Nordic Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.96 Billion |

| Market Size (2026) | USD 0.98 Billion |

| Market Size (2031) | USD 1.10 Billion |

| Growth Rate (2026 - 2031) | 2.34% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nordic Cartonboard Market Analysis by Mordor Intelligence

The Nordic cartonboard market size is projected to expand from USD 0.96 billion in 2025 and USD 0.98 billion in 2026 to USD 1.10 billion by 2031, registering a CAGR of 2.34% over 2026-2031. Growth in the Nordic cartonboard market is being shaped less by tonnage gains and more by changes in pack specifications, as regulatory requirements, brand sustainability targets, and consumer-facing packaging choices shift demand toward premium fresh-fiber grades and PFAS-free barrier structures. The PPWR timeline has already brought forward purchasing decisions for Nordic FMCG and pharmaceutical buyers, supporting earlier demand for compliant board grades and tightening the link between packaging design and procurement cycles. Sweden’s integrated forest and paper base, together with Finland’s recent capacity additions, gives the region a strong supply position and keeps the Nordic cartonboard market important in export trade and product development. Norway and Denmark remain important demand centers for food, dairy, pharmaceutical, and liquid packaging, while oat drinks and dairy alternatives are adding new pressure on liquid carton structures. This leaves the Nordic cartonboard market on a path where value growth exceeds volume growth, pricing is more important than tonnage, and supplier rationalization continues to favor mills that can offer recyclable, PFAS-free, and certified substrates with stable quality.

Key Report Takeaways

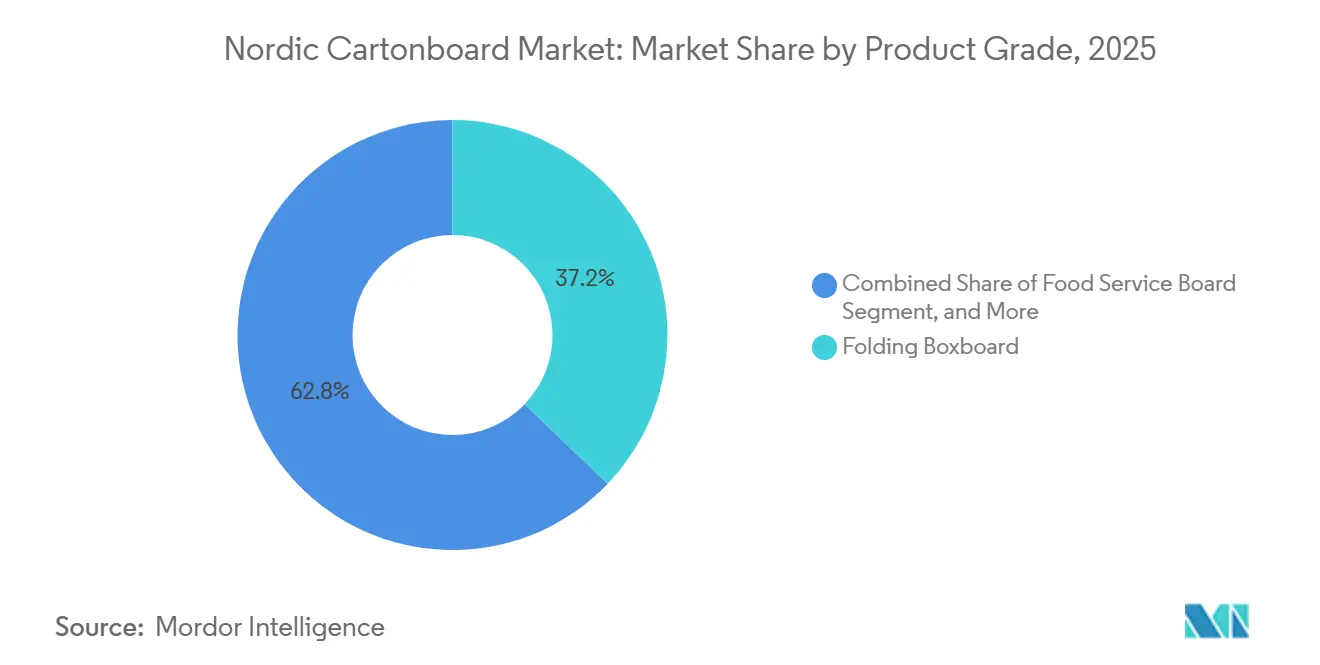

- By product grade, folding boxboard captured 37.17% of the Nordic cartonboard market share in 2025.

- By packaging format, the Nordic cartonboard market size for the liquid packaging segment is forecast to advance at a 2.95% CAGR through 2031.

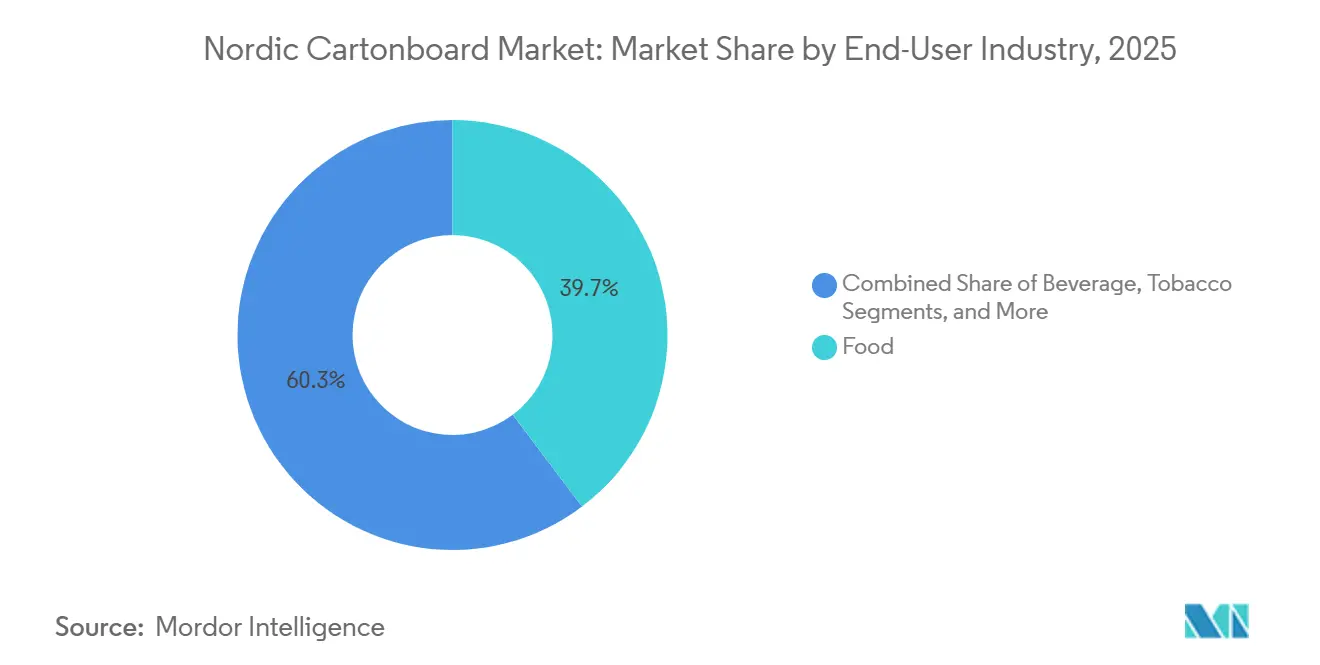

- By end-user industry, food captured 39.71% of the Nordic cartonboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Nordic Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recyclability-Ready Packaging Portfolio Shifts | +0.8% | Pan-Nordic, strongest regulatory pull in Sweden and Finland | Medium term (2-4 years) |

| Premiumization Of Fresh And Chilled Food Cartons | +0.6% | Norway and Denmark dairy clusters, Sweden premium food retail | Medium term (2-4 years) |

| Brand Migration From Plastic To Fiber Packs | +0.5% | Pan-Nordic, FMCG brands headquartered in Sweden and Norway | Short term (≤ 2 years) |

| Shelf-Ready Secondary Packaging Demand | +0.3% | Sweden and Denmark grocery retail hubs | Short term (≤ 2 years) |

| PFAS-Free Barrier Innovation Adoption | +0.2% | Finland and Sweden mill and converter clusters | Medium term (2-4 years) |

| Nordic Oat And Dairy Alternative Pack Expansion | +0.2% | Sweden and Finland oat-drink production centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Recyclability-Ready Packaging Portfolio Shifts

The PPWR applies from August 12, 2026, and requires packaging placed on the EU market to be recyclable, making recyclability a direct commercial requirement rather than a voluntary packaging preference. In the Nordic cartonboard market, that timing has compressed decision cycles for FMCG and pharmaceutical buyers, who are now pre-qualifying recyclable carton structures before the formal application date. Demand is splitting within the same product grade because mills that can demonstrate design-for-recycling alignment are winning forward-book contracts earlier than those still adjusting barrier systems. The effect is especially visible in fresh-fiber folding boxboard and liquid packaging board, where converters want documented recyclability before they commit to new pack formats. UPM Specialty Materials and BASF formalized a collaboration in May 2026 to accelerate the adoption of recyclable fiber-based packaging by combining barrier-based papers with Joncryl HPB resin technology, demonstrating how the upstream chemical chain is moving toward fiber-compatible solutions.[1]BASF, “UPM and BASF Accelerate the Transition to Recyclable, Fiber-Based Packaging,” BASF, basf.com That progress is reducing technical hesitation across the Nordic cartonboard market and is making compliant premium grades easier to specify in commercial tenders.

Premiumization Of Fresh And Chilled Food Cartons

Fresh and chilled food categories are lifting value per unit in the Nordic cartonboard market, even though volume growth remains measured. Organic dairy, plant-based beverages, artisanal chilled foods, and convenience-led refrigerated formats all need strong print quality, food-contact reliability, and shelf appeal, in formats that still meet recycling rules. This is pushing brand owners toward fiber-based and low-emission board structures as standard purchase conditions rather than optional sustainability upgrades. The change matters because it supports better contract pricing for mills that can pair visual quality with credible environmental credentials. Elopak produced 16 billion cartons in 2025, and EMEA accounted for 69% of its revenue, which reflects the scale at which chilled and fresh liquid packaging demand is feeding into board procurement across Northern Europe. As retailers and consumer brands keep refining pack formats to align with real consumption habits, the Nordic cartonboard market continues to reward suppliers that can deliver premium grades without requiring filling-line changes.

Brand Migration From Plastic To Fiber Packs

The plastic-to-fiber shift is moving fastest in secondary and transit packaging because those formats can often be redesigned faster than primary food-contact packs in the Nordic cartonboard market. Walki stated that its paper-based solutions grew 27% in 2025, while recyclability in its consumer packaging portfolio improved from 62% to 65%, which shows that conversion programs are already moving at scale.[2]Walki Group, “Supporting the Transition Toward Circular, Fibre-Based Packaging, Walki’s 2026 Outlook,” Walki Group, walki.com Consumer preference is also supporting these redesigns, as a survey referenced in a KCL and Kemira webinar found that 89% of European consumers would choose cartonboard packaging over plastic when given the option.[3]KCL, “High-Performance Barrier Coatings - KCL-BIOHUB Webinar,” KCL, kcl.fi In practical terms, the first wave of conversion tends to land in standard folding boxboard and white-lined chipboard applications for sleeves, trays, and other outer-pack formats. Once those changes are in place, brand owners are more willing to fund more complex primary-pack reformulations. That sequence is helping the Nordic cartonboard market build demand in steps rather than through one-time portfolio resets.

Shelf-Ready Secondary Packaging Demand

Shelf-ready packaging is gaining ground because Nordic grocery chains want replenishment formats that move directly from delivery units to store shelves with less manual handling. This is changing board selection in the Nordic cartonboard market, as converters must now meet strength, stacking, visibility, and machine-handling requirements within the same pack. The shift favors suppliers that can deliver lightweight formats with stable performance rather than only low-cost commodity grades. It also adds complexity because some shelf-ready structures use layered fiber solutions that must still fit under the PPWR design-for-recycling approach. Retail automation standards are therefore becoming a quiet but important gatekeeper for board qualification across food and convenience categories. In the Nordic cartonboard market, this gives an edge to mills and converters that can align lightweight design, logistics performance, and recycling compatibility in one specification.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Nordic Energy And Fiber Input Costs | -0.5% | Pan-Nordic, most acute in southern bidding zones of Sweden and Norway | Medium term (2-4 years) |

| PFAS Compliance And Reformulation Risk | -0.2% | Finland and Sweden, food-contact barrier specialists | Short term (≤ 2 years) |

| Composite Liquid Carton Recycling Gaps | -0.1% | Pan-Nordic, Norway and Denmark sorting infrastructure gaps | Medium term (2-4 years) |

| Supplier Base Rationalization By Large FMCG Buyers | -0.1% | Sweden and Finland, major FMCG procurement clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Nordic Energy And Fiber Input Costs

Cost pressure remains one of the clearest limits on faster expansion in the Nordic cartonboard market because board production still depends on energy-intensive assets and stable raw material sourcing. The International Energy Agency stated that the Nordic region saw fewer hours of negative-priced electricity in 2025 as battery deployment reduced excess renewable generation, meaning mills had less access to very low off-peak power than in prior periods.[4]International Energy Agency, “Electricity 2026 - Prices,” International Energy Agency, iea.org The same report noted that EU Emissions Trading System prices averaged EUR 75 per tonne of CO2 in 2025, which added to the operating costs of energy-intensive board machines. Internal price divergence between northern and southern bidding zones in Sweden and Norway is also creating uneven pressure across mill locations. That matters because mills near large demand centers may face a different cost profile than mills connected to lower-cost northern power zones. In the Nordic cartonboard market, this forces producers to balance energy hedging, on-site power projects, and boardline upgrades with the need to protect margins in premium product categories.

PFAS Compliance And Reformulation Risk

PFAS-related reformulation remains a near-term restraint because food-contact cartonboard grades cannot simply wait for the PPWR deadline before technical changes begin. The Nordic cartonboard market now faces combined pressure from recyclability requirements and the need to move away from PFAS-based barrier chemistry in coated food-contact applications. The EU-funded ZeroF project is developing safe, sustainable-by-design coating alternatives for food packaging, including cellulose fatty acid ester approaches that could replace PFAS compounds in relevant applications. Even once a workable substitute is identified, mills still need coating line adjustments, qualification testing, and customer approval before commercial rollout can scale. The pressure is more severe in liquid packaging and other sensitive food applications because barrier performance directly affects shelf life and product integrity. Smaller specialty mills are more exposed in the Nordic cartonboard market because they cannot spread reformulation and equipment costs across as many product families as larger integrated producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Folding Boxboard Anchors Share As Liquid Packaging Board Accelerates

Folding boxboard held the largest share by product grade at 37.17% in 2025, which kept it at the center of demand across food, cosmetics, and pharmaceutical secondary packs in the Nordic cartonboard market. The segment’s hold is supported by lightweighting, as producers continue to improve stiffness-to-weight performance and extend folding boxboard into uses that once leaned more heavily on solid bleached board. Solid bleached board still keeps a clear role in premium pharmaceutical packs and luxury cosmetics because those applications prioritize print quality, purity, and pack finish over cost. Metsä Board launched MetsäBoard Pro FBB Go in March 2026 as an OBA-free folding boxboard with hard sizing for frozen applications, produced at Husum in Sweden, and offered with short delivery windows across Europe.

Liquid packaging board is projected to post the fastest growth in the Nordic cartonboard market, with a CAGR of 3.19% from 2026 to 2031. That pace reflects strong demand from dairy producers and plant-based beverage brands that are redesigning cartons to increase fiber content and reduce reliance on aluminum and conventional polymers. Stora Enso launched Performa Natura Aqua in April 2026, a dispersion-coated folding boxboard for foodservice and bakery packaging that uses less plastic on the reverse side and allows faster repulping, which points to the broader direction of barrier development in the region. The food service board is also advancing as quick-service restaurants and workplace catering operators shift toward fiber-based single-material constructions that better align with national EPR and recyclability expectations.

By Packaging Format: Folding Cartons Lead While Liquid Packaging Gains Ground

Folding cartons accounted for 57.86% of the Nordic cartonboard market in 2025, making them the dominant packaging format across food retail, pharmaceutical distribution, and personal care applications. Their position remains especially firm in pharmaceutical distribution, where folding cartons continue to serve as the standard secondary pack for unit-dose, OTC, and prescription products. Sleeve and tray formats are also gaining traction in seafood, fresh produce, and convenience food because retailers want formats that work well with automated replenishment and clean shelf presentation. Huhtamäki’s collaboration with Hesburger on fiber lids eliminated nearly 41,000 kg of plastic per year from the restaurant chain’s operations, underscoring the broader shift from plastic and foam to fiber-based foodservice and adjacent packaging formats.

Liquid packaging is the fastest-growing format in the Nordic cartonboard market and is projected to expand at a CAGR of 2.95% between 2026 and 2031. Elopak’s 2025 output of 16 billion cartons, with EMEA accounting for 69% of revenue, shows the strong underlying pull for liquid board formats linked to dairy and plant-based beverages. Tetra Pak and García Carrión launched the first 1-liter aseptic carton with a paper-based barrier in December 2025, raising renewable content and providing a practical template for future long-shelf-life carton upgrades. This format is also benefiting from a wider move toward higher paperboard content and better alignment with forthcoming recycled-content rules for the remaining polymer fraction in fiber-based cartons.

By End-User Industry: Food Holds Largest Share As Pharmaceutical Packaging Grows Fastest

Food represented 39.71% of the Nordic cartonboard market share in 2025, supported by the region’s strong chilled-food culture, high packaged dairy consumption, and mature cold-chain infrastructure. Retail procurement standards in Nordic food channels often require FSC chain-of-custody and Nordic Swan Ecolabel alignment, effectively narrowing procurement to producers that can demonstrate fresh-fiber sourcing and documented compliance. Beverage packaging remains a major growth area, with oat drinks and dairy alternatives broadening the use of aseptic and chilled carton formats across regional retail channels. Elopak’s aseptic Pure-Pak Sense carton was adopted by The Green Dairy in Sweden for IKEA’s European Food Market channels, showing how plant-based beverage formats are widening cartonboard demand into new commercial routes.

Pharmaceutical and healthcare packaging is expected to record the fastest growth by end user, with a CAGR of 3.12% from 2026 to 2031 in the Nordic cartonboard market. Demand is rising because GLP-1 analogs, biologics, and specialty drugs require high-specification secondary cartons with unit-dose integrity, moisture resistance, and surfaces suitable for serialization and traceability printing. Mayr-Melnhof stated in its 2025 annual financial report that pharma and healthcare packaging had become a new growth area after its market entry in late 2022, with particular relevance to GLP-1 analog packaging. Cosmetics and toiletries remain stable, while tobacco continues to contract, and other end-user categories, such as apparel, household goods, toys, automotive, and electrical products, provide diversification without altering the broader demand pattern.

Geography Analysis

Sweden remains the production and innovation center of the Nordic cartonboard market because it combines large board capacity, integrated forest resources, and a well-established converting base. Major sites linked to Billerud, Holmen, and Stora Enso keep Sweden central to premium cartonboard exports across the region and wider European markets. Swedish procurement conditions also tend to favor certified, recyclable fiber packaging, thereby strengthening demand for PPWR-aligned board specifications across food, retail, and public-sector channels. This gives the domestic market an early-adoption role when new pack formats move from pilot stage into commercial rollouts. Sweden’s renewable electricity base supports mill competitiveness, though internal power price differences still put pressure on operations closer to southern demand centers.

Finland is the capacity frontier in the Nordic cartonboard market because Stora Enso’s BM6 consumer board line at Oulu is moving toward full operational status from 2027 and will add significant fresh-fiber supply to the regional base. Metsä Board’s 2026-2030 strategy targets an EBITDA improvement of EUR 200 million (USD 208 million) by the end of 2028 through production efficiency, cost restructuring, and portfolio expansion in consumer brand packaging. Specialized producers such as Pankaboard and MM Kotkamills add depth in kraft-look and recycled-fiber niches that sit outside standard premium FBB applications. Finland’s pharmaceutical manufacturing base also supports demand for high-quality secondary cartons in unit-dose and blister packaging.

Norway and Denmark add stable demand to the Nordic cartonboard market through food, beverage, and pharmaceutical applications, even though their production bases are smaller than those of Sweden and Finland. Elopak, headquartered in Oslo, procures large volumes of liquid packaging board for its Pure-Pak platform, and its 2025 output of 16 billion cartons shows the scale of this demand pull on regional supply. Danish consumption is supported by pharmaceutical packaging needs and a strong food and beverage retail sector that continues to rely on fiber-based secondary formats. Iceland and the smaller Nordic territories contribute less to total value, but they still add import demand for fresh-fiber cartonboard produced by Finnish and Swedish mills.

Competitive Landscape

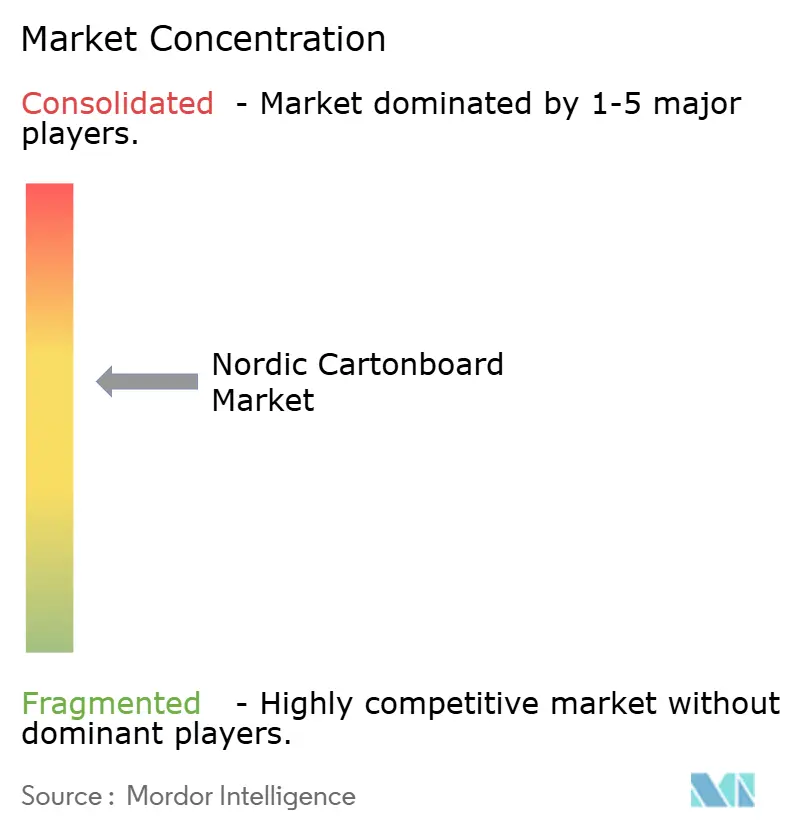

The Nordic cartonboard market is moderately concentrated at the board-producer level, while the converting base remains fragmented across foodservice, pharmaceutical, and shelf-ready specialty niches. Integrated producers have an advantage because they can combine forest and pulp linkages with stronger certification coverage and faster commercialization of new board grades. Billerud’s 2026 investor communication showed a clear focus on higher-value packaging materials and North American capacity upgrades, while its CrownBoard range continues to support differentiation in European cartonboard. Metsä Board stated that its transformation program had delivered nearly EUR 100 million (USD 104 million) in annualized EBITDA run-rate improvement by the end of Q1 2026, reflecting the broader push toward cost control and premium-grade specialization. In the Nordic cartonboard market, competitive strength now depends as much on verified recyclability and execution speed as it does on base production capacity.

A clear opening remains in PFAS-free food-contact barriers for short- to medium-term shelf-life formats because technical progress at large producers has not yet fully spread through the converter network. UPM Specialty Materials and BASF moved this area forward in May 2026 by combining barrier base papers with Joncryl HPB resin technology to support recyclable fiber-based packaging designs. Pharmaceutical cartons linked to GLP-1 and biologic therapies also offer attractive pricing because the pool of fully qualified suppliers remains limited. That combination favors companies that can offer compliance, short lead times, and stable print performance in the Nordic cartonboard market.

Competition is also being shaped by adjacent fiber innovators that may influence formats close to the cartonboard value chain. The European Investment Bank extended a EUR 20 million (USD 21.6 million) loan to PulPac in 2025 to support the development and commercialization of dry molded fiber as an alternative to single-use plastics. PulPac then presented fiber-based plastic-like bottle caps at Interpack 2026, showing that fiber innovation is starting to reach closures and nearby components that were long held by plastics. At the same time, PPWR-linked documentation, better process control, and shorter-run digital conversion are shifting procurement toward suppliers that can prove performance as clearly as they can deliver output

Nordic Cartonboard Industry Leaders

Stora Enso Oyj

Metsa Board Corporation

Billerud Aktiebolag

Holmen AB

Mayr-Melnhof Karton AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Stora Enso launched Performa Natura Aqua, a dispersion-coated folding boxboard (GC2 cartonboard) for foodservice and bakery packaging, available in 195-320 g/m² grammages. The board's reverse-side Aqua coating uses less plastic, enables faster repulping, and increases fiber recovery in recycling streams, directly supporting PPWR design-for-recycling compliance for food-contact carton converters.

- March 2026: Metsä Board launched MetsäBoard Pro FBB Go, an OBA-free folding boxboard for food and pharmaceutical packaging produced at the Husum mill in Sweden. The product is available via the FastTrack Service and the ExpressTrack Service for European customers, reducing exposure to supply chain lead times.

- March 2026: Metsä Board disclosed its new "Lead the Pack" strategy for 2026-2030, targeting EUR 200 million (approximately USD 208 million) in EBITDA improvement by end of 2028 through cost restructuring and commercial growth in consumer brand packaging. By end of Q1 2026, the transformation programme had already delivered approximately EUR 100 million (USD 104 million) in annual run-rate improvement.

- December 2025: Tetra Pak and García Carrión launched the first 1-liter aseptic carton with a paper-based barrier (Tetra Brik Aseptic 1000 Edge), increasing renewable content to 90% when combined with plant-based polymers and delivering a carbon footprint reduction of up to 50% as verified by the Carbon Trust. The technology is directly relevant to Nordic dairy and juice producers considering long-shelf-life carton upgrades.

Nordic Cartonboard Market Report Scope

The Nordic Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The Nordic Cartonboard Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and Other Packaging Formats), and End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics and Toiletries, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

Key Questions Answered in the Report

What is the size of the Nordic cartonboard market?

The Nordic cartonboard market was valued at USD 0.96 billion in 2025, rises to USD 0.98 billion in 2026, and is forecast to reach USD 1.10 billion by 2031 at a 2.34% CAGR.

What is driving cartonboard demand across Nordic packaging applications?

Demand is being supported by PPWR-led recyclability rules, brand migration from plastic to fiber, stronger demand for premium fresh-fiber grades, and expanding use in liquid food and pharmaceutical packs.

Which product grades are leading and growing fastest in the region?

Folding boxboard led with a 37.17% share in 2025, while liquid packaging board is projected to grow the fastest at a 3.19% CAGR through 2031.

Why is pharmaceutical packaging becoming more important for Nordic suppliers?

Pharmaceutical and healthcare packaging is the fastest-growing end-user segment at a 3.12% CAGR, supported by demand for cartons used with GLP-1 analogues, biologics, and serialization-compliant secondary packs.

Which packaging format holds the strongest position in Nordic cartonboard use?

Folding cartons led with 57.86% of market value in 2025 because they remain the standard format across food retail, pharmaceutical distribution, and a wide range of personal care applications.

Which countries shape supply and demand most strongly across the Nordics?

Sweden leads in production and innovation, Finland is adding major fresh-fiber capacity, and Norway and Denmark remain important demand centers for liquid packaging, food, and pharmaceutical carton applications.

Page last updated on: