Endometrial Ablation Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

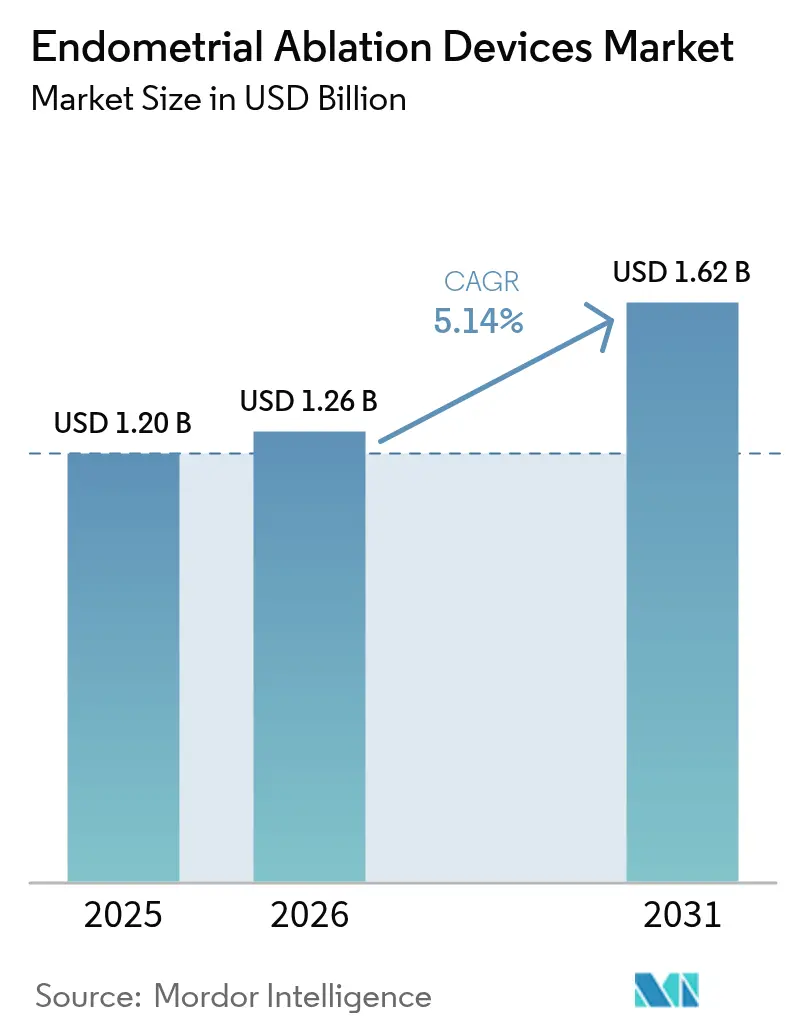

| Market Size (2026) | USD 1.26 Billion |

| Market Size (2031) | USD 1.62 Billion |

| Growth Rate (2026 - 2031) | 5.14% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Endometrial Ablation Devices Market Analysis by Mordor Intelligence

The endometrial ablation devices market size was valued at USD 1.20 billion in 2025 and estimated to grow from USD 1.26 billion in 2026 to reach USD 1.62 billion by 2031, at a CAGR of 5.14% during the forecast period (2026-2031). Demand is rising as clinicians replace hysterectomy with less invasive solutions for abnormal uterine bleeding (AUB). Thermal systems remain dominant, but non-thermal technologies are scaling quickly on precision benefits. Regulatory guidance that tightens safety verification, broader reimbursement for office-based care, and investments in single-use platforms collectively shape near-term growth. Competitive focus is shifting to artificial-intelligence (AI) guidance, disposable hysteroscopic instruments, and outpatient-friendly designs that lower total procedure cost.

Key Report Takeaways

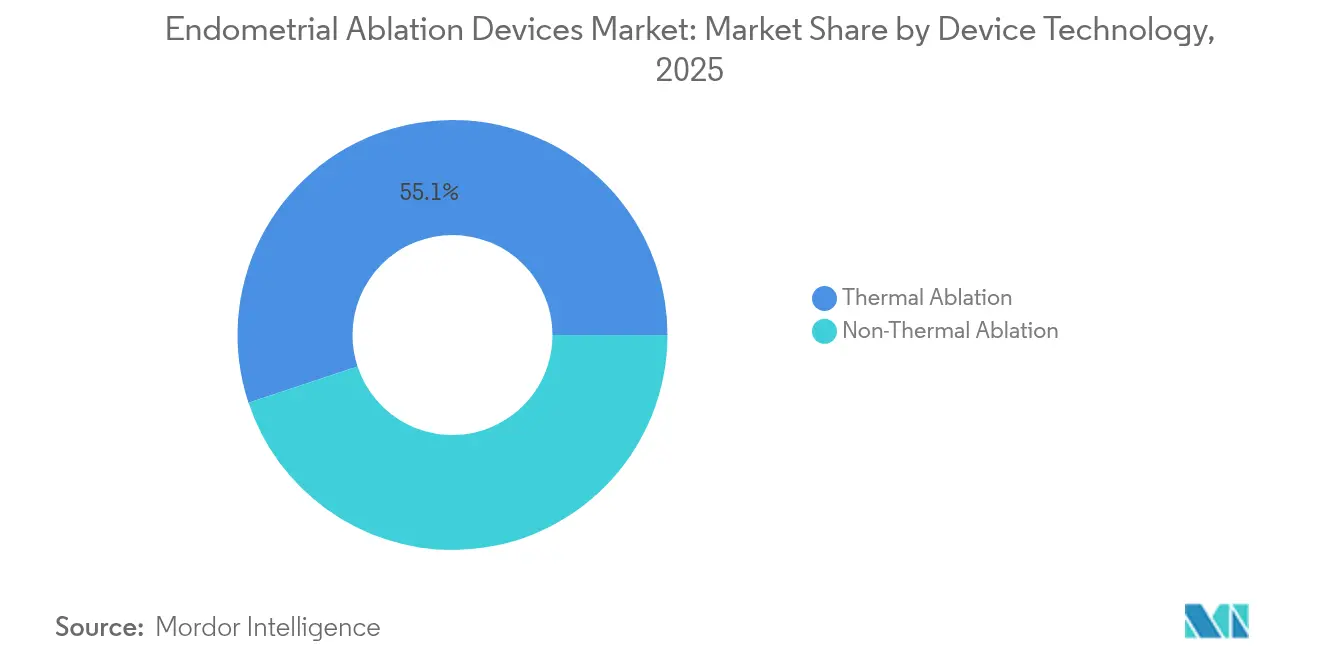

- By device technology, thermal platforms led with 55.10% revenue share in 2025, while non-thermal options are advancing at a 9.12% CAGR to 2031.

- By device type, radiofrequency systems accounted for 44.10% of the endometrial ablation devices market share in 2025; balloon ablators are forecast to expand at an 8.05% CAGR through 2031.

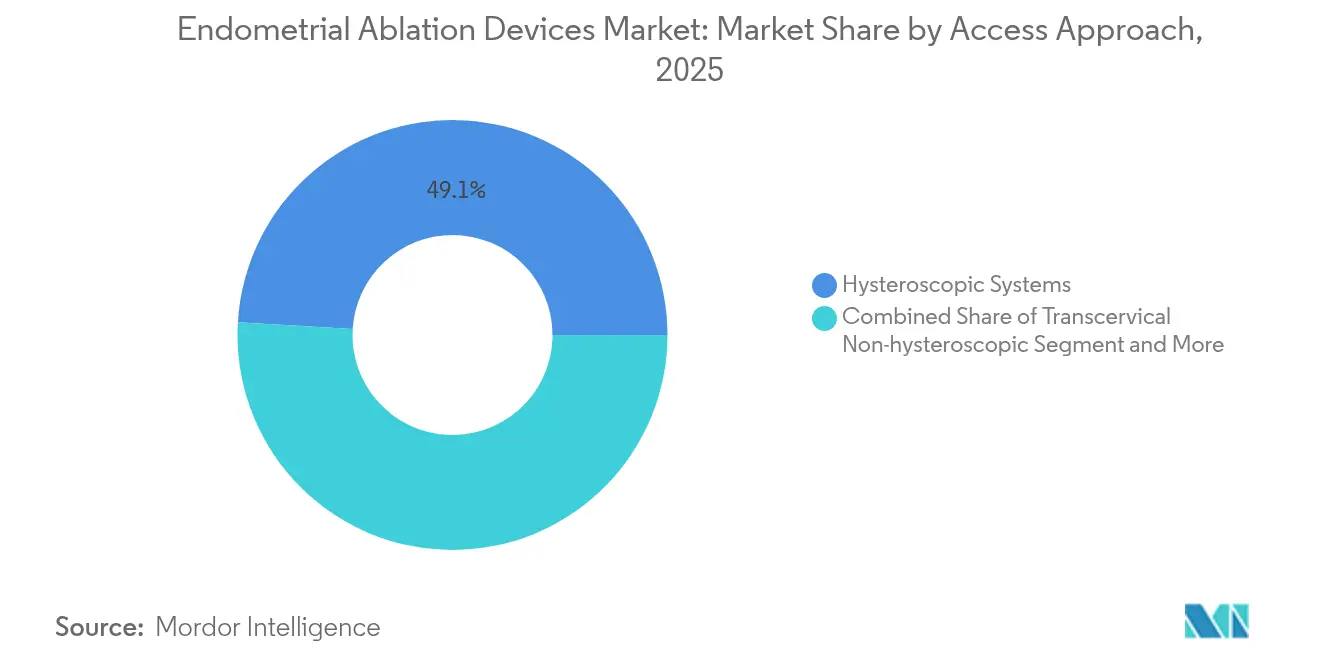

- By access approach, hysteroscopic systems held 49.05% of 2025 revenue, yet image-guided extra-uterine procedures are growing fastest at an 11.32% CAGR.

- By end user, hospitals captured 44.30% revenue in 2025, whereas ambulatory surgical centers (ASCs) are climbing at a 10.05% CAGR through 2031.

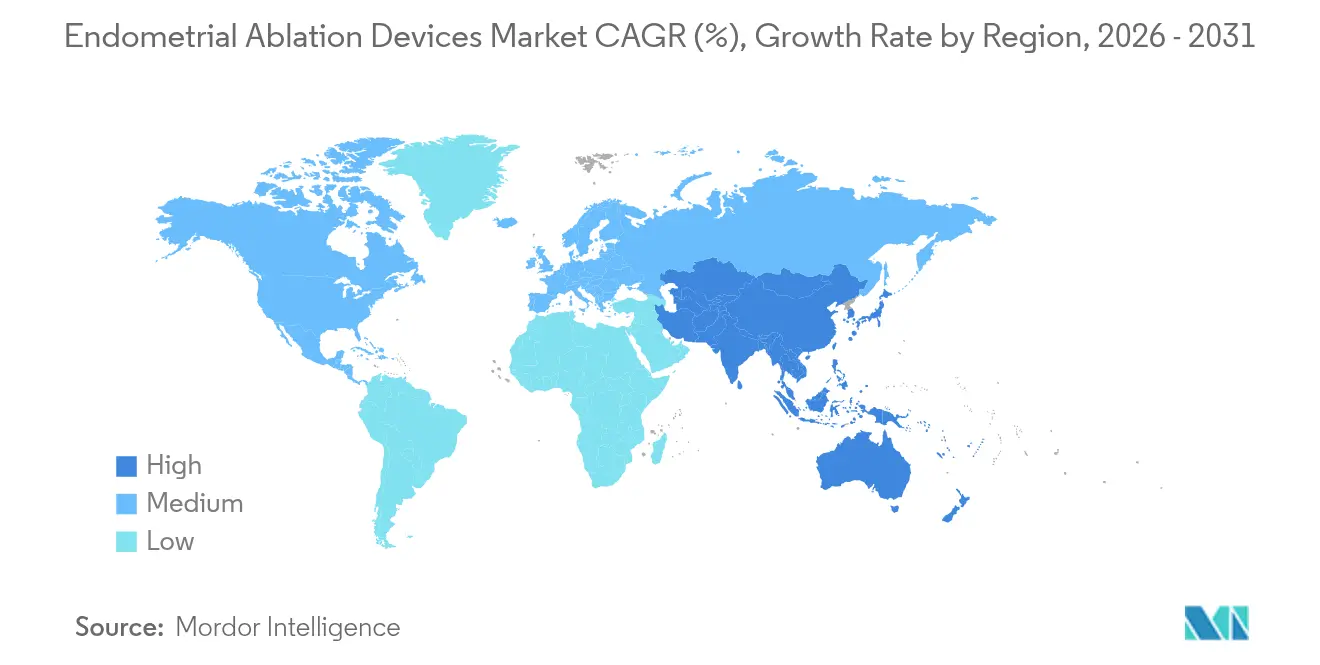

- By geography, North America dominated with 41.35% of 2025 sales; Asia-Pacific is set to grow at an 8.10% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Endometrial Ablation Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Abnormal Uterine Bleeding (AUB) | +1.2% | Global, with higher impact in North America & Europe | Long term (≥ 4 years) |

| Growing Demand For Minimally-Invasive Gynecologic Procedures | +0.8% | Global, accelerated in APAC emerging markets | Medium term (2-4 years) |

| Rapid Outpatient Migration To Ambulatory Surgery Centers | +1.5% | North America & EU core, expanding to APAC | Short term (≤ 2 years) |

| Increasing Reimbursement Coverage For Office-Based Ablation | +0.9% | North America primary, selective EU markets | Medium term (2-4 years) |

| AI-Guided Imaging Improving Procedural Accuracy | +1.1% | North America & EU early adoption, APAC following | Long term (≥ 4 years) |

| Emergence Of Single-Use Hysteroscopic Systems Lowering Infection Risk | + 0.7% | Global, with premium market focus initially | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Abnormal Uterine Bleeding (AUB)

AUB affects 14–25% of reproductive-age women, and incidence climbs in the 40–50 age group. Recent findings flag heavy menstrual bleeding as an independent cardiovascular risk factor, pushing clinicians toward definitive therapy earlier in the care pathway[1]Janesh Gupta, “Abnormal Uterine Bleeding – Symptoms, Diagnosis and Treatment,” BMJ Best Practice, bestpractice.bmj.com. Greater awareness widens the treatable population and sustains demand for ablation, enlarging the endometrial ablation devices market.

Growing Demand for Minimally-Invasive Gynecologic Procedures

Enhanced imaging, such as indocyanine-green fluorescence, lowers complication rates, while novel manipulation methods shorten operating time by 25%. Office-based ablation cuts per-patient costs by USD 1,498, making minimally invasive care compelling for payers and providers alike.

Rapid Outpatient Migration to ASCs

Patient satisfaction remains high, with 96% reporting sustained bleeding reduction five years after NovaSure treatment[2]Hologic, “NovaSure Endometrial Ablation,” Hologic, hologic.co.uk. Payers favor ASC procedures that trim facility fees, and device makers have responded with systems optimized for small-footprint settings.

AI-Guided Imaging Improving Procedural Accuracy

Deep-learning algorithms now detect uterine pathologies in ultrasound scans with 99% accuracy, offering intra-procedure guidance that standardizes outcomes and lowers the training barrier for new operators. AI integration differentiates premium offerings in the endometrial ablation devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unfavorable Or Heterogeneous Regulatory Pathways | -0.6% | Global, with varying intensity by region | Long term (≥ 4 years) |

| High Capital Cost Of Advanced RF & HIFU Platforms | -0.4% | Emerging markets primary, selective developed markets | Medium term (2-4 years) |

| Shortage Of Trained Hysteroscopists In Emerging Markets | -0.3% | APAC, MEA, Latin America focus | Long term (≥ 4 years) |

| Slow Procedural Adoption Due To Fertility-Preservation Concerns | -0.2% | Global, with cultural variations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Unfavorable or Heterogeneous Regulatory Pathways

Divergent rules extend approval timelines and inflate compliance costs. The FDA’s draft guidance on thermal effects adds premarket data burdens, and India’s evolving framework creates uncertainty for foreign entrants.

High Capital Cost of Advanced RF & HIFU Platforms

Upfront investment for Class III systems can exceed USD 5 million, straining budgets in cost-sensitive regions and delaying adoption until volume scales lower per-procedure expense.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Technology: Thermal Dominance Faces Non-Thermal Disruption

Thermal platforms generated 55.10% of 2025 revenue, confirming their role as the clinical mainstay of the endometrial ablation devices market. Proven safety and surgeon familiarity underpin this lead. Meanwhile, non-thermal modalities are forecast to grow at 9.12% CAGR. Cryoablation is gaining share through expanded European adoption, and MRI-guided focused ultrasound secured five new therapeutic indications in 2024.

Competitive dynamics now hinge on specialty applications where thermal limits arise—for instance, cases requiring ultra-precise tissue sparing. That shift widens the clinical footprint of non-thermal solutions without immediately eroding thermal revenue streams.

By Device Type: RF Systems Lead While Balloon Technologies Surge

Radiofrequency systems represented 44.10% revenue in 2025, and their broad utility keeps them central to procedure volumes. Balloon ablators, however, are set for an 8.05% CAGR to 2031 as simplified, single-use models reduce infection risk and learning curve. Hologic’s smart-depth technology and cavity-integrity assessment continue to anchor RF’s popularity, whereas Minerva’s silicone-mesh array illustrates how design differentiation propels balloon adoption.

The endometrial ablation devices market size for balloon technologies is projected to expand at the fastest clip within the device-type hierarchy, emphasising an industry-wide pivot to outpatient-friendly tools.

By Access Approach: Hysteroscopic Dominance Challenged by Image-Guided Innovation

Hysteroscopic systems supplied 49.05% of 2025 sales and remain the visualization gold standard. Yet MRI-guided and ultrasound-guided extra-uterine ablation, regulated as Class III products, is gaining momentum with an 11.32% CAGR. Image-guided offerings promise non-invasive treatment plus granular targeting, appealing to patients preferring no cervical entry.

Transcervical methods sit between these extremes, balancing broader eligibility with modest infrastructure needs. As precision medicine expands, image guidance will likely pull share from legacy platforms, but hysteroscopy’s entrenched install base will preserve meaningful volume through 2031.

By End User: Hospital Dominance Shifts Toward Ambulatory Settings

Hospitals maintained 44.30% of 2025 demand owing to comprehensive support services for complex cases. ASCs, on a 10.05% CAGR path, capture growth by pairing lower facility fees with rapid recovery. Evidence shows office ablation matches hospital safety while saving nearly USD 1,500 per case.

Specialty clinics further broaden access, especially where single-use scopes sidestep reprocessing issues highlighted in ACOG guidance. As these outpatient venues build procedural scale, the endometrial ablation devices market size linked to office settings is expected to rise steadily.

Geography Analysis

North America commanded 41.35% of 2025 revenue, underwritten by comprehensive reimbursement, dense specialist networks, and patient awareness. The endometrial ablation devices market size in the region will advance at mid-single-digit rates as AI guidance and disposable scopes deepen penetration.

Europe remains an innovation center that values evidence-based adoption. Structured procurement favors proven technologies, yet ASC migration in the United Kingdom, France, and Germany should accelerate growth.

Asia-Pacific, advancing at an 8.10% CAGR, benefits from widening insurance coverage, urban middle-class expansion, and government incentives for women’s health. Local manufacturing partnerships in India and export-oriented Chinese players broaden device availability.

Emerging markets in South America, the Middle East, and Africa exhibit early-stage demand. Investments in tertiary hospitals and specialty centers gradually unlock procedure capacity, though economic volatility tempers near-term volume.

Competitive Landscape

The endometrial ablation devices market shows moderate fragmentation. Global leaders leverage broad portfolios, strong clinical data, and after-sales service to shield share. Hologic’s NovaSure platform has treated more than 3 million patients with durable outcomes. Boston Scientific is scaling cryoablation centers across France, evidencing multinational push into non-thermal niches.

Strategic themes include AI overlays that standardize treatment, single-use hysteroscopes that cut reprocessing cost, and platform robotics exemplified by Johnson & Johnson’s IDE-cleared OTTAVA system. Smaller innovators such as Meditrina raise capital to commercialize bipolar RF systems tailored for office workflows, signaling investor confidence in outpatient trends.

Value-oriented entrants from China plan to compete on cost-performance balance, a strategy that could compress pricing in middle-income markets over the forecast period.

Endometrial Ablation Devices Industry Leaders

Olympus Corporation

Boston Scientific Corporation

CooperSurgical, Inc.

Medtronic plc

Johnson & Johnson (Ethicon)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Hologic launched an AI-enabled cavity-assessment module for NovaSure in select EU markets.

- May 2024: Meditrina secured FDA 510(k) clearance for its Gen 2 bipolar RF hysteroscopy system and Aveta Glo device, following a USD 77 million Series C funding round.

- March 2024: Boston Scientific expanded its cryoablation therapy network to 40 centers in France.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the endometrial ablation devices market as all single-use or reusable systems, consoles, and catheters specifically cleared to remove or destroy the endometrial lining in women with abnormal uterine bleeding. Products covered span radiofrequency, thermal balloon, hydrothermal, cryo, and microwave platforms that are intended for office, ASC, or hospital settings worldwide.

Scope exclusion: energy generators or electrosurgical tools marketed for broader gynecologic surgery but not labeled for endometrial ablation are outside this scope.

Segmentation Overview

- By Device Technology

- Thermal Ablation

- Non-Thermal Ablation

- By Device Type

- Hysteroscopy Devices

- Thermal Balloon Ablators

- Radiofrequency Endometrial Ablation Devices

- Hydrothermal Ablators

- Electrical Ablators

- Cryoablation Systems

- Microwave Ablation Probes

- By Access Approach

- Hysteroscopic Systems

- Transcervical Non-hysteroscopic (RF, Balloons)

- Image-Guided Extra-uterine (MRI-/US-guided HIFU)

- By End-User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Office-based Gynecology Practices

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed practicing gynecologic surgeons, ASC procurement heads, and regional distributors across North America, Europe, Asia-Pacific, and Latin America. These conversations clarified disposable-to-capital ratios, learning-curve driven utilization shifts, and discounting practices, allowing us to reconcile secondary signals and finalize key assumptions.

Desk Research

We gathered baseline data from tier-1 health agencies (WHO, CDC), procedure statistics posted by national obstetric-gynecology associations, import-export records from Volza, and peer-reviewed journals tracking menorrhagia prevalence. Company 10-Ks, device approvals in FDA 510(k) and CE databases, and reimbursement fee schedules further anchored average selling prices. Where device counts were sparse, we referenced D&B Hoovers and Dow Jones Factiva to approximate installed base and shipment trends. This list is illustrative; many additional sources informed the evidence pool.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-cohort buildout estimated the yearly addressable procedure pool, which was then validated through selective bottom-up supplier roll-ups of device shipments. Core variables, such as abnormal uterine bleeding incidence, hysteroscopic equipment penetration, average device re-use cycles, disposable catheter ASPs, reimbursement tariff trajectories, and gynecologist adoption rates, drive our model. Multivariate regression links these factors to historical revenues and projects demand to 2030. Data gaps in shipment splits were bridged by regional channel checks before we iterated the model.

Data Validation & Update Cycle

Outputs undergo variance checks versus external procedure counts, senior analyst review, and a second pass prior to publication. We refresh each model annually, issuing interim revisions when material regulatory or recall events arise.

Why Mordor's Endometrial Ablation Devices Baseline Commands Reliability

Published estimates often diverge because firms choose dissimilar product baskets, convert currencies at different points, or freeze models for years.

Key gap drivers include: some publishers fold fibroid ablation tools into totals, others apply aggressive replacement-rate assumptions, while a few model only U.S. CPT reimbursements and then extrapolate globally.

Mordor's disciplined device-level scope, annual refresh cadence, and cross-verification with clinician volumes temper such extremes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.20 B (2025) | Mordor Intelligence | - |

| USD 1.30 B (2024) | Global Consultancy A | includes microwave fibroid ablation systems and estimates universal ASC adoption |

| USD 1.25 B (2024) | Trade Journal B | converts revenues at fixed 2022 FX rates and omits LATAM markets |

| USD 1.50 B (2024) | Industry Association C | assumes single-use catheter replacement every procedure without reuse allowances |

In sum, by anchoring on clearly defined devices, verified utilization metrics, and timely price checks, Mordor delivers a transparent, balanced baseline that decision-makers can trace back to reproducible steps and trust for strategic planning.

Key Questions Answered in the Report

What is driving the current growth of the endometrial ablation devices market?

Rising abnormal uterine bleeding prevalence, expanding reimbursement for office-based procedures, and AI-guided imaging that improves accuracy are key growth catalysts.

Which device technology is growing fastest through 2031?

Non-thermal systems—such as cryoablation and laser platforms—are expected to expand at a 9.12% CAGR, outpacing thermal modalities.

Why are ambulatory surgical centers important for future market uptake?

ASCs offer cost savings near USD 1,500 per case, shorter recovery times, and high patient satisfaction, making them the fastest-growing end-user segment at a 10.05% CAGR.

How are regulations affecting product launch timelines?

Divergent global rules and new FDA thermal-effect guidance increase data requirements, extending approval timelines and raising compliance costs, especially for novel platforms.

Which geographic region will contribute most to additional revenue by 2031?

Asia-Pacific, forecast to grow at an 8.10% CAGR, will add the greatest share of incremental revenue as healthcare access and disposable incomes rise.

Page last updated on: