AI-Powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.85 Billion |

| Market Size (2031) | USD 11.76 Billion |

| Growth Rate (2026 - 2031) | 19.38% CAGR |

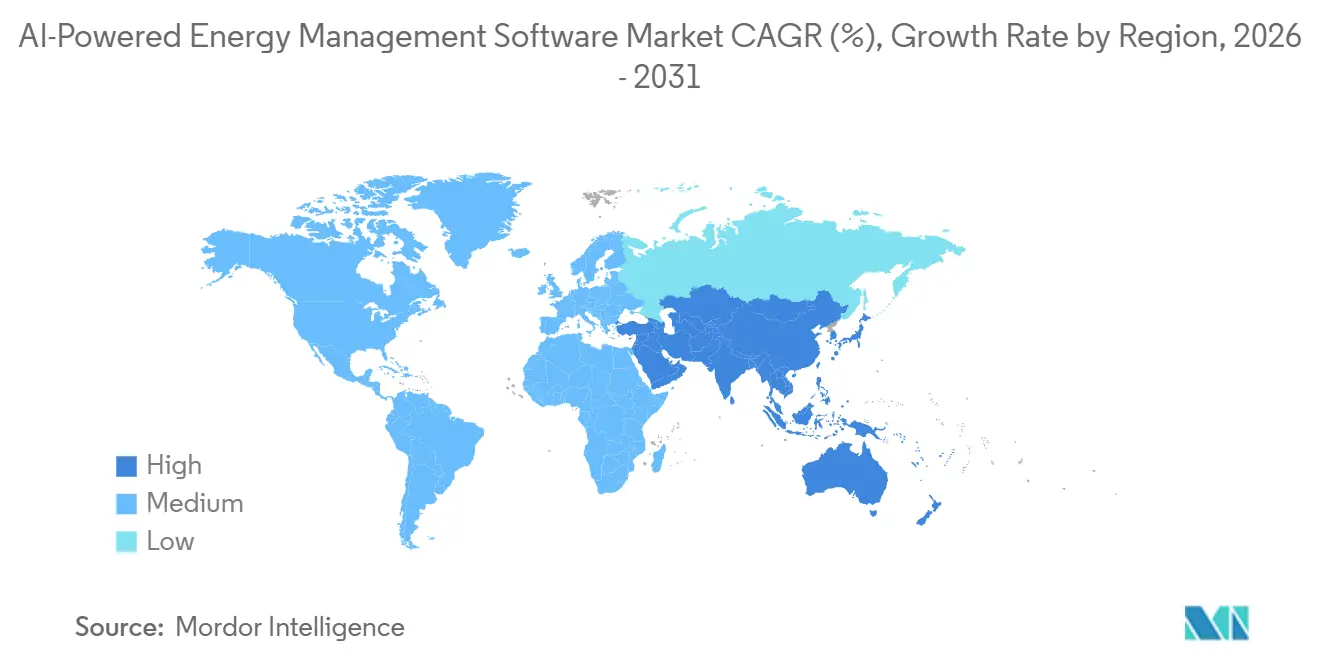

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

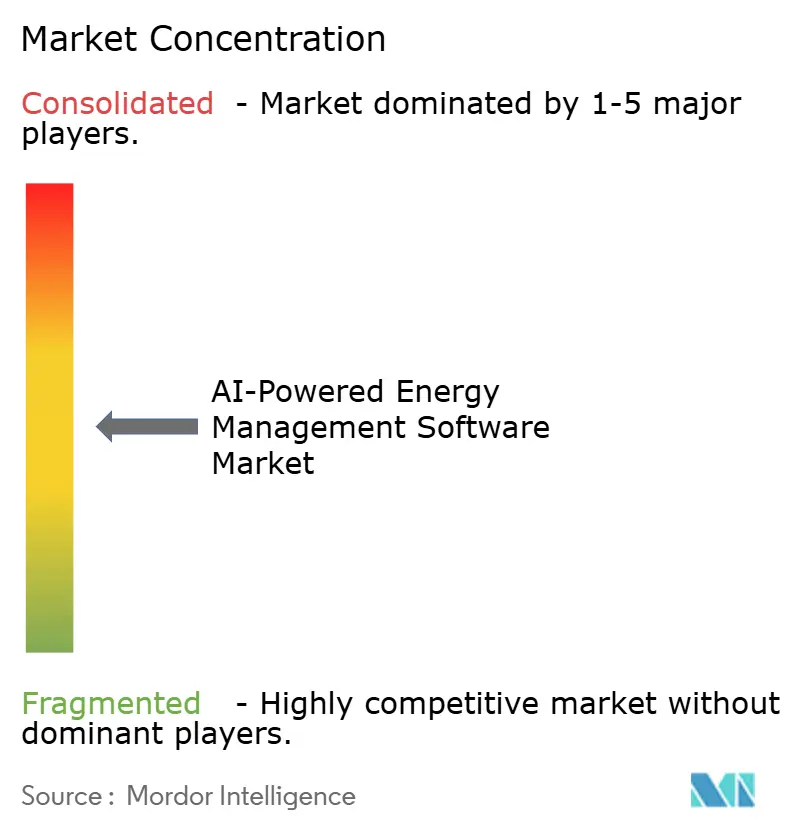

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-Powered Energy Management Software Market Analysis by Mordor Intelligence

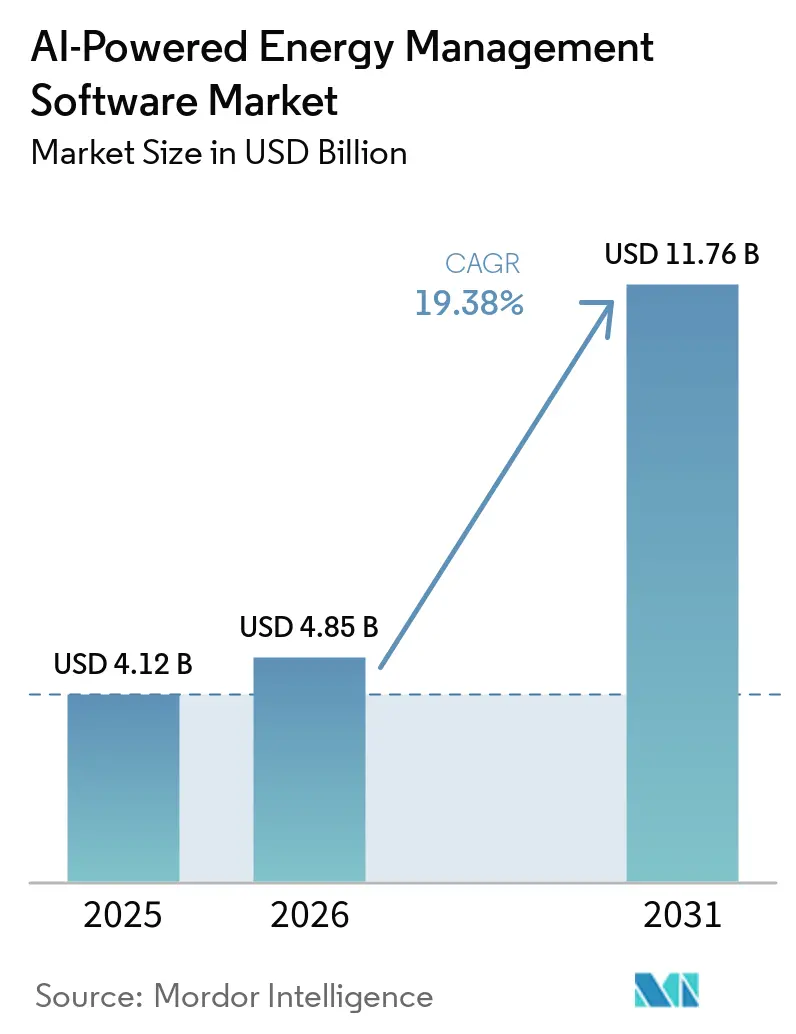

The AI-powered energy management software market size is expected to grow from USD 4.12 billion in 2025 to USD 4.85 billion in 2026 and is forecast to reach USD 11.76 billion by 2031 at 19.38% CAGR over 2026-2031. Growth in the AI-powered energy management software market is being shaped by stricter energy disclosure rules, more volatile grid conditions, and broader use of AI in daily operations across buildings, utilities, and industrial sites. Buyers are moving beyond software that only tracks consumption, because they now want systems that can recommend or automate load shifts, improve renewable balancing, and support predictive maintenance inside the same operating environment. The competitive field is developing around large automation and building technology vendors with wide installed bases, while smaller AI-led companies are gaining traction where model precision and application depth matter more than scale. The AI-powered energy management software market is also opening new opportunities for hybrid delivery models, managed services, and retrofit-led deployments, as many users need both real-time control and stronger analytics without replacing their entire installed infrastructure. Adoption still depends on integration quality, cybersecurity readiness, and the ability to prove savings within standard contract periods, especially in smaller facilities where the return profile is less visible.

Key Report Takeaways

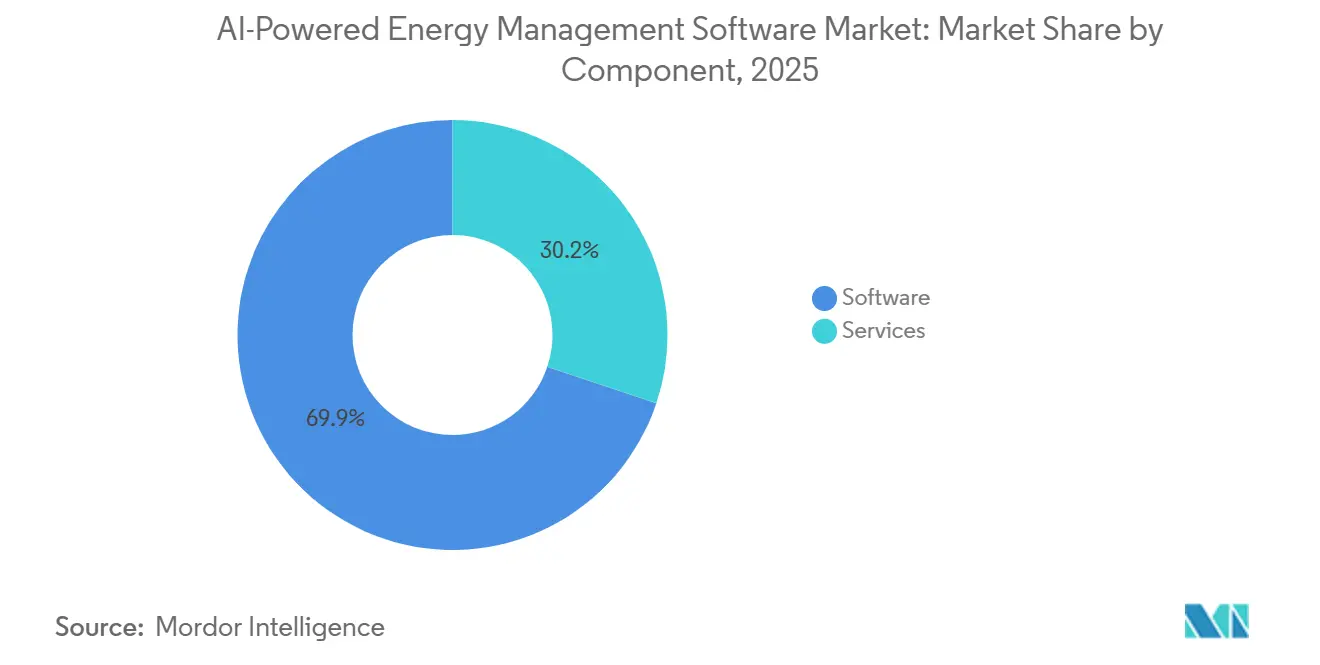

- By component, software held 69.85% share of the AI-powered energy management software market in 2025, while services are projected to expand at 20.12% CAGR through 2031.

- By deployment mode, cloud-based deployment held 66.41% share in 2025, while hybrid deployment is projected to expand at 19.92% CAGR through 2031.

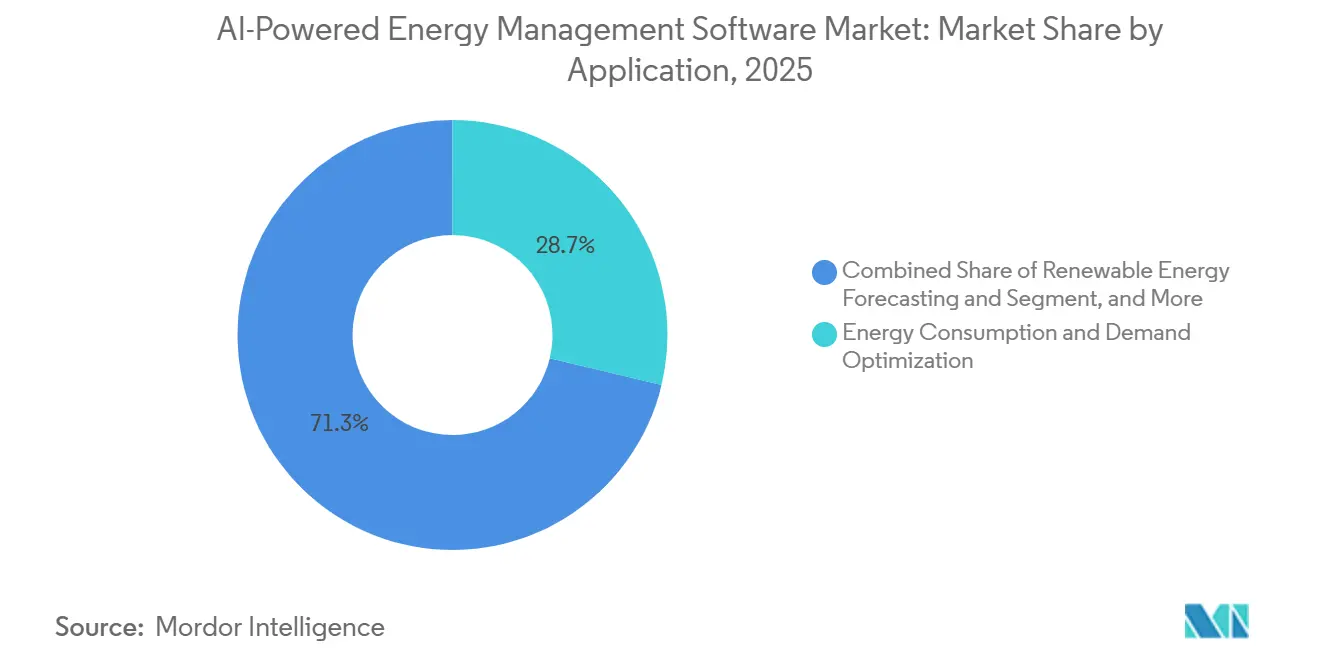

- By application, energy consumption and demand optimization accounted for 28.74% of the market share in 2025, while renewable energy forecasting and integration are projected to grow at a 20.34% CAGR through 2031.

- By end user, utilities held 30.12% share in 2025, while commercial buildings are projected to expand at 19.87% CAGR through 2031.

- By geography, Europe held 34.56% share in 2025, while Asia-Pacific is projected to grow at 20.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-Powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Need for Real-Time Energy Optimization in Commercial and Industrial Facilities | +4.2% | Global, concentrated in North America, Europe, and Asia-Pacific industrial corridors | Short term (≤ 2 years) |

| AI Integration With Smart Grids and Distributed Energy Resources | +3.8% | Global, with Asia-Pacific at the core and spillover into North America and Europe | Medium term (2-4 years) |

| Increasing Demand for Automated Demand Response and Peak Load Management | +3.2% | North America and Europe, with expansion in Asia-Pacific | Short term (≤ 2 years) to Medium term (2-4 years) |

| Expansion of ESG Reporting and Carbon Accounting Workflows | +2.6% | Europe, North America, and selective spillover into Asia-Pacific | Medium term (2-4 years) |

| Edge AI Adoption for Site-Level Energy Control and Fault Detection | +2.1% | Global, with Asia-Pacific and North America leading deployment scale | Medium term (2-4 years) |

| Growing Retrofit Demand From Aging Building and Industrial Infrastructure | +1.8% | North America and Europe, with brownfield industrial demand in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Need For Real-Time Energy Optimization in Commercial And Industrial Facilities

Real-time optimization is emerging as the clearest near-term value driver for the AI-powered energy management software market because it transforms software from a passive reporting layer into an active operating tool. Commercial and industrial users are facing sharper power price swings, wider time-of-use tariff exposure, and tighter internal pressure to reduce avoidable peak demand without affecting uptime.[1]B. Tang, “Building-Level Energy Prediction and Control Based on BIM and IIoT Technologies,” Scientific Reports, doi.org That is why the AI-powered energy management software market is gaining traction in facilities that need load schedules to adjust against live prices, production cycles, and changing site conditions rather than against fixed rules. A 2026 study showed that a schedule-aware XGBoost model using production-schedule inputs achieved an RMSE of 2.67 kW and an R² of 0.9698, supporting the case for high-accuracy forecasting in multi-line industrial settings without relying on full internal sensor visibility. This kind of performance matters because it makes AI useful in real operating environments where incomplete plant data often limits traditional optimization tools. As more sites seek to cut demand charges and stabilize energy use during volatile tariff windows, the AI-powered energy management software market is increasingly tied to daily operational savings rather than longer-cycle sustainability projects.

AI Integration With Smart Grids and Distributed Energy Resources

The rise of distributed energy resources is also driving the AI-powered energy management software market, as grid conditions are now shaped by rooftop solar, batteries, EV charging, and flexible loads that require constant coordination. Conventional dispatch logic struggles when power flows become bidirectional and when decisions must be made across thousands of small assets rather than a few centralized generation points. That shift is expanding the role of the AI-powered energy management software market from site-level optimization to grid-aware orchestration, where forecasting, balancing, and dispatch must work together. A 2026 paper on edge-AI-enabled renewable microgrid control demonstrated the technical maturity of secure, energy-efficient coordination across IoT-linked assets, reinforcing the broader move toward AI-led control in distributed energy systems. Japan’s decision to open low-voltage distributed energy resources to demand-response markets from FY2026 is expected to expand the domestic resource aggregator SaaS platform market by 33.5 times between FY2024 and FY2035, to JPY 6.7 billion, which was already converted to USD 44 million. The AI-powered energy management software market, therefore, benefits not only from more connected assets but also from rule changes that turn those assets into monetizable flexibility resources.[2]Nikkei, “RA Platform SaaS Market for Distributed Energy Resource Management,” Nikkei, nikkei.com

Increasing Demand for Automated Demand Response and Peak Load Management

Automated demand response is becoming a stronger buying trigger because large energy users are being asked to show controllable load in exchange for favorable tariffs, grid participation, or more resilient operating costs. Manual curtailment processes are harder to defend when the response window is measured in minutes or seconds and when a single decision must coordinate HVAC systems, batteries, process loads, and site controls simultaneously. The AI-powered energy management software market is well placed here because AI platforms can act on live data and execute site-specific actions without requiring an operator to step through each response event. This need is becoming more visible as utilities and large building portfolios seek repeatable load flexibility that can be documented, audited, and used across many facilities rather than managed as one-off interventions. The same trend is making the AI-powered energy management software market more relevant to power market participation, because peak management now affects both cost control and access to flexibility revenues. As adoption grows, vendors that can combine site automation, forecasting, and event execution into a single workflow are likely to hold a stronger position than those offering only monitoring and reporting.

Expansion of ESG Reporting and Carbon Accounting Workflows

Sustainability disclosure is changing software buying behavior because enterprises increasingly want a single system that connects energy data, carbon reporting, and operational actions. The AI-powered energy management software market is benefiting from this shift because energy performance is no longer viewed solely as a utility cost issue; it is also considered in audit trails, emissions reporting, and management accountability. In practice, that means buyers are giving greater weight to carbon accounting modules, Scope 2 traceability, and data structures that support both compliance and operating teams. The European Commission’s building decarbonization agenda and the implementation path under the recast EPBD have increased pressure for more granular building performance visibility, which supports greater use of digital tools that connect compliance and control. The technical checklist issued under CEN/TR 18276:2026 also reflects the move toward more formalized building automation compliance, which encourages software architectures that can document and structure energy data more consistently. As reporting expectations deepen, the AI-powered energy management software market is moving closer to the center of enterprise compliance and operating workflows rather than sitting at the edge of facilities management.[3]European Commission, “Commission Sets the EU's Building Sector on a Pathway Towards Greater Energy Efficiency and Decarbonisation,” European Commission, europa.eu

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity With Legacy OT and IT Systems | -2.8% | Global, most acute in North America and Europe with older industrial infrastructure | Medium term (2-4 years) |

| Data Quality, Interoperability, and Sensor Fragmentation Issues | -2.2% | Global, especially in Asia-Pacific brownfield sites and the Middle East and Africa | Long term (≥ 4 years) |

| Cybersecurity and Data Sovereignty Concerns for Critical Energy Assets | -1.6% | Global, with regulatory friction concentrated in Europe and North America | Medium term (2-4 years) |

| Payback Uncertainty in Small and Mid-Sized Sites With Limited Load Density | -1.1% | Global, with higher pressure in South America and the Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity Across Legacy OT and IT Systems

Legacy operational environments remain a major restraint because many plants, utilities, and large buildings still run on separate data layers, proprietary historians, and industrial protocols that were not built for modern AI workflows. In those environments, the AI-powered energy management software market cannot scale smoothly unless vendors can bridge SCADA, building management systems, enterprise software, and edge devices without disrupting live operations. This is a bigger issue than software compatibility alone, because strict IT-OT separation often forces vendors to redesign deployment patterns around segmented networks, local inference, and controlled data exchange. Rockwell Automation reported in 2025 that only 30% of organizations had fully integrated IT and OT security operations centers, underscoring the foundational coordination work that remains before AI can operate consistently across both environments. A 2025 technical report on cyber-physical situational awareness in energy systems also reflected how advanced control environments depend on secure, structured integration rather than simple data access. The AI-powered energy management software market, therefore, faces slower deployment cycles in brownfield settings, where architectural challenges are as important as software capabilities.[4]Rockwell Automation, “OT Cybersecurity in 2025: 6 Trends to Watch,” Rockwell Automation, rockwellautomation.com

Data Quality, Interoperability, and Sensor Fragmentation

Data quality remains a structural barrier because energy data often arrives from meters, sensors, building systems, and industrial controls that use different formats, sampling rates, and communications standards. That means the AI-powered energy management software market often has to solve data normalization and data cleaning before it can deliver optimization, forecasting, or predictive maintenance at the level promised during sales cycles. The burden is especially high in brownfield sites, where missing values, inconsistent tags, and incomplete telemetry can delay model training and reduce confidence in automated recommendations. A 2026 paper noted that AI systems in energy settings must connect with existing SCADA platforms, IoT networks, and data lakes, while legacy infrastructure often lacks the real-time access pattern required for AI-led automation. This issue not only slows implementation but also makes expansion from pilot projects to multi-site programs more difficult, as each new site may introduce another data-mapping problem. Until interoperability improves, the AI-powered energy management software market will continue to incur additional costs and time at the integration stage, especially in facilities without dedicated engineering support.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Managed Services Extend Spending Beyond Licenses

Software held a 69.85% share in 2025, indicating that most spending still sat in core platforms rather than in surrounding support layers. That lead reflects the installed-base advantage of vendors already embedded in utility control rooms, building systems, and industrial optimization environments, where switching risk is high and integration history matters. In the AI-powered energy management software market, these software platforms usually combine dashboards, forecasting engines, dispatch logic, carbon accounting modules, and overlays that sit above existing control systems rather than replacing them. This position also benefits from data network effects: the longer a platform remains in use, the more valuable its operational history becomes for tuning models and maintaining customer relationships. The software category, therefore, keeps a durable revenue base even as buyers broaden their requirements.

Services are projected to grow at a 20.12% CAGR through 2031, making them the fastest-growing component of the AI-powered energy management software market. The main reason is that energy AI becomes less accurate without regular retraining to account for local load behavior, changing tariffs, weather shifts, and new asset configurations. A 2026 study on cache-augmented multimodal generative AI for predictive maintenance supported the value of ongoing model support because the architecture outperformed standalone analytical approaches in real-time anomaly detection for energy-intensive equipment. Buyers also need service support for integration, model governance, user enablement, and audit-ready reporting, especially when they use AI to support ISO 50001 or internal performance reviews. That pattern is widening the revenue pool beyond one-time license sales and pushing more recurring relationships into the AI-powered energy management software industry.

By Deployment Mode: Hybrid Models Balance Control And Scale

Cloud-based deployment accounted for 66.41% of the AI-powered energy management software market share in 2025, as it supports faster onboarding, simpler updates, and easier integration with enterprise data environments. This model works well for commercial building operators and mid-sized industrial users that want analytics, reporting, and optimization without large on-site infrastructure commitments. In the AI-powered energy management software market, cloud delivery also enables centralized portfolio visibility, which is important when a single owner manages many facilities across multiple locations. The scale advantage is meaningful because it allows vendors to roll out new functions faster and lets customers compare energy performance across sites within one environment. That is why cloud remains the volume leader even as users ask for more site-specific control.

Hybrid deployment is projected to grow at a 19.92% CAGR through 2031, and the AI-powered energy management software market for hybrid deployment is projected to expand at a 19.92% CAGR as utilities and large industrial operators seek both edge responsiveness and cloud analytics. This pattern is gaining strength because many high-value use cases need low-latency action at the site while still depending on heavier forecasting and optimization workloads in the cloud. A 2025 article on edge AI fault detection reported 92.0% detection rates with response times below 150 milliseconds, compared with 200 milliseconds for cloud alternatives, while using less energy per inference cycle. A separate 2026 study on renewable microgrid control further supported the deployment of edge AI for energy-critical cyber-physical coordination. On-premises deployment still plays a defined role, where data sovereignty and critical infrastructure requirements limit remote processing, but the strongest growth is toward mixed architectures rather than either extreme alone.

By Application: Renewable Forecasting Raises Performance Standards

Energy consumption and demand optimization accounted for 28.74% of the market in 2025, making it the largest application because it applies across almost every facility type and usually offers the clearest payback path. This use case often serves as the entry point into the AI-powered energy management software market, as customers can link it directly to demand charge reduction, tariff response, and operating discipline without waiting for a broader digital transformation program. Demand optimization is also easier to explain internally, since finance, operations, and sustainability teams can all see the same savings logic from the same data stream. That broad relevance gave it a larger base than specialized applications tied to particular asset types or market structures. It remains the most common first purchase, even when long-term platform plans are more comprehensive.

Renewable energy forecasting and integration is projected to grow at a 20.34% CAGR through 2031, and the AI-powered energy management software market for renewable energy forecasting and integration is projected to expand at a 20.34% CAGR as variable generation creates greater scheduling pressure. Solar and wind output introduce uncertainty that static dispatch tools cannot manage well enough once renewable penetration reaches scale, especially in balancing environments that penalize deviations. The AI-powered energy management software market is therefore placing greater value on models that combine weather, satellite, and operational data to deliver better day-ahead and intraday forecasts. C3 AI’s June 2026 expansion with Shell, covering more than 13,000 pieces of equipment and adding AI agent-based root-cause analysis, shows how predictive and operational AI is moving deeper into large energy systems rather than remaining at the pilot stage. Smart grid and distributed energy resource management are also growing quickly as EV charging, storage, and rooftop generation increase coordination needs, while energy trading and pricing tools are gaining relevance where liberalized power markets expose customers to real-time price movement. Together, these shifts are raising the technical standard for the AI-powered energy management software market and pushing vendors toward broader orchestration capability.

By End User: Commercial Buildings Grow Fast While Utilities Stay Largest

Utilities held a 30.12% share in 2025, making them the largest end-user group, as they already manage grid-side operations, distributed assets, and regulated procurement structures that support software adoption. In the AI-powered energy management software market, utilities also benefit from larger operating datasets and clearer reasons to invest in dispatch coordination, renewable balancing, and load flexibility. Their role is changing from retrospective analytics to always-on operational optimization, favoring platforms embedded closer to dispatch and field systems rather than tools used only for periodic reporting. That shift helps explain why utilities kept the volume lead even as other buyer groups accelerated. Their spending is anchored by system needs rather than by isolated building or equipment use cases.

Commercial buildings are projected to grow at a 19.87% CAGR through 2031, and the AI-powered energy management software market for commercial buildings is projected to expand at a 19.87% CAGR as building owners seek lower energy costs and greater reporting visibility without large structural retrofits. This demand is being supported by tighter building automation requirements, broader emissions reporting expectations, and the need to manage multi-site portfolios with fewer manual interventions. Honeywell’s 2025 launch of Honeywell Connected Solutions, with Verizon Communications and Vanderbilt University among early adopters, showed how major vendors are positioning AI-led building management for mainstream enterprise and institutional use. Industrial facilities remain a high-value group because of their high energy intensity and visible downtime costs, but implementation complexity often slows rollout compared with commercial buildings. Residential buildings are still the smallest by revenue, yet they carry meaningful unit-growth potential as home energy management, storage, solar, and EV charging become more connected. The result is a broader end-user base for the AI-powered energy management software market, with utilities holding the largest volume and buildings driving faster expansion.

Geography Analysis

Europe held 34.56% of the AI-powered energy management software market share in 2025, as regulation around buildings, energy performance, and reporting is more developed there than in other regions. The recast EPBD entered into force in 2024, and EU member states must transpose it into national law by May 29, 2026, thereby increasing the practical relevance of building automation and control systems in large non-residential properties. The technical report CEN/TR 18276:2026 adds a compliance checklist for building automation under the EPBD framework, which supports more formal implementation pathways for digital energy management systems. Germany, the United Kingdom, France, and Italy remain the main country markets, while the Nordics and Central and Eastern Europe are building momentum through renovation activity, electrification, and stricter efficiency standards.

Asia-Pacific is projected to grow at a 20.45% CAGR through 2031, making it the fastest-growing region in the AI-powered energy management software market. China leads regional deployment volume because grid modernization, industrial scale, and dual-carbon goals create a large need for optimization across power and facility systems. India is also becoming more important as compliance-linked energy management demand builds in major industrial corridors, especially where large energy users face tighter monitoring and audit expectations. Japan adds another growth layer as low-voltage distributed energy resources enter demand-response participation from FY2026, expanding the economic case for software that can aggregate and control flexible assets. South Korea and Australia are also supporting the regional outlook through higher renewable integration and grid digitization, while Southeast Asia offers a longer runway in brownfield industrial retrofits as manufacturing capacity expands.

North America held a substantial share in 2025, supported by mature demand-response structures, deep adoption of commercial buildings, and strong investment in AI-related infrastructure. The region also benefits from a large base of utilities and enterprise operators willing to connect operational data to cloud-scale AI environments when security and control requirements are met. AWS was named a strategic cloud provider for Siemens Energy in April 2026, reflecting how major vendors are combining operational domain expertise with hyperscale computing support in the energy field. South America remains an emerging part of the AI-powered energy management software market, while the Middle East and Africa are still earlier in adoption but continue to attract selective investment as renewable buildout and infrastructure modernization advance.

Competitive Landscape

The AI-powered energy management software market is moderately consolidated at the top, with large industrial automation and building technology companies using their installed base strength, broad product portfolios, and long enterprise relationships to defend their leadership. Schneider Electric, Siemens, Honeywell, Johnson Controls, and ABB compete across multiple functions, such as monitoring, forecasting, predictive maintenance, building controls, and distributed energy management, which gives them an advantage with larger accounts that want a single integrated platform. At the same time, AI-native companies continue to win attention in narrower use cases where model performance, deployment speed, or application depth matter more than platform breadth. This creates a two-level structure within the AI-powered energy management software market, where incumbents lead in scale, and challengers often drive innovation faster within targeted workflows. The result is a competitive field that is active but not dominated by a single company or product architecture.

Strategic moves in 2026 show that incumbents are still expanding AI capability through partnerships and acquisitions instead of relying only on internal development. Johnson Controls acquired Nantum AI in April 2026 to strengthen OpenBlue with HVAC optimization and airflow management algorithms, which points to the value placed on proven energy-saving intelligence that can be embedded into an existing installed base. AWS also became a strategic cloud provider for Siemens Energy in April 2026, showing how the AI-powered energy management software market is increasingly tying operational technology platforms to hyperscale computing environments for model deployment and digital transformation. Honeywell’s February 2026 partnership with Tata Consultancy Services followed the same logic, combining Honeywell Forge IoT analytics with broader enterprise integration capability to support autonomous operations in building and industrial settings. These moves show that competitive advantage now depends as much on delivery architecture and integration reach as on core algorithms.

The AI-powered energy management software market still has clear barriers to entry, especially where deployments touch grid operations, critical infrastructure, or tightly segmented OT environments. Vendors that can document strong cyber-physical awareness, secure integration design, and reliable control workflows are better positioned to compete for larger utility and industrial contracts. Model accuracy is becoming more important, but accuracy alone is not enough if a vendor cannot integrate quickly, support governance needs, and prove savings within a short operating cycle. This leaves room for specialists in areas such as energy trading, real-time demand flexibility, and distributed asset orchestration, but it also means the AI-powered energy management software market favors companies that can pair AI capability with mature deployment discipline.

AI-Powered Energy Management Software Industry Leaders

Siemens AG

Schneider Electric SE

ABB Ltd.

Honeywell International Inc.

IBM Corporation 7.0%

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: C3 AI and Shell extended their multi-year collaboration under a new agreement, scaling C3 AI Reliability across Shell's global operations to cover more than 13,000 pieces of equipment, the extension adds AI agent-based root cause analysis and automated maintenance remediation beyond equipment anomaly detection, deployed on Microsoft Azure.

- April 2026: Johnson Controls acquired Nantum AI, a New York-based company specializing in AI algorithms for HVAC performance optimization and real-time airflow management, strengthening the OpenBlue digital ecosystem with proven, proprietary energy-savings capabilities across healthcare campuses and advanced manufacturing facilities.

- April 2026: AWS was designated as strategic cloud provider for Siemens Energy under an expanded collaboration to advance digital transformation in the energy sector and develop new approaches to energy infrastructure management for Amazon data center scaling.

- February 2026: Honeywell and Tata Consultancy Services, TCS, announced a strategic partnership to integrate Honeywell Forge IoT analytics with TCS IT and consultancy capabilities, enabling enterprise-wide autonomous operations for building and industrial clients by unifying OT data flows with IT systems.

Global AI-Powered Energy Management Software Market Report Scope

The AI-Powered Energy Management Software market refers to intelligent platforms and services that leverage artificial intelligence, machine learning, and advanced analytics to optimize energy consumption, improve operational efficiency, and support sustainability goals across diverse sectors. These solutions provide capabilities such as real-time energy visibility and demand optimization, predictive asset maintenance, smart grid and distributed energy resource (DER) management, renewable energy forecasting and integration, and energy trading with market intelligence.

The AI-Powered Energy Management Software market report is segmented by Component (Software and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Smart Grid and Distributed Energy Resource (DER) Management, Renewable Energy Forecasting and Integration, Energy Trading, Pricing and Market Intelligence), End User (Utilities, Commercial Buildings, Industrial Facilities, Residential Buildings), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment Mode | Cloud-Based | ||

| On-Premises | |||

| Hybrid | |||

| By Application | Energy Consumption and Demand Optimization | ||

| Asset Performance and Predictive Maintenance | |||

| Smart Grid and Distributed Energy Resource (DER) Management | |||

| Renewable Energy Forecasting and Integration | |||

| Energy Trading, Pricing and Market Intelligence | |||

| By End User | Utilities | ||

| Commercial Buildings | |||

| Industrial Facilities | |||

| Residential Buildings | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast value of the AI-powered energy management software market?

The AI-powered energy management software market was valued at USD 4.12 billion in 2025, stands at USD 4.85 billion in 2026, and is forecast to reach USD 11.76 billion by 2031 at 19.38% CAGR.

Which region leads adoption of AI-powered energy management software?

Europe led with 34.56% share in 2025, supported by a dense regulatory framework around building performance, automation, and compliance.

Which region is expected to grow fastest through 2031?

Asia-Pacific is projected to expand at 20.45% CAGR through 2031, supported by grid modernization, distributed energy resource growth, and regulatory changes in markets such as Japan.

Which component is growing fastest in this space?

Services are the fastest-growing component at 20.12% CAGR because customers increasingly need model retraining, integration support, managed analytics, and reporting support after deployment.

What is the largest application for AI-powered energy management software?

Energy consumption and demand optimization held the largest share at 28.74% in 2025 because it applies across most facility types and has a clearer savings case than narrower use cases.

Which end-user group offers the strongest near-term growth opportunity?

Commercial buildings are projected to grow at 19.87% CAGR through 2031, while utilities remain the largest end-user segment with 30.12% share in 2025.

Page last updated on: