Herbal Tea Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.98 Billion |

| Market Size (2031) | USD 8.07 Billion |

| Growth Rate (2026 - 2031) | 6.81% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Herbal Tea Market Analysis by Mordor Intelligence

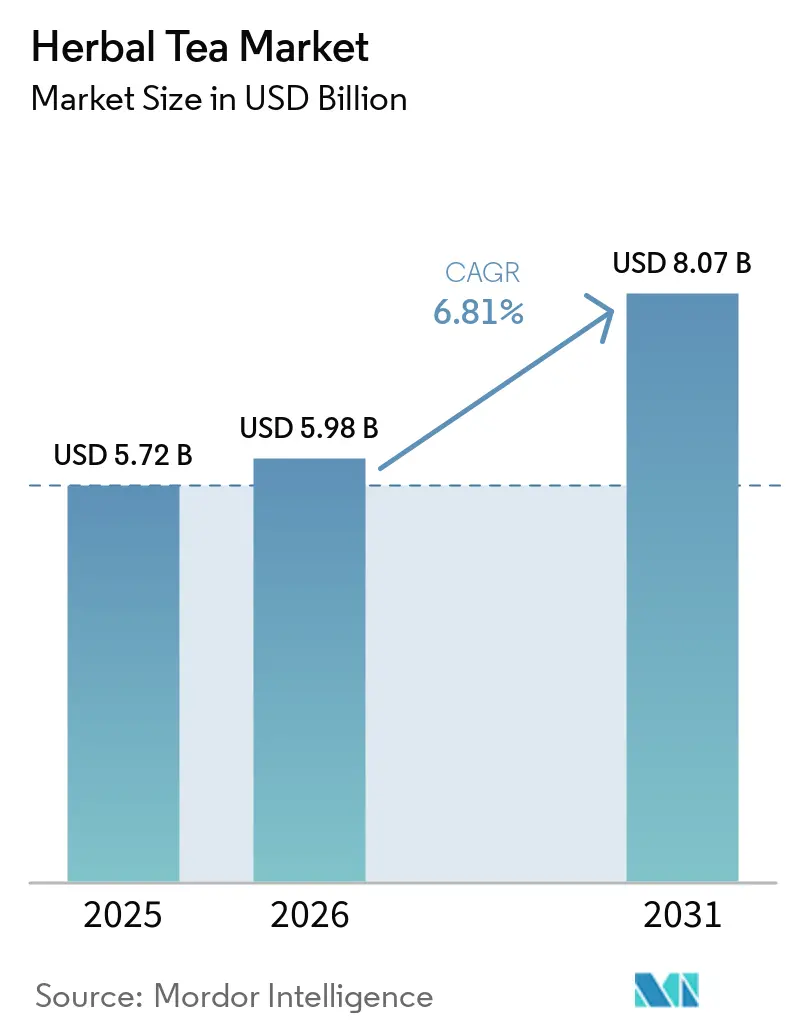

The herbal tea market size is expected to increase from USD 5.72 billion in 2025 to USD 5.98 billion in 2026 and reach USD 8.07 billion by 2031, growing at a CAGR of 6.2% over 2026-2031. The herbal tea market is expanding as more consumers move away from caffeinated and high-sugar drinks and adopt wellness products as part of their daily routines. The category is also benefiting from stronger demand for organic beverages in the United States and deep-rooted consumption of herbal and fruit infusions in Germany, which supports premium pricing and repeat buying in the herbal tea market. E-commerce has widened access for specialty brands, which has made it easier for smaller companies to build direct relationships with consumers and test premium formulations in the herbal tea market. Competitive activity remains active across both multinational and specialist brands, while tighter scrutiny of botanical health claims in Europe is making substantiation and label discipline more important in the herbal tea market. Raw material volatility remains a constraint, but demand for clean-label and function-led products is still supporting the medium-term outlook for the herbal tea market.

Key Report Takeaways

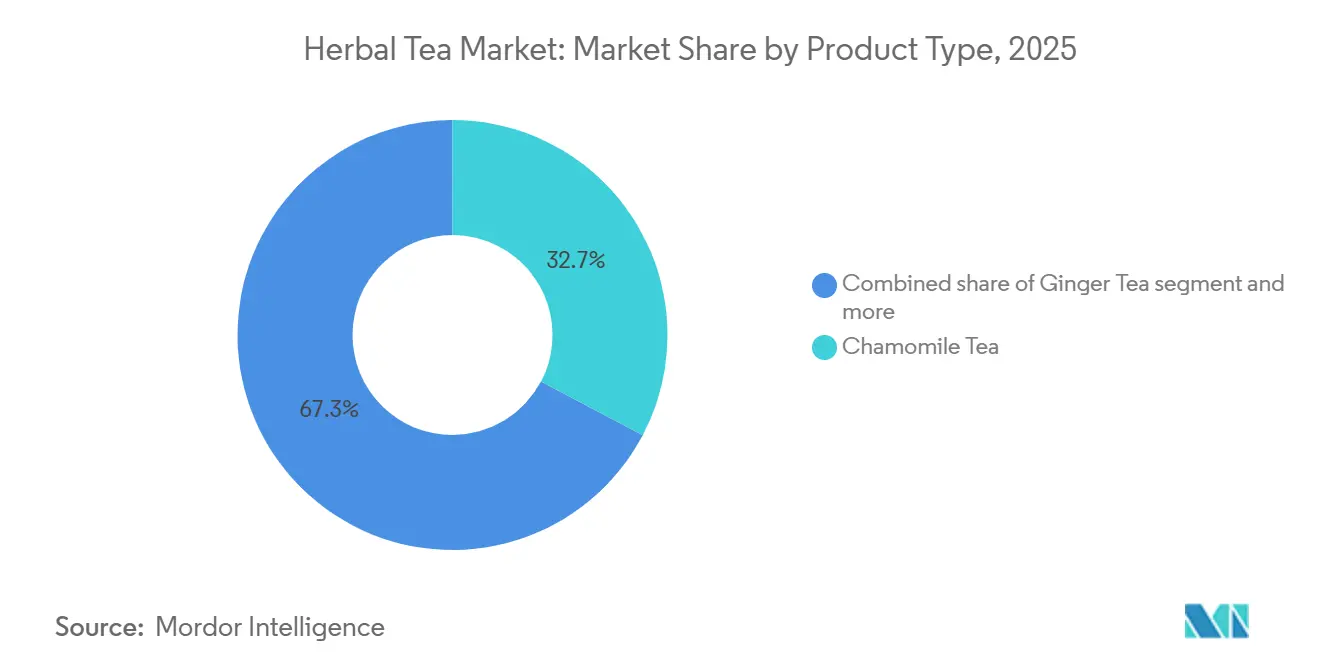

- By product type, chamomile tea accounted for the largest share of the herbal tea market, at 32.7% in 2025, while ginger tea is projected to grow at the fastest CAGR of 7.5% during 2026-2031.

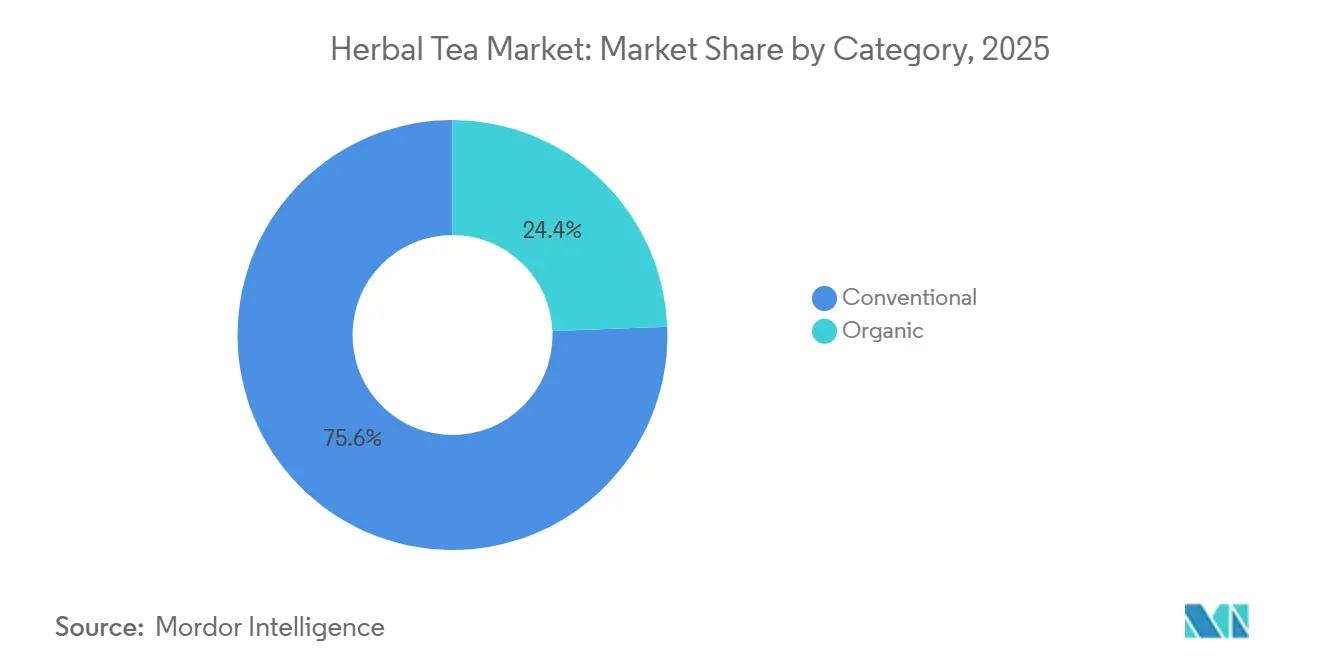

- By category, conventional herbal tea retained 75.6% share of the herbal tea market in 2025, whereas organic herbal tea is forecast to expand at an 8.1% CAGR through 2031.

- By distribution channel, retail channels accounted for the largest share of the herbal tea market, at 72.1% in 2025, while foodservice is projected to grow at the fastest CAGR of 7.5% during 2026-2031.

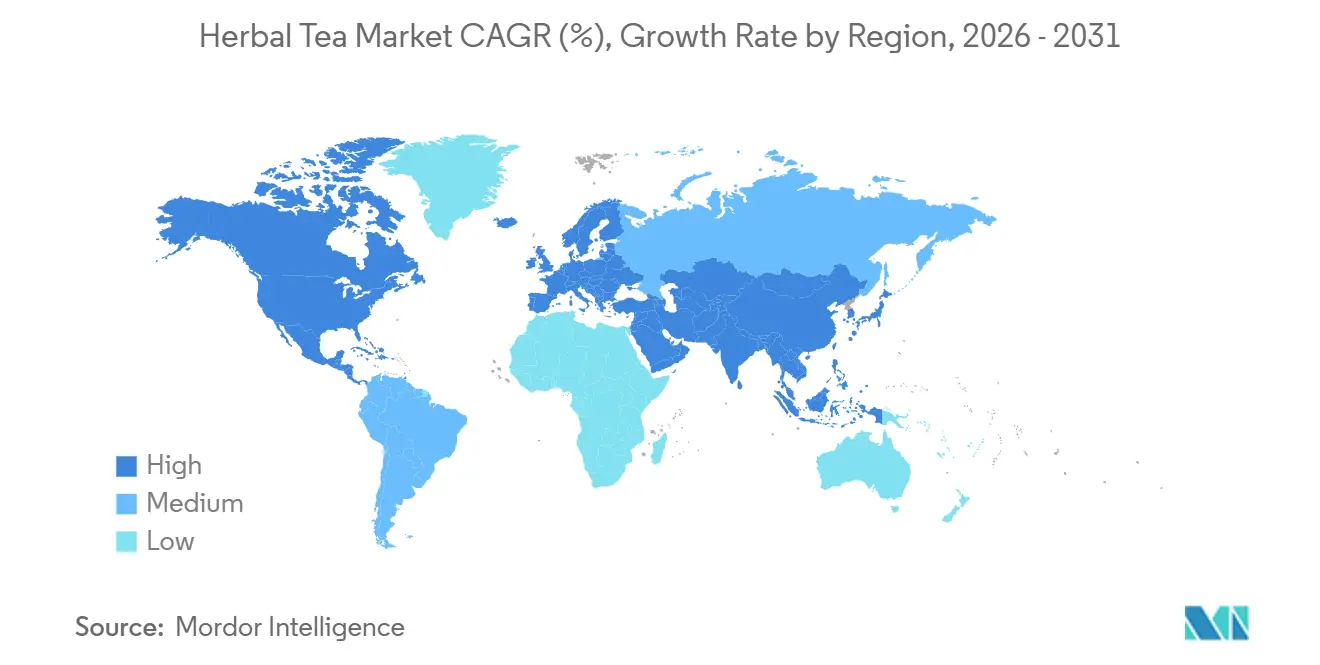

- By geography, Europe accounted for the largest share of the herbal tea market, at 36.4% in 2025, while Asia-Pacific is projected to grow at the fastest CAGR of 8.0% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Herbal Tea Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Caffeine-Free Wellness Beverages | +1.8% | Global | Short term (≤ 2 years) |

| Growth Of Clean-Label and Organic Tea Purchasing | +1.2% | Europe and North America core, expanding to the Asia-Pacific | Medium term (2–4 years) |

| Expanding E-Commerce and Direct-to-Consumer Distribution | +0.9% | Global, the Asia-Pacific leading adoption | Short term (≤ 2 years) |

| Premiumization Through Functional Botanical Blends | +0.8% | North America and Europe core, expanding to the Asia-Pacific | Medium term (2–4 years) |

| Shift Away from Sugary and Carbonated Drinks | +0.7% | Global; strongest in the Asia-Pacific, the Middle East, and Africa | Medium term (2–4 years) |

| RTD and Convenience Format Innovation | +0.6% | North America, the Asia-Pacific, and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for caffeine-free wellness beverages

Driven by a focus on sleep disruption, stress management, and digestive health, consumers are increasingly turning to herbal teas. This shift has led to a demand profile that prioritizes outcomes over price, distinguishing it from traditional tea categories. The World Tea News 2025 State of the Tea Industry Survey revealed that 26.3% of industry respondents pinpointed consumer health and wellness interests as the top influencer on tea sales, marking it as the study's leading driver. This evolving consumer behavior has notable distribution implications: those seeking herbal teas for wellness are more inclined to experiment with premium and specialty variants, reducing the price sensitivity that often limits mass-market growth. Brands tailoring their product formulations to address specific needs, be it sleep, immunity, or digestion, are witnessing significantly higher repeat purchase rates compared to those offering generic herbal blends. In its November 2025 expansion into the herbal category, Lipton Teas and Infusions highlighted that formulations like mint for digestion and chamomile for relaxation outperformed generic blends in consumer panel tests.

Growth of clean-label and organic tea purchasing

Certified organic herbal teas are witnessing a surge in demand, outpacing the broader beverage category. Projections indicate that from 2026 to 2031, organic herbal tea will grow at an 8.11% CAGR, marking a premium of roughly 2 percentage points over the overall market rate. The Organic Trade Association's 2026 Market Report highlighted that U.S. organic beverage sales hit USD 10.2 billion in 2025, boasting a growth rate of 7.2%, more than thrice that of the total beverage market[1]Source: Organic Trade Association, “2026 Organic Market Report,” Organic Trade Association, domain not provided in source draft.. Data from Oekolandbau revealed that in 2024, organic tea's share of Germany's total tea volume climbed by 2.2 percentage points to 17.7%. This is notable when juxtaposed with the overall German organic food market's share of a mere 6.5%. Such a trend, where tea consumers lean more towards organic purchases than the general food market, underscores a structural pricing advantage for producers of certified-organic herbal teas. For brands aiming at the premium tier in European and North American retail channels, adhering to the EU Organic Regulation 2018/848 and obtaining the USDA National Organic Program (NOP) certification are essential baseline requirements.

Premiumization through functional botanical blends

In the evolving herbal tea market, while commodity chamomile and peppermint teas grapple with price compression, blends infused with adaptogens, nootropics, and multi-herb functional stacks are enjoying significantly higher retail price points. This trend of premiumization stems from consumers' readiness to invest in specific outcomes; for instance, a blend targeting cortisol regulation or gut microbiome support engages in a distinctly different pricing dialogue compared to a standard relaxation tea. The fusion of age-old herbal traditions, notably Indian Ayurveda and Traditional Chinese Medicine, with modern evidence-based functional nutrition is birthing product concepts that are both culturally rich and scientifically validated. This blend strikes a chord with discerning millennial consumers, who often question unverified wellness claims. Supporting this trend, a 2025 systematic review in the journal Critical Reviews in Food Science and Nutrition highlights that "economic dynamics and market trajectories significantly influence consumption patterns," underscoring how functional positioning is steering premium pricing in the herbal tea market.

Shift away from sugary and carbonated drinks

The growing shift away from sugary and carbonated beverages is significantly driving the global herbal tea market as consumers increasingly seek healthier, natural alternatives that support long-term wellness. Public health organizations such as the World Health Organization continue to advocate reducing free sugar intake to combat obesity, diabetes, and cardiovascular diseases, encouraging consumers to replace sugar-laden soft drinks with lower-calorie beverage options. Herbal teas benefit from this transition due to their caffeine-free nature, natural ingredients, and perceived digestive, relaxation, and immunity-supporting properties. Industry sources report that consumers are increasingly moving away from sugary beverages toward herbal and wellness-focused drinks, while tea markets globally are benefiting from demand for low-calorie alternatives to carbonated soft drinks. Reflecting this trend, in May 2025, Starbucks launched a new RTD Coffee Tea line in China targeting health-conscious consumers, while in January 2026, Nestlé expanded its portfolio with carbonated herbal and fruit-infused tea beverages featuring clean-label and wellness-oriented positioning. Additionally, beverage manufacturers are increasingly introducing herbal, botanical, and functional tea formulations to capture consumers seeking alternatives to traditional sugary soft drinks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonal Herb Supply Volatility | -0.5% | Global supply chain; sourcing hubs in South Asia and North Africa | Short term (≤ 2 years) |

| Competition from Other Functional Beverages | -0.5% | Global; strongest in North America and Europe | Medium term (2–4 years) |

| Tight Regulatory Scrutiny on Botanical Health Claims | -0.4% | EU primary; spill-over to the United Kingdom GCC markets | Medium term (2–4 years) |

| Quality Inconsistency in Multi-Origin Herbal Inputs | -0.3% | Global sourcing is concentrated in South and Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Seasonal herb supply volatility

The herbal tea industry grapples with procurement risks tied to its reliance on geographically concentrated agricultural sources. This dependence not only jeopardizes margin stability but also threatens product availability. Chamomile, commanding a dominant 32.71% share in 2025, predominantly hails from Egypt and Argentina. The U.S., with an import reliance of 85–95%, finds its manufacturers vulnerable to crop yield fluctuations. These fluctuations are often driven by temperature spikes, droughts, and unpredictable rainfall during crucial harvest windows. Meanwhile, ginger, the industry's fastest-growing segment, is set to witness a CAGR of 7.46% from 2026 to 2031. Yet, it too contends with supply disruptions. For instance, the 2025 ginger season in Peru wrapped up ahead of schedule, tightening global supplies just as demand surged. This scenario allowed China and Thailand to capitalize on the constrained market. Furthermore, the herbal botanical supply chain grapples with quality adulteration challenges. Under procurement pressures, the risk of adulteration escalates, leading to verification costs. These costs pose a significant burden for smaller brands. In contrast, producers boasting vertically integrated sourcing or long-term agricultural contracts are fortifying their supply chain resilience, turning it into a competitive advantage. However, asset-light brands find themselves navigating challenges related to margins and product availability.

Tight regulatory scrutiny on botanical health claims

In April 2025, the CJEU ruling in Case C-386/23 (Novel Nutriology) mandated that food advertising's botanical health claims must secure explicit authorization from the European Commission, as per Regulation (EC) No 1924/2006. This decision effectively ended a decade-long regulatory ambiguity that numerous herbal tea brands had navigated. The European Food Safety Authority (EFSA) had paused its evaluation of botanical health claims, leaving over 2,078 claims in a provisional "on-hold" state[2]Source: European Food Safety Authority, “Botanical Health Claims Status and Related Materials,” EFSA, domain not provided in source draft.. However, the recent CJEU ruling has tightened the reins on this commercial practice. Historically, EFSA has dismissed over 90% of botanical health claims evaluated under Article 13.1 of Regulation (EC) No 1924/2006, pointing to a lack of adequate human intervention study evidence, as highlighted in a 2025 study in the journal Nutrients MDPI Nutrients. Brands operating within EU markets now face the daunting task of overhauling their packaging, digital marketing, and retail materials. While larger companies with specialized regulatory teams can navigate these changes with relative ease, the burden is disproportionately heavy on smaller specialists. Meanwhile, across the Atlantic, the US FDA, under the Dietary Supplement Health and Education Act (DSHEA), allows structure/function claims but mandates substantiation. This creates a parallel compliance landscape for brands catering to both the EU and US markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Chamomile Anchors Volume While Ginger Captures Functional Premium

In 2025, chamomile tea led the herbal tea market with a 32.71% share, solidifying its role as the category's cornerstone. Widely recognized, chamomile tea has consistent consumer demand for relaxation and sleep-support benefits across mass retail and specialty outlets. Ginger tea is the fastest-growing product, with a projected 7.46% CAGR from 2026 to 2031, driven by clinical recognition of its digestive and nausea relief benefits, along with its appeal in ready-to-drink (RTD) and foodservice menus. Peppermint tea, a digestion-focused staple, is particularly strong in Europe. The Deutscher Tee and Kräutertee Verband's Tea Report 2025 highlighted peppermint and mint blends as the top single-variety herbal category in Germany, holding a 7.5% volume share. Hibiscus tea is gaining popularity in iced and RTD formats for its antioxidants and visual appeal, while rooibos maintains a niche but loyal consumer base in Europe, where its South African origin adds brand value. Turmeric tea, combining anti-inflammatory wellness and Ayurvedic heritage, is set for rapid growth as its benefits gain mainstream recognition.

The "Other Herbal Teas" segment, including blends with adaptogens, mushrooms, and multi-botanical formulations, drives innovation in the category. Teapigs' May 2026 launch of four new herbal blends on Amazon, including its first Reishi mushroom-infused tea, highlights the category's expansion. This growth is expected to accelerate as functional food-as-medicine gains consumer acceptance. Cross-category blends, such as ginger with turmeric, chamomile with lavender, and hibiscus with rosehip, enhance perceived value and support premium pricing. Contract manufacturers are fueling this innovation. For example, Caraway Tea Company's April 2026 entry into adaptogen and mushroom-based blends reflects rising demand for scientifically curated multi-botanical formulations.

By Category: Conventional Holds Volume Share but Organic Is the Growth Engine

In 2025, conventional herbal tea dominated the market, holding a 75.62% share, underscoring the strong foothold of budget-friendly branded teas in mass retail. Yet, the organic segment is on a notable upswing: with a projected CAGR of 8.11% from 2026 to 2031, organic herbal tea is outpacing the overall market by roughly 2 percentage points. This growth differential suggests that conventional teas may soon see their volume leadership wane, especially at the premium end. Data from Germany's Tea Report 2025 highlights a distinct trend: while organic tea made up 17.7% of Germany's tea volume in 2024, this figure is nearly threefold compared to the 6.5% organic share in the broader German food market. Such a disparity indicates that herbal tea enthusiasts are particularly receptive to organic offerings, granting certified producers a significant edge in pricing and brand loyalty.

For brands eyeing the premium tier in Europe and North America, adhering to the EU Organic Regulation 2018/848 and securing the USDA's National Organic Program (NOP) certification is just the starting point. A more pivotal development lies in how the conventional segment is adapting: In November 2025, Lipton Teas and Infusions rolled out a new herbal line, infusing familiar wellness herbs like chamomile for relaxation and mint for digestion. This move aims to seamlessly connect the conventional and functional realms, ensuring the mid-premium space isn't solely claimed by certified-organic players. The industry is increasingly acknowledging the fading lines between conventional and functional herbal teas. Today's consumers demand transparency in ingredients and their origins, even within the conventional tier. Brands that proactively emphasize transparent supply chains and clean-label formulations in the conventional segment stand a better chance of retaining consumers who might consider a shift to certified organic.

By Distribution Channel: Retail Leads as Foodservice Redefines Consumer Discovery

In 2025, retail channels dominated herbal tea distribution, accounting for 72.13% of the market share. Supermarkets and hypermarkets were the primary access points for global mass-market consumers. Meanwhile, the foodservice sector is forecasted to grow at a 7.51% CAGR from 2026 to 2031, driven by café chains, wellness centers, and specialty tea bars introducing botanical infusion menus that boost brand visibility and encourage at-home purchases. Within retail, online stores are the most dynamic sub-channel. Direct-to-consumer platforms and Amazon-centric launches, like teapigs' introduction of four new herbal blends in May 2026, allow brands to test formulations with reduced risks while gathering consumer data to guide future innovations. Specialty stores attract a premium consumer base; the Deutscher Tee and Kräutertee Verband reported a nearly 2 percentage point year-on-year increase in foot traffic at specialist tea shops in Germany for 2024, reflecting growing consumer interest in dedicated tea retail experiences.

Convenience stores, though underutilized, are becoming pivotal for herbal ready-to-drink (RTD) formats. As traditional sugary beverages make way, shelf space is opening for canned and bottled botanical teas. The shift in convenience format, from pyramid tea bags to instant-dissolve sachets and refrigerated high-pressure processed (HPP) RTD bottles, bolsters growth in foodservice and convenience channels. Manufacturers are investing in this evolution. For instance, Evolution Fresh launched organic RTD teas at Whole Foods Market in April 2026, blending brewed tea with cold-pressed juice in a pioneering HPP format, setting a premium benchmark for refrigerated herbal drinks in retail spaces adjacent to specialty foodservice, as reported by Business Wire. Subscription services within the direct-to-consumer model are emerging as loyalty tools. Platforms offering tailored herbal blend subscriptions ensure consistent revenue and enhance consumer lifetime value. Channel evolution is faster in APAC regions, where social commerce and livestreaming are accelerating e-retail, driving quicker online discovery and trial compared to Western markets.

Geography Analysis

In 2025, Europe is set to command a 36.40% share of the global herbal tea market, with Germany, the UK, France, and the Netherlands leading the charge. In these nations, herbal infusions are deeply embedded in the culture as daily wellness rituals. Germany stands out: in 2024, the country consumed 39,398 tonnes of herbal and fruit infusions, accounting for 67.7% of Germany's total tea market, surpassing the global average, as highlighted in the Tea Report 2025 by Deutscher Tee and Kräutertee Verband. In 2025, Germany's organic food and beverage market hit EUR 18.23 billion (~USD 19.7 billion), marking a 6.7% growth. Organic tea's growth outpaced overall organic food penetration, according to Oekolandbau.de. The UK market is shaped by Twinings and Pukka Herbs, leading in mass and premium channels. Eastern European nations like Poland and Sweden present expansion opportunities for mid-tier brands. Sweden's specialty tea shop culture and Belgium's premium food retail scene remain largely untapped. The German Tea Report 2025 noted that in 2024, innovative herbal and fruit tea blends and cold brew formats emerged as top performers, reflecting a shift in consumer preferences towards novel formats over traditional loose-leaf and tea bags.

North America, with the U.S. at the helm, is a market of strategic importance. Health-conscious consumers aged 25–45 are driving the growth of specialty and organic herbal teas. The OTA's 2026 Organic Market Report revealed that U.S. organic beverage sales grew by 7.2% in 2025, reaching USD 10.2 billion. Herbal tea benefited from the prevailing "food as medicine" trend. Canada showcases strong engagement with premium herbal wellness brands. Traditional Medicinals, a leading organic tea company in Canada, launched its Organic Stress Soother Tension Relief Tea in January 2026, underscoring the country's priority status. Mexico and other parts of North America are in the early stages of adoption, with growth driven by modern retail formats and rising health awareness among urban middle-class consumers.

Asia-Pacific is on a rapid ascent, projected to grow at a 7.98% CAGR from 2026 to 2031. China leads the region, where age-old herbal medicine practices meet a modern pivot: consumers increasingly favor sugar-free RTD teas over sugary carbonated drinks. This shift is evident in the 2025 observation of the Chinese beverage market's move towards sugar-free teas, functional drinks, and premium bottled water. India is also witnessing rapid growth. VAHDAM India reported a 31% year-on-year revenue growth in FY26, reaching INR 350 crore (~USD 42 million), underscoring the potential of premium herbal and botanical teas rooted in Ayurvedic traditions[3]Source: VAHDAM India, “FY26 Company Disclosure Referenced in Draft,” VAHDAM India, domain not provided in source draft.. Japan, South Korea, Thailand, and Indonesia each have unique demand profiles shaped by local herbal customs, with RTD formats gaining traction in convenience and modern trade channels. South America, the Middle East, and Africa are emerging players. Brazil's growing urban middle class and the Gulf Cooperation Council's premium food retail segment, aligned with wellness trends, stand out as prime targets for brands with the right distribution channels.

Competitive Landscape

In the herbal tea market, large multinational tea groups vie for dominance alongside niche herbal wellness brands. Associated British Foods, through its Twinings brand, along with LIPTON Teas and Tata Consumer Products, leverage their scale for advantages in distribution, brand visibility, and retailer access. Meanwhile, specialists like Pukka Herbs, Traditional Medicinals, Yogi Tea, and VAHDAM India command a premium wellness image and enjoy heightened consumer loyalty. This duality underscores the market's complexity: both broad shelf presence and deep brand trust are pivotal, influenced by pricing tiers and sales channels. Thus, the herbal tea landscape isn't a zero-sum game; both scale and specialization cater to distinct consumer desires.

A strategic divide is evident in the herbal tea arena. Major players are broadening their horizons, venturing into herbal, wellness, and organic domains to fortify their market stance. In contrast, specialists are carving out growth through direct sales, compelling narratives, and cultivating tight-knit, engaged communities. A testament to this trend, Tata Consumer Products bolstered its herbal portfolio with the 2024 acquisition of Organic India for a hefty INR 1,900 crore (USD 229 million). This strategic move not only expanded Tata's tea and wellness offerings but also intertwined herbal tea with supplements, Ayurveda, and the overarching demand for natural health. Concurrently, established brands are gravitating towards well-known wellness herbs like chamomile and mint, signaling a shift: even traditional players are pivoting towards function-driven demands, moving beyond mere accessibility.

There's still ample opportunity for specialist brands in the herbal tea domain. Premium consumers often prioritize ingredient provenance, clarity, and targeted wellness benefits. VAHDAM India's impressive FY26 revenue growth of 31%, reaching INR 350 crore (USD 42 million), underscores the potential for premium botanical tea brands to flourish when brand identity aligns with distribution strategies. The market's most promising avenues lie in evidence-backed blends targeting sleep, digestion, and stress relief, as well as daily wellness. Additionally, the ready-to-drink segment presents a lucrative opportunity, positioning botanical tea as a contender in the functional beverage arena, rather than just another tea variant. This evolution underscores the significance of product design, innovative formats, and substantiated claims in the herbal tea sector. Companies that master the art of trusted sourcing, articulate efficacy, and ensure widespread access are poised to lead the next competitive wave in the herbal tea market.

Herbal Tea Industry Leaders

Associated British Foods plc

Lipton Teas and Infusions B.V.

Tata Consumer Products Limited

Unilever PLC

The Hain Celestial Group, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Teapigs launched 4 caffeine-free herbal tea blends on Amazon. The launch included Ginger and Manuka Honey, Strawberry and Juniper, Chamomile Lullaby, and Pumpkin Spice Chai, marking the brand's first product innovation in over 5 years and introducing its first Reishi mushroom-infused tea. The Amazon-first strategy signals a deliberate pivot toward DTC channel growth ahead of wholesale retail distribution.

- May 2026: Caraway Tea Company expanded manufacturing capacity at its Poughkeepsie, NY facility specifically for sleep and stress-support herbal blends, citing these as "one of the fastest-moving consumer wellness categories of 2026," and opened Q3 2026 production inquiry slots for brand and retailer partners.

- April 2026: Evolution Fresh (Starbucks) launched a full line of 4 organic RTD teas at select Whole Foods Market stores nationwide, combining brewed tea with cold-pressed juice in a first-of-kind refrigerated HPP-format certified USDA Organic and Non-GMO Project Verified. The 16-oz bottles span chamomile/lavender, hibiscus, and energizing tea variants.

Global Herbal Tea Market Report Scope

Herbal tea is a beverage made by infusing or steeping dried fruits, flowers, spices, roots, or herbs in hot water. The global herbal tea market is segmented by product type, category, distribution channel, and geography. By product type, the market is segmented into chamomile tea, peppermint tea, ginger tea, hibiscus tea, turmeric tea, rooibos tea, and other herbal teas. By category, the market is segmented into conventional and organic. By distribution channel, the market is segmented into foodservice and retail. The retail segment is further sub-segmented into supermarkets/hypermarkets, convenience stores, specialty stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Chamomile Tea |

| Peppermint Tea |

| Ginger Tea |

| Hibiscus Tea |

| Turmeric Tea |

| Rooibos Tea |

| Other Herbal Teas |

| Conventional |

| Organic |

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Chamomile Tea | |

| Peppermint Tea | ||

| Ginger Tea | ||

| Hibiscus Tea | ||

| Turmeric Tea | ||

| Rooibos Tea | ||

| Other Herbal Teas | ||

| Category | Conventional | |

| Organic | ||

| Distribution Channel | Foodservice | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the herbal tea space, and how fast is it growing?

The herbal tea market stood at USD 5.72 billion in 2025, reached USD 5.98 billion in 2026, and is projected to hit USD 8.07 billion by 2031 at a 6.2% CAGR.

Which region currently leads global demand for herbal tea?

Europe led in 2025 with a 36.4% share, supported by mature retail infrastructure and long-standing consumer familiarity with herbal infusions.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is forecast to expand at an 8.0% CAGR through 2031, helped by traditional herbal medicine systems, urban income growth, and wider modern retail access.

Which product type has the strongest position today?

Chamomile tea held the largest share at 32.7% in 2025 because it appeals to both everyday tea buyers and consumers seeking relaxation-oriented wellness products.

Page last updated on: