Nordic AI-powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

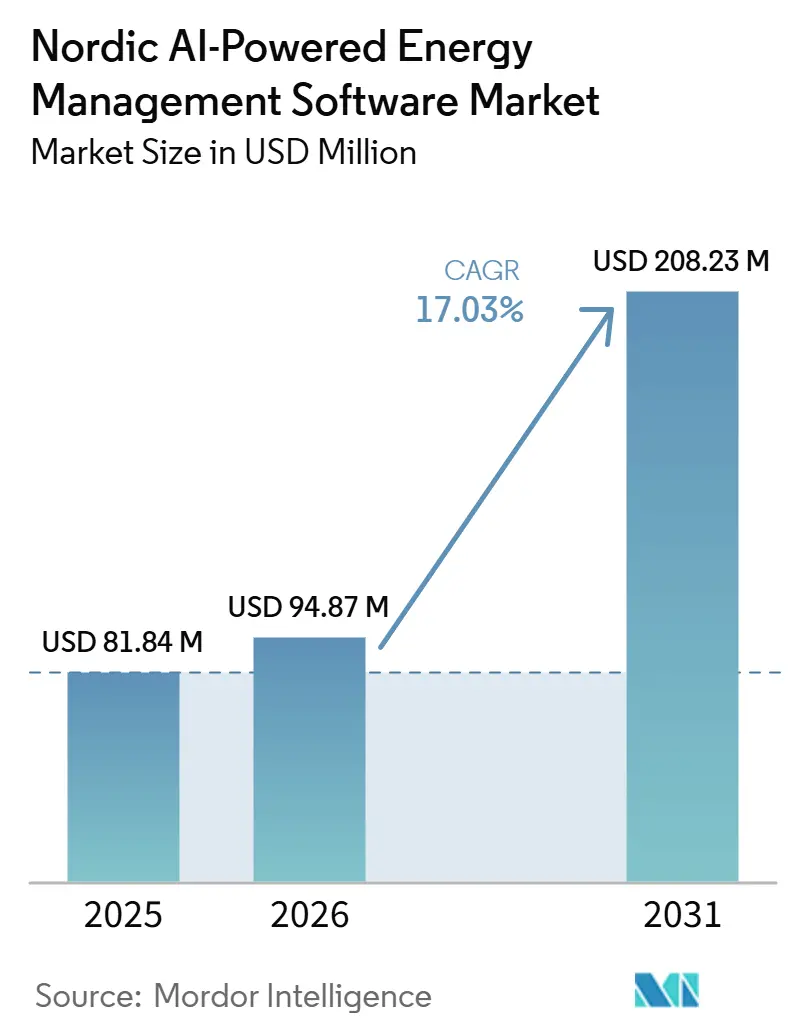

| Base Year Market Size (2025) | USD 81.84 Million |

| Market Size (2026) | USD 94.87 Million |

| Market Size (2031) | USD 208.23 Million |

| Growth Rate (2026 - 2031) | 17.03% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nordic AI-powered Energy Management Software Market Analysis by Mordor Intelligence

The Nordic AI-powered Energy Management Software Market size is projected to expand from USD 81.84 million in 2025 and USD 94.87 million in 2026 to USD 208.23 million by 2031, registering a CAGR of 17.03% between 2026 and 2031. The Nordic AI-powered Energy Management Software Market is growing in a region where power systems already rely heavily on renewable generation, but grid operators and energy users now need tighter alignment between variable supply and real-time demand than legacy tools can deliver. AI-based software is meeting that need by turning smart meter data, grid sensor feeds, and weather inputs into dispatch, forecasting, and optimization actions that have become commercially necessary since 2024. Compliance demand is also widening the buyer base, as CSRD reporting obligations and ESRS E1 energy disclosure requirements in 2026 are pushing large enterprises toward interval-level monitoring and audit-ready automation across commercial real estate and industrial operations. The Nordic AI-powered Energy Management Software Market is also being shaped by a strong shift toward cloud deployment, broader service-led contracts, and utility demand for flexibility orchestration, while interoperability issues in brownfield assets and higher cybersecurity compliance costs continue to slow adoption in parts of the installed base. Competition is intensifying as global automation vendors bundle software, hardware, and managed services, while Nordic specialists focus on targeted use cases such as frequency regulation, peak shaving, and intraday trading.

Key Report Takeaways

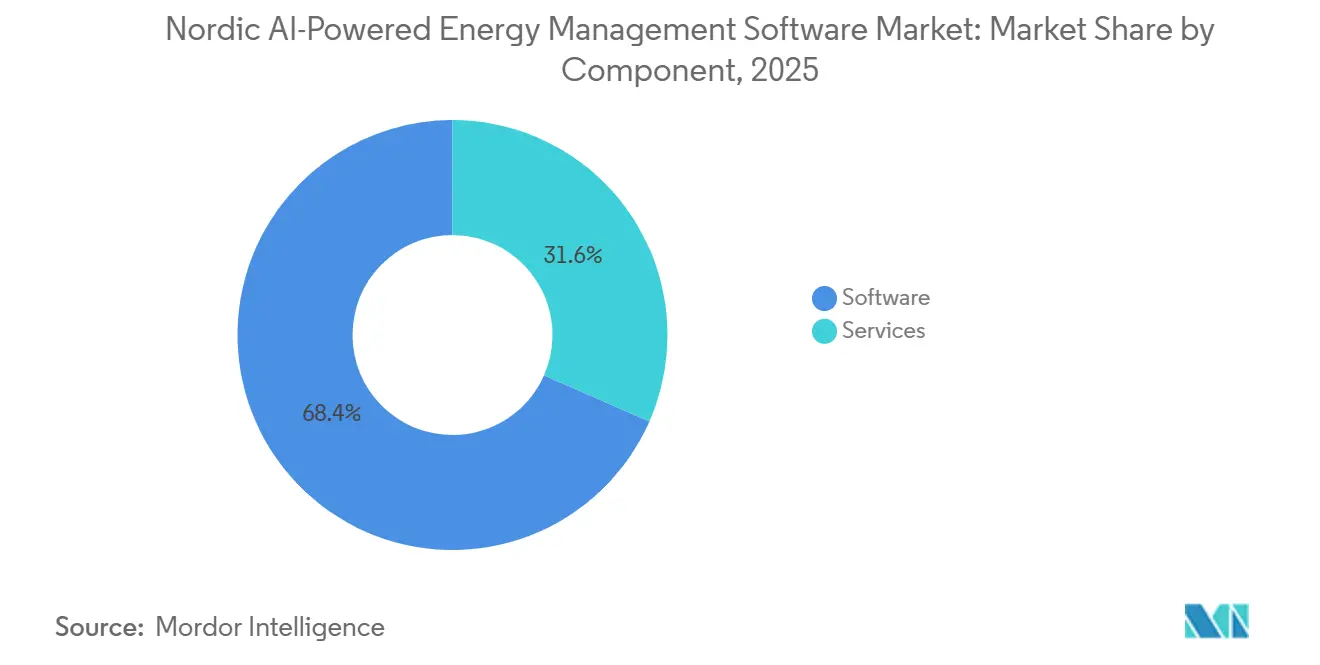

- By component, software held 68.42% of the Nordic Artificial Intelligence Powered Energy Management Software Market revenue in 2025, while services are projected to expand at a 19.91% CAGR through 2031.

- By deployment mode, cloud held 61.36% of the Nordic Artificial Intelligence Powered Energy Management Software Market revenue in 2025, while hybrid is projected to expand at a 19.46% CAGR through 2031.

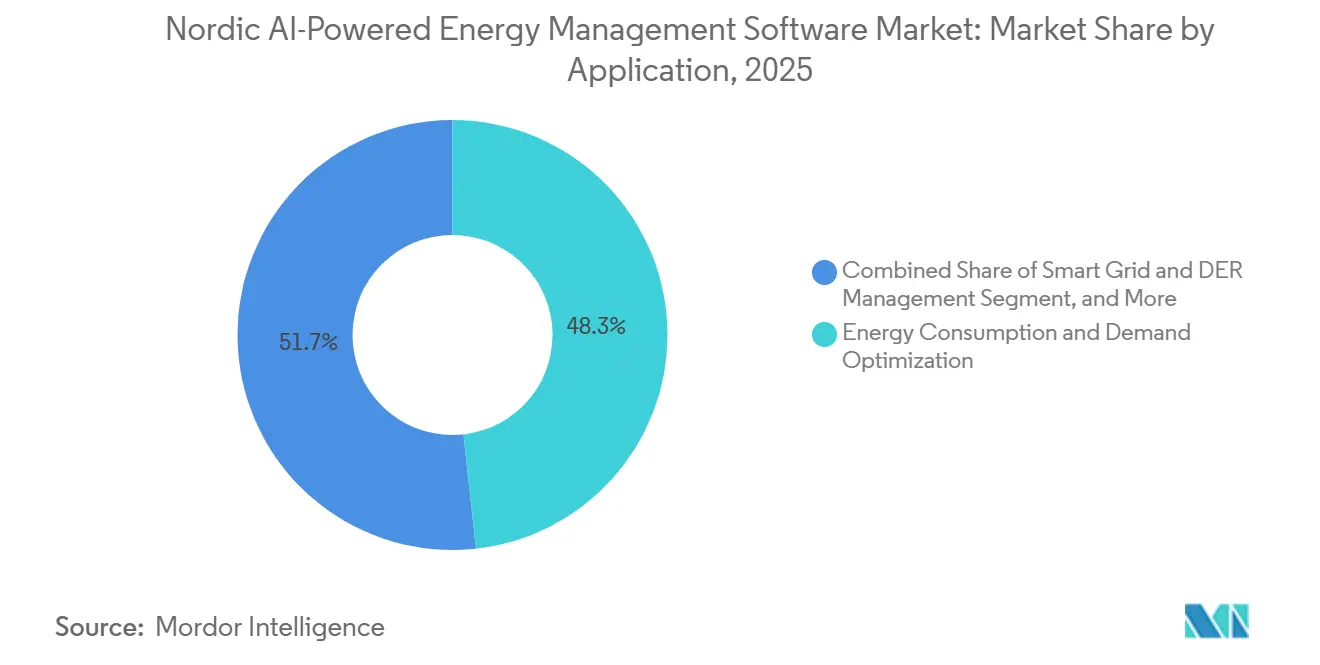

- By application, Energy Consumption and Demand Optimization accounted for 48.26% share of the Nordic AI-powered Energy Management Software Market size in 2025, while Renewable Energy Forecasting and Integration is projected to expand at an 18.34% CAGR through 2031.

- By end user, commercial buildings held 57.81% of revenue in 2025, while utilities are projected to expand at a 19.02% CAGR through 2031.

- By geography, Sweden held 47.23% of the Nordic AI-powered Energy Management Software Market share in 2025, while Denmark is projected to expand at an 18.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Nordic AI-powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Carbon Reporting and Net Zero Compliance Across Nordic Enterprises | +4.2% | Global, with concentrated effect across Sweden, Denmark, Norway, Finland | Short term (≤ 2 years) |

| Smart Meter and Grid Data Availability Improving Model Accuracy | +3.1% | Sweden, Finland, Norway core, spill-over to Denmark and Iceland | Medium term (2-4 years) |

| Utility and Building Automation Shift Toward AI Orchestration Layers | +2.6% | Denmark and Sweden primary, Norway and Finland secondary | Medium term (2-4 years) |

| Cloud-Delivered Analytics Reducing Upfront Deployment Friction | +2.3% | Global, particularly impactful for SME-dense Nordic markets | Short term (≤ 2 years) |

| Demand Response and Flexibility Markets Creating New Software Monetization Paths | +1.8% | Nordic cross-border, concentrated in Denmark, Sweden, Finland | Medium term (2-4 years) |

| Industrial Electrification Increasing Need for Real-Time Load Optimization | +1.5% | Sweden, Norway, Finland industrial clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Carbon Reporting and Net-Zero Compliance Across Nordic Enterprises

Mandatory CSRD-aligned reporting has moved AI energy software from a cost tool into a compliance requirement for many enterprise buyers in the Nordic AI-powered Energy Management Software Market. ESRS E1 reporting requires granular interval-level energy information across Scope 1 and Scope 2 boundaries, and manual reconciliation does not provide the level of consistency or audit quality that large organizations now need. The effect extends beyond utilities, as commercial property owners and industrial operators also need software that can document energy use more frequently. The compliance pull is set to widen further as the phased expansion from 2026 brings more mid-sized companies into the reporting framework. Nordic Energy Research reported in 2025 that all 5 Nordic countries remained below their carbon-neutrality path in industrial and heating activities, which keeps pressure high for more detailed consumption management and reporting discipline. Once the software is installed for disclosure and audit support, buyers often extend into optimization modules within 12 to 18 months, which supports longer customer relationships in the Nordic Artificial Intelligence Powered Energy Management Software Market.

Smart Meter and Grid Data Availability Improving Model Accuracy

The Nordic AI-powered Energy Management Software Market benefits from one of the strongest metering and grid data environments in the world. This matters because model quality depends on the breadth, frequency, and reliability of the input data feeding demand forecasts, load optimization, and renewable balancing logic. Sweden’s large installed metering base and grid-edge infrastructure support its leading revenue position, while Finland and Norway also provide strong conditions for model training and operational learning. The result is that platforms trained on Nordic conditions can produce more accurate forecasts and dispatch decisions than generic international products that were not built around the same market design and data depth. In 2026, Itron and Norgesnett announced the first grid-edge computing deployment in the Nordics, with 10,000 distributed intelligence-enabled smart endpoints supporting real-time grid awareness and flexible resource management. That widening data advantage is creating a structural edge for region-specialized vendors in the Nordic AI-powered Energy Management Software Market.

Utility and Building Automation Shift Toward AI Orchestration Layers

The Nordic AI-powered Energy Management Software Market is moving beyond rule-based control, as utilities and building operators increasingly seek AI layers that can optimize multiple inputs simultaneously. Traditional SCADA and building management systems were built for fixed logic, but newer software is expected to learn local load signatures, renewable generation patterns, and price response behavior across grid zones. This change is also altering how vendors compete, as buyers now consider model performance and workflow automation alongside interface quality. Schneider Electric introduced Foresight Operation in November 2025 as an AI-native platform that combines energy, power, and building systems into a single architecture, with a broader release planned for Q3 2026. In parallel, Siemens advanced its Building X roadmap in March 2025 with named generative AI agents that support a deeper, more autonomous control path within cloud-native building software.[1]Siemens AG, “Building X - AI-Native Building Platform,” Siemens AG, siemens.com As this layer becomes a recurring software service, the Nordic AI-powered Energy Management Software Market is shifting further from capital-led procurement toward operating expenditure models.

Cloud-Delivered Analytics Reducing Upfront Deployment Friction

Cloud delivery is lowering the cost and time barriers that historically limited adoption in the Nordic AI-powered Energy Management Software Market. Older on-premises deployments needed longer integration cycles, dedicated internal IT support, and more extensive commissioning, which kept many mid-sized sites out of the addressable pool. Cloud-based delivery reduces that burden by shortening implementation time and replacing large upfront spending with subscription payments that are easier to justify. This matters most in the sub-500-employee segment, where buyers remain sensitive to payback periods and internal technical staffing limits. The shift is also visible in product design, because software vendors are packaging upgrades, analytics, and support into managed services rather than one-time installations. Hybrid deployment still matters for utilities and industrial users with legacy control systems, but the larger direction of travel in the Nordic AI-powered Energy Management Software Market remains toward cloud-led analytics and vendor-managed software operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy OT and BMS Interoperability Constraints in Brownfield Assets | -3.2% | Sweden and Finland industrial sectors, Denmark and Norway commercial real estate | Medium term (2-4 years) |

| High Cybersecurity and Data Governance Expectations for Critical Infrastructure | -2.1% | Global, most acute in Norway and Denmark given critical infrastructure exposure | Short term (≤ 2 years) |

| Shortage of Nordic AI and Energy Analytics Specialists | -1.4% | Sweden, Finland, Norway, Denmark, concentrated in university cities | Long term (≥ 4 years) |

| Payback Sensitivity in Small and Medium-Sized Commercial Sites | -0.9% | Finland and Iceland SME-dense commercial portfolios | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy OT and BMS Interoperability Constraints in Brownfield Assets

A large share of the installed base of buildings and industrial systems in the Nordics still runs on OT and BMS platforms that were not built for open cloud connectivity. In the Nordic AI-powered Energy Management Software Market, this means many projects need protocol translation, edge devices, and specialized integration before any optimization layer can even start operating. The supplied draft noted that this early integration work can absorb 30% to 50% of total project budgets, which makes approval harder in sites where energy savings are not immediate or easy to measure. The issue is more persistent in facilities that cannot accept long shutdowns, because integration windows often align with scheduled maintenance cycles that can sit 2 to 3 years apart. This creates uneven adoption across brownfield commercial portfolios and industrial sites, even when the software value proposition is clear. The restraint, therefore, acts less like a short disruption and more like a structural brake on how quickly the Nordic AI-powered Energy Management Software Market can scale across legacy assets.

High Cybersecurity and Data Governance Expectations for Critical Infrastructure

Cybersecurity requirements are rising quickly for any vendor serving utilities and other critical energy assets in the Nordic AI-powered Energy Management Software Market. NIS2 implementation raised the compliance bar from October 2024, and utility buyers now expect tighter incident reporting, supply chain controls, and technical risk management before approving connected software. Vendors also need to show stronger audit trails and OT-oriented controls, including alignment with IEC 62443 expectations in many procurement processes. These steps increase development costs and extend qualification cycles, especially in public utility accounts, where security reviews now carry more weight than before. The effect is strongest when connected optimization touches operational environments rather than only business reporting layers. As a result, higher cybersecurity and data governance expectations are increasing sales friction even while they also strengthen long-term vendor quality standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Revenue Accelerates as Software Matures

Software held 68.42% of the Nordic AI-powered Energy Management Software Market in 2025, reflecting the earlier wave of enterprise platform adoption among large utilities and commercial building operators. Much of that base was built through multi-year licensing agreements signed during the initial expansion of cloud-enabled energy platforms between 2020 and 2025. Within software, the strongest seat volumes came from energy consumption optimization and renewable forecasting, because those modules delivered direct operating value and fit the most urgent buyer needs. The Nordic AI-powered Energy Management Software Market also showed that buyers increasingly preferred broad platform environments over narrow rule-based tools, especially in larger portfolios where centralized visibility mattered. That helped software remain the largest component even as the market began shifting toward more service-rich contracts.

Services are projected to expand at a 19.91% CAGR through 2031, making them the fastest-growing component of the Nordic AI-powered Energy Management Software Market. The increase reflects a move away from one-time implementation and toward managed analytics, model retraining, API integration support, and vendor-led optimization subscriptions. As deployments spread across multiple sites and across mixed asset classes, customers need more external expertise than internal teams can maintain in-house. This is raising switching costs because integration depth, workflow design, and model tuning become embedded in everyday operations over time. The result is a more complementary software and services mix, where software anchors the installed base and services expand contract value and retention over the life of the customer relationship.

By Deployment Mode: Cloud Leads, But Hybrid Fits Industrial Reality

Cloud deployment accounted for 61.36% of revenue in 2025, giving it the lead position in the Nordic AI-powered Energy Management Software Market. That dominance came from commercial buildings and many utility users that could move analytics workloads to the cloud without replacing core control systems. Cloud models also align with the region’s preference for faster rollouts, centralized updates, and lower internal IT burden. For vendors, cloud delivery improved scale economics because upgrades and analytics features could be managed across large customer bases through a single service layer. That combination made the cloud the default route for many first-stage deployments in the Nordic AI-powered Energy Management Software Market.

Hybrid deployment is projected to grow at a 19.46% CAGR through 2031, because many industrial operators still need local inference for fast operational decisions while keeping higher-level analytics in the cloud. This model is well-suited to plants and utility environments where legacy OT remains critical, but buyers still want portfolio-level visibility and AI optimization. Sweden’s Elflexibel Industri program, launched in 2026 with nearly 50 participating organizations and investment above SEK 300 million (USD 28.8 million), is directly focused on AI-based forecasting, automated flexibility management, and digital twin development across industrial settings. Hybrid adoption, therefore, reflects operational realities rather than buyer hesitation, and it provides the Nordic AI-powered Energy Management Software Market with a practical migration path away from purely on-premises environments. On-premises deployment remains relevant in some utility and sovereignty-sensitive settings, but its role is likely to narrow as hybrid models become easier to implement and govern.

By Application: Demand Optimization Holds the Core, While Forecasting Expands Fast

Energy Consumption and Demand Optimization accounted for 48.26% of application revenue in 2025, keeping it at the center of the Nordic AI-powered Energy Management Software Market. Buyers favored this segment because it addressed the most visible operating issue: controlling energy costs through better scheduling and peak-demand reduction. Commercial property owners and large industrial facilities had the longest operating history with this application, and that helped create a broad installed base across multi-site portfolios. The category also aligns with the stronger reporting environment, as interval-level visibility supports both audit needs and cost control within the same workflow. That combination kept demand optimization as the most established use case in the Nordic AI-powered Energy Management Software Market.

Renewable Energy Forecasting and Integration is projected to expand at a 18.34% CAGR through 2031, reflecting the growing complexity of balancing variable generation in the region. Offshore wind growth, utility-scale solar additions, and the need for sub-hourly forecasting are driving demand for probabilistic production models that account for weather uncertainty. Asset Performance and Predictive Maintenance also continue to expand, supported by operational use cases such as Aalborg University’s RACE project in Denmark, where a digital twin for district heating management was expected to reduce pump energy use by 10% to 20% through continuous optimization. Smart Grid and DER Management is also gaining relevance as operators need more visibility over prosumers, EV chargers, batteries, and local flexibility resources. Energy Trading, Pricing, and Market Intelligence remains smaller in absolute terms, but it is attracting more interest from utilities and aggregators seeking AI support across day-ahead, intraday, and balancing markets.

By End User: Commercial Buildings Anchor Revenue, While Utilities Add the Strongest Growth

Commercial buildings accounted for 57.81% of end-user revenue in 2025, making them the largest demand base in the Nordic AI-powered Energy Management Software Market. The segment benefited from the scale of the regional commercial real estate stock and from the fact that energy cost controls and carbon reporting obligations apply to a broad set of property owners simultaneously. Sweden and Denmark have particularly dense concentrations of commercially managed buildings with active energy procurement structures, which give vendors a large and relatively consistent customer base. This also helps commercial buildings adopt portfolio tools more quickly, as many operators already manage multiple sites through centralized processes. The segment, therefore, provides revenue stability for the Nordic AI-powered Energy Management Software Market, even as other use cases mature.

Utilities are projected to expand at a 19.02% CAGR through 2031, which makes them the fastest-growing end-user group. That growth reflects a shift from passive monitoring toward active flexibility procurement, forecasting, and AI-supported balancing across grid operations. Industrial facilities remain the second-largest revenue segment, with demand rooted in paper and pulp, metals, and chemicals, where power costs directly affect margins. Residential buildings still represent the smallest segment, but they are drawing more attention as aggregators begin to enroll EV chargers, heat pumps, and connected appliances into flexibility programs. Fortum’s Hiven became the first technical aggregator in Sweden to receive regulatory approval for FCR-D support from EVs and off-the-shelf chargers, demonstrating that distributed assets are becoming a real software-controlled resource.[2]Fortum Corporation, “Hiven Breaks New Ground in Balancing the Grid,” Fortum, fortum.com This widens the long-term opportunity set for the Nordic Artificial Intelligence Powered Energy Management Software Market beyond traditional enterprise sites.

Geography Analysis

Sweden held 47.23% of the Nordic AI-powered Energy Management Software Market share in 2025, giving it a clear lead in the regional revenue mix. The country combined early adoption with advanced metering infrastructure, strong renewable penetration, and a large base of energy-intensive manufacturing. Those conditions created commercial demand for AI-driven optimization before stricter disclosure rules fully took effect. Nordic Energy Research documented Sweden as one of the region’s active flexibility case-study markets in December 2025, supporting the view that software-led coordination is already producing practical grid value at the distribution level. Sweden also continued to deepen this position when Ingrid Capacity launched an AI-driven peak-shaving product with Varbergortens Elnät in December 2025, using a 20MW/20MWh battery system to reduce the need for added grid capacity by up to 90%.[3]Ingrid Capacity, “Ingrid Launches Peak Shaving Products to Strengthen Local Power Grids,” Ingrid Capacity, ingridcapacity.com In 2026, Ingrid doubled its battery storage portfolio to more than 1GWh, which signaled growing confidence in AI-optimized flexibility as a scalable business model.

Norway and Denmark both hold important positions in the Nordic AI-powered Energy Management Software Market, but demand patterns differ in each country. Norway’s hydro-based system creates a strong need for reservoir optimization, real-time balancing, and EV load forecasting as charging demand expands. Denmark is projected to grow at a 18.66% CAGR through 2031, making it the fastest-growing geography in the Nordic AI-powered Energy Management Software Market. That momentum is tied to offshore wind integration, mature demand-response structures, and a stronger need for software that can manage system flexibility at a higher resolution. The supplied draft also highlighted Denmark’s role in cross-border value creation, where software-enabled coordination can improve the flow of renewable power across the wider Nordic system.

Finland and Iceland are smaller in terms of revenue, but each adds a distinct demand pattern to the Nordic Artificial Intelligence Powered Energy Management Software Market. Finland is developing a more complex asset base that includes batteries, industrial systems, and energy-linked data center infrastructure, all of which require real-time coordination across heat, power, and grid services. Elisa Industriq’s Gridle platform was selected by Vantaan Energia in 2025 for a new 10MW battery in Rekola, with AI used to analyze market conditions and optimize bids across balancing and wholesale power markets. EPV Energy then created a digital twin of the Vaskiluoto energy system in June 2026, demonstrating that Finnish operators are moving toward always-on digital energy management. Iceland remains a small revenue contributor, but its fully renewable electricity base supports rising interest in geothermal dispatch optimization and data center load balancing tied to renewable supply contracts.

Competitive Landscape

The Nordic AI-powered Energy Management Software Market has a moderately concentrated leading tier and a fragmented specialist layer below it. Large automation vendors such as ABB, Schneider Electric, and Siemens benefit from installed hardware relationships, long service histories, and enterprise credibility that help them cross-sell software into existing accounts. That advantage is important in utility and industrial settings, where buyers often prefer integrated vendors that can support hardware, control systems, and analytics under one commercial relationship. Schneider Electric strengthened this position in late 2025 through Foresight Operation, which brought energy, power, and building systems into a single AI-native platform with a broader commercial release planned for Q3 2026.[4]Schneider Electric SE, “Foresight Operation - AI-Native Energy and Building Management Platform,” Schneider Electric, se.com Siemens also pushed further into cloud-native building software in March 2025 through its Building X roadmap and the introduction of generative AI agents, signaling a deeper move toward autonomous decision support within operational environments.

The Nordic AI-powered Energy Management Software Market still has meaningful white space despite the presence of large incumbents. Small- and medium-sized commercial sites remain underserved because many still rely on manual energy reviews and lack the budget or technical staff for heavy implementation. The EV fleet aggregation layer is also still open, and this is where smaller Nordic players are challenging larger firms by turning charging behavior into flexibility revenue. Fortum’s Hiven approval in Sweden showed that virtual power plant models based on EVs and standard chargers can now enter regulated grid support services without additional on-site hardware. Cross-border flexibility coordination is another open area, as incumbent platforms still offer limited depth in software that can optimize portfolios across multiple transmission zones and market rules simultaneously.

Data ownership and data quality are becoming another competitive lever in the Nordic AI-powered Energy Management Software Market. Landis+Gyr holds a strong upstream position because its smart metering infrastructure shapes the data foundation on which AI platforms depend, and its 15-year partnership with TREFOR in Denmark extends that role across cloud-based metering infrastructure. Vaisala also holds strategic value because weather intelligence is critical for renewable energy production forecasting and lifecycle management, and its Compass platform was launched in 2025 to unify forecasts, measurements, and asset data in a single cloud environment. These positions show that competition is not only about the application layer but also about who controls the data streams that enable high-quality AI forecasting and optimization. That structure supports the view that the Nordic Artificial Intelligence Powered Energy Management Software Market will continue to reward vendors that can combine trusted infrastructure access with software performance and recurring service depth.

Nordic AI-powered Energy Management Software Industry Leaders

Cisco Systems, Inc.

IBM Corporation

Honeywell International Inc.

Schneider Electric SE

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: EPV Energy created a digital twin of the Vaskiluoto energy system in Vaasa, Finland, integrating satellite data, open data sources, and real-time IoT measurements. The twin-supported simulation of planned high-temperature heat pumps and the analysis of industrial-area heat profiles, with the University of Vaasa collaborating on system-level modeling. This was among the first operational industrial digital twins in the Finnish energy sector, designed explicitly for AI-driven energy planning.

- May 2026: Ingrid Capacity doubled its battery storage portfolio to over 1GWh of assets in operation or under construction, following a SEK 400 million (USD 38.5 million) bond issuance. The expansion extended Ingrid’s AI optimization platform, which processes over 100,000 variables in real time, across a larger portfolio of Nordic grid-flexibility assets, including its first Finland deployment in Nivala.

- May 2026: Sweden launched Elflexibel Industri, led by Chalmers Industriteknik with Vinnova support and nearly 50 participating organizations. With investment exceeding SEK 300 million (USD 28.8 million), the initiative covers AI-based load forecasting, automated flexibility management, and energy sharing across 8 industrial demonstration environments. A national digital twin for the Swedish industrial energy system is being developed as a core output.

- November 2025: Schneider Electric announced Foresight Operation at its Innovation Summit North America, an AI-native platform integrating energy, power, and building systems in a single architecture, a multi-domain convergence approach with no direct equivalent among competing platforms. Beta availability began immediately, with wider commercial release planned for Q3 2026.

Nordic AI-powered Energy Management Software Market Report Scope

The Nordic AI-powered Energy Management Software Market encompasses advanced digital solutions that are revolutionizing energy management in highly developed and sustainability-focused economies. These advanced platforms, by integrating with renewable energy systems and smart grids, facilitate real-time monitoring and predictive optimization. The market thrives on robust regulatory frameworks, a deep penetration of renewable energy, and unwavering commitments to carbon neutrality. Organizations leveraging these solutions witness marked improvements in efficiency, significant reductions in emissions, and bolstered resilience of their energy systems. Given the region's relentless pursuit of digital innovation and sustainability, it has emerged as a global frontrunner in adopting AI-driven energy management technologies.

The Nordic AI‑Powered Energy Management Software Market Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud‑Based, On‑Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Smart Grid and Distributed Energy Resource (DER) Management, Renewable Energy Forecasting and Integration, and Energy Trading, Pricing and Market Intelligence), End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential Buildings), and Geography (Sweden, Norway, Denmark, Finland, and Iceland). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| Sweden |

| Norway |

| Denmark |

| Finland |

| Iceland |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings | |

| By Geography | Sweden |

| Norway | |

| Denmark | |

| Finland | |

| Iceland |

Key Questions Answered in the Report

What is the size of the Nordic AI-powered Energy Management Software Market?

The Nordic AI-powered Energy Management Software Market was valued at USD 81.84 million in 2025, is estimated at USD 94.87 million in 2026, and is forecast to reach USD 208.23 million by 2031 at a 17.03% CAGR.

Which application leads demand in this space?

Energy Consumption and Demand Optimization led with 48.26% of application revenue in 2025 because buyers continue to prioritize lower energy costs, peak demand reduction, and better reporting visibility.

Which end-user group is creating the largest revenue base?

Commercial buildings accounted for 57.81% of end-user revenue in 2025, supported by broad exposure to energy costs, portfolio management needs, and carbon reporting requirements.

Which Nordic country is leading adoption?

Sweden led the regional revenue mix with 47.23% in 2025, helped by strong metering infrastructure, renewable penetration, and a large base of energy-intensive industrial activity.

What is driving the fastest future growth?

Denmark is expected to post the fastest geographic growth at 18.66% CAGR through 2031, while utilities are projected to be the fastest-growing end-user group at 19.02% CAGR.

Why are cloud and hybrid models gaining traction?

Cloud led with 61.36% of revenue in 2025 because it lowers deployment friction, while hybrid is projected to grow at 19.46% CAGR as industrial and utility users balance legacy OT needs with cloud analytics benefits.

Page last updated on: