North America Cartonboard Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

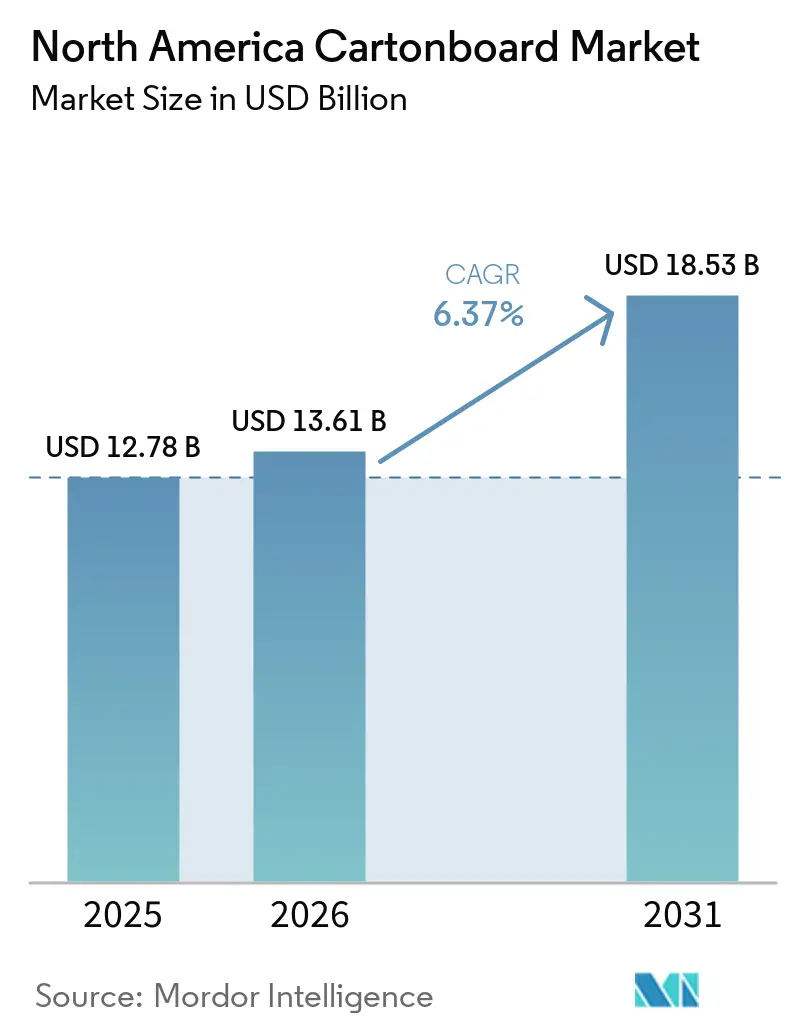

| Base Year Market Size (2025) | USD 12.78 Billion |

| Market Size (2026) | USD 13.61 Billion |

| Market Size (2031) | USD 18.53 Billion |

| Growth Rate (2026 - 2031) | 6.37% CAGR |

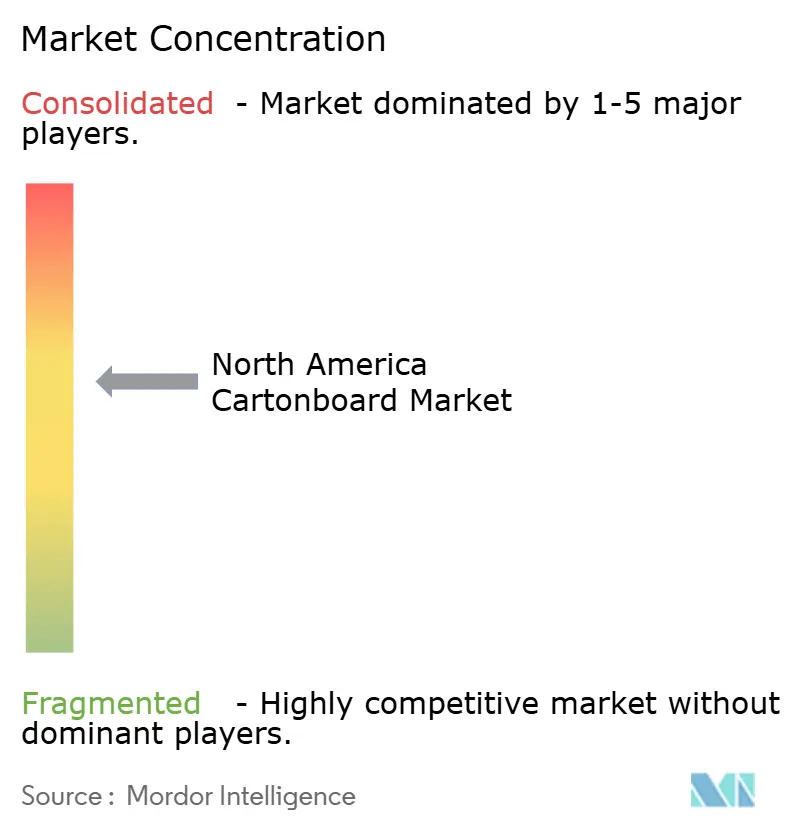

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Cartonboard Market Analysis by Mordor Intelligence

The North America cartonboard market size is projected to expand from USD 12.78 billion in 2025 and USD 13.61 billion in 2026 to USD 18.53 billion by 2031, registering a CAGR of 6.37% between 2026 to 2031. The North America cartonboard market is being lifted by tighter rules on plastic packaging, steady demand from quick-service restaurants shifting to certified compostable board formats, and stronger use of premium pharmaceutical cartons under DSCSA requirements. A key change in the North America cartonboard market is the move away from polyethylene-extruded cup stock toward aqueous and bio-based barriers, as that shift often requires heavier-caliper board for the same filled unit. The North America cartonboard market is also supported by the region’s strong mill base, converting infrastructure, and deep packaged goods supply chains, which help larger producers defend volumes and pricing even as product specifications become more demanding. Margin recovery remains uneven because pulp, recovered fiber, energy, and specialty coating costs remained volatile through 2025 and into early 2026, prompting some producers to rationalize and reset portfolios. Competitive conditions in the North America cartonboard market remain moderate to high, and the clearest opportunities are centered on PFAS-free barriers, PE-free foodservice board, and higher-value cartons for healthcare, premium food, and retail-ready packaging.

Key Report Takeaways

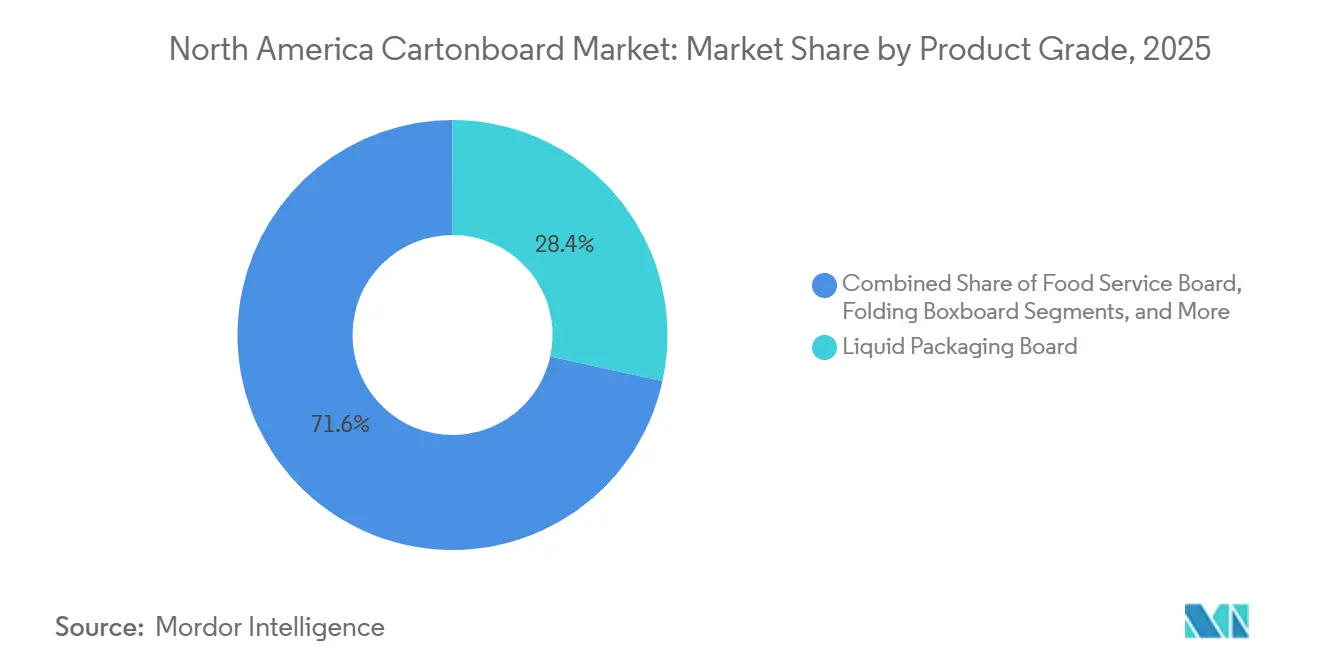

- By product grade, liquid packaging board captured 28.44% of the North America cartonboard market share in 2025.

- By packaging format, the North America cartonboard market size for the liquid packaging segment is forecast to advance at a 7.82% CAGR through 2031.

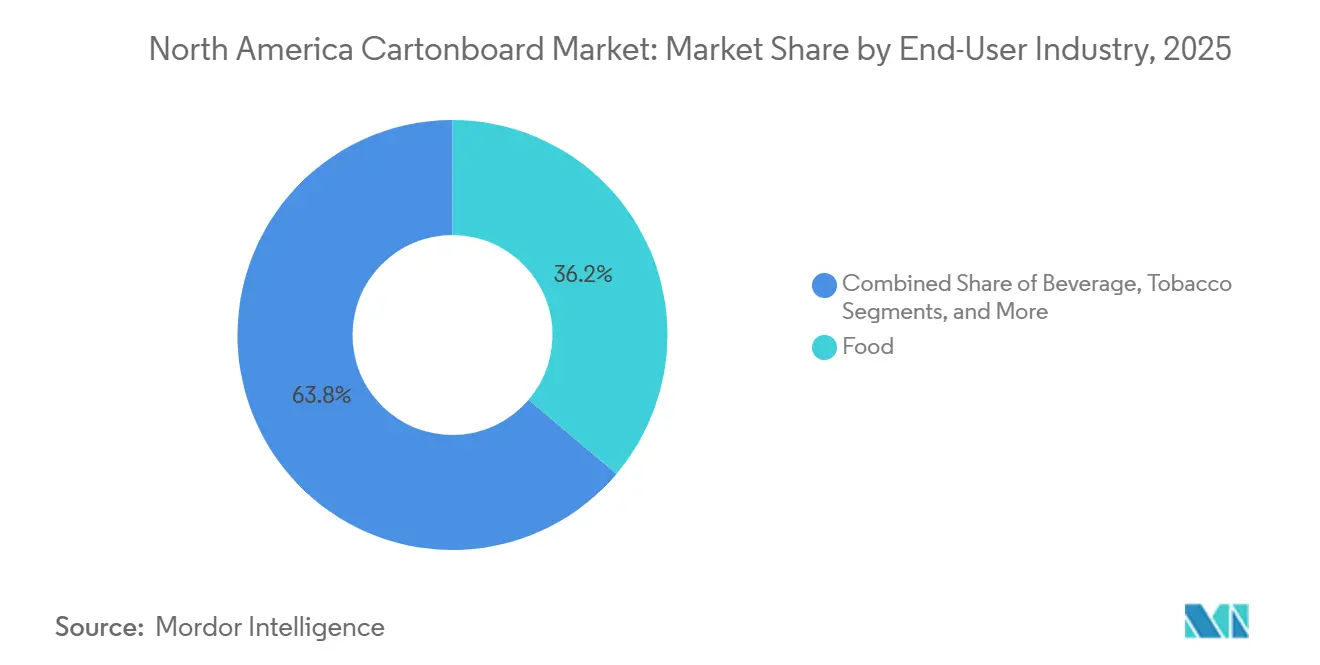

- By end-user industry, food captured 36.19% of the North America cartonboard market share in 2025.

- By geography, the North America cartonboard market size for the Mexico segment is forecast to advance at a 7.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainable Substitution From Plastic Packaging | +1.8% | United States and Canada, with acceleration in Mexico | Long term (≥ 4 years) |

| Growth In Packaged Food And Beverage Demand | +1.5% | Global, with largest footprint in US Midwest and Southeast grocery corridors | Medium term (2-4 years) |

| E-Commerce And Club Retail Secondary Packaging Demand | +0.9% | United States, Mexico nearshoring clusters | Medium term (2-4 years) |

| PFAS-Free And PE-Free Barrier Board Innovation | +0.6% | United States, Canada | Short term (≤ 2 years) |

| Premium Print And Shelf Appeal Demand In Beauty And Personal Care | +0.4% | United States, Canada | Medium term (2-4 years) |

| Pharmaceutical Serialization And Biologics Carton Complexity | +0.3% | United States, Canada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sustainable Substitution From Plastic Packaging

Sustainable substitution has become one of the clearest long-run supports for the North America cartonboard market because packaging changes are now being shaped by compliance as much as by brand preference. State and provincial packaging rules have pushed brand owners to reassess both primary and secondary formats, thereby widening the role of cartonboard in foodservice, consumer goods, and retail display applications. The shift is not limited to replacing one package with another, because many conversions require specific grades, such as SBS and coated unbleached kraft, which increase both carton counts and basis-weight requirements per unit. The FDA’s confirmation in January 2025 that all 35 food contact notifications for PFAS-containing grease-proofing agents in paper and paperboard food packaging were no longer effective accelerated new specification work across the United States.[1]U.S. Food and Drug Administration, “Market Phase-Out of Grease-Proofing Substances Containing PFAS,” U.S. Food and Drug Administration, fda.gov That change also strengthened demand for PFAS-free barrier board in food-contact applications, where buyers now need validated alternatives rather than transitional materials.[2]U.S. Food and Drug Administration, “Questions and Answers on PFAS in Food,” U.S. Food and Drug Administration, fda.gov The North America cartonboard market also benefits when plastic-to-paper conversions in cup stock require heavier board to preserve strength after the polymer layer is removed, thereby raising tonnage demand beyond simple unit substitution.

Growth In Packaged Food And Beverage Demand

The North America cartonboard market continues to draw stable support from packaged food and beverage demand because cartonboard remains deeply embedded in grocery, frozen, chilled, and foodservice packaging systems. Food accounted for 36.19% of revenue in 2025, underscoring the material's widespread use across branded shelf-ready formats where visual presentation and transport performance matter simultaneously. The National Restaurant Association stated that enduring demand would continue to shape restaurant activity in 2026, which supports ongoing packaging trials and replenishment needs across branded foodservice chains.[3]National Restaurant Association, “Persistent Cost Increases and Enduring Demand Will Shape the Restaurant Industry in 2026,” National Restaurant Association, restaurant.org Clearwater Paper said in its first-quarter 2026 commentary that folding carton demand remained solid and that foodservice cup and plate grades showed strength, which points to sustained pull for food-contact paperboard applications. That demand is important for the North America cartonboard market because carry-out containers, cup stock, and laminated trays are tied to high-frequency consumption patterns that are difficult for alternatives to displace quickly. It also gives board producers a steadier path to multi-year supply agreements, since food and beverage pack formats often remain fixed for long production runs once brand owners complete their line qualification work.

E-Commerce And Club Retail Secondary Packaging Demand

The North America cartonboard market is also being shaped by fulfillment and club-retail requirements that favor board formats able to deliver both branded graphics and stronger structural performance. Direct-to-consumer fulfillment has increased the need for retail-ready packs and secondary formats that can move through automated systems without losing shelf appeal or product protection. Club-retail sleeves and multi-item cases use thicker board structures than single-unit retail packs, which supports tonnage growth even as shipment volumes rise more slowly. This matters because the North America cartonboard market gains not only from more packages, but also from heavier pack specifications that must withstand sorting, stacking, and higher distribution stress. The same pattern is visible in e-commerce-focused converting investments, where producers are adding right-sizing capability and digital printing to serve shorter runs and faster product cycles. Cascades’ updated first-quarter 2026 commentary showed cautious packaging demand against restrained consumer spending, yet the company still pointed to cost and volume conditions that suggest medium-term packaging infrastructure shifts remain intact across North America.

PFAS-Free And PE-Free Barrier Board Innovation

Barrier innovation is moving from a product development theme to a commercial requirement in the North America cartonboard market, especially in foodservice and food-contact uses. The FDA said in February 2024 that greaseproofing agents containing PFAS had been withdrawn from the United States market, and the January 2025 Federal Register notice formalized the removal of all related food-contact notifications. With the June 30, 2025, exhaustion deadline for legacy PFAS-containing food packaging paper already passed, new carton specifications now depend on replacement systems such as water-based and bio-based barriers. That shift has commercial importance because PE-free barrier board usually commands a higher price than conventional PE-coated stock, creating a value opportunity for mills that have already completed finished-product testing and regulatory review. It also favors producers that can meet food-contact performance rules while keeping board stiffness, sealability, and print quality within line requirements. The North America cartonboard market, therefore, gains not only from regulation itself but also from the premiumization that follows when converters move to validated barrier platforms with fewer legacy inputs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Fiber, Energy, And Chemical Input Costs | -0.8% | North America, with acute exposure in US Southeast and Midwest kraft mill clusters | Medium term (2-4 years) |

| Competition From Flexible Packaging And Alternative Formats | -0.7% | United States and Canada, particularly in dry food and confectionery categories | Long term (≥ 4 years) |

| State-Level PFAS Compliance Retrofits And Qualification Cycles | -0.3% | United States, Canada | Short term (≤ 2 years) |

| Canadian Cartonboard Capacity Tightness And Import Dependence | -0.2% | Canada, with spillover into the US Northeast | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Fiber, Energy, And Chemical Input Costs

Input-cost volatility remains the main earnings constraint across the North America cartonboard market because raw material and utility movements do not reset in line with contract pricing cycles. Smurfit Westrock reported a weather-related EBITDA impact of USD 65 million in the first quarter of 2026, largely in North America, while also pursuing a second wave of price increases to offset rising cost pressure.[4]Smurfit Westrock, “Smurfit Westrock Reports First Quarter 2026 Results,” Smurfit Westrock, smurfitwestrock.com Graphic Packaging reported adjusted EBITDA of USD 232 million in the first quarter of 2026, down from USD 365 million a year earlier, and said input and other cost inflation accounted for USD 37 million of that decline. Cascades also pointed to continued upward pressure on input costs in its first-quarter 2026 results, indicating that recycled fiber networks are exposed to the same broad cost pressures even when mill structures differ. These pressures matter in the North America cartonboard market because they widen the advantage of vertically integrated producers with captive pulp and internal conversion assets. They also accelerate consolidation because smaller mills and independent operators have less room to absorb lagged pricing or sudden cost spikes in energy, recovered fiber, and specialty coatings.

Competition From Flexible Packaging And Alternative Formats

Flexible packaging remains a clear restraint on the North America cartonboard market in dry food, snack, confectionery, and single-serve categories, where weight efficiency and barrier performance are highly valued. Brand owners still view pouches and film-based alternatives as commercially attractive because they lower secondary packaging weight and fit installed filling equipment that companies may be reluctant to replace. That pressure is strongest in ambient food categories where stand-up pouch formats have gained wider shelf acceptance and now compete more directly with rigid cartons. The North America cartonboard market has responded with lightweighting and specification redesign rather than simple price competition, which suggests the threat is structural rather than temporary. Clearwater Paper’s March 2026 Velora launch reflected that response, as the new lightweight folding carton paperboard was positioned to improve yield and reduce material use in everyday packaging applications. Even so, flexible alternatives continue to limit the speed at which cartonboard can expand in categories where barrier needs, line economics, and shipping efficiency still favor non-board formats.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Liquid Packaging Board Holds The Scale Lead While Food Service Board Lifts Growth

Liquid Packaging Board held 28.44% of the North America cartonboard market share in 2025, making it the largest product grade in the regional mix. Its position rests on highly consolidated aseptic and gable-top supply chains that support dairy, plant-based beverage, juice, and broth packaging, where filling-line integration tends to lock in long procurement cycles. In the North America cartonboard market, this gives LPB a stable demand base that is less exposed to sudden format changes than many discretionary consumer packaging uses. Folding Boxboard still serves premium consumer goods where caliper consistency, high whiteness, and strong print results remain central to brand presentation. Solid Unbleached Board and White-Lined Chipboard continue to serve cost-sensitive beverage multipacks and general retail packaging, although sustainability requirements have heightened scrutiny of grade selection and fiber credentials.

The North America cartonboard industry also shows a clear split between legacy scale grades and newer growth grades tied to food-contact conversion. The Food Service Board is projected to expand at a 7.14% CAGR through 2031, driven by plastic bans, demand for compostable formats, and the steady rise in off-premise consumption. Clearwater Paper said in its first-quarter 2026 commentary that extruded products, including cup and polycoated folding carton grades, were sold out, signaling tight supply in food-contact applications linked to reformulation and conversion activity. That condition matters because the move toward PFAS-free and PE-free solutions does not just change chemistry; it often changes caliper, conversion rates, and the value captured per ton. The North America cartonboard industry is therefore seeing product architecture shift toward grades that deliver barrier performance, regulatory compliance, and stronger yield economics in a single offer. The launch of lightweight mid-market SBS alternatives also points to a more selective buying pattern, in which converters are comparing usable output and print performance rather than relying solely on headline board prices.

By Packaging Format: Folding Cartons Stay In Front While Foodservice Containers Expand Faster

Folding cartons accounted for 52.17% of the North America cartonboard market in 2025, making them the leading packaging format across the region. Their lead reflects broad applicability across cereals, consumer staples, over-the-counter healthcare, and branded retail packaging, where shelf presence and pack efficiency must work together. That scale advantage remains important in the North America cartonboard market because converters and brand owners already have well-established tooling, printing, and distribution systems built around the format. Liquid packaging formats also kept a distinct role, especially in UHT dairy, plant-based beverages, juice, and broth, where aseptic systems still provide an ambient shelf-life advantage that has been difficult to displace. Sleeve and tray formats gained greater relevance in club retail and e-commerce, where both structural rigidity and printable surface area matter.

In North America, the cartonboard industry is witnessing a rapid surge in liquid packaging, outpacing other major formats. Projections indicate that cartons for dairy products, juices, plant-based beverages, and ready-to-drink items will grow at a robust 7.82% CAGR from 2026 to 2031. This uptick is largely driven by an escalating demand for shelf-stable beverages, a heightened consumption of convenient on-the-go products, and a mandated pivot away from rigid plastic packaging. Such plastics are increasingly scrutinized under the lenses of recycling and sustainability. Furthermore, liquid packaging cartons are undergoing redesigns, adhering to stricter material and barrier-performance standards. These heightened specifications often place added demands on board grades. Consequently, the North American cartonboard market is witnessing a pronounced need for liquid packaging boards. These boards must adeptly balance stiffness, printability, and moisture and oxygen barrier performance, all while ensuring compliance with regulatory standards.

By End-User Industry: Food Keeps The Broadest Base While Healthcare Raises Specification Intensity

Food accounted for 36.19% of total revenue in 2025, making it the largest end-user in the North America cartonboard market. That position reflects the wide spread of ambient, chilled, and frozen carton SKUs across grocery supply chains, where branded packs and retail-ready presentation remain central to category competition. Food demand also tends to stay durable because board formats are often embedded in long design and approval cycles, which slows substitution once a format is established. Beverage uses continue to rely on Liquid Packaging Board and folding carton multipacks, where caliper control and print registration are important for high-speed filling and display consistency. Cosmetics and toiletries also sustain demand for premium grades, as visual finish and structural precision continue to shape launch quality and consumer trial in those channels.

The North America cartonboard industry is seeing the fastest end-user growth in pharmaceutical and healthcare applications, with the segment projected to rise at a 7.16% CAGR through 2031. DSCSA-related serialization requirements have heightened the need for cartons that can accommodate precise data printing without bleed, which has raised material and ink system standards across pharmaceutical packaging. In the North America cartonboard market, this favors premium SBS and similar substrates that can hold small-format codes, lot information, and expiration details with reliable scan quality. The use of biologics and specialty therapies adds to that pressure because these products often demand tighter traceability, stronger product protection, and more complex packaging execution. Tobacco continues to weaken as a source of carton demand across North America, while the broader “other” category remains linked to general economic activity, export manufacturing, and new factory investment. The North America cartonboard industry, therefore, has a growth pattern in which food preserves volume stability while healthcare lifts the quality threshold and value per converted unit.

Geography Analysis

The United States accounted for 78.54% of the North America cartonboard market share in 2025, making it the clear anchor for regional supply, demand, and investment. The country’s lead rests on integrated mill infrastructure, broad converting capacity, and the scale of packaged consumer goods, food-contact, and pharmaceutical production. In the North America cartonboard market, United States demand is weighted toward premium grades for food, healthcare, and beauty applications where print quality, surface consistency, and certified fiber programs remain important. Graphic Packaging reported first-quarter 2026 net sales of USD 2,156 million, up 2% year over year, with volumes up 1%, indicating resilient branded packaging demand despite cost inflation and macro pressures. California’s packaging policy direction also continues to influence carton specification decisions well ahead of its long-term compliance horizon, extending the planning window for mills and converters focused on plastic substitution.

Canada remained the second-largest national market, but its position was shaped by tighter domestic converting capacity and greater exposure to cross-border freight and currency effects. Smurfit Westrock announced in February 2026 that it would permanently close a paper machine at La Tuque, Quebec, removing 127,000 tons of annual SBS capacity from the system and tightening local supply conditions. The same country also faces growing demand for premium food and pharmaceutical packaging, underscoring the importance of reliable bleached board supply. Cascades invested CAD 6.9 million (USD 5 million) in March 2026 at its Papier Kingsey Falls uncoated recycled boxboard plant in Quebec to improve surface finish and print quality for food packaging applications.

Mexico is the fastest-growing country in the North America cartonboard market, with a projected CAGR of 7.21% from 2026 to 2031. Nearshoring-led manufacturing expansion, stronger packaged food consumption, and rising pressure to replace plastic packaging are all supporting demand. Manufacturing foreign direct investment in Mexico reached USD 40.8 billion in 2025, with manufacturing accounting for 36% of committed capital, supporting ongoing demand for retail-ready and export-spec carton packaging. USMCA trade alignment is also moving Mexican carton specifications closer to United States retail and performance standards, which should support more consistent quality requirements across export-oriented supply chains.

Competitive Landscape

The North America cartonboard market is moderately consolidated at the mill level, with a small group of vertically integrated producers controlling much of primary board capacity while a broader field of independent converters competes downstream. This structure gives large producers pricing and supply advantages, especially when raw material costs are volatile or when customers need validated food-contact and pharmaceutical grades. Graphic Packaging entered 2026 with a stronger focus on cash flow generation and deleveraging following its 90-day business review, while continuing to use innovation as a core differentiator through patent activity and packaging development. Smurfit Westrock continued to signal scale ambitions through its medium-term plan, which targeted adjusted EBITDA of approximately USD 7 billion by 2030 and pointed to a sustained investment view for packaging infrastructure. Clearwater Paper’s transformation into a focused paperboard supplier after the divestiture of its tissue business also sharpened its role as a leading independent SBS source for converters that prefer not to buy from integrated rivals.

Strategic moves in the North America cartonboard market have centered on capacity quality, portfolio simplification, and grade innovation rather than on broad new-build expansion alone. Graphic Packaging reduced its 2026 capital spending guidance to approximately USD 450 million from USD 922 million in 2025, signaling a shift away from heavy capacity spending toward productivity, margin discipline, and free cash flow. Smurfit Westrock also continued to reshape its asset base, using rationalization and modernization to protect competitiveness in board and converting operations. Clearwater Paper’s Velora launch added a lightweight option aimed at converters seeking domestic alternatives to imported folding boxboard, underscoring how competition is increasingly tied to yield and format economics as much as to nominal price.

White-space opportunities in the North America cartonboard market are concentrated in PFAS-free and PE-free foodservice barriers, premium pharmaceutical cartons, and lightweight grades that can replace imported board at workable economics. Smaller specialty converters such as Diamond Packaging, Keystone Folding Box Co., and American Carton Company continue to defend niche positions through digital printing and short-run capability for premium beauty and healthcare customers. That part of the market is less exposed to pure scale competition because it depends on customization, print precision, and faster qualification cycles. Certification programs such as FSC and SFI, along with traceability requirements in pharmaceutical packaging, are also raising entry barriers and helping established suppliers protect premium accounts.

North America Cartonboard Industry Leaders

Graphic Packaging Holding Company

Smurfit Westrock plc

International Paper Company

Georgia-Pacific LLC

Packaging Corporation of America

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Graphic Packaging reported Q1 2026 net sales of USD 2,156 million, up 2% year over year, with volumes rising 1%; the company filed 13 new patents during the quarter, adding to a portfolio of approximately 3,100 patents, and received two WorldStar 2026 Awards and 8 awards at the 2026 PAC Global Awards for sustainable packaging solutions.

- March 2026: Clearwater Paper Corporation launched Velora, a new lightweight folding carton paperboard engineered to deliver dependable performance and higher yield for everyday packaging without requiring premium SBS grades. The product carries SFI fiber certification and FDA 21 CFR food-contact compliance, and is targeted at converters seeking an alternative to imported folding boxboard, with commercial production at Clearwater's US mills.

- March 2026: Cascades invested CAD 6.9 million (USD 5 million) in its Papier Kingsey Falls uncoated recycled boxboard plant in Quebec, improving sheet surface finish and printing quality to better meet food packaging industry requirements.

- February 2026: Smurfit Westrock released its updated medium-term plan through 2030, targeting adjusted EBITDA of approximately USD 7 billion, market growth of 1.6% in North America and 2.0% in South America, and USD 14 billion in cumulative discretionary free cash flow, signaling a sustained multi-year investment cycle in North American packaging infrastructure.

North America Cartonboard Market Report Scope

The North America Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging in the United States, Canada, and Mexico. Key product grades in the market include Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The North America Cartonboard Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, Other Packaging Formats), End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, Other End-User Industries), and Geography (United States, Canada, Mexico). Market Forecasts are in Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| United States |

| Canada |

| Mexico |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America cartonboard market in 2026, and what is the outlook through 2031?

The North America cartonboard market stood at USD 13.61 billion in 2026 and is projected to reach USD 18.53 billion by 2031 at a 6.37% CAGR.

Which country leads regional demand for cartonboard?

The United States led the region with a 78.54% revenue share in 2025, supported by its integrated mill base, converting infrastructure, and large packaged goods sector.

Which product grade leads the North America cartonboard market?

Liquid Packaging Board was the largest product grade in 2025 with a 28.44% share, reflecting the strength of aseptic and gable-top beverage carton systems.

Which packaging format is growing the fastest in North America?

Foodservice containers are projected to grow the fastest at a 7.82% CAGR through 2031 as off-premise consumption rises and plastic bans push substitution toward board-based formats.

Why is pharmaceutical packaging becoming more important for cartonboard suppliers?

Pharmaceutical and healthcare applications are projected to grow at a 7.16% CAGR through 2031 because DSCSA-related serialization and biologics packaging needs are raising substrate and print-quality requirements.

What is the biggest risk to profitability for producers in this space?

The main risk is input-cost volatility across pulp, recovered fiber, energy, and specialty chemicals, which has already pressured margins and contributed to rationalization moves in 2025 and 2026.

Page last updated on: