Intrauterine Contraceptive Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

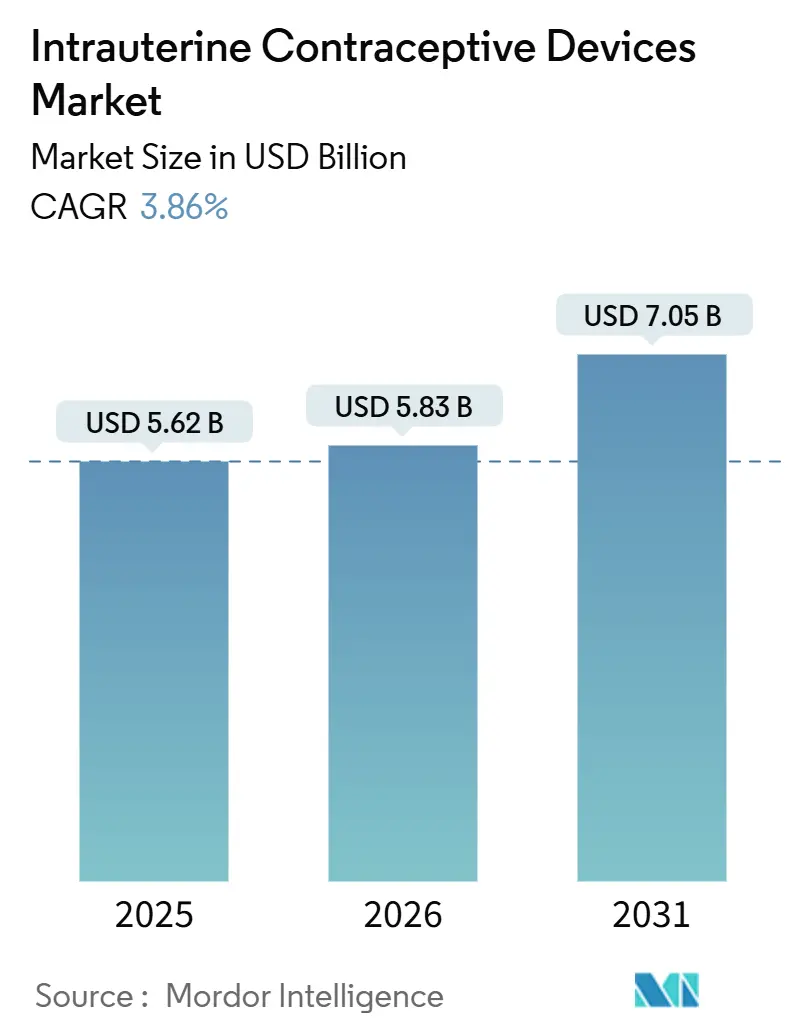

| Market Size (2026) | USD 5.83 Billion |

| Market Size (2031) | USD 7.05 Billion |

| Growth Rate (2026 - 2031) | 3.86% CAGR |

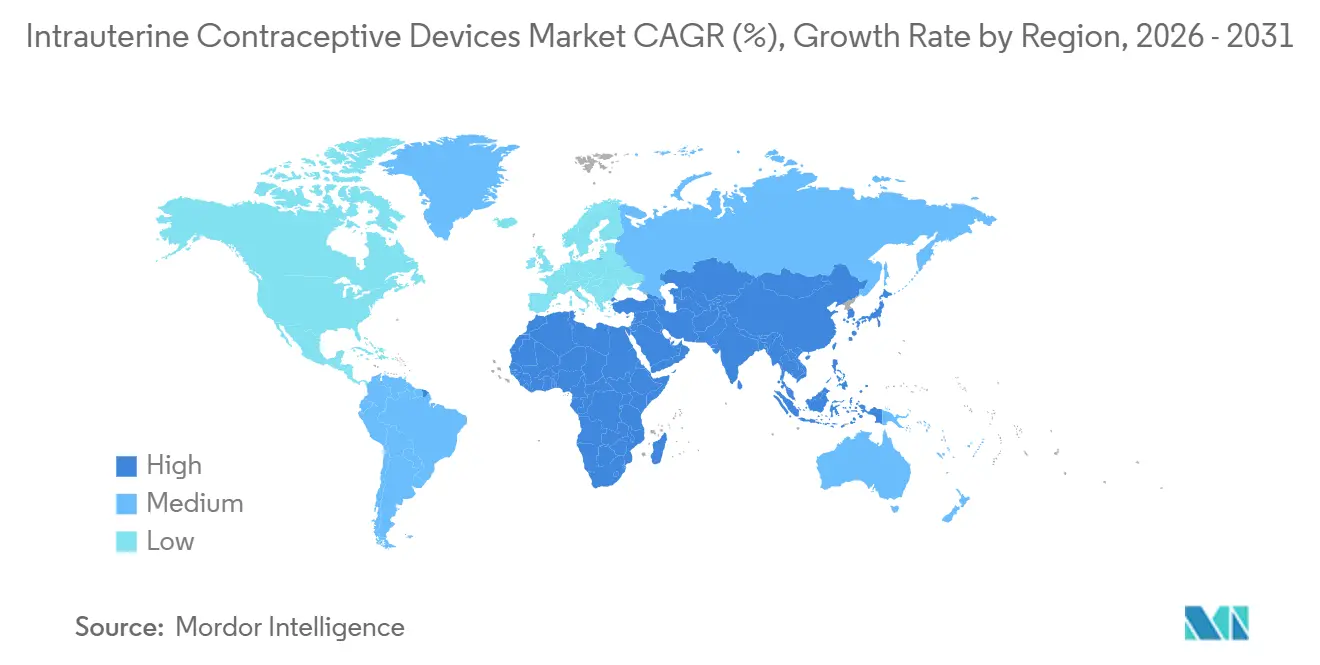

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

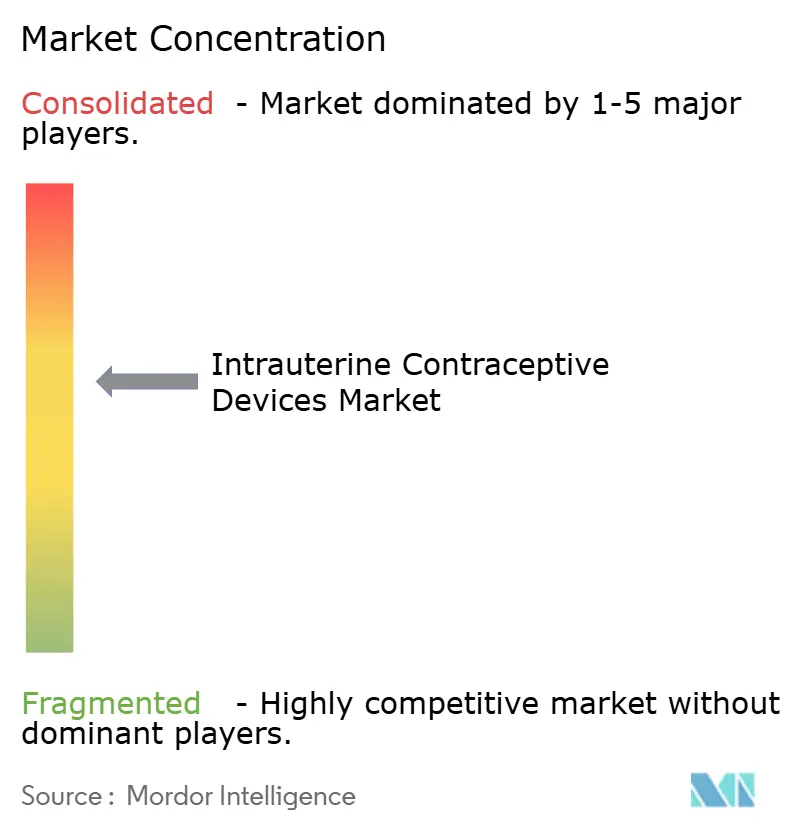

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Intrauterine Contraceptive Devices Market Analysis by Mordor Intelligence

The Intrauterine Contraceptive Devices Market size is expected to increase from USD 5.62 billion in 2025 to USD 5.83 billion in 2026 and reach USD 7.05 billion by 2031, growing at a CAGR of 3.86% over 2026-2031.

Demand continues to pivot from short-acting methods toward long-acting reversible alternatives because a single IUD insertion offers up to ten years of pregnancy protection, removes daily compliance risk, and lowers per-patient service costs in publicly funded programs. Payors are responding by raising reimbursement ceilings for IUDs, while providers expand task-shifting protocols that allow nurses and midwives to perform insertions in primary care settings. Copper designs still dominate because of their hormone-free profile and low unit cost. However, levonorgestrel systems are moving faster on the back of dual indications that bundle contraception with heavy menstrual bleeding therapy.

Key Report Takeaways

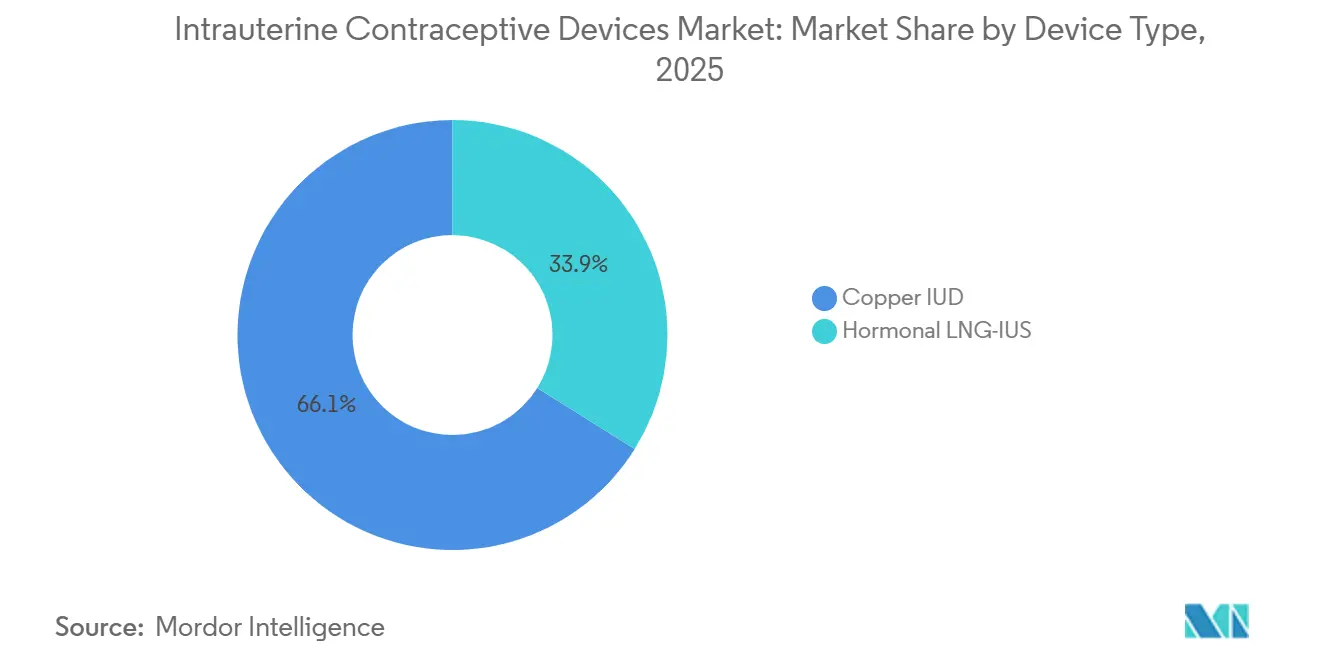

- By device type, copper IUDs led with 66.10% of the intrauterine contraceptive devices market share in 2025. Hormonal levonorgestrel IUS is forecast to expand at a 6.25% CAGR through 2031.

- By indication, contraception accounted for 78.80% of the intrauterine contraceptive devices market in 2025. Endometrial protection during hormone-replacement therapy is advancing at a 9.28% CAGR to 2031.

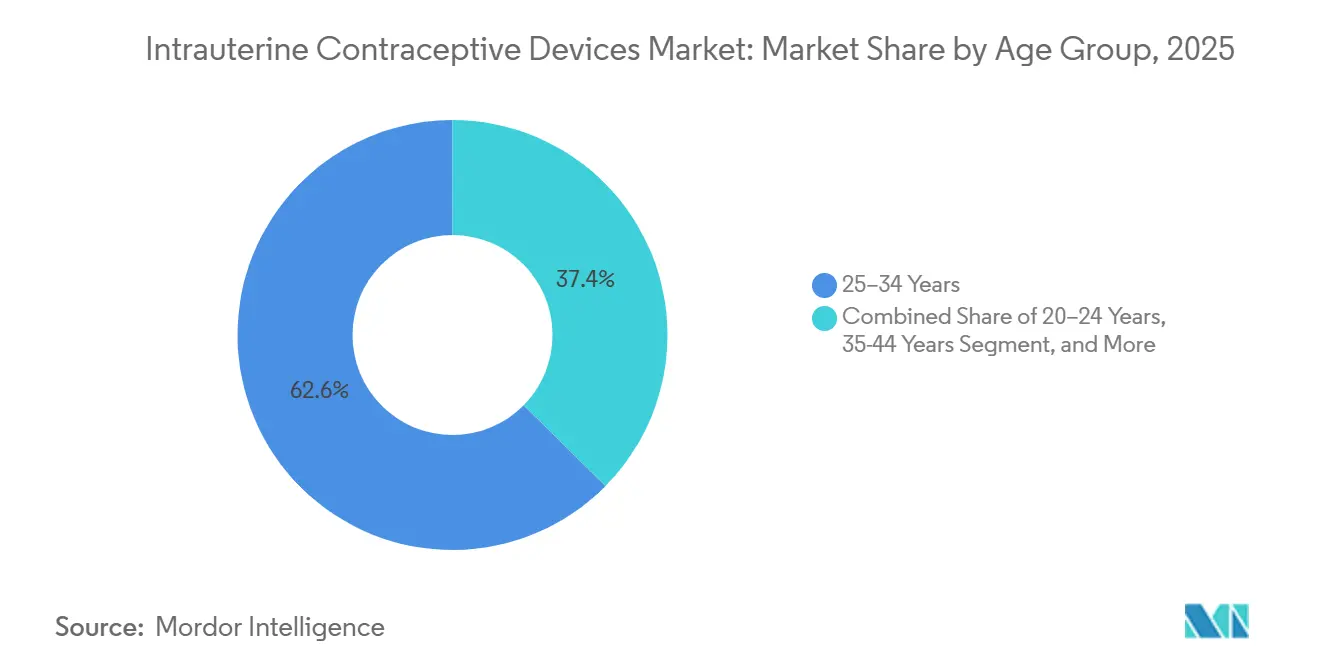

- By age group, women aged 25-34 years accounted for 62.60% in 2025. The <20 years cohort is recording the highest projected CAGR at 7.28% through 2031.

- By end user, hospitals accounted for 58.07% in 2025. Community health centers are growing at a 6.75% CAGR to 2031.

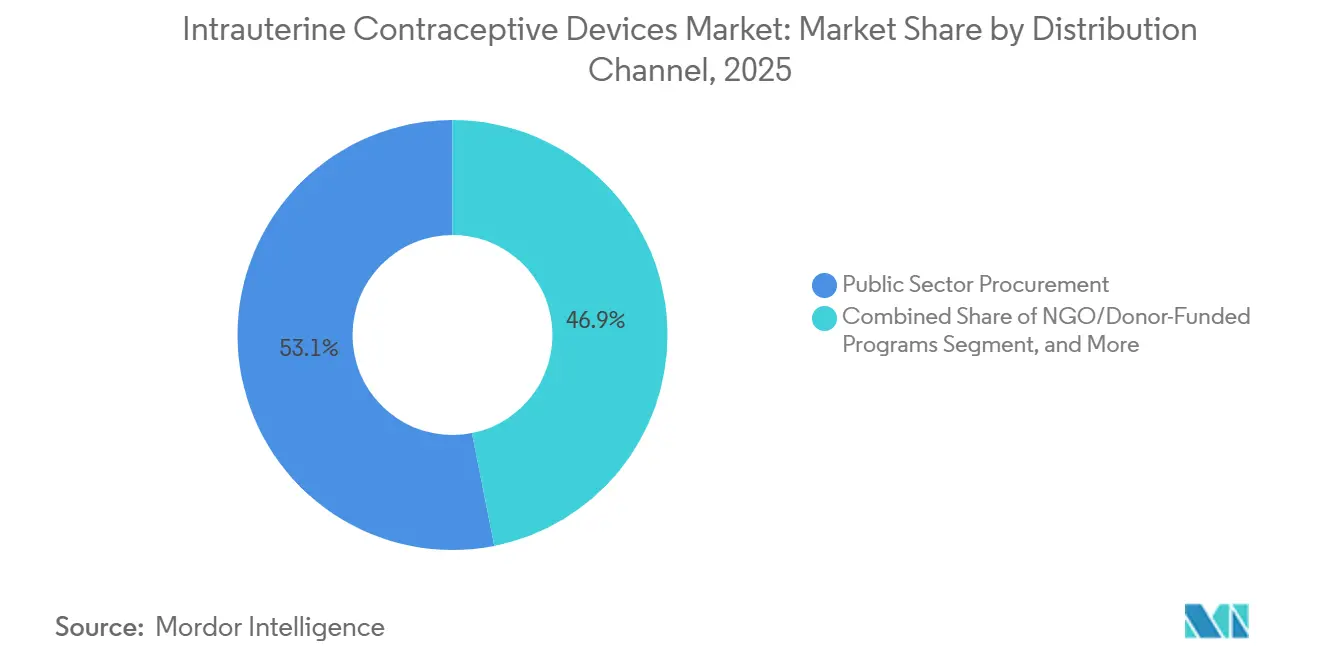

- By distribution channel, public procurement accounted for 53.11% in 2025. NGO-funded programs are growing at a 7.63% CAGR through 2031.

- By geography, North America accounted for 39.90% in 2025. Asia-Pacific is the fastest-growing region, with a 6.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Intrauterine Contraceptive Devices Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~ ) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Technological innovation leading to effective contraceptives and fewer side effects | +1.2% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Rising demand for long-acting reversible contraceptives (LARCs) | +1.5% | Global, strongest in Asia-Pacific and North America | Long term (≥ 4 years) |

| Government initiatives and support policies | +0.9% | Asia-Pacific, Latin America, Sub-Saharan Africa | Short term (≤ 2 years) |

| Favorable recommendations from global health organizations | +0.7% | Global, with spillover to Middle East and Africa | Medium term (2-4 years) |

| Increasing trend of delayed childbirth | +1.5% | Global, strongest in Asia-Pacific and North America | Long term (≥ 4 years) |

| Expansion of NGO-led social-marketing and public-private distribution | +0.9% | Asia-Pacific, Latin America, Sub-Saharan Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Technological Innovation Leading to Effective Contraceptives and Fewer Side Effects

New materials and engineering approaches are redefining copper devices. The FDA-cleared MIUDELLA uses a nitinol frame and 50% less copper yet keeps 99% efficacy, easing pain and heavy bleeding previously linked to conventional designs. Research teams are testing flexible iron-based frames that could cut inflammatory responses while safeguarding contraceptive strength. These improvements matter most in markets where fear of adverse events still deters uptake, and they give suppliers an edge with premium pricing tied to better user comfort. Bayer’s Kyleena uses a 19.5 mg hormone load and a 3.8 mm inserter, cutting insertion-pain scores by 30% compared with 52 mg predecessors, which lifts 12-month continuation to 88%. These refinements make the intrauterine contraceptive devices market more attractive to first-time users and younger patients who previously favored short-acting options.

Rising Demand for Long-Acting Reversible Contraceptives (LARCs)

Healthcare providers are steering patients toward devices that require no daily action and have a <1% first-year failure rate.[1]United Nations Population Fund, “Contraceptive Procurement and Distribution,” UNFPA.ORG Women aged 25-34 already represent nearly two-thirds of IUD use, mirroring their desire for extended protection while postponing pregnancies. Updated U.S. practice guidelines in 2024 place LARCs first in counseling scripts, a move likely to ripple into other national protocols.

Global fertility fell to 2.3 births per woman in 2025, with East Asia at 1.2 and Southern Europe at 1.3. Users postponing childbirth now prize methods that remove daily adherence and equal sterilization in effectiveness, a perception that propels the intrauterine contraceptive devices market.[2]Centers for Disease Control and Prevention, “U.S. Selected Practice Recommendations for Contraceptive Use,” CDC, cdc.gov A 2024 Guttmacher survey across 15 nations showed 62% of LARC users cited “set-and-forget” convenience as the primary reason for choosing an IUD, up from 38% for short-acting methods. Uptake closely tracks female labor-force participation above 55%, which underscores the link between economic empowerment and sustained contraceptive demand.

Government Initiatives and Support Policies

Public procurement programs are scaling in Kenya, Nigeria, and Vietnam, combining free device provision, provider training, and supply-chain upgrades that jointly address cost and access barriers. Kenya’s public hospitals began offering hormonal IUDs at no cost in 2024, widening access beyond private clinics.[3]United Nations Population Fund, “UNFPA Supplies Performance Measurement Report 2023,” UNFPA, unfpa.org Similar models in Nigeria aim to raise modern-method prevalence to 27% by 2026.

Favorable Recommendations from Global Health Organizations

The World Health Organization includes IUDs in essential contraceptive care and offers technical toolkits to help ministries embed them into national formularies.[4]World Health Organization, “Contraception,” WHO, who.intThe International Contraceptive Access Foundation has donated more than 250,000 hormonal devices to low-resource settings, linking supply to hands-on provider mentoring. The World Health Organization moved nulliparous women and adolescents to Category 1 eligibility in its 2024 guidance, signaling that there are no restrictions on copper or hormonal IUDs. The American College of Obstetricians and Gynecologists echoed that stance in 2025 by labeling IUDs as first-line contraceptives for all ages. These endorsements unlock policy changes that oblige payors to list at least one IUD on contraceptive formularies, accelerating placement of the intrauterine contraceptive devices market into routine care pathways across high- and middle-income settings.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Side effects and complications | –0.8% | Global (more acute where specialist care is scarce) | Short term (≤ 2 years) |

| Cultural & religious opposition plus low awareness | –1.1% | Middle East, Africa, rural Asia, conservative U.S. regions | Long term (≥ 4 years) |

| Skilled provider shortage for insertions | –0.7% | Emerging markets, remote areas worldwide | Medium term (2-4 years) |

| High upfront device and insertion cost | –0.6% | Low-income countries, uninsured groups in high-income markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Risk of Side Effects and Complications

Heavy bleeding, cramping, and misplaced insertions remain the top deterrents. A 2024 study in the International Journal of Pharmaceutics links polymer formulation and curing conditions to variable LNG release, which can influence the occurrence of adverse events.[5]International Journal of Pharmaceutics, “Drug Content Uniformity and Release Rate of Levonorgestrel Systems,” sciencedirect.com Provider skill also matters; malposition rates are nearly double when generalists insert devices versus obstetric-gynecology specialists. Bleeding changes and insertion pain still lead to 22% discontinuation among copper users and 14% among levonorgestrel users within 12 months, according to a 2025 meta-analysis of 47 studies.[6]Contraception Journal Editors, “IUD Design Innovations and Clinical Outcomes,” CONTRACEPTIONJOURNAL.ORG Even low perforation rates trigger malpractice suits, raising liability premiums for clinics. These realities dampen provider enthusiasm in low-resource areas, moderating expansion of the intrauterine contraceptive devices market despite high unmet need.

Cultural and Religious Opposition Coupled with Lack of Awareness

Misconceptions that IUDs cause abortion or permanent infertility persist in parts of sub-Saharan Africa and the Middle East. Community surveys in Ethiopia’s Afar and Somali regions found religious concerns to be the leading barrier to modern contraceptive use. Comparable narratives shape recent U.S. state restrictions on Medicaid coverage for IUDs, underscoring the influence of ideology on policy and personal choice.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Hormonal LNG-IUS Gains Despite Copper Dominance

Copper models captured 66.10% of the intrauterine contraceptive devices market share in 2025, driven by their hormone-free appeal and low device cost. Levonorgestrel systems are growing at a 6.25% CAGR because they treat heavy menstrual bleeding while preventing pregnancy, allowing insurers to allocate expenses across two benefit categories. This dual utility boosts willingness to fund higher device prices that nonetheless undercut the USD 15,000-25,000 cost of hysterectomy or ablation. The February 2025 approval of MIUDELLA featuring a flexible nitinol frame and reduced copper illustrates how engineering refinements address historic pain and bleeding complaints, boosting acceptance in regions where side effects once limited uptake. Academic teams pursuing iron-based frames highlight a potential next class of non-hormonal products with softer inflammatory profiles that could lure users who previously avoided copper models.

Manufacturers are also enhancing supply-chain efficiency to lower production costs, a change that supports public-sector tenders seeking bulk volumes at modest price points. Given these trends, copper units will remain volume leaders. Still, hormonal devices are set to capture incremental value share as higher reimbursement ceilings in Europe and North America favor premium pricing.

By Indication: Contraception Dominates, HRT Protection Surges

Contraception held 78.80% of the intrauterine contraceptive devices market size in 2025. Endometrial protection during hormone-replacement therapy shows the fastest growth at 9.28% CAGR since the North American Menopause Society endorsements revived systemic estrogen use for women under 60. Mirena’s HRT-linked label allows gynecologists to serve both contraception and menopausal symptom management with one device, adding appeal among perimenopausal women.

Heavy-bleeding therapy is growing as primary-care physicians shift first-line management from oral drugs to IUD insertion. Manufacturers diversify revenue streams toward menopausal cohorts, hedging against shrinking fertility populations yet keeping intrauterine contraceptive devices market relevance across life stages.

By Age Group: Youth Adoption Accelerates Amid Established Adult Use

Women aged 25-34 years accounted for 62.60% of births in 2025 because this group actively spaces births during career consolidation. Minors under 20 are growing at a 7.28% CAGR, enabled by after-school clinics and revised consent laws that allow same-day insertions without parental permission. California pharmacists may now prescribe and refer for IUD placement, which shrinks access gaps for adolescents seeking confidential services.

Women 35-44 adopt devices for spacing or to control heavy bleeding as they near menopause, while the >44 cohort shows nascent but unexpected uptake for HRT protection. These shifts broaden age diversification in the intrauterine contraceptive devices market. Policy moves that permit confidential youth access and school-based counseling also influence uptake. Meanwhile, uptake among women above 35 remains steady as many seek reliable spacing after completing families but avoid permanent sterilization.

By End User: Community Health Centers Disrupt Hospital Hegemony

Hospitals accounted for 58.07% of placements in 2025, driven by postpartum insertions. Yet, community health centers are advancing at a 6.75% CAGR because nurse and midwife task-shifting shortens wait times and reaches uninsured users. A Health Affairs study noted Medicaid beneficiaries were 2.3 times more likely to select LARC when offered within their usual care point rather than via hospital referral. Specialist OB-GYN clinics retain a loyal base among privately insured women, whereas family-planning centers continue to serve as safety-net providers for uninsured populations.

By Distribution Channel: NGO Programs Outpace Public Procurement

Government tenders still accounted for 53.11% of the intrauterine contraceptive devices market share in 2025, but NGO programs are growing at a 7.63% CAGR as donors advance 2030 contraception targets. DKT International’s social marketing lowers prices to USD 1-3, capturing women beyond state clinics. Private practices and retail pharmacies are gaining momentum in middle-income economies, where out-of-pocket payments align with consumer preferences for convenience.

Telemedicine partners now combine virtual counseling with clinic insertion in two visits rather than three, an efficiency that resonates with tech-savvy urban users. Such hybrid models hint at evolving supply chains that may redefine value metrics in the intrauterine contraceptive devices market.

Geography Analysis

North America retained 39.90% of % intrauterine contraceptive devices market share in 2025, buoyed by Medicaid expansion in 12 states and zero-copay rules under the Affordable Care Act. The United States contributed roughly three-quarters of regional volume, while Canada’s provincial plans added device coverage in 2024. Between 2026 and 2031, the region is forecast to maintain mid-single-digit growth as payors tie reimbursement to continuation rates that favor IUD longevity.

Asia-Pacific is rising fastest, with a 6.45% CAGR. China’s policy shift toward larger families amplifies demand for reversible contraception, and India’s scaled-up free IUD program widens rural access. Indonesia, Vietnam, and the Philippines follow with middle-class uptake of levonorgestrel systems that tackle heavy bleeding. Despite price sensitivity, donor subsidies and domestic manufacturing keep the intrauterine contraceptive devices market affordable in lower-income pockets.

The Middle East and Africa are the fastest-growing regions as multilateral initiatives expand product availability and provider capacity, though cultural resistance still dampens absolute penetration. UNFPA’s Supplies Partnership now covers 54 countries, with IUD availability at secondary care sites rising to 65% in 2024. Sub-Saharan Africa’s average modern-method prevalence sits at 28.4%, and only 9.6% of women use long-acting methods, highlighting vast untapped potential as training and outreach progress.

Competitive Landscape

The arena is moderately fragmented. Bayer AG, CooperSurgical, and Organon leverage extensive global distribution and brand equity, while niche players such as Sebela Women’s Health capture attention with product differentiators that reduce user discomfort. CooperSurgical’s Paragard remains the only FDA-approved non-hormonal IUD in the U.S., underpinning stable cash flows. Sebela’s MIUDELLA launch demonstrates how innovation can carve share even in mature markets, prompting incumbents to invest in frame flexibility and metal-surface optimization. Academic-industry collaboration is intensifying around alternative metals and dual-protection concepts that incorporate antiretroviral release for HIV prevention.

Regional producers, notably in India and China, undercut global brands on price, strengthening their grip on public tenders. Strategic acquisitions and co-manufacturing agreements are proliferating as firms seek cost synergies and faster market entry.

Intrauterine Contraceptive Devices Industry Leaders

-

Abbvie Inc (Allergan Plc)

-

Bayer AG

-

CooperSurgical Inc.

-

DKT International

-

EUROGINE, S.L

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Plan A by NEXT Life Sciences introduced Vasalgel, a reversible and non-hormonal male contraceptive. This long-acting innovation gained significant traction among men, couples, and physicians, addressing a long-standing market demand.

- January 2025: Bayer received FDA approval for a 3-year levonorgestrel IUS with a 13.5 mg hormone load designed for women aged 18-25.

- January 2025: 49Care launched Yanae, a flexible-inserter copper IUD, across Canadian pharmacies with a USD 140 retail price.

- October 2025: Sebela Women’s Health garnered a Contraception journal award for Phase III data on MIUDELLA, its copper intrauterine system.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the intrauterine contraceptive devices market as the annual revenue generated from new copper and hormonal systems that are inserted into the uterus for long-acting pregnancy prevention, across all clinical end-user channels.

According to Mordor Intelligence, refurbished devices, diaphragms, contraceptive implants, and emergency-use copper IUDs sold outside regular family-planning settings are excluded.

Segmentation Overview

-

By Device Type

- Hormonal LNG-IUS

- Copper IUD

-

By Indication

- Contraception

- Heavy Menstrual Bleeding therapy

- Endometrial Protection during HRT

-

By Age Group

- <20 Years

- 20-24 Years

- 25-34 Years

- 35-44 Years

- >44 Years

-

By End-User

- Hospitals

- Gynecology & Obstetrics Clinics

- Community Health Centers

- Family-Planning / Sexual-Health Centers

- Tele-health Enabled Home-Insertion Programs

-

By Distribution Channel

- Public Sector Procurement

- Private Clinics & Retail

- NGO/Donor-Funded Programs

- Online & Pharmacy E-commerce

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed obstetricians, hospital procurement leads, and NGO supply-chain managers across North America, India, Nigeria, and Brazil. These conversations clarified real-world insertion fees, public versus private mix shifts, copper to hormonal conversion rates, and expected device lifespans, giving us confidence to refine model drivers surfaced during desk work.

Desk Research

We began with open datasets from the WHO family-planning dashboard, UNFPA contraceptive commodity procurement files, the CDC's National Survey of Family Growth, Eurostat birth-control sales codes, and Demographic & Health Surveys, which revealed age-cohort adoption, public-sector tender values, and unit imports. Company 10-Ks, FDA device registries, and trade-association briefs (FIGO, ACOG) anchored average selling prices and technology refresh cycles. Paid look-ups on D&B Hoovers and Dow Jones Factiva filled recent revenue splits and launch timelines. The sources cited here are illustrative; many additional references were reviewed during validation.

Market-Sizing & Forecasting

A top-down demand pool was built from the female reproductive-age population, modern-method prevalence, and IUD penetration ratios, which are then multiplied by weighted ASPs. Select bottom-up roll-ups of major suppliers' device shipments tested total plausibility. Key variables like procurement budgets, postpartum insertion policies, hormonal system price premiums, and region-specific discontinuation rates power a multivariate regression that projects value through 2030. Gap years in shipment disclosures are bridged with scenario curves aligned to interview consensus.

Data Validation & Update Cycle

Outputs pass three-layer checks: automatic variance flags, senior analyst peer review, and quarterly re-contacts when policy shocks or recalls arise. Reports refresh every twelve months; interim patches are issued if material events shift our baseline.

Why Our Intrauterine Contraceptive Devices Baseline Commands Reliability

Published estimates diverge because firms frame scope, price, and refresh cadence differently. Mordor's disciplined exclusions, dual-track modeling, and annual update rhythm keep our numbers grounded for planners. Scope drift, mixed device baskets, and currency timing explain most gaps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| $5.62 B (2025) | Mordor Intelligence | - |

| $4.30 B (2025) | Global Consultancy A | Leaves NGO volumes out; uses ex-factory pricing. |

| $6.47 B (2024) | Industry Journal B | Combines IUDs with subdermal implants, inflating base year. |

| $4.56 B (2024) | Regional Consultancy C | Models only copper devices in revenue pool. |

The comparison shows that once differing device mixes and channel coverages are stripped away, Mordor's balanced, transparent baseline, anchored to clearly cited variables and repeatable steps, remains the dependable reference point for strategy teams.

Key Questions Answered in the Report

What is the current value of the intrauterine contraceptive devices market?

The intrauterine contraceptive devices market size stands at USD 5.83 billion in 2026 and is projected to reach USD 7.05 billion by 2031.

How fast is the intrauterine contraceptive devices market expected to grow?

Between 2026 and 2031 the market is forecast to expand at a 3.86% CAGR.

Which device type leads global sales?

Copper IUDs held 66.10% of intrauterine contraceptive devices market share in 2025.

Which region shows the strongest growth momentum?

Asia-Pacific is forecast to post the fastest regional CAGR at 6.45% through 2031.

What factor most boosts adolescent uptake?

Revised consent laws and school-based same-day insertion programs drive a 7.28% CAGR in the <20 years cohort.

Which company recently secured FDA approval for a shorter-duration IUS?

Bayer earned January 2025 approval for a 3-year levonorgestrel IUS targeting younger women.

Page last updated on: