India Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

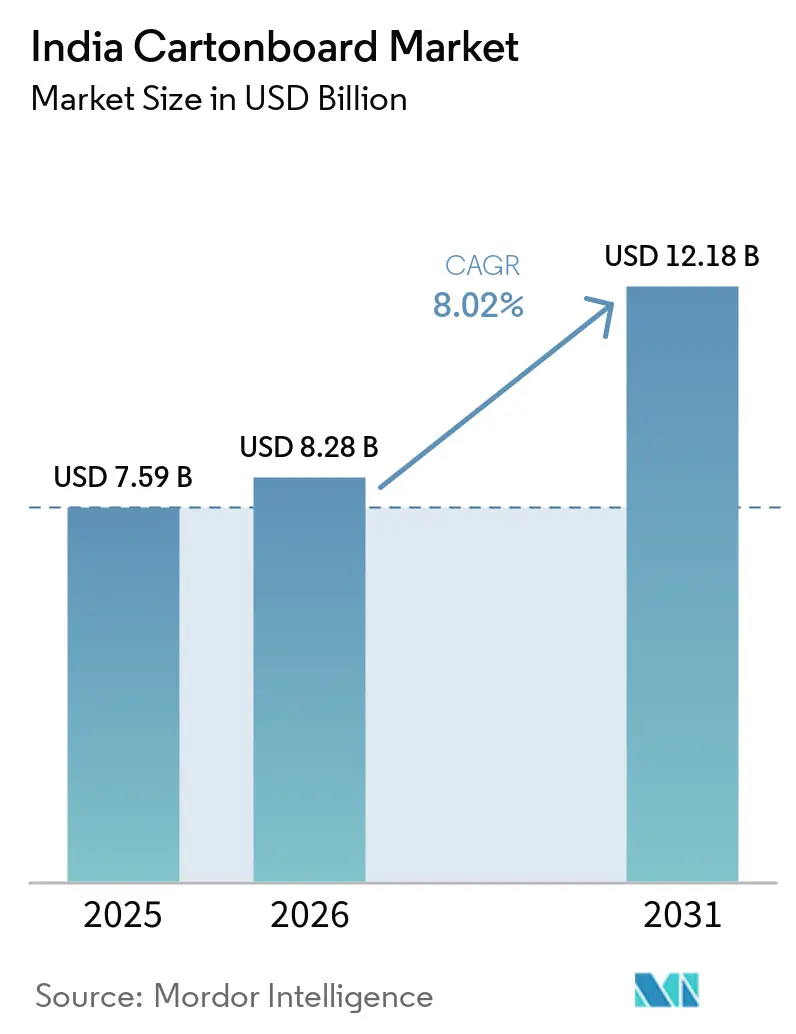

| Base Year Market Size (2025) | USD 7.59 Billion |

| Market Size (2026) | USD 8.28 Billion |

| Market Size (2031) | USD 12.18 Billion |

| Growth Rate (2026 - 2031) | 8.02% CAGR |

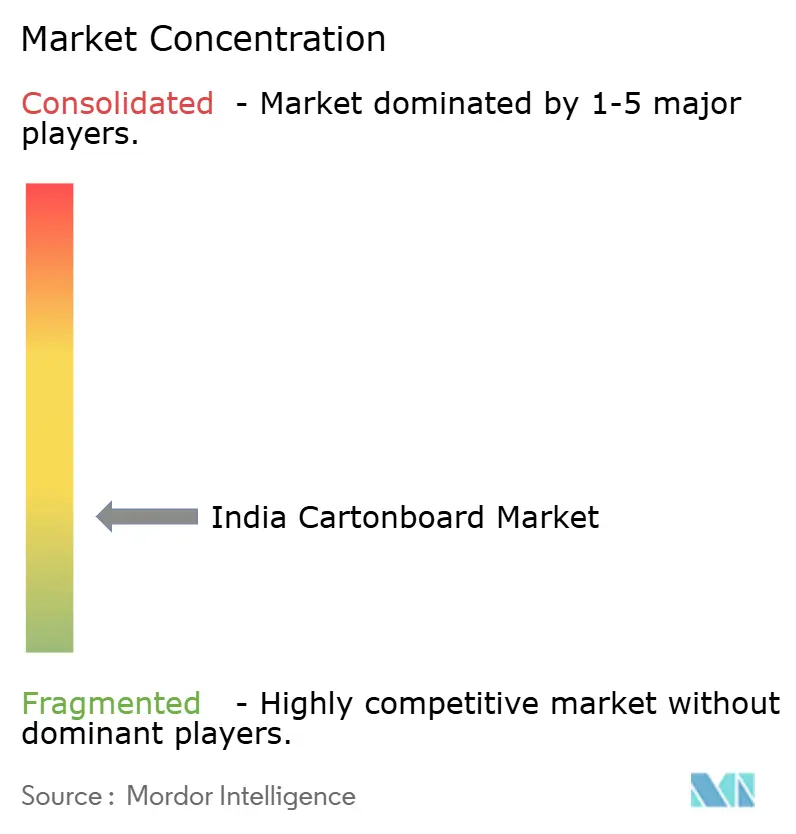

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Cartonboard Market Analysis by Mordor Intelligence

The India cartonboard market size is projected to expand from USD 7.59 billion in 2025 and USD 8.28 billion in 2026 to USD 12.18 billion by 2031, registering a CAGR of 8.02% between 2026 to 2031. The current growth cycle is being shaped by tighter pressure on single-use plastics, stronger demand for premium folding cartons in food and pharmaceutical packaging, and rising consumption from quick-commerce and aseptic beverage channels. The shift is not limited to simple substitution, because brand owners are also moving from white-lined chipboard toward folding boxboard and solid bleached board to improve compliance, finish quality, and product positioning. This is changing the demand mix in a way that lifts value per tonne, especially where packaging must meet stricter food-contact and product-traceability needs. Competitive strategy is also evolving, with integrated mills and larger converters investing in capacity, acquisitions, and backward integration to protect margins and lock in higher-value demand. Imported virgin-fiber paperboard and higher pulp costs continue to put pressure, yet alignment between regulation, consumption growth, and mill investment keeps the India cartonboard market on a durable growth path through 2031.

Key Report Takeaways

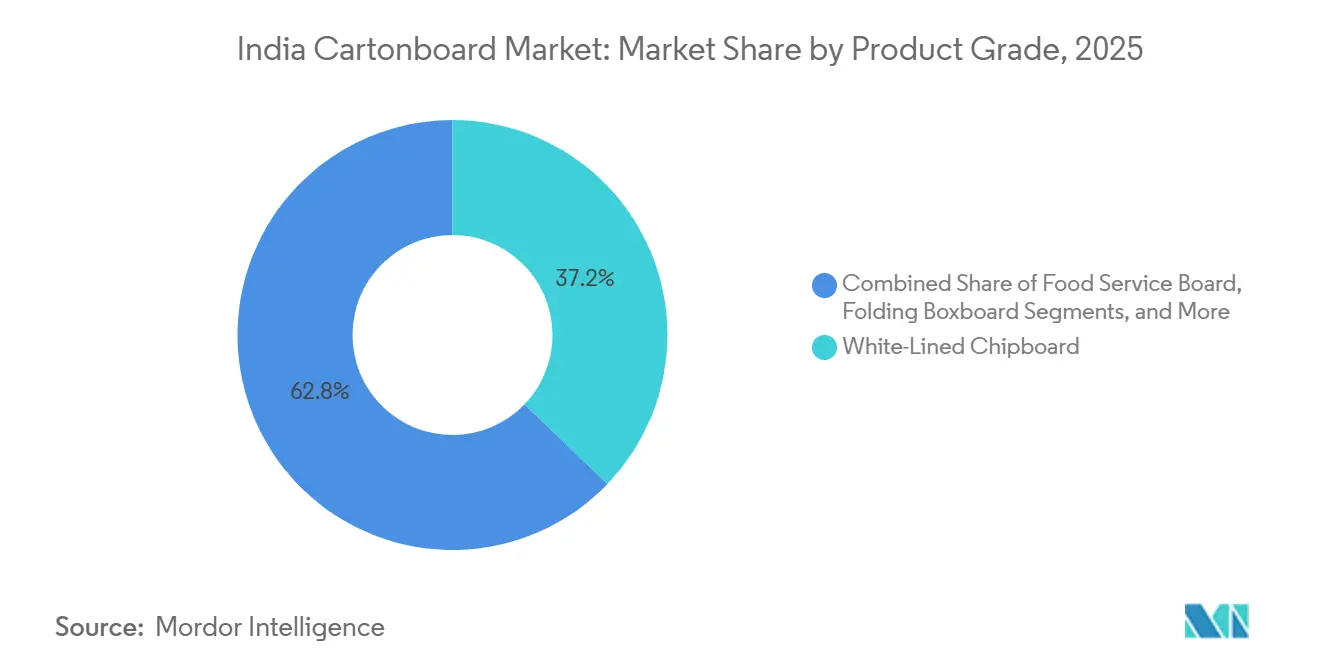

- By product grade, white-lined chipboard captured 37.19% of the India cartonboard market share in 2025.

- By packaging format, the India cartonboard market size for the liquid packaging segment is forecast to advance at an 8.74% CAGR through 2031.

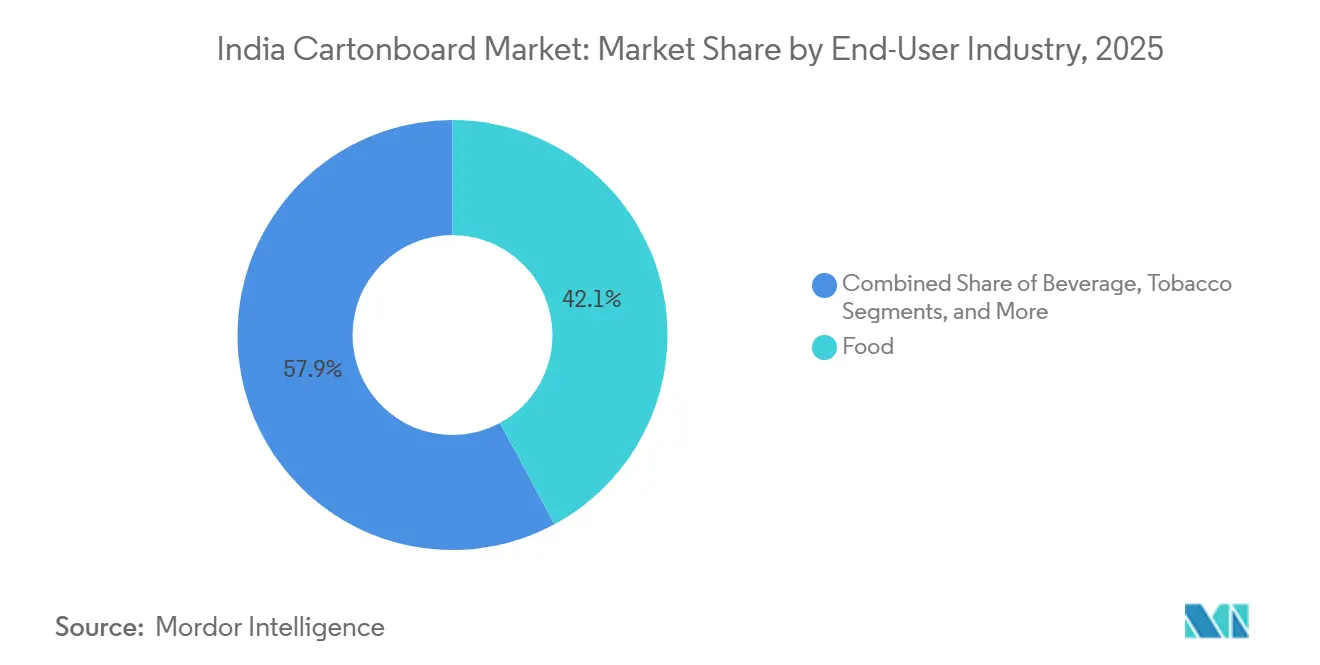

- By end-user industry, food captured 42.14% of the India cartonboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EPR-Ready Paper Packaging Compliance Advantage From 2026 | +2.1% | National, with concentrated impact in Maharashtra, Delhi NCR, Tamil Nadu, and Karnataka where large brand-owner operations are registered | Short term (≤ 2 years) |

| Substitution Of Single-Use Plastics With Paperboard | +1.8% | National, highest acceleration in states with active plastic-ban enforcement squads, including Delhi, Karnataka, Maharashtra | Short term (≤ 2 years) |

| Rising Premiumization In Food And Pharma Folding Cartons | +1.2% | National, led by South India pharma clusters and metro FMCG hubs | Medium term (2-4 years) |

| Aseptic Dairy And Juice Expansion Supporting Liquid Packaging Board | +0.7% | Pan-India, with Gujarat and Maharashtra as key supply nodes | Medium term (2-4 years) |

| Organized Retail, E-Commerce, And Quick-Commerce Packaging Demand | +0.5% | Tier-1 and Tier-2 cities, with dark-store saturation in Mumbai, Bengaluru, Delhi, Hyderabad, Pune | Short term (≤ 2 years) to Medium term (2-4 years) |

| FSSAI-Compliant Food-Contact Paperboard Adoption | +0.3% | National, with early adoption in processed-food and dairy manufacturing clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EPR-Ready Paper Packaging Compliance Advantage From 2026

The India cartonboard market is gaining support from the growing stringency of plastic compliance obligations for brand owners that rely heavily on rigid plastic formats. India’s single-use plastic enforcement has already shown that regulation is not merely symbolic, as penalties collected in Delhi and Karnataka exceeded INR 198 million (USD 2.2 million) through 2024.[1]Press Information Bureau, “Single-Use Plastic Ban Enforcement,” Government of India, pib.gov.in That enforcement backdrop is pushing packaging teams to look for formats that reduce compliance friction and simplify audit trails. Cartonboard benefits by helping lower dependence on plastic in secondary packs and selected foodservice applications, which matters more as environmental reporting becomes part of commercial procurement. Mills and converters that can document supply origin, substrate quality, and customer-specific compliance are therefore improving their position in annual sourcing cycles. The India cartonboard market is also becoming more selective, as large buyers increasingly favor suppliers that can pair board performance with documentation discipline, rather than the lowest selling price.

Substitution Of Single-Use Plastics With Paperboard

The India cartonboard market is also moving higher as paper-based formats replace plastic in a wider set of everyday packaging uses. The continued enforcement of the single-use plastic ban encouraged a shift toward kraft bags, molded-fiber trays, and food-contact cartonboard in foodservice and takeaway applications. This change matters because it widens cartonboard demand beyond traditional folding cartons and brings in categories that were once served by low-cost plastic or expanded polystyrene packs. At the same time, food-contact applications require improved grease resistance, cleaner barrier performance, and greater reliability in compliance with India’s packaging rules regarding migration.[2]Food Safety and Standards Authority of India, “Food Safety and Standards (Packaging) Regulations, 2018 - Compendium As Of April 2025,” FSSAI, fssai.gov.in That is improving the demand mix for food service board and other higher-specification grades rather than only adding more recycled board volume. The India cartonboard market is therefore capturing both substitution demand and quality upgrading simultaneously, making the shift more durable than a short-term policy response.

Rising Premiumization In Food And Pharma Folding Cartons

Premiumization is increasing value in the Indian cartonboard market because food and pharmaceutical brand owners now want packaging that does more than just hold a product. Converters are investing in features such as embossing, foil, varnish, tamper-evidence, and Braille capability to enable cartons to meet both shelf-display needs and tighter compliance standards. Integrity Packaging’s installation of a Bobst Novafold folder-gluer with AccuBraille showed that Indian converters are preparing for this requirement with equipment upgrades rather than waiting for demand to become unavoidable. This shift is especially important in pharmaceutical cartons, where accessibility, traceability, and print quality matter alongside cost and machine efficiency. It also reflects the rise of digitally native brands that want premium visual identity even in short production runs, which rewards converters with better finishing and faster changeovers. The India cartonboard market benefits from premiumization, which lifts realization per carton and gives higher-grade substrates a stronger role in the mix.

Aseptic Dairy And Juice Expansion Supporting Liquid Packaging Board

Liquid packaging is becoming a stronger growth engine for the Indian cartonboard market as dairy and juice brands expand shelf-stable formats across a wider retail footprint. SIG opened its first aseptic carton plant in India in February 2025 with an initial capacity of 4 billion packs per year, and it also approved a second investment phase for a local extrusion line by 2027.[3]SIG, “SIG Opens Its First Aseptic Carton Plant In India,” SIG, sig.biz UFlex’s Asepto business also expanded its Sanand facility from 7 billion to 12 billion aseptic carton packs per year in October 2025, materially increasing domestic conversion capacity for aseptic cartons. This matters because domestic filling and conversion capacity reduces bottlenecks and gives beverage and dairy brands more confidence to scale paper-based liquid formats. Tetra Pak’s extension of paper-based barrier technology to high-speed A3/Speed lines in Asia also narrows the performance gap between paper-based and aluminum-foil-based structures, which supports wider adoption where throughput is critical.[4]Tetra Pak, “Tetra Pak Extends Paper-Based Barrier Packaging To High-Speed Lines In Asia,” Tetra Pak, tetrapak.com The India cartonboard market is therefore gaining from both demand growth in ambient beverages and a technology base that is becoming more commercially practical for local producers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wastepaper, Pulp, And Energy Cost Volatility | -1.3% | National, most acute for recycled-fiber mills in Gujarat, Maharashtra, and West Bengal with limited backward integration | Short term (≤ 2 years) to Medium term (2-4 years) |

| Price-Led Competition From Cheap Imports And Regional Duplex Mills | -1.0% | National, with highest import penetration in West and South India near major ports | Medium term (2-4 years) |

| PFAS-Free Barrier Transition Raises Qualification Costs | -0.4% | National, concentrated among food-service board converters and grease-resistant specialty grade producers | Long term (≥ 4 years) |

| Flexible Packaging Still Wins In High-Barrier, Low-Cost Applications | -0.3% | National, most pronounced in commodity snack, confectionery, and ready-to-eat categories in rural and semi-urban markets | Medium term (2-4 years) to Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Wastepaper, Pulp, And Energy Cost Volatility

Input cost volatility remains the most immediate operating restraint for the India cartonboard market. Hardwood pulp prices moved above USD 615 per metric tonne in early 2026, driven by supply tightness due to mill maintenance shutdowns and raw material disruptions in Indonesia. Domestic mills also faced a sharp rise in wood and recovered fiber costs, which increased raw material pressure and made it more difficult to maintain price discipline on lower-value grades. This matters most for mills that rely on imported pulp or purchased wastepaper, because they have less room to protect margins when customers resist price increases. Integrated producers are better positioned because in-house access to pulp or fiber provides them with a structural cost buffer during volatile periods. The India cartonboard market is therefore seeing a clearer split between suppliers that can absorb cost shocks through integration and those that remain more exposed to sudden changes in global fiber and energy conditions.

Price-Led Competition From Cheap Imports And Regional Duplex Mills

Import competition is another major restraint for the Indian cartonboard market, especially in grades where customers still primarily buy on price. India’s paper and paperboard imports reached 2.05 million tonnes in FY25, up from 1.08 million tonnes in FY21, with China contributing 27% and ASEAN 20% of total volumes in value terms. These imports have often landed at prices below domestic production economics, putting pressure on realizations for Indian board makers and weakening the investment case for smaller mills. The government responded with a minimum import price of INR 67,220 (USD 771.4) per tonne on virgin multi-layer paperboard through March 2026, which offered partial support to domestic producers. Even so, regional duplex and white-lined chipboard mills remain squeezed between rising wastepaper costs on one side and low-priced imported board on the other. The India cartonboard market is likely to keep consolidating under this pressure, because scale, integration, and customer relationships matter more when price competition turns structural.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: White-Lined Chipboard Dominates, Food Service Board Accelerates

White-lined chipboard held 37.19% of the Indian cartonboard market share in 2025, which reflects the continued strength of recycled-fiber board in mass-market secondary packaging. The grade remains widely used across toys, apparel, and fast-moving consumer goods because it offers acceptable printability and cost efficiency at scale. Its position has also become more resilient because improvements in topcoats and surface treatments have narrowed part of the historical finish gap between recycled grades and premium virgin-fiber options. That allowed brand owners to maintain shelf presence while still using a lower-cost base board in many secondary applications. The India cartonboard market has therefore maintained a broad recycled-fiber foundation even as customer expectations for appearance and consistency have risen.

The food service board market is projected to expand at a 9.17% CAGR from 2026 to 2031, and this segment of the India cartonboard market is strengthening as restaurant chains, delivery platforms, and takeaway formats shift toward paper-based food packaging. Demand is rising because foodservice applications need grease resistance, migration compliance, and better forming performance than basic recycled trays can deliver under stricter packaging scrutiny. Folding boxboard and solid bleached board remain the premium end of the India cartonboard industry, serving higher-value pharmaceutical, cosmetics, and confectionery packaging where brightness, stiffness, and print performance matter more. Tamil Nadu Newsprint and Papers Limited also continued to reposition its board mix toward higher-realization folding boxboard, and its board unit reached 200,075 metric tonnes of production in FY26. Solid unbleached board still serves niche industrial and heavy-goods secondary packaging, but its role remains smaller because the strongest growth is moving toward food-contact and premium printed cartons rather than utility-heavy transport formats.

By Packaging Format: Folding Cartons Lead, Liquid Packaging Closes In

Folding cartons accounted for 58.56% of the India cartonboard market size in 2025, making them the most established packaging format across pharmaceuticals, cosmetics, food, and general FMCG applications. Their lead comes from the sheer width of use cases, from blister-pack cartons and personal care boxes to branded secondary packs for packaged foods. The format also benefits from converter investments in automation, finishing quality, and multi-location supply, which makes it easier for national brands to standardize packaging across plants and regions. TCPL Packaging expanded this national footprint with a greenfield folding carton plant near Chennai in 2025, taking its network to 10 manufacturing facilities. The India cartonboard market continues to rely on folding cartons as the core value pool because the format supports both volume stability and premium conversion opportunities.

Liquid packaging is forecast to grow at an 8.74% CAGR through 2031, making it the fastest-growing segment of the Indian cartonboard market within packaging formats. Domestic aseptic investment is central to that shift, because SIG created an initial 4 billion-pack base in Ahmedabad and approved further expansion, while UFlex increased Asepto’s annual capacity to 12 billion packs. Tetra Pak’s paper-based barrier rollout for high-speed lines is also important because it improves the operating case for paper-rich structures where filling efficiency is critical. Sleeve and tray formats are expanding steadily with organized retail and e-commerce, while cups and foodservice containers are moving faster as restaurants replace plastic-heavy packs with board-based alternatives. Within the India cartonboard industry, this means liquid packaging is no longer a niche adjacency, because it is becoming one of the clearest areas where technology, consumption growth, and sustainability priorities are aligning.

By End-User Industry: Food Anchors Demand, Pharma Drives Premium Growth

The food segment accounted for 42.14% of the India cartonboard market in 2025, underscoring how strongly processed and packaged food still anchors overall demand. Food packaging uses more board not only because volumes are high, but also because cartons support display, branding, stacking, and transport protection across a wide range of stock-keeping units. Quick-commerce is changing the specification of these packs, since products now move through dark stores and short-cycle fulfillment points that put more handling stress on cartons before final delivery. This is leading food brands to use packs that protect product condition while still presenting well in digital-first merchandising environments. The India cartonboard market, therefore, benefits from both the scale of food demand and the growing packaging intensity of modern distribution channels.

The pharmaceutical and healthcare sector is projected to grow at an 8.94% CAGR from 2026 to 2031, making it one of the strongest premium demand segments in the Indian cartonboard market. Export-oriented generic manufacturing is tightening carton specifications because packs must support tamper evidence, clear printing, migration-compliant materials, and accessibility features such as Braille for regulated markets. The same pattern is reinforcing the move toward certified, traceable supply chains, as food and pharma buyers both require greater process discipline from board suppliers and converters. Cosmetics, toiletries, tobacco, toys, apparel, and automotive parts add steady supporting demand, with beauty and personal care cartons benefiting from strong design requirements and higher visual standards. Across the Indian cartonboard industry, this creates a favorable mix, as large food volumes keep utilization stable while pharmaceutical and premium personal care packs improve average realization.

Geography Analysis

South India carried the deepest production concentration in the Indian cartonboard market in 2025, with Telangana, Andhra Pradesh, and Tamil Nadu hosting several of the country’s largest integrated mill assets. ITC’s facilities at Bhadrachalam, Coimbatore, Tribeni, and Bollaram together represented an installed capacity of nearly 1.07 million tonnes per year by early 2025, giving it the broadest single-company production base in the country. Andhra Paper and Tamil Nadu Newsprint and Papers Limited add further depth to the southern supply chain, which keeps the region central to domestic board availability. Demand is also favorable in the South because Hyderabad’s pharmaceutical base and Bengaluru’s electronics and consumer goods manufacturing need higher-specification cartons with better consistency. That mix supports stronger realizations for folding boxboard and solid bleached board than in regions where packaging remains more price-led.

West India stands out as the most dynamic demand center in the India cartonboard market, led by Gujarat and Maharashtra, as aseptic packaging, branded foods, and FMCG procurement continue to scale. SIG’s Ahmedabad plant and its follow-on extrusion plan made Gujarat an important node in liquid packaging for the next phase of carton-based beverage growth. UFlex’s Sanand expansion from 7 billion to 12 billion packs per year reinforced the regional advantage by increasing local aseptic carton conversion capacity. Maharashtra adds a different strength because Mumbai houses many FMCG and pharmaceutical headquarters, while Pune contributes substantial pharmaceutical manufacturing demand. These factors make the western region highly relevant for both packaging innovation and board qualification activity, and they also support the rising use of food service boards as quick-commerce density increases.

North India combines high consumption density with relatively limited mill capacity, so large volumes of board still move into the region from South and West India. Delhi NCR remains important because it concentrates consumption, brand offices, and organized retail activity, even though it is not the country’s main board manufacturing base. East India supports regional converters through assets such as Emami Paper Mills in Balasore, and the January 2025 PM4 headbox upgrade improved sheet formation quality for folding boxboard customers. As modern retail and fast-delivery networks spread into eastern and northern cities, freight efficiency and service lead time are becoming more important in carton sourcing decisions. The India cartonboard market is therefore becoming more regionally nuanced, because the balance between mill location, converter presence, and end-use demand cluster now shapes competitiveness more directly than in earlier years.

Competitive Landscape

The India cartonboard market remains fragmented, but the strongest competitive positions are held by integrated manufacturers that control a larger share of the pulp-to-board chain. ITC Limited, JK Paper Limited, and Tamil Nadu Newsprint and Papers Limited form the leading upstream group, while smaller recycled-fiber mills remain more exposed to cost swings and lower-price competition. ITC strengthened that leadership position in April 2025 when it acquired the Century Pulp and Paper undertaking from Aditya Birla Real Estate Limited for INR 3,498 crore (USD 418 million), adding around 480,000 tonnes of annual installed capacity and lifting its total paper manufacturing capacity by nearly 50% to more than 1.5 million tonnes per annum. JK Paper also continued to push backward integration through its planned bleached chemi-thermomechanical pulp investment at Songadh, Gujarat, underscoring how strongly cost control now shapes strategy in the Indian cartonboard market. The balance of power is therefore shifting toward companies that can pair scale with fiber security, rather than those competing mainly on machine capacity and spot market pricing.

The converter layer is also stratified, with TCPL Packaging and Parksons Packaging competing nationally while many regional specialists continue to serve district and state-level customers. TCPL’s Chennai plant expanded its network to 10 facilities, thereby improving its reach across South India’s pharmaceutical and FMCG corridors. The company also commissioned a gravure cylinder manufacturing facility under Accura Technik in Q3 FY26, which is a useful example of how converters are trying to lock in critical inputs and shorten response times. This matters because premium carton work now depends on reliable print tooling, shorter runs, tighter artwork changes, and stronger customer service. Converters that still rely on basic commodity production face greater margin pressure as brand owners demand traceability, embellishment, and greater performance consistency across multiple packaging lines.

The aseptic carton niche is much more concentrated than the broader Indian cartonboard market because entry depends on filling-line compatibility, barrier know-how, and established relationships with dairy and beverage customers. SIG’s local plant and Tetra Pak’s work on paper-based barrier technology show that equipment ecosystem and substrate science can matter as much as baseboard supply in this sub-segment. Another important theme is preparation for PFAS-free food-contact solutions, since proposed packaging changes could raise the technical threshold for food service boards and specialty applications. This combination of import pressure, compliance investment, and technology-led differentiation suggests that consolidation in the Indian cartonboard market will continue to favor scaled players with stronger capital access and broader customer relationships.

India Cartonboard Industry Leaders

ITC Limited

N R Agarwal Industries Limited

JK Paper Limited

Tamil Nadu Newsprint and Papers Limited

Emami Paper Mills Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: ITC Limited, JK Paper Limited, and Tamil Nadu Newsprint and Papers Limited reported their strongest quarterly performance in FY26, benefiting from partial relief provided by the minimum import price regime, volume gains in premium packaging grades, and moderation in wood input prices, signaling improving operating leverage for integrated board producers ahead of FY27 capacity additions.

- February 2026: Tetra Pak extended its paper-based barrier technology to high-speed Tetra Pak A3/Speed filling lines, reducing the barrier-performance gap between paper-based and aluminum-foil-based aseptic carton structures and enabling dairy producers in India and across Asia to adopt low-carbon packaging without sacrificing filling-line throughput.

- October 2025: UFlex Limited's Asepto unit completed a debottlenecking project at its Sanand, Gujarat aseptic packaging plant, increasing annual production capacity from 7 billion to 12 billion carton packs, a 71% capacity addition, positioning Asepto to serve growing demand from domestic dairy and non-carbonated soft drink producers.

- October 2025: Valmet received an order from ITC Limited for a sixth new wood chipping line at its Bhadrachalam, Telangana pulp mill, designed for low wood losses and superior chip quality, with commissioning scheduled for end of 2026 to support ITC's expanding paperboard and specialty paper output.

India Cartonboard Market Report Scope

The India Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include solid bleached board, solid unbleached board, folding boxboard, white-lined chipboard, liquid packaging board, and food service board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The India Cartonboard Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and Other Packaging Formats), and End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics and Toiletries, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

Key Questions Answered in the Report

What is the current and forecast value of the India cartonboard sector?

The India cartonboard market size was USD 7.59 billion in 2025, reached USD 8.28 billion in 2026, and is forecast to reach USD 12.18 billion by 2031 at an 8.02% CAGR.

Which product grade leads demand in India cartonboard?

White-lined chipboard led with 37.19% share in 2025, supported by its wide use in mass-market secondary packaging across consumer goods categories.

Which packaging format is growing the fastest in cartonboard applications?

Liquid packaging is the fastest-growing format, with an 8.74% CAGR expected through 2031, helped by aseptic dairy and juice investments.

Why is food still the largest end-user for cartonboard in India?

Food held 42.14% share in 2025 because packaged foods use cartons for display, transport protection, branding, and increasing quick-commerce fulfillment needs.

What is driving premium demand in pharmaceutical cartons?

Pharmaceutical and healthcare is projected to grow at an 8.94% CAGR through 2031 as export-oriented drug makers require better traceability, print quality, tamper evidence, and compliant materials.

What are the main risks for cartonboard producers in India?

The biggest risks are pulp and wastepaper cost volatility, lower-priced imports, higher qualification costs for food-contact coatings, and continued competition from flexible packaging in barrier-heavy applications.

Page last updated on: