United Kingdom AI-powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

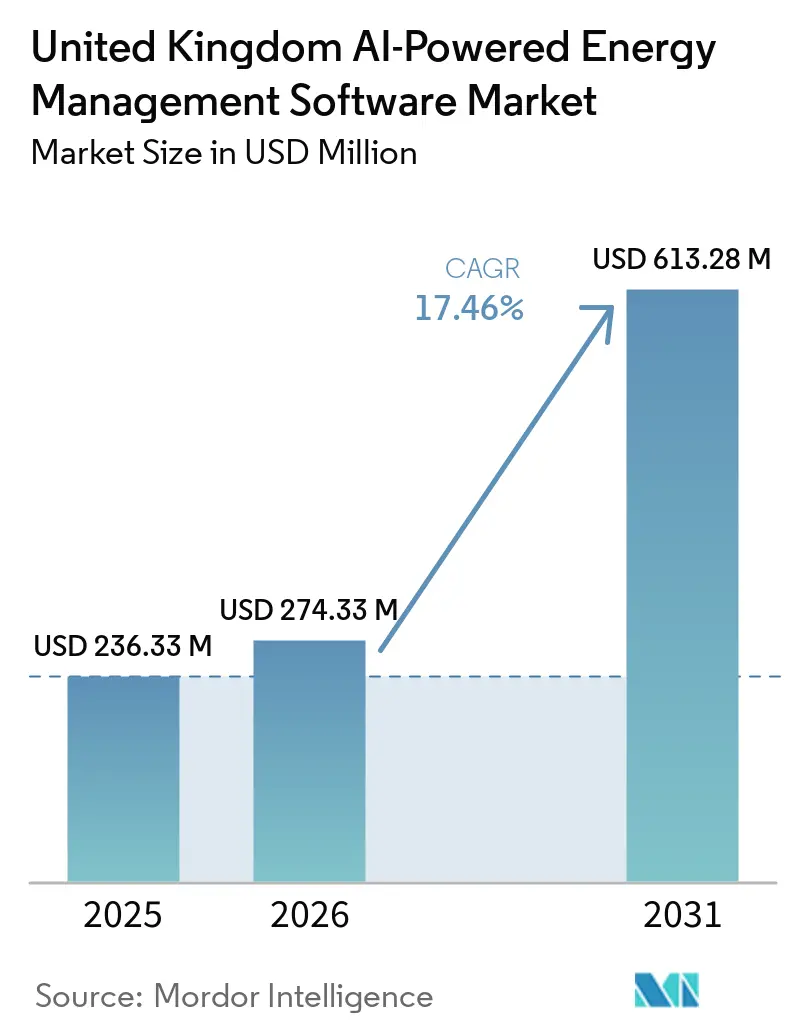

| Base Year Market Size (2025) | USD 236.33 Million |

| Market Size (2026) | USD 274.33 Million |

| Market Size (2031) | USD 613.28 Million |

| Growth Rate (2026 - 2031) | 17.46% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom AI-powered Energy Management Software Market Analysis by Mordor Intelligence

The United Kingdom AI-powered Energy Management Software Market size was valued at USD 236.33 million in 2025 and estimated to grow from USD 274.33 million in 2026 to reach USD 613.28 million by 2031, at a CAGR of 17.46% during the forecast period 2026-2031. The UK AI-powered energy management software market is being shaped by the country’s net-zero 2050 target and the Clean Power 2030 push, both of which are making digital control of flexible energy assets more central to system planning. The UK AI-powered energy management software market is also gaining support from the Energy Digitalization Framework, which is moving the sector toward common interoperability standards and more coordinated data sharing. Rising power cost pressure, broader carbon reporting obligations, and the need to manage demand with greater accuracy are pushing buyers to move from basic monitoring tools to decision-oriented platforms. The United Kingdom AI-powered Energy Management Software Market is also seeing demand from AI-related power loads, especially as new digital infrastructure increases pressure on grid access and connection management. At the same time, legacy operational technology, long integration cycles, and stricter cyber assurance requirements are shaping vendor strategy, contract design, and deployment timelines across the UK AI-powered energy management software market.

Key Report Takeaways

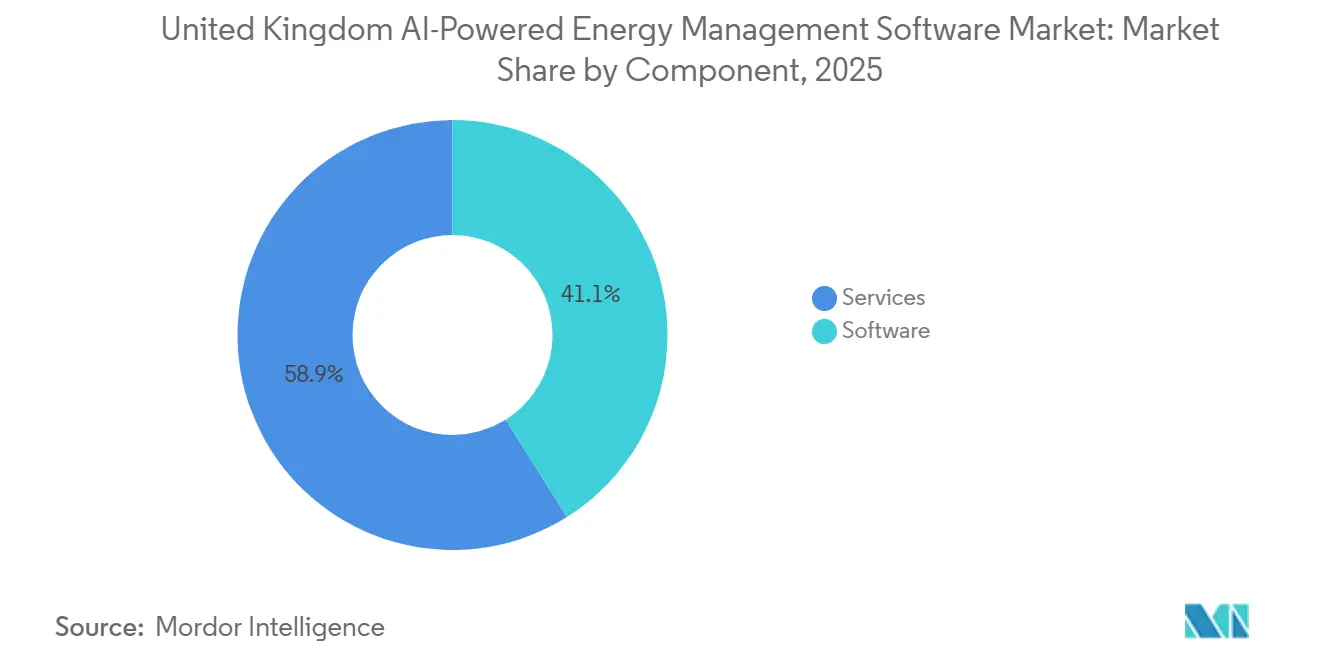

- By offering, software led with 41.07% revenue share of the United Kingdom AI-powered Energy Management Software Market in 2025, while services are projected to expand at 19.78% CAGR through 2031.

- By deployment mode, cloud-based platforms held 58.15% share of the UK AI-powered energy management software market in 2025, while hybrid deployment is projected to expand at 18.67% CAGR through 2031.

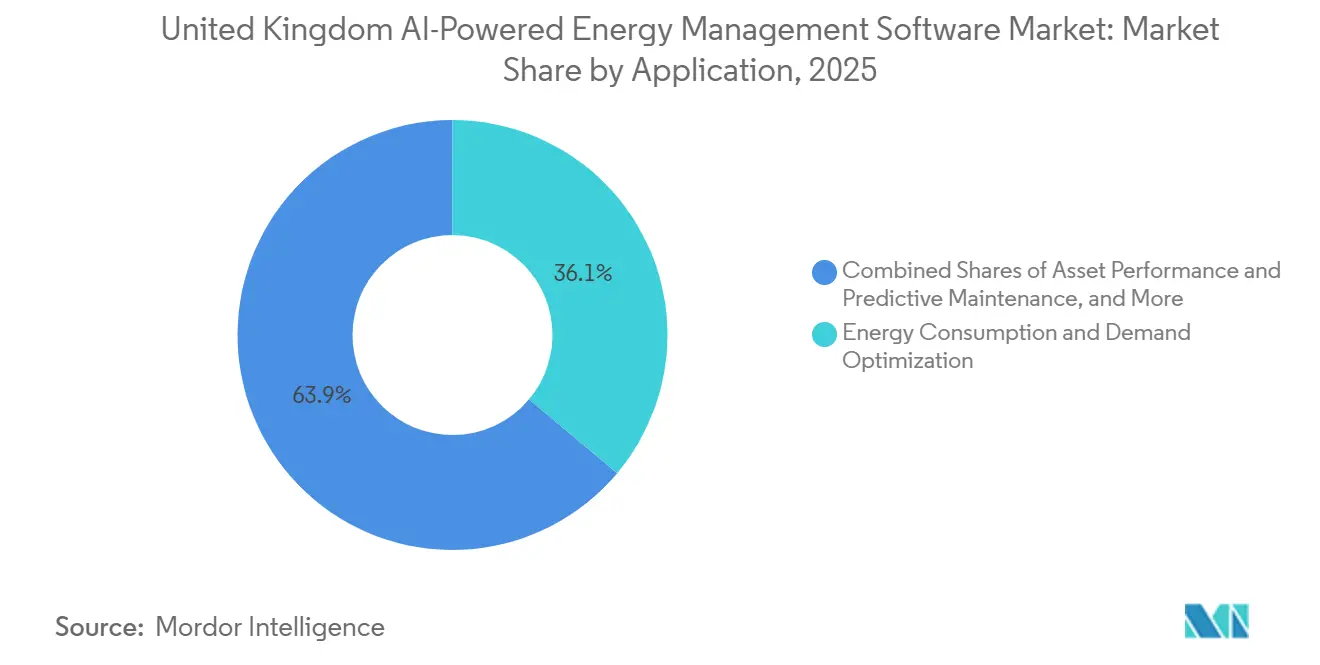

- By application, energy consumption and demand optimization accounted for 36.11% share of the United Kingdom AI-powered Energy Management Software Market in 2025, while asset performance and predictive maintenance are projected to expand at 19.62% CAGR through 2031.

- By end user, commercial buildings held 34.04% of the UK AI-powered energy management software market share in 2025, while utilities are projected to expand at 20.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom AI-powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Based Real-Time Load Optimization Across Distributed Assets | +4.8% | Global, with concentrated UK grid-edge deployment in South East England and AI Growth Zones | Short term (≤ 2 years) |

| UK Net-Zero Compliance and Carbon Reporting Pressure | +4.2% | National, UK-specific policy mandate under DESNZ and Ofgem frameworks | Long term (≥ 4 years) |

| Rising Electricity Price Volatility and Peak Demand Exposure | +3.2% | National, with acute pressure in London and South East industrial and data center clusters | Short term (≤ 2 years) |

| Smart Meter, IoT, and Building Automation Data Readiness | +2.3% | National, with accelerating non-domestic rollout in urban commercial centers | Medium term (2-4 years) |

| Digital Twin Adoption for Predictive Energy Control | +1.8% | National, concentrated in National Grid transmission and distribution system operator planning | Medium term (2-4 years) |

| Data Center, Commercial Property, and Industrial Efficiency Mandates | +1.4% | National, concentrated in London and South East and government-designated AI Growth Zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI-Based Real-Time Load Optimization Drives Structural Platform Demand

The United Kingdom AI-powered Energy Management Software Market is gaining from the shift in real-time load optimization from a performance feature to a grid management requirement as distributed assets become harder to coordinate. National Grid’s Emerald AI trial showed that AI-enabled data centers could flex power demand by up to 40% in under a minute in response to live grid signals. The Department for Science, Innovation and Technology stated in June 2026 that probabilistic and risk-aware optimization is the key feature that separates production-grade deployment from pilot activity in clean energy applications. This matters because many grid-edge and industrial assets need control decisions in sub-second timeframes, which gives an advantage to suppliers that combine edge computing with AI rather than relying only on remote cloud execution. As a result, buying criteria in the United Kingdom AI-powered Energy Management Software Market are moving toward local inference, rapid response, and deeper control-system integration.

UK Net-Zero Compliance Generates Policy-Led Software Demand

The United Kingdom AI-powered Energy Management Software Market is also supported by policy obligations that are more durable than short-cycle cost-reduction programs. The government’s climate action update in June 2026 backed the proposed 7th Carbon Budget, which targets an 87% reduction in emissions across 2038-2042 and reinforces the long planning horizon for low-carbon infrastructure decisions.[1]Department for Science, Innovation and Technology, “Interim AI Adoption Plan, Clean Energy,” GOV.UK, gov.uk The Energy Digitalization Framework described digitalization as enabling infrastructure for a coordinated, connected energy system and tied it directly to the need for 51-66 GW of flexible capacity. The same policy direction is likely to shorten the path from strategy to procurement, especially for regulated operators, which typically accelerate system investment once governance standards and data rules are formalized. This gives the UK AI-powered energy management software market a policy base that extends beyond energy savings alone and supports demand in utilities, infrastructure, and larger commercial estates.

Rising Electricity Price Volatility Sharpens The Commercial Case

Electricity cost pressure remains a direct demand driver for the UK AI-powered energy management software market, as unstable energy bills make cost-saving optimization easier to justify.[2]UK Parliament House of Commons Library, “Gas and Electricity Prices During the Energy Crisis and Beyond,” House of Commons Library, commonslibrary.parliament.uk The UK Parliament House of Commons Library reported that UK wholesale electricity prices had risen 26.29% since the start of 2026 and that retail unit prices were set to rise another 6% in July 2026 under the Ofgem price cap path. It also noted that mid-2026 geopolitical disruption pushed gas prices to double from their early March 2026 levels, which added another layer of operating uncertainty for energy-intensive buyers. UK Steel reported that British steelmakers paid 40% more for electricity than French peers in 2025/26, which added GBP 41 million, USD 52.35 million, to annual electricity bills.[3]UK Steel, “Industrial Electricity Prices, Barrier to Growth and Competitiveness,” UK Steel, uksteel.org This kind of price gap strengthens the case for AI-led demand response, tariff management, and process optimization across industrial and commercial accounts in the United Kingdom AI-powered Energy Management Software Market.

Smart Meter And IoT Data Readiness Expands AI Use Cases

The United Kingdom AI-powered Energy Management Software Market is benefiting from a wider flow of structured consumption data, especially from smart metering and connected building systems. As of 2025, 41 million smart and advanced meters were in operation across Great Britain, which represented 71% of all meters, and more than 37 million were operating in smart mode or classified as advanced meters. The post-2025 non-domestic rollout framework also projected a net present value of GBP 161 million (USD 205.58 million) to GBP 340 million (USD 434.15 million) from expanded non-domestic smart meter coverage by 2030. Elexon’s Market-wide Half-Hourly Settlement work is turning this larger meter base into 30-minute consumption signals, which supports predictive load forecasting, tariff optimization, and automated demand response at building and portfolio scale.[4]Elexon, “Digitalisation Strategy and Action Plan,” Elexon, elexon.co.uk The installation pace slowed by 5.8% in 2025, but that slowdown may itself increase demand for productivity-focused analytics as suppliers work against the 2030 completion timetable.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy OT Integration And Data Interoperability Complexity | -1.4% | National, with acute impact on aging transmission assets and industrial OT environments | Long term (≥ 4 years) |

| Cybersecurity And Data Sovereignty Concerns | -0.9% | National, critical infrastructure focus across transmission, distribution, and flexibility platforms | Medium term (2-4 years) |

| Unclear Payback Period For Mid-Market Buyers | -0.5% | National, concentrated among SMEs and multi-site operators outside enterprise procurement | Short to Medium term (2-4 years) |

| Shortage Of AI, Energy, And Controls Talent | -0.4% | National, acutely felt outside the London and South East technical hiring hub | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy OT Integration And Data Interoperability Complexity Slows Deployment

Legacy control environments remain a major brake on the United Kingdom AI-powered Energy Management Software Market because many energy assets were not designed for interoperable data exchange or modern cyber controls. DESNZ research on operational technology vulnerabilities stated that many of these systems have little integrated protection beyond the IT network that manages them. This pushes buyers into longer deployment cycles because platform providers must address data extraction, control logic, safety validation, and compliance review before live operation begins. The Energy Sector Cyber Security Strategy for 2026-2030 calls the bridge between OT engineering and cybersecurity one of the hardest and most important issues in the sector. Until common architectures are more widely established, integration costs will remain uneven across projects and will keep slowing deployment in the United Kingdom AI-powered Energy Management Software Market.

Cybersecurity And Data Sovereignty Concerns Constrain Enterprise Adoption Pace

Cyber assurance is another constraint on the United Kingdom AI-powered Energy Management Software Market, as energy operators are being asked to prove resilience, not just policy alignment. Ofgem’s January 2026 update to NIS guidance for downstream gas and electricity operators reflects a system that is far more digital and distributed than it was when the original framework was introduced.[5]Ofgem, “NIS Guidance for Downstream Gas and Electricity Operators of Essential Services in Great Britain v3.0,” Ofgem, ofgem.gov.uk The scope of regulation is also widening to include large load control as an essential service, which brings AI-enabled flexibility and demand-side platforms into a stricter assurance environment. National security treatment of some energy system data further narrows the set of acceptable hosting and processing arrangements for certain contracts. These conditions delay commercial go-live even when the software is technically ready, which weighs most on regulated users in the United Kingdom AI-powered Energy Management Software Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Leads While Services Gain Momentum

Software held 41.07% of the market in 2025, making it the leading offering in the United Kingdom AI-powered Energy Management Software Market. Buyers favored integrated software because it could combine baseline monitoring, optimization, and reporting in a single operating layer. This was especially relevant for commercial buildings, utilities, and industrial facilities that needed better visibility across multiple assets and reporting requirements. The SaaS model also supported wider adoption by reducing initial contract size and allowing vendors to expand later through analytics modules, connectors, and integration layers.

Services are projected to expand at a 19.78% CAGR through 2031, making them the fastest-growing segment. This growth reflects the fact that many buyers need help with OT integration, model retraining, controls tuning, and ongoing reporting after the initial software purchase. Trane Technologies’ move into BrainBox AI showed how equipment and building-system players are using AI software capabilities to deepen long-term service value in energy management and autonomous building control.[6]Trane Technologies and BrainBox AI Inc., “Trane Technologies Launches BrainBox AI Lab to Transform Energy Management and Sustainability in Buildings,” BrainBox AI, brainboxai.com In practice, the value gap between software installation and realized savings is pushing more contracts toward managed or outcome-linked services across the UK AI-powered energy management software market.

By Deployment Mode: Cloud Remains Largest While Hybrid Fits Operational Needs

Cloud-based deployment accounted for 58.15% of the United Kingdom AI-powered Energy Management Software Market size in 2025, which kept it as the dominant deployment model. Many commercial building operators preferred cloud platforms because they offered faster onboarding and lower infrastructure burden than isolated on-premises systems. Cloud platforms also fit well with broader interoperability goals because they can expose standardized interfaces across meter, asset, and consumer data environments. This made cloud deployment a practical choice in less latency-sensitive use cases where central analytics and portfolio-wide visibility mattered most.

Hybrid deployment is projected to expand at a 18.67% CAGR through 2031 and is gaining popularity because some control decisions must be made close to the asset. Battery storage, EV charging, heat pumps, and smart inverters often need very fast local decision-making, which pure cloud architectures cannot always deliver. The push toward hybrid systems is therefore based on operational need as much as on cyber assurance or data residency concerns. This balance between central analytics and local control is likely to keep hybrid adoption strong as the UK AI-powered energy management software market moves deeper into utility, industrial, and grid-edge use cases.

By Application: Demand Optimization Leads While Asset Performance Advances Fast

Energy consumption and demand optimization accounted for 36.11% of the United Kingdom AI-powered Energy Management Software Market in 2025, making it the largest application area. Its lead came from the direct savings opportunity tied to energy use, tariff management, and load shifting in a high-cost operating environment. The large installed base of smart and advanced meters has also made this segment more actionable because consumption data is now available at a much higher frequency than before. This created a broader commercial base for anomaly detection, automated scheduling, and consumption forecasting across the UK AI-powered energy management software market.

Asset performance and predictive maintenance are projected to expand at a 19.62% CAGR through 2031, making it the fastest-growing application segment. Growth in this area is tied to the age profile of network infrastructure and the need to improve visibility into asset condition before failures occur. The FoSMo project, led by National Grid, Keen AI, and UK Power Networks, demonstrated how shared AI models can support visual condition monitoring and reduce customer interruptions and annual power loss. As this model spreads, vendors will have more room to build differentiated applications on top of common monitoring capabilities rather than competing only on basic detection features.

By End User: Commercial Buildings Lead While Utilities Set The Growth Pace

Commercial buildings accounted for 34.04% of the market in 2025, making them the largest end-user segment in the United Kingdom AI-powered Energy Management Software Market. Large building portfolios in London and the South East have been the natural early buyers because multi-site operations create stronger savings visibility and easier software scaling across assets. Carbon reporting, energy audits, and building performance goals have also supported the broader adoption of AI-based diagnostics and controls in this segment. These conditions gave commercial real estate and institutional property owners a relatively clear operating case for adoption.

Utilities are projected to expand at a 20.54% CAGR through 2031, making them the fastest-growing end-user group. Their growth is tied more to regulated digital procurement and flexibility management needs than to simple internal efficiency programs. Kyndryl and UK Power Networks illustrated this direction with the Megawatt Dispatch platform, launched with NESO support to improve renewable energy distribution and coordinated flexibility dispatch in South East England. Residential and industrial demand also continues to build, and Passiv Systems’ June 2026 heat pump compatibility expansion showed how AI-enabled controls are widening the practical deployment base outside large enterprise estates.

Geography Analysis

England remained the clear center of the United Kingdom AI-powered Energy Management Software Market in 2025, with the Greater London and South East corridor holding the deepest mix of demand concentration and vendor activity. Commercial building density, grid connection pressure, and the presence of large energy users give this region the broadest near-term demand base for optimization, control, and compliance software. The Department for Science, Innovation and Technology stated that the UK would need at least 6 GW of AI-capable data center capacity by 2030, which reinforces the importance of energy management tools around high-load infrastructure. National Grid and Atos launched Triton in January 2026 to cover the England and Wales transmission network, and the tool reduced network reinforcement planning decision time by 70%. This kind of planning digitization supports a wider rollout path for the United Kingdom AI-powered Energy Management Software Market because it links AI from individual facilities to system-level infrastructure decisions.

Scotland and Wales are developing a different demand profile within the UK AI-powered energy management software market, with more weight on renewable integration, flexibility management, and distributed control. Their energy mix makes forecasting and dispatch more important, especially where intermittent generation and electrified residential loads are rising together. The Future Homes Standard and the spread of smart control technologies are also creating more repeatable residential deployment routes across England and Wales. The same transmission and flexibility tools piloted in England are becoming more transferable to Scotland and Wales as grid operators expand digital asset management and system balancing programs.

Northern Ireland has a more distinct operating context because it participates in the all-island Single Electricity Market with the Republic of Ireland. That reduces the direct role of some Great Britain policy mechanisms, but it creates room for vendors that can work across cross-border balancing, renewable forecasting, and flexibility settings. Across all UK nations, policy-backed digitalization and AI-related infrastructure growth are widening the regional opportunity set beyond the South East alone. This means the United Kingdom AI-powered Energy Management Software Market is likely to broaden geographically over the forecast period even though England will continue to set the pace for scale and procurement depth.

Competitive Landscape

The United Kindom AI-powered energy management software market is moderately fragmented, with competition spread across building control platforms, grid flexibility tools, utility demand management software, and AI-native analytics providers. No single company holds a dominant position across all major application areas, which keeps competition focused on integration depth, deployment capability, and regulatory readiness rather than on scale alone. The Energy Digitalization Framework has also shifted the competitive test toward interoperability across the core energy system, behind-the-meter assets, consumer domain, and metering data domain. This favors companies that can cleanly connect to future UK data-sharing architectures without forcing customers into major system redesign. The United Kindom AI-powered energy management software market is therefore moving toward a model where technical fit and governance readiness matter as much as software feature breadth.

Large incumbents are using acquisitions, partnerships, and bundled deployments to protect or expand their positions. Trane Technologies’ acquisition-led expansion around BrainBox AI showed how established building-system players are adding autonomous AI control to strengthen their software and services footprint. National Grid and Keen AI’s FoSMo initiative, supported by Ofgem’s innovation funding, also set a precedent for shared foundational models in grid asset monitoring. If that model spreads, vendors will need to differentiate more strongly through workflow design, integration speed, and decision-support layers rather than relying solely on basic monitoring.

Smaller and UK-origin players are building position through niche strengths and scalable software platforms. Kaluza’s September 2025 global licensing agreement with ENGIE showed that a UK-developed energy intelligence platform could scale across 20 million business-to-consumer contracts worldwide. Kyndryl and UK Power Networks also showed that coordinated flexibility dispatch is becoming a more credible option at the commercial and network operations layers in the UK. Companies that can combine certified data connectivity, control-system familiarity, and fast deployment will be better placed to win in the United Kindom AI-powered energy management software market as procurement becomes more formal and more technical.

United Kingdom AI-powered Energy Management Software Industry Leaders

Schneider Electric SE

Siemens AG

C3.ai, Inc.

Uplight, Inc.

GridBeyond Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: ev.energy launched Eve, an AI-native multi-DER orchestration platform that coordinates EVs, home batteries, solar, and other flexible loads as a single dispatchable resource. Eve is deployed across 55+ programs and 300,000+ customers in North America and Europe, with UK utility customers as a target segment for expansion.

- June 2026: Passiv Systems Limited expanded its Smart Thermostat compatibility to 17 heat pump manufacturers, aligning with the UK Smart and Secure Energy Systems framework and the Future Homes Standard, enabling AI-driven tariff and solar optimization from initial installation.

- May 2026: DESNZ, NCSC, NESO, and Ofgem jointly published the Energy Sector Cyber Security Strategy (2026-2030), establishing a four-year roadmap to strengthen cyber resilience across Great Britain’s digitalized energy system, with explicit targets to bridge the OT-engineering-to-cyber gap by end-2027.

- January 2026: National Grid and Atos launched Triton, a digital twin and data visualization tool covering the England and Wales transmission network, reducing the time required for network reinforcement planning by 70% and directly supporting the Great Grid Upgrade program.

United Kingdom AI-powered Energy Management Software Market Report Scope

The United Kingdom AI-powered Energy Management Software Market Report is Segmented by Component (Software and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Application (Energy Control, Asset Performance, Smart Grid Analytics, Renewable Energy Management, and Energy Trading), and End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings |

Key Questions Answered in the Report

What is the current and forecast value of the United Kingdom AI-powered energy management software space?

The United Kingdom AI-powered Energy Management Software Market was valued at USD 236.33 million in 2025, stands at USD 274.33 million in 2026, and is forecast to reach USD 613.28 million by 2031 at a 17.46% CAGR.

What is driving adoption of AI-based energy software in the United Kingdom?

The main factors are net-zero compliance, flexible grid requirements, rising electricity price volatility, broader smart meter data availability, and stricter energy reporting and control needs.

Which offering type leads spending in this field?

Software led with 41.07% share in 2025, while services are growing faster because buyers increasingly need support for integration, retraining, and ongoing optimization.

Which deployment model is growing fastest for UK buyers?

Cloud-based deployment remained the largest at 58.15% share in 2025, but hybrid deployment is growing fastest at 18.67% CAGR because many use cases need both central analytics and local control.

Which application area has the strongest position today?

Energy consumption and demand optimization led with 36.11% share in 2025, supported by higher-value use cases in tariff management, load shifting, and high-frequency monitoring.

Which end-user group is expanding fastest?

Utilities are projected to grow at 20.54% CAGR through 2031 because regulated digital procurement, flexibility programs, and grid modernization are pushing AI adoption faster in that segment.

Page last updated on: