Netherlands AI-Powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

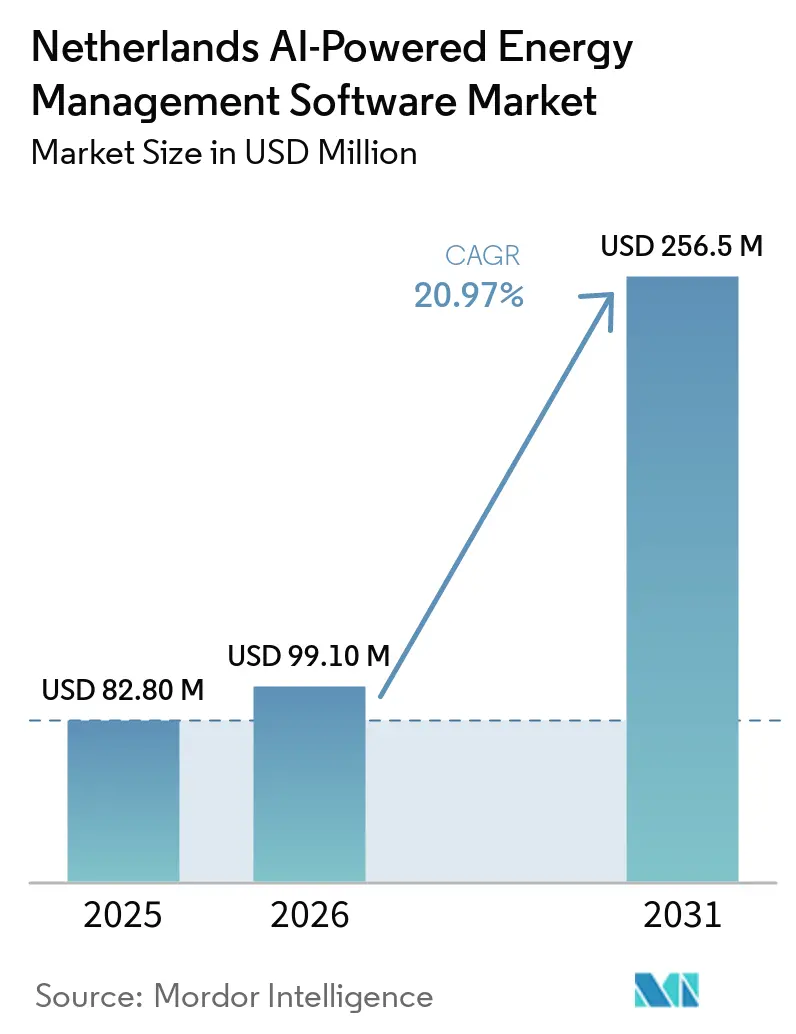

| Base Year Market Size (2025) | USD 82.80 Million |

| Market Size (2026) | USD 99.10 Million |

| Market Size (2031) | USD 256.5 Million |

| Growth Rate (2026 - 2031) | 20.97% CAGR |

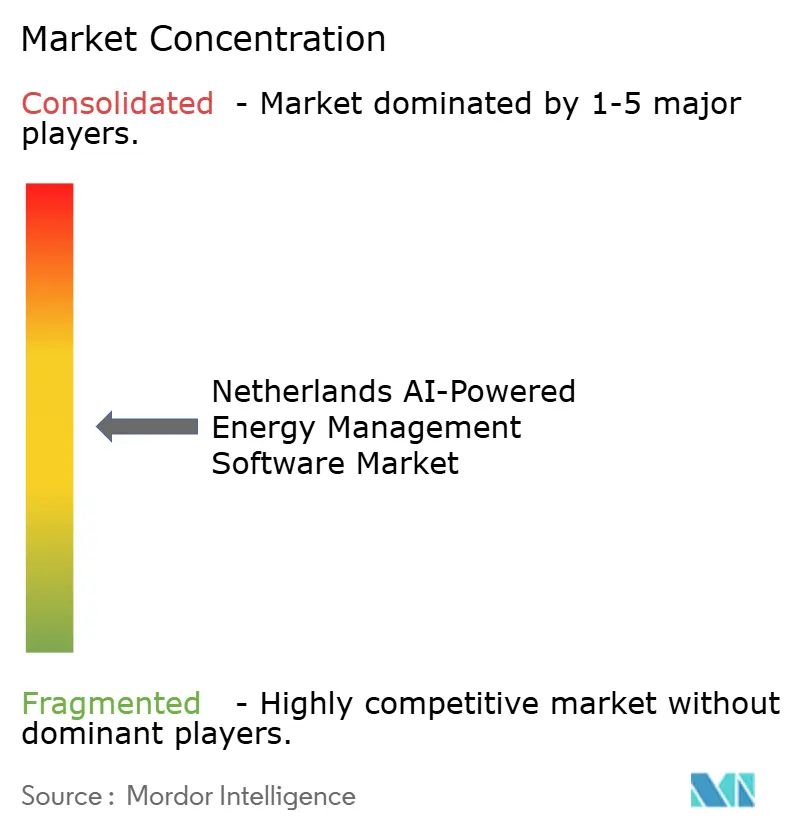

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands AI-Powered Energy Management Software Market Analysis by Mordor Intelligence

The Netherlands AI-Powered Energy Management Software Market size is projected to expand from USD 82.8 million in 2025 and USD 99.1 million in 2026 to USD 256.51 million by 2031, registering a CAGR of 20.97% between 2026 and 2031. The Netherlands AI-Powered Energy Management Software Market is growing because electricity price volatility has made continuous load control more valuable than periodic energy reviews. Grid congestion is adding to that urgency, as businesses and network operators need software that can optimize consumption and flexibility inside existing capacity limits while physical upgrades take time. Regulatory changes are widening adoption because building compliance, operational data exchange, and digital resilience are now shaping everyday energy decisions across utilities, commercial properties, and industrial sites. Competition remains active between multinational automation vendors and Dutch software specialists, and that mix is keeping product development focused on interoperability, security, and faster deployment. The strongest opportunities are emerging where demand optimization, renewable integration, and flexibility bidding can be combined into a single operating layer that protects continuity and improves asset utilization.

Key Report Takeaways

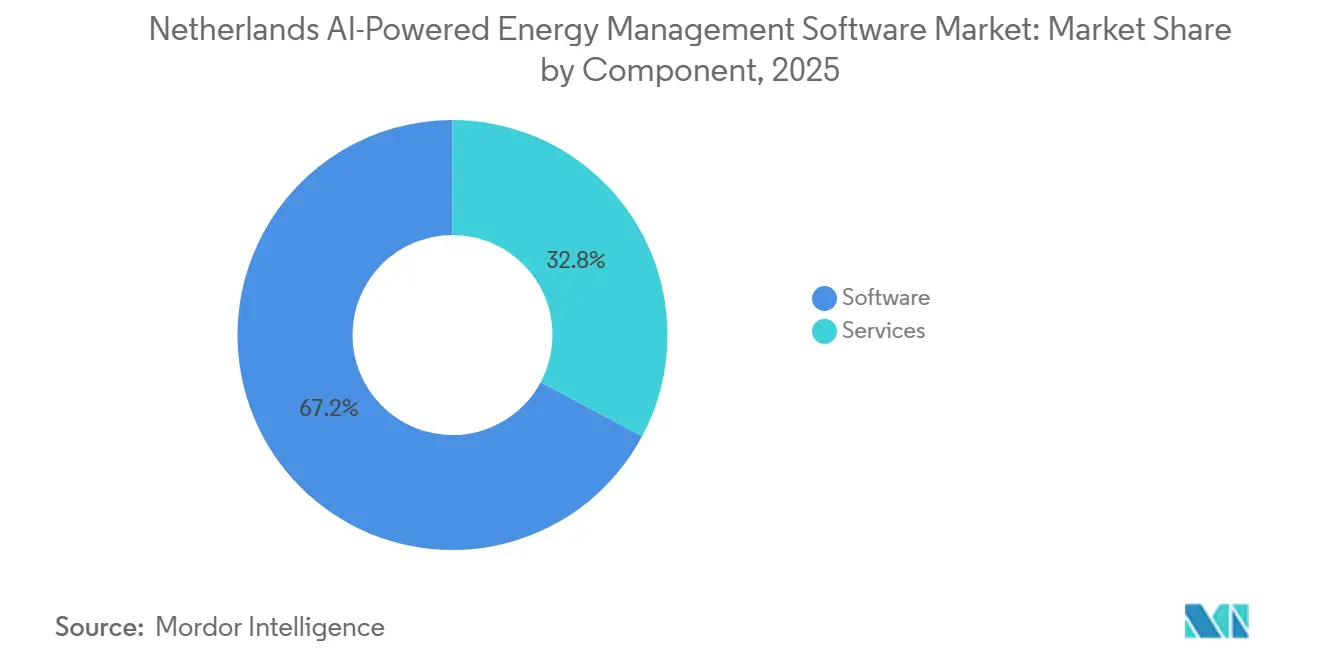

- By component, software held a 67.19% share of the Netherlands AI-Powered Energy Management Software Market in 2025, while services are projected to expand at a 21.12% CAGR through 2031.

- By deployment mode, cloud-based platforms held a 57.14% share in 2025, while hybrid deployment is projected to expand at a 21.23% CAGR through 2031.

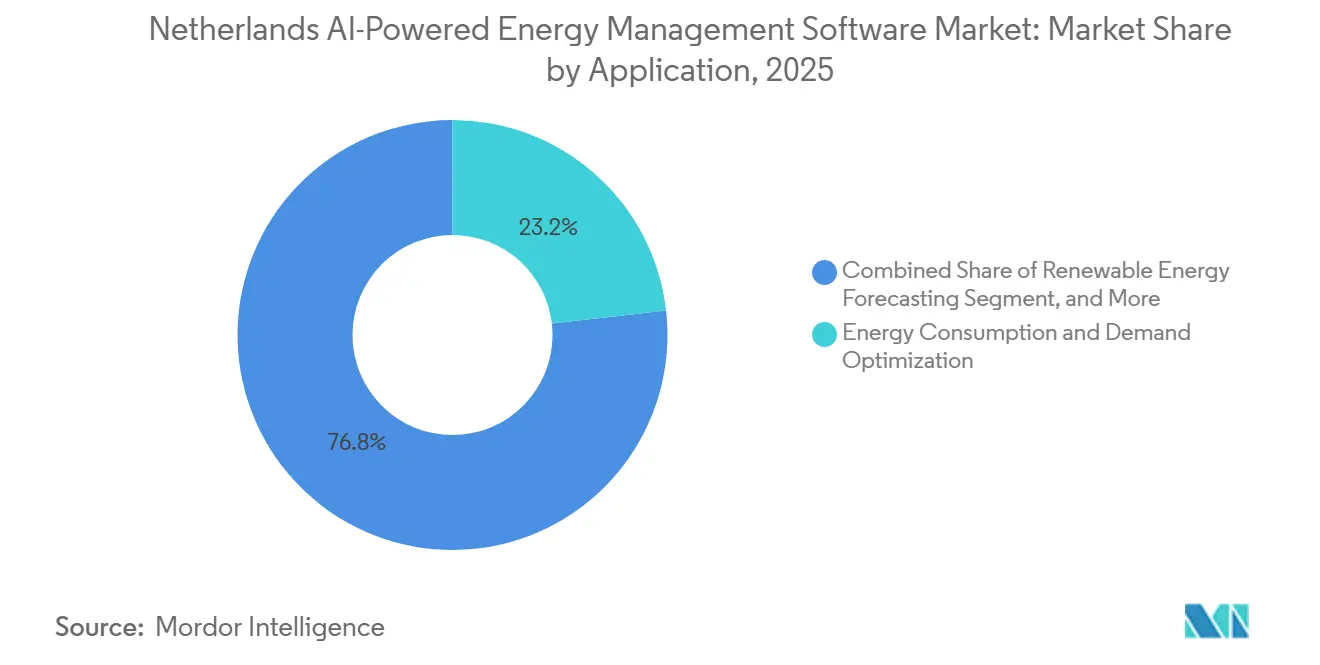

- By application, energy consumption and demand optimization accounted for a 23.18% share in 2025, while renewable energy forecasting and integration are projected to expand at a 21.34% CAGR through 2031.

- By end user, utilities held 34.15% of the Netherlands AI-Powered Energy Management Software Market share in 2025, while industrial facilities are projected to expand at a 21.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Netherlands AI-Powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Electricity Cost Sensitivity in Dutch Commercial Facilities | +3.0% | Netherlands-wide, with strongest effect in Amsterdam, Rotterdam, Utrecht, and The Hague | Short term (≤ 2 years) |

| Grid Congestion Management Needs In Dense Load Centers | +2.8% | Flevoland, Gelderland, Utrecht, North Brabant, and Groningen | Short term (≤ 2 years) |

| Net Zero Compliance Pressure On Building Portfolios | +2.5% | Netherlands-wide, with strongest effect in large commercial portfolios | Medium term (2-4 years) |

| AI-Enabled Demand Response Revenue Optimization | +2.2% | National, with higher relevance for utilities and large industrial sites | Medium term (2-4 years) |

| Granular Submetering Adoption In Multi-Tenant Assets | +1.8% | Urban commercial clusters, especially Amsterdam, Rotterdam, and Eindhoven | Medium term (2-4 years) |

| Utility And Facility Data Convergence For Forecasting Accuracy | +1.5% | National, with strongest effect in utility control centers and large industrial campuses | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Electricity Cost Sensitivity in Dutch Commercial Facilities

Dutch commercial facilities faced a sharper pricing environment in 2025, when day-ahead electricity prices climbed 12% to EUR 87/MWh, equivalent to USD 94.83/MWh, and hours priced above EUR 200/MWh increased from 98 to 127.[1]TenneT TSO B.V., “Rising Electricity Prices, Increased Electricity Exports and Stable Congestion Management Costs,” TenneT, tennet.eu Negative-price hours also rose from 458 to 584 in 2025, indicating volatility was moving in both directions, not just during peak periods. This pattern pushed many property and facility teams away from annual benchmarking and toward continuous control of HVAC systems, charging loads, refrigeration, and other flexible assets. The Netherlands AI-Powered Energy Management Software Market benefits from this shift because buyers now need software that can respond within a day rather than rely on manual adjustments after bills arrive. For large commercial portfolios, the value of AI now comes from maintaining performance during price spikes and capturing savings during low-price windows. As that operating logic becomes more common, software budgets are becoming easier to defend against other building technology priorities.

Grid Congestion Management Needs in Dense Load Centers

Grid congestion has become one of the clearest growth drivers for the Netherlands AI-Powered Energy Management Software Market, as network stress is now affecting normal operational decisions for both utilities and end users. In the Flevoland, Gelderland, and Utrecht congestion area, redispatch volumes rose by 31% in 2025, and regular congestion management costs increased by 42% to EUR 48 million, equivalent to USD 53.28 million. The Dutch government responded with the Aansluitoffensief in February 2026, which committed an additional EUR 500 million (USD 555 million) per year in 2026 and 2027 for flexibility procurement above the minimum threshold.[2]Minister Sophie Hermans, “Gezamenlijk Plan Om De Wachtrij Voor Het Volle Stroomnet Komende Jaren Fors Te Versnellen,” Rijksoverheid, rijksoverheid.nl That policy choice matters because it supports software-led demand response and congestion management while larger grid reinforcement projects move through longer timelines. Utilities, aggregators, and large industrial sites are therefore treating AI control systems as an operating requirement instead of a discretionary efficiency tool. The commercial effect is that software demand is increasingly linked to continuity, connection access, and curtailment management.

Net Zero Compliance Pressure on Building Portfolios

The Netherlands began implementing the first tranche of the EU Energy Performance of Buildings Directive on May 29, 2026, and this step is pushing building owners to improve data visibility and automation.[3]CFP Green Buildings, “Nederland Start Met Invoering EPBD IV, Dit Verandert Er,” CFP Green Buildings, cfp.nl The new framework increases the relevance of building automation and control systems, energy performance certificates, and measured performance across commercial portfolios. For buildings larger than 1,000 m², life-cycle global warming potential calculations will be required from January 2028, which moves reporting preparation into current investment plans. The Netherlands AI-Powered Energy Management Software Market gains from this timetable because owners need cleaner operational data and more reliable control records before mandatory deadlines arrive. Compliance spending in this case is closely tied to software capability, since manual energy tracking becomes difficult at a portfolio scale. That makes the buying cycle more predictable than a standard retrofit cycle that depends only on voluntary savings targets.

AI-Enabled Demand Response Revenue Optimization

The revenue case for flexibility is improving in the Netherlands, making the Netherlands AI-Powered Energy Management Software Market more attractive to both industrial and commercial buyers. From January 2025, users connected to TenneT's high-voltage network became eligible for a congestion pricing discount when they voluntarily reduced consumption during peak periods. The same operating environment also saw market-based renewable curtailment exceed 1 TWh in 2025, up 33.5% from 2024, which showed how quickly imbalance costs can build when flexible assets are not coordinated in real time. AI platforms help users decide when to reduce load, when to store power, and when to shift production without weakening site operations. That matters because the value pool is no longer limited to energy savings alone and now includes avoided congestion costs and better participation in flexibility programs. Vendors that can combine these revenue and protection functions within a single control layer are better positioned to win broader contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Building Automation Integration Complexity | -2.0% | National, with the highest exposure in older commercial and industrial properties | Medium term (2-4 years) |

| Cybersecurity And Privacy Concerns around Operational Energy Data | -1.5% | National, with higher sensitivity in utility and critical infrastructure environments | Short term (≤ 2 years) |

| Fragmented Procurement across Property Portfolios | -1.0% | National, especially in multi-tenant and decentralized property groups | Medium term (2-4 years) |

| Limited In-House AI and Energy Analytics Talent | -0.8% | National, with stronger constraints outside major technology corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy Building Automation Integration Complexity

Legacy building automation remains a significant barrier to the Netherlands AI-Powered Energy Management Software Market, as many sites still run on older control stacks that were not built for AI-led optimization. Those systems often require additional gateways, custom middleware, and local engineering before data can flow smoothly between equipment and software. In multi-site portfolios, the problem becomes larger because each property may use a different control setup, sensor layout, or maintenance standard. Dutch specialists are responding with approaches that combine AI with physical building models to address incomplete data and uneven sensor coverage. Even with these workarounds, buyers still face longer deployment schedules and higher implementation costs than the software license alone suggests. That slows conversion, especially in portfolios where payback decisions are reviewed site-by-site rather than centrally.[4]Entune, “Hoe BuildingAI Gebouwen Verandert In Intelligente Energiesystemen,” Entune, entune.nl

Cybersecurity and Privacy Concerns Around Operational Energy Data

Cybersecurity is becoming a more challenging buying criterion for the Netherlands AI-Powered Energy Management Software Market, as AI control increasingly depends on deeper integration between operational technology and information technology systems. The Rijksdienst voor Digitale Infrastructuur identified energy sector cybersecurity as a 2026 supervisory priority and linked that focus to the Network Code on Cybersecurity and wider resilience obligations for operators of essential services. The Dutch Energy Act, which came into force on January 1, 2026, has increased attention among energy market participants on data exchange, smart metering, and system protection. Buyers now ask for clearer proof on access control, hosting, audit trails, and operational resilience before approving connected energy platforms. This extra review is especially important for utilities and industrial operators that treat energy systems as part of critical production infrastructure. As a result, vendors with stronger security documentation and certified processes move through procurement more smoothly than suppliers that only emphasize optimization performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Ground As Deployments Become More Demanding

Software held 67.19% of the Netherlands AI-Powered Energy Management Software Market in 2025, which confirmed that platform licensing remained the main revenue base at this stage of adoption. The software lead reflects the importance of forecasting engines, dashboards, load control tools, and demand response modules across utilities, commercial buildings, and industrial sites. Buyers usually enter the category through a core platform because that is the layer that connects price signals, grid constraints, and site-level operating logic. This also explains why the segment stays ahead even when implementation work is intensive, since the control and analytics layer carries the direct operating value. In many accounts, software brings together energy cost management, asset visibility, and flexibility decisions.

Services are projected to expand at a 21.12% CAGR through 2031, slightly ahead of the broader market, because deployment quality increasingly shapes realized value after the initial sale. The need for data mapping, control integration, commissioning, cybersecurity checks, and ongoing model tuning is turning service work into a recurring revenue stream rather than a one-time activity. In older buildings and mixed industrial estates, this support is often essential because system data is incomplete or spread across incompatible control environments. The Netherlands AI-Powered Energy Management Software Market is therefore moving toward a model where recurring advisory and managed support help customers sustain savings and maintain control of quality over time. Vendors that can pair software with implementation depth are better positioned to reduce churn, since customers are less likely to replace platforms tightly integrated with site operations. That shift also widens the roles of partners, system integrators, and energy specialists who can help maintain performance stability after launch.

By Deployment Mode: Hybrid Models Fit Dutch Grid Conditions Better

Cloud-based deployment accounted for 57.14% of revenue in 2025, indicating that many buyers still favored a centralized software model for multi-site visibility and easier rollouts. Cloud systems are attractive because they reduce local infrastructure requirements and enable operators to compare performance across buildings or facilities through a single interface. They also support faster updates, shared analytics models, and portfolio-level reporting, which is useful for real estate groups and energy service providers. In a market where many users are still building their digital energy capabilities, that lower operational burden remains a strong advantage. Cloud adoption also suits buyers who want quick access to forecasting and benchmarking without rebuilding a local control architecture from scratch.

Hybrid deployment is projected to expand at a 21.23% CAGR through 2031, as Dutch users increasingly need local response speed together with broader cloud analytics. This model is gaining support because real-time dispatch and congestion responses often need local control logic, while forecasting, reporting, and multi-site optimization still benefit from centralized processing. The Netherlands opened a public consultation on the AI Regulation implementation act in April 2026, and the treatment of certain infrastructure-related AI systems is reinforcing interest in retaining stronger control over critical operating functions. The Netherlands AI-Powered Energy Management Software Market is well-suited to this architecture because grid-sensitive operations vary by province, site type, and connection condition. On-premises systems will remain in some utility and industrial settings, but hybrid designs are better aligned with the need to combine resilience, flexibility, and scale. Vendors that let customers configure cloud and edge components separately should remain more competitive than those that insist on a single standard deployment model.

By Application: Demand Optimization Leads While Renewable Integration Advances Fastest

Energy consumption and demand optimization held 23.18% of revenues in 2025, making it the largest application because it serves almost every major buyer group in the market. Utilities use it to reduce imbalance pressure, commercial operators use it to manage tariffs and building loads, and industrial facilities use it to protect production while controlling energy costs. The appeal of this segment lies in its direct link to measurable financial outcomes, as users can compare performance against existing tariff exposure and site operating patterns. In practical terms, it remains the easiest application to justify because the link between better scheduling and lower costs is readily apparent. This broad usefulness is why the segment remained ahead even as newer applications gained attention.

Renewable energy forecasting and integration is projected to expand at a 21.34% CAGR through 2031, underscoring the market's strong shift toward grid-aware optimization. The Dutch offshore wind roadmap targets 21 GW of installed offshore wind capacity by 2031, which will keep pressure on forecasting quality, balancing, and connection management. Market-based renewable curtailment exceeded 1 TWh in 2025, 33.5% higher than in 2024, indicating that dispatch and integration decisions are becoming more time-sensitive. Research from Utrecht University also showed that hybrid AI methods for real-time solar irradiance forecasting can improve grid integration performance beyond single-model approaches. Asset performance, DER management, and energy trading applications remain relevant, but the strongest momentum is now emerging for handling forecasting, curtailment, and dispatch together. The Netherlands AI-Powered Energy Management Software Market is therefore moving toward application stacks that simultaneously manage both cost and grid stability.

By End User: Utilities Lead Revenue While Industrial Sites Drive Expansion

Utilities held 34.15% of the Netherlands AI-Powered Energy Management Software Market share in 2025, making them the largest end-user group in the market. Their leading position reflects the immediate need to manage congestion, redispatch, variable generation, and increasingly complex network balancing decisions. Utilities also influence vendor selection by placing greater weight on scalability, interoperability, and security in their procurement standards. When utilities adopt a control platform, that often shapes expectations across connected aggregators, service providers, and downstream users. This makes the utility segment important not only for revenue but also for setting technical requirements that other buyers later follow.

Industrial facilities are projected to expand at a 21.45% CAGR through 2031, reflecting the stronger pressure they face from grid constraints, energy price swings, and continuity risks. Large sites need more than passive monitoring because they must decide when to shift load, curtail, and coordinate on-site assets without disrupting output. The pricing incentives for peak reduction, which took effect for high-voltage users in January 2025, have added another reason for industrial operators to invest in automated control. The Netherlands AI-Powered Energy Management Software Market is seeing this segment shift from analysis to active dispatch, especially when flexible production, storage, or thermal processes can be coordinated in real time. Commercial buildings and residential buildings remain smaller today, but tighter building rules and stronger automation requirements should gradually widen adoption beyond the earliest utility and industrial users.

Geography Analysis

The Netherlands AI-Powered Energy Management Software Market stood at USD 99.00 million in 2026 and is projected to reach USD 256.50 million by 2031 at a 20.97% CAGR, indicating that demand is building across the country rather than in a single cluster. The national backdrop is defined by stronger electricity volatility, deeper electrification, and more active congestion management, which gives software a direct operating role. In 2025, day-ahead electricity prices rose 12% to EUR 87/MWh, equivalent to USD 94.83/MWh, and negative-price hours increased to 584, which confirmed that the Dutch power system now experiences more frequent pricing swings on both sides. The offshore wind roadmap points to 21 GW of installed offshore wind capacity by 2031, which will keep grid balancing and integration high on the national agenda. TenneT also reported net electricity exports of 14 TWh in 2025, worth more than EUR 1 billion, indicating that the country can experience periods of surplus even while local constraints remain severe.

The Randstad remains the most concentrated commercial demand zone because it combines dense office portfolios, data centers, transport activity, and large corporate energy users. This makes Amsterdam, Rotterdam, The Hague, and Utrecht important revenue centers for building-focused control platforms and portfolio analytics. The Flevoland, Gelderland, and Utrecht congestion area is also central to adoption because redispatch volumes rose 31% there in 2025, and regular congestion management costs reached EUR 48 million, equivalent to USD 53.28 million. In these regions, the software case is tied as much to operating continuity as it is to energy cost management. The Port of Rotterdam and the surrounding industrial corridor add another demand center because energy-intensive activity, trading exposure, and flexibility needs are concentrated in a small area.

North Brabant is also important because its advanced manufacturing base creates steady demand for software that can manage flexible production and constrained grid access. Groningen also plays a growing role, as the northern system connects industrial assets with renewable generation and evolving network requirements. The Aansluitoffensief adds a nationwide support layer by allocating an additional EUR 500 million (USD 555 million) per year in 2026 and 2027 for flexibility procurement above the minimum threshold. Geography in this market, therefore, matters less as a simple regional ranking and more as a map of where congestion, industrial intensity, and compliance pressure converge most quickly.

Competitive Landscape

The Netherlands AI-Powered Energy Management Software Market remains moderately fragemented, with multinational automation vendors and smaller Dutch specialists serving different parts of the opportunity set. Large vendors still benefit from installed equipment bases, long customer relationships, and broader control system portfolios. Smaller specialists compete by offering faster deployment, lower integration requirements, and software designed for Dutch congestion and flexibility conditions. This balance prevents the market from consolidating around a single dominant model or supplier. It also means product selection is often determined by use-case fit, security readiness, and integration speed rather than brand scale alone.

Several recent moves show how suppliers are trying to stand out in the market. Tibo Energy achieved ISO 27001:2022 certification in May 2026, strengthening its position with buyers who now conduct more stringent cybersecurity reviews. In June 2026, Tibo Energy also won the Grid Congestion Innovation Competition 2026 in the SME category for its Zeist fire station deployment, which highlighted the value of AI-led control in a constrained connection environment. TNO and Jungle AI announced a collaboration in June 2025 to develop AI-based cyberattack detection for wind turbines, linking optimization needs with security capabilities within hybrid power environments. Siemens also reported in its Infrastructure Transition Monitor 2025 that 72% of energy-sector executives believe AI will transform their organizations within 3 years, supporting the view that demand is broadening across the value chain.

Competition is therefore moving beyond standard energy dashboards and toward secure, operationally embedded control platforms. Buyers increasingly compare vendors on data handling, implementation depth, utility compatibility, and the ability to work with legacy assets. Managed services matter more in this setting because many customers still lack enough internal energy analytics and AI talent to run complex systems on their own. The Netherlands AI-Powered Energy Management Software Market still has room to grow in mid-sized industrial facilities and multi-tenant building portfolios, where buyers need strong outcomes without long, customized deployments.

Netherlands AI-Powered Energy Management Software Industry Leaders

Schneider Electric SE

Siemens AG

Honeywell International Inc.

Johnson Controls International plc

ABB Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Tibo Energy won the Grid Congestion Innovation Competition 2026 (SME category) for its Zeist fire station deployment, demonstrating that AI-coordinated building energy management can achieve decarbonization within existing grid connection limits in a moratorium zone. The case proved that AI software can unlock latent capacity in existing connections, reducing the need for costly grid upgrades.

- May 2026: Tibo Energy achieved ISO 27001:2022 certification across all operations, including its cloud-based EMS platform, in response to increasing digitalization and tighter European energy sector regulation. This positions the company as one of the first AI energy management software providers in the Netherlands with independently validated information security.

- February 2026: The Dutch government and grid operators announced the Aansluitoffensief, an eight-measure grid congestion action plan that commits to procuring an additional EUR 500 million (USD 555 million) per year above the minimum flexibility threshold in 2026 and 2027, effectively creating a EUR 1 billion (USD 1.11 billion) budget for AI-managed demand response contracting.

- January 2026: The Dutch Energy Act (Energiewet) entered into force, replacing the Electricity Act 1998 and Gas Act and introducing new obligations for cybersecurity, smart metering, and data exchange across energy market participants. Provisions covering vital process protection and digital resilience took effect immediately, while additional requirements are phased through 2026.

Netherlands AI-Powered Energy Management Software Market Report Scope

The Netherlands AI-Powered Energy Management Software market refers to platforms and services that leverage artificial intelligence to optimize energy consumption, enhance asset performance, and enable smarter grid and distributed energy resource (DER) management. These solutions provide advanced capabilities, including predictive maintenance, renewable energy forecasting, demand-side optimization, and market intelligence for energy trading and pricing.

The Netherlands AI-Powered Energy Management Software market report is segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Smart Grid and Distributed Energy Resource (DER) Management, Renewable Energy Forecasting and Integration, and Energy Trading, Pricing and Market Intelligence), and End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential Buildings). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings |

Key Questions Answered in the Report

What is the size outlook for the Netherlands AI-Powered Energy Management Software Market?

The Netherlands AI-Powered Energy Management Software Market was valued at USD 82.8 million in 2025, stands at USD 99.1 million in 2026, and is projected to reach USD 256.5 million by 2031 at a 20.97% CAGR.

Which deployment model is expanding fastest in the Netherlands?

Hybrid deployment is projected to expand at a 21.23% CAGR through 2031 because buyers need local control speed together with centralized cloud analytics.

Which application is growing the fastest in this space?

Renewable energy forecasting and integration is projected to expand at a 21.34% CAGR through 2031, supported by offshore wind growth and higher curtailment pressure.

Which end-user group currently leads demand?

Utilities led with 34.15% revenue share in 2025 because grid congestion, redispatch, and balancing needs made them early adopters of AI-enabled control platforms.

What is driving adoption among industrial facilities in the Netherlands?

Industrial sites are projected to grow at a 21.45% CAGR through 2031 as they respond to volatile prices, connection constraints, and new incentives for peak reduction and flexibility.

What is the main obstacle slowing wider adoption?

Integration with legacy building and industrial control systems remains a major obstacle because it raises deployment effort, increases costs, and slows the path to realized value.

Page last updated on: