Iced Tea Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 61.47 Billion |

| Market Size (2031) | USD 76.25 Billion |

| Growth Rate (2026 - 2031) | 4.41% CAGR |

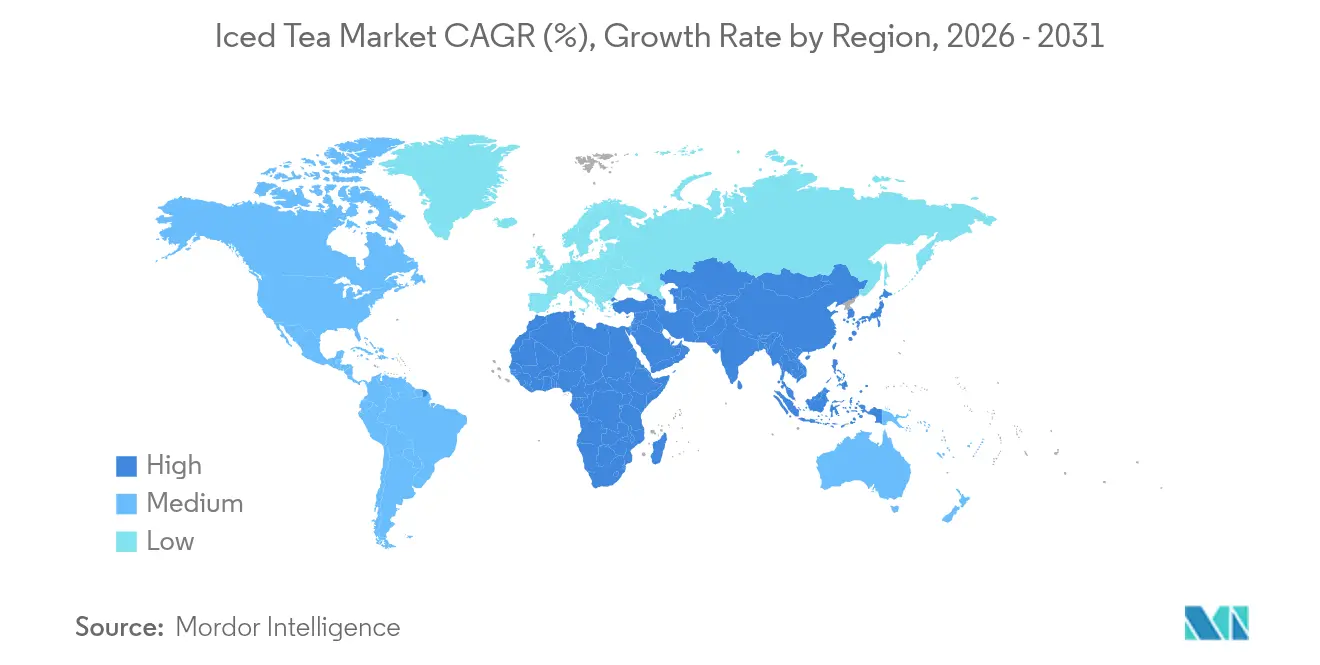

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

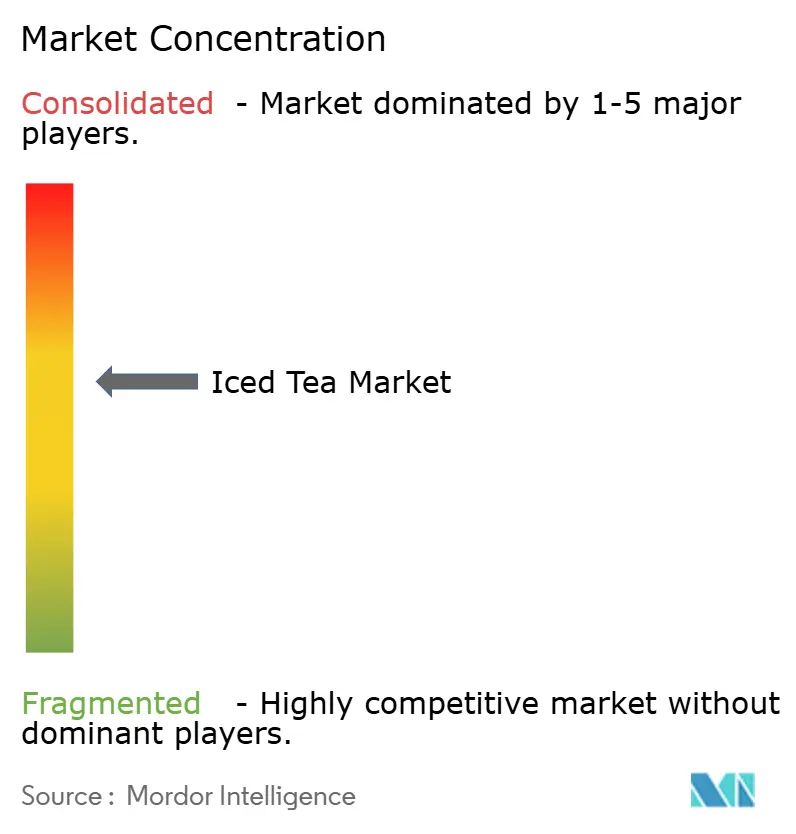

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Iced Tea Market Analysis by Mordor Intelligence

The iced tea market size was valued at USD 58.87 billion in 2025 and estimated to grow from USD 61.47 billion in 2026 to reach USD 76.25 billion by 2031, at a CAGR of 4.41% during the forecast period (2026-2031). This growth is driven by increasing health awareness and a shift toward healthier drinks as people move away from carbonated soft drinks. North America leads the market, while Asia-Pacific is the fastest-growing region. Under the format options, ready-to-drink iced tea is the most popular, but powder/premix options are becoming more popular due to their convenience and customization. Flavored iced tea is the preferred choice, but unflavored options are gaining attention as consumer preferences change. By product type, black iced tea has the largest market share in 2024, while herbal iced tea is growing the fastest because of its health benefits. Similarly, PET bottles are the most commonly used packaging, but TetraPacks packs becoming more popular due to their eco-friendly and premium appeal. Most sales happen through off-trade channels, but on-trade sales are increasing. Drive-thru beverage concepts are also becoming a key trend, catering to consumers looking for convenience. The market is moderately competitive, with large multinational companies such as PepsiCo Inc., Nestlé SA, AriZona Beverages USA, among others, competing alongside smaller regional players.

Key Report Takeaways

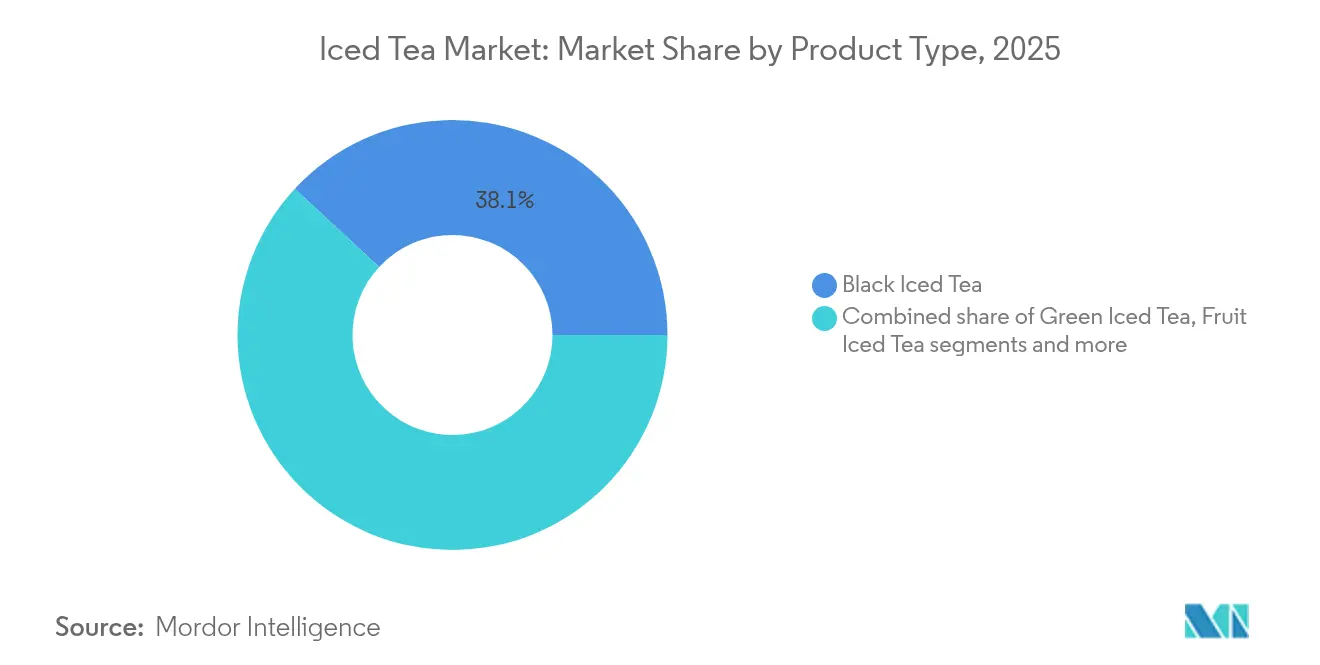

- By product type, black iced tea held a 38.10% share of the iced tea market in 2025, while herbal iced tea is projected to record a 6.04% CAGR between 2026 and 2031.

- By form, ready-to-drink formats captured 78.60% of the iced tea market share in 2025, yet powder/premix is expected to expand at a 5.38% CAGR through 2031.

- By flavor profile, flavored variants accounted for 75.15% of 2025 sales in 2025; however, unflavored options are forecast to register a 6.18% CAGR to 2031.

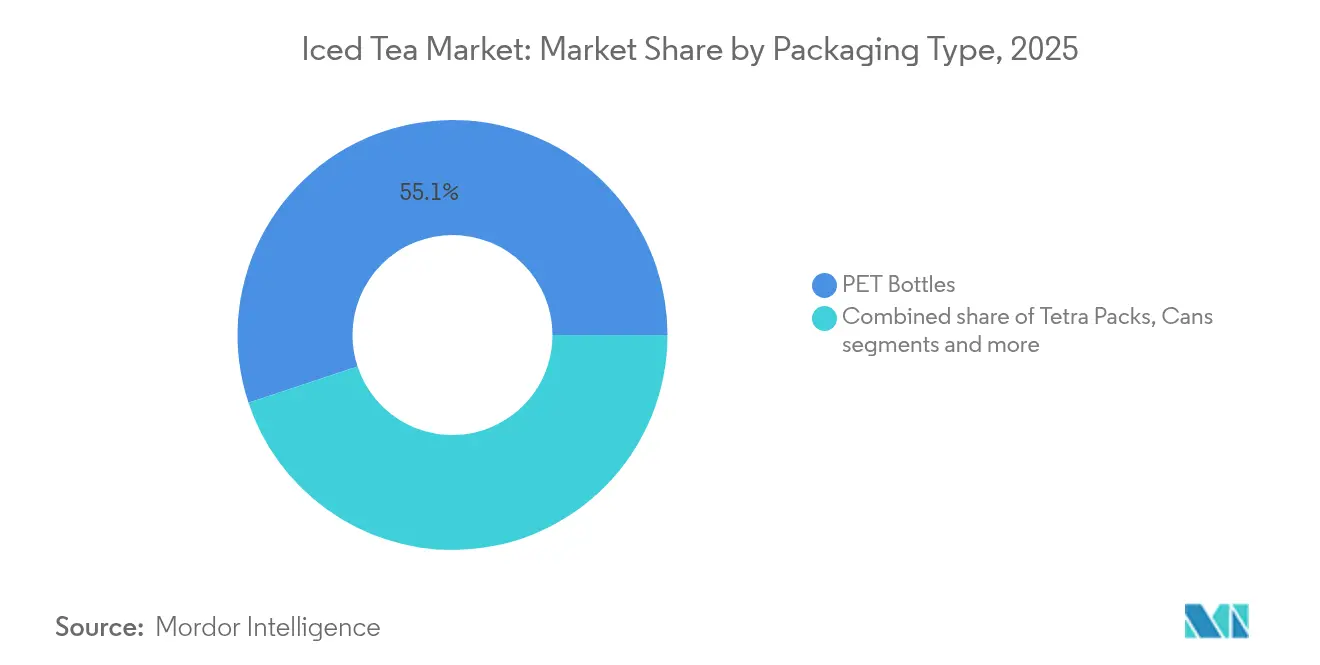

- By packaging type, PET bottles dominated with 55.10% revenue in 2025, yet tetra packs are predicted to advance at a 5.83% CAGR over the outlook period.

- By distribution channel, off-trade outlets contributed 81.95% of 2025 volume, while on-trade is set to grow at a 7.32% CAGR through 2031.

- By geography, North America accounted for 44.20% of 2025 sales in 2025; yet, Asia-Pacific is forecast to register a 7.14% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Iced Tea Market Trends and Insights

Drivers Impact Table*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising preference for healthier alternative to carbonated soft-drinks | +1.2% | Global, with strongest adoption in North America and Europe | Medium term (2-4 years) |

| Continuous flavor innovation and line extensions | +0.8% | Global, led by Asia-Pacific innovation hubs | Short term (≤ 2 years) |

| Convenience and on-the-go consumption | +0.6% | North America and Asia-Pacific urban centers | Short term (≤ 2 years) |

| Premiumisation and clean-label positioning | +0.5% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Indulgence of social media and collaboration | +0.4% | Global, youth-focused markets | Short term (≤ 2 years) |

| Increasing awareness of sustainability and ethical sourcing | +0.3% | Europe and North America, spreading globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising preference for healthier alternatives to carbonated soft drinks

The iced tea market is expanding as more people prioritize healthier beverage options. Consumers are increasingly moving away from sugary sodas and choosing tea-based drinks that are refreshing, lower in calories, and often come with added health benefits. In 2024, a report by the International Bottled Water Association revealed that 69% of Americans prefer convenient and healthy packaged drinks over sodas[1]Source: International Bottled Water Association, "Water Drinkers’ Love for Bottled Water is Stronger Than Ever, Survey Finds", bottledwater.org. Similarly, a 2024 International Food Information Council (IFIC) survey found that 62% of consumers consider health a key factor when purchasing beverages[2]Source: International Food Information Council, "2024 IFIC Food and Health Survey", ific.org. This growing focus on health has led to a rise in demand for low-sugar, functional, and clean-label iced teas. To meet this demand, many brands are introducing products enriched with vitamins, probiotics, and natural extracts like herbs and botanicals, which appeal to wellness-focused buyers. These innovations are making iced tea a popular and attractive choice in the market.

Convenience and on-the-go consumption

Busy lifestyles are driving the growing demand for convenient, ready-to-drink iced tea options, making packaging and accessibility crucial factors in the market's growth. With a global employment rate of 95.1% as of April 2025, as reported by the Organisation for Economic Co-operation and Development (OECD), many consumers are constantly on the move and prefer beverages that are quick and easy to carry[3]Source: Organisation for Economic Co-operation and Development, "Employment Rate", oecd.org. Single-serve bottles with resealable caps and drive-thru options are becoming increasingly popular to meet this need for convenience. For instance, in January 2025, Rosenberger’s introduced its iced tea and lemonade and new energy iced teas in 12-oz cans. These products not only offer portability and classic flavors but also provide a caffeine boost of 120–180 mg per can, catering to consumers looking for both refreshment and energy. This focus on convenient packaging, functional benefits strategies is contributing to the steady growth of the global ready-to-drink iced tea market.

Continuous flavor innovation and line extensions

Flavor innovation and strategic product expansions are driving growth in the iced tea market. Brands are moving beyond traditional flavors like lemon and peach to more complex combinations that include botanicals and dairy-free creamers, offering a premium and unique taste experience. For instance, Keurig Dr Pepper introduced snapple peach tea and lemonade in March 2025, blending tea with lemonade flavors to attract consumers looking for variety. Similarly, in February 2024, Tilray launched two cold brew iced teas, peach cranberry and wildberry hibiscus, under its Solei wellness brand. These products cater to the growing demand for functional beverages that promote wellness. With the help of introducing innovative flavors and functional benefits, brands are positioning themselves to charge premium prices, further boosting market growth.

Premiumization and clean-label positioning

The iced tea market is growing due to the rising demand for premium and sustainable products. In 2024, a report by Pubonline Informs Org revealed that 80% of global consumers are willing to pay more for eco-friendly options[4]Source: PubsOnLine Informs Org, "The Price Dilemma in Sustainable Products: A Barrier to Adoption", pubsonline.informs.org. This trend is supported by new regulations like the USDA’s Strengthening Organic Enforcement (SOE) rule, introduced in March 2024, which ensures stricter organic certification and better product traceability. Similarly, the European Union’s Organic Regulation (EU) 2018/848 enforces strict rules on organic labeling, supply chain transparency, and environmental sustainability. Players in the market are responding to such changes and offering products that align with these dynamics. For instance, Wild Orchard Tea offers its Regenerative Organic Certified range, reflecting the growing interest in environmentally friendly and health-focused products. These consumer preferences and new regulations are pushing the iced tea market toward being more sustainable, authentic, and high-quality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense competition from other healthy beverages | -0.7% | Global, particularly in developed markets | Short term (≤ 2 years) |

| Sugar-reduction regulations raising reformulation costs | -0.5% | North America and Europe, expanding globally | Medium term (2-4 years) |

| Regulatory and labelling compliance | -0.4% | Global, with varying regional requirements | Medium term (2-4 years) |

| Potential caffeine sensitivity concerns | -0.3% | Global, health-conscious demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sugar-reduction regulations raising reformulation costs

Sugar-reduction regulations are slowing the growth of the global iced tea market by increasing reformulation costs. In the United States, the Food and Drug Administration's (FDA's) proposed front-of-pack labeling rule, set to take effect in 2025, will require manufacturers to clearly label added sugars on their products. This change is pushing companies to accelerate reformulation efforts and invest heavily in research and development to comply with these new standards. Moreover, the 2024 International Food Information Council (IFIC) survey reveals that 66% of American consumers are actively trying to reduce their sugar intake this year, further pressuring producers to lower sugar content in their products. To address these challenges, companies are turning to alternative sweeteners and texture enhancers to maintain the taste and quality of their iced teas. However, this shift also requires renegotiating supply contracts due to reduced use of traditional white sugar.

Intense competition from other healthy beverages

The iced tea market is facing increasing competition from health-focused beverages like kombucha, cold-pressed juices, and protein waters, which are popular among health-conscious consumers. This has made the market more crowded and competitive. Private-label products that offer premium quality at lower prices are adding to the pricing challenges for established brands. At the same time, new and innovative drinks that combine hydration, vitamins, and energy have raised consumer expectations for beverages that provide multiple benefits. As a result, iced tea brands are being pushed to invest in improved formulations that not only maintain great taste but also deliver added value to meet these demands. Iced tea brands must prioritize innovation and develop clear, compelling branding strategies to stand out and retain customer loyalty in this challenging environment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Herbal Innovation Expands Category Headroom

Black iced tea accounted for 38.10% of total sales in 2025, mainly due to its well-known health benefits, such as supporting immunity, and its status as a traditional and trusted beverage. Its familiar taste and versatility make it a go-to choice for a wide range of consumers. Black iced tea is often used as a base for flavored variants, which further boosts its popularity. The introduction of innovative blends, such as fruit-infused black teas, has also attracted younger consumers looking for refreshing and unique options. This balance between classic appeal and modern innovation has helped black iced tea maintain its strong position in the market.

Herbal iced teas are expected to grow at a CAGR of 6.04% from 2026 to 2031, driven by the increasing demand for beverages that offer functional health benefits. These teas often include ingredients like adaptogens (e.g., ashwagandha) and digestive aids (e.g., ginger), which appeal to health-conscious consumers seeking natural remedies. The growing focus on holistic wellness has positioned herbal iced teas as a premium product category, allowing brands to target niche markets and charge higher prices. Their association with relaxation and stress relief makes them particularly attractive in today’s fast-paced lifestyle.

By Form: Powder/Premix Builds Customization Appeal

Ready-to-drink iced tea formats accounted for 78.60% of the market share in 2025, primarily due to their convenience and widespread availability. These products are pre-packaged and ready for immediate consumption, making them highly appealing to busy consumers. Strong brand recognition and extensive distribution networks have further solidified their dominance in the market. Concentrate syrups, on the other hand, continue to be popular in foodservice operations, especially in high-traffic areas like restaurants and cafes. These syrups offer efficiency and cost-effectiveness, allowing businesses to prepare large quantities of iced tea quickly while maintaining consistent quality.

Powder/Premix iced tea products are expected to grow at a CAGR of 5.38% through 2031, driven by their convenience and customization options. These products are particularly popular among consumers who prefer to adjust the strength and sweetness of their beverages. The lightweight nature of powder and premix formats also makes them cost-effective for transportation and storage, and their longer shelf life has encouraged manufacturers to expand their offerings, including single-serve sachets and multi-serve pouches. This trend is attracting both established brands and new entrants looking to cater to the growing demand for customizable and portable beverage solutions.

By Flavor Profile: Rising Sophistication Favors Unflavored SKUs

Flavored iced tea accounted for 75.15% of the market revenue in 2025, driven by strong consumer demand for popular flavors like peach, lemon, and other tropical blends. Seasonal and limited-edition flavors have been particularly successful in attracting customers, especially in convenience stores where impulse purchases are common. These flavored options appeal to a broad audience, including younger consumers and those seeking refreshing, ready-to-drink beverages. Brands are utilizing innovative flavor combinations and marketing campaigns to maintain consumer interest and expand their customer base. The availability of flavored iced tea in various packaging formats, such as PET bottles and cans, further supports its widespread adoption.

Unflavored iced teas are projected to grow at a CAGR of 6.18% through 2031, as more consumers gravitate toward beverages with minimal processing and natural flavors. This trend aligns with the growing clean-label movement, where buyers prioritize products with fewer ingredients and transparent sourcing practices. Unflavored iced tea appeals to health-conscious individuals who prefer beverages without added sugars or artificial flavors. The rise in single-origin tea sourcing and premium tea leaves has contributed to the increasing demand for unflavored variants. These products are gaining traction as they cater to a niche but expanding segment of consumers seeking authenticity and wellness-focused options.

By Packaging Type: Tetra Packs Anchor Sustainability Narrative

PET bottles accounted for 55.10% of the market revenue in 2025, primarily due to their affordability, widespread recycling infrastructure, and familiarity among consumers. These bottles are lightweight, durable, making them a preferred choice for manufacturers and consumers alike. Cans remain popular in convenience stores, driven by the growing demand for sustainable and innovative packaging options that appeal to environmentally conscious consumers. PET bottles continue to dominate because they strike a balance between cost-effectiveness and recyclability, ensuring their relevance in the market.

Tetra Packs are expected to grow at a CAGR of 5.83% during the forecast period, driven by their eco-friendly design and lower environmental impact. These cartons are made from renewable materials and have a smaller carbon footprint compared to other packaging types, aligning with sustainability goals set by retailers and foodservice providers. Tetra Packs support aseptic filling processes, which allow for preservative-free iced tea products, catering to the rising demand for clean-label beverages. Their lightweight and compact design also makes them convenient for storage and transportation, further boosting their appeal in both retail and foodservice channels.

By Distribution Channel: On-Trade Rebound Unlocks Experience-Led Value

Off-trade channels, such as supermarkets/hypermarkets, contributed 81.95% of the iced tea volume in 2025. These channels remain dominant due to their widespread availability and convenience for consumers. The rise of omnichannel grocery models, which combine online and in-store shopping experiences, has further strengthened this segment. While online grocery shopping grew significantly after the pandemic, it has complemented rather than replaced traditional in-store purchases. Consumers continue to rely on physical stores for immediate purchases and to explore a variety of options, making off-trade channels a critical part of the market's distribution network.

On-trade channels are expected to grow at a CAGR of 7.32% through 2031. This growth is driven by the resurgence of café culture and the increasing popularity of quick-service restaurants focused on beverages. Many foodservice operators are introducing innovative menu options, such as customized iced tea brews and craft-style presentations, to attract customers and differentiate themselves from packaged products. These offerings not only enhance the customer experience but also allow businesses to generate higher margins on non-alcoholic beverages.

Geography Analysis

North America dominated the iced tea market in 2025, accounting for 44.20% of the total value sales. This growth is attributed to the region's extensive retail network, strong consumer trust in ready-to-drink (RTD) brands, and a well-established cold chain distribution system. Regulatory measures, such as the standardized labeling deadline set for January 2028, provide clarity for businesses to plan ahead but may challenge smaller companies in adapting quickly. With most households already consuming iced tea, major brands are now focusing on premium offerings like organic and functional-enhanced products to sustain growth in this mature market.

Asia-Pacific is expected to grow at a 7.14% CAGR through 2031, fueled by a strong cultural connection to tea and the growing popularity of café culture. Younger consumers, particularly in China, prioritize factors like authenticity, social media appeal, and product traceability, which are accelerating the growth of premium iced tea segments. The region benefits from its proximity to major tea-producing countries like China and India, which provide cost advantages and ensure fresher products. These factors are helping local brands expand their presence in both domestic and export markets.

Europe, South America, and the Middle East and Africa are emerging as key regions for market expansion. In Europe, strict regulations on sustainability and sugar content are pushing brands to highlight eco-friendly practices and low-calorie options. South America is utilizing its favorable climate to produce high-quality black and herbal teas for export, while domestic consumption is gradually shifting from traditional beverages like maté and coffee to ready-to-drink iced teas, especially among younger, on-the-go consumers. Meanwhile, urbanization and improving cold-chain infrastructure in the Middle East and Africa are creating opportunities for multinational brands to enter the market, catering to the increasing demand for convenient and refreshing beverages.

Competitive Landscape

The iced tea market shows moderate competition, with the top five players accounting for a valuable share of the retail value in 2024. This indicates a moderately consolidated market. Large beverage companies dominate by offering diverse product portfolios, including juices, sports drinks, and sparkling waters, which they use to cross-promote and strengthen their distribution channels. For instance, PepsiCo and Unilever jointly manage Lipton, leveraging their manufacturing scale and marketing expertise. Similarly, Coca-Cola has revitalized its FUZE brand, utilizing its extensive foodservice distribution network to expand its reach and appeal to consumers.

Strategic mergers and acquisitions continue to shape the market. A notable example is Tata Consumer Products’ acquisition of Organic India in January 2024, which enhanced its capacity for certified herbal products and allowed it to tap into global wellness markets. Vertical integration strategies, such as this, help companies reduce supply chain risks while supporting claims of product traceability, which is increasingly important to consumers. Partnerships with technology providers, like Tetra Pak’s Factory Sustainable Solutions, are helping beverage companies reduce operational emissions and meet carbon-neutral goals, fostering long-term supplier relationships and sustainability commitments.

Emerging brands are disrupting the market by focusing on direct-to-consumer (DTC) subscription models and limited-edition product launches, which resonate with tech-savvy and younger consumers. Collaborations with influencers from industries like fashion and gaming, such as AriZona’s partnership with GOAT USA apparel in September 2024, are helping these brands build cultural relevance, particularly among Gen Z audiences. To succeed, companies must prioritize agile innovation, transparent environmental, social, and governance (ESG) practices, and omnichannel strategies that cater to retail stores and premium specialty outlets, ensuring they meet the diverse preferences of modern consumers.

Iced Tea Industry Leaders

-

The Coca Cola Company

-

Nestle SA

-

Keuring Dr Pepper Inc.

-

PepsiCo. Inc.

-

AriZona Beverages USA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Continental Coffee, recognized as one of India’s prominent beverage brands and a subsidiary of CCL Products (India) Limited, introduced a refreshing addition to its expanding portfolio, the Continental lemon iced tea premix. This product, which became available across India, marked the brand’s first consumer-facing entry into the tea segment.

- May 2025: Ready-to-drink tea brand Kaytea introduced a new range of instant iced tea powder products, aiming to bring ‘next generation hydration’ to the United Kingdom market. The powders were introduced in 3 flavors – Peach and Mango, Lemon, and Classic Milk Tea.

- February 2025: Keurig Dr Pepper launched Snapple Peach Tea and Lemonade as part of its efforts to expand its cold-beverage portfolio. This introduction was accompanied by several other innovative cold-beverage offerings, showcasing the company's commitment to catering to evolving consumer preferences for refreshing and diverse drink options.

- July 2024: Gulabs launched a new line of "Iced Tea Concentrate," offering customers a range of flavors. The new flavors included Lemon Iced Tea, Lemon Ginger Iced Tea, and Lemon Mint Iced Tea, all available in 200 ml glass bottles.

Global Iced Tea Market Report Scope

Iced tea is a cold beverage with different flavors, such as lemon, raspberry, lime, passion fruit, peach, orange, strawberry, and cherry.

The iced tea market is segmented based on product type, form, distribution channel, and geography. The market is segmented by product type into black iced tea, green iced tea, herbal iced tea, and others. The market is segmented by form into powder/premix and liquid/ready-to-drink. The market is segmented by distribution channel into supermarkets/ hypermarkets, convenience stores, online retail stores, and other retail distribution channels. By geography, the market is segmented by North America, Europe, Asia-Pacific, South America, the Middle East, and Africa.

The report offers the market size in value terms in USD for all the abovementioned segments.

| Black Iced Tea |

| Green Iced Tea |

| Herbal Iced Tea |

| Fruit Iced Tea |

| Other Product Types |

| Ready-to-Drink |

| Powder/Premix |

| Concentrate/Syrup |

| Unflavored |

| Flavored |

| PET Bottles |

| Tetra Packs |

| Cans |

| Other Packaging Types |

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Food-service and HoReCa | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Colombia | |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Product Type | Black Iced Tea | |

| Green Iced Tea | ||

| Herbal Iced Tea | ||

| Fruit Iced Tea | ||

| Other Product Types | ||

| By Form | Ready-to-Drink | |

| Powder/Premix | ||

| Concentrate/Syrup | ||

| By Flavor Profile | Unflavored | |

| Flavored | ||

| By Packaging Type | PET Bottles | |

| Tetra Packs | ||

| Cans | ||

| Other Packaging Types | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Food-service and HoReCa | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Colombia | ||

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the iced tea market in 2026?

The iced tea market size is USD 61.47 billion in 2026, with a forecast value of USD 76.25 billion by 2031.

Which form factor is growing fastest within iced tea?

Powder/Premix formats are projected to expand at 5.38% CAGR as consumers favor customization and portability.

Which product type is set to outpace others by 2031?

Herbal iced tea, boosted by adaptogenic and immune-supporting ingredients, is forecast to post a 6.04% CAGR over the outlook period.

What drives Asia-Pacific’s strong growth in iced tea market?

Rising disposable income, tea-centric culture, and expanding café chains underpin a regional CAGR of 7.14% through 2031.

Page last updated on: