Fruit Tea Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.74 Billion |

| Market Size (2031) | USD 2.29 Billion |

| Growth Rate (2026 - 2031) | 5.65% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

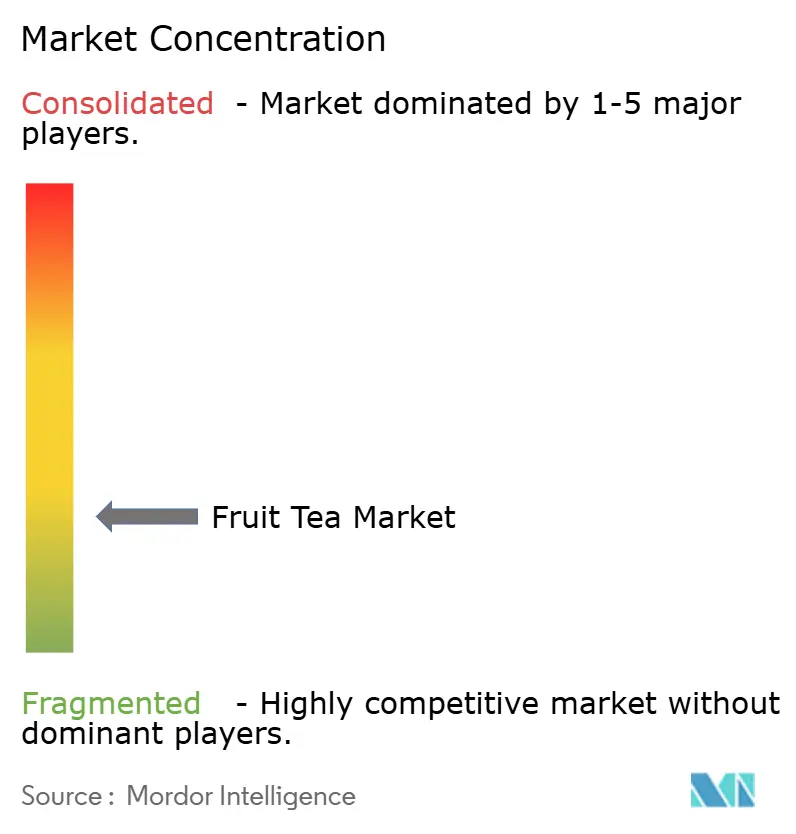

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fruit Tea Market Analysis by Mordor Intelligence

The fruit tea market size is expected to increase from USD 1.64 billion in 2025 to USD 1.74 billion in 2026 and reach USD 2.29 billion by 2031, growing at a CAGR of 5.65% over 2026-2031. The fruit tea market is moving forward because consumers are shifting away from sugary carbonated drinks and toward beverages that feel more natural and lighter in daily use. Regulatory attention around sugar reduction and functional beverage claims is also shaping the fruit tea market, which is pushing brands to tighten formulations, labels, and proof behind wellness positioning. The category remains resilient because fruit-infused teas serve hydration, flavor, and better-for-you consumption in one product, which helps demand hold up across different spending cycles. The fruit tea market also benefits from Asia-Pacific scale, North American premium demand, and faster online discovery of niche products, which together broaden the route to growth. Competitive pressure remains moderate to high in the fruit tea market, and brands with stronger sourcing, cleaner formulations, and wider omnichannel reach are better placed to manage raw material swings and shelf-life constraints.

Key Report Takeaways

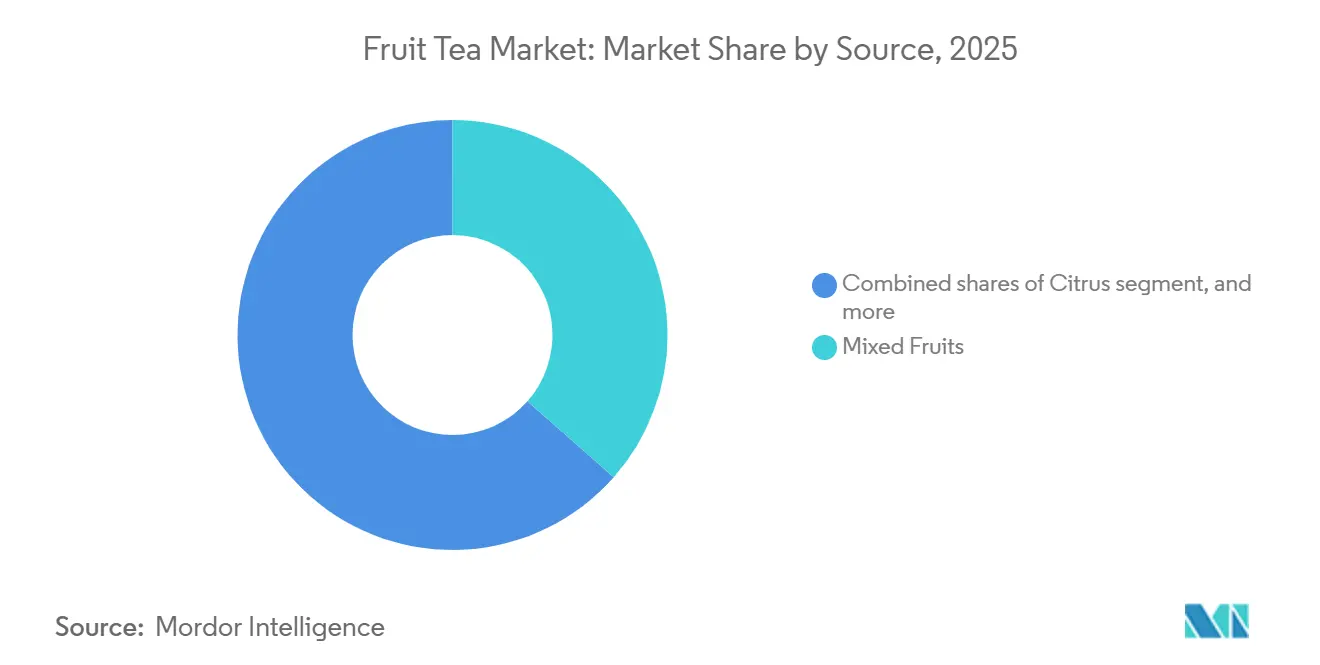

By source, Mixed Fruit held 36.50% of revenue in 2025, while the same segment is forecast to grow fastest at a 6.40% CAGR through 2031.

By form, tea bags led with a 70.01% share in 2025, while loose-leaf tea is projected to expand fastest at a 6.70% CAGR through 2031.

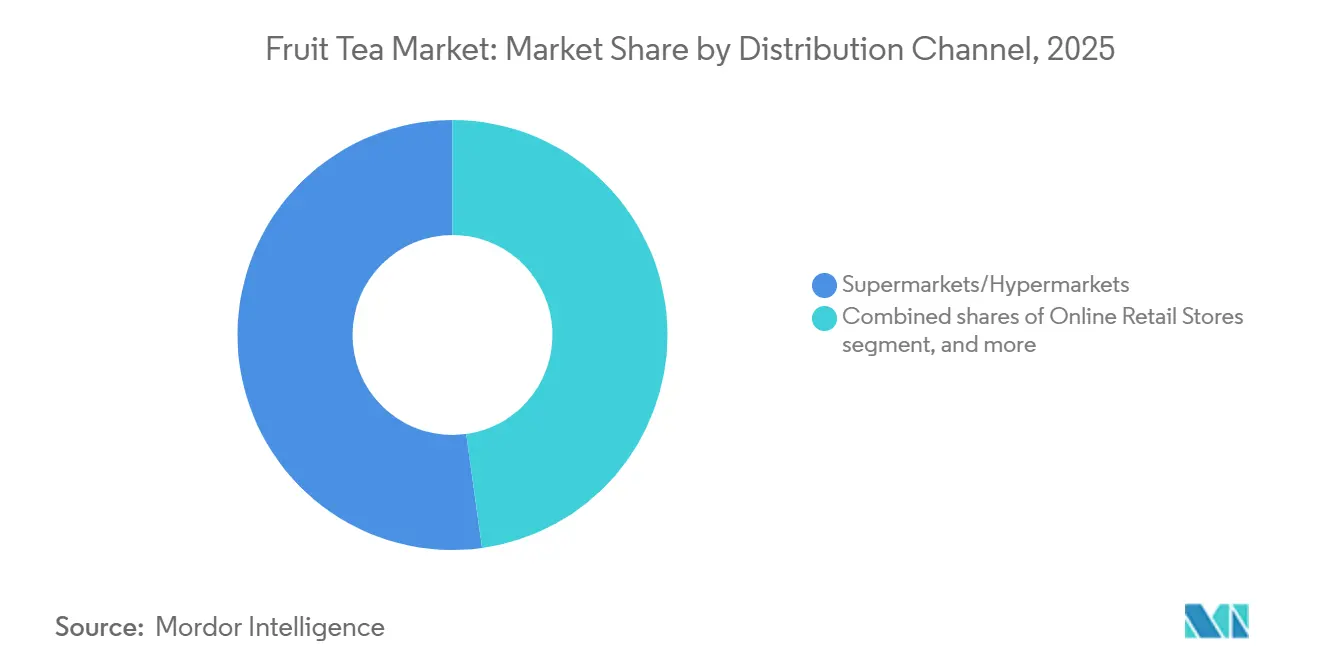

By distribution channel, supermarkets and hypermarkets accounted for 52.20% of sales in 2025, while online retail stores are expected to record the fastest growth at a 7.50% CAGR through 2031.

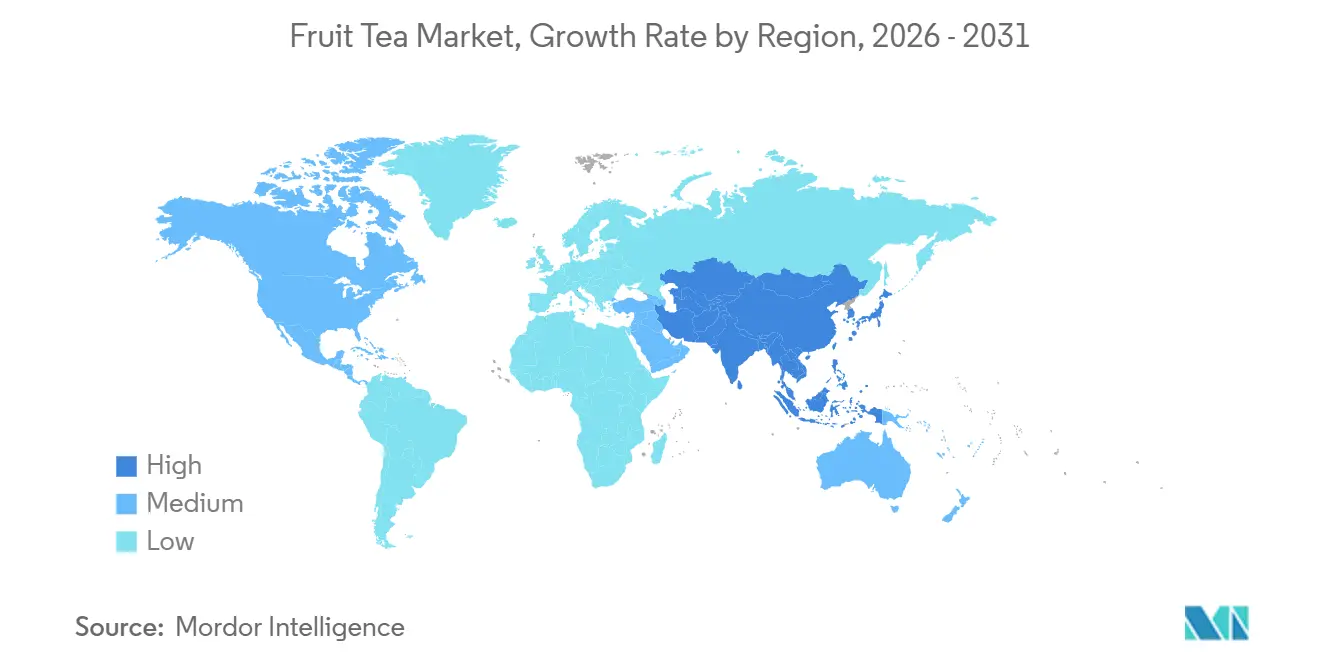

By geography, Asia-Pacific held 37.54% of global sales in 2025, while North America is forecast to post the fastest regional CAGR at 9.80% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fruit Tea Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health-and-wellness positioning of fruit-infused beverages | +1.4% | Global, with strongest pull in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Rising demand for caffeine-free and herbal fruit tea blends | +1.1% | North America, Asia-Pacific, with spillover to Europe | Short term (≤ 2 years) |

| E-commerce expansion into specialty tea SKUs | +0.8% | North America and Asia-Pacific core, with spillover to Europe | Medium term (2-4 years) |

| Product premiumization in Asia-Pacific | +0.7% | APAC core, including China, Japan, South Korea, and India | Long term (≥ 4 years) |

| Up-cycling of fruit by-products for “zero waste” teas | +0.4% | Europe and North America, with Asia-Pacific emerging | Long term (≥ 4 years) |

| Cross-category kombucha/fruit-tea hybrids | +0.5% | Global, with early gains in North America, the United Kingdom, and Southeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health-and-wellness positioning of fruit-infused beverages

The fruit tea market is gaining from a clearer health-led use case, not just a flavor trend. Consumers are giving more weight to low-sugar profiles, cleaner labels, and ingredients that appear closer to whole food and less processed beverage formats. That change matters because it shifts demand away from products built around sweetness and toward products that can justify repeat use through everyday wellness. Regulatory oversight in major markets is also making claims more disciplined, which favors brands that can support antioxidant, vitamin, or reduced-sugar positioning with cleaner formulations. This is widening the gap between brands with traceable ingredients and brands that depend on softer marketing language. The fruit tea market, therefore, has a stronger base when wellness, hydration, and moderate indulgence are presented together than as separate purchase reasons. For instance, according to Glanbia Nutritionals' 2025 report, over the past twelve months, more than a quarter of consumers globally purchased functional food and beverage products for gut health (28%), weight management (27%), and energy and stamina (26%) globally[1]Source: Glanbia PLC, "The Latest Trends in Functional Nutrition: Elevating Product Innovation", glanbianutrition.com.

Rising demand for caffeine-free and herbal fruit tea blends

The increasing demand for caffeine-free and herbal fruit tea blends is driven by growing consumer awareness of health and wellness. There is a rising preference for natural, organic, and functional beverages that provide benefits such as immunity support, digestion aid, and relaxation without caffeine. For example, a 2024 survey by Kerry Group plc revealed that Canadian consumers prioritize natural claims in beverages, defining clean-label products as free from artificial colors, flavors, or preservatives[2]Source: Kerry Group PLC, "How Consumers React to New Canadian Nutrition Symbol Regulation', kerry.com. Consumers are shifting from traditional tea and coffee to alternatives containing herbs like chamomile, peppermint, turmeric, ashwagandha, and ginger, which are associated with sleep support, stress relief, and overall well-being. Companies are responding to this trend with product innovations. In January 2025, Kaytea introduced electrolyte-infused whole-leaf teabags in four caffeine-free fruit flavors (Pineapple & Hibiscus, Peach & Green Tea, Lime & Mint, Lemon & Mate), all with zero sugar. The widespread availability of e-commerce platforms has further facilitated global access to creative blends and specialty caffeine-free options.

E-commerce expansion into specialty tea Stock Keeping Units (SKUs)

Digital retail is changing how the fruit tea market reaches niche demand pockets that physical shelf space often misses. Online channels give brands room to sell smaller collections, seasonal blends, and premium flavor mixes that would struggle in crowded mass retail assortments. This matters because fruit tea often wins on specific flavor combinations, ingredient stories, and repeat purchase behavior, all of which are easier to test and refine online. Subscription and auto-renewal models also improve visibility on repeat demand and reduce dependence on promotion-heavy store traffic. At the same time, the fruit tea market is seeing higher pressure around disclosure and subscription compliance, which can raise costs for smaller operators. Larger brands and well-funded specialists are in a stronger position because they can combine digital marketing, legal compliance, and fulfillment at scale.

Up-cycling of fruit by-products for "zero waste" Teas

Upcycled ingredients are creating a more distinct sustainability path in the fruit tea market. Research published in the Processes Journal in September 2025 showed that spray-dried kombucha powders flavored with grape and mango peel extracts retained high levels of phenolic compounds, which supports the case for functional use of fruit by-products[3]Source: MDPI, "Powdered Kombucha Flavored with Fruit By-Products: A Sustainable Functional Innovation,” mdpi.com. This matters because ingredient reuse can lower waste, support brand differentiation, and give manufacturers a clearer environmental story without leaving beverage use occasions. The approach also fits with tighter packaging and sustainability expectations in Europe and North America, where circular sourcing narratives are becoming more visible in product communication. Smaller innovators have already shown that by-product streams can be turned into tea-style beverages with commercial relevance, even if scaling still takes time. The fruit tea market gains from this trend because sustainability and functionality can be combined in one formulation story.

Volatile tropical-fruit raw material costs

The fruit tea market is impacted by fluctuating prices of mango, passion fruit, and other tropical ingredients, which are highly sensitive to weather conditions and harvest schedules. These price fluctuations often result from unpredictable factors such as adverse weather events, seasonal variations, and supply chain disruptions, making cost management a persistent challenge for manufacturers. When fruit prices increase significantly, manufacturers face a choice between absorbing the additional costs, which reduces profit margins, or passing the costs to consumers, which may lead to lower sales volumes. This challenge is particularly pronounced for fruit tea compared to other beverages, as maintaining flavor consistency is critical, and ingredient substitution is often difficult in single-fruit or signature blends. Supply uncertainties also influence product launch schedules, as brands are reluctant to scale up when ingredient availability is uncertain. This hesitancy can delay the introduction of new products, impacting market competitiveness.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Volatile tropical-fruit raw material costs | -0.6% | Asia-Pacific core, North America, and Middle East and Africa, with disruptions in producing regions | Short term (≤ 2 years) |

| Intense competition from herbal and functional beverages | -0.5% | Global, with stronger pressure in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Shelf-life challenges for clean-label infusions | -0.3% | Emerging markets in Asia-Pacific, Middle East and Africa, and South America with cold-chain gaps | Long term (≥ 4 years) |

| Non-Tariff barriers on dried-fruit imports | -0.4% | Global, with sharper pressure in EU-United States, China-United States, and India-United States trade corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intense competition from herbal and functional beverages

The fruit tea market now competes within a crowded better-for-you beverage set that includes herbal tea, adaptogen drinks, kombucha, fortified waters, and reduced-sugar refreshment products. Ryl Tea launched zero-sugar iced teas inspired by Jolly Rancher flavors in April 2026, which shows how adjacent brand identities can enter tea-based refreshment with strong flavor recognition. That pressure is important because consumers often compare these products against the same wellness and snack budgets rather than within a narrow tea-only frame. Brands that do not build a clear flavor distinction or credible functional positioning can lose attention to categories that feel more novel or more targeted. Larger incumbents have some protection because they can invest in formulation, compliance, and retail presence at the same time. Smaller operators in the fruit tea market face a tougher environment because differentiation now has to work across both taste and claimed benefit.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Mixed Fruit Anchors Volume While Flavor Breadth Supports Faster Growth

Mixed Fruit accounted for 36.50% of the fruit tea market share in 2025, making it the leading revenue segment. This position reflects the segment's ability to deliver layered flavor in one product, which is harder for consumers to replicate through single-fruit brewing at home. Mixed combinations also support product development because manufacturers can balance sweetness, acidity, aroma, and color more effectively across several fruit inputs. That flexibility is especially useful when brands want to match wellness cues with drinkability, since blends can combine familiar fruits with more distinctive notes without becoming too narrow in appeal.

The fruit tea market for mixed fruit is projected to advance at a 6.40% CAGR through 2031, which means the segment leads both in share and in forecast growth. That dual role matters because it suggests Mixed Fruit is still attracting incremental volume rather than only defending an established base. Citrus, berry, and stone fruit variants still matter because they help organize shelves and serve consumers looking for sharper, sweeter, or more familiar profiles. Yet Mixed Fruit remains better placed to absorb premiumization, wellness cues, and digital flavor discovery in one segment. The fruit tea market is therefore likely to keep using Mixed Fruit as the main bridge between mass appeal and specialty positioning.

By Form: Tea Bags Lead Through Accessibility While Loose-Leaf Gains on Premium Appeal

Tea Bags accounted for 70.01% of the fruit tea market by form in 2025, keeping the format well ahead of loose-leaf and other forms. This dominance comes from convenience, portion control, broad retail placement, and strong compatibility with private-label programs. Tea bags also fit the everyday purchase cycle better than many premium formats because they are easy to store, easy to prepare, and familiar across household use occasions. For many consumers, the first interaction with the fruit tea market still happens through boxed tea bags on supermarket shelves.

Loose-Leaf Tea is forecast to grow at a 6.70% CAGR through 2031, which makes it the fastest-growing form in the fruit tea market size by format. The faster pace reflects demand for gifting, specialty retail, visible ingredients, and higher perceived authenticity. Loose-leaf products also align well with online retail because packaging, origin stories, and blend details can be explained with more depth than on a crowded store shelf. At the same time, the growth of loose-leaf shows that premium occasions are widening rather than replacing mainstream demand. The fruit tea market, therefore, keeps its volume base in tea bags while creating more value at the upper end through loose-leaf presentation and higher-spec blends.

By Distribution Channel: Supermarkets Hold Scale While Online Retail Expands Faster

Supermarkets and Hypermarkets accounted for 52.20% of the fruit tea market in 2025, which made them the largest distribution channel by a wide margin. Their lead comes from high traffic, everyday visibility, multipack promotions, and strong support for private-label tea programs. For emerging brands, a supermarket listing still acts as a quality signal because it helps validate the brand to both consumers and other channel partners. The format also suits regular stock-up behavior, especially for tea bags and family-use packs that move through repeat basket building. This keeps physical retail highly relevant even as online channels gain share.

Online Retail Stores are projected to grow at a 7.50% CAGR through 2031, making them the fastest-growing route in the fruit tea market. Online growth is important because it changes the margin structure, giving brands more room to spend on packaging, ingredient quality, and retention marketing instead of only retailer trade terms. It also helps smaller brands reach flavor-specific demand that would be difficult to justify through national shelf placement. Launch patterns now often combine digital rollout with targeted store presence rather than treating e-commerce as a secondary route. The fruit tea market is therefore becoming more balanced across channels, with supermarkets holding scale and online improving mix, targeting, and recurring demand.

Geography Analysis

Asia-Pacific held 37.54% of the fruit tea market share in 2025, which made it the largest regional contributor. The region benefits from deep tea-drinking habits, a broad range of consumption occasions, and stronger acceptance of fruit-led and functional flavor combinations. China remains central because fresh tea culture, rapid product turnover, and wellness-oriented beverage demand create a strong base for fruit-infused formats. India adds momentum through rising interest in premium packaged beverages and growing consumer openness to functional refreshment beyond traditional tea routines. Japan and South Korea support the fruit tea market through premium retail, gifting, quality expectations, and demand for cleaner presentation.

North America is forecast to record the fastest regional growth at a 9.80% CAGR through 2031, which gives the region the quickest expansion pace in the fruit tea market size by geography. Premiumization is a key driver because value growth is being pushed by cleaner labels, specialty blends, and ready-to-drink innovation rather than only simple household penetration. Online retail and subscription behavior also help the region because they let premium and experimental products reach consumers faster than broad physical distribution alone.

Europe remains a significant part of the fruit tea market because herbal and fruit tea consumption is already embedded in routine beverage use across several countries. Germany, the United Kingdom, France, and the Netherlands are important because shoppers are familiar with fruit-led tea formats and are receptive to certified, higher-spec, or artisanal propositions. Supply-chain rules, sustainability expectations, and packaging scrutiny are pushing the market toward stronger documentation and cleaner sourcing narratives. South America, the Middle East, and Africa are smaller today, but these regions still offer room for premium specialty retail, wellness-led foodservice demand, and gradual channel development as modern trade deepens.

Competitive Landscape

The fruit tea market remains moderately fragmented, with large global tea and beverage groups competing alongside private-label manufacturers, specialty tea houses, and new ready-to-drink challengers. Unilever, Tata Consumer Products, and R. Twining and Company have strong brand recognition and shelf access, while smaller premium brands often shape flavor trends and ingredient transparency standards. This mix keeps pricing power uneven because scale helps in procurement and distribution, but specialty positioning helps in premium margins. The result is a competitive field where size matters, but product story and channel choice also matter. The fruit tea market, therefore, does not behave like a highly concentrated category, even though a few companies remain very visible.

Strategic developments in 2025 and 2026 indicate that prioritizing control over sourcing, manufacturing, and market access is becoming more critical than expanding product variety. TreeHouse Foods finalized its acquisition of Harris Tea in January 2025, gaining significant private-label scale in North America. This acquisition not only strengthened TreeHouse Foods' position in the private-label market but also enhanced its ability to manage supply chains and ensure consistent product availability. Consequently, competition in the fruit tea market is increasingly focused on manufacturing capabilities, sourcing reliability, and customer reach rather than merely broadening product assortments. Companies are now emphasizing operational efficiency and strategic partnerships to secure a competitive edge.

Innovation remains significant, but its effectiveness is enhanced when paired with credible execution. Upcycled ingredients offer an additional advantage by enabling brands to integrate sustainability with functional benefits. These ingredients not only address consumer demand for environmentally friendly products but also provide an opportunity for differentiation in a competitive market. However, these claims require robust supply chains, stringent quality control measures, and appropriate channel alignment to achieve scalability. In the fruit tea market, companies that successfully link innovation with dependable operations, ensuring consistent product quality and meeting consumer expectations, are being rewarded, rather than those focused solely on rapid product launches.

Fruit Tea Industry Leaders

-

Unilever PLC

-

ITO EN Ltd.

-

Tata Consumer Products Ltd.

-

The Hain Celestial Group Inc.

-

Associated British Foods PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: United Kingdom tea brand Kaytea launched a new "Hydro Infusions" range, which combines whole-leaf tea with electrolytes to create beverages aimed at hydration, energy, and wellness. The range includes four flavors: pineapple and hibiscus, peach and green tea, lime and mint, and lemon and mate.

- November 2025: Blasphetea, a new Irish loose-leaf tea brand, launched unique blends of fruit teas, including blood orange, and others, promoting relaxation, ethical sourcing, and a calmer lifestyle through premium loose-leaf teas.

- July 2025: Lipton, a brand of Unilver PLC, launched a new range of Fruit and Herbal teas targeting consumers seeking flavorful, wellness-oriented tea options with a contemporary taste profile. Notable flavors include Golden Chamomile, Peach Paradise, Smooth Mint, Lemon Ginger Refresh, and Berry Bliss.

Global Fruit Tea Market Report Scope

Fruit tea is defined as a functional beverage that blends the sweetness and flavors of fruits such as berries, citrus, peach, apple, and tropical varieties. It is designed to serve as a healthier alternative to sugary and caffeinated beverages. The product range includes tea bags, loose-leaf teas, and others. The fruit tea market report is segmented by source, form, distribution channel, and geography. By source, the market is segmented into citrus, berries, stone fruits, mixed fruits, and others. By form, the market is segmented into loose-leaf, tea bags, and others. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience/grocery stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Citrus |

| Berries |

| Stone Fruits |

| Mixed Fruits |

| Others |

| Loose-Leaf |

| Tea Bags |

| Others |

| Supermarkets/ Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| France | |

| Netherlands | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| By Source | Citrus | |

| Berries | ||

| Stone Fruits | ||

| Mixed Fruits | ||

| Others | ||

| By Form | Loose-Leaf | |

| Tea Bags | ||

| Others | ||

| By Distribution Channel | Supermarkets/ Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| France | ||

| Netherlands | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 outlook for fruit tea demand worldwide?

The fruit tea market is projected at USD 1.74 billion in 2026 and is expected to reach USD 2.29 billion by 2031, supported by a 5.65% CAGR over the forecast period.

Which region leads global sales of fruit-infused tea?

Asia-Pacific led with 37.54% of global sales in 2025, supported by strong tea-drinking habits, broad flavor adoption, and deeper familiarity with premium tea formats.

Which region is expanding the fastest through 2031?

North America is forecast to grow fastest at a 9.80% CAGR, helped by premium ready-to-drink launches, cleaner labels, and stronger online discovery of specialty products.

Which source segment is strongest in consumer demand?

Mixed Fruit led with a 36.50% share in 2025 and is also projected to grow fastest at a 6.40% CAGR, reflecting strong demand for layered flavor profiles.

Page last updated on: