Uterine Manipulation Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

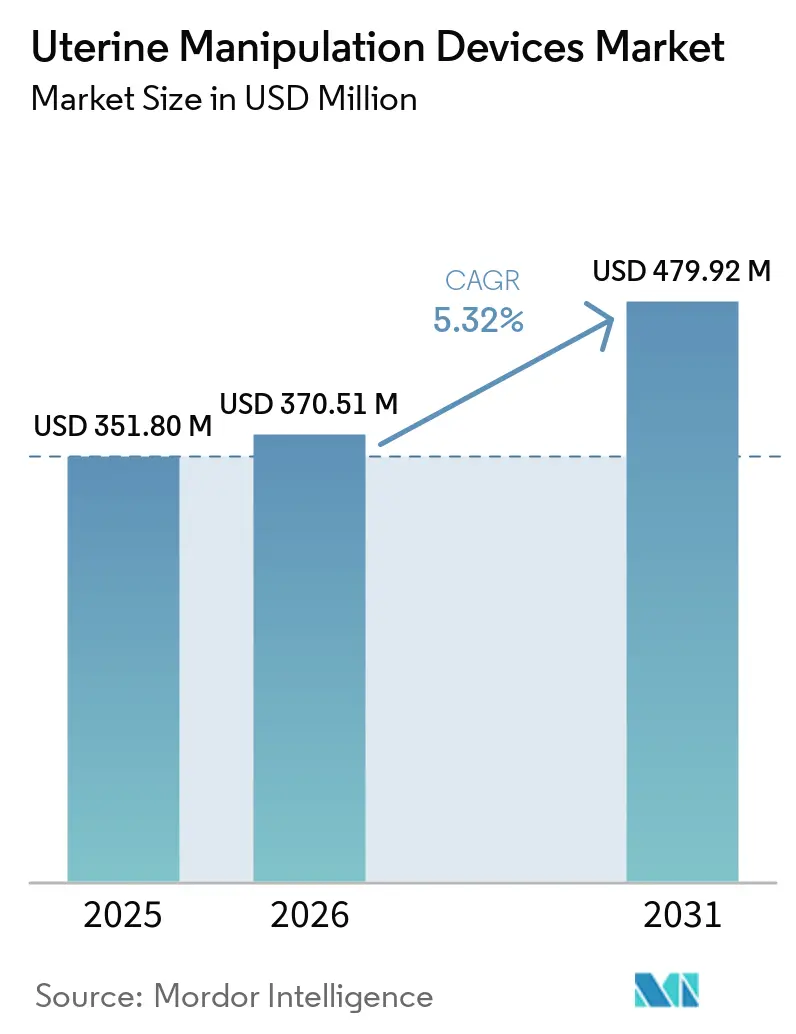

| Market Size (2026) | USD 370.51 Million |

| Market Size (2031) | USD 479.92 Million |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Uterine Manipulation Devices Market Analysis by Mordor Intelligence

The Uterine Manipulation Devices Market size was valued at USD 351.80 million in 2025 and is estimated to grow from USD 370.51 million in 2026 to reach USD 479.92 million by 2031, at a CAGR of 5.32% during the forecast period (2026-2031).

Growth stems from a sustained shift toward minimally invasive gynecologic surgery, rising adoption of robotic‐assisted platforms, and hospital preference for single-use sterile devices that reduce reprocessing burdens. Accelerated uptake of total laparoscopic hysterectomy, rising from 35.9% to 44.2% of all hysterectomies in recent years, underlines demand for sophisticated manipulators that provide enhanced tip articulation and ergonomic control. Device makers also benefit from new Medicare reimbursement codes that better reward laparoscopic complexity, while supply-chain vulnerabilities in medical-grade silicones temper near-term output expansion. Competitive rivalry remains moderate as leaders such as CooperSurgical, KARL STORZ, Olympus and Medtronic deploy M&A and AI-enabled design upgrades to defend share in the uterine manipulation devices market.

Key Report Takeaways

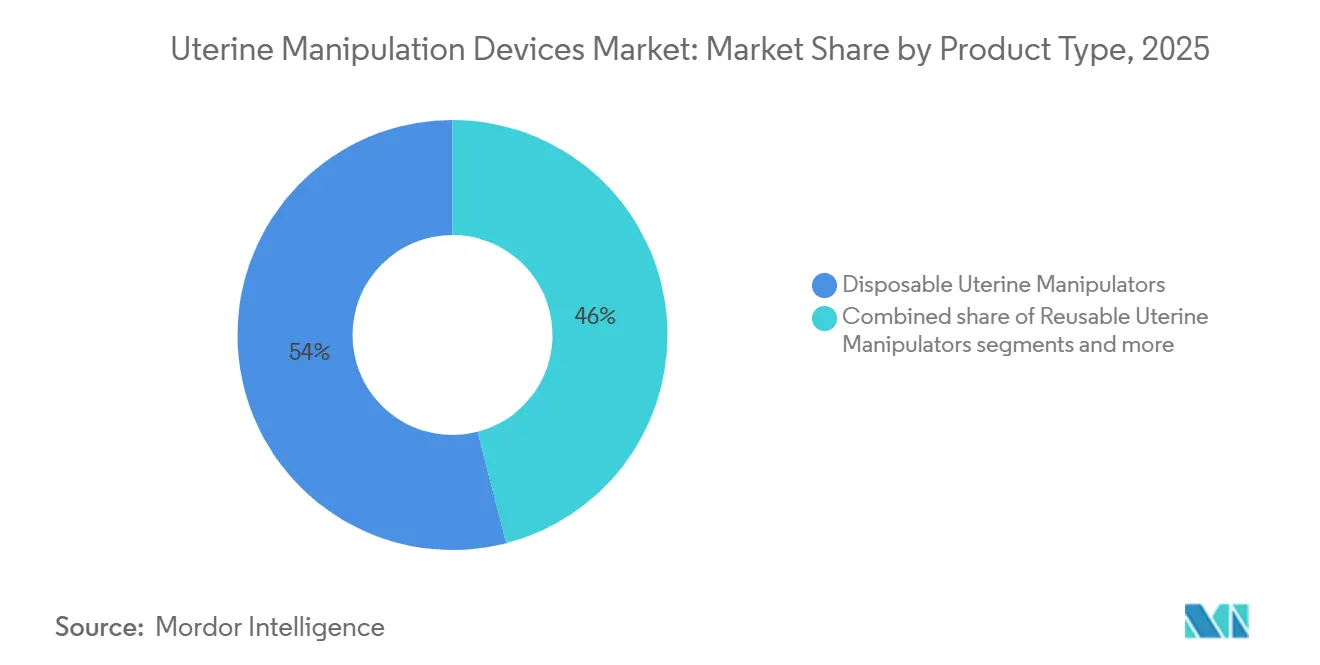

- By product type, disposable devices led with 54.02% of uterine manipulation devices market share in 2025 while hybrid/reposable designs are projected to grow at a 6.05% CAGR through 2031.

- By tip movement, articulating tiltable-tip manipulators commanded 47.55% of uterine manipulation devices market size in 2025 and flexible-tip solutions are forecast to expand at a 6.44% CAGR to 2031.

- By procedure, total laparoscopic hysterectomy accounted for 38.21% of uterine manipulation devices market share in 2025, while robotic-assisted hysterectomy is advancing at a 6.78% CAGR through 2031.

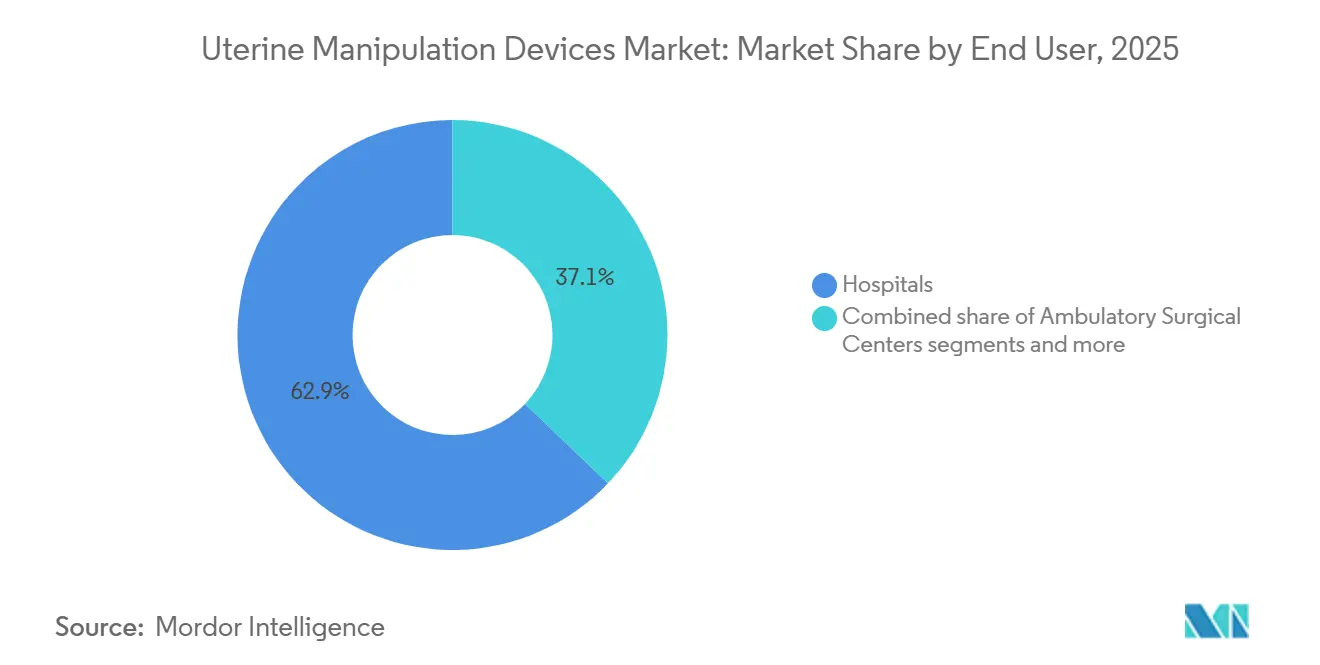

- By end user, hospitals held 62.88% share of the uterine manipulation devices market size in 2025 and ambulatory surgery centers (ASC) are rising at a 7.28% CAGR forecast to 2031.

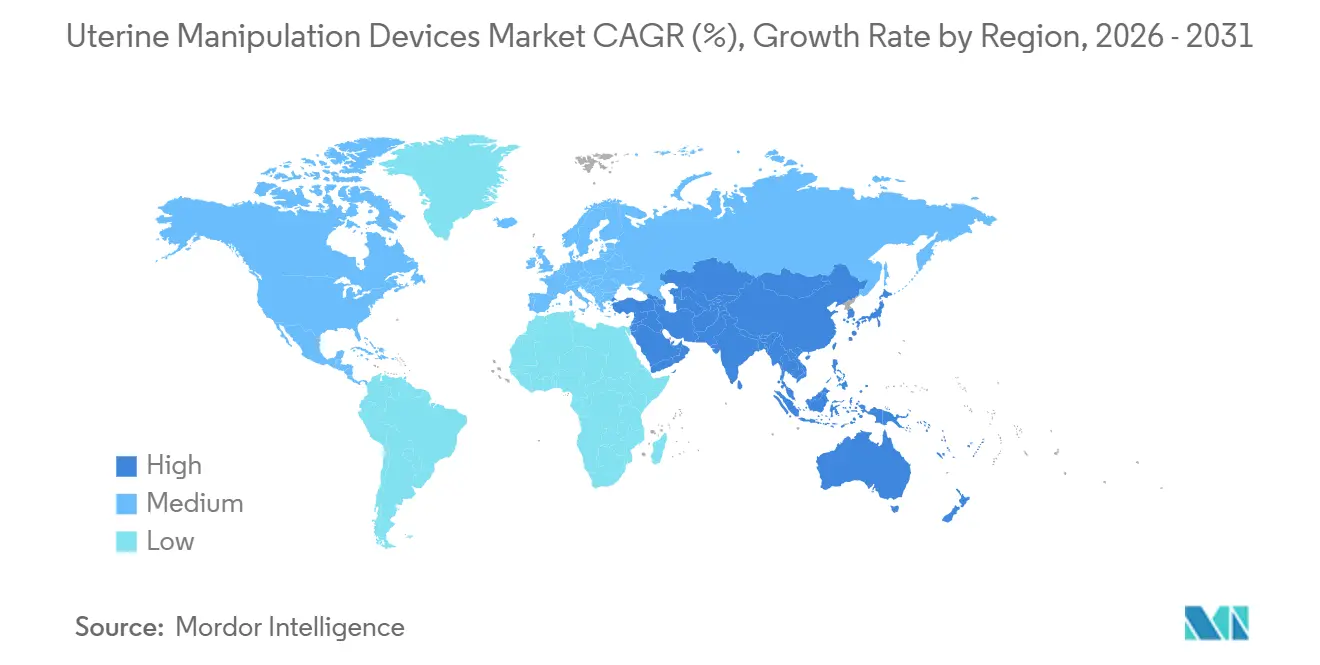

- By geography, North America maintained 41.90% uterine manipulation devices market share in 2025, whereas Asia-Pacific is expected to post the fastest 7.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Uterine Manipulation Devices Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of minimally invasive hysterectomy procedures | +1.8% | Global, with North America and Europe leading | Medium term (2-4 years) |

| Shift toward single-use sterile devices to cut infection risk | +1.2% | Global, with stronger adoption in developed markets | Short term (≤ 2 years) |

| Increasing prevalence of fibroids & gynecologic cancers | +0.9% | Global, with higher impact in aging populations | Long term (≥ 4 years) |

| New reimbursement codes boosting laparoscopic surgery uptake | +0.7% | North America primarily, expanding to Europe | Medium term (2-4 years) |

| Proliferation of ambulatory surgery centers in Asia-Pacific | +0.6% | Asia-Pacific core, spillover to other emerging markets | Medium term (2-4 years) |

| Robotic-ready articulating manipulators enhance ergonomics | +0.5% | Global, concentrated in advanced healthcare systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising adoption of minimally invasive hysterectomy procedures

Laparoscopic hysterectomy rates climbed from 11.3% in 2015 to 52.7% by 2020, and continued rising to approximately 58-62% by 2022-2023 as surgeon confidence and patient preference shifted toward shorter hospital stays and reduced pain. Enhanced visualization tools and wireless laparoscopy improve surgical ergonomics, prompting hospitals to invest in uterine manipulators with multi-plane articulation matched to robotic consoles. Medicare’s site-neutral payments encourage outpatient hysterectomy, pushing ASCs to procure efficient devices that enable same-day discharge. Enhanced Recovery After Surgery protocols further prioritize instruments that minimize tissue trauma and bleeding, reinforcing demand for premium manipulators.

Shift toward single-use sterile devices to cut infection risk

Hospitals accelerate the move to disposable manipulators after CDC guidance warned that single-use items should not be reprocessed because of contamination risks. The Olympus MAJ-891 recall and FDA reprocessing warnings intensified scrutiny, prompting purchasing managers to favor sterile, ready-to-use instruments despite higher unit pricing. EU packaging-waste directives complicate adoption, requiring suppliers to demonstrate recycling pathways or sustainable materials for disposables. Low-volume centers still find disposables cost-effective because capital outlays for sterilizers outweigh per-case savings, while high-volume hospitals weigh hybrid options that balance infection control and expense.

Increasing prevalence of fibroids & gynecologic cancers

The global burden of uterine fibroids rose 67.07% in incidence and 78.82% in prevalence between 1990 and 2019, with preliminary data suggesting continued increases of 15-20% from 2019 to 2023, particularly affecting women aged 35-39. Simultaneously, uterine cancer incidence increased by over 50% from 2010 to 2020 and continued rising at 3-5% annually through 2023, particularly among Black women who now face up to 3.5-4 times higher mortality risk compared to white women according to recent SEER data analysis. Surgeons therefore perform more myomectomies, fibroid ablations and oncologic hysterectomies that depend on manipulators delivering precise uterine positioning for margins and fertility preservation. Radiofrequency and microwave ablation systems rely on stable uterine orientation, pushing manufacturers to create devices with integrated locking and sensor guidance.

New reimbursement codes boosting laparoscopic surgery uptake

CMS updated the 2025 Physician Fee Schedule, assigning higher Relative Value Units to complex laparoscopic gynecologic codes, narrowing the payment gap with open surgery. New CPT descriptors covering non-opioid pain management dovetail with ERAS protocols, reinforcing payer backing for minimally invasive approaches. Site-neutral reimbursement also removes the pricing advantage of hospital outpatient departments over ASCs, spurring device purchases by freestanding centers that need compact, intuitive manipulators to keep turnover high.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Device-related perforation & litigation concerns | -0.8% | Global, with higher impact in litigious markets | Short term (≤ 2 years) |

| Inconsistent reprocessing rules for reusable devices | -0.6% | Global, with regulatory fragmentation across regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Device-related perforation & litigation concerns

Uterine perforation occurs in 1% of hysteroscopic procedures and up to 4% in certain intrauterine interventions, stoking malpractice claims and insurance premiums. Lawsuits alleging thermal injury from robotic instrumentation have heightened scrutiny of all accessory devices, including manipulators, leading risk-averse surgeons to prefer established brands with long safety records. FDA warning letters demanding corrective actions on robotic systems add compliance pressures; hospitals now reinforce credentialing and simulation training, slowing adoption of unfamiliar manipulator designs. Legal precedent in the United States places manufacturer-equivalent liability on hospitals that reprocess single-use devices, discouraging reuse unless strict validation is documented.

Inconsistent reprocessing rules for reusable devices

Article 17 of the EU Medical Device Regulation permits each member state to set its own single-use reprocessing policy, creating a patchwork of requirements that complicates product labeling and supply-chain planning. FDA obligates reprocessors to meet manufacturer-level quality systems, a costly hurdle for small facilities and global exporters. Divergent bioburden test methods, device-tracking mandates and documentation standards produce barriers for companies marketing reusable manipulators in multiple jurisdictions. Smaller innovators face high regulatory overhead to validate cleaning cycles across ultrasonics, steam and low-temperature vaporized hydrogen peroxide, constraining new-product rollouts and slowing uterine manipulation devices market penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Disposable devices drive infection control

Disposable designs accounted for 54.02% of uterine manipulation devices market share in 2025 thanks to heightened infection-control vigilance after well-publicized contamination events. Hospitals view single-use manipulators as an insurance policy against costly surgical site infections and complex sterility audits. Yet reusable instruments still appeal to high-volume centers that amortize sterilization equipment over thousands of cases. Manufacturers respond with hybrid, limited-use models that support 5-10 cycles, balancing waste reduction and cost; this niche is forecast for 6.05% CAGR, outpacing the overall uterine manipulation devices market.

Innovations in fluoro-elastomer materials allow reusable shafts to withstand more than 1,000 steam cycles without degradation, lowering life-cycle cost and boosting resilience against silicone shortages. RFID chips embedded in handles log sterilization counts and temperature exposure, feeding data into hospital asset-management platforms that trigger preventive maintenance alerts.

By Tip Movement: Articulating technology enhances surgical precision

Articulating tiltable-tip devices dominated, representing 47.55% of uterine manipulation devices market size in 2025 as surgeons sought broader range of motion for complex robotic and laparoscopic cases. Fixed-tip models remain staples in straightforward procedures due to simplicity and lower price, but lack the angles needed for deep pelvic exposure. Flexible-tip manipulators—using polymer joints and cable drives—are forecast to post the fastest 6.44% CAGR because they pair with 3D imaging for real-time contouring of uterine position.

Robotic integration layers new expectations: automated “follow-me” algorithms match uterine displacement to camera movements, minimizing repositioning time and assistant fatigue. Academic prototypes cut operative time by 12% in early trials, pointing to future smart manipulators that learn surgeon preferences over repeated cases. The uterine manipulation devices market continues to reward suppliers that fuse mechanics, sensors and software into an intuitive ergonomic package preferred by high-volume gynecologic oncology teams.

By Procedure: Robotic-assisted hysterectomy accelerates growth

Total laparoscopic hysterectomy retained 38.21% uterine manipulation devices market share in 2025, anchored by long-standing clinical evidence of improved recovery and lower blood loss. Robotic-assisted hysterectomy is the clear growth engine, registering 6.78% CAGR as new console installs rise and hospital marketing promotes scar-minimizing technology. Endometrial cancer cases feed demand for manipulators with smoke evacuation ports and extended articulation, while fibroid ablation procedures require slim shafts compatible with transcervical ultrasound catheters.

Procedures such as vNOTES benefit from devices that maintain pneumovaginal seal and permit in-line visualization; same-day discharge protocols support premium instruments that shorten operative time. Fertility surgeries and tubal ligations rely on gentle tip pressure to avoid fallopian damage, sustaining a baseline need for low-profile manipulators in the uterine manipulation devices industry.

By End User: Ambulatory centers drive market expansion

Hospitals captured 62.88% of uterine manipulation devices market size in 2025 because multi-specialty ORs handle complex oncology procedures demanding high-end devices. However, ASCs represent the fastest-growing channel at 7.28% CAGR through 2031 as payers bundle payments and patients seek convenient same-day care. ASC administrators prefer disposables to eliminate sterilizer capital outlays and reduce turnaround time, driving bulk purchasing agreements with manufacturers.

Specialty gynecology clinics thrive on personalized care and fertility services, adopting miniature manipulators and ultrasound-guided systems; although small in value, this segment influences design trends such as ergonomic handles sized for smaller hands. Widespread ASC growth, 12% projected volume expansion in five years, will lift sales of mid-tier manipulators optimized for staff who alternate across multiple surgical specialties.

Geography Analysis

North America preserved 41.90% uterine manipulation devices market share in 2025 on the back of early robotic adoption, robust reimbursement and a dense network of fellowship-trained minimally invasive gynecologic surgeons. U.S. hospitals routinely upgrade to articulating, sensor-enabled devices compatible with 4K visualization, while ASC chains drive volume for disposable kits that streamline turnover.

Europe follows with steady uptake as aging demographics push hysterectomy demand and sustainability legislation nudges hospitals toward reusable or hybrid manipulators meeting EU waste directives. Regional procurement consortia reward suppliers demonstrating carbon-neutral manufacturing processes, spurring R&D into biopolymer handles and recyclable packaging.

Asia-Pacific is the uterine manipulation devices market’s growth engine, projected at 7.55% CAGR through 2031, propelled by rapid ASC construction, urban middle-class expansion and government funding for robotic platforms in China, India and South Korea. Surgeons in tier-2 Chinese cities increasingly perform laparoscopic hysterectomy using cost-effective disposables imported under local distribution partnerships, squeezing margins for premium brands but expanding unit volumes.

South America shows gradual adoption with Brazil and Mexico leading, constrained by currency volatility affecting import pricing. Middle East & Africa post incremental gains tied to private-sector hospital group investment in Gulf states and large-scale health-city initiatives, which include turnkey robotic suites requiring compatible manipulators. Donor-funded women’s health programs in sub-Saharan Africa occasionally procure basic fixed-tip devices, but volumes remain modest.

Competitive Landscape

The uterine manipulation devices market remains moderately concentrated, with the top five players controlling roughly 60% of revenue. CooperSurgical strengthened its portfolio through the September 2024 purchase of obp Surgical, adding single-hand inserter technology that appeals to outpatient clinics. KARL STORZ’s USD 0.35-per-share acquisition of Asensus Surgical aligns manipulators with the upcoming LUNA robotic system and broadens distribution reach.

Olympus focuses on infection-control messaging after high-profile endoscope recalls, highlighting sterile single-use uterine manipulators with validated barrier packaging. Medtronic leverages its Hugo robotic platform, courting third-party developers to design AI-integrated manipulators that auto-synchronize with camera articulation, aiming for FDA submission in 2025. Niche firms pursue hybrid devices with peel-off sterile sheaths to balance waste concerns and cost, while contract manufacturers in Malaysia and Costa Rica offer OEM services to global brands seeking supply-chain redundancy against silicone shortages.

Smaller disruptors target fertility clinics with ultra-slim manipulators for transcervical fibroid ablation or office-based hysteroscopy. Competitive differentiation increasingly hinges on embedded sensor arrays that log intrauterine pressure and angle, feeding operative analytics dashboards for credentialing compliance.

Uterine Manipulation Devices Industry Leaders

Conkin Surgical Instrument Ltd.

CooperSurgical Inc.

B. Braun Melsungen AG

KARL STORZ GmbH & Co. KG

CONMED Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: CooperSurgical completed acquisition of obp Surgical, expanding its gynecologic device lineup.

- August 2024: KARL STORZ finalized acquisition of Asensus Surgical to reinforce robotic surgery portfolio

Global Uterine Manipulation Devices Market Report Scope

As per the scope of the report, uterine manipulation devices are surgical devices that are used in gynecological surgery to effectively hold the cervix in place while the surgeon performs a laparoscopic procedure in the uterine environment of a female. The uterine manipulation devices market is segmented by application (total laparoscopy hysterectomy (TLH), laparoscopic supracervical hysterectomy (LSH), laparoscopically assisted vaginal hysterectomy (LAVH), Sacrocolpopexy and other applications), product type (Donnez type uterine manipulators, Tintara type uterine manipulators, Clermont -Ferrand type uterine manipulators, Hohl type uterine manipulators, and Advincula arch type uterine manipulators), end user (hospitals, specialized gynecology clinics, and ambulatory surgical centers) and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Disposable Uterine Manipulators |

| Reusable Uterine Manipulators |

| Hybrid Devices |

| Fixed / Static Tip |

| Articulating Tiltable Tip |

| Flexible Tip |

| Total Laparoscopic Hysterectomy |

| Robotic-Assisted Hysterectomy |

| Tubal Ligation & Fertility |

| Endometrial Cancer Surgery |

| Myomectomy & Fibroid Removal |

| Other Gynecologic Surgeries |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Gynecology Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type (Value) | Disposable Uterine Manipulators | |

| Reusable Uterine Manipulators | ||

| Hybrid Devices | ||

| By Tip Movement (Value) | Fixed / Static Tip | |

| Articulating Tiltable Tip | ||

| Flexible Tip | ||

| By Procedure (Value) | Total Laparoscopic Hysterectomy | |

| Robotic-Assisted Hysterectomy | ||

| Tubal Ligation & Fertility | ||

| Endometrial Cancer Surgery | ||

| Myomectomy & Fibroid Removal | ||

| Other Gynecologic Surgeries | ||

| By End User (Value) | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Gynecology Clinics | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the uterine manipulation devices market?

The uterine manipulation devices market size reached USD 370.51 million in 2026, with a projected USD 479.92 million by 2031.

Which product type leads sales?

Disposable uterine manipulators hold 54.02% market share in 2025 because hospitals emphasize infection-control and regulatory compliance.

Why is Asia-Pacific considered the fastest-growing region?

Healthcare system modernization, new ambulatory centers and rising surgical volumes fuel a 7.55% CAGR for Asia-Pacific through 2031.

How are reimbursement changes affecting demand?

CMS updated 2025 codes that better reward complex laparoscopy, encouraging hospitals and ASCs to adopt minimally invasive procedures requiring manipulators.

What technological trends shape future device design?

AI-assisted robotic platforms and RFID-enabled sensor feedback are driving next-generation articulating manipulators with automated positioning and usage tracking.

Page last updated on: