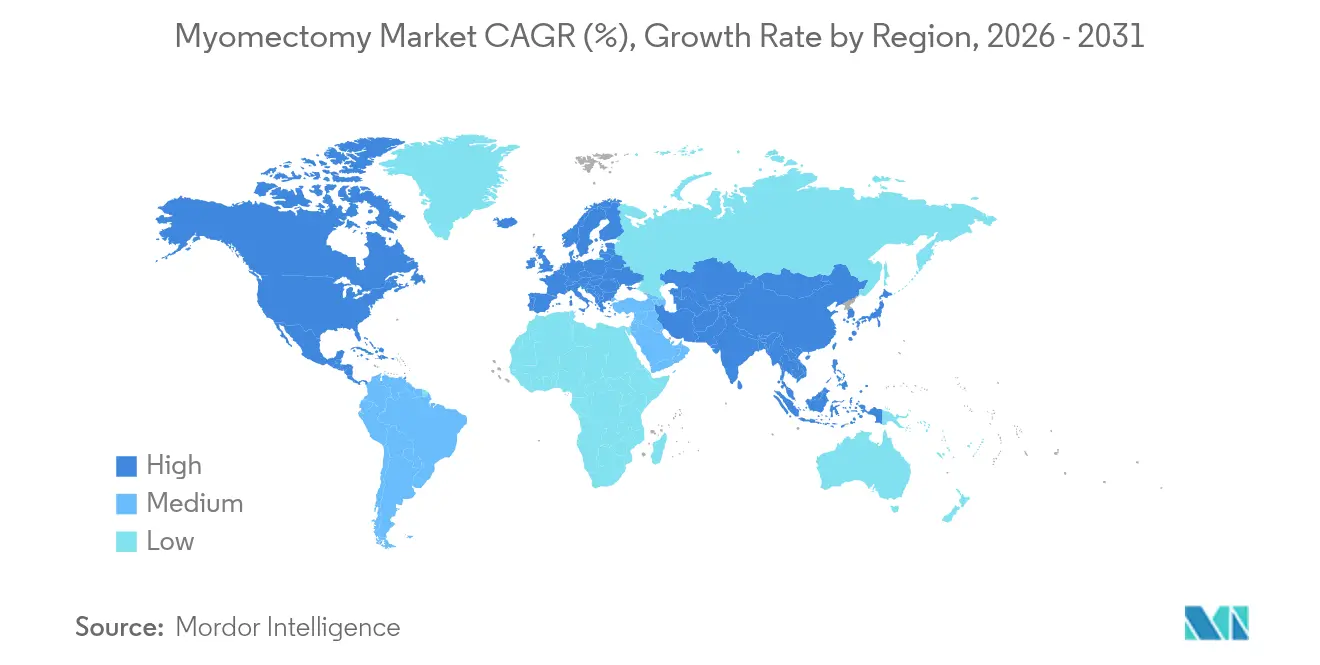

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Myomectomy Market Analysis by Mordor Intelligence

Myomectomy market size in 2026 is estimated at USD 742.3 million, growing from 2025 value of USD 0.69 billion with 2031 projections showing USD 1.07 billion, growing at 7.58% CAGR over 2026-2031. Sustained demand arises from women who postpone childbirth into their 30s and 40s, when fibroid incidence peaks, and who therefore favor uterus-sparing surgery over hysterectomy. Laparoscopic techniques still dominate but face increasing competition from robotic platforms that offer force-feedback precision and improved ergonomics. Regulatory endorsement of contained morcellation systems is steering product design toward safety without sacrificing minimally invasive access. At the care-delivery level, outpatient reimbursement for ambulatory surgical centers (ASCs) is expanding, encouraging procedure migration out of hospitals. Geographic growth patterns are split: North America preserves its lead share through established infrastructure, while Asia-Pacific (APAC) posts the fastest gains as governments invest in surgical capacity.

Key Report Takeaways

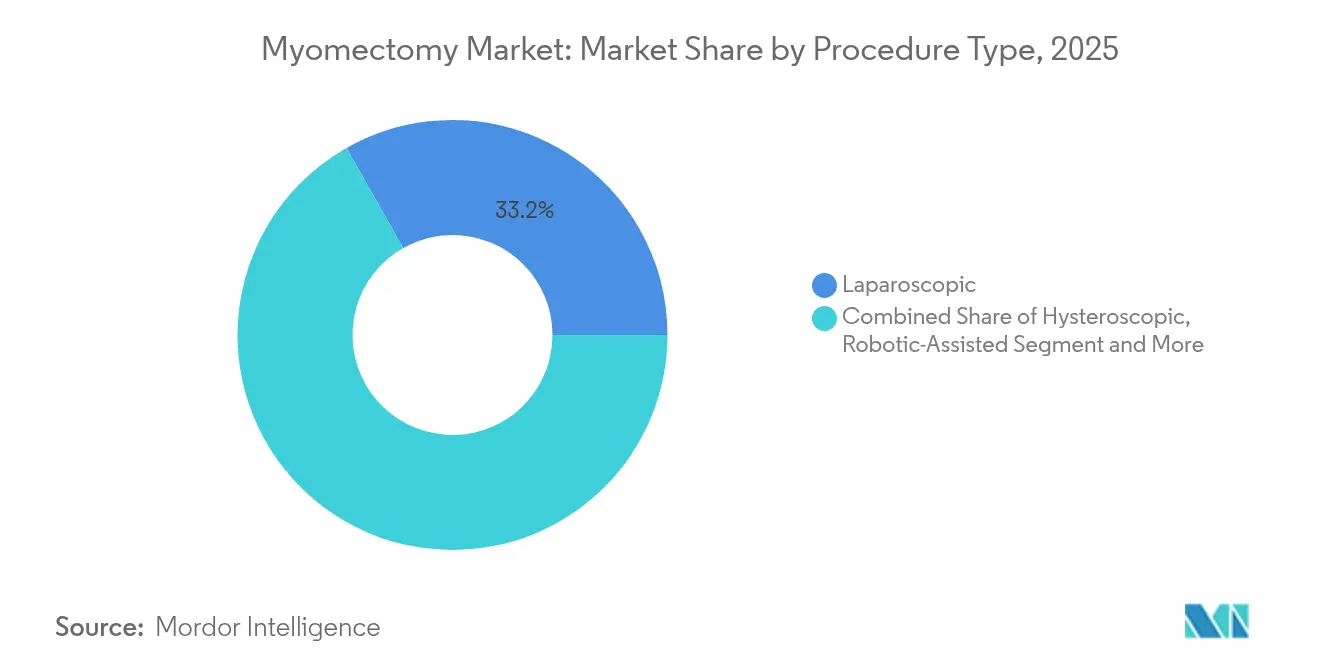

- By procedure type, laparoscopic surgery held 33.20% of myomectomy market share in 2025; robotic-assisted techniques are projected to grow at 9.46% CAGR to 2031.

- By product, laparoscopic power morcellators accounted for 21.10% share of the myomectomy market size in 2025, whereas tissue-removal systems are advancing at 9.92% CAGR through 2031.

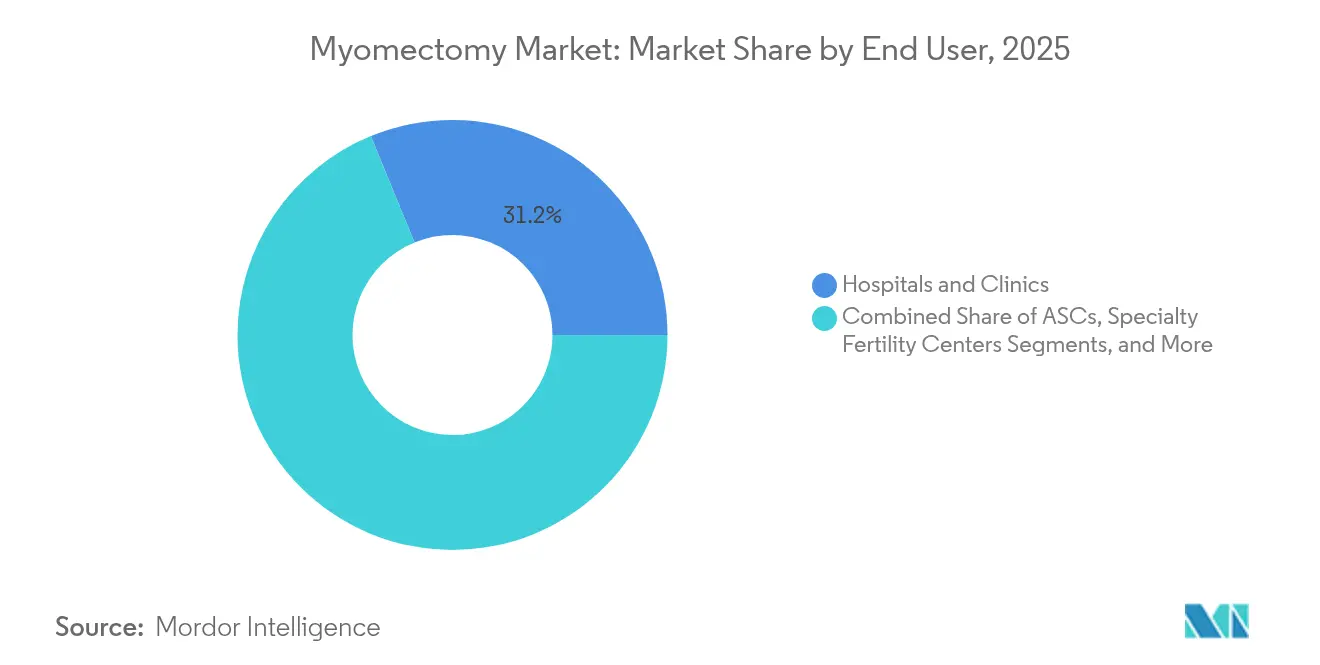

- By end user, hospitals & clinics led with 31.20% revenue share in 2025; ASCs display the highest forecast CAGR at 6.85% through 2031.

- By geography, North America controlled 31.40% myomectomy market share in 2025, while APAC is set to expand at 8.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Myomectomy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Incidence Of Uterine Fibroids Among Reproductive-Age Women | +1.80% | Global, with higher prevalence in North America and Sub-Saharan Africa | Long term (≥ 4 years) |

| Rising Adoption Of Minimally Invasive & Robotic-Assisted Surgeries | +2.10% | North America & Europe leading, APAC catching up | Medium term (2-4 years) |

| Increasing Fertility-Preservation Preference Delaying Hysterectomy | +1.50% | Global, particularly in developed markets | Long term (≥ 4 years) |

| Emergence Of Outpatient Reimbursement Models For ASC Procedures | +1.20% | North America primarily, expanding to Europe | Short term (≤ 2 years) |

| FDA Approval Of Contained Power Morcellators & New CPT Codes | +0.90% | North America, with regulatory spillover to other regions | Medium term (2-4 years) |

| Surge In Adjunct Uterine-Sparing Technologies | +1.00% | Global, with innovation centers in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Incidence of Uterine Fibroids Among Reproductive-Age Women

Fibroids now affect up to 70-80% of women by age 50, but the burden is most acute for those aged 25-44, the prime fertility window. Global surveillance recorded 9.6 million newly diagnosed cases in 2024.[1]Y. Zhang et al., “Global Trends in Uterine Fibroids Incidence,” cmj.orgAfrican ancestry doubles to triple the risk, compelling healthcare systems to prioritize uterus-sparing options. United States payers already spend USD 34.4 billion annually on fibroid care, reinforcing surgical demand. As delayed childbirth trends intersect with higher fibroid prevalence, the myomectomy market continues to expand.

Rising Adoption of Minimally Invasive & Robotic-Assisted Surgeries

From 2013 to 2019, robotic procedures grew from 16.3% to 30.3% of total U.S. surgeries; gynecology accounted for a substantial share.[2]A. Reynolds et al., “Robotic Surgical Volumes 2013-2019,” ajog.org The da Vinci 5 platform adds tactile feedback that lowers tissue trauma by 43%, addressing concerns over knot-tying accuracy and ergonomic strain. Nonetheless, capital outlays exceed USD 2 million per unit, and surgeons need 20–40 cases to achieve competence, slowing uptake in resource-constrained settings. Technical advantages, however, are gradually overriding cost hesitancy, feeding double-digit segment growth.

Increasing Fertility-Preservation Preference Delaying Hysterectomy

Prospective cohorts reveal similar quality-of-life outcomes for myomectomy and hysterectomy at 12 months, while pregnancy rates surpass 80% after minimally invasive myomectomy.[3]M. Bedient et al., “Fertility Outcomes after Myomectomy,” fertstert.org These clinical gains align with societal shifts toward later motherhood, reinforcing myomectomy as a first-line surgical option even for large or multiple fibroids. Body-image and sexual-function scores further tilt patient choice toward uterus preservation, strengthening procedure volumes.

Emergence of Outpatient Reimbursement Models for ASC Procedures

Medicare’s 2025 Outpatient Prospective Payment System added separate payment ladders for laparoscopic and robotic myomectomy, narrowing hospital–ASC parity gaps. Private insurers typically reimburse 200% of Medicare, enabling ASCs to cover capital and staffing costs efficiently. Clinical data confirm safety equivalence: it means blood loss averages 192 mL and discharge occurs within 23 hours. Pandemic-era patient preference for short stay further propels ASC share.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Advanced Laparoscopic & Robotic Systems | -1.40% | Global, particularly affecting emerging markets | Long term (≥ 4 years) |

| Safety Concerns Over Morcellation-Related Malignancy Spread | -0.80% | Global, with strictest regulations in North America | Medium term (2-4 years) |

| Skill Gap In Minimally Invasive Gynecologic Surgery In Emerging Markets | -1.10% | APAC, Latin America, Middle East & Africa | Long term (≥ 4 years) |

| Socio-Racial Disparities Limiting Access To Minimally Invasive Care | -0.60% | Global, with highest impact in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Laparoscopic & Robotic Systems

Hospitals face USD 2 million up-front costs plus maintenance when adopting robotic platforms, stretching capital budgets. Even with volume sharing, reaching economic break-even demands 150–200 annual cases. Emerging markets, where reimbursement is nascent, delay procurement and rely on conventional laparoscopy, restricting global diffusion.

Safety Concerns over Morcellation-Related Malignancy Spread

FDA advisories on power morcellation lowered usage rates until the bags, such as PneumoLiner, were contained and cleared. Trials record significant drops in peritoneal cell dissemination when containment is used. Nevertheless, additional device cost and longer operative time temper adoption, particularly for lower-resource centers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Procedure Type: Robotic Precision Challenges Laparoscopic Dominance

Laparoscopic surgery maintained a 33.20% myomectomy market share in 2025, thanks to surgeon familiarity and broad availability. Robotic-assisted procedures, advancing at 9.46% CAGR, are eroding this lead by offering 3-dimensional vision and articulated instruments that simplify suturing in confined pelvic spaces. Abdominal open myomectomy persists for very large or numerous fibroids, but steadily declines as minimally invasive proficiency climbs. Hysteroscopic resection holds traction for submucosal fibroids, aided by improved single-use shavers that lessen fluid overload risk. Vaginal approaches remain niche, reserved for select posterior wall tumors.

Technological progress reinforces the shift: force-feedback sensors in next-generation robots decrease unintended tissue strain, while single-port laparoscopy enhances cosmesis for select cases. Training initiatives from professional societies are accelerating skilled labor supply, which in turn widens patient access to minimally invasive care across tertiary centers. The combined impact cements robots as a future mainstream modality within the myomectomy market.

By Product: Contained Morcellation Drives Innovation

In 2025, laparoscopic power morcellators represented 21.10% revenue, yet face heightened scrutiny. Contained tissue-removal systems are rising at 9.92% CAGR as surgeons adopt bag-in-bag devices that satisfy regulatory guidance. Energy and sealing platforms, such as advanced bipolar or ultrasonic generators, deliver fine thermal control, improving hemostasis and shortening operative duration. Knotless barbed sutures accelerate closure, while enhanced visualization stacks integrate near-infrared imaging to delineate vasculature.

Product pipelines emphasize safety first: bagged morcellators reduce parasitic tissue implantation, and modular energy devices minimize collateral thermal spread. Smaller form-factor cameras with 4K resolution assist depth perception. Ancillary disposables, although low in unit price, generate repeatable revenue streams and incentivize vendors to bundle full procedural kits, shaping procurement dynamics in the myomectomy market.

By End User: ASCs Challenge Hospital Dominance

Hospitals and clinics accounted for 31.20% of procedures in 2025, benefiting from comprehensive perioperative infrastructure and resident training capacity. ASCs are gaining 6.85% CAGR momentum, underpinned by shorter scheduling queues, predictable operating costs, and physician ownership models that align incentives. Specialty fertility centers carve out a growing sub-segment, blending reproductive endocrinology services with fertility-preserving surgery to offer an integrated patient pathway.

Outcomes data favor outpatient care when patient selection protocols are strictly adhered to; conversion to inpatient status remains below 2%. Pay-for-performance frameworks increasingly reimburse on bundled episodes, awarding efficiency and low complication rates. Consequently, ASCs will continue to siphon elective, low-acuity myomectomy cases away from inpatient settings.

Geography Analysis

North America led the myomectomy market size at 31.40% share in 2025 due to robust insurance coverage and the world’s highest concentration of robotic systems, over 6,000 installed units. Early adoption of FDA-cleared containment devices sustains minimally invasive momentum despite heightened morcellation scrutiny. Yet access inequity persists; Black women are 30% less likely than their counterparts to receive laparoscopic myomectomy even when clinically eligible. Federal and state programs are funding surgeon-training scholarships to narrow this gap.

Asia Pacific is forecast to post the fastest regional CAGR of 8.52% to 2031, propelled by national health-insurance expansions, rising middle-class expectations, and localized medical-device manufacturing. China’s domestic robot makers are filing for National Medical Products Administration approvals, aiming to lower unit costs by up to 35% relative to imported systems. Japan and South Korea maintain procedure volumes comparable to Western peers, while India and Indonesia prioritize capacity building with laparoscopic platforms first who.int. Professional exchanges, online simulation modules, and traveling fellowships are lifting surgical skill levels.

Europe retains steady growth under the harmonized Medical Device Regulation that guarantees high safety standards. Public health systems reimburse minimally invasive gynecology widely, though austerity policies limit robotic capital budgets in certain markets.

Middle East & Africa are nascent but promising; flagship hospitals in Saudi Arabia and South Africa have adopted robotic programs, often via public-private partnerships. Latin America shows moderate expansion; in Mexico’s public sector only 16.5% of fibroid procedures are laparoscopic, yet private institutions in Brazil have introduced comprehensive myomectomy centers that double as regional training hubs.

Competitive Landscape

The myomectomy market is moderately fragmented, with Intuitive Surgical anchoring the robotic niche, Medtronic and Stryker supplying multi-specialty energy and visualization tools, and Hologic leading hysteroscopic tissue-extraction solutions. The collective market share of the top five suppliers reached 42% in 2024, leaving room for specialist entrants focused on contained morcellation or AI-guided image analytics.

Strategic consolidation is accelerating. Hologic finalized a USD 350 million acquisition of Gynesonics in January 2025, adding radiofrequency ablation to its fibroid portfolio and broadening cross-selling opportunities within gynecologic surgery. Medtronic expanded the footprint of its Hugo robot by signing multi-year procurement agreements with leading U.S. hospital chains. Intuitive Surgical, meanwhile, rolled out the da Vinci 5 with 150 improvements, most notably force-feedback haptics and enhanced 3D optics.

Emerging companies are disrupting cost structures. Domestic Asian manufacturers aim to supply sub-USD 1 million robotic platforms, and start-ups such as Anovo have demonstrated 97.6% performance equivalence to established electrosurgical tools while offering improved thermal safety margins. Portfolio differentiation now hinges on AI-driven workflow orchestration, reusable versus single-use instrumentation economics, and comprehensive post-sale training services. Competitive intensity is projected to rise as proprietary patents expire and regional players pursue CE marking and FDA clearance.

Myomectomy Industry Leaders

Medtronic PLC

Intuitive Surgical Inc.

Johnson & Johnson

Stryker Corporation

Karl Storz SE & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: FDA cleared the da Vinci 5 robotic platform, featuring 150 engineering enhancements.

- January 2025: Hologic completed its USD 350 million takeover of Gynesonics, integrating the incision-free Sonata System into its surgical suite.

- June 2024: The European Medical Device Coordination Group extended MDR transition provisions, safeguarding market continuity for legacy devices.

- March 2024: Boston Scientific launched upgraded CO₂ lasers for gynecology, expanding fibroid-resection options.

Global Myomectomy Market Report Scope

Myomectomy is a surgical procedure to remove fibroids from the uterus. It allows the uterus to be left in place. It is for women who wish to get pregnant after receiving treatment for their fibroids. This procedure is considered the standard of care for removing fibroids and preserving the uterus.

The myomectomy market is segmented by type, product, end user, and geography. By type, the market is segmented into abdominal, laparoscopic, hysteroscopic, and robotic. By product, the market is segmented into laparoscopic power morcellators, harmonic scalpels, laparoscopic sealers, and others. By end user, the market is segmented into clinics/hospitals and ambulatory surgical centers. By geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the World. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (USD) for all the segments mentioned above.

| Abdominal (Open) Myomectomy |

| Laparoscopic Myomectomy |

| Hysteroscopic Myomectomy |

| Robotic-Assisted Myomectomy |

| Vaginal Myomectomy |

| Laparoscopic Power Morcellators |

| Tissue Removal Systems (Hysteroscopic Morcellators) |

| Energy & Sealing Devices |

| Suturing & Closure Devices |

| Imaging & Navigation Systems |

| Ancillary Instruments & Consumables |

| Hospitals & Clinics |

| Ambulatory Surgical Centers |

| Specialty Fertility Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Procedure Type | Abdominal (Open) Myomectomy | |

| Laparoscopic Myomectomy | ||

| Hysteroscopic Myomectomy | ||

| Robotic-Assisted Myomectomy | ||

| Vaginal Myomectomy | ||

| By Product | Laparoscopic Power Morcellators | |

| Tissue Removal Systems (Hysteroscopic Morcellators) | ||

| Energy & Sealing Devices | ||

| Suturing & Closure Devices | ||

| Imaging & Navigation Systems | ||

| Ancillary Instruments & Consumables | ||

| By End User | Hospitals & Clinics | |

| Ambulatory Surgical Centers | ||

| Specialty Fertility Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current myomectomy market size?

The myomectomy market size stands at USD 742.3 million in 2026 and is projected to hit USD 1.07 billion by 2031.

Which procedure type is growing fastest?

Robotic-assisted myomectomy is expanding at 9.46% CAGR, outpacing laparoscopic and open techniques.

Why are ambulatory surgical centers important for myomectomy?

Enhanced reimbursement and patient preference for outpatient care allow ASCs to grow at 6.85% CAGR while delivering comparable safety outcomes.

What regions hold the greatest growth opportunity?

Asia Pacific leads with an 8.52% CAGR forecast, driven by rising healthcare investment and technology localization.

How do FDA guidelines influence morcellation products?

Containment mandates have sparked innovation in tissue-extraction systems, shifting demand toward compliant devices.

Page last updated on: