United States AI-Powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

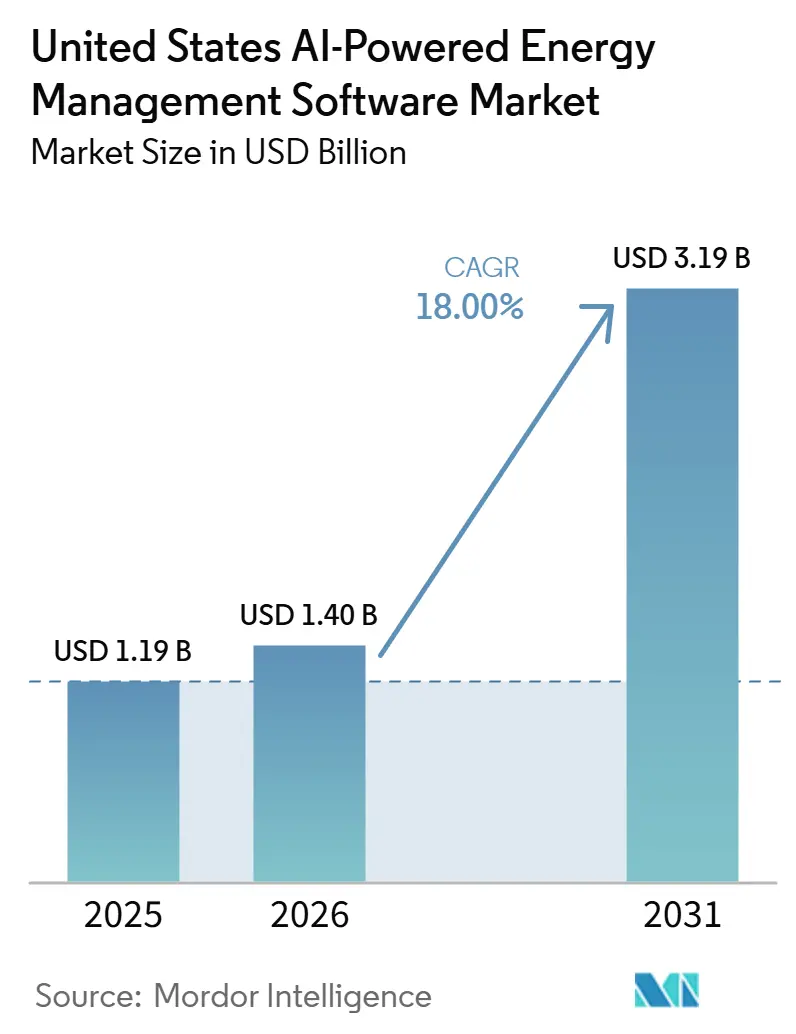

| Base Year Market Size (2025) | USD 1.19 Billion |

| Market Size (2026) | USD 1.40 Billion |

| Market Size (2031) | USD 3.19 Billion |

| Growth Rate (2026 - 2031) | 18.00% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States AI-Powered Energy Management Software Market Analysis by Mordor Intelligence

The United States AI-powered energy management software market size was valued at USD 1.19 billion in 2025 and estimated to grow from USD 1.40 billion in 2026 to reach USD 3.19 billion by 2031, at a CAGR of 18.00% during the forecast period 2026 to 2031. The United States AI-powered energy management software market is moving from a discretionary software purchase to an operating tool because electricity costs stayed elevated in 2025, data center power demand kept rising, and building owners faced wider compliance requirements for energy use and emissions reporting. The United States AI-powered energy management software market is also benefiting from utility grid modernization programs that need better demand visibility at the customer edge and from cloud connectivity that makes cross-site monitoring easier for large portfolios. Competitive activity is centered on platform expansion, acquisitions, and partnerships as large incumbents add AI capabilities to installed automation bases and pure-play vendors push deeper analytics for utilities and multi-site commercial clients. The clearest near-term opportunity is in portfolio operators that need continuous optimization, carbon reporting, and automated flexibility across many sites, especially where policy pressure and power costs are both rising. At the same time, the United States AI-powered energy management software market still faces slower rollout in older facilities because legacy controls, cybersecurity requirements, and limited implementation talent can delay full deployment even when demand conditions are favorable.

Key Report Takeaways

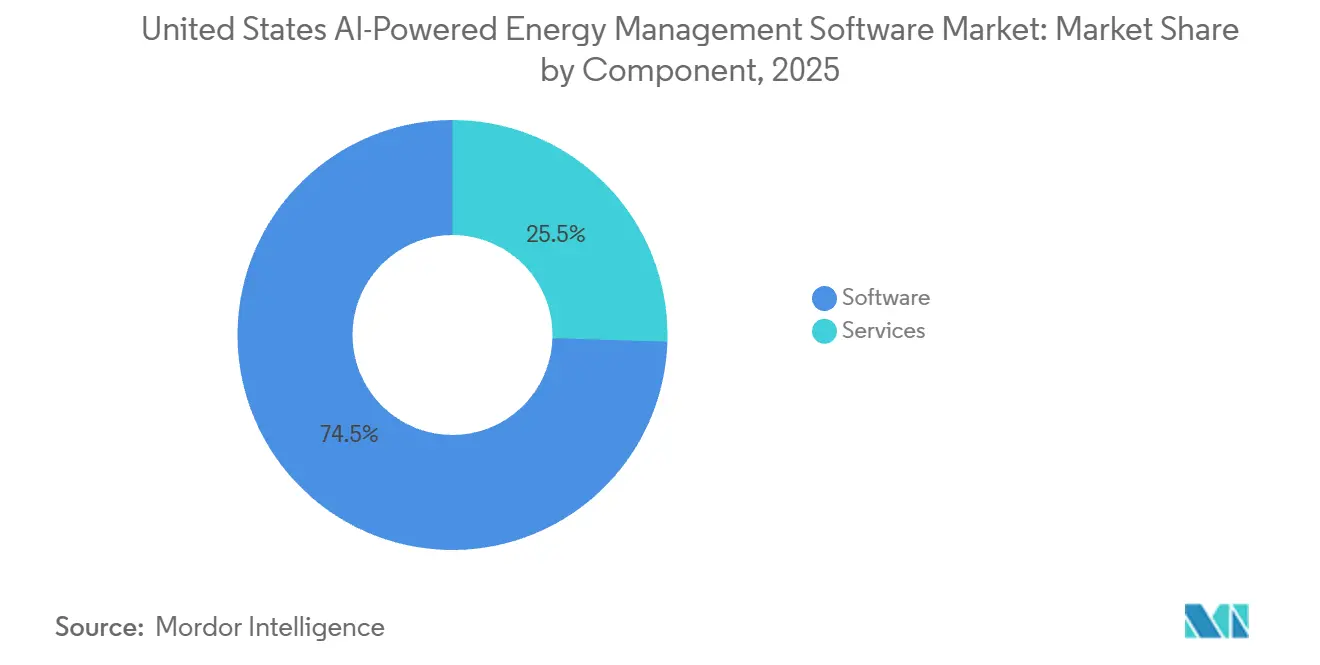

- By component, software led with a 74.50% share of the United States AI-powered energy management software market in 2025, while services recorded the highest projected CAGR at 20.80% through 2031.

- By deployment mode, cloud-based platforms held 58.20% share in 2025, while cloud-based platforms also posted the fastest CAGR at 21.10% through 2031.

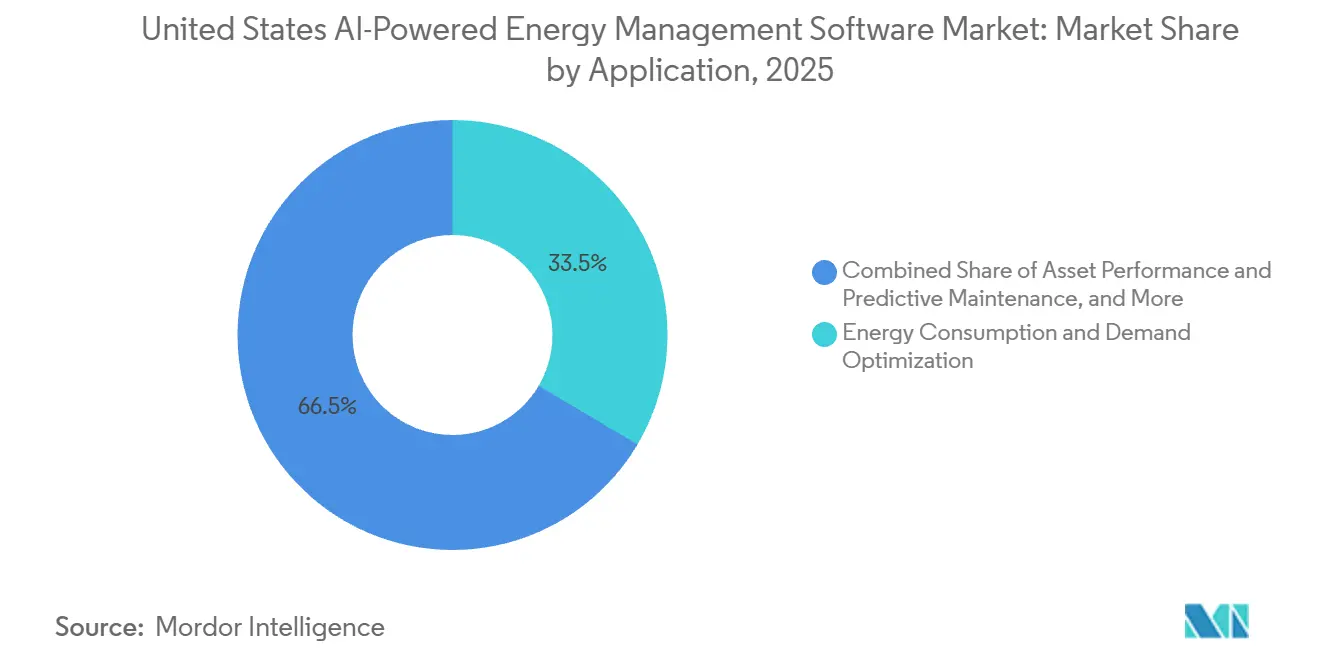

- By application, energy consumption and demand optimization accounted for a 33.50% share in 2025, while renewable energy forecasting and integration is advancing at a 21.80% CAGR through 2031.

- By end user, utilities held 36.50% share of the United States AI-powered energy management software market in 2025, while residential buildings recorded the highest projected CAGR at 21.50% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States AI-Powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Utility Data Digitization and Grid Modernization Programs | +3.5% | National, with strongest near-term impact in Mid-Atlantic, Texas, and Midwest ISO territories | Short term (≤ 2 years) |

| Federal and State Decarbonization Targets for Commercial Buildings and Industry | +3.0% | National, early traction in California, Massachusetts, Colorado, Washington, Maryland, and Oregon | Medium term (2-4 years) |

| AI-Enabled Peak Demand Reduction and Automated Load Flexibility | +2.8% | National, with concentrated impact in PJM, ERCOT, MISO, and CAISO organized markets | Short term (≤ 2 years) |

| Cloud-Native Integration with Existing BMS, EMS, and IoT Stacks | +2.3% | National, strongest adoption in New York, Chicago, Dallas, and San Francisco | Medium term (2-4 years) |

| Portfolio-Level Carbon Reporting Pressure from Enterprise Buyers | +1.8% | National, accelerated in states with active climate disclosure timelines | Medium term (2-4 years) |

| Data Center Energy Intensity and Continuous Optimization Needs | +1.6% | Northern Virginia, Texas, Arizona, Georgia, Iowa, and emerging secondary markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Utility Data Digitization and Grid Modernization Programs

Utilities are expanding digital grid programs at the same time that large loads from AI infrastructure are becoming harder to manage with older operating models. The U.S. Department of Energy stated in 2024 that domestic data center electricity consumption is expected to double or triple by 2028 and reach 325TWh to 580TWh, which raises the need for better monitoring and control across both grid and customer assets.[1]U.S. Department of Energy, “DOE Releases New Report Evaluating Increase in Electricity Demand from Data Centers,” U.S. Department of Energy, energy.gov GridPoint stated that utilities filed USD 18.2 billion in aggregate rate increase requests in 2025 to support grid investment, which supports demand for software that can turn interval data and operating signals into load flexibility. Argonne National Laboratory introduced GridMind in 2026 as an AI co-pilot for power system operators, which shows that utility-side AI adoption is moving from concept to operating use. In the United States AI-powered energy management software market, that shift matters because utilities that modernize their own control environments also create demand for customer-side software that can respond to grid conditions in real time.

Federal and State Decarbonization Targets for Commercial Buildings and Industry

Building performance standards are widening the compliance burden for commercial property owners and pushing continuous monitoring into routine operations. The Institute for Market Transformation reported that by 2025, 4 states and at least 9 local jurisdictions had enacted building performance standards, while around 30 additional governments had committed to adoption. Washington State enacted House Bill 1543 in 2025, and Evanston, Illinois, passed its Healthy Buildings Ordinance in 2025, extending the policy push beyond the largest coastal cities. These rules create a recurring need for measurement, reporting, and operational adjustment rather than a single benchmarking exercise. In the United States AI-powered energy management software market, that makes subscription platforms more useful than periodic audit tools for owners managing large building portfolios.

AI-Enabled Peak Demand Reduction and Automated Load Flexibility

Demand flexibility is becoming more valuable because grid operators and commercial customers both need faster response during high-stress periods. Constellation Energy and GridBeyond launched an AI-powered demand response program in the PJM interconnection in July 2025, using real-time grid data and automated sub-meter load control for business customers. In February 2026, CPower, Bentaus, and Supermicro demonstrated that AI compute workloads running on Supermicro servers with NVIDIA B200 GPUs could cut electricity use by as much as 75% during grid stress events while maintaining service-level agreements. That result extends the use case beyond simple bill management and into capacity support for high-load assets such as AI data centers. The United States AI-powered energy management software market gains from this shift because software value is tied more directly to dispatch, automation, and revenue-linked grid participation.

Cloud-Native Integration with Existing BMS, EMS, and IoT Stacks

Integration is improving because vendors are linking operational technology, enterprise systems, and site-level controls through cloud and edge architectures. Honeywell and Tata Consultancy Services formalized a collaboration in February 2026 to build a unified OT-to-IT foundation with Honeywell Forge for buildings and industrial facilities.[2]Honeywell International, “Honeywell and TCS Collaborate to Enhance Autonomous Operations for Buildings and Industries With AI,” Honeywell, honeywell.com Stem and Nuvation Energy entered a partnership in April 2026 to connect PowerTrack Energy Management System with Nuvation's Battery Management System in a cloud-to-edge control setup. These moves reduce the effort needed to bring utility coordination, battery management, and building-level control into one operating layer. In the United States AI-powered energy management software market, easier integration supports wider adoption among mid-sized buyers who previously found custom connectivity too costly or too slow.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Brownfield Integration Cost with Legacy OT and Building Controls | -2.3% | National, most acute in industrial belts of the Midwest and Southeast and in pre-2000 commercial stock across major metros | Medium term (2-4 years) |

| Cybersecurity and Critical Infrastructure Compliance Burden | -2.0% | National, heightened in bulk electric system perimeters under NERC CIP jurisdiction and in cloud-adjacent OT environments | Medium term (2-4 years) |

| Fragmented Energy Data Across Sites, Utilities, and Vendors | -1.5% | National, most acute in multi-state enterprise portfolios with heterogeneous utility data environments | Long term (≥ 4 years) |

| Shortage of AI, Controls, and Energy Management Implementation Talent | -1.2% | National, concentrated in Tier 2 and Tier 3 metro markets outside major technology hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Brownfield Integration Cost with Legacy OT and Building Controls

Brownfield integration remains a major brake on deployment, especially in older commercial and industrial sites. Many facilities still run proprietary automation systems that need gateways, middleware, and custom engineering before AI tools can ingest and use the data. The cost is higher when building operators cannot accept long maintenance windows or downtime during control system work. The problem becomes harder in multi-site portfolios because utility interval data, billing formats, and demand charge structures still vary across service territories. In the United States AI-powered energy management software market, this keeps adoption faster among technically sophisticated enterprise buyers than among smaller owners with limited internal resources.

Cybersecurity and Critical Infrastructure Compliance Burden

Cybersecurity compliance adds cost, longer procurement cycles, and design limits for vendors serving utility and critical infrastructure customers. The Federal Energy Regulatory Commission approved NERC CIP-015-1 in June 2025, requiring internal network security monitoring for medium and large bulk electric system cyber systems with external routable connectivity, and high- and medium-impact entities must reach full compliance by October 1, 2028. This means vendors need stronger audit trails, clearer configuration baselines, and architecture choices that hold up under formal compliance review. Smaller companies can find it harder to absorb the burden because compliance work competes with product development and customer delivery. In the United States AI-powered energy management software market, the result is a slower rollout in regulated utility environments, even when the operating need for AI is clear.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Signals a Platform Maturation Shift

Software accounted for 74.50% of the 2025 segment mix, while services is projected to expand at a 20.80% CAGR through 2031. This split shows that the United States AI-powered energy management software market still draws most revenue from the core platform layer, but growth is moving toward implementation and post-deployment support. Buyers are asking for more than dashboards because integration, optimization, and reporting now affect realized savings and compliance outcomes. That makes professional and managed services more central to vendor strategy than in earlier phases of adoption.

The services opportunity includes system integration, AI model tuning, ongoing performance monitoring, and carbon reporting support. In the United States AI-powered energy management software industry, this reflects a shift from software procurement alone to outcome-based engagements that remain active after installation. Bidgely's 2025 launch of UtilityAI Pro across AWS, Snowflake, and Databricks environments supports this direction because it lets utilities run proprietary models within their own data environments while leaning on vendor expertise. As building owners face recurring compliance and optimization needs, vendors with strong service delivery can hold relationships longer and defend pricing more effectively.

By Deployment Mode: Cloud Platforms Lead, Hybrid Architectures Gain Strategic Traction

Cloud-based deployment held 58.20% of the market in 2025 and also posts the fastest projected CAGR at 21.10% through 2031. This leadership reflects the advantage of real-time data ingestion, centralized updates, and benchmarking across multi-site portfolios. The United States AI-powered energy management software market has favored cloud platforms because large users need a single operating view across buildings, devices, and utility interfaces. That is especially useful when companies manage many sites with different demand profiles and compliance obligations.

On-premises deployments still matter in industrial and utility settings where direct cloud exposure remains limited by operating policy or security design. Hybrid models are gaining importance because they allow latency-sensitive controls at the edge while sending portfolio data to the cloud for analytics and reporting. The United States AI-powered energy management software market is therefore not moving toward cloud in a simple way, but toward architecture choices that match site-level risk and control needs. Vendors that support flexible deployment models are better positioned to serve utilities, critical facilities, and large enterprises with mixed asset bases. Hybrid architectures are also being reinforced by vendor partnerships that connect edge and cloud capabilities. Honeywell's 2026 collaboration with Tata Consultancy Services points to broader OT and IT convergence for autonomous operations.

By Application: Demand Optimization Anchors Revenue as Renewable Integration Accelerates

Energy consumption and demand optimization accounted for 33.50% of the 2025 application mix, while renewable energy forecasting and integration is projected to grow at a 21.80% CAGR through 2031. The United States AI-powered energy management software market still earns most application revenue from bill reduction and load management because those benefits are easier to measure and approve internally. Demand optimization remains the anchor for broad adoption across utilities, commercial portfolios, and industrial sites. At the same time, renewable integration is rising faster because operating conditions are becoming harder to manage with fixed schedules and static forecasting methods.

Nature Communications published a 2026 research showing that probabilistic day-ahead forecasting methods can reduce renewable curtailment and improve ancillary service optimization when integrated into energy management platforms.[3]Nature Communications, “Probabilistic Day-Ahead Forecasting of System-Level Renewable Energy and Electricity Demand,” Nature Communications, nature.com That supports a stronger demand for software that can connect forecast quality with dispatch and procurement choices. The United States AI-powered energy management software market is therefore widening from efficiency-focused applications into coordination across variable generation, reserve planning, and real-time operations. This is particularly relevant where renewable penetration is rising, and system operators need more confidence in short-term balancing decisions.

By End User: Utilities Lead Portfolio, Residential Adoption Curve Steepens

Utilities held 36.50% of the 2025 end-user base, while residential buildings is projected to grow at a 21.50% CAGR through 2031. This makes utilities the largest institutional buyers in the United States AI-powered energy management software market, while the fastest growth is moving into the household layer. Utilities lead because they are investing in grid digitization, distributed resource management, and demand response at scale. They also act as a distribution channel that can extend software use into downstream customer programs.

Commercial buildings and industrial facilities remain large demand centers because they face direct pressure from energy cost management, operational continuity, and building-level carbon reporting. Residential growth is rising because smart meters, home electrification, and flexible load programs are creating a more active market for home energy optimization. The United States AI-powered energy management software market, therefore, has a two-layer structure in which utilities buy for system needs and also help activate customer-side participation. That pattern strengthens software demand across both centralized and distributed use cases.

Geography Analysis

The Northeast is the most mature regional pocket within the United States AI-powered energy management software market because policy pressure, power costs, and institutional demand are all strong in the same geography. Massachusetts, New York, New Jersey, and Connecticut have layered building benchmarking rules, emissions goals, and demand response structures that support continuous software use. The Institute for Market Transformation noted that Newton, Massachusetts, adopted its Building Emissions Reduction and Disclosure Ordinance in December 2024, covering 385 commercial buildings across 25.3 million square feet.[4]Institute for Market Transformation, “2025 Building Policies Outlook, More and Smaller Cities Still Passing Building Performance Standards,” Institute for Market Transformation, imt.org The same source noted that Clayton, Missouri, adopted a benchmarking ordinance in February 2025, which shows that policy spread is not limited to the largest coastal cities.

This policy density supports stronger demand from building owners that need reporting, optimization, and compliance tracking on an ongoing basis. It also suits large portfolios in finance, healthcare, and education because these users often need standardized reporting across many sites. In the United States AI-powered energy management software market, the Northeast stands out not because of one single trigger, but because regulation and operating economics reinforce each other. That combination tends to support earlier adoption of broader software suites instead of stand-alone monitoring tools. The region, therefore, remains important for vendors selling portfolio-wide carbon, energy, and operational management functionality.

Texas and the South Central region offer the strongest near-term expansion case in the United States AI-powered energy management software market because demand growth is being driven by new load rather than by regulation alone. Rising data center power requirements are tightening the need for real-time optimization, flexibility, and site-level control across the ERCOT footprint. In this geography, software value is tied closely to uptime, peak management, and the ability to respond quickly to grid conditions. That makes the buying case immediate for high-load industrial operators and technology facilities. The Western states form another growth pocket, led by California's push toward AI-enabled grid operations. California announced a pilot in July 2025 using OATI's Genie AI platform for outage management, which indicates stronger utility-side acceptance of AI in live grid workflows.

Competitive Landscape

The United States AI-powered energy management software market is moderately concentrated, with a leading group of global building and energy technology companies and a wider field of AI-focused specialists. Schneider Electric, Siemens, Johnson Controls International, Honeywell International, ABB, Emerson Electric, and Trane Technologies benefit from long customer relationships, integrated automation stacks, and broad service networks. These incumbents can layer AI software onto installed equipment and building management systems, which lowers account acquisition friction. That advantage remains important in large commercial, industrial, and utility settings where buyers prefer fewer integration points.

Strategic activity shows that major vendors are buying or partnering for AI capability instead of building every function internally. Johnson Controls acquired Nantum AI in April 2026 to add HVAC optimization and building energy algorithms to its OpenBlue platform. Trane Technologies completed its acquisition of BrainBox AI in January 2025, bringing autonomous HVAC controls and generative AI building technology into its portfolio. Schneider Electric and Kraken announced a partnership in June 2026 to connect EcoStruxure DERMS with demand-side flexibility orchestration, which shows a broader move toward end-to-end grid and customer coordination. In the United States AI-powered energy management software market, these moves narrow the gap between energy software, grid software, and building controls.

White-space demand still exists in the mid-market commercial building range, where buyers are too large to ignore compliance needs but too small for some enterprise-priced solutions. Another opening remains in data center power flexibility, where software must operate closer to high-density AI compute loads and fast grid events. The United States AI-powered energy management software market is therefore competitive, but it is not settled across all use cases. Product depth in controls integration, demand flexibility, and site-level orchestration is becoming more important than stand-alone analytics alone.

United States AI-Powered Energy Management Software Industry Leaders

GridPoint, Inc.

Bidgely, Inc.

Uplight, Inc.

EnergyCAP, LLC

BrainBox AI Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: EnergyCAP launched Watts Chat, the first generative AI capability built on its Watts AI engine, delivering natural-language access to financial-grade utility data for energy, sustainability, and finance teams. The release marks EnergyCAP's entry into agentic AI for energy management and is available to all existing customers at no additional license cost.

- June 2026: Schneider Electric and Kraken announced a partnership to combine EcoStruxure DERMS with Kraken's demand-side flexibility orchestration platform. The collaboration enables distribution system operators and utilities to forecast congestion, monitor grid conditions, and shift electricity demand in real time, targeting faster load interconnection without additional infrastructure buildout.

- May 2026: Uplight and The Brattle Group released research demonstrating that an integrated demand stack strategy could increase a representative utility's flexible capacity from 146 MW to 235 MW by 2030, a 60% gain, through coordinated demand response, energy efficiency, and time-of-use programs.

- April 2026: Johnson Controls acquired Nantum AI, a New York-based AI energy optimization company, integrating its proprietary HVAC optimization and building energy algorithms into the OpenBlue digital ecosystem to accelerate AI-driven energy management across commercial, industrial, and healthcare portfolios.

United States AI-Powered Energy Management Software Market Report Scope

The United States AI-powered energy management software market comprises software platforms and associated services that utilize artificial intelligence (AI), machine learning (ML), advanced analytics, and predictive algorithms to monitor, analyze, forecast, and optimize energy consumption across utilities, commercial buildings, industrial facilities, and residential environments. These solutions enable organizations to improve operational efficiency, reduce energy costs, support decarbonization objectives, optimize distributed energy resources (DERs), and enhance grid reliability through real-time and predictive decision-making.

The United States AI-Powered Energy Management Software Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Smart Grid and Distributed Energy Resource (DER) Management, Renewable Energy Forecasting and Integration, and Energy Trading, Pricing and Market Intelligence), and End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential Buildings). Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings |

Key Questions Answered in the Report

What is the 2031 value outlook for AI-powered energy management software in the United States?

The market is forecast to reach USD 3.19 billion by 2031 from USD 1.40 billion in 2026, growing at an 18.00% CAGR over 2026 to 2031.

Which component category leads current revenue?

Software led the 2025 mix with a 74.50% share, while services is growing faster at a 20.80% CAGR through 2031.

Why are utilities the largest buyers of these platforms?

Utilities held 36.50% of the 2025 end-user base because they are investing in grid digitization, demand response, and distributed energy resource management at scale.

Which deployment model is gaining the most momentum?

Cloud-based deployment held 58.20% share in 2025 and is also the fastest-growing deployment mode with a 21.10% CAGR through 2031.

Which application area is expanding fastest?

Renewable energy forecasting and integration is the fastest-growing application with a 21.80% CAGR through 2031, while demand optimization still held the largest 2025 share at 33.50%.

What is slowing adoption in older facilities?

Brownfield integration costs, legacy control systems, and cybersecurity compliance are extending deployment timelines, especially in older commercial and industrial assets.

Page last updated on: