Canada AI-powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

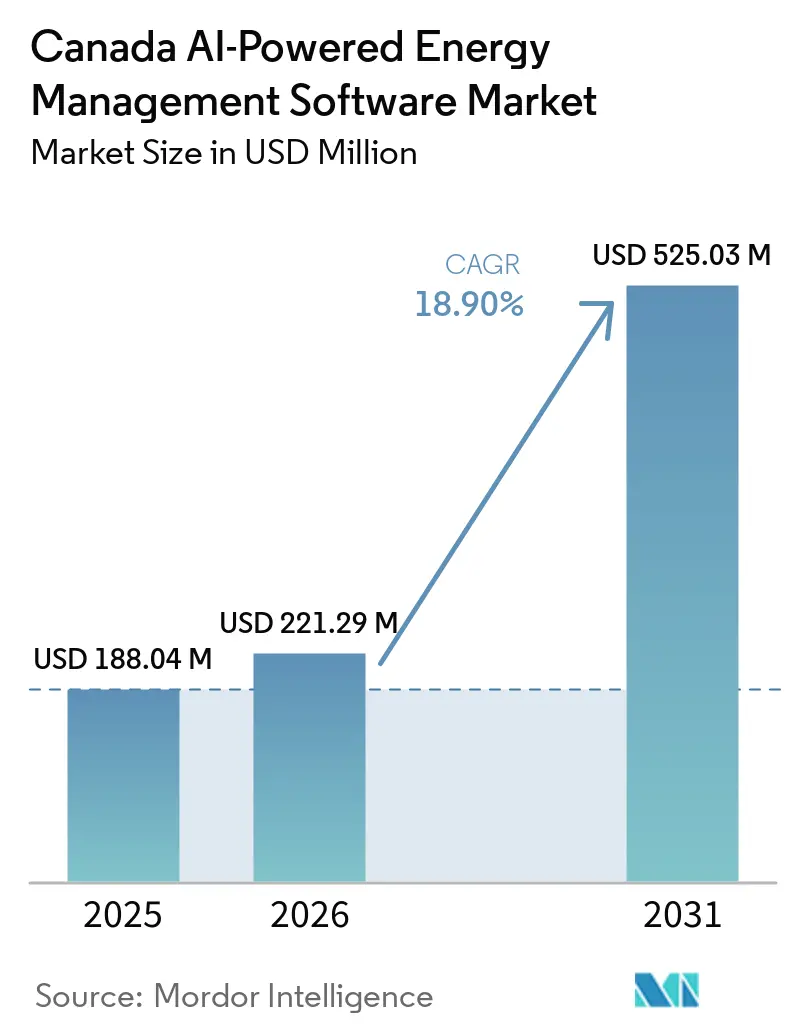

| Base Year Market Size (2025) | USD 188.04 Million |

| Market Size (2026) | USD 221.29 Million |

| Market Size (2031) | USD 525.03 Million |

| Growth Rate (2026 - 2031) | 18.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada AI-powered Energy Management Software Market Analysis by Mordor Intelligence

The Canada AI-powered Energy Management Software Market size is projected to be USD 188.04 million in 2025, USD 221.29 million in 2026, and reach USD 525.03 million by 2031, growing at a CAGR of 18.90% from 2026 to 2031. Demand is rising as electricity price volatility, federal decarbonization rules, and the limits of static building management systems are pushing buyers toward software that can respond in real time. The 2025 National Energy Code for Buildings has added a clearer greenhouse gas framework alongside energy efficiency tiers, which is making software-led control and monitoring more relevant across commercial and institutional properties. The Canada AI-powered Energy Management Software Market is also moving beyond cost control, because utilities and large building operators are using AI tools to support peak management, renewable integration, and distributed energy coordination that can create direct economic value. Competition is strengthening as global building automation companies use their installed base and service contracts to defend accounts, while software-led specialists compete on faster optimization and more autonomous control. Adoption is still likely to remain strongest among utilities, large real estate portfolios, and data-intensive facilities, because older control systems and workforce shortages continue to slow smaller site owners.

Key Report Takeaways

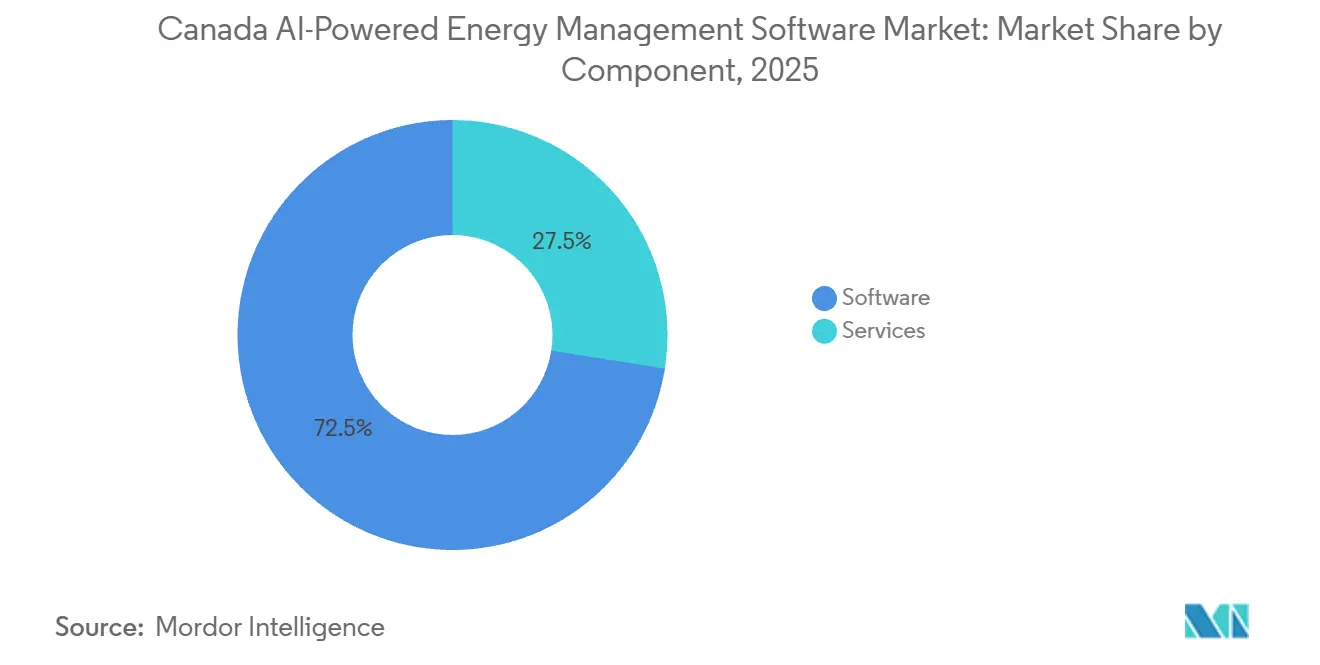

- By component, software held 72.50% of the Canada AI-powered Energy Management Software Market share in 2025, while services is projected to expand at a 21.90% CAGR through 2031.

- By deployment mode, cloud-based architecture accounted for 55.00% of the Canada AI-powered Energy Management Software Market size in 2025 and is also projected to record the fastest CAGR at 22.10% through 2031.

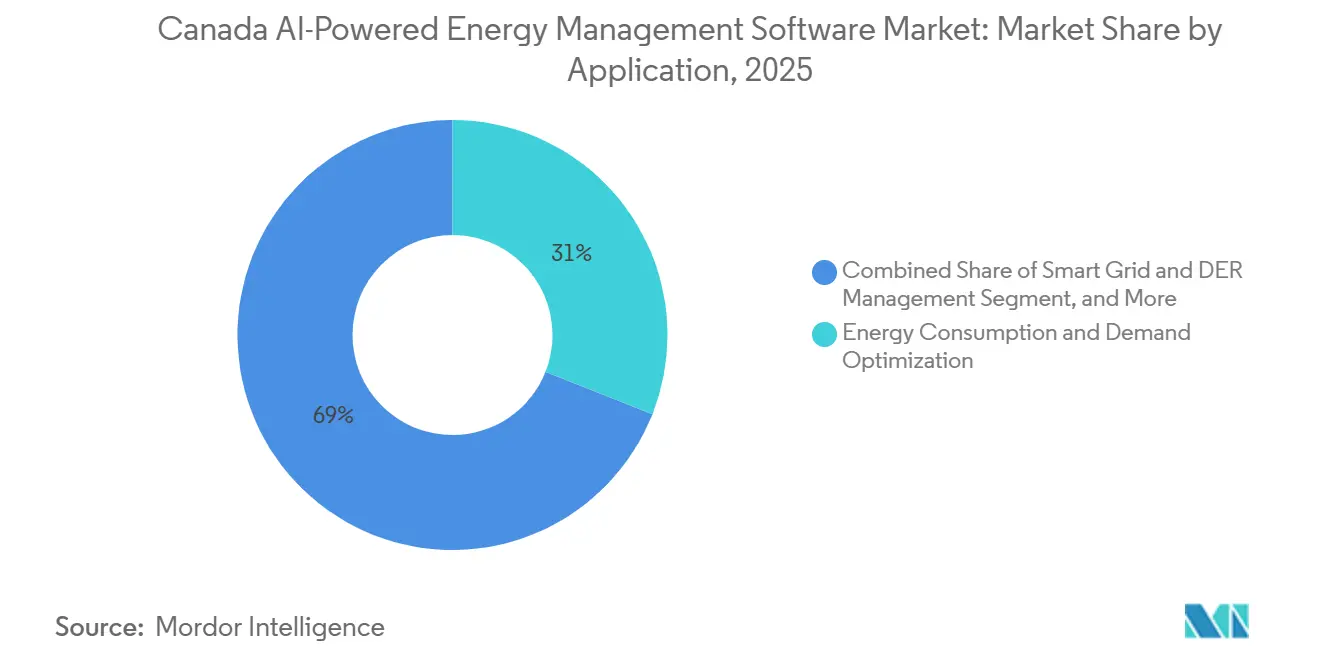

- By application, energy consumption and demand optimization accounted for a 31.00% share in 2025, while renewable energy forecasting and integration is projected to expand at a 23.50% CAGR through 2031.

- By end user, utilities held a 38.00% share in 2025, while residential buildings is projected to record the highest CAGR at 22.80% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada AI-powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift From Static EMS to AI-Driven Prescriptive Control | +4.2% | National, concentrated in major urban centers - Toronto, Vancouver, Montreal, Calgary | Short term (≤ 2 years) |

| Canada Net-Zero Compliance Pressure on Buildings and Industry | +3.8% | National, with early gains in Ontario, British Columbia, Quebec | Medium term (2-4 years) |

| Rising Electricity Price Volatility in Commercial Portfolios | +3.5% | Ontario, Alberta, with spillover to Atlantic provinces | Short term (≤ 2 years) |

| Utility Demand Response and Peak-Shaving Monetization | +3.1% | Ontario, Quebec, British Columbia, with growing relevance in Alberta | Short term (≤ 2 years) |

| Underused Building Data Lakes and Sensorization Unlock AI Upside | +2.3% | National, highest density in Toronto, Vancouver, Montreal | Medium term (2-4 years) |

| Growth of Managed Energy Services for Multi-Site Enterprises | +2.0% | National, with concentration in multi-site retail and commercial clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift From Static EMS to AI-Driven Prescriptive Control

Traditional energy management systems rely on fixed schedules and threshold-based responses, which limit their ability to react to rapid price swings or forecast load conditions in advance. AI-driven prescriptive control changes that model by using occupancy patterns, weather inputs, and operating data to adjust HVAC, lighting, and storage decisions with much greater precision. This makes the Canada AI-powered Energy Management Software Market more relevant for operators that need sub-hourly control rather than periodic manual tuning. The shift also reduces dependence on constant human intervention, which matters in a labor market where AI-ready talent is harder to attract inside the energy sector.[1]Electricity Canada, “The Dao of Artificial Intelligence in the Canadian Electricity Industry,” Electricity Canada, electricity.ca As more sites move from monitoring to autonomous optimization, procurement is increasingly focused on software that can make operational decisions rather than just report conditions.

Canada Net-Zero Compliance Pressure on Buildings and Industry

Canada’s building decarbonization path is creating a direct compliance case for advanced control software across new construction and retrofit activity. The 2025 National Energy Code for Buildings introduced greenhouse gas emissions requirements alongside energy efficiency tiering, which raised the performance threshold that owners and developers now have to meet. Federal support has reinforced this shift through the Canada Green Buildings Strategy, which committed nearly USD 1 billion in new funding for building decarbonization measures and included support for benchmarking and innovation programs. In the Canada AI-powered Energy Management Software Market, that pressure is making continuous monitoring and control more important for institutional and commercial portfolios that have to manage both energy use and emissions performance. Compliance is also becoming part of asset management practice, because certification and disclosure expectations are pushing owners toward platforms that can document performance continuously rather than through periodic audits.

Rising Electricity Price Volatility in Commercial Portfolios

Commercial operators are facing a more difficult power cost environment, especially when they have multiple sites and a limited ability to shift load manually. Alberta’s wholesale pool price reached USD 948.63/MWh during a peak event on March 26, 2026, which showed how quickly supply conditions can move against unhedged buyers.[2]Alberta Market Surveillance Administrator, “Wholesale Market Report, Q1 2026,” Alberta MSA, albertamsa.ca In the Canada AI-powered Energy Management Software Market, this kind of volatility supports demand for software that can manage curtailment, load shifting, and peak reduction in real time. The value is even stronger at the portfolio level, because a coordinated platform can balance decisions across many buildings instead of optimizing a single site in isolation. That is why adoption is moving ahead even before regulation forces it, particularly where exposure to market-based electricity pricing makes the savings case easier to prove.

Utility Demand Response and Peak-Shaving Monetization

Provincial systems are increasingly treating flexible demand as a dispatchable resource, which changes the role of AI software from a conservation tool to a grid participation layer. Natural Resources Canada invested USD 6 million in Hydro Ottawa’s Ottawa Distributed Energy Resource Accelerator program in December 2025, supporting AI-enhanced predictive analytics that turn smart thermostats, EV chargers, and home batteries into active grid resources. The Canadian Climate Institute also reported that Hydro-Québec’s Hilo service engaged more than 400,000 households and generated 2,330 MW of combined flexible capacity during the 2024-2025 winter season. This gives the Canada AI-powered Energy Management Software Market a stronger revenue logic, because software can help aggregate customer-side assets into grid-facing capacity. As that model expands, building portfolios are being treated less like fixed loads and more like controllable energy assets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy OT and BMS Integration Complexity | -3.2% | National, most acute in industrial Alberta and Ontario manufacturing belts | Long term (≥ 4 years) |

| Cybersecurity and Data Sovereignty Concerns | -2.5% | National, particularly in regulated utilities and federal buildings | Medium term (2-4 years) |

| Shortage Of AI-Ready Energy Operations Talent | -1.8% | National, especially outside Toronto, Vancouver, Montreal tech hubs | Medium term (2-4 years) |

| ROI Uncertainty for Small and Mid-Sized Site Owners | -1.4% | National, heaviest in SME-dense Prairie provinces and Atlantic Canada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Legacy OT And BMS Integration Complexity

A large part of Canada’s commercial and industrial stock still runs on older operational technology and building management systems that were not designed for high-frequency, two-way AI integration. That creates a practical limit for the Canada AI-powered Energy Management Software Market, because many sites cannot deliver the clean and continuous data streams that AI tools need for reliable optimization. Electricity Canada identified legacy systems, data silos, incompatible infrastructure, and skills gaps as major barriers that reduce the effectiveness of AI deployments even after organizations commit to them. The problem is not only integration cost, but also operating risk, because incomplete or noisy data can weaken optimization outcomes and make facility managers less willing to scale deployments. Since OT replacement cycles are long, the market is likely to stay skewed toward newer buildings, recently retrofitted assets, and customers that can negotiate portfolio-wide contracts.

Cybersecurity And Data Sovereignty Concerns

Connecting energy infrastructure to cloud-based AI systems adds exposure that many utilities, public institutions, and regulated operators have historically tried to avoid. The Canadian Center for Cyber Security assessed in its 2025-2026 threat outlook that state-sponsored actors would likely attempt to disrupt vulnerable internet-connected operational technology inside Canadian critical infrastructure. The Canadian Cyber Threat Exchange also found that 75% of energy companies identified supply chain risks as a top concern, with older OT systems making remediation more difficult. In the Canada AI-powered Energy Management Software Market, this slows procurement because buyers must review hosting models, vendor access controls, and data handling practices before rollout. Data sovereignty adds another layer for crown corporations and municipalities, because server location and provider choice can narrow the list of acceptable platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Leads While Services Gain Depth

Software held 72.50% of the market in 2025, making it the core revenue base of the Canada AI-powered Energy Management Software Market. Enterprise SaaS platforms and utility-grade analytics suites drove most early deployments because buyers first needed visibility, forecasting, and centralized control. Services is projected to expand at a 21.90% CAGR from 2026 to 2031, which shows that many customers now need help with configuration, integration, model retraining, and continuous optimization. This creates a layered model in which software remains the base product while service intensity rises around it.

The services shift is strongest among multi-site operators without large in-house AI or controls teams. Electricity Canada reported that entry-level salaries in the technology sector run 30% higher than comparable roles in the energy sector, which helps explain why many operators prefer outsourced optimization support. Canada Infrastructure Bank’s support for the IonicBlue and Johnson Controls retrofit model also reflects demand for bundled performance-based offerings that combine platform delivery with execution support.[3]Canada Infrastructure Bank, “IonicBlue and Johnson Controls Retrofits,” Canada Infrastructure Bank, cib-bic.ca Over time, this should keep software in the lead while allowing services to capture a larger role in how the Canada AI-powered Energy Management Software Market is delivered across commercial and institutional portfolios.

By Deployment Mode: Cloud-Based Architecture Sets the Pace

Cloud-based deployment accounted for 55.00% of the market in 2025, and it is also projected to post the fastest growth at a 22.10% CAGR through 2031. That dual position shows that buyers see faster scalability, lower infrastructure burden, and easier multi-site coordination in cloud-led architectures. On-premises systems remain relevant for operators with strict internal controls, while hybrid models are becoming more common where edge responsiveness and centralized analytics both matter. In this segment, cloud-led design is reshaping the baseline for the Canada AI-powered Energy Management Software Market.

Hybrid demand is rising because many organizations want sensitive operating data to remain close to the asset while still using centralized AI tools for forecasting and optimization. Cyber risk is a major reason, since internet-connected operational environments are now more exposed to targeted disruption attempts inside critical infrastructure. Vendor selection is also affected by data handling concerns, because energy companies continue to view supply chain and platform security as major barriers to wider rollout. As a result, cloud adoption in the Canada AI-powered Energy Management Software Market is advancing with a stronger preference for domestic hosting options, clear access controls, and deployment flexibility.

By Application: Demand Optimization Leads While Renewable Forecasting Expands Fast

Energy consumption and demand optimization accounted for 31.00% of the Canada AI-powered Energy Management Software Market size in 2025, which kept it as the largest application area. That lead reflects the immediate value of cutting peak demand charges, improving load scheduling, and aligning operations with evolving utility incentives. Renewable energy forecasting and integration is projected to grow at a 23.50% CAGR through 2031, showing that grid modernization is widening the role of AI beyond building efficiency alone. The application mix, therefore, combines established savings use cases with newer grid-facing requirements.

Asset performance and predictive maintenance remain important in industrial and utility settings where outages carry a high operating cost. C3.ai expanded its multi-year collaboration with Shell in June 2026 to scale AI-based reliability tools across global asset operations, which reinforces the role of predictive analytics in capital-intensive energy environments.[4]C3.ai, “C3 AI and Shell Expand Collaboration, Scaling Reliability AI Deployment Across Global Asset Operations,” C3.ai, c3.ai Electricity Canada also noted that Natural Resources Canada’s AI funding priorities included tools such as AI-managed dynamic line rating for more efficient grid management. In Alberta, the Q1 2026 price spike to USD 948.63/MWh further supports interest in energy trading and market intelligence tools inside the Canada AI-powered Energy Management Software Market.

By End User: Utilities Hold the Lead While Residential Buildings Accelerate

Utilities held 38.00% of the Canada AI-powered Energy Management Software Market share in 2025, which made them the largest end-user group. Their lead comes from grid stability needs, renewable integration requirements, and the need to manage peak demand across large service territories. Residential buildings are projected to expand at a 22.80% CAGR from 2026 to 2031, making them the fastest-growing end-user segment. This gap between current size and future growth shows how utility programs are widening the market toward smaller distributed assets.

Commercial and industrial users still represent a large adoption base because compliance, power cost management, and equipment reliability remain urgent across those sites. The Canadian Climate Institute reported that Hydro-Québec’s Hilo program delivered an average incentive payout of USD 205 per enrolled household during the 2024-2025 winter season, which supports the financial viability of residential participation. The same source showed the scale that flexible residential demand can reach when utilities treat homes as dispatchable resources rather than passive customers. That is why the Canada AI-powered Energy Management Software Market is likely to maintain a utility-led revenue base while accelerating growth through customer-side coordination models in homes.

Geography Analysis

Eastern and central Canada represent the largest concentration of demand in the Canada AI-powered Energy Management Software Market in 2026. Ontario remains the biggest demand center because it combines the country’s largest electricity market with a large commercial and industrial building base. That makes real-time load management especially relevant for property owners and large power users that face tighter operating margins. Quebec adds a different growth path, because low-cost hydro generation is being paired with flexible demand tools and customer-side participation programs. The Canadian Climate Institute reported that Hydro-Québec’s Rate Flex D tariffs delivered peak demand reductions of up to 22% during winter 2024-2025 events, which shows how pricing design can strengthen the need for intelligent energy control.

British Columbia and Alberta present different but complementary demand conditions for the Canada AI-powered Energy Management Software Market. Natural Resources Canada reported that BC Hydro’s 10-year capital investment plan committed USD 36 billion to expand, reinforce, and modernize electricity infrastructure, while its efficiency plan targeted 400 MW of demand response capacity savings by 2030. That creates a durable opening for vendors with grid-edge analytics and distributed energy coordination tools. Alberta’s fully deregulated electricity market creates a stronger direct pricing signal than other provinces. The province’s wholesale pool price hit USD 948.63/MWh during a peak event in Q1 2026, which makes automated demand control and energy procurement support especially relevant for large commercial and industrial users.

Smaller provincial markets still represent an earlier stage of deployment in the Canada AI-powered Energy Management Software Market. Nova Scotia and Manitoba are expanding through efficiency and demand response programs rather than through large existing software bases. The Canadian Climate Institute reported that EfficiencyOne delivered 172.8 GWh of electricity savings and 30.7 MW of demand savings in 2024, while Efficiency Manitoba launched new demand response pilots in 2025-2026. At the national level, Natural Resources Canada projected that electricity demand will more than double to over 1,200 TWh per year by 2050 and estimated that grid investment will exceed USD 1 trillion from 2025 to 2050, which supports long-range demand for software across generation, networks, and end-use management.

Competitive Landscape

The Canada AI-powered Energy Management Software Market is moderately concentrated, with large building automation and industrial technology companies holding an advantage through installed systems, service reach, and long-standing customer relationships. Schneider Electric, Siemens, Honeywell, IBM, Johnson Controls, and Microsoft remain visible because buyers often prefer vendors that can connect software into existing control environments. At the same time, software-led challengers such as BrainBox AI, C3.ai, Uplight, GridPoint, Verdigris, CopperTree Analytics, and BluWave-ai compete on algorithm depth, faster deployment, and use-case specialization. This keeps the Canada AI-powered Energy Management Software Market open to new entrants, even though incumbent scale still shapes procurement outcomes. The competitive pattern is therefore defined by installed-base strength on one side and AI specialization on the other.

Large companies are expanding their position through direct product investment and selective acquisitions. Johnson Controls acquired Nantum AI in April 2026 to strengthen OpenBlue with additional AI-driven HVAC optimization capability, showing how incumbents are buying specialized intellectual property to deepen software control and analytics. Honeywell launched Honeywell Connected Solutions in June 2025 as an AI-powered platform that brings building software and technologies into a single interface with remote monitoring, predictive prompts, and energy management functions. Eaton also introduced Brightlayer Energy in March 2026 for healthcare, education, and retail buildings, which shows that electrical equipment companies are moving deeper into software-led optimization. These moves are raising the competitive baseline, because buyers now expect software, controls, analytics, and service support to work together as one offer.

Software-native and Canada-linked players still have room to differentiate inside the Canada AI-powered Energy Management Software Market. BrainBox AI opened its Montreal AI Lab and Showroom in May 2026 with a permanent team of around 100 researchers and scientists focused on next-generation AI for HVAC and building optimization.[5]BrainBox AI, “Our AI Lab and Showroom Is Officially Open,” BrainBox AI, brainboxai.com C3.ai’s expanded work with Shell also reinforces the appeal of enterprise-grade predictive maintenance and reliability platforms in industrial energy use cases. Over time, interoperability, domestic deployment options, and the ability to support utility, building, and distributed asset workflows together will matter as much as core algorithm performance. That is likely to keep competition active across both conglomerates and software specialists.

Canada AI-powered Energy Management Software Industry Leaders

Bidgely Inc.

C3.ai, Inc.

GridPoint, Inc.

Uplight, Inc.

BrainBox AI Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: C3.ai and Shell signed a new multi-year agreement expanding the C3 AI Reliability deployment across Shell's global operations to introduce agentic AI-based root cause analysis and remediation, scaling from monitoring 13,000+ pieces of equipment to a fully autonomous predictive maintenance and remediation framework. This partnership, which started in 2018, demonstrates C3.ai's enterprise AI energy management credentials at a scale that directly validates its platform for large industrial energy users in Canada.

- May 2026: Trane Technologies officially opened the BrainBox AI Trane Technologies AI Lab and Showroom in Montreal, a permanent facility housing approximately 100 researchers and scientists developing next-generation AI for HVAC and building energy optimization.

- April 2026: Johnson Controls acquired Nantum AI, a New York-based company specializing in AI algorithms for HVAC energy optimization, strengthening its OpenBlue digital ecosystem with proprietary AI intellectual property. The acquisition accelerates Johnson Controls' ability to deliver AI-driven energy optimization at scale for commercial and institutional buildings across North America, including Canada

- March 2026: Eaton unveiled Brightlayer Energy, an AI-powered energy management and optimization system (EMOS) for commercial buildings in healthcare, education, and retail. The platform combines real-time data analytics, forecasting, and automated control to maximize value from electrical infrastructure and distributed energy resources while meeting local regulatory requirements.

Canada AI-powered Energy Management Software Market Report Scope

The Canada AI-powered Energy Management Software Market comprises AI-driven software solutions and related services that optimize energy production, distribution, storage, and consumption through intelligent analytics, automation, and predictive modeling. These platforms leverage machine learning, artificial intelligence, digital twins, advanced forecasting, and real-time monitoring technologies to improve energy efficiency, enhance asset utilization, facilitate renewable energy integration, and support Canada's decarbonization and net-zero objectives.

The Canada AI-Powered Energy Management Software Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Smart Grid and Distributed Energy Resource (DER) Management, Renewable Energy Forecasting and Integration, and Energy Trading, Pricing and Market Intelligence), and End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential Buildings). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings |

Key Questions Answered in the Report

What is the size of the Canada AI-powered Energy Management Software Market?

The Canada AI-powered Energy Management Software Market was valued at USD 188.04 million in 2025, stands at USD 221.29 million in 2026, and is forecast to reach USD 525.03 million by 2031 at a CAGR of 18.90%.

Which component leads demand in Canada?

Software led with a 72.50% share in 2025, while services is projected to grow faster at a 21.90% CAGR through 2031.

Why are utilities the largest buyers of AI energy software in Canada?

Utilities held 38.00% share in 2025 because they need stronger grid stability, renewable integration, and peak demand management across large service areas.

Which application is growing the fastest?

Renewable energy forecasting and integration is projected to post the fastest growth at a 23.50% CAGR through 2031, reflecting wider grid modernization needs.

Why is cloud deployment gaining ground?

Cloud-based architecture held 55.00% share in 2025 and is also the fastest-growing deployment model at 22.10% CAGR because it supports multi-site scale and centralized analytics more easily.

What is the biggest barrier to wider adoption across smaller sites?

Legacy control systems, cybersecurity reviews, and limited AI-ready talent continue to slow deployment, especially where buyers cannot justify complex retrofits or dedicate internal operating teams.

Page last updated on: