China AI-Powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

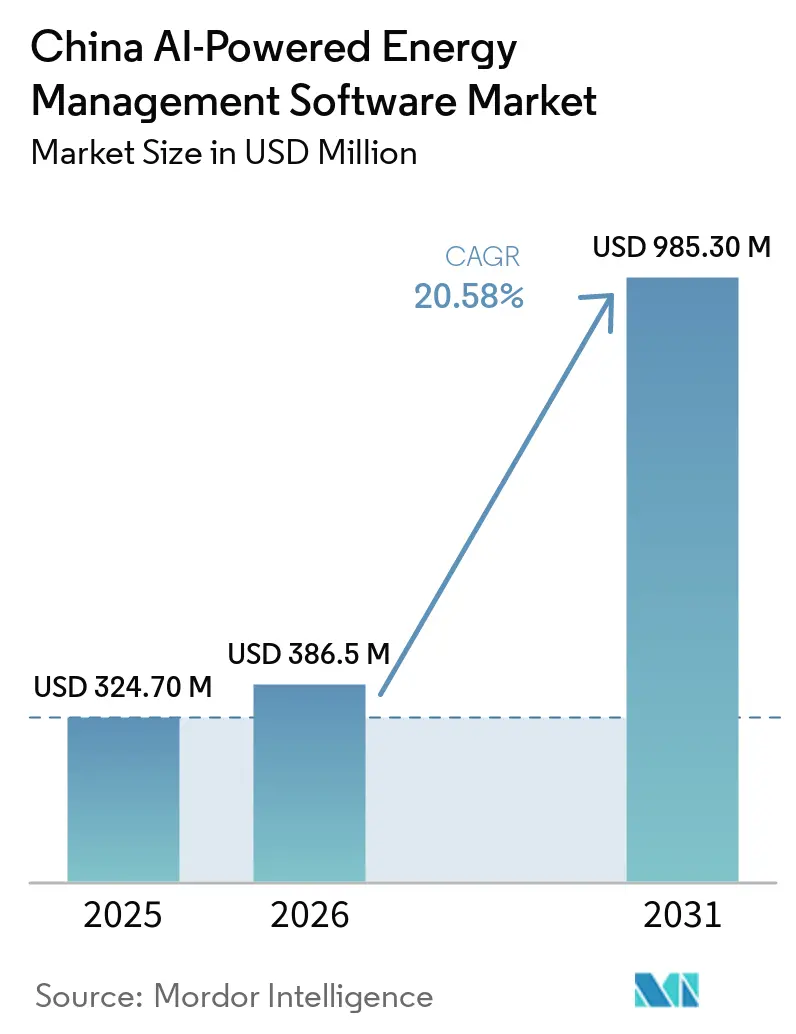

| Base Year Market Size (2025) | USD 324.70 Million |

| Market Size (2026) | USD 386.5 Million |

| Market Size (2031) | USD 985.30 Million |

| Growth Rate (2026 - 2031) | 20.58% CAGR |

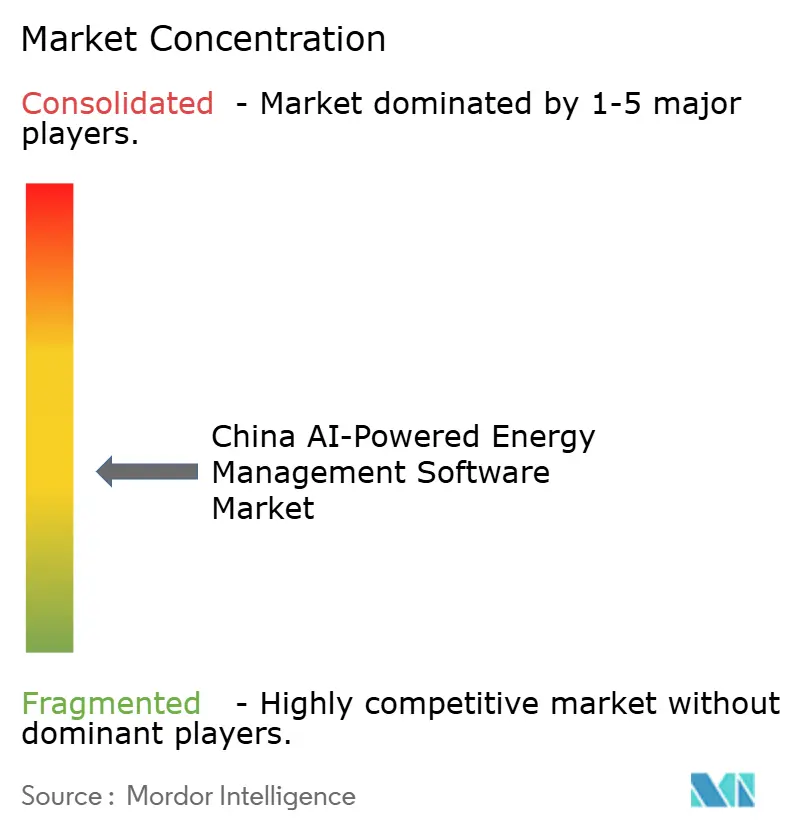

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China AI-Powered Energy Management Software Market Analysis by Mordor Intelligence

The China AI-Powered Energy Management Software market size is projected to be USD 324.7 million in 2025, USD 386.5 million in 2026, and reach USD 985.3 million by 2031, growing at a CAGR of 20.58% from 2026 to 2031. The China AI-Powered Energy Management Software Market is advancing as policy support now links AI adoption more closely with grid modernization, industrial efficiency, and carbon management needs. Power demand from AI infrastructure is rising quickly, which is increasing the need for software that can balance loads, improve forecasting, and reduce avoidable consumption across utilities and large facilities. The market is also benefiting from a shift in buyer behavior, as many enterprises now view energy software as part of compliance and operational control rather than a stand-alone cost tool. Competitive activity remains active across automation vendors, cloud platforms, and specialized energy software providers, with buyers placing greater weight on local deployment capability, integration support, and data governance readiness. The strongest openings through 2031 are likely to remain in hybrid architectures, industrial deployments, carbon accounting workflows, and utility-linked applications that connect AI models to operational systems.

Key Report Takeaways

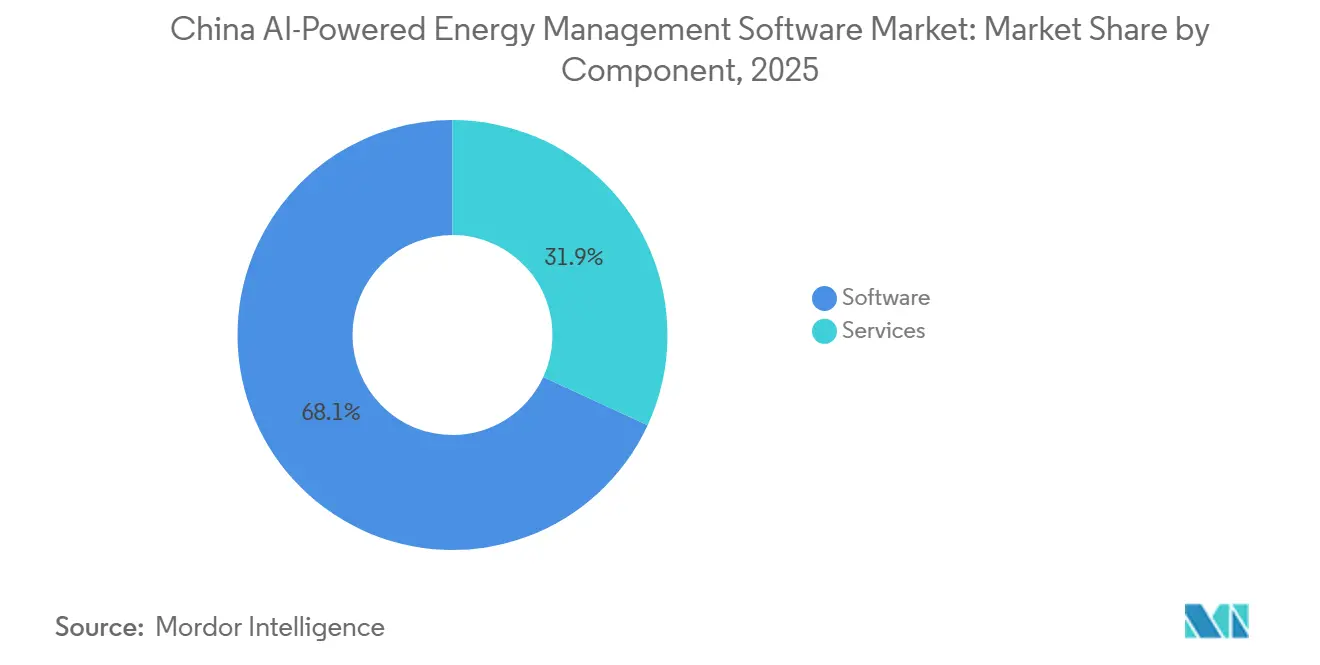

- By component, software led with 68.11% revenue share of the China AI-Powered Energy Management Software market in 2025, while services are projected to expand at a 21.22% CAGR through 2031.

- By deployment mode, cloud-based deployment held 58.16% of the China AI-Powered Energy Management Software market share in 2025, while hybrid deployment recorded the highest projected CAGR at 21.34% through 2031.

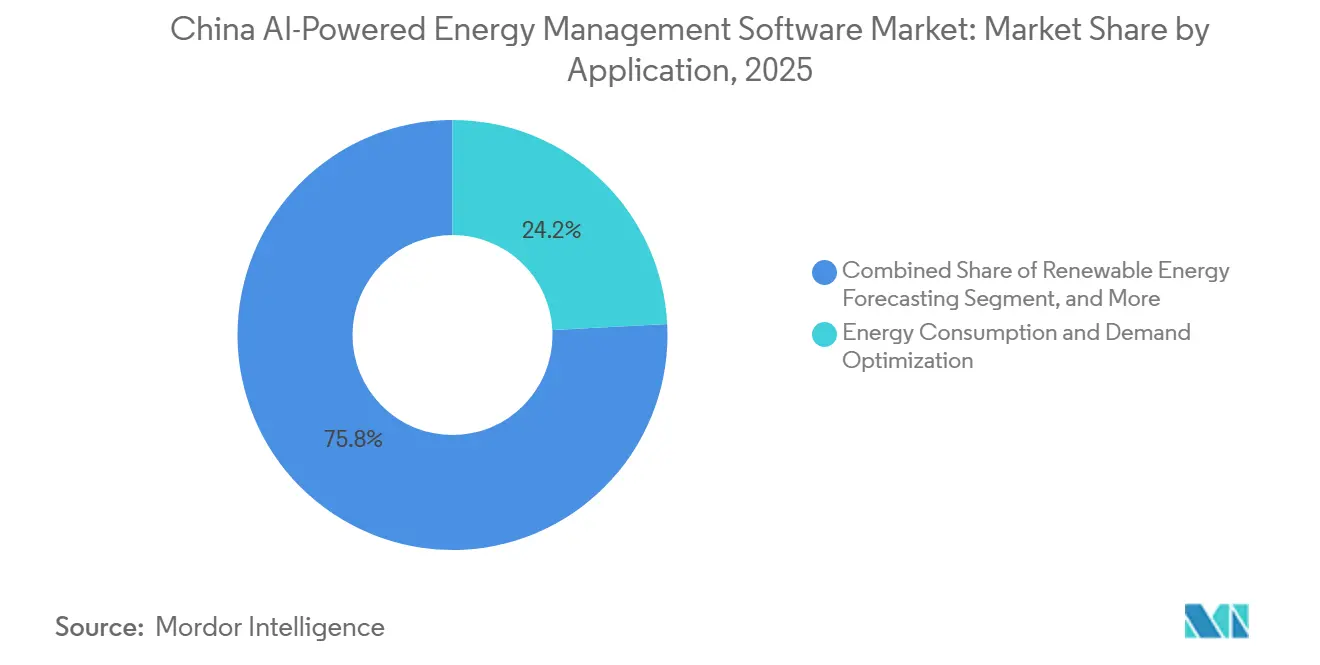

- By application, energy consumption and demand optimization accounted for 24.19% of the China AI-Powered Energy Management Software market in 2025, while renewable energy forecasting and integration is projected to grow at a 21.46% CAGR through 2031.

- By end user, utilities held 33.13% of revenue in 2025, while industrial facilities are expected to expand at a 21.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China AI-Powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| river | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Need for Real-Time Energy Optimization in Commercial and Industrial Facilities | +4.5% | National, with high concentration in Guangdong, Jiangsu, Zhejiang, and Shandong industrial corridors | Short term (≤ 2 years) |

| Integration of AI with Smart Grid and Distributed Energy Resources | +3.8% | National grid operators, concentrated in eastern coastal and northern grid regions | Medium term (2-4 years) |

| Increasing Demand for Automated Demand Response and Peak Load Management | +3.2% | National, with early gains in Guangdong, Shanghai, and Jiangsu provincial electricity spot markets | Medium term (2-4 years) |

| Expansion of ESG Reporting and Carbon Accounting Workflows | +2.8% | National, intensified in export-oriented manufacturing hubs including the Pearl River Delta and Yangtze River Delta | Medium term (2-4 years) |

| Edge AI Adoption for Site-Level Energy Control and Fault Detection | +2.0% | National, with strongest uptake in western China data-center clusters and remote industrial sites | Long term (≥ 4 years) |

| Growing Retrofit Demand From Aging Building and Industrial Infrastructure | +1.5% | National, with the greatest backlog in northeastern provinces and tier-2 city industrial parks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Need For Real-Time Energy Optimization in Commercial and Industrial Facilities

Industrial and commercial energy users remain central to the China AI-Powered Energy Management Software Market, as they face growing pressure to control consumption while meeting increasingly stringent efficiency and carbon-emission targets. The September 2025 implementation opinions from the National Development and Reform Commission and the National Energy Administration moved AI in energy from a broad policy theme to a defined application agenda across power, coal, and oil and gas systems.[1]National Energy Administration, “Notice on Action Plan for Promoting Two-Way Empowerment of AI and Energy,” National Energy Administration, nea.gov.cn The May 2026 action plan then expanded on that direction by setting out 51 AI and energy application scenarios, providing enterprises and utilities with a clearer path for procurement and deployment. This policy structure matters because buyers now have stronger reasons to justify software spending that improves monitoring, control, and reporting across plants and buildings. It also helps explain why the China AI-Powered Energy Management Software Market is seeing demand not only for core analytics tools, but also for implementation support and workflow integration tied to real operating decisions.

Integration of AI With Smart Grid and Distributed Energy Resources

The China AI-Powered Energy Management Software Market is also gaining support from the grid side, where integrating renewables and balancing power have become more difficult to manage with static tools. China’s renewables already accounted for 48% of installed power capacity, and that has raised the value of software that can forecast variable output and coordinate distributed resources more effectively.[2]Editorial Team, “Cover Story, China’s AI Boom Is Rewiring Its Power Grid,” Caixin Global, caixinglobal.com The 2026 national action plan specifically included smart grids, virtual power plants, and new energy forecasting among its priority application areas, indicating that grid-facing AI use cases are now part of formal state planning. That creates a stronger demand base for vendors whose products can work across grid operations, distributed assets, and enterprise energy systems. It also raises the bar in the China AI-Powered Energy Management Software Market, as suppliers increasingly need credible local deployment experience and architectures that comply with utility operating rules.

Increasing Demand for Automated Demand Response and Peak Load Management

Automated demand response is becoming increasingly relevant in the China AI-Powered Energy Management Software Market, as power flexibility is now seen as an operational need rather than a pilot concept. By the end of 2025, China had 470 registered virtual power plant projects with a tested maximum adjustable capacity of 16.85 GW, indicating that load management is moving into broader commercial use.[3]Staff Reporter, “First ‘Computing-Follows-Power’ Deal in Guangdong, VPPs Enter Super Track,” 21st Century Economic Herald, 21jingji.com Guangdong pushed that trend further in May 2026 when three large telecom data centers were brought into the provincial electricity spot market through virtual power plant mechanisms. The national action plan also recognized virtual power plants and forecasting applications, which support continued demand for software that automates dispatch, optimizes loads, and enables price-responsive participation. As this part of the market develops, software aimed at data-center operators and other flexible loads is likely to become a more visible part of the China AI-Powered Energy Management Software Market.

Expansion of ESG Reporting and Carbon Accounting Workflows

Carbon accounting is becoming a more practical software use case in the China AI-Powered Energy Management Software Market as disclosure and reporting tasks move deeper into day-to-day operations. In April 2026, the Shanghai Advanced Research Institute of the Chinese Academy of Sciences released the ScienceOne-Yuheng Carbon Accounting Large Model, described as the first panoramic AI-based carbon-emission accounting system covering production, consumption, and natural sources.[4]Shanghai Advanced Research Institute, “ScienceOne-Yuheng Carbon Accounting Large Model Version 1.0 Released,” Chinese Academy of Sciences, english.sari.cas.cn That matters because it reduces the manual effort required to compile inventories and provides enterprises with a more direct path to connect energy data to carbon reporting. The 2026 national action plan also strengthened the broader link between AI capability building and energy management scenarios, which supports the use of such tools in structured enterprise programs. The result is that the China AI-Powered Energy Management Software Market is benefiting from both energy optimization demand and the need to document emissions performance with greater consistency and speed.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity with Legacy OT And IT Systems | -3.5% | National, most acute in legacy industrial corridors of northeastern China, Shandong, and Shanxi | Short term (≤ 2 years) |

| Data Quality, Interoperability, and Sensor Fragmentation Issues | -2.8% | National, particularly pronounced in tier-2 and tier-3 city industrial parks and secondary grid networks | Medium term (2-4 years) |

| Cybersecurity and Data Sovereignty Concerns For Critical Energy Assets | -2.0% | National, with a heightened compliance burden for foreign-origin platforms targeting utilities and grid operators | Medium term (2-4 years) |

| Payback Uncertainty in Small and Mid-Sized Sites with Limited Load Density | -1.2% | National, concentrated in western provinces and lower-tier commercial real estate | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity with Legacy OT and IT Systems

Legacy control environments remain one of the clearest constraints on the China AI-Powered Energy Management Software Market, as AI tools depend on stable, structured operational data. A 2025 peer-reviewed survey on IT and OT integration found that industrial digitalization depends on five linked domains: communication, IT-driven OT support, human centricity, security, and advanced industrial applications, and each one needs dedicated engineering effort. That helps explain why many projects still move slowly when sites rely on old PLCs, siloed supervisory systems, and custom interfaces built over many years. The issue is not only technical cost, because long integration cycles also delay the point at which buyers can see measurable savings or compliance gains. In the China AI-Powered Energy Management Software Market, vendors that simplify data capture and system integration are likely to convert more opportunities than those that depend on full-site modernization before value can be demonstrated.

Data Quality, Interoperability, and Sensor Fragmentation Issues

Data fragmentation remains a practical restraint for the China AI-Powered Energy Management Software Market because software quality depends on the quality and consistency of the signals it receives. The same 2025 ScienceDirect survey showed that communication and security layers are closely linked to advanced industrial applications, suggesting that poor interoperability can slow or weaken higher-value AI functions. In real-world operating environments, multi-vendor devices, incompatible protocols, and uneven sensor coverage can stretch deployment timelines and increase post-launch maintenance work. This challenge is especially relevant when enterprises want to scale from a successful pilot to wider site networks that do not share the same equipment or data structure. As a result, the China AI-Powered Energy Management Software Market still favors platforms and service teams that can normalize data across mixed environments rather than relying on uniform infrastructure that many sites do not yet have.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Led Revenue While Services Extended Growth

Software accounted for 68.11% of revenue in 2025, making it the largest component of the China AI-Powered Energy Management Software Market. This lead reflects the central role of platform licenses, software subscriptions, analytics modules, and control applications in enterprise deployments. Large utility contracts and multi-site industrial rollouts also tend to concentrate spending in core platforms first, since buyers usually need a system of record before they add advisory or optimization layers. The China AI-Powered Energy Management Software Market, therefore, continued to lean on software as the basis for value creation, especially when monitoring, forecasting, and operational control needed to be integrated across multiple assets.

Services are projected to expand at a 21.22% CAGR from 2026 to 2031, which makes them the fastest-growing component over the forecast period. This rise shows that buyers are not stopping at software purchase, because many deployments require model tuning, implementation support, carbon accounting workflows, and ongoing optimization to produce usable results. The March 2026 implementation plan for energy-saving equipment called for the development of large-scale AI-based energy-saving and carbon-reducing models and for promoting intelligent device management services, which directly support a broader software adoption service layer. The shift is important because it gives vendors more room to grow recurring revenue from delivery and support, not just from initial software sales. It also explains why the China AI-Powered Energy Management Software Market is becoming more dependent on execution capability and local service depth, rather than on product features alone.

By Deployment Mode: Cloud-Based Scale Supported Hybrid Growth

Cloud-based deployment held 58.16% of the China AI-Powered Energy Management Software Market share in 2025, making it the largest deployment mode. This position reflected the rapid expansion of domestic cloud infrastructure and the appeal of centralized access, faster updates, and wider data aggregation across distributed operations. The market benefited from this setup because many enterprises wanted to connect monitoring, analytics, and reporting without building fully separate software stacks at every site. Cloud deployment also suited newer use cases in commercial buildings and lighter industrial environments where buyers favored flexibility and lower upfront infrastructure needs.

Hybrid deployment is projected to expand at a 21.34% CAGR from 2026 to 2031, which makes it the fastest-growing architecture in the market. This pattern aligns with the stricter treatment of energy and operational data, especially for utilities and critical infrastructure operators that must keep sensitive information within approved jurisdictions. The December 2025 measures for data security management in the energy sector, effective July 1, 2026, strengthened the practical case for keeping some data and workloads local while still using cloud resources for aggregation and reporting. The China AI-Powered Energy Management Software Market is therefore shifting toward deployment models that let enterprises keep OT-sensitive functions close to the asset while still using broader analytics and benchmarking across sites. That balance is likely to remain important as AI use cases expand across utilities, manufacturing, and data center environments.

By Application: Demand Optimization Anchored Revenue While Renewable Forecasting Accelerated

Energy consumption and demand optimization accounted for 24.19% of application revenue in 2025, making it the leading use case in the China AI-Powered Energy Management Software Market. This result was logical because buyers often start with applications that can directly affect peak demand, load balancing, and energy cost control. These tools are also easier to justify internally because they connect software investment to operating savings and process visibility in a short time frame. The market kept returning to this application area because it addresses both commercial and industrial priorities with a clearer path to action than many advanced use cases.

Renewable energy forecasting and integration is projected to grow at a 21.46% CAGR from 2026 to 2031, making it the fastest-growing application segment. The market is moving in that direction because variable renewable energy output creates a stronger need for predictive tools to improve dispatch planning and grid stability. Huairou Laboratory reported that its native power system large-scale model increased renewable energy integration at the Dali power grid by an expected 120 million kWh annually and reduced CO2 emissions by 60,000 metric tons annually. The May 2026 national action plan also included new energy forecasting among the priority AI scenarios, reinforcing the role of predictive applications in future system management. This is one of the clearest areas where the China AI-Powered Energy Management Software Market is moving from site-level efficiency toward system-level coordination across power assets.

By End User: Utilities Held The Lead While Industrial Facilities Advanced Fastest

Utilities accounted for 33.13% of end-user revenue in 2025, making them the largest segment in the China AI-Powered Energy Management Software Market. Their lead came from large-scale demand for grid optimization tools, distributed energy resource management, fault detection, and orchestration software that can work across wide infrastructure networks. Utilities also tend to have larger budgets and more direct policy pressure to modernize operations, which strengthens their purchasing role in this market. As a result, the China AI-Powered Energy Management Software Market remains closely tied to utility investment cycles and to the pace at which grid operators widen AI use beyond pilot programs.

Industrial facilities are projected to expand at a 21.57% CAGR from 2026 to 2031, making them the fastest-growing end-user group. This growth reflects the practical need to improve energy performance at plants that face both efficiency targets and more demanding reporting requirements. A 2026 Scientific Reports article showed how BIM and Industrial IoT-based systems can support building-level energy prediction and control, underscoring the broader value of connected energy data in operational settings. At the same time, the policy push for AI-enabled efficiency improvements in industrial sectors is giving plant operators stronger reasons to adopt software that links monitoring, control, and carbon management in a single workflow. That combination is likely to keep industrial sites among the most active growth engines in the China AI-Powered Energy Management Software Market.

Geography Analysis

Eastern China remained the largest concentration point in the China AI-Powered Energy Management Software Market because it combines dense industrial activity, more developed electricity trading conditions, and a large base of export-facing manufacturers. Guangdong, Jiangsu, Zhejiang, and Shanghai are especially important because they bring together advanced digital infrastructure with strong pressure to improve energy efficiency and emissions reporting. Guangdong also became an early proof point for demand response innovation when three large telecom data centers entered the provincial electricity spot market through virtual power plant mechanisms in May 2026. That development matters because it widened the range of flexible energy users beyond traditional factories and commercial buildings. The market is therefore especially active in the eastern region, where software can be tied to real-time pricing, dispatch participation, and carbon-linked enterprise reporting.

Northern China presented a different but equally important profile. Beijing supported demand by concentrating regulators, enterprise headquarters, and organizations that need stronger ESG and carbon accounting workflows. The wider northern belt also includes major industrial loads and fast-growing AI computing infrastructure, which increases the need for forecasting and load management tools. Inner Mongolia, especially Ulanqab, emerged as a critical data-center cluster under the Eastern Data, Western Computing strategy, with 67% green power supply and low latency to Beijing. In this setting, the market serves not only utilities and factories but also data infrastructure operators whose power profiles are more variable and time-sensitive.

Western and central China are becoming the fastest-moving sub-geographies for forecasting, renewable integration, and grid-linked software. Provinces such as Sichuan, Yunnan, Xinjiang, and Ningxia matter because they anchor large renewable generation bases and support broader computing and transmission strategies. The May 2026 action plan specifically highlighted new energy forecasting, smart grids, and virtual power plants, which support stronger software demand in regions where renewable balancing is central to operations. Huawei and State Grid Fujian Integrated Energy Service also signed a framework cooperation agreement in April 2026 to develop intelligent solutions across green energy, energy efficiency, and carbon reduction, demonstrating how domestic technology partnerships are expanding regional reach beyond the coastal core.

Competitive Landscape

The China AI-Powered Energy Management Software Market had a moderately fragmented top tier, but competition was still broad enough to prevent any single vendor group from dominating the full landscape. Global automation companies such as Siemens AG, Schneider Electric SE, ABB Ltd., and Honeywell International remained active in utility and industrial accounts, while IBM, Microsoft, and Oracle also competed through cloud and enterprise software routes. This meant that buyers often evaluated vendors on deployment fit, local delivery support, and compliance readiness as much as on software capability. The market also favored companies that could show local proof points, especially in regulated energy settings where a reference project carries more weight than a generic platform claim. As a result, competition increasingly centered on who could connect software performance with Chinese operating conditions and governance requirements.

Strategic moves in 2025 and 2026 showed that vendors were strengthening their portfolios rather than relying solely on existing products. Johnson Controls completed the acquisition of Nantum AI in April 2026 to deepen the AI-driven energy optimization capabilities of its OpenBlue platform. TCS and Siemens Energy AG also signed two memoranda of understanding in April 2026 covering AI and digital collaboration, AI infrastructure for data centers, and integration with grid technology platforms. Honeywell and TCS announced a separate strategic partnership in February 2026 to advance autonomous operations in buildings and industries through AI, reinforcing the importance of OT-to-IT integration for competitive positioning. These moves suggest that the market rewards firms that can combine software, data integration, and domain execution in a single offer. They also show that partnerships and acquisitions are becoming a practical way to quickly close capability gaps.

Domestic players are becoming more influential because they are better placed to align with local data rules, grid conditions, and language-specific model training. Huawei’s virtual power plant platform service highlighted a domestic approach that is closely tied to adjustable resource aggregation and multi-provincial grid participation. ABB’s iCE600 Smart Energy and Carbon Management Platform received formal domestic recognition in 2025, which showed that foreign-origin platforms can still succeed when localization is treated as a core strategy rather than a minor product adaptation. Oracle also expanded its utilities network management capabilities in March 2025 with new DER orchestration modules aimed at demand response and load shaping. Taken together, these moves point to a market where local relevance, deployment credibility, and ecosystem fit still matter more than scale alone.

China AI-Powered Energy Management Software Industry Leaders

Schneider Electric SE

Siemens AG

Honeywell International Inc.

Johnson Controls International plc

ABB Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: China's NDRC, NEA, MIIT, and National Data Bureau jointly issued the "Action Plan on Promoting Two-Way Empowerment of AI and Energy," releasing 51 high-value AI and energy application scenarios across eight categories, including smart grids, virtual power plants, and new energy forecasting, with binding 2027 and 2030 national capability targets.

- April 2026: Johnson Controls completed the acquisition of Nantum AI, a New York-based company specializing in proprietary AI algorithms for HVAC energy optimization, to deepen the AI-driven energy optimization capabilities of its OpenBlue digital platform.

- April 2026: Shanghai Advanced Research Institute of the Chinese Academy of Sciences released the "ScienceOne-Yuheng Carbon Accounting Large Model," the world's first panoramic AI carbon emission accounting system covering production, consumption, and natural sources, enabling automated national greenhouse gas inventory compilation and corporate carbon footprint tracking.

- April 2026: Siemens Energy AG and TCS signed 2 memoranda of understanding covering AI and digital technology collaboration, AI infrastructure development for data centers, and integration of Siemens Energy's grid technology platforms with TCS's IT and operations consulting capabilities.

China AI-Powered Energy Management Software Market Report Scope

The China AI-Powered Energy Management Software market refers to platforms and services that leverage artificial intelligence to optimize energy consumption, improve asset performance, and enable smarter grid and distributed energy resource (DER) management. These solutions include predictive maintenance, renewable energy forecasting, demand-side optimization, and market intelligence for energy trading and pricing.

The China AI-Powered Energy Management Software market report is segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Smart Grid and Distributed Energy Resource (DER) Management, Renewable Energy Forecasting and Integration, and Energy Trading, Pricing and Market Intelligence), and End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential Buildings). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings |

Key Questions Answered in the Report

What is the 2026 value of the China AI-Powered Energy Management Software Market?

The China AI-Powered Energy Management Software Market stands at USD 386.5 million in 2026 and is forecast to reach USD 985.3 million by 2031 at a 20.58% CAGR.

What is driving adoption of AI-powered energy management software in China?

The strongest demand drivers are policy-led AI deployment in energy, rising need for real-time optimization, growth in virtual power plants, and wider carbon accounting workflows.

Which component leads revenue and which one is growing fastest?

Software held the largest share at 68.11% in 2025, while services are projected to grow fastest at a 21.22% CAGR through 2031.

Why is hybrid deployment gaining traction in China?

Hybrid deployment is growing because utilities and critical infrastructure operators need local control over sensitive energy data while still using cloud tools for aggregation and reporting.

Which application area is expanding the fastest through 2031?

Renewable energy forecasting and integration is the fastest-growing application, with a projected CAGR of 21.46% from 2026 to 2031.

Which end-user group offers the strongest growth opportunity?

Industrial facilities are expected to post the fastest growth at a 21.57% CAGR, supported by stronger efficiency targets and broader demand for integrated energy and carbon workflows.

Page last updated on: