Thyroid Ablation Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

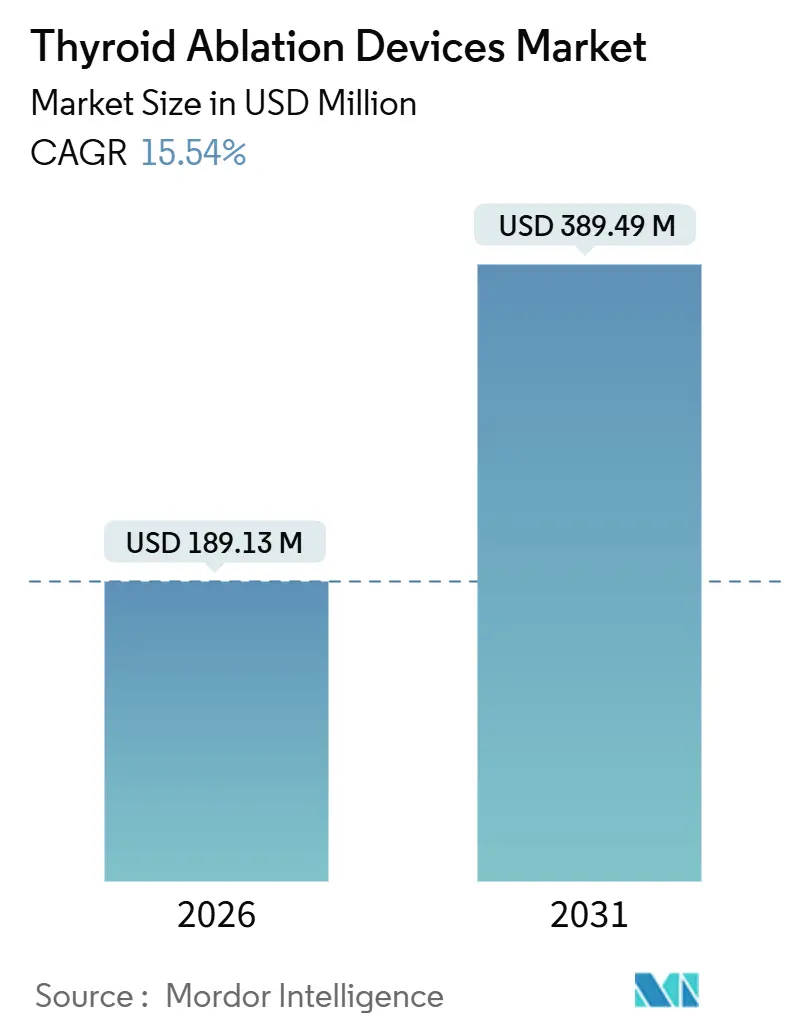

| Market Size (2026) | USD 189.13 Million |

| Market Size (2031) | USD 389.49 Million |

| Growth Rate (2026 - 2031) | 15.54% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thyroid Ablation Devices Market Analysis by Mordor Intelligence

The Thyroid Ablation Devices Market size is estimated at USD 189.13 million in 2026, and is expected to reach USD 389.49 million by 2031, at a CAGR of 15.54% during the forecast period (2026-2031).

A pronounced shift from thyroidectomy toward image-guided thermal procedures, favorable reimbursement changes, and rising nodule prevalence are the primary forces behind this expansion. Radiofrequency ablation (RFA) is entrenched as the workhorse modality, but microwave ablation (MWA) is gaining traction as operators target faster energy delivery for nodules larger than 3 cm. Detection of thyroid nodules has risen sharply 19.5 million cases each year in the United States alone while worldwide thyroid cancer incidence is projected to advance from 586,000 cases in 2020 to 794,000 by 2040, fueling a steady pipeline of procedures. Regulatory momentum adds further lift; the U.S. Centers for Medicare & Medicaid Services (CMS) included CPT 60660 in the Ambulatory Surgical Center (ASC) payment system effective January 2025, encouraging outpatient migration of thyroid ablation.

Key Report Takeaways

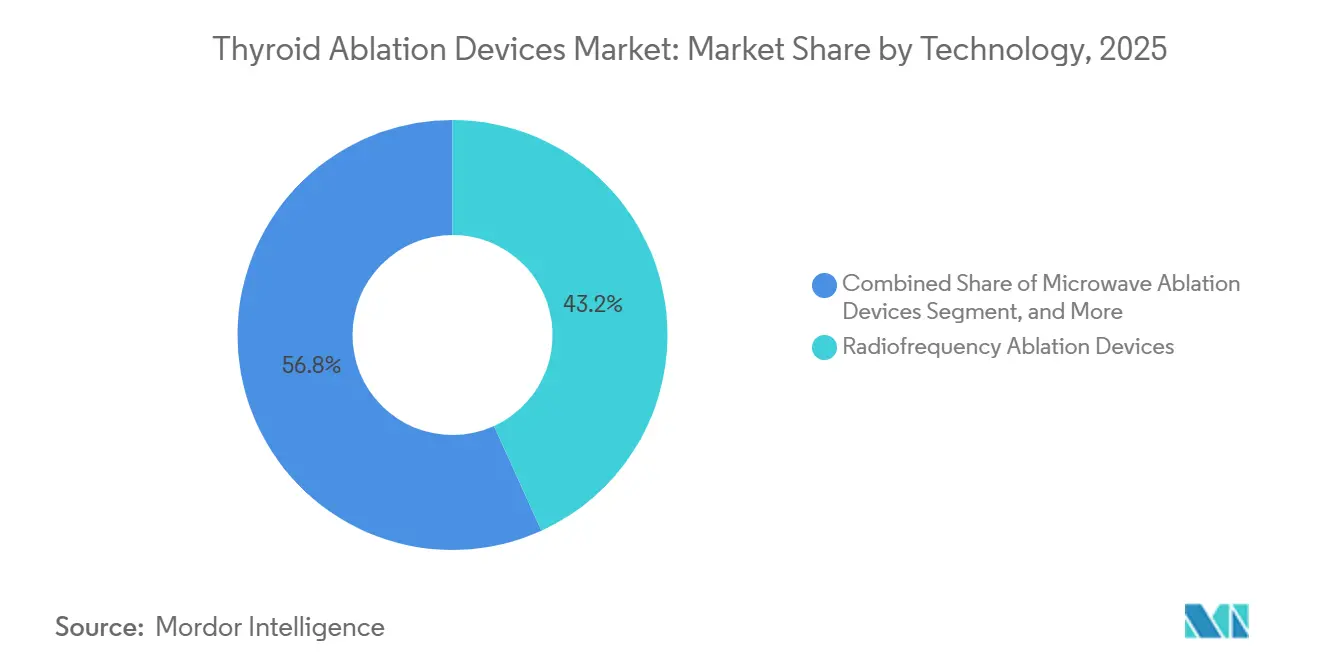

- By technology, radiofrequency ablation led with 43.21% of thyroid ablation devices market share in 2025, whereas microwave ablation is set to register the fastest 17.07% CAGR through 2031.

- By application, benign thyroid nodules captured 42.73% of the thyroid ablation devices market in 2025 and are poised to expand at a 16.95% CAGR through 2031.

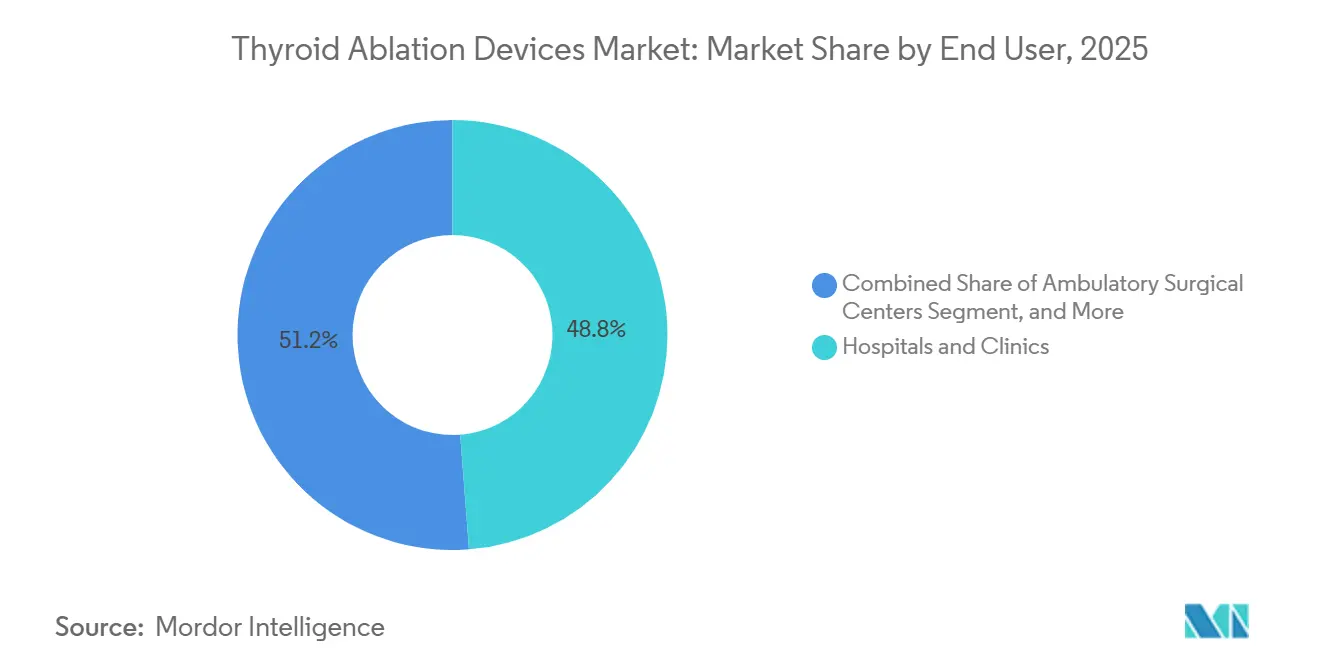

- By end user, hospitals and clinics accounted for 48.76% of revenue in 2025, while ASCs are projected to log the highest 18.13% CAGR through 2031 as payers reward lower-cost outpatient settings.

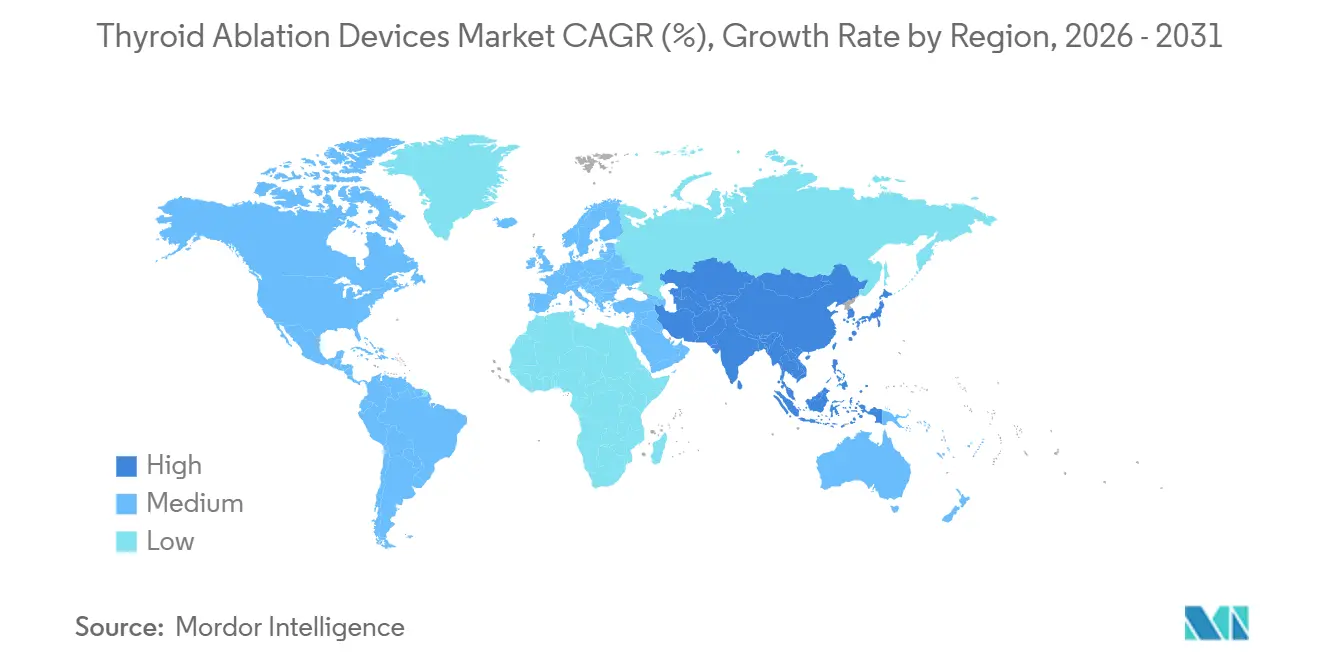

- By geography, North America accounted for 42.53% of 2025 revenue, whereas Asia-Pacific is forecast to clock a 19.93% CAGR through 2031, driven by accelerating regulatory approvals in China and Korea.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Thyroid Ablation Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of thyroid nodules & cancer | +3.2% | Global, highest in Korea, China, United States | Medium term (2–4 years) |

| Rapid adoption of minimally invasive treatment | +4.1% | North America, Europe, urban APAC | Short term (≤ 2 years) |

| Technological advances in RFA/MWA platforms | +2.8% | Global, led by North America & East Asia | Medium term (2–4 years) |

| Favorable clinical-practice guidelines | +2.5% | North America, Europe, Korea, Japan | Short term (≤ 2 years) |

| AI-driven real-time thermal monitoring | +1.7% | North America & EU first adopters, spill-over to APAC | Long term (≥ 4 years) |

| Expansion of office-based suites & ASC models | +3.3% | United States dominant, emerging in Canada & Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Thyroid Nodules & Cancer

Thyroid nodule detection surged as point-of-care ultrasound became routine in primary care, pushing annual U.S. volumes to 19.5 million cases.[1]National Institutes of Health, “Thyroid Nodule Prevalence and Thyroid Cancer Incidence Trends,” PMC, nih.gov Globally, thyroid cancer diagnoses are expected to climb to 794,000 by 2040, with Korea and China shouldering the heaviest incidence. Epidemiologic pressure is steering health systems toward thermal ablation because it eliminates the need for general anesthesia, preserves thyroid function, and reduces inpatient stays. Bethesda III and IV nodules, once managed with diagnostic surgery, are now increasingly undergoing ablation, reducing postsurgical complications and the total cost of care. Payers view avoidance of permanent hypoparathyroidism and vocal-cord injury as savings that justify coverage for benign and low-risk lesions.

Rapid Adoption of Minimally Invasive Treatments Over Thyroidectomy

The share of ablation in benign nodule treatment rose to an estimated 22%–28% in North America and Europe in 2025, up from single digits in 2020. A 2024 randomized trial demonstrated that microwave ablation reduced average procedure time by 30% while achieving an 80% volume-reduction ratio, only marginally below RFA’s 86% benchmark.[2]Radiology Editorial Board, “Randomized Controlled Trial: Microwave vs Radiofrequency Ablation for Thyroid Nodules,” Radiology, pubs.rsna.org Surgeons are incorporating ablation to retain patient volumes, and interventional radiologists have opened stand-alone thyroid clinics that bypass surgical referral pathways. Endorsement from the American Thyroid Association (ATA) in its 2025 guidelines, which recognize ablation as a valid alternative to active surveillance for T1a microcarcinomas, is accelerating payor acceptance. Insurers have relaxed prior authorization as three-year data confirm low regrowth and minimal complications.

Technological Advances in Image-Guided Platforms

Next-generation RFA generators now employ impedance-controlled algorithms that mitigate electrode charring, while 2.45 GHz MWA systems deliver energy independent of tissue conductivity. Ceramic-coated electrodes launched in 2024 dissipate heat evenly, reduce skin-burn risk, and probes embedded with fiber Bragg grating sensors provide real-time sub-millimeter temperature feedback.[3]MDPI Sensors Team, “Fiber Bragg Grating Temperature Sensors for Ablation Monitoring,” Sensors, mdpi.com Fusion imaging overlays CT or MRI on live ultrasound, enabling safe targeting of posterior nodules near the recurrent laryngeal nerve. High-intensity focused ultrasound (HIFU) maintains a niche share given its EUR 250,000 capital price, but zero-incision appeal is winning patients in Japan and France.

Favorable Clinical-Practice Guidelines Endorsing Ablation

Korea’s 2025 guidelines recommend RFA as first-line therapy for biopsy-proven recurrent papillary carcinoma, legitimizing ablation beyond benign disease. China issued a 2024 consensus standardizing patient selection, technique, and follow-up across more than 2,000 hospitals. In the United States, the 2023 ATA safety statement required operators to complete 20–30 supervised cases, prompting academic centers to establish formal fellowships. Europe still relies on the 2020 European Thyroid Association guidance for benign nodules, yet national societies in Germany and Italy have embedded those recommendations into reimbursement statutes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & disposable costs | -2.4% | Global, acute in APAC & MEA price-sensitive hubs | Short term (≤ 2 years) |

| Reimbursement variability | -1.9% | Europe fragmented; Latin America, MEA limited | Medium term (2–4 years) |

| Operator-skill and training requirements | -1.6% | Global, largest gaps in tier-2 urban centers | Medium term (2–4 years) |

| Long-term oncologic outcome uncertainty | -1.3% | North America & Europe surgical strongholds | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital & Disposable Costs of Ablation Systems

HIFU systems exceed EUR 250,000 (USD 270,000) while RFA and MWA generators cost EUR 17,000–25,000 (USD 18,500–27,200), stretching public-hospital budgets in Eastern Europe, Southeast Asia, and Latin America. Single-use electrodes priced at EUR 700-1,250 (USD 760-1,360) push consumable spend toward USD 200,000 annually for high-volume centers. Informal electrode reuse in India and Brazil seeks to lower costs but raises infection risk and voids warranties. Leasing and pay-per-use models are emerging but require multi-year commitments, which deters facilities unsure of case flow.

Reimbursement Variability Across Regions

Germany’s statutory insurance covers RFA for symptomatic benign nodules, but France and the United Kingdom limit coverage to trials, forcing patients to self-pay EUR 1,500–3,000 per session. Latin American payers label thyroid ablation experimental and impose case-by-case approvals that delay scheduling by up to six weeks. China’s provincial payment rates range from CNY 3,000 to 9,000 (USD 420–1,260), creating uneven access. Harmonizing policies will demand multi-year health-technology assessments and real-world evidence, slowing entry into regions where cost-effective surgical alternatives are sorely needed.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & disposable costs | -2.4% | Global, acute in APAC & MEA price-sensitive hubs | Short term (≤ 2 years) |

| Reimbursement variability | -1.9% | Europe fragmented; Latin America, MEA limited | Medium term (2–4 years) |

| Operator-skill and training requirements | -1.6% | Global, largest gaps in tier-2 urban centers | Medium term (2–4 years) |

| Long-term oncologic outcome uncertainty | -1.3% | North America & Europe surgical strongholds | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital & Disposable Costs of Ablation Systems

HIFU systems exceed EUR 250,000 (USD 270,000) while RFA and MWA generators cost EUR 17,000–25,000 (USD 18,500–27,200), stretching public-hospital budgets in Eastern Europe, Southeast Asia, and Latin America. Single-use electrodes priced at EUR 700-1,250 (USD 760-1,360) push consumable spend toward USD 200,000 annually for high-volume centers. Informal electrode reuse in India and Brazil seeks to lower costs but raises infection risk and voids warranties. Leasing and pay-per-use models are emerging but require multi-year commitments, which deters facilities unsure of case flow.

Reimbursement Variability Across Regions

Germany’s statutory insurance covers RFA for symptomatic benign nodules, but France and the United Kingdom limit coverage to trials, forcing patients to self-pay EUR 1,500–3,000 per session. Latin American payers label thyroid ablation experimental and impose case-by-case approvals that delay scheduling by up to six weeks. China’s provincial payment rates range from CNY 3,000 to 9,000 (USD 420–1,260), creating uneven access. Harmonizing policies will demand multi-year health-technology assessments and real-world evidence, slowing entry into regions where cost-effective surgical alternatives are sorely needed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Microwave Gains on Procedural Speed

The thyroid ablation devices market for microwave systems is projected to grow at a 17.07% CAGR between 2026 and 2031, outpacing overall industry growth. Radiofrequency retains 43.21% thyroid ablation devices market share owing to entrenched reimbursement and trained operators, yet new Chinese platforms priced 25%–35% lower are accelerating microwave penetration in price-sensitive Asia-Pacific hospitals. The 2024 Radiology study demonstrated a 30% reduction in procedure time for MWA with an 80% twelve-month volume-reduction ratio, nearly matching RFA outcomes. Laser ablation maintains 8%–10% technology revenue, favored for fiber-optic delivery that limits thermal spread, while HIFU remains a 5%–7% niche due to high capital costs and 90-minute workflows. FDA 510(k) clearances for new microwave and RFA platforms during 2024–2025 expand the supplier roster and intensify price competition.

Regulatory convergence is improving time-to-market; IEC revisions to harmonize safety standards for high-frequency surgical equipment will underpin multi-country filings. Vendors now bundle generators, ultrasound software, and starter electrodes, mirroring razor-and-blade models standard in surgical energy. Ceramic-coated electrodes that diffuse heat evenly and embedded fiber Bragg sensors are rapidly becoming “must-have” features rather than premium add-ons.

By Application: Benign Nodules Anchor Procedural Volume

Benign nodules commanded 42.73% of 2024 revenue and are projected to grow at 16.95% annually as more patients pursue cosmetic improvement and symptom relief without surgery. Meta-analyses confirm 67%–93.6% nodule reduction and regrowth under 14%, results that resonate with patient expectations. Primary thyroid cancer remains a smaller slice; skepticism around long-term oncologic control deters insurers despite promising five-year microwave data. Recurrent carcinoma in the thyroid bed or neck nodes is emerging as a surgical adjunct; Korea’s new guidelines endorse RFA for locoregional recurrence, catalyzing uptake in Seoul and Busan.

Payers are aligning coverage with data showing lower total episode costs compared with lobectomy, specifically by avoiding permanent hypoparathyroidism (2%–5%) and recurrent nerve injury (1%–2%). Bethesda III/IV nodule ablation is expanding despite limited reimbursement, as physicians and patients seek to avoid diagnostic surgery.

By End User: ASCs Capture Outpatient Migration

ASC revenue is projected to grow at an 18.13% CAGR, driven by CMS’s 2025 CPT 60660 listing, which delivers favorable bundling. The ASC model appeals to providers seeking better economics and to patients who prefer same-day discharge. Hospitals and clinics remain the largest channel at 48.76% revenue share, performing complex cases near critical anatomy or managing comorbid patients. Specialty cancer centers integrate ablation into multidisciplinary pathways but grow more slowly as their focus skews toward malignant disease. Office-based labs, powered by compact RFA generators, are a fast-growing “others” segment that captures both professional and technical fees.

Private-equity roll-ups of thyroid clinics are driving volume purchasing agreements that squeeze device pricing. Hospitals counter with outpatient thyroid intervention suites to retain commercially insured patients, while specialty cancer centers partner with manufacturers on investigator-initiated trials to reinforce thought-leadership status.

Geography Analysis

North America supplied 42.53% of 2025 global revenue. Integration into endocrinology and interventional radiology fellowships, plus CMS-driven reimbursement changes, underpin growth. Canadian provinces are piloting ablation, but inconsistent reimbursement is stretching public wait times beyond 6 months. Mexico’s private network attracts U.S. patients seeking costs of USD 2,500–3,500 versus USD 5,000–8,726 domestically. Operator shortages persist; fewer than 20 U.S. programs offer structured thyroid intervention curricula, limiting procedure availability in rural regions.

Asia-Pacific is the fastest-growing region with a projected 19.93% CAGR through 2031. China’s NMPA approvals for domestic RFA systems in 2024–2025 and a 2024 National Health Commission consensus standardized care across more than 2,000 hospitals. Korea, with the world’s highest thyroid cancer incidence, embeds RFA in recurrent-disease guidelines, driving cases in Seoul and Busan. Japan’s aging population values non-scarring outpatient options, accelerating adoption. India and Australia are nascent but expanding through private-hospital investment, yet public systems remain surgical-centric. Payment disparities persist; Chinese provincial rates vary threefold, and Southeast Asia lacks procedural codes, concentrating demand in cash-pay medical-tourism hubs.

Europe owns roughly one-fifth of 2024 revenue. Germany reimburses RFA for symptomatic benign nodules, whereas France and the United Kingdom limit reimbursement to trials or compassionate use, leaving patients to self-fund EUR 1,500–3,000 per session. Italy and Spain expand academic center programs in line with the European Thyroid Association's guidance. Adoption in the Middle East and Africa is uneven; Gulf Cooperation Council states reimburse through government insurance, but sub-Saharan Africa’s lack of codes pushes adoption toward private facilities in South Africa and Kenya. South America remains reimbursement-constrained, yet pilots in Brazil and Argentina test bundled-payment models that could unlock future growth.

Competitive Landscape

The market is moderately fragmented. Boston Scientific, Medtronic, Johnson & Johnson (Ethicon NeuWave), Olympus, and STARmed together significant share in 2025. These conglomerates leverage existing hepatic and renal-tumor platforms, bundling generators with ultrasound consoles to penetrate thyroid workflows. Chinese challengers such as Baird Medical and Kangyou Medical undercut prices by up to 35% to win share in Asia-Pacific and Middle Eastern hospitals. Theraclion promotes premium HIFU systems to academic centers, but high capital cost and long case times constrain scale.

Competitive focus is shifting from pure energy delivery to software differentiation. In 2024–2025, Boston Scientific and Medtronic filed more than a dozen patents for AI-assisted thermal monitoring and ceramic-coated electrodes. PIUR Imaging integrates AI-driven 3-D ultrasound into ablation procedures, demonstrating an 18% reduction in procedure time. Single-use electrodes that eliminate reprocessing are another wedge for new entrants targeting infection-control-conscious ASCs. Partnerships between device makers and ASC chains accelerate, as volume commitments justify discounted pricing that hospital purchasing groups struggle to match.

Regulatory convergence aids smaller vendors. The International Electrotechnical Commission’s forthcoming updates to IEC 60601-2-2 are expected to standardize safety testing for thyroid-specific thermal devices, enabling multi-market filings and intensifying competition. Vendors are responding with value bundles: portable generators, ultrasound software, and electrode starter kits priced below USD 30,000 to court office-based endocrinologists.

Thyroid Ablation Devices Industry Leaders

Boston Scientific Corporation

Integra LifeSciences Holdings

Johnson & Johnson

Medtronic

Olympus Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Baird Medical sponsored a microwave ablation master-class in Arizona, training U.S. surgeons on next-generation thyroid protocols.

- March 2024: Baird Medical obtained NMPA Class III approval for its RFA device, the first domestic Chinese system cleared for thyroid indications, prompting a 15% price cut among import brands.

- February 2024: PIUR Imaging released tUS Infinity, an AI-powered 3-D ultrasound platform that trims thyroid ablation time by 18% and lifts volume-reduction ratios by seven points in early users.

- January 2024: Hygea secured U.S. FDA 510(k) clearance for its microwave ablation platform, expanding U.S. options for energy-based thyroid therapy.

Global Thyroid Ablation Devices Market Report Scope

The Thyroid Ablation Devices Market Report is Segmented by Technology (Radiofrequency Ablation Devices, Microwave Ablation Devices, Laser Ablation Devices, High-Intensity Focused Ultrasound Systems, Other Technologies), Application (Benign Thyroid Nodules, Primary Thyroid Cancer, Recurrent Thyroid Cancer), End User (Hospitals & Clinics, Ambulatory Surgical Centers, Specialty Cancer Centers, Others), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Radiofrequency Ablation Devices |

| Microwave Ablation Devices |

| Laser Ablation Devices |

| High-Intensity Focused Ultrasound Systems |

| Other Technologies (Cryoablation Devices, Imaging & Guidance Accessories, etc.) |

| Benign Thyroid Nodules |

| Primary Thyroid Cancer |

| Recurrent Thyroid Cancer |

| Hospitals & Clinics |

| Ambulatory Surgical Centers |

| Specialty Cancer Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Radiofrequency Ablation Devices | |

| Microwave Ablation Devices | ||

| Laser Ablation Devices | ||

| High-Intensity Focused Ultrasound Systems | ||

| Other Technologies (Cryoablation Devices, Imaging & Guidance Accessories, etc.) | ||

| By Application | Benign Thyroid Nodules | |

| Primary Thyroid Cancer | ||

| Recurrent Thyroid Cancer | ||

| By End User | Hospitals & Clinics | |

| Ambulatory Surgical Centers | ||

| Specialty Cancer Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the thyroid ablation devices market expected to grow between 2026 and 2031?

The industry is projected to advance at a 15.54% CAGR, scaling from USD 189.13 million in 2026 to USD 389.49 million by 2031.

Which modality is gaining share against radiofrequency ablation?

Microwave ablation is gaining adoption due to faster energy delivery and is forecast to grow at a 17.07% CAGR through 2031.

Why are ambulatory surgical centers important for future procedure volumes?

CMS added CPT 60660 to the ASC fee schedule in January 2025, enabling higher reimbursement and accelerating outpatient migration.

What limits ablation use for primary thyroid cancers today?

Lack of 10-year comparative oncologic data and absence of full endorsement from Western surgical societies keep primary cancer adoption modest.

Which region will record the highest growth rate by 2031?

Asia-Pacific will post the fastest CAGR at 19.93%, propelled by Chinese and Korean policy support and local manufacturer approvals.

Page last updated on: