Australia Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

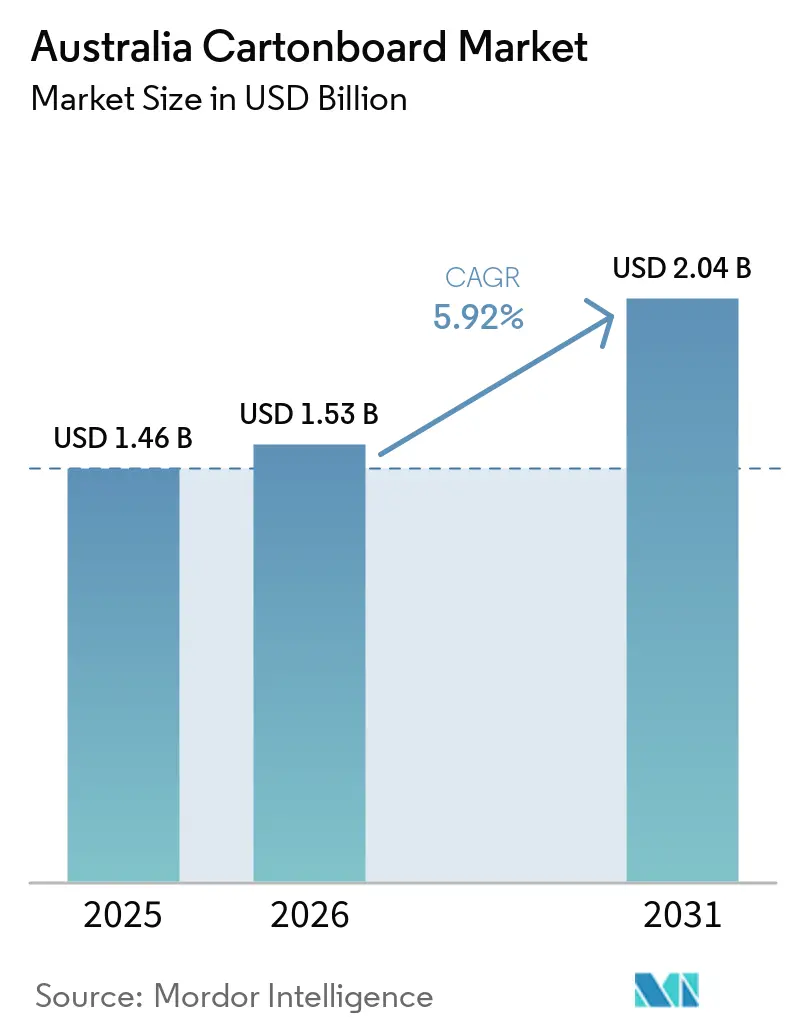

| Base Year Market Size (2025) | USD 1.46 Billion |

| Market Size (2026) | USD 1.53 Billion |

| Market Size (2031) | USD 2.04 Billion |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

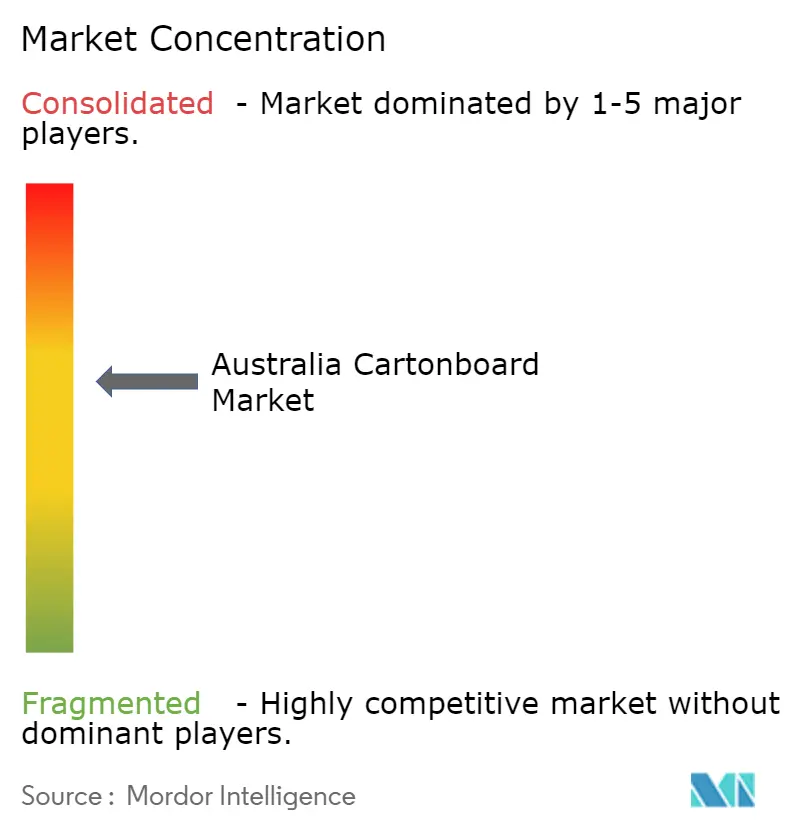

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Cartonboard Market Analysis by Mordor Intelligence

The Australia cartonboard market size was valued at USD 1.46 billion in 2025 and is forecast to reach USD 2.04 billion by 2031, expanding at a CAGR of 5.92% over 2026-2031. State-led plastic restrictions are shaping the growth path, the shift away from PFAS in food-contact packaging, and stronger compliance needs in pharmaceutical cartons, which are lifting demand across a wide range of converted board formats. APCO's 2025 recyclability baseline has also made cartonboard more important in packaging decisions, as brand owners now need formats that can meet compliance, recovery, and reporting requirements simultaneously. The lack of any domestic coated cartonboard mill keeps the Australia cartonboard market exposed to imported board availability, freight swings, and currency pressure, but it also pushes converters to compete on sourcing discipline, design quality, and faster qualification cycles. Retail shelf-ready requirements from major grocery chains are reinforcing the move toward higher-specification cartons that support clean presentation, automated scanning, and smoother in-store handling. As a result, the Australia cartonboard market is growing through a mix of regulation, retailer standards, and value-added converting rather than through simple volume expansion alone.

Key Report Takeaways

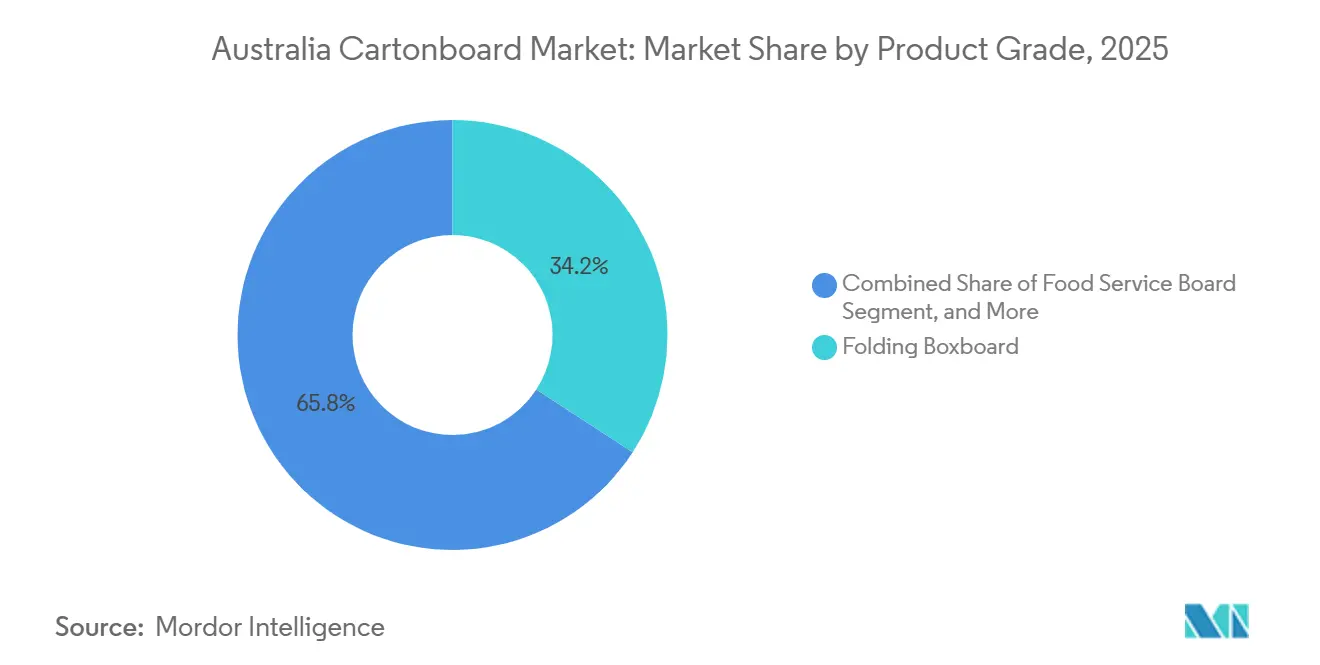

- By product grade, folding boxboard captured 34.18% of the Australia cartonboard market share in 2025.

- By packaging format, the Australia cartonboard market size for the Liquid Packaging segment is forecast to advance at a 6.84% CAGR through 2031.

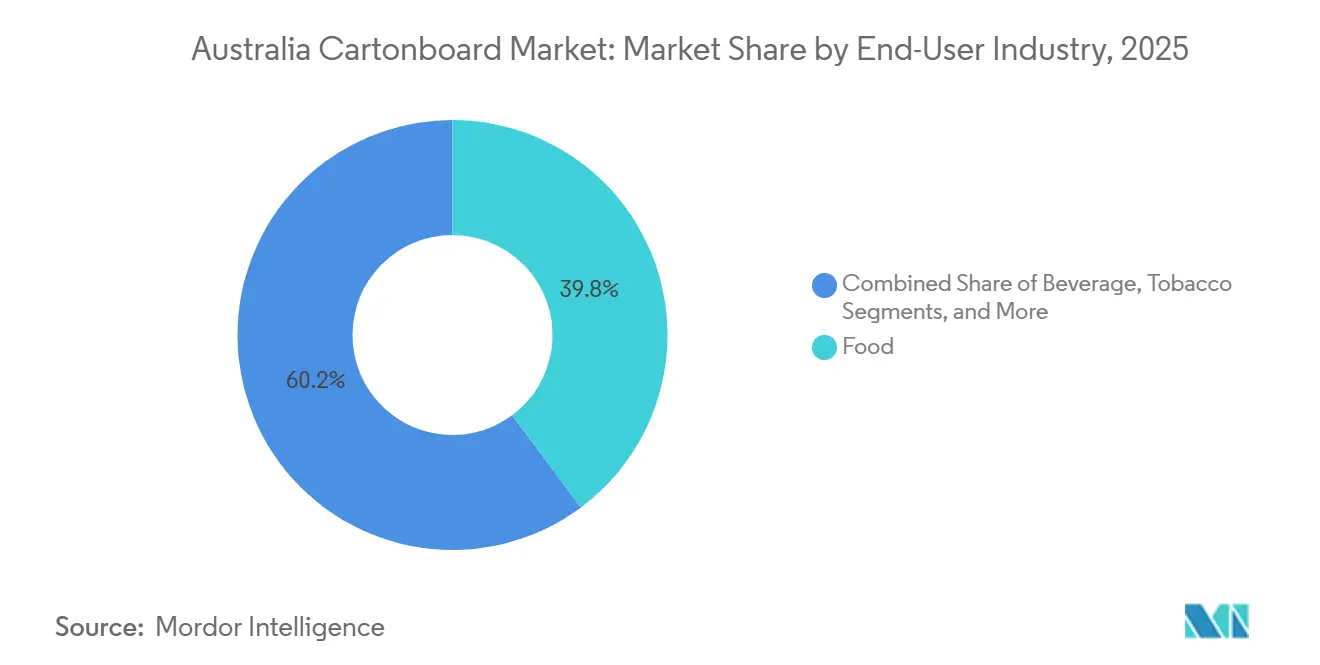

- By end-user industry, food captured 39.81% of the Australia cartonboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic-To-Paper Substitution In Foodservice And Retail Packaging | +1.8% | National, with regulatory acceleration in NSW, Victoria, WA, and ACT | Medium term (2-4 years) |

| Food Retail Volume Expansion Supporting Shelf-Ready Cartons | +1.2% | National, strongest pull in NSW and Victoria supermarket networks | Medium term (2-4 years) |

| PFAS-Free Barrier Migration Creating New Fibre Conversion Demand | +0.9% | National, with early commercial adoption in QLD food-service hubs | Short term (≤ 2 years) |

| Pharmaceutical Serialization And Tamper-Evident Packaging Requirements | +0.7% | National, concentrated in NSW and Victoria pharmaceutical manufacturing clusters | Medium term (2-4 years) |

| Beverage-Carton Recycling Infrastructure Expansion | +0.6% | National, strongest in NSW and Victoria | Long term (≥ 4 years) |

| Premiumization In Beauty, Wellness, And Functional Food Cartons | +0.5% | National, with premium brand uptake concentrated in urban NSW and Victoria | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Plastic-To-Paper Substitution In Foodservice And Retail Packaging

Australia's staggered plastic phase-out schedule has created a rolling conversion pipeline for the Australian cartonboard market, as each state has moved at a different pace, providing converters with a steady stream of replacement work rather than a single short spike in demand. Western Australia banned molded expanded plastic packaging from July 1, 2025, which immediately improved the case for grease-resistant board in cups, trays, clamshells, and other everyday takeaway formats.[1]Western Australian Government, “Plastic Free July Marked with Next Stage of Plan for Plastics Ban,” Government of Western Australia, wa.gov.au New South Wales extended that direction when NSW Plastics Plan 2.0, released in November 2025, set out additional phase-outs for bread tags, pizza savers, plastic bags with handles, condiment containers, and produce stickers through 2027.[2]NSW Environment Protection Authority, “NSW Plastics Plan 2.0,” NSW Government, epa.nsw.gov.au Each plastic-to-paper switch often creates multiple carton specifications because operators must serve different portion sizes, temperature conditions, and merchandising formats, thereby increasing the number of stock-keeping units a converter must manage. That pattern favors larger converters with digital workflows, finishing flexibility, and faster design approval cycles, as they can handle short runs and a wider range of formats without the same level of disruption. In effect, substitution is not only increasing board demand but also changing the cost and service expectations that shape competition in the Australian cartonboard market.

Food Retail Volume Expansion Supporting Shelf-Ready Cartons

Food retail remains a strong demand engine for the Australian cartonboard market because the two major grocery chains continue to push suppliers toward packs that move directly from transport to shelf presentation with minimal store handling. Woolworths Group launched more than 350 new Own and Exclusive Brand products in Australia during fiscal 2025 and recorded 5.0% own-brand sales growth, widening the flow of new carton specifications through the supply chain.[3]Woolworths Group, “Woolworths Group Annual Report 2025,” Woolworths Group Ltd, woolworthsgroup.com.au Shelf-ready packaging requires clean tear lines, consistent dimensions, strong print registration, and machine-readable bar codes, so converters are being asked to supply cartons that work equally well in automated distribution centers and on crowded retail shelves. This shift also supports better board quality because retail-ready cartons usually require greater stiffness and cleaner surfaces than basic transit packs, thereby improving the commercial position of higher-grade converted board. APCO's 2025 packaging framework reinforced this trend because recyclability and packaging performance now sit closer together in customer decision-making. As a result, the Australian cartonboard market is benefiting from food retail growth not only through volume, but also through specification upgrades that raise conversion value per job.

PFAS-Free Barrier Migration Creating New Fibre Conversion Demand

The 2025 shift away from PFAS in food-contact packaging has prompted a broad substrate review across the Australian cartonboard market, as converters can no longer rely on older barrier systems for grease, moisture, and oil resistance in many applications.[4]Australian Packaging Covenant Organisation, “Action Plan to Phase Out PFAS in Fibre-Based Food Contact Packaging,” APCO, packagingcovenant.org.au Food service board, frozen-food cartons, and fresh-produce tray formats have all required new qualification work because brand owners need coatings and barriers that meet food-contact performance requirements without introducing new compliance risk. These requalification cycles can run for many months on a single stock-keeping unit, especially when brand owners want performance testing, migration review, and line trials before approving new material. APCO also brought PFAS reporting into sharper focus, shifting accountability beyond converters and placing greater pressure on brand owners to select documented, traceable, and pre-cleared substrates. That dynamic is favoring premium folding boxboard and solid bleached board grades because buyers are willing to pay for certainty when the cost of a failed qualification can include launch delays and pack redesign. The outcome is a forced upgrade cycle that supports the Australian cartonboard market, even as it adds complexity to sourcing and technical approvals.

Pharmaceutical Serialization And Tamper-Evident Packaging Requirements

Pharmaceutical packaging is becoming an increasingly important growth segment for the Australian cartonboard market, as regulatory compliance now affects carton design, print layout, and finishing details, rather than only label content. TGO 106 made GS1 DataMatrix encoding mandatory for serialized prescription medicines supplied in Australia, and the July 1, 2026, start of mandatory Unique Device Identification labeling for most medical devices extends that compliance burden into another regulated product group. Each secondary carton must now carry machine-readable and human-readable data, including product identifiers, batch numbers, expiry information, and serial details, which is pushing print zones and carton dimensions toward more standardized layouts. Tamper-evident features such as tear bands and perforated seals also depend on the board substrate itself, so stiffness, grain direction, and converting precision now matter more than they did in less regulated packaging work. Many pharmaceutical converters have already absorbed waves of redesign work as brand owners move older packs into full compliance and seek to avoid supply interruptions in prescription categories. This is raising the value of regulated carton work inside the Australia cartonboard market because converters that can manage validation, print quality, and repeat accuracy are better placed to retain long-term customer contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Full Import Dependence For Coated Cartonboard Grades | -1.5% | National, with exposure concentrated at Port of Melbourne and Port Botany, NSW | Long term (≥ 4 years) |

| Energy, Freight, And Port-Related Cost Volatility | -0.9% | National, most acute at Sydney and Melbourne container terminals | Short term (≤ 2 years) |

| Paper And Paperboard Recovery Gap Versus Recycling Potential | -0.7% | National, with widest recovery shortfall in regional and remote areas | Medium term (2-4 years) |

| Food-Contact Coating Reform And Compliance Cost Inflation | -0.6% | National, with strong compliance influence from AICIS and APCO frameworks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Full Import Dependence For Coated Cartonboard Grades

Full reliance on imported coated cartonboard remains the biggest structural restraint for the Australian cartonboard market, as converters cannot fall back on domestic mill supply when international freight, currency, or port conditions turn unfavorable. This dependence affects folding boxboard, solid bleached board, and liquid packaging board alike, meaning several of the most important growth grades share the same external supply risk. A disruption in one trade lane can often be managed, but simultaneous pressure across multiple origins creates a wider problem because converters still need the same grades, coatings, and caliper profiles to satisfy existing customer approvals. That risk encourages larger operators to hold stronger supplier relationships, diversify sourcing, and secure inventory buffers, while smaller converters remain more exposed to lead-time shocks and short-notice cost increases. WML Paperboard's distribution partnership with JB Paper Trading Pty Ltd has improved Australian access to the Formakote range, but it still serves as a partial risk offset rather than a full substitute for broad-based domestic coated board capacity. In practical terms, the Australian cartonboard market can still grow under this structure, but growth becomes more dependent on procurement skills and working capital than it would be in a market with local coated board production.

Energy, Freight, And Port-Related Cost Volatility

Energy, freight, and port-related volatility continue to pressure the Australian cartonboard market, as converting margins are sensitive to both imported raw material costs and the local costs of printing, cutting, laminating, and gluing board into finished packs. Port delays can stretch container dwell times and tighten raw material buffers, creating knock-on effects on production schedules, customer lead times, and factory utilization across converter networks. Freight spikes tend to hit smaller buyers hardest because they have less ability to lock forward rates, consolidate orders, or spread cost movements across broader customer books. This matters beyond short-term profitability because uncertain landed costs make converters more cautious about investing in new barrier-coating lines, digital presses, and other upgrades needed for premium and regulated carton work. The Fair Work Commission's approval of the Graphic Packaging International Australia Converting Limited workplace agreement improved labor-cost visibility at one major New South Wales site, but it did not remove the broader exposure that the Australian cartonboard market still faces from energy and freight swings. Even large operators remain cautious about capital planning, and Graphic Packaging's 2026 emphasis on stronger cash flow and lower capital spending reflected that broader discipline across the packaging chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Food Service Board Leads Grade Transition

Folding Boxboard held 34.18% of the Australia cartonboard market share within product grades in 2025, which reflected its broad role in consumer-facing cartons where print clarity, surface quality, and stiffness directly affect retail presentation. The grade remained especially important in confectionery, dry food, health and beauty, and promotional multi-pack applications because it supports both branding and efficient converting across high-volume retail programs. Solid Bleached Board also remained important in premium food and personal care work because buyers in these categories place greater weight on brightness, cleanliness, and food-contact assurance than on lowest-cost supply alone. Solid Unbleached Board continued to serve more robust or utility-focused uses, while White-Lined Chipboard remained relevant in price-sensitive cartons where visual appearance mattered but the cost envelope was tighter. Together, these grades show that the Australia cartonboard market is still anchored in a broad retail pack mix where converters must balance visual standards, compliance, and machine performance rather than optimize around one single board property.

Food Service Board is projected to expand at a 6.49% CAGR from 2026 to 2031, making it the fastest-growing product grade as regulation reshapes demand in takeaway, quick-service, and convenience-led food channels. Western Australia's July 2025 ban on moulded expanded plastic packaging accelerated demand for grease-resistant cups, trays, and clamshell formats that rely on fiber-based alternatives. The shift away from PFAS has added another layer because converters now need food service board that delivers oil and moisture resistance while fitting APCO's documented phaseout direction for fibre-based food-contact packaging. Liquid Packaging Board remained tied to long-life dairy and plant-based beverages, so demand in that grade continued to depend on barrier performance, aseptic compatibility, and the credibility of recyclability claims in end markets. Across the Australia cartonboard industry, grade selection is increasingly being shaped by regulatory fit and end-use function, which gives higher-specification board a stronger commercial position than low-cost commodity alternatives.

By Packaging Format: Liquid Packaging Fastest As Aseptic Formats Expand

Folding Cartons accounted for 56.54% of the Australian cartonboard market share within packaging formats in 2025, keeping them well ahead of other converted forms because they serve the broadest range of food, pharmaceutical, cosmetic, and tobacco applications. Their leadership came from versatility rather than a single standout end use, since the same basic carton format can support shelf-ready grocery units, secondary pharmaceutical packs, gift-ready cosmetic sets, and everyday retail packs with minimal structural changes. Major grocery chains have also reinforced this format's position by favoring fold-flat retail-ready units that balance transit efficiency with clean shelf presentation, thereby raising demand for reliable creasing, clean tear performance, and stable board caliper. That preference matters for converters because it rewards production consistency and design discipline, and it also reduces the appeal of lower-specification material that may underperform in automated packing and scanning environments. In the Australian cartonboard market, folding cartons remain the core value pool because they sit at the intersection of branding, logistics, compliance, and day-to-day retail execution.

Liquid Packaging is projected to grow at a 6.84% CAGR through 2031, which makes it the fastest-expanding packaging format as aseptic applications spread across plant-based dairy, functional drinks, flavored milk, and ready-to-drink categories. These formats benefit from ambient shelf life, lower breakage risk than rigid alternatives, and a sustainability message that carries more weight once recovery infrastructure is in place and visible to retailers and consumers. Tetra Pak and saveBOARD supported Australia's first beverage carton recycling facility in Warragamba, and a second facility in Campbellfield followed in late 2024, which improved the recovery narrative for used beverage cartons in the local market. Sleeve and tray formats also have room to expand because fresh produce suppliers and retailers have already tested recyclable cardboard packs as replacements for plastic in store-facing produce lines. Cups and food service containers should continue to gain relevance as plastic restrictions widen across daily-use retail and takeaway formats, which means the Australian cartonboard market is likely to see share gains in formats that combine substitution potential with visible consumer use.

By End-User Industry: Pharma Overtakes Tobacco As Value-Growth Engine

Food accounted for 39.81% of the Australian cartonboard market in 2025, reflecting the depth and frequency of carton use across grocery categories ranging from frozen meals and pantry staples to fresh produce, condiments, and promotional food packs. This lead was supported by the non-discretionary nature of food demand, which provides converters with a steady base of repeat carton work even as other consumer categories become more volatile. Beverage remained the second-largest end-user group because long-life juice, flavored milk, and plant-based drinks continue to rely on carton formats that combine shelf life, transport efficiency, and recognizable sustainability positioning. The significant role of food and beverage also means retailer requirements carry extra weight in board selection, as those channels demand packaging that works across merchandising, logistics, and compliance without frequent disruptions. In the Australian cartonboard market, this creates a durable demand base that supports converting volume while still enabling premiumization through better print surfaces, improved barriers, and stronger sustainability claims.

The pharmaceutical and healthcare sector is projected to expand at a 6.71% CAGR through 2031, making it the fastest-growing end-user group, even though its absolute size remains smaller than that of the food and beverage sector. The category is gaining value because TGA rules now shape the carton itself, from the space needed for serialized data to the physical design needed for tamper-evident closures and secure handling. As prescription medicines and medical devices move deeper into coded, traceable packaging, converters must deliver stronger print accuracy, consistent repeatability, and documented process control on every regulated job. Tobacco has continued to lose momentum under structural demand pressures, while cosmetics and toiletries remain an attractive premium niche in which visual finish, board cleanliness, and sustainability certification influence brand choices. Household goods, apparel, and automotive aftermarket packs still represent a fragmented long tail, but together they add meaningful incremental volume and help the Australian cartonboard market avoid overdependence on any one consumer category.

Geography Analysis

New South Wales accounted for the largest share of converting activity in the Australian cartonboard market in 2025, reflecting Sydney's role as the country's leading e-commerce fulfillment hub and its proximity to dense retail distribution networks. The state's advantage was not only about demand volume, because its established converter base also supports faster design approval, shorter delivery cycles, and closer service links to brand owners and retailers concentrated along the eastern seaboard. NSW Plastics Plan 2.0, published in November 2025, expanded the list of plastic items scheduled for phase-out through 2027, creating a clearer path for additional fiber substitutions in foodservice and convenience-led packaging. Western Sydney also gained strategic relevance through the Warragamba beverage carton recycling facility, which strengthened the state's position in carton recovery and conversion.

Victoria followed as the second-largest state market, supported by Melbourne's diversified manufacturing base, strong freight links, and broad exposure to food, beverage, consumer goods, and health-related packaging work. The state also showed clear traction in fresh produce pack conversion, with commercial retail trials of recyclable cardboard packs indicating that carton substitution had moved beyond concept work and into scaled customer testing. Queensland recorded the fastest regional growth in the Australian cartonboard market, as population expansion in the southeast continued to support grocery, healthcare, and e-commerce consumption. The logistics corridor centered on Yatala and Hemmant remained important because it connected warehousing, transport, and converter operations, thereby supporting shorter lead times for large consumer goods flows. South Australia remained smaller by volume, but it strengthened its role as a development center for new fiber packaging concepts through Detmold's planned Regency Park headquarters and LaunchPad R&D facility.

Western Australia, the Northern Territory, and the ACT form a smaller but important frontier where policy changes can quickly alter pack selection across foodservice and beverage categories, as base volumes are lower and compliance shifts show up faster. Western Australia's 2025 plastic ban has already pushed toward more immediate substitution toward fiber-based takeaway and foodservice packs, giving the state outsized influence on format change relative to its population size. Across all states, APCO's 2025 reporting direction on recyclability and PFAS content has made procurement more consistent, as buyers increasingly seek traceable substrates that meet both internal review and external reporting expectations. That shared compliance backdrop means state differences now affect timing and customer mix more than the overall direction of the Australian cartonboard market.

Competitive Landscape

The Australia cartonboard market was moderately concentrated at the converting level and more fragmented across smaller print-and-fold specialists that serve regional, short-run, or highly customized work. A limited group of larger operators, including Graphic Packaging International, SIG Combibloc, Detmold Group, Opal, and other established converters, accounted for much of the premium, compliance-heavy volume, where service reliability and technical control matter most. Because Australia does not have domestic coated cartonboard manufacturing, leadership is defined less by mill ownership and more by procurement scale, converting capability, technical support, and the ability to secure customer approvals quickly. This structure allows scale players to lead in regulated and complex work, while leaving room for smaller firms that can win on responsiveness, niche formats, or local customer relationships.

Graphic Packaging Holding Company completed the ramp-up of its recycled paperboard facility in Waco in February 2026 and reaffirmed 2026 guidance for strong adjusted free cash flow with sharply lower capital spending, which supported a more stable supply outlook for its wider packaging network. SIG strengthened its position through material innovation when it commercially launched SIG Terra Alu-free + Full barrier in October 2025, offering a lower-carbon aseptic carton option for oxygen-sensitive products such as fruit juices, nectars, flavored milk, and plant-based beverages. Detmold added a different kind of strategic signal by starting work on a new Adelaide headquarters in June 2025 and then publishing a 12-month sustainability performance update in February 2026, tying physical expansion to a stronger sustainability positioning. WML Paperboard improved its reach in Australia through a distribution partnership with JB Paper Trading Pty Ltd, giving converters broader access to the Formakote range through local sheeting, inventory support, and national distribution. Taken together, these moves show that the Australia cartonboard market is being contested through reliability, technical performance, and route-to-market strength more than through simple price competition alone.

The clearest competitive white spaces remain PFAS-free barrier work, regulated pharmaceutical cartons, and high-graphic short-run applications where approval speed and technical precision matter more than standard-volume throughput. Operators that can pre-qualify substrates, document compliance, and deliver consistent print and finishing performance are better placed because customers increasingly want fewer qualification cycles and less regulatory exposure. The Fair Work Commission's October 2025 approval of the Graphic Packaging International Australia Converting Limited workplace agreement also provided one large New South Wales site with greater labor-cost clarity through September 2028, which matters in a market where operational certainty supports customer retention. Even so, the long tail of regional and specialty converters continues to keep the Australia cartonboard market competitive, particularly in local accounts, specialty formats, and customer programs that value agility over national scale.

Australia Cartonboard Industry Leaders

Detmold Australia Sales Pty Ltd.

Graphic Packaging International Australia Pty Limited

Tetra Pak Marketing Pty Limited

SIG Combibloc Australia Pty Ltd.

Labelmakers Group Pty Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Graphic Packaging Holding Company completed the ramp-up of its USD 1.67 billion recycled paperboard facility in Waco, Texas, and reaffirmed 2026 guidance of USD 700 million to USD 800 million adjusted free cash flow, with capital spending reduced sharply to approximately USD 450 million from USD 935 million in 2025. The operational stabilization signals restored supply reliability for Graphic Packaging's Australian converting operations.

- December 2025: Costa, Coles, and Opal launched a large-scale trial transitioning Perino tomato packaging from 80% rPET plastic punnets to recyclable cardboard packaging across Coles' Victorian stores. This collaboration, announced on December 2, 2025, is one of the most commercially significant fresh-produce plastic-to-cartonboard conversion events in Australia's recent packaging history.

- October 2025: SIG commercially launched SIG Terra Alu-free + Full barrier for multi-serve aseptic cartons globally, the world's first aluminum-layer-free full-barrier packaging material for this format, achieving up to 61% lower carbon footprint versus standard aseptic cartons and extending application to oxygen-sensitive products including fruit juices, nectars, flavored milk, and plant-based beverages.

- June 2025: Detmold Group commenced site works on its new AUD-valued, 5,100 m² global headquarters at Regency Park, Adelaide, consolidating eight Adelaide-area business units, including Detpak, PaperPak, Detmold Medical, Cup and Carry, and the LaunchPad R&D facility, under one roof by end of 2026. The investment reinforces South Australia's position as a center for fiber-based packaging innovation.

Australia Cartonboard Market Report Scope

The Australia Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include solid bleached board, solid unbleached board, folding boxboard, white-lined chipboard, liquid packaging board, and food service board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The Australia Cartonboard Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and Other Packaging Formats), and End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics and Toiletries, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

Key Questions Answered in the Report

What is the current size of the Australia cartonboard market?

The Australia cartonboard market was valued at USD 1.46 billion in 2025 and is forecast to reach USD 2.04 billion by 2031 at a 5.92% CAGR over 2026-2031.

What is driving cartonboard demand in Australia?

Growth is being supported by plastic bans, PFAS-free packaging changes, shelf-ready grocery formats, and stricter pharmaceutical compliance requirements.

Which product grade is growing the fastest in Australia?

Food Service Board is the fastest-growing product grade, with a projected 6.49% CAGR through 2031 as takeaway and foodservice packs move away from plastic.

Why are folding cartons still the dominant packaging format?

Folding Cartons held 56.54% of packaging format value in 2025 because they work across food, pharmaceuticals, cosmetics, and retail-ready grocery applications.

Why is pharmaceutical packaging becoming more important for converters?

Pharmaceutical and healthcare is projected to grow at a 6.71% CAGR through 2031 as serialization, DataMatrix coding, and UDI labeling increase the need for compliant cartons.

Which states matter most for demand and growth?

New South Wales remains the largest converting center, Victoria stays important through its manufacturing base and retail trials, and Queensland is the fastest-growing regional area.

Page last updated on: