South Africa AI-Powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

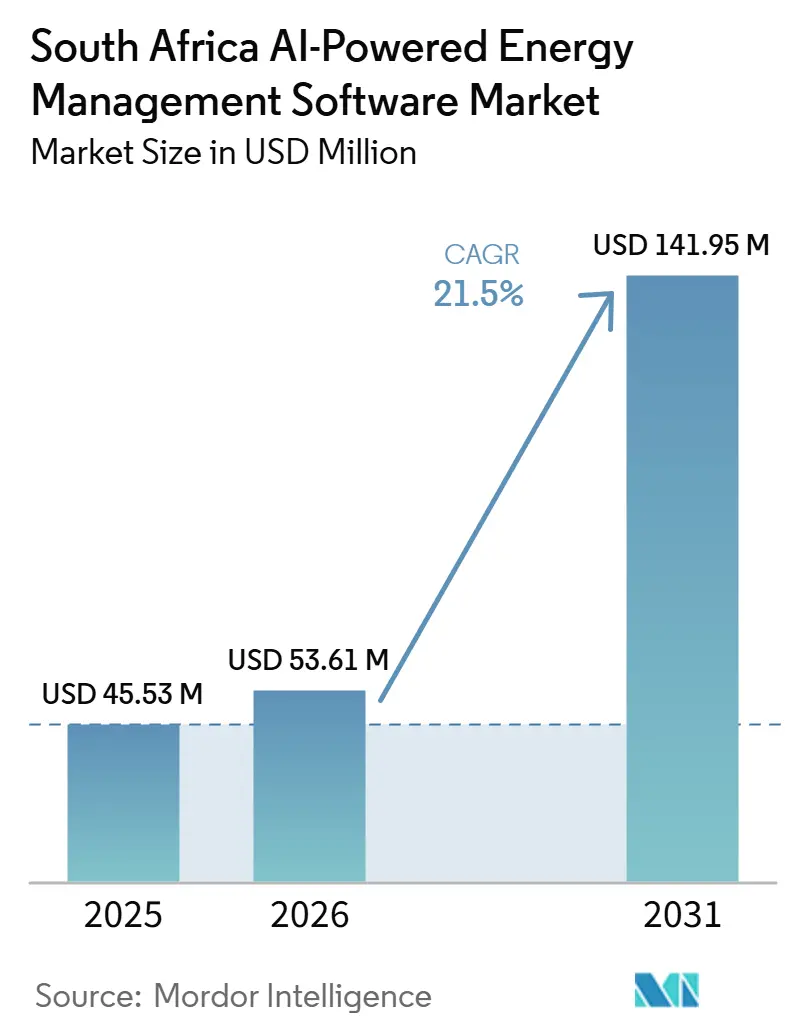

| Base Year Market Size (2025) | USD 45.53 Million |

| Market Size (2026) | USD 53.61 Million |

| Market Size (2031) | USD 141.95 Million |

| Growth Rate (2026 - 2031) | 21.50% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa AI-Powered Energy Management Software Market Analysis by Mordor Intelligence

The South Africa AI-powered energy management software market size was valued at USD 45.53 million in 2025 and estimated to grow from USD 53.61 million in 2026 to reach USD 141.95 million by 2031, at a CAGR of 21.50% during the forecast period (2026-2031). Rising electricity tariffs and repeated supply disruptions have made AI-led demand control, tariff response, and outage planning more relevant for enterprises that run energy-intensive sites and cannot rely on manual intervention during unstable grid conditions. Policy changes are also widening the software opportunity, because IRP 2025 and the shift toward a more competitive wholesale electricity structure are increasing the need for renewable forecasting, distributed resource coordination, and real-time dispatch support across utilities and large power users. Cloud deployment is gaining faster acceptance as multi-site building owners, industrial groups, and utilities seek centralized visibility across assets, while local data center expansion reduces latency and data residency concerns that had previously slowed adoption. Competition remains shaped by global OEMs with long-standing BMS and SCADA relationships, but local platforms are winning attention where South African tariff logic, load-shedding patterns, and municipal billing complexity require models trained on country-specific operating conditions. Integration friction at older commercial and industrial sites still slows rollout, yet that same friction is pushing more buyers toward managed implementation and optimization support, which is steadily making the South Africa AI-powered energy management software market more service-intensive as deployments scale.

Key Report Takeaways

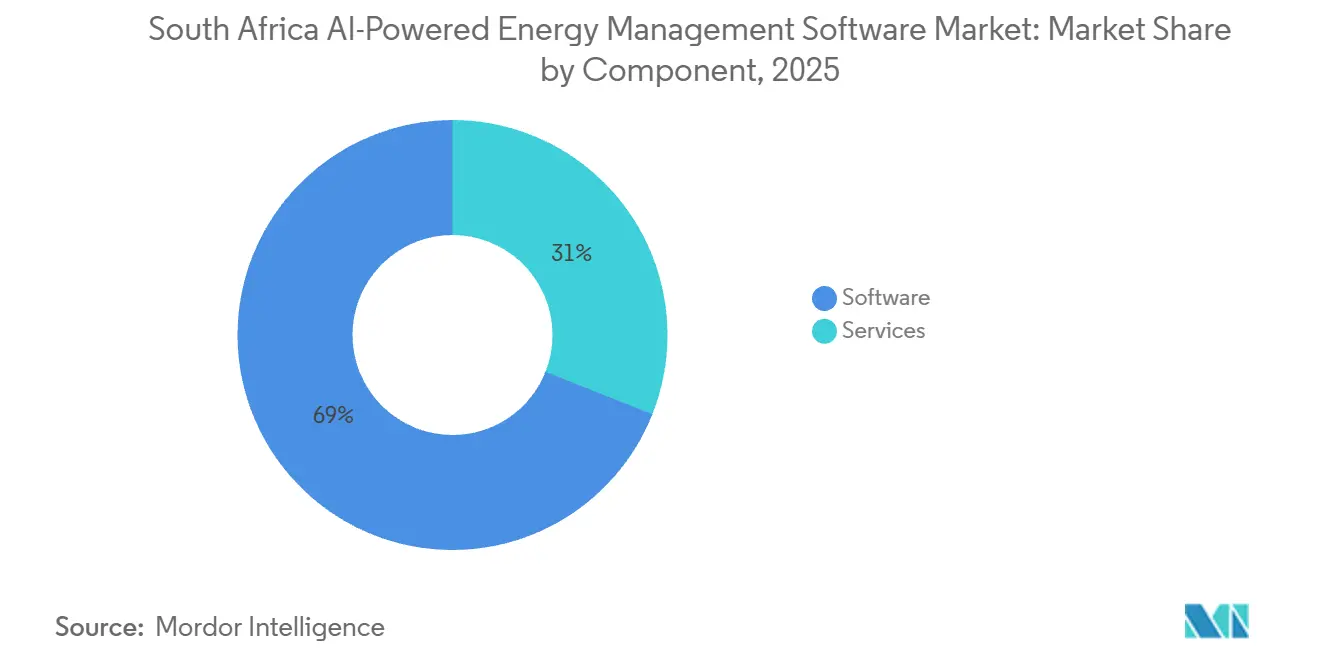

- By component, software held 69.00% of the South Africa AI-powered energy management software market size in 2025, while services are projected to expand at a 24.20% CAGR through 2031.

- By deployment mode, cloud-based deployment accounted for 54.50% of revenue in 2025 and is also projected to record the highest CAGR at 24.80% through 2031.

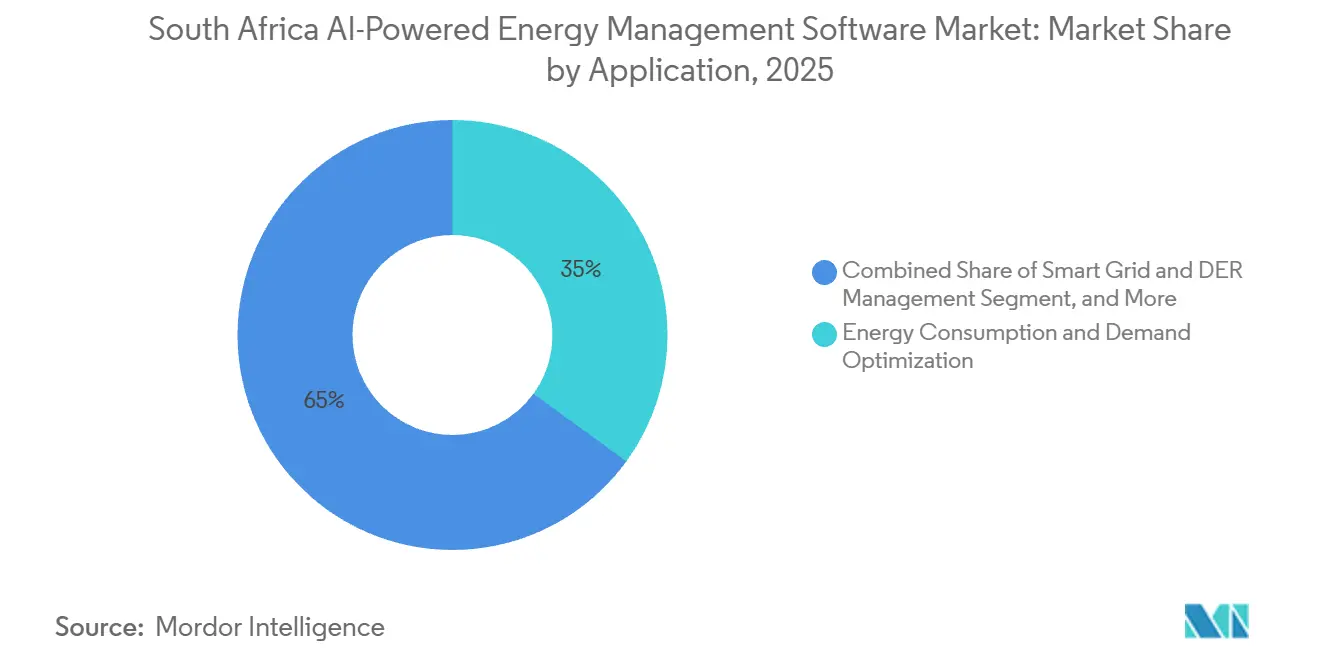

- By application, energy consumption and demand optimization captured 35.00% of market revenue in 2025, while renewable energy forecasting and integration is projected to expand at a 26.50% CAGR through 2031.

- By end user, utilities held 37.00% of the South Africa AI-powered energy management software market share in 2025, while commercial buildings are projected to post the fastest CAGR at 24.60% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Africa AI-Powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Electricity Tariffs and Load-Shedding Pressure | +5.5% | National, with the highest impact in Gauteng, Western Cape, and KwaZulu-Natal industrial corridors | Short term (≤ 2 years) |

| Corporate Net-Zero Commitments and Energy Cost Control | +4.5% | National, with faster uptake across JSE-listed corporates and RE100 signatory operations | Medium term (2-4 years) |

| Expansion of Cloud-Based Building and Industrial Analytics | +3.5% | National, with early gains in Johannesburg, Cape Town, and Durban data center clusters | Medium term (2-4 years) |

| Utility Demand Response and Flexibility Program Adoption | +3.0% | National, concentrated at Eskom NTCSA and large industrial load providers | Medium term (2-4 years) |

| Edge AI for Site-Level Fault Detection and Autonomous Control | +2.5% | National, especially at critical infrastructure sites, mines, and healthcare networks | Long term (≥ 4 years) |

| Cyber-Resilient On-Premises Demand from Critical Sites | +2.0% | National, with concentration in defense, energy, and financial services critical infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Electricity Tariffs and Load-Shedding Pressure

South Africa’s tariff path has tightened software payback periods because Eskom’s increase was 12.74% from April 2025 and 8.76% from April 2026, with a further 8.83% anticipated from April 2027. This has shifted procurement reviews away from long capital cycles and toward operating cost decisions, especially at sites where every tariff revision directly affects margins, tenant recoveries, or production economics. Facilities teams that once relied on periodic audits are now favoring continuous monitoring and automated control because the financial penalty of delayed response has become much clearer during peak periods and disruption events. South Africa’s load-shedding pattern also rewards models trained on local dispatch behavior, because generic scheduling logic does not respond well to fast changes in site conditions, battery use, or municipal supply interruptions. Wetility’s AI Mode showed this local advantage during beta testing across hundreds of sites, where the platform analyzed millions of data points and maintained zero power outages during active load-shedding events. As a result, the South Africa AI-powered energy management software market is moving toward tools that can act in real time, protect uptime, and convert volatile grid conditions into measurable cost control rather than reactive site management.

Corporate Net-Zero Commitments and Energy Cost Control

South Africa’s second Nationally Determined Contribution, submitted in October 2025, raised the importance of structured decarbonization planning for companies exposed to export requirements and future carbon-related trade rules. More than 100 RE100 member companies with South African operations are committed to 100% renewable electricity use by 2050, and corporate sentiment in 2025 also leaned strongly toward renewable investment over fossil-based expansion. This is bringing together 2 budgets that were often treated separately, because companies now want one software layer that supports both cost optimization and energy accountability. Platforms that combine renewable energy certificate workflows, electricity consumption monitoring, and tariff-aware load management are becoming more attractive than separate energy accounting and demand-side tools bought under different mandates. That shift matters in listed corporates, export-facing manufacturers, and portfolio owners that must report more consistently while also controlling power costs across many sites. In the South Africa AI-powered energy management software market, vendors that connect carbon accountability to visible operating savings are improving their position with buyers that need both board-level reporting and site-level efficiency.

Expansion of Cloud-Based Building and Industrial Analytics

The launch of local hyperscale infrastructure in Johannesburg removed a long-standing barrier for enterprise customers that had been reluctant to move sensitive operating workloads into remote environments with higher latency and weaker residency comfort. As a result, cloud-native building and industrial platforms are now managing broader site portfolios through a single interface, allowing teams to compare buildings, flag anomalies, predict failures, and benchmark performance without separate site servers. Schneider Electric reinforced this direction in April 2026 when it transitioned to EcoStruxure Energy Intelligence and enrolled more than 60 South African Alliance Partners into the program, giving the model a wider deployment channel. The cloud case is especially strong for listed REITs and multi-site operators that must normalize Eskom-direct and municipal supply data across buildings that face different tariff structures, equipment types, and compliance demands. Once that data is centralized, procurement teams can compare performance by site and justify upgrades with a level of visibility that isolated local systems rarely provide. This keeps cloud architecture at the center of the South Africa AI-powered energy management software market, even as some regulated facilities still retain a clear preference for local control over selected workloads.

Utility Demand Response and Flexibility Program Adoption

NTCSA’s demand response program had built around 1,400 MW of flexible demand capacity by November 2025, combining very fast response for sudden grid events with supplemental peak relief and a virtual power station structure for contract and dispatch management.[1]GO15, “NTCSA Demand Response Strategy to Ensure Grid Stability and Flexibility in South Africa,” GO15, go15.org This matters because flexibility is no longer only a site-level optimization choice; it is becoming part of how market participants interact with the grid and earn value from responsive load behavior. NERSA’s May 2026 consultation on SAWEM building blocks moved this process closer to formal wholesale competition, which raises the likelihood of more structured participation rules for enrolled generators, traders, and demand response assets. That shift will lift demand for software that can manage interval metering, bidding logic, dispatch compliance, event verification, and settlement support within a local market framework. Vendors whose systems fit South African billing cycles, utility workflows, and wheeling arrangements are likely to benefit more than generic DERMS suppliers that still rely on heavily templated market logic. This driver broadens the South Africa AI-powered energy management software market beyond pure efficiency applications and moves it closer to the operating core of load flexibility, market participation, and electricity trading.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity with Legacy OT, BMS, and Metering Assets | -3.5% | National, with highest friction at aging mines, municipalities, and secondary-tier commercial buildings | Short term (≤ 2 years) |

| Weak Data Quality Across Disparate Site Systems | -2.5% | National, particularly acute at multi-owner industrial parks, logistics hubs, and distributed commercial portfolios | Medium term (2-4 years) |

| Budget Sensitivity and Unclear Payback for Smaller Facilities | -2.0% | National, concentrated in sub-10,000 m² commercial buildings and small municipalities | Medium term (2-4 years) |

| Data Sovereignty and Cybersecurity Constraints in Critical Infrastructure | -1.5% | National, with highest impact at power utilities, healthcare, defense, and financial sector sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity with Legacy OT, BMS, And Metering Assets

A large share of South Africa’s commercial and industrial building stock still runs on older controllers, proprietary meters, and site-specific SCADA configurations that do not connect easily with modern AI layers. This raises the cost of deployment because vendors often need middleware, custom interfaces, selective sensor replacement, or a phased rollout before analytics can even begin producing dependable outputs. The burden falls unevenly across the buyer base, since major utilities, mines, and national portfolios can absorb that work while smaller facilities often delay projects until cost recovery is easier to prove. It also slows reporting readiness, because energy optimization depends on stable, continuous data collection long before users can claim a successful AI deployment or align it to structured management standards. Vendors are adapting with staged implementations that protect installed hardware, but those models still take time and require close client support during commissioning and recalibration. For the South Africa AI-powered energy management software market, this keeps the near-term sales opportunity large while stretching deployment timelines and delaying the point at which savings become visible to cautious buyers.

Weak Data Quality Across Disparate Site Systems

Even where sites are already connected, data quality often remains uneven because different meters, sampling intervals, and naming conventions create incomplete records and inconsistent baselines across buildings, plants, and mixed-use portfolios. Load-shedding adds another layer of disruption because it introduces gaps and abnormalities into time-series data, which forces vendors to recalibrate models more often than they would in a stable-grid operating environment. Energy Partners showed the payoff from better normalization through its Syntiro deployment across 114 Netcare healthcare sites, where the platform tracked 28,000 data points and delivered a 34% reduction in energy use. Data governance demands have also become more material in regulated settings, because operational records may sit close to sensitive business or user information and require stronger controls over how data is collected, stored, and reported. Buyers, therefore, do not evaluate software performance alone; they also evaluate whether the vendor can clean and structure the underlying site data without creating new compliance or reliability concerns. Until that foundation improves across more properties and industrial portfolios, the South Africa AI-powered energy management software market will continue to see uneven results between well-instrumented sites and buildings where data quality limits model confidence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Leadership With Services Gaining Weight

Software accounted for 69.00% of revenue in 2025, making it the largest component of the South Africa AI-powered energy management software market. That leading position reflects the breadth of software demand, because enterprises are not buying a single function; they are buying monitoring, reporting, forecasting, fault detection, predictive maintenance, and distributed resource control inside one operating layer. Large users in mining, utilities, healthcare, and commercial property have also preferred software licenses and subscriptions that can be mapped directly to cost savings, outage reduction, and operating visibility rather than treated as open-ended consulting spend. Eskom’s disclosure of around 200 active AI pilot projects in March 2026, including predictive fault management and an intelligent substation initiative with Huawei, showed the scale of software deployment already underway inside the utility environment. That activity matters because the utility segment remains a reference point for the wider buyer base, and major Eskom-related programs tend to shape expectations around analytics capability, grid responsiveness, and long-term software relevance.

Services are projected to expand at a 24.20% CAGR through 2031, which makes them the fastest-growing component as more buyers need help after the initial platform sale. Many midmarket facilities and distributed portfolios do not have internal teams that can manage model tuning, site onboarding, data cleansing, and regulatory reporting with the speed required for stable outcomes. Buyers are therefore looking for vendors that can package software with integration planning, ongoing optimization, and performance review support rather than leave internal staff to manage a fragmented rollout. Energy Partners’ work across Netcare’s hospital portfolio illustrated how service-led delivery can turn large, complex data environments into measurable efficiency gains. This is gradually shifting value capture within the South Africa AI-powered energy management software industry, because implementation depth and recurring optimization are becoming as important to margins as the software license itself.

By Deployment Mode: Cloud Preference Expands While On-Premises Demand Stays Relevant

Cloud-based deployment held 54.50% of revenue in 2025, and it is also the fastest-growing mode with a projected 24.80% CAGR through 2031. This rare combination of current leadership and top growth shows that the market is not simply testing the cloud; it is actively reorganizing around it for new procurement cycles. One reason is the entry of local cloud infrastructure, which reduced latency concerns and made remote analytics more acceptable for enterprises that need quick response across many buildings and operational sites. Another reason is vendor strategy, because large platform suppliers have been shifting their offers toward cloud-native operating models that make upgrades, benchmarking, and portfolio management easier to scale. Schneider Electric’s April 2026 move to EcoStruxure Energy Intelligence, supported by more than 60 South African Alliance Partners, showed how channel investment is accelerating this change in actual field deployment rather than in product marketing alone.

Cloud also suits listed REITs, healthcare groups, and multi-site operators because a centralized platform can compare buildings that face different municipal tariffs, equipment mixes, and service-level expectations. The ability to supervise many sites from one interface has become more valuable as building owners try to reduce manual operating effort while still maintaining reliable audit trails and performance benchmarking across the portfolio. At the same time, on-premises deployment retains durable demand in utilities, hospitals, financial institutions, and other sensitive facilities where operators want stronger control over system access, latency, and internal data flows. Hybrid architecture remains the smallest base, but it should gain traction as edge-to-cloud models allow sensitive data to be processed locally while aggregated intelligence moves into a broader analytics layer. This split means the South Africa AI-powered energy management software market is not moving toward one architecture only; it is moving toward a clearer division between scale-led cloud adoption and control-led local deployment.

By Application: Demand Optimization Leads While Renewables Forecasting Accelerates Fastest

Energy consumption and demand optimization captured 35.00% of revenue in 2025, which gave it the largest share within application demand. That leadership reflects the practical nature of the use case, because tariff arbitrage, peak shaving, outage response, and load scheduling produce visible savings faster than many other AI applications. Eskom’s tariff schedules for 2025-2026 and 2026-2027 also increased the value of automated response, particularly as the Generation Capacity Charge phase-in reached 30% for the 2026 and 2027 financial years. In parallel, NTCSA’s flexibility program created a structured role for metering and response capability, because participating load providers need the visibility and verification that AI platforms can support. These conditions keep demand optimization at the heart of present-day deployment decisions, and they explain why this use case continues to anchor early budgets across the South Africa AI-powered energy management software market.

Renewable energy forecasting and integration is projected to expand at a 26.50% CAGR through 2031, making it the fastest-growing application in the forecast period. IRP 2025 set a clear buildout path with 25 GW of utility-scale solar PV, 34 GW of onshore wind, and 8.5 GW of battery storage planned by 2039, which raises the need for software that can forecast, coordinate, and dispatch a more diverse generation mix. Eskom’s May 2026 Strategic Development Agreement with Energy Vault for gravity storage at Hendrina Power Station added another example of the more complex operating environment that AI tools will need to support across storage and variable renewable assets. Smart grid and DER management is also gathering momentum as wholesale market rules develop, while electricity trading and market intelligence remain earlier-stage categories that are becoming more relevant with the spread of wheeling and independent power activity. Together, these shifts are broadening the South Africa AI-powered energy management software market from site efficiency software into a wider operating layer for forecasting, flexibility, and market-facing grid coordination.

By End User: Utilities Hold the Largest Base While Commercial Buildings Grow the Fastest

Utilities accounted for 37.00% of revenue in 2025, giving them the largest role in the end-user mix and a strong influence over product direction, procurement standards, and integration expectations. This leadership reflects Eskom’s weight in SCADA, distribution management, and advanced metering environments, where large contracts can shape vendor positioning for years after the initial deployment. ABB stated that its Ability Network Manager SCADA and DMS supports more than 75% of the power distributed across Eskom service territories, giving the company a powerful installed-base bridge for future analytics expansion.[2]ABB, “ABB Ability-Based Software Solutions Support Digitalization of South African Power Grid,” ABB News Center, new.abb.com Municipal utilities are also becoming a more distinct buying group because tariff pass-through, rising behind-the-meter solar activity, and the shift toward more competitive market structures all increase the need for monitoring and settlement capability. As the SAWEM transition advances, utility-side software demand is likely to extend beyond grid visibility and into participant registration, market compliance, interval metering, and dispatch readiness across a wider set of public and private actors.

Commercial buildings are projected to expand at a 24.60% CAGR through 2031, which makes them the fastest-growing end-user segment in the South Africa AI-powered energy management software market. The segment is moving faster because sustainability deadlines, occupancy expectations, energy accountability frameworks, and tariff pressure are all compressing approval cycles for building operators and property owners. Existing BMS relationships also help, because vendors such as Honeywell and Johnson Controls can layer analytics into infrastructure that many commercial customers already know and operate. Industrial users in mining, manufacturing, and food processing remain equally important in value terms, since high power intensity and downtime risk support larger contracts and faster payback logic than lower-load facilities. Residential buildings remain the smallest end-user group, but they continue to matter as a long-term commercialization path for distributed control models that may later scale through service providers, virtual power arrangements, and appliance-level coordination.

Geography Analysis

The South Africa AI-powered energy management software market growth underlines the country’s role as the main center of AI-enabled energy management software activity in sub-Saharan Africa. South Africa’s commercial-scale grid, formal metering environment, and large enterprise base make it structurally different from smaller neighboring markets where software adoption is often constrained by weaker infrastructure or narrower industrial demand. Gauteng remains the densest procurement zone because Johannesburg concentrates listed REIT portfolios, mining-linked operations, financial activity, and a growing data center corridor that all support complex energy management requirements.

South Africa differs from most of sub-Saharan Africa because the central issue is not basic electricity access; it is the reliability and cost control of power for already connected enterprises with large and measurable energy exposure. That difference narrows the buyer base toward organizations with clear operating savings potential, but it also lifts contract sophistication because software is being bought to protect uptime, manage tariffs, and coordinate distributed assets under difficult grid conditions. South Africa’s second NDC, submitted in October 2025, set a path toward a net-zero electricity sector by 2050, with coal declining from 58% in 2025 to 27% by 2039, while wind rises from 8% to 24% and solar PV increases from 10% to 18%. Every step in that transition increases the operational need for forecasting, balancing, and flexible resource coordination across the South Africa AI-powered energy management software market.

GIZ’s SAGEN 4 program is helping municipalities such as Buffalo City, Mangaung, and Ekurhuleni strengthen practical energy management capability, which supports expansion beyond the most advanced metro areas.[3]Deutsche Gesellschaft für Internationale Zusammenarbeit, “Support for the Transformation of the South African Energy Sector, SAGEN 4,” GIZ, giz.de This matters because secondary cities still lag Gauteng and the Western Cape in system readiness, technical staffing, and data consistency, which leaves a meaningful adoption gap within the country itself. NERSA’s May 2026 consultation on the SAWEM Wholesale Price Framework and Transitional Generation Pricing Framework marked an important policy step toward more competitive power market operations. Once those rules are finalized, real-time metering, dispatch, and settlement needs are likely to broaden the addressable base for the South Africa AI-powered energy management software market across municipal and industrial demand centers that were not previously active software buyers.

Competitive Landscape

The South Africa AI-powered energy management software market remains moderately concentrated, with global OEMs controlling much of the installed base while local AI companies and focused specialists compete for new deployments, managed services, and market-adjacent use cases. Schneider Electric, ABB, Honeywell, Siemens, and Johnson Controls benefit from long-standing building and industrial control relationships that reduce switching friction and make AI add-ons easier to position inside existing client environments. ABB stated that its Ability Network Manager SCADA and DMS supports more than 75% of the power distributed across Eskom service territories, which gives it a strong installed pathway for analytics upgrades and adjacent software services. Schneider Electric strengthened its local channel in April 2026 through the move to EcoStruxure Energy Intelligence and a partner network of more than 60 South African Alliance Partners, which extended its field reach across industrial, commercial, and infrastructure customers. That means incumbents are competing less on stand-alone software claims and more on their ability to attach AI capability to a hardware and controls base that customers already operate.

Local challengers are pursuing a different route because they are building around South African tariff structures, load-shedding behavior, wheeling activity, and site-level dispatch needs rather than starting from globally templated operating assumptions. Wetility’s AI Mode gave a clear example when beta testing across hundreds of sites maintained zero outages during active load-shedding events, showing how local operating data can shape more responsive control logic. Open Access Energy has also pushed into an area that large OEMs have not fully defined, using its EnergyPro platform and its May 2026 partnership with Mezzanine to support virtual wheeling and real-time electricity trading workflows. Plentify’s oversubscribed Series A round in November 2025 further showed that investors view South Africa’s grid conditions as a credible proving ground for locally engineered intelligent energy platforms.[4]Plentify, “Plentify Closes Oversubscribed Series A to Accelerate Global Rollout of Its Intelligent Energy Platform,” Plentify, plentify.io

White space remains strongest in smaller commercial buildings, secondary municipalities, and new trading-related workflows where enterprise-grade platforms can be too expensive, too rigid, or too dependent on modernized infrastructure. Eskom’s disclosure of around 200 active AI pilot projects in March 2026 also showed that the utility is building internal analytical capability, which may gradually alter how software vendors engage with the largest buyer in the country. The May 2026 agreement between Eskom and Energy Vault for a gravity storage deployment at Hendrina Power Station created another visible test case for vendors that can coordinate storage, renewable output, and dispatch decisions in real time. In this setting, competitive advantage in the South Africa AI-powered energy management software market comes from a mix of installed-base access, local model training, and strong implementation support rather than from software features alone.

South Africa AI-Powered Energy Management Software Industry Leaders

ABB Ltd.

Accruent, LLC

AutoGrid Systems, Inc.

Bidgely, Inc.

C3.ai, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Eskom and Energy Vault Holdings announced a Strategic Development Agreement to deploy Energy Vault’s EVx 2.0™ gravity energy storage system at Hendrina Power Station, Mpumalanga, with an initial capacity of 25 MW and 100 MWh and a target of up to 4 GWh across the SADC region by 2035. The partnership uses coal-ash re-use blocks as a storage medium, supporting South Africa’s Just Energy Transition goals while creating a new integration requirement for AI-powered DER management platforms capable of coordinating long-duration storage dispatch alongside solar and wind generation assets.

- May 2026: Mezzanine and Open Access Energy partnered to accelerate virtual wheeling adoption in South Africa, combining Mezzanine’s grid-wheeling technology platform with Open Access Energy’s AI-powered EnergyPro software to enable multi-party real-time electricity trading across independent power producers, municipalities, and commercial consumers. The collaboration represents the first commercially structured AI energy trading infrastructure deployment aligned to the incoming SAWEM market rules.

- April 2026: Schneider Electric launched a localized channel program in Sub-Saharan Africa, transitioning EcoStruxure to EcoStruxure Energy Intelligence, an AI-powered platform for real-time operational visibility across industrial, commercial, and infrastructure segments. Over 60 South African Alliance Partners are enrolled, embedding AI-driven analytics at scale across the domestic market.

- March 2026: Eskom disclosed around 200 active AI pilot projects, including a predictive fault management system and an intelligent substation initiative developed with Huawei, as part of a long-term aspiration to build a self-healing national grid. The utility, which reported its first profit in 8 years in 2025, plans to invest ZAR 320 billion (USD 17.3 billion), over 5 years, sustaining a multi-year software procurement pipeline.

South Africa AI-Powered Energy Management Software Market Report Scope

The South Africa AI-powered energy management software market comprises AI-driven software solutions and related services that optimize energy production, distribution, storage, and consumption through intelligent analytics, automation, and predictive modeling. These platforms leverage machine learning, artificial intelligence, digital twins, advanced forecasting, and real-time monitoring technologies to improve energy efficiency, enhance asset utilization, facilitate renewable energy integration, and support Canada's decarbonization and net-zero objectives.

The South Africa AI-Powered Energy Management Software Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Smart Grid and Distributed Energy Resource (DER) Management, Renewable Energy Forecasting and Integration, and Energy Trading, Pricing and Market Intelligence), and End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential Buildings). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings |

Key Questions Answered in the Report

How large is the South Africa AI-powered energy management software market in 2026?

The South Africa AI-powered energy management software market registers USD 53.61 million in 2026 and is projected to reach USD 141.95 million by 2031 at a 21.50% CAGR.

What is driving demand for AI-powered energy management software in South Africa?

Rising Eskom tariffs, repeated load-shedding, tighter corporate energy accountability, and the need for better demand optimization are the main demand drivers.

Which application area is expanding the fastest in South Africa?

Renewable energy forecasting and integration is projected to grow the fastest, with a 26.50% CAGR through 2031, supported by IRP 2025 and expanding storage and renewables deployment.

Which deployment model leads the South Africa AI-powered energy management software space?

Cloud-based deployment led with 54.50% of revenue in 2025 and is also the fastest-growing mode at a 24.80% CAGR because multi-site operators want centralized visibility and analytics.

Which end-user group spends the most on these platforms in South Africa?

Utilities were the largest end-user segment in 2025 with 37.00% of revenue, reflecting Eskom’s role in grid software, SCADA, and metering-driven procurement.

Why are services growing so quickly in this space?

Services are projected to grow at a 24.20% CAGR because many buyers need help with legacy integration, data normalization, ongoing optimization, and compliance-oriented reporting after the initial software sale.

Page last updated on: