United States Bubble Tea Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

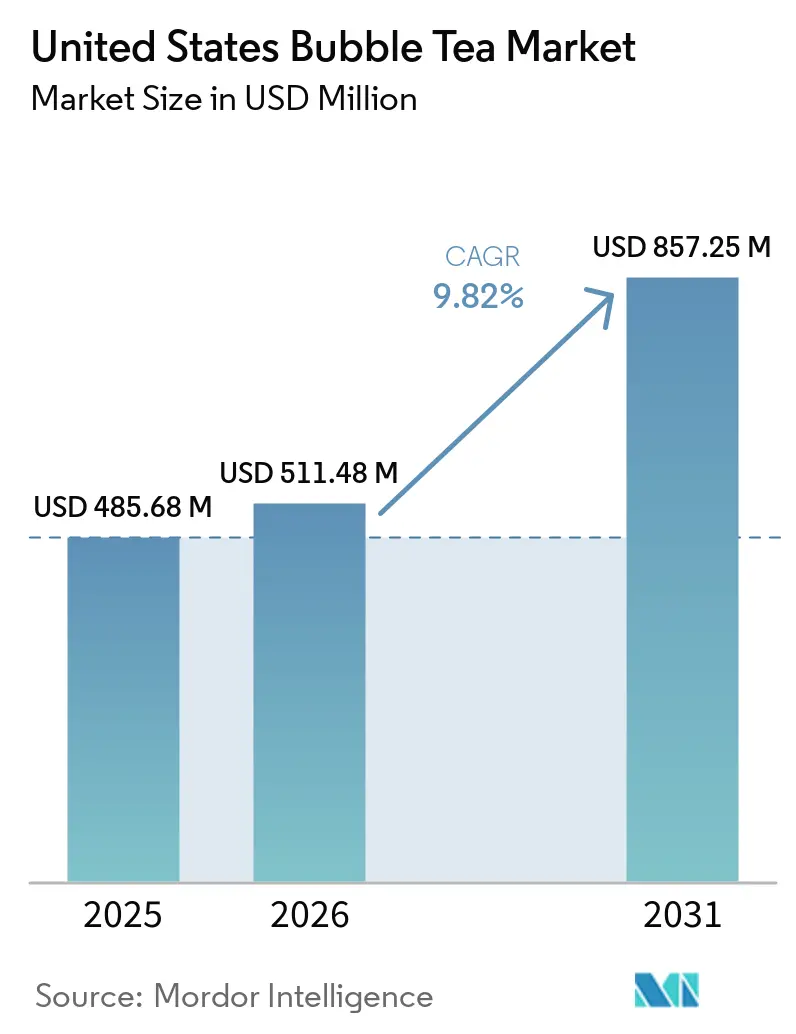

| Base Year Market Size (2025) | USD 485.68 Million |

| Market Size (2026) | USD 511.48 Million |

| Market Size (2031) | USD 857.25 Million |

| Growth Rate (2026 - 2031) | 9.82% CAGR |

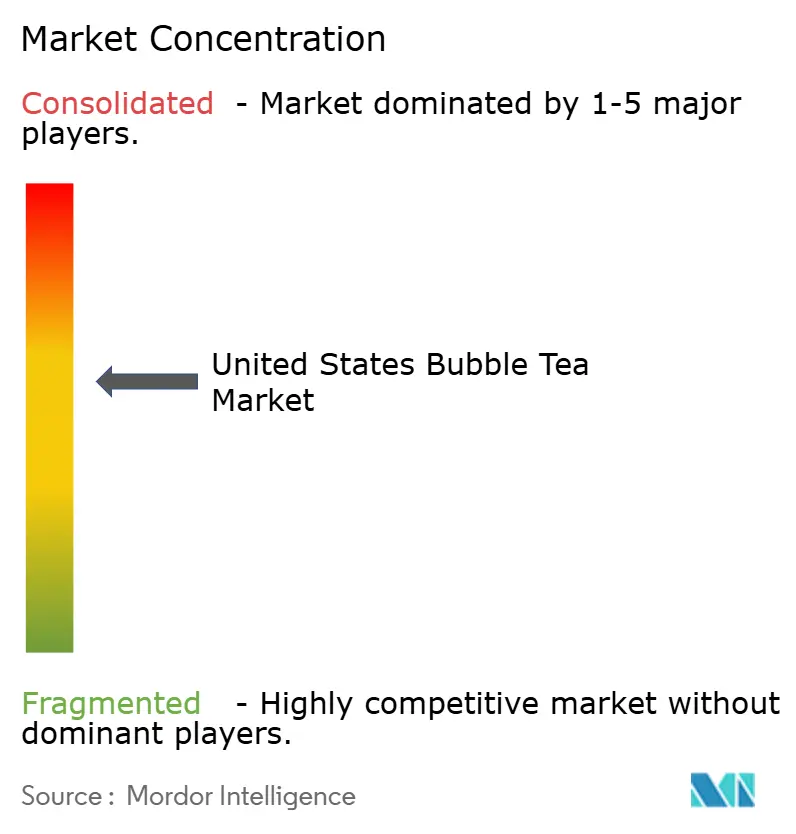

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Bubble Tea Market Analysis by Mordor Intelligence

The United States bubble tea market is valued at USD 511.48 million in 2026 and is projected to reach USD 857.25 million by 2031 at a CAGR of 9.82%. Milk-based drinks still set the baseline for volume, while plant-based formats are widening the premium end of the category. Foodservice remains the leading route to consumers, but retail demand is rising as ready-to-drink products move into broader shelf space. Franchise expansion, stronger menu innovation, and digital ordering are helping the category reach new occasions and new trade areas through 2026. At the same time, sugar scrutiny and higher tapioca input costs are raising the operating bar for smaller chains and independent stores. This leaves the United States bubble tea market on a growth path that favors brands that can manage consistency, supply, and product refresh cycles at scale.

Key Report Takeaways

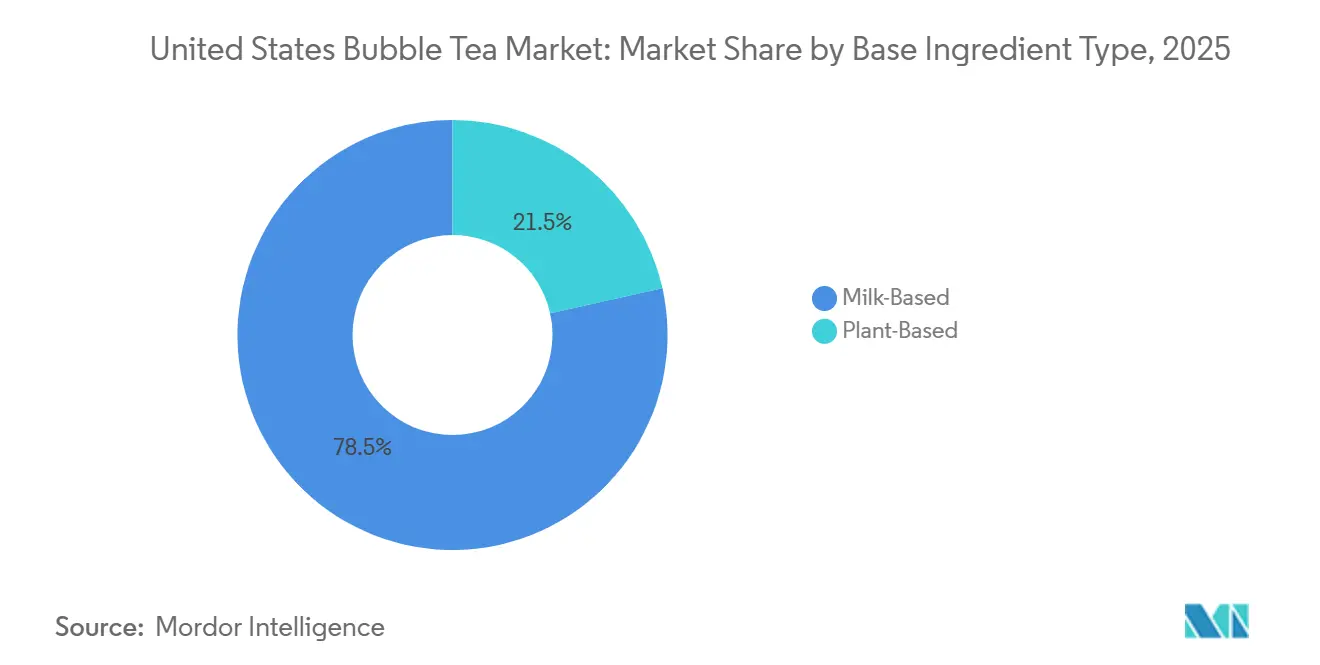

- By base ingredient type, milk-based formulations led with 78.48% revenue share in 2025, while plant-based formulations are projected to expand at a 10.67% CAGR through 2031.

- By tea type, black tea held 38.72% share in 2025, while green tea is forecast to grow at an 11.02% CAGR through 2031.

- By packaging form, PET/glass bottles accounted for 48.62% share in 2025, while aluminium cans are projected to advance at an 11.25% CAGR through 2031.

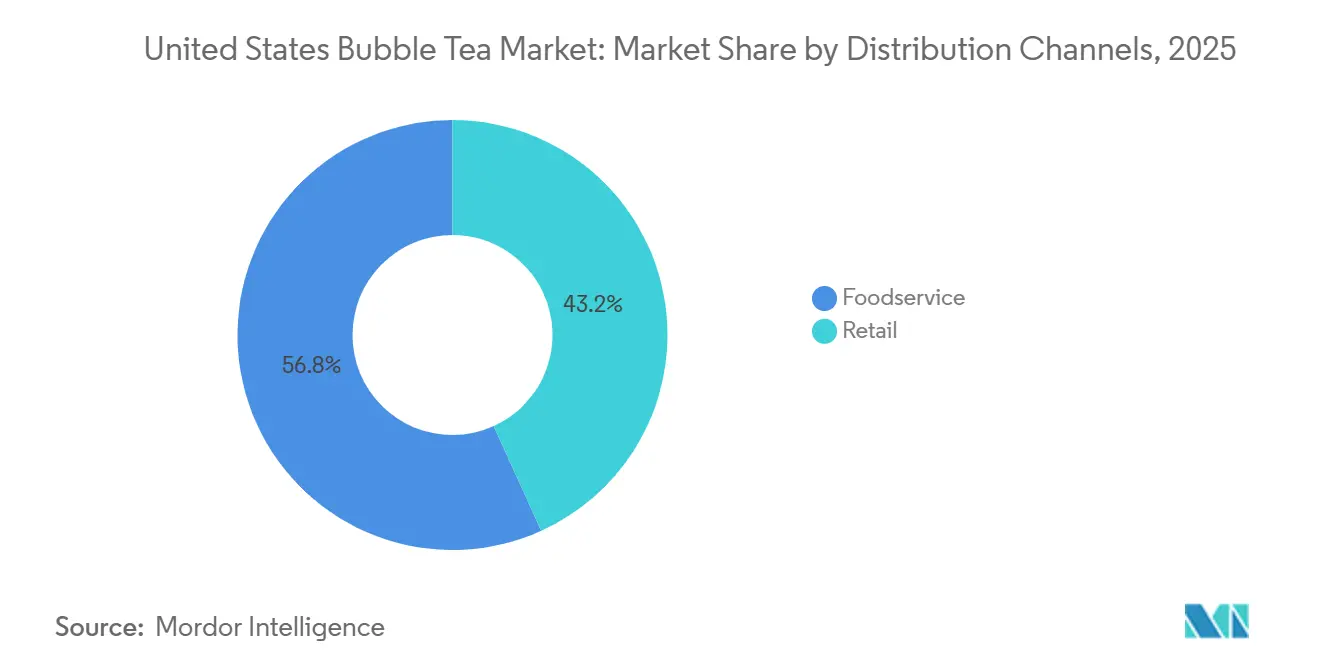

- By distribution channel, foodservice captured 56.78% share in 2025, while retail is expected to record the highest CAGR at 10.95% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Bubble Tea Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Popularity of Asian Food and Beverage Culture | +1.8% | National, with early intensity in California, New York, and Texas | Long term (≥ 4 years) |

| Rising Demand Among Gen Z and Millennials | +2.1% | National, strongest in urban metros and university towns | Medium term (2-4 years) |

| Expansion of Bubble Tea Franchise Chains | +1.5% | National, accelerating in Southeast and Mountain West | Medium term (2-4 years) |

| Increasing Demand for Customizable Beverages | +1.4% | National | Medium term (2-4 years) |

| Product Innovation in Flavors and Ingredients | +0.9% | National, influenced by Pacific Rim taste corridors | Short term (≤ 2 years) |

| Expansion of Delivery and Online Ordering Platforms | +0.7% | National, highest density in major metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Popularity of Asian Food and Beverage Culture

The United States bubble tea market is benefiting from the wider acceptance of Asian food and drink across mainstream retail and foodservice channels. That change is reducing the distance between a specialty drink purchase and an everyday beverage occasion. It is also increasing consumer comfort with Taiwanese-origin menus, which supports stronger pricing for brands that keep familiar flavors, toppings, and tea bases at the center of the offer. Operators that present clear cultural identity and recognizable ingredient cues are in a better position to defend traffic as more chains expand nationally. For the United States bubble tea market, this means demand is being supported by broader cultural familiarity rather than a short novelty cycle.

Rising Demand Among Gen Z and Millennials

The United States bubble tea market is drawing from 2 consumer groups that buy for different reasons, and that difference is shaping menus and promotions. Many millennials still treat the drink as a premium indulgence and return to trusted chains and classic formats. Gen Z is more responsive to visually distinctive drinks, limited editions, and products that fit social content and collectible behavior. Kung Fu Tea used that pattern in December 2025 with its Pokémon collaboration and again in March 2026 with its Care Bears launch, both of which tied beverage demand to entertainment properties and repeat store visits. This is pushing the United States bubble tea market toward a menu structure that balances permanent core drinks with a steady stream of temporary releases.

Expansion of Bubble Tea Franchise Chains

The United States bubble tea market is in a phase where franchise growth is shifting from coastal concentration to wider national rollout. Gong cha brought 170 U.S. store territories in-house across 13 states in March 2026 and linked that move to its goal of building 1,000 U.S. locations over time. Chatime also entered Nevada in June 2026 with 6 Las Vegas locations planned, which adds another brand to the Mountain West buildout. Kung Fu Tea had already moved beyond a simple beverage format in June 2025 by opening KFT Marketplace in Chester, New York, where boba sits beside Taiwanese fried chicken and Japanese ramen in one food hall setting. As more operators pursue direct franchising, larger-format stores, and first-state entries, the United States bubble tea market is becoming easier to scale across regions that were once secondary to the West Coast and Northeast.

Product Innovation in Flavors and Ingredients

The United States bubble tea market is moving ahead through product refreshes as much as through unit growth. Kung Fu Tea entered functional beverages in February 2026 with HYDRATION+ Immunity, which blended tea flavors with supplement positioning and expanded distribution through Amazon and ADVANCED.gg. HTeaO widened consumer exposure to matcha in March 2026 by launching a 3-drink matcha lineup across all 150+ U.S. locations. Oversized canned formats that can carry pearls are also opening a path into broader retail shelf space, which supports ready-to-drink growth beyond specialty outlets. This keeps the United States bubble tea market tied to fast-moving flavor cycles, new beverage functions, and new usage occasions instead of a fixed core menu alone.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Sugar Content Concerns | -1.4% | National, with heightened scrutiny in California and New York | Medium term (2-4 years) |

| Growing Competition from Health-Oriented Beverage Alternatives | -0.9% | National | Medium term (2-4 years) |

| Premium Pricing Compared to Traditional Beverages | -0.6% | National, more pronounced in lower-income suburban and rural markets | Short term (≤ 2 years) |

| Volatility in Raw Material Costs | -0.5% | Global sourcing concentration, impact felt most by smaller U.S. operators | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Sugar Content Concerns

The United States bubble tea market is facing a more structured health challenge because sugar content is moving from a consumer awareness issue into a regulatory and institutional one. A March 2026 article that reviewed peer-reviewed evidence noted that typical bubble tea servings contain 20-50 g of sugar, which puts many drinks near or above the level of a standard cola can. New York City’s Department of Health treats added sugar as a public health issue and highlights sugary beverages as a concern in diet quality[1]Source: New York City Department of Health and Mental Hygiene, “Nutrition, Added Sugars,” New York City Department of Health and Mental Hygiene, nyc.gov. The FDA’s updated healthy nutrient content claim, effective from 2025, also tightens the standard around products that want to lean on a health-oriented message in retail. This makes reformulation important, but it also creates risk because too much sugar reduction can change the taste profile that supports repeat purchasing in the United States bubble tea market.

Volatility in Raw Material Costs

The United States bubble tea market is also exposed to a supply-side issue through its dependence on imported tapioca inputs. Thai tapioca starch prices reached USD 490/tonne in Q1 2026, while Thai factory utilization was only 62% because of raw cassava shortages and related supply pressures. Since April 2025, cassava chip prices in Thailand and Vietnam rose more than 30% cumulatively in a single quarter, which kept export pricing under pressure through mid-2026. Larger chains can buffer part of that volatility through sourcing scale and forward purchasing, but smaller operators have less room to absorb it. That cost gap can push the United States bubble tea market toward faster consolidation if franchise systems keep widening their procurement advantage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Base Ingredient Type: Plant-Based Formats Test Milk’s Stronghold

Milk-based formulations held 78.48% of the United States bubble tea market share in 2025, which keeps this segment at the center of volume generation across chains and independent outlets. Its lead reflects how deeply dairy and creamer-based recipes are built into training systems, sourcing routines, and consumer expectations around classic pearl milk tea and taro milk tea. These products still represent the most familiar entry point for many buyers, and that familiarity helps chains maintain order consistency across locations. The scale of the milk-based segment also gives operators a stable base from which they can trial seasonal or premium menu additions without changing the core offer.

The plant-based segment is projected to grow at a 10.67% CAGR through 2031, which makes it the faster-moving side of the United States bubble tea industry. Growth is being shaped by more than a simple health preference because non-dairy bases now signal menu completeness in many urban beverage concepts. Brands that allow oat, almond, or coconut substitutions without operational friction are better aligned with current ordering behavior. This creates a two-track structure in the United States bubble tea market, where milk-based formats keep the largest volume base while plant-based formats carry a larger share of premium and incremental growth.

By Tea Type: Black Tea Anchors Volume While Green Tea Captures Growth

Black tea held 38.72% share in 2025 and remained the largest tea base in the United States bubble tea market because it underpins classic pearl milk tea and Thai milk tea. According to the Beverage Industry Magazine data from 2025, U.S. canned and bottled tea dollar sales were essentially flat at approximately USD 4.8 billion[2]Source: Beverage Industry Magazine, "2025 State of the Beverage Industry: Tea market sees sales up, volume declines", bevindustry.com. The segment benefits from broad supply availability, strong familiarity, and easy pairing with both creamy and fruit-forward profiles. That combination keeps black tea central to the core menu architecture of most chains. It also gives operators a reliable base for scaled production when speed and flavor consistency matter.

Green tea is projected to expand at an 11.02% CAGR through 2031, which makes it the strongest growth engine within tea type. HTeaO widened the addressable audience for matcha in March 2026 by rolling out 3 matcha beverages nationally across more than 150 stores. That move shows how green tea flavors are moving beyond specialist boba shops into broader tea-led concepts. In the United States bubble tea industry, this supports a more premium and visually distinctive menu mix while black tea continues to anchor everyday order volume.

By Packaging Form: Aluminium Cans Redefine the Retail Opportunity

PET/glass bottles accounted for 48.62% of the United States bubble tea market size in 2025, which left them as the leading packaging format for ready-to-drink products. Their advantage comes from visual presentation because layered colors and visible pearls support the category’s merchandising appeal. This format is also familiar to specialty grocery and convenience buyers that already stock imported or niche packaged beverages. As a result, PET and glass still provide the clearest bridge between café-led demand and retail shelf presence.

Aluminium cans are forecast to grow at an 11.25% CAGR through 2031, giving them the strongest packaging momentum in the United States bubble tea market. Cans fit mainstream shelf layouts more easily, move through distribution with less handling complexity, and align with a convenience-led purchase occasion. Oversized can designs also help brands package pearls in a format that works better for broader retail channels. For packaged products, the FDA’s labeling framework on added sugars makes compliance and front-panel positioning more important as brands push deeper into mass retail[3]Source: U.S. Food and Drug Administration, “FDA Finalizes Updated Healthy Nutrient Content Claim,” U.S. Food and Drug Administration, fda.gov.

By Distribution Channel: Foodservice Leads as Retail Closes the Gap

Foodservice captured 56.78% share in 2025 and remained the leading distribution channel in the United States bubble tea market because made-to-order drinks still depend on in-store preparation and customization. Sweetness, ice level, toppings, and tea base choice give the foodservice channel an experience advantage that ready-to-drink formats do not fully replicate. The ongoing store rollout by national chains reinforces that lead. Gong cha’s direct expansion push and Kung Fu Tea’s 440+ location base show how physical presence still matters to traffic capture and repeat purchasing.

Retail is projected to grow at a 10.95% CAGR through 2031, which makes it the faster-moving route in the United States bubble tea market. Ready-to-drink expansion, delivery familiarity, and at-home consumption are all helping the channel close part of the gap with foodservice. Retail also offers a lower-commitment entry path for overseas brands that want shelf visibility before a full franchise rollout. This gives the United States bubble tea market a broader demand base because growth can now come from both destination beverage trips and routine packaged beverage purchases.

Geography Analysis

California represented the clearest anchor state for the United States bubble tea market in 2026, and the draft base showed that it accounted for 15.4% of national bubble tea store presence. That position reflects the state’s deep Asian food culture, large urban centers, and long-standing openness to Taiwanese and broader East Asian beverage formats. Florida also stood out as an important state because its metropolitan growth and younger consumer base support strong beverage experimentation. Together, these states show how the United States bubble tea market still relies on large, diverse, and high-traffic urban regions to set volume direction.

The next wave of expansion is moving through the Southeast and the Mountain West. Gong cha’s March 2026 transaction covered 13 states, including Texas, Florida, North Carolina, South Carolina, and Georgia, which shows where organized franchise growth is being prioritized. The company had already added first-state agreements in Milwaukee, Portland in Maine, and Nashville in October 2025, which confirmed that its U.S. buildout is extending beyond established coastal clusters. Chatime then entered Nevada in June 2026 with plans for 6 Las Vegas locations, adding another signal that leisure and tourism-heavy markets are moving onto the map. In the United States bubble tea market, this regional broadening matters because it shifts future demand away from a small set of gateway geographies.

Midsize cities, suburban corridors, and campus-linked locations are also becoming more relevant to the United States bubble tea market. The draft highlighted university-area and secondary-city openings as evidence that demand can build outside large coastal enclaves when brands target younger consumers at the point of routine social spending. That pattern supports a more distributed growth map, where awareness is not limited to places with the highest Asian population density. It also means operators may need more flexible pricing and store formats as the United States bubble tea market moves into secondary trade areas with different traffic, rent, and spending conditions.

Competitive Landscape

The United States bubble tea market remains semi-consolidated, and the draft indicated that no single brand controls more than 5% of national share. Kung Fu Tea, Gong cha, Chatime, CoCo Fresh Tea and Juice, and Sharetea are the most visible multi-location operators within this field. The competitive structure still favors scale building rather than scale defense, which is why footprint growth and operating systems matter so much. In the United States bubble tea market, brands are still trying to secure durable national presence rather than protect an already concentrated position.

Gong cha’s March 2026 move to acquire master franchise rights for 170 U.S. stores was one of the clearest strategic actions because it shifted the company toward a direct-to-franchisee model and tighter control over execution. Kung Fu Tea took a different path in February 2026 when it entered functional beverages through HYDRATION+ Immunity, which widened the brand beyond standard indulgence-led positioning. It had also opened KFT Marketplace in June 2025, which tested a broader Asian dining format instead of a single-product beverage store. Chatime’s June 2026 Nevada debut added another example of market entry through first-state rollout rather than densification of existing hubs. These moves show that the United States bubble tea market is being shaped by distinct playbooks around franchising, format expansion, and product adjacency.

Competitive pressure is also rising from Chinese tea brands that are entering the United States with faster flavor cycles, stronger digital marketing habits, and investor backing familiar with a highly competitive domestic tea environment. That pressure narrows the room for slower-moving legacy operators that rely only on store openings without strong menu refreshes. At the same time, smaller challengers still have room to differentiate through brewing methods, premium ingredients, or suburban convenience-oriented formats. The result is a United States bubble tea market where operating scale helps, but brand relevance and menu pace still determine who can convert expansion into repeat demand.

United States Bubble Tea Industry Leaders

-

Kung Fu Tea

-

Gong cha

-

CoCo Fresh Tea and Juice

-

Boba Guys

-

Bubbles Tea and Juice Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Chatime debuts in Nevada with 6 Las Vegas locations planned. Chatime, one of the world's largest bubble tea brands with 1,400+ global locations, opened its first Nevada store near UNLV and announced expansion to a second Arts District location, marking a significant entry into the Mountain West region.

- June 2026: Kung Fu Tea partners with Red Bull for World Cup-themed "Fearless Infusions" lineup. Kung Fu Tea launched a co-branded summer collaboration with Red Bull across all US locations from June 1-July 24, 2026, introducing 3 soccer-themed drinks with collectible packaging and a consumer sweepstakes, targeting the FIFA World Cup audience to drive incremental footfall.

- February 2026: Kung Fu Tea launches HYDRATION+ Immunity functional beverage line. Kung Fu Tea partnered with supplement brand ADVANCED® to launch a functional wellness beverage line blending tea flavors with immunity supplements, distributed via Amazon and ADVANCED.gg, marking the brand's first move into the functional beverage segment.

United States Bubble Tea Market Report Scope

| Milk-based |

| Plant-based |

| Black Tea |

| Green Tea |

| Oolong Tea |

| Other Types (Herbal Tea, Floral Tea, Specialty Blends) |

| PET/Glass Bottles |

| Aluminium Cans |

| Pouches and Sealed-Cup Packaging |

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Channels | |

| Other Distribution Channels |

| By Base Ingredient Type | Milk-based | |

| Plant-based | ||

| By Tea Type | Black Tea | |

| Green Tea | ||

| Oolong Tea | ||

| Other Types (Herbal Tea, Floral Tea, Specialty Blends) | ||

| By Packaging Form | PET/Glass Bottles | |

| Aluminium Cans | ||

| Pouches and Sealed-Cup Packaging | ||

| By Distribution Channel | Foodservice | |

| Retail | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Channels | ||

| Other Distribution Channels | ||

Key Questions Answered in the Report

What is the forecast value of the United States bubble tea market by 2031?

The United States bubble tea market is projected to reach USD 857.25 million by 2031, up from USD 511.48 million in 2026, at a CAGR of 9.82%.

Which segment leads by base ingredient type in the United States bubble tea space?

Milk-based formulations led with 78.48% share in 2025, which shows that classic dairy and creamer-based drinks still anchor order volume.

Which tea type is growing fastest in the United States bubble tea market?

Green tea is the fastest-growing tea type with an 11.02% CAGR through 2031, while black tea remained the largest tea base at 38.72% share in 2025.

How competitive is the United States bubble tea business today?

The market is semi-consolidated, with the draft indicating that no single brand controls more than 5% of national share, even though chains such as Kung Fu Tea, Gong cha, and Chatime are expanding actively.

Page last updated on: