Asia-Pacific AI-Powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

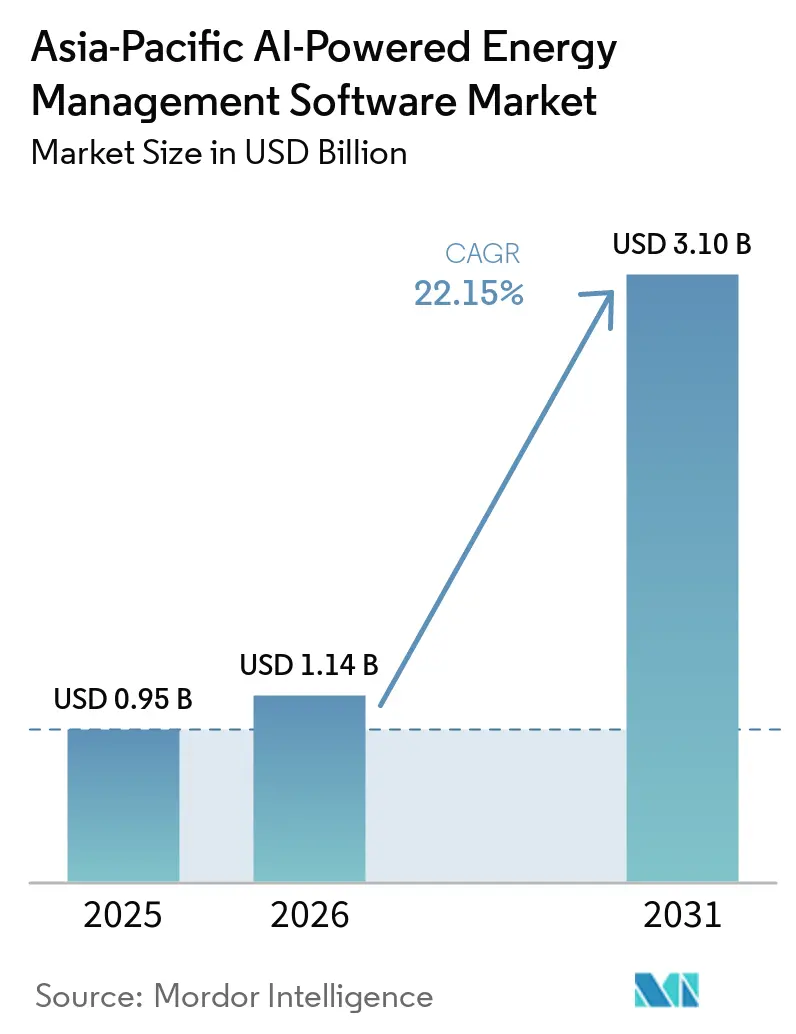

| Base Year Market Size (2025) | USD 0.95 Billion |

| Market Size (2026) | USD 1.14 Billion |

| Market Size (2031) | USD 3.10 Billion |

| Growth Rate (2026 - 2031) | 22.15% CAGR |

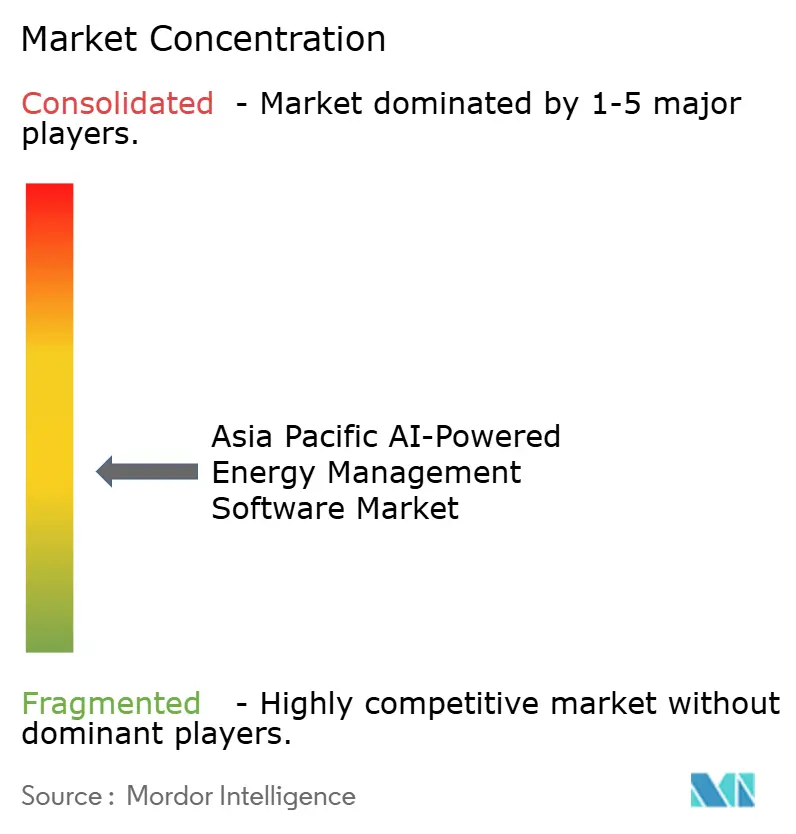

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific AI-Powered Energy Management Software Market Analysis by Mordor Intelligence

The Asia-Pacific AI-powered energy management software market size was valued at USD 0.95 billion in 2025 and is forecast to reach USD 3.10 billion by 2031, advancing at a CAGR of 22.15% during 2026-2031. Growth is being supported by rapid renewable energy additions across the region, which are increasing the need for software that can forecast variable generation and coordinate distributed assets in real time. The complexity of electricity tariffs in major economies is also pushing commercial and industrial users toward systems that can optimize load, storage, and on-site generation with less manual intervention. Compliance needs are widening the buying base, as energy data now matters not only to facility teams but also to finance and reporting functions. Deployment choices are becoming more nuanced, with cloud platforms expanding quickly while hybrid models remain important for users who need local control and lower latency. Competition in the Asia-Pacific AI-powered energy management software market is therefore centered on platform breadth, integration capability, and the ability to deliver measurable savings within practical payback periods.

Key Report Takeaways

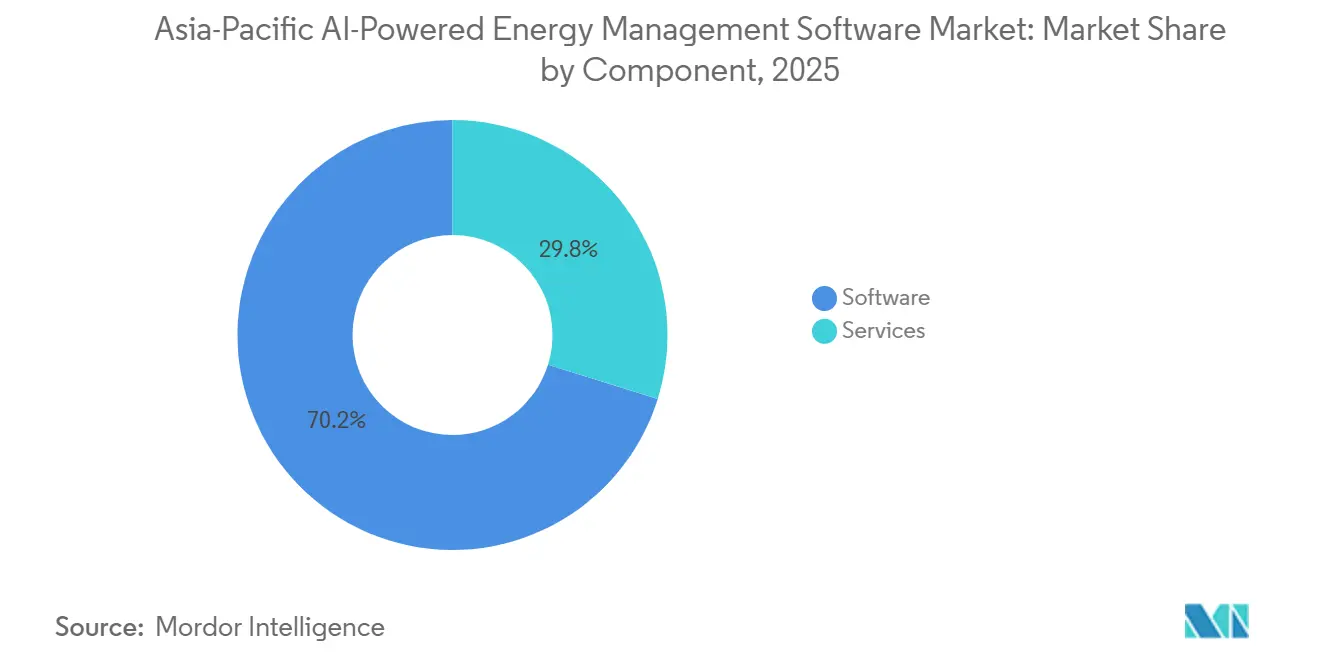

- By component, software held 70.18% of the Asia-Pacific AI-powered energy management software market share in 2025, while services are projected to expand at a 22.23% CAGR through 2031.

- By deployment mode, cloud-based solutions accounted for 61.14% of the market in 2025, while hybrid deployment is projected to record the fastest 22.34% CAGR through 2031.

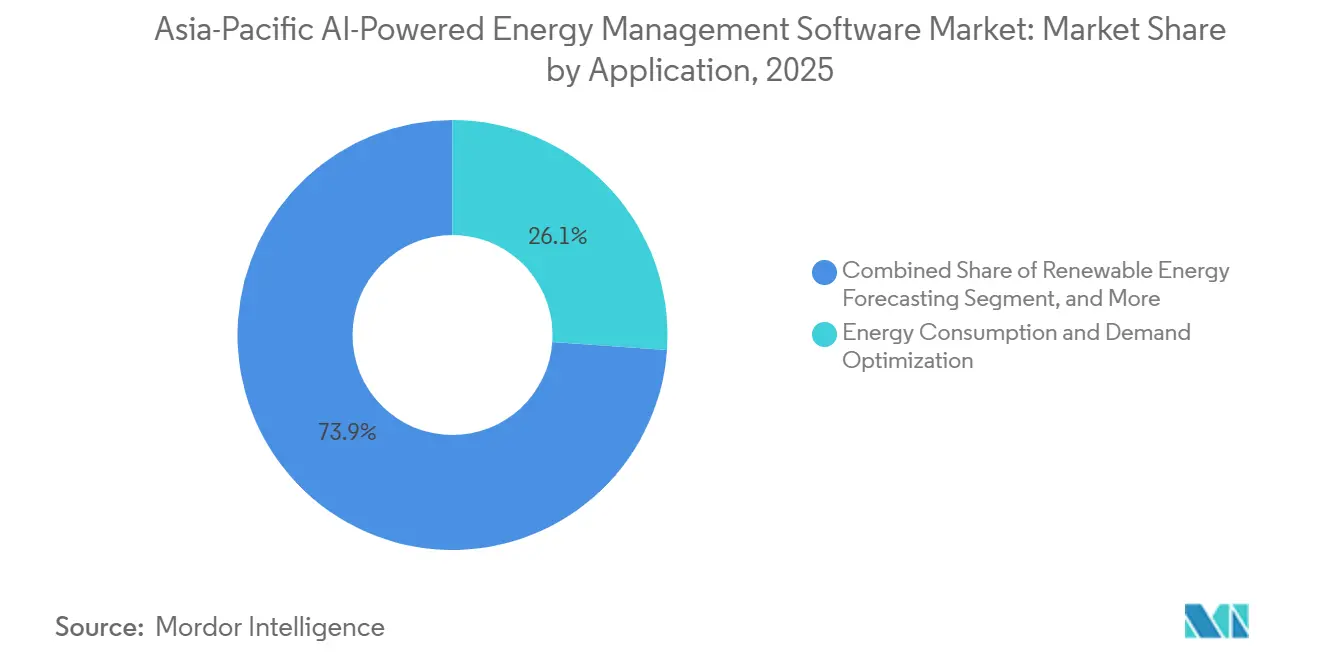

- By application, energy consumption and demand optimization accounted for 26.12% of the Asia-Pacific AI-powered energy management software market size in 2025, while renewable energy forecasting and integration are projected to advance at a 22.47% CAGR through 2031.

- By end user, utilities held 30.11% share in 2025, while industrial facilities are projected to expand at a 22.58% CAGR through 2031.

- By geography, China held 37.16% share in 2025, while India is projected to record the fastest 22.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific AI-Powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Need for Real-Time Energy Optimization in Commercial and Industrial Facilities | +5.0% | APAC-wide, concentrated in China, India, Japan, and South Korea | Short term (≤ 2 years) |

| AI Integration With Smart Grids and Distributed Energy Resources | +4.5% | China, India, Japan, South Korea, Australia and New Zealand | Medium term (2-4 years) |

| Increasing Demand for Automated Demand Response and Peak Load Management | +3.0% | Japan, South Korea, Australia and New Zealand, China | Short term (≤ 2 years) |

| Expansion of ESG Reporting and Carbon Accounting Workflows | +3.0% | Singapore, Japan, Hong Kong, China, Australia and New Zealand | Medium term (2-4 years) |

| Edge AI Adoption for Site-Level Energy Control and Fault Detection | +2.5% | APAC industrial corridors, China, India, South Korea, Southeast Asia | Medium term (2-4 years) |

| Growing Retrofit Demand From Aging Building and Industrial Infrastructure | +1.5% | Japan, South Korea, Australia and New Zealand, secondary in ASEAN | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Need For Real-Time Energy Optimization in Commercial And Industrial Facilities

Commercial and industrial operators across the Asia-Pacific are dealing with tariff structures that penalize peak demand as heavily as total consumption. In India, high-tension distribution tariffs include time-of-day peak rates that run 40-70% above off-peak levels, while demand charges account for 30-40% of total electricity bills. This pricing structure devalues passive monitoring and increases demand for AI platforms that can schedule battery storage, manage solar output, and shift loads in real time. The Asia-Pacific AI-powered energy management software market is benefiting from this trend, as large manufacturing and commercial sites can often adjust energy use without interrupting core operations. Honeywell and Tata Consultancy Services announced a partnership in February 2026 to advance AI-driven autonomous operations for buildings and industries, with India as the initial focus market.[1]Honeywell, “Honeywell and TCS Collaborate to Enhance Autonomous Operations for Buildings and Industries with AI,” Honeywell, honeywell.com

AI Integration with Smart Grids and Distributed Energy Resources

AI integration with smart grids and distributed resources is improving dispatch quality and system visibility across the region. Korea Electric Power Corporation operates a virtual power plant platform that aggregates more than 2.8 GW of distributed resources and uses AI to coordinate batteries, HVAC systems, and industrial loads.[2]AIVPP, “Asia-Pacific,” AIVPP, aivpp.com.au China added another layer of support in May 2026 when the National Energy Administration and other agencies issued an action plan with 51 AI and energy application scenarios and a 2030 capability target. Utilities that both deploy and operate these systems gain an advantage because they become vendors, operators, and reference customers simultaneously. This underscores the value of proven orchestration tools in the Asia-Pacific AI-powered energy management software market, especially for utilities that need software that can operate across grid, load, and storage layers.

Increasing Demand for Automated Demand Response and Peak Load Management

Automated demand response is moving from a utility program to a built-in capability within AI energy management platforms. Kansai Electric Power launched a demand-shift demand response program in April 2025 using Nature Inc.'s demand response support service and smartphone-linked home energy management controls.[3]Nature Inc., “Nature's ‘Demand Response Support Service’ Adopted for Kansai Electric Power's New Initiative ‘DR Project (Demand Shift Type)’,” III Three, iii-three.com This shift allows batteries, building systems, and connected devices to respond to price signals and grid events with less manual coordination. Vendors benefit because they can turn previously idle flexibility into a revenue-generating service layer for utilities and site operators. The Asia-Pacific AI-powered energy management software market is well-positioned for this model, as the region already has large pools of residential and commercial assets that can be aggregated into utility-grade flexible capacity.

Expansion of ESG Reporting and Carbon Accounting Workflows

Climate and carbon reporting requirements are widening the use case for energy management software beyond direct energy savings. Buyers increasingly need facility-level data that supports internal tracking, external reporting, and operational decisions from a single platform. This changes purchasing behavior because finance, compliance, and sustainability teams are becoming more involved in software selection alongside facility managers. The Asia-Pacific AI-powered energy management software market is benefiting from platforms that link operational data with traceable reporting outputs, which meet a broader set of business needs. This trend also favors vendors that can customize dashboards, data models, and reporting workflows without requiring a full rebuild of the core platform.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity with Legacy OT and IT Systems | -2.0% | APAC-wide, most acute in Japan, South Korea, and legacy industrial corridors in China and India | Short term (≤ 2 years) |

| Data Quality, Interoperability, and Sensor Fragmentation Issues | -1.5% | ASEAN, India, China secondary cities, Rest of Asia-Pacific | Medium term (2-4 years) |

| Cybersecurity and Data Sovereignty Concerns for Critical Energy Assets | -1.2% | APAC-wide, especially utilities in Australia, India, and Southeast Asia | Medium term (2-4 years) |

| Payback Uncertainty in Small and Mid-Sized Sites With Limited Load Density | -0.8% | ASEAN, India tier-2 and tier-3 markets, Rest of Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity with Legacy OT And IT Systems

A major obstacle in the Asia-Pacific AI-powered energy management software market is the gap between modern software stacks and long-installed operational technology. Many utilities, factories, and large buildings still rely on proprietary protocols and control systems that were never designed for open data exchange. That forces vendors to build site-specific connectors and middleware, which raises cost and extends deployment timelines. The problem also lasts longer than a normal software cycle because energy and industrial assets are often replaced over 15-25 years rather than every few years. As a result, vendors that can handle mixed environments with less customization are more likely to scale across public utilities and heavy industry.

Data Quality, Interoperability, and Sensor Fragmentation Issues

AI energy optimization depends on continuous, granular, and reliable data, but many sites still operate with fragmented meters and incompatible data formats. The result is weaker model accuracy, slower optimization feedback, and more work during deployment. This issue is usually less severe in large urban sites with better digital infrastructure, but it remains pronounced in secondary industrial zones and smaller commercial facilities. The Asia-Pacific AI-powered energy management software market, therefore, advances at different speeds across the region, even when demand conditions appear similar at a high level. Vendors that can normalize incomplete or uneven data have a clear advantage in these environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component, Software Dominance Masks A Services Acceleration

Software held 70.18% of the Asia-Pacific AI-powered energy management software market share in 2025, reflecting the strong preference for platform-led deployments over isolated point tools. This share was supported by subscription models that moved spending into operating budgets and simplified the buying process for many users. Software also remained the main commercial layer because forecasting, optimization, and reporting are now expected to sit on a single interface rather than across separate tools. Within the Asia-Pacific AI-powered energy management software market, this gave vendors with broader platform capability a clear advantage in early and mid-stage deployments.

Services are projected to expand at a 22.23% CAGR during 2026-2031, which shows that deployment support is rising almost as quickly as core software demand. Clients still need system integration, model tuning, data pipeline maintenance, and workflow customization after the initial installation. This keeps services relevant well beyond launch and raises switching costs once a platform is embedded into daily operations. Honeywell's February 2026 partnership with Tata Consultancy Services reflected this direction by pairing technology capability with implementation depth for buildings and industrial sites.

By Deployment Mode, Cloud Leads While Hybrid Gains With Control-Sensitive Users

Cloud-based deployment accounted for 61.14% of the market in 2025, supported by expanding digital infrastructure across China, India, Singapore, Japan, and Australia. Cloud models appeal to users who want lower in-house IT requirements, easier updates, and faster rollout across multiple sites. This has been especially relevant for commercial building operators and smaller utilities that do not want to maintain their own full data stack. The Asia-Pacific AI-powered energy management software market continues to favor cloud for scalability, but the pattern is not uniform across all end users.

Hybrid deployment is projected to grow at a 22.34% CAGR from 2026 to 2031, making it the fastest-growing mode in the market. This reflects the needs of utilities and industrial operators that want local control for latency-sensitive functions while still using cloud analytics for broader optimization. Hybrid setups are also easier to accept when data sovereignty policies or operational risk make a full cloud migration difficult. Over time, this creates an opening for vendors that can coordinate edge processing, on-site control, and centralized analytics without forcing customers into a single architecture.

By Application, Demand Optimization Leads While Renewable Forecasting Builds Fastest

Energy consumption and demand optimization accounted for 26.12% of the Asia-Pacific AI-powered energy management software market size in 2025, making it the largest application area. The segment led because peak shaving, load shifting, and bill reduction are easier for customers to measure than many longer-cycle software benefits. Asset performance, predictive maintenance, smart grid management, and energy trading use cases are also expanding, but demand optimization still offers the clearest near-term payback. In the Asia-Pacific AI-powered energy management software market, this keeps.

Renewable energy forecasting and integration is projected to expand at a 22.47% CAGR through 2031, reflecting the region's growing need to manage variable solar and wind output. As renewable penetration rises, operators need stronger sub-hourly and day-ahead forecasting to schedule balancing resources and reduce curtailment risk. Research published in 2025 on climate-aware multi-agent reinforcement learning for Indian smart grids reported 40-57% performance improvement over reactive control baselines across Tamil Nadu, Odisha, Rajasthan, and Bihar. This supports the view that forecasting and coordination tools will move from a specialist function into a more standard platform requirement.

By End User, Utilities Hold Scale While Industrial Facilities set The Growth Pace

Utilities accounted for 30.11% of the market in 2025, making them the largest end-user group by revenue. They remain anchor customers because they deploy software across larger operating footprints that include grid management, forecasting, and distributed asset coordination. Utility contracts also serve as strong reference points for vendors entering adjacent accounts in generation, buildings, and industrial sites. This gives utilities a central role in shaping demand patterns across the Asia-Pacific AI-powered energy management software market.

Industrial facilities are projected to grow at a 22.58% CAGR during 2026-2031, driven by cost pressure in energy-intensive operations such as steel, aluminum, chemicals, and semiconductor fabrication. These sites have large controllable loads, which makes AI-led optimization more financially meaningful than in lighter-use settings. Commercial buildings are also scaling, with Johnson Controls reporting up to 30% energy reduction at Jakarta's Thamrin Nine through its building management and OpenBlue platform deployment. Residential adoption remains earlier in its development path, but time-based tariffs and connected devices in markets such as Japan and Australia continue to improve the case for household-level AI energy control.[4]Johnson Controls, “Johnson Controls Helps Cut Energy Use by 30% at Jakarta's Thamrin Nine,” Johnson Controls Singapore, johnsoncontrols.sg

Geography Analysis

China held 37.16% of the Asia-Pacific AI-powered energy management software market share in 2025, maintaining its leading regional position. The country's scale is reinforced by strong policy alignment, especially following the May 2026 action plan, which introduced 51 AI and energy application scenarios and a 2030 capability target. This creates a clearer deployment pathway for vendors that already have accepted references in utility and grid settings. At the same time, data sovereignty expectations continue to favor domestic platforms, making joint development or licensing more practical for foreign participants.

India is projected to record the fastest 22.67% CAGR in the Asia-Pacific AI-powered energy management software market through 2031. Its growth is supported by rapid renewable additions, complex distribution utility tariffs, and strong demand for localized software logic that reflects state-level billing structures. Honeywell and Tata Consultancy Services selected India as the first launch market for their AI-driven autonomous operations partnership in February 2026. Vendors that can work across multiple DISCOM environments have a stronger localization moat and better chances of scaling across commercial and industrial portfolios.

Japan and South Korea remain important reference markets because they combine grid complexity with mature operating environments. In Japan, Kansai Electric Power's demand-shift initiative showed how demand response is moving toward device-level automated control rather than simple monitoring. South Korea's large virtual power plant activity strengthens the case for AI-led aggregation and dispatch at utility scale. Australia and New Zealand are also advancing through distributed flexibility and home energy control, with Enphase launching IQ Energy Management in March 2026. The rest of Asia-Pacific, especially Southeast Asia, remains a large underpenetrated pool where vendors can still build first-mover positions by adapting to fragmented grids and uneven sensor coverage.

Competitive Landscape

The Asia-Pacific AI-powered energy management software market includes large automation and industrial technology vendors, major cloud infrastructure providers, and AI-native specialists. Companies such as Siemens, Schneider Electric, ABB, and Honeywell compete on breadth across grid, building, and energy optimization functions. Microsoft and Amazon Web Services are also relevant because they embed analytics capability into digital infrastructure that many customers already use. At the same time, specialists such as Bidgely and C3.ai continue to gain attention where predictive performance and distributed energy resource analytics matter most.

Strategic moves in 2025 and 2026 show that capability expansion is happening through both acquisition and partnership. Bidgely acquired Grid4C in March 2025 and combined consumer-side disaggregation with grid-side predictive analytics inside a single UtilityAI platform. Johnson Controls acquired Nantum AI in April 2026 to add proprietary AI HVAC optimization algorithms to its OpenBlue ecosystem. Honeywell and Tata Consultancy Services also formed a February 2026 partnership to advance AI-driven autonomous operations for buildings and industries, which points to rising interest in combined platform and execution models.

Open space remains in hybrid virtual power plant software for ASEAN utilities, AI-native analytics for India's fragmented distribution environment, and operational energy platforms that support wider reporting needs. Edge processing is becoming more important because some users need fault detection and dispatch decisions without waiting for cloud round trips. Vendors with strong regional deployment references are therefore gaining an advantage over firms that rely only on brand recognition or a broad global product list. The Asia-Pacific AI-powered energy management software market still leaves room for specialists because customer needs differ widely across utilities, industrial sites, and buildings. Large vendors keep an installed-base advantage, but specialists can still win where they solve local integration, forecasting, or control problems more precisely.

Asia-Pacific AI-Powered Energy Management Software Industry Leaders

Schneider Electric SE

Siemens AG

Honeywell International Inc.

IBM Corporation

Johnson Controls International plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: China's NDRC, NEA, MIIT, and National Data Bureau jointly issued the "Action Plan for Promoting AI-Energy Bidirectional Empowerment" (Document No. 34), releasing 51 high-value AI+energy application scenarios and mandating targets for world-leading AI energy capabilities by 2030, with 25 energy enterprises signing an open-scene commitment at the NEA's national AI+energy field conference in Shenzhen.

- April 2026: Johnson Controls acquired Nantum AI, a New York-based AI algorithm specialist, to integrate proprietary AI-driven HVAC optimization algorithms into its OpenBlue digital ecosystem; Nantum AI's deployed solutions were already delivering over 10% energy savings per facility at the time of acquisition.

- March 2026: Enphase Energy launched IQ Energy Management in Australia and New Zealand, combining AI with the IQ Energy Router suite to manage home solar, batteries, electric water heaters, and EV chargers, with autonomous control aligned to variable electricity rates; Enphase has shipped approximately 86.4 million microinverters globally to date.

- February 2026: Honeywell and Tata Consultancy Services (TCS) announced a strategic partnership to advance AI-driven autonomous operations for buildings and industries in India, combining Honeywell's AI-powered industrial and building technologies with TCS's AI and engineering capabilities; the initiative will extend to global regions after the India launch.

Asia-Pacific AI-Powered Energy Management Software Market Report Scope

The Asia-Pacific AI-Powered Energy Management Software market comprises platforms and services that leverage artificial intelligence to optimize energy consumption, enhance asset performance, and enable smarter grid and distributed energy resource (DER) management across the region. These solutions provide advanced capabilities, including predictive maintenance, renewable energy forecasting, demand-side optimization, and market intelligence for energy trading and pricing.

The Asia-Pacific AI-Powered Energy Management Software market report is segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Smart Grid and Distributed Energy Resource (DER) Management, Renewable Energy Forecasting and Integration, and Energy Trading, Pricing and Market Intelligence), End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential Buildings), and Geography (China, India, Japan, South Korea, Australia and New Zealand, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| China |

| India |

| Japan |

| South Korea |

| Australia and New Zealand |

| Rest of Asia-Pacific |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current size and 2031 outlook for Asia-Pacific AI-powered energy management software?

The market was valued at USD 0.95 billion in 2025 and is forecast to reach USD 3.10 billion by 2031 at a 22.15% CAGR during 2026-2031.

Which component leads revenue and which one grows fastest in this space?

Software led with 70.18% share in 2025, while services are projected to grow fastest at a 22.23% CAGR through 2031.

Why are hybrid deployments gaining traction across Asia-Pacific energy software platforms?

Hybrid models are growing at a 22.34% CAGR because utilities and industrial operators want local control for low-latency functions while still using cloud analytics.

Which application is expanding the fastest across AI-led energy platforms in the region?

Renewable energy forecasting and integration is projected to grow at a 22.47% CAGR, supported by rising solar and wind penetration and the need for better balancing decisions.

Which country leads the region today and which one is growing the fastest?

China led with 37.16% share in 2025, while India is projected to post the fastest 22.67% CAGR through 2031.

How are leading companies strengthening their position in this market?

Vendors are using acquisitions and partnerships, including Bidgely's Grid4C deal, Johnson Controls' Nantum AI acquisition, and the Honeywell-TCS partnership in India.

Page last updated on: