United States Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

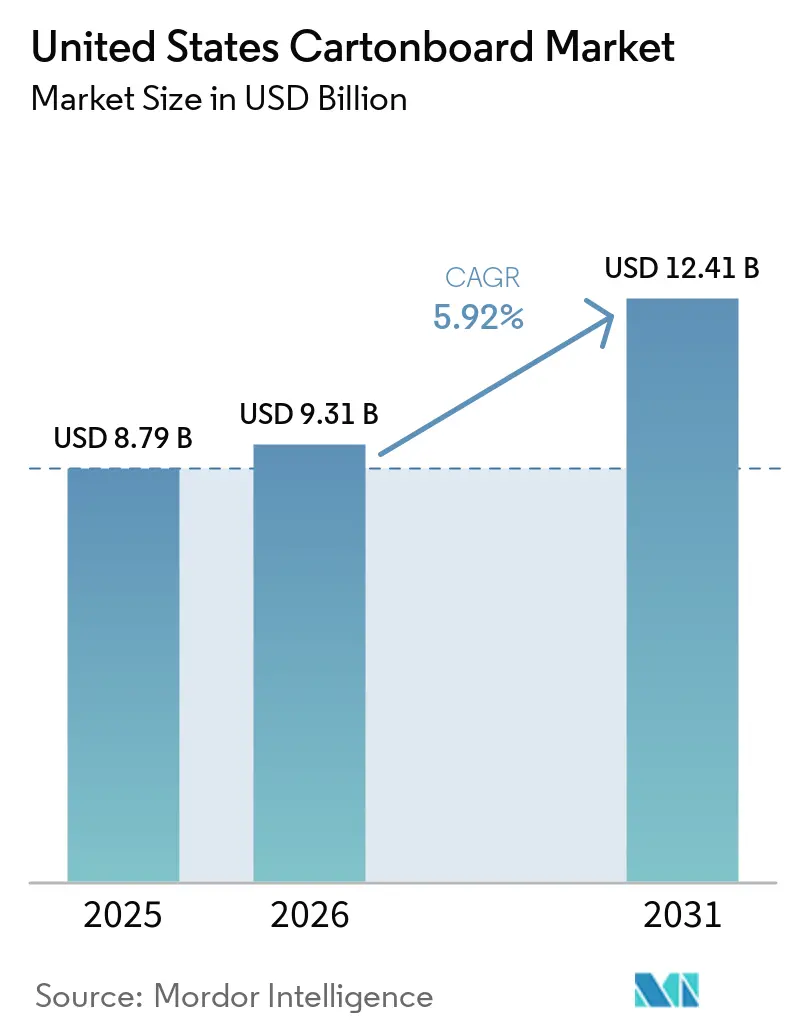

| Base Year Market Size (2025) | USD 8.79 Billion |

| Market Size (2026) | USD 9.31 Billion |

| Market Size (2031) | USD 12.41 Billion |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

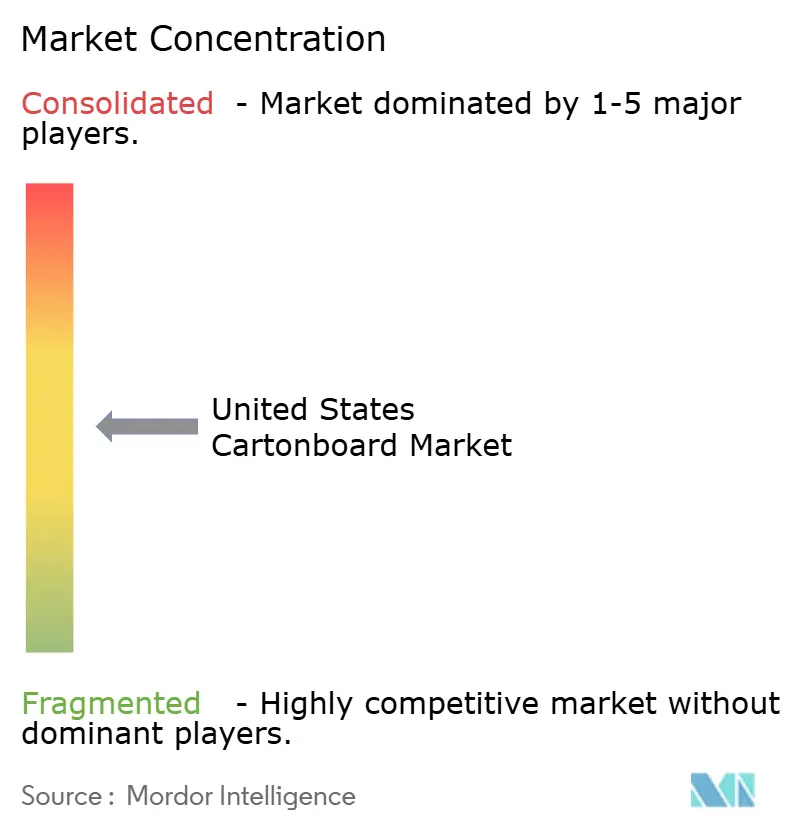

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Cartonboard Market Analysis by Mordor Intelligence

The United States cartonboard market size was valued at USD 8.79 billion in 2025 and estimated to grow from USD 9.31 billion in 2026 to reach USD 12.41 billion by 2031, at a CAGR of 5.92% during the forecast period (2026-2031). Growth in the United States cartonboard market was tied less to short-cycle demand swings and more to durable shifts in packaging choice across retail, healthcare, foodservice, and branded consumer goods. Retailers increasingly pushed suppliers toward plastic-free fiber formats, keeping cartonboard relevant even in a cost-conscious packaging environment. Pharmaceutical supply chains also raised the technical value of folding cartons as serialization rules moved cartons from simple outer packs to traceable components in a regulated system. Consumer demand for premium shelf presentation in food, beverage, and personal care supported higher-value grades with stronger printability, barrier properties, and compliance credentials. Rising energy, fiber, and freight costs still created pressure, but those same conditions favored larger integrated producers that could spread input volatility across wider mill and converting networks.

Key Report Takeaways

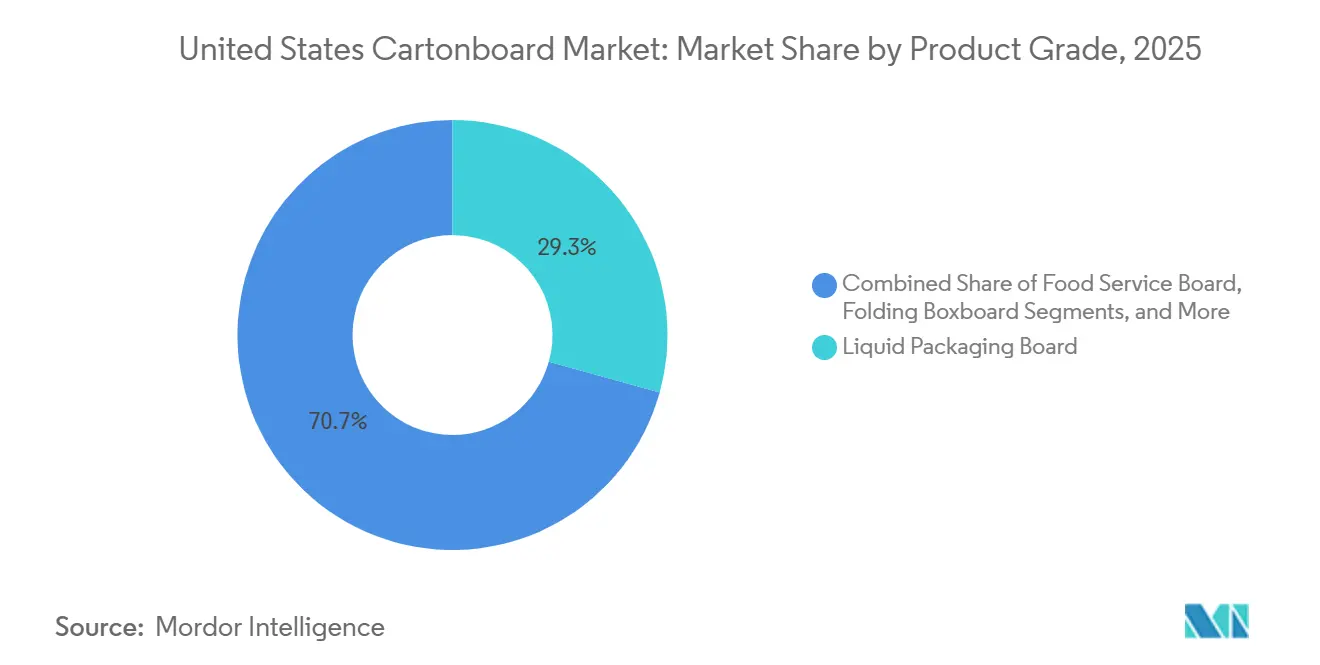

- By product grade, liquid packaging board captured 29.31% of the United States cartonboard market share in 2025.

- By packaging format, the United States cartonboard market size for the liquid packaging segment is forecast to advance at a 6.52% CAGR through 2031.

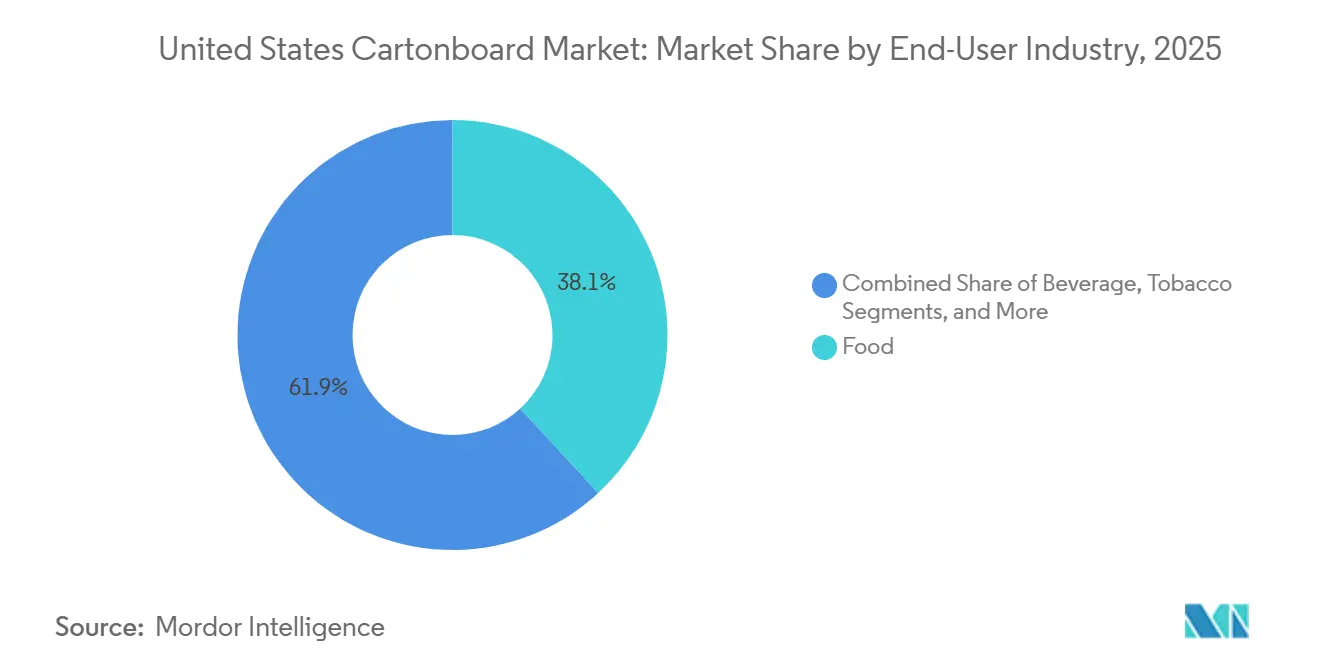

- By end-user industry, food captured 38.14% of the United States cartonboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Packaged Food And Fresh Convenience Demand | +1.8% | National, with strongest gains in the Southeast and Midwest food processing corridors | Short term (≤ 2 years) to Medium term (2-4 years) |

| Premiumization And Shelf-Impact Requirements In Health And Beauty Packaging | +1.0% | National, concentrated in major retail markets, including the Northeast, California, and Texas | Medium term (2-4 years) |

| Pharmaceutical Serialization And Tamper-Evident Carton Demand | +0.7% | National, with early gains in the Northeast and Mid-Atlantic pharmaceutical hubs | Short term (≤ 2 years) |

| Shift From Plastic Rings To Paperboard Beverage Multipacks | +0.5% | National, with early implementations in the Mid-Atlantic and Southeast | Short term (≤ 2 years) to Medium term (2-4 years) |

| Higher-Paper-Content Aseptic Carton Innovation | +0.4% | National, with supply infrastructure developing in the South-Central United States | Long term (≥ 4 years) |

| Retailer Pull For PFAS-Free Fiber Foodservice Packaging | +0.3% | National, led by states with active mandates, including California, Washington, Maine, and Maryland | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Packaged Food And Fresh Convenience Demand

Food remained the broadest demand base for the United States cartonboard market, accounting for 38.14% of total demand in 2025 across dry grocery, frozen meals, refrigerated products, and convenience-led formats.[1]Paperboard Packaging Council, “2025-26 Trends Industry Outlook and Market Data Report,” Paperboard Packaging Council, paperbox.org The food mix also shifted toward branded cartons that signaled ingredient clarity, storage integrity, and stronger shelf presence in premium health food, meal kit, and private-label grocery lines. The Paperboard Packaging Council’s 2025-26 outlook, prepared with Fastmarkets RISI, identified food as one of 7 end-use markets expected to expand by more than 1% annually through 2029, and that supported a steady floor for board consumption. That demand pattern favored grades with specific performance requirements, including moisture resistance, grease resistance, and compliance with 21 CFR FDA requirements for food-contact uses.[2]U.S. Food and Drug Administration, “Questions and Answers on PFAS in Food,” FDA, fda.gov As a result, the United States cartonboard market increasingly rewarded suppliers that could qualify targeted specifications rather than sell undifferentiated tonnage into broad commodity channels. That shift also improved revenue quality because more buyers were selecting based on function, compliance, and branding value rather than on simple volume procurement.

Premiumization And Shelf-Impact Requirements In Health And Beauty Packaging

Health, beauty, and personal care brands used cartonboard as a visible part of price positioning, especially where print quality and pack finish influenced retail conversion. Circana reported that United States prestige beauty retail sales reached USD 36 billion in 2025, up 4% year over year, while mass beauty sales rose 5% to USD 72.7 billion, keeping demand active across both premium and value carton formats. Prestige brands leaned toward higher-brightness solid bleached board and refined folding carton finishes, while mass-market brands upgraded graphics and structure to improve shelf visibility without moving fully into luxury-grade specifications. State packaging EPR laws also strengthened the case for recyclable fiber formats because implementation continued in California, Colorado, Maine, Maryland, Minnesota, Oregon, and Washington during 2026 and 2027. That policy setting gave fiber-based packs a practical compliance edge over complex multi-material formats that were harder to recover and more exposed to future fee pressure. In the United States cartonboard market, this meant aesthetic value and regulatory fit increasingly moved together, which supported durable demand for folding cartons in beauty aisles.

Pharmaceutical Serialization And Tamper-Evident Carton Demand

The DSCSA enforcement cycle concluded in stages through 2025, with manufacturer compliance effective on May 27, 2025, wholesale distributor compliance on August 27, 2025, and dispenser compliance on November 27, 2025. That schedule established a fully serialized United States pharmaceutical supply chain and made the carton a traceable component rather than a low-spec outer pack.[3]GS1 US, “Frequently Asked Questions by the Pharmaceutical Industry in Preparing for the US DSCSA,” GS1 US, gs1us.org Each saleable pharmaceutical carton now requires a unique product identifier in both human-readable and machine-readable formats, prompting converters to integrate print, verification, and data-control systems into existing lines. DLA Piper also noted that exemptions for small dispensers with 25 or fewer full-time employees extended until November 27, 2026, so a final phase of specification changes continued to move through the system in 2026. This increased the unit value of pharmaceutical cartons by incorporating serialization, anti-tamper design, and audit-ready documentation into the product specification. It also favored established converters with validated healthcare operations, including Oliver Inc. and Nosco, Inc., and added another high-barrier demand layer to the United States cartonboard market.

Shift From Plastic Rings To Paperboard Beverage Multipacks

Beverage brands accelerated the switch from plastic ring carriers to paperboard alternatives as sustainability commitments started to translate into installed production assets. In June 2024, Liberty Coca-Cola Beverages and WestRock completed the first United States installation of a paperboard multipack carrier system at the Philadelphia facility, supported by a USD 3.5 million capital investment. That project was expected to replace 200,000 pounds of plastic rings each year, and it gave the United States cartonboard market a visible proof point for high-volume substitution in beverage secondary packaging. Molson Coors also committed USD 85 million to remove plastic six-pack rings across its Americas portfolio, and Coors Light completed the North American shift to recyclable paperboard wrap carriers. Public commitments from AB InBev, PepsiCo, and Molson Coors signaled that the transition extended beyond a single pilot and was becoming a format choice with broader category relevance. That mattered because beverage multipacks can deliver repeat board demand at scale, and successful conversion in cans can open similar pathways in water, sports drinks, and ready-to-drink cocktails.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Virgin Fiber, Energy, And Freight Cost Volatility | -1.1% | National, with particular exposure in energy-intensive Southeast and inland mills | Short term (≤ 2 years) to Medium term (2-4 years) |

| Food-Contact Compliance Constraints On Recycled And Barrier-Coated Board | -0.7% | National, most acute in states with active food packaging regulations | Medium term (2-4 years) |

| PFAS Reformulation And Requalification Costs | -0.5% | National, led by states with active mandates, including California, Washington, and Maine | Short term (≤ 2 years) |

| Barcode, Serialization, And Converting-Line Upgrade Burdens | -0.4% | National, concentrated in pharmaceutical and healthcare converting clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Virgin Fiber, Energy, And Freight Cost Volatility

Input cost inflation remained the most immediate restraint on the United States cartonboard market because fiber, energy, and freight pressures rose simultaneously in 2026. Sonoco announced a USD 70 per ton price increase for uncoated recycled paperboard, effective in April 2026, followed by an 8% increase on converted paperboard products, showing how quickly higher costs were being passed downstream. Smurfit Westrock moved on a USD 50 per ton increase in containerboard, effective in June 2026, and International Paper announced USD 70 per ton hikes for the same period as energy and freight costs rose. AF and PA data for Q1 2026 showed North American containerboard production fell by more than 8% year over year, and that tightening supply conditions strengthened producer pricing power. The Ohio State University also cited analysis showing that United States pulp production costs were 40% higher than in South America, leaving domestic producers with less room to absorb sudden cost shocks internally. The pressure was most severe for smaller converters because they had limited buying leverage, narrower sourcing flexibility, and weaker ability to spread inflation across a broad product portfolio.

Food-Contact Compliance Constraints On Recycled And Barrier-Coated Board

Recycled-content cartonboard faced tighter food-contact scrutiny as brands and regulators focused more directly on contamination risk in direct-contact packaging.[4]U.S. Food and Drug Administration, “Questions and Answers on PFAS in Food,” FDA, fda.gov PFAS compounds used in grease-resistant treatments could persist in recycled fiber streams, limiting how far converters can push recycled content in sensitive food applications. The FDA revoked 35 food-contact notifications for PFAS-containing greaseproofing agents in January 2025 and set June 30, 2025, as the deadline to exhaust existing inventory, forcing the supply chain to requalify food-contact paperboard. Dairy Reporter reported that more than 15,000 PFAS-related lawsuits were pending in the United States in early 2026, raising legal costs associated with incomplete supply chain documentation. The compliance burden was especially significant in states that already enforced PFAS packaging restrictions, as converters had to document grade-level conformity more carefully before launching new products. That slowed substitution decisions in the United States cartonboard market because recycled and barrier-coated grades could no longer compete on price alone when qualification time and regulatory exposure were also part of the buying decision.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Liquid Board Anchored The Base As Foodservice Grades Led Growth

Liquid packaging board accounted for 29.31% of the United States cartonboard market in 2025, making it the largest product grade in the country. Its lead position came from durable demand across dairy, juice, plant-based beverages, and aseptic food formats, where barrier performance, printability, and shelf life remained difficult to replicate with simpler substitutes. Solid bleached board stayed important in premium folding carton applications for pharmaceuticals and beauty because brightness, print surface, and food or drug contact compliance carried clear commercial value in regulated uses. Solid unbleached board served a narrower but stable role in beverage multipacks and other strength-led applications where rigidity mattered more than premium surface appearance. Folding boxboard competed with SBB in health, beauty, and food grocery segments, although European suppliers such as Stora Enso Oyj and Metsa Board Corporation faced tariff-related headwinds in 2026 when serving United States converters.

Food service board was the fastest-growing product grade in the United States cartonboard market and was projected to advance at a 6.18% CAGR from 2026 to 2031 as PFAS reformulation and plastic substitution moved into commercial execution. Sappi North America introduced LusterFSB OGR at its Somerset Mill in Maine, and the grade was designed to deliver oil- and grease-resistance without polyethylene coatings, addressing an immediate reformulation need in foodservice converting. Clearwater Paper launched Velora in March 2026 as a lightweight folding carton paperboard that met FDA 21 CFR requirements and was targeted at converters seeking a cost-conscious domestic alternative to premium SBS. The regulatory pull grew stronger as Maine’s plant-fiber PFAS food packaging restriction took effect in May 2026, while Washington and California continued to set the pace on food-contact packaging compliance.

By Packaging Format: Folding Cartons Dominated While Liquid Packaging Accelerated

Folding cartons accounted for 53.18% of the United States cartonboard market in 2025, making them the clear lead format across the value chain. That position reflected broad use across food grocery, pharmaceutical secondary packaging, cosmetics, personal care, and other retail goods that needed shape, print clarity, and good stacking performance. The format also remained durable because the same converting footprint could support commodity packs, premium cartons, anti-counterfeit features, embossing, spot UV, and serialized print, depending on the customer category. Sleeve and tray applications addressed more specific structural needs in beverage multipacks and club-store retail, where cartonboard wraps continued to displace plastic shrink film and ring carriers. Other packaging forms, including cups, foodservice containers, and composite cans, were more closely tied to restaurant traffic, school meal programs, and institutional demand patterns than to discretionary retail cycles.

Liquid packaging was the fastest-growing format and is expected to expand at a 6.52% CAGR through 2031, which kept it ahead of the overall United States cartonboard market growth rate. The growth path was supported by greater use of aseptic cartons in dairy alternatives, ready-to-drink beverages, and longer-shelf-life food products, which benefited from lightweight distribution and stable shelf presentation. Tetra Pak announced a EUR 60 million (USD 71.2 million) paper-based barrier pilot plant in January 2026 to increase paper content in aseptic cartons to 80% and total renewable content to 92%, reducing reliance on aluminum foil layers. Elopak’s first United States plant in Little Rock opened in April 2025, and the company reported 18% organic revenue growth in the Americas in 2025, as a second production line ramped in 2026, targeting USD 110 million in additional annual revenue.

By End-User Industry: Food Grounded Demand While Pharma Led The Growth Cycle

Food held 38.14% of the United States cartonboard market share in 2025, keeping it as the largest end-user base by a clear margin. Its scale reflected cartonboard’s continued role in cereal, confectionery, frozen food, dry pasta, refrigerated produce, and a wide range of secondary and direct-contact grocery applications. Food demand also acted as a stabilizer for the United States cartonboard industry because growth in private-label premiumization and convenience-oriented grocery use offset pressure from flexible formats in selected snack and single-serve categories. The beverage end-user mix shifted as liquid cartons and paperboard multipacks gained ground against plastic rings and shrink film, supported by visible adoption from Liberty Coca-Cola Beverages, Molson Coors, and AB InBev. Tobacco remained a modest but stable cartonboard consumer through rigid outer packaging, while cosmetics and toiletries continued to drive demand as beauty retail sales expanded across both prestige and mass channels.

Pharmaceuticals and healthcare were the fastest-growing end-user segments and are projected to advance at a 6.72% CAGR from 2026 to 2031, placing them above the broader United States cartonboard market trajectory. The DSCSA required each saleable pharmaceutical unit to carry a unique GS1 DataMatrix identifier, turning every compliant folding carton into part of a verified traceability system. Specialty converters such as Oliver Inc., Nosco, Inc., and JohnsByrne Company benefited because they already served regulated accounts that needed anti-tamper features, variable data, and repeatable print control. That combination of qualification depth, compliance systems, and customer stickiness kept pharma packaging one of the highest-barrier demand pools in the United States cartonboard industry.

Geography Analysis

Regional demand in the United States cartonboard market was strongest in the Southeast and Mid-Atlantic corridor, where consumer goods manufacturing, converting activity, and pharmaceutical packaging demand were concentrated. The Southeast and South-Central regions served as the main production spine because they combined mill assets, converting plants, forest fiber access, and efficient links to broad domestic distribution routes. Graphic Packaging International’s base in Atlanta anchored a large converting network across the region and reinforced the Southeast’s role in board production and downstream packaging services. Elopak opened its first United States carton-converting plant in Little Rock, Arkansas, in April 2025, with a USD 100 million investment, adding domestic liquid carton capacity to a region already strong in packaging logistics. Clearwater Paper’s Cypress Bend, Arkansas, mill remained an important SBS source even after output was reduced to around 50% of capacity in late 2025 in response to softer market conditions. The Northeast and Mid-Atlantic formed the most concentrated cluster for pharmaceutical and premium beauty packaging demand in the United States cartonboard market.

New Jersey, Pennsylvania, and New York remained important pharmaceutical secondary packaging states because high-value healthcare production and distribution activity were closely tied to serialization-ready carton demand. Maine also stood out in high-specification board production because Sappi’s Somerset Mill supplied SBS grades for premium packaging and launched the LusterFSB OGR foodservice board for grease-resistant applications. State compliance pressure was also stronger in this corridor because Maine’s first-phase PFAS restriction for plant-fiber food packaging took effect in May 2026, and Maryland continued advancing its EPR framework.

This created a higher compliance baseline for converters serving national accounts, as large retailers typically expected a single-pack format that met the most demanding state requirements. The West Coast acted as the regulatory frontier for the United States cartonboard market because California and Washington shaped expectations for recyclable fiber packaging and PFAS-free food-contact formats. California’s SB 54 framework attached lower producer fees to recyclable fiber packaging, and Washington’s phased PFAS ban for plant-fiber food packaging had already reached full coverage by 2025. Import dynamics added another regional layer, as European board suppliers, including Metsa Board Corporation and Billerud Aktiebolag (publ), saw weaker United States deliveries in Q1 2026 amid higher tariffs that raised landed costs. That gave domestic producers a near-term advantage in cost-sensitive grades, especially at a time when North American supply was tightening, and price increases were moving through the system.

Competitive Landscape

The United States cartonboard market was moderately concentrated at the board production level, as a small set of integrated producers controlled broad mill, converting, and customer service capabilities. Smurfit Westrock plc and Graphic Packaging International, LLC stood out for scale, vertical integration, and the ability to manage both board supply and downstream packaging programs across large national accounts. Smurfit Westrock’s February 2026 medium-term plan targeted USD 7 billion in adjusted EBITDA by the end of 2030 and USD 14 billion in cumulative discretionary free cash flow, supported by USD 2.4 to USD 2.8 billion in annual capital expenditures. Graphic Packaging completed its USD 1.67 billion Waco, Texas, recycled paperboard facility in late 2025 and described it as North America’s most advanced and efficient recycled paperboard production platform. That upper-tier scale contrasted with a far more fragmented converting layer, where specialty suppliers competed more on technical fit and customer validation than on raw production volume.

Competitive differentiation in the United States cartonboard market is increasingly centered on material innovation, regulatory readiness, and the ability to offer compliant substitutes without long qualification delays. Clearwater Paper’s March 2026 launch of Velora showed that lightweight SBS alternatives had become a real competitive tool for converters facing cost pressure and lead-time risk. Sappi North America’s LusterFSB OGR launch demonstrated a different strategy, with barrier innovation aimed directly at customers facing PFAS-related reformulation deadlines in foodservice packaging. Liquid carton suppliers also expanded their North American footprint because Elopak scaled up in Arkansas and SIG Group announced a phased expansion in Queretaro to double aseptic carton output to 3 billion packs per year by 2028.

Those moves mattered because packaging buyers increasingly wanted domestic or near-regional supply resilience while also asking for higher paper content, stronger recyclability claims, and more predictable compliance support. A notable opening remained in mid-market pharmaceutical converting, where DSCSA requirements created structural demand that many smaller regional players were not fully equipped to serve. That favored converters such as Oliver Inc., Nosco, Inc., and JohnsByrne Company because they could combine regulated printing capability with customer-specific validation and documentation needs. European groups also expanded through United States converting operations rather than direct board exports, which reduced tariff exposure and kept them closer to regulated customers. Mayr-Melnhof Karton AG operated 6 converting facilities in the United States focused on pharma packaging, while Stora Enso’s Performa Lumi launch in March 2026 targeted beauty, personal care, and healthcare packaging with a graphics-led offer.

United States Cartonboard Industry Leaders

Smurfit Westrock plc

Graphic Packaging International, LLC

Clearwater Paper Corporation

Sonoco Products Company

International Paper Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Graphic Packaging International completed a 90-day business review and implemented a workforce reduction of more than 500 employees, approximately 3% of its global workforce and 10% of full-time salaried positions, as part of cost-reduction actions targeting USD 60 million in 2026 savings, adjusted cash flow guidance of USD 700 to USD 800 million is reaffirmed for the year.

- April 2026: International Paper Company entered into a definitive agreement to acquire North Pacific Paper Company (NORPAC) for USD 360 million, NORPAC operates a Longview, Washington mill with approximately 1 million tons of annual containerboard and other grade capacity, strengthening IP's West Coast supply position and expanding its recycled containerboard capabilities.

- April 2026: SIG Group AG announced a phased expansion of its Queretaro, Mexico manufacturing plant to double aseptic carton production capacity from 1.5 billion to 3 billion packs per year by 2028, with Phase I new finishing and printing technologies beginning in 2026 and Phase II extrusion integration by end-2028, reinforcing the company's North American supply footprint.

- March 2026: Clearwater Paper Corporation launched Velora, a lightweight folding carton paperboard certified under FDA 21 CFR and Sustainable Forestry Initiative (SFI) standards, the grade targets converters seeking a cost-efficient domestic SBS alternative with stable lead times, complementing Clearwater's premium Candesce brand.

United States Cartonboard Market Report Scope

The United States Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The United States Cartonboard Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, Other Packaging Formats), End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, Other End-User Industries). Market Forecasts are in Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

Key Questions Answered in the Report

What is the current and future size of the United States cartonboard sector?

The United States cartonboard market size was USD 8.79 billion in 2025, was estimated at USD 9.31 billion in 2026, and is forecast to reach USD 12.41 billion by 2031 at a 5.92% CAGR.

Which product grade leads demand in the United States cartonboard space?

Liquid packaging board led product grade demand with a 29.31% share in 2025, supported by dairy, juice, plant-based beverage, and aseptic food applications.

Which packaging format is growing fastest in the United States cartonboard business?

Liquid packaging is projected to record the fastest format growth at a 6.52% CAGR through 2031 as aseptic and chilled carton use expands.

Why is pharmaceutical packaging becoming more important for cartonboard suppliers in the United States?

DSCSA serialization requirements raised the technical value of pharma cartons, and pharmaceutical and healthcare is projected to grow at a 6.72% CAGR through 2031.

What is driving the shift from plastic to cartonboard in beverage packaging?

Beverage brands are replacing plastic rings with paperboard multipacks to meet sustainability targets and state packaging rules, with Liberty Coca-Cola Beverages and Molson Coors among visible adopters.

What is the biggest near-term challenge for cartonboard producers and converters in the United States?

The main near-term challenge is input cost volatility across fiber, energy, and freight, which has already led to multiple producer price increases in 2026 and tighter margin conditions for smaller converters.

Page last updated on: