North America AI-Powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

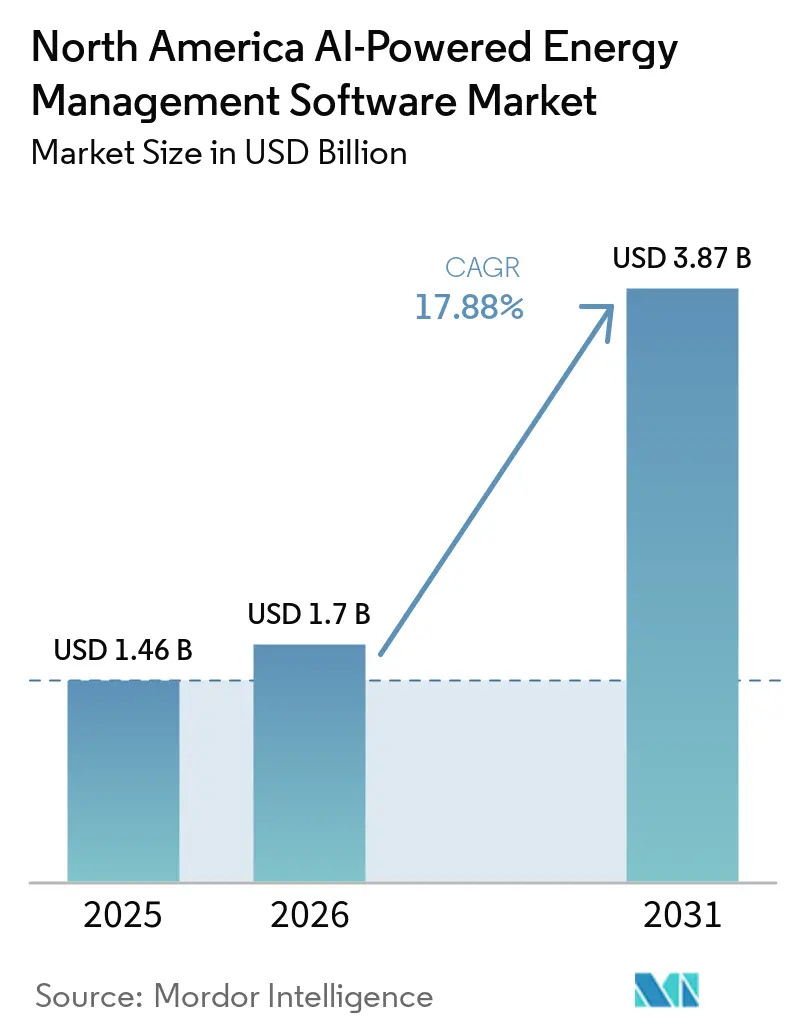

| Base Year Market Size (2025) | USD 1.46 Billion |

| Market Size (2026) | USD 1.7 Billion |

| Market Size (2031) | USD 3.87 Billion |

| Growth Rate (2026 - 2031) | 17.88% CAGR |

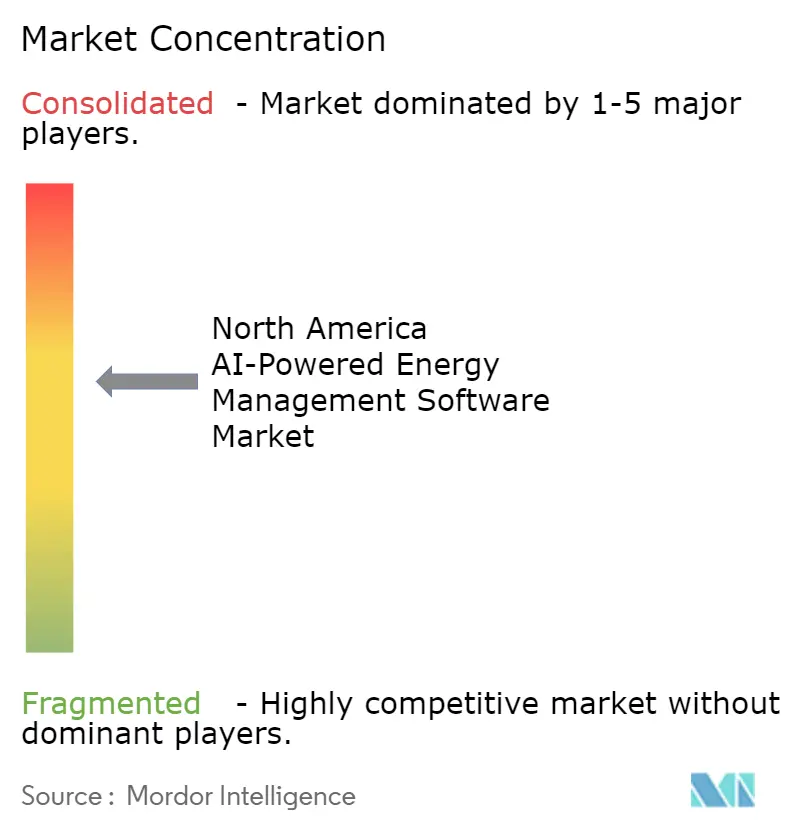

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America AI-Powered Energy Management Software Market Analysis by Mordor Intelligence

The North America AI-Powered Energy Management Software Market size is projected to expand from USD 1.46 billion in 2025 and USD 1.70 billion in 2026 to USD 3.87 billion by 2031, registering a CAGR of 17.88% between 2026 and 2031. Growth is being supported by rising data center electricity demand, tighter enterprise decarbonization accountability, and a power system that is becoming harder to manage with older control tools. These conditions are pushing software budgets closer to operating and emissions targets, which makes spending decisions more durable than standard facility upgrade cycles. Vendors are also expanding their offerings through acquisitions, orchestration tools, and bundled service models to remain embedded after the initial software deployment. Cybersecurity checks and legacy system integration are still slowing some projects, especially in regulated and older building environments. Even with those barriers, the opportunity remains strong because utilities, campuses, data-heavy facilities, and new industrial sites need faster energy decisions i more connected power environments.

Key Report Takeaways

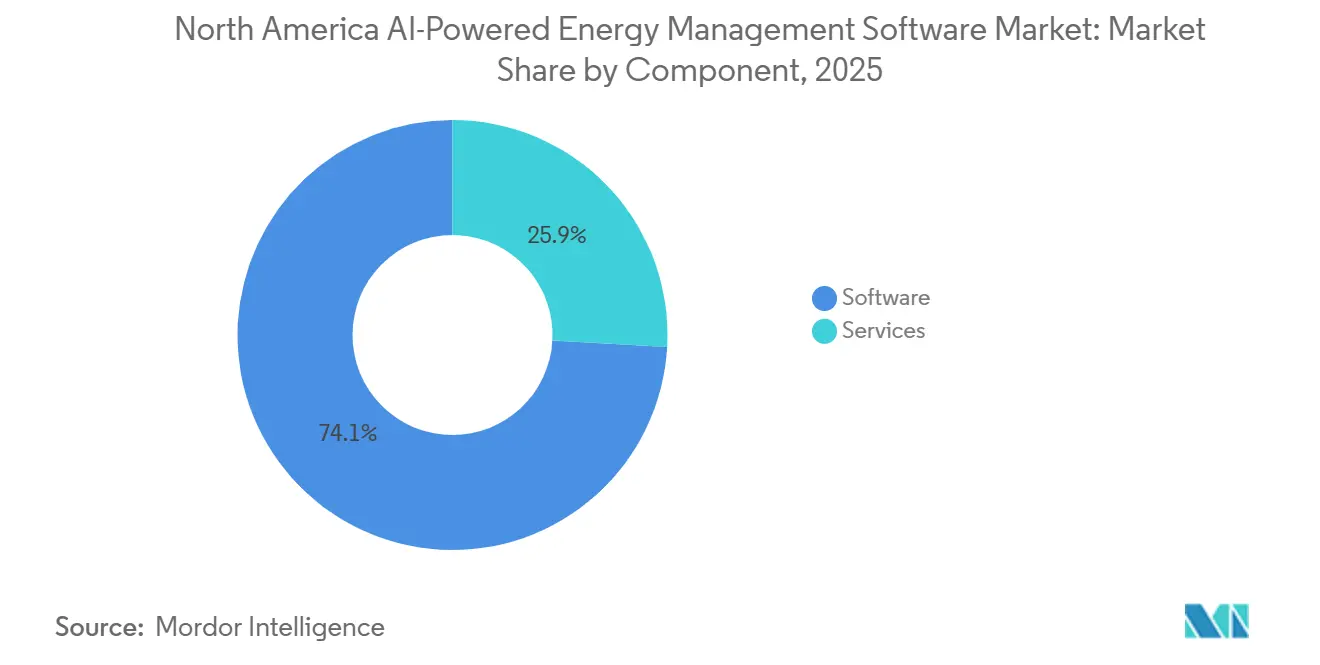

- By component, software held 74.12% of the North America AI-Powered Energy Management Software Market in 2025, while services are projected to expand at a 17.93% CAGR through 2031.

- By deployment mode, cloud-based deployment accounted for 63.14% of the market in 2025, while hybrid deployment is expected to grow at a 18.02% CAGR through 2031.

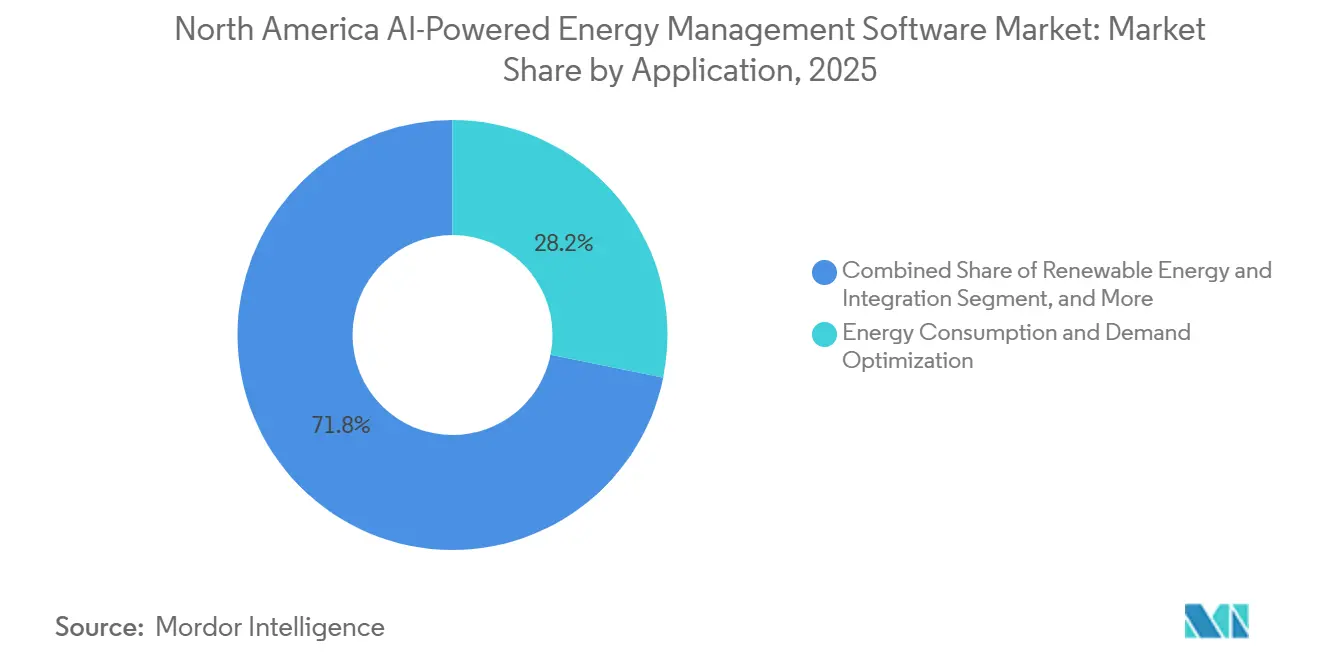

- By application, Energy Consumption and Demand Optimization accounted for 28.17% share in 2025, while Renewable Energy Forecasting and Integration is projected to advance at an 18.21% CAGR through 2031.

- By end user, utilities held 29.12% share in 2025, while industrial facilities are expected to expand at an 18.34% CAGR through 2031.

- By geography, the United States accounted for 66.18% share in 2025, while Mexico is projected to grow at an 18.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America AI-Powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Smart Meter and IoT Sensor Penetration Across Commercial Sites | +3.5% | North America, concentrated in United States and Canada | Short term (≤ 2 years) |

| Rising Utility Tariffs and Demand Charges for Peak Load Customers | +2.8% | United States, particularly California, Texas, and the Northeast | Short term (≤ 2 years) |

| Portfolio Decarbonization Commitments From Enterprises and Campuses | +2.2% | North America, with large corporates in the United States and Canada leading adoption | Medium term (2-4 years) |

| Integration With Distributed Energy Resources and Battery Storage | +1.8% | United States, especially ERCOT, CAISO, and MISO, and Canada, especially Ontario | Medium term (2-4 years) |

| AI-Enabled Fault Detection Reducing Energy Waste From Hidden Equipment Drift | +1.4% | North America, with follow-on relevance in similar advanced markets | Medium term (2-4 years) |

| New Utility Incentives for Automated Demand Response Participation | +1.0% | United States and Canada, with state and province specific programs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Smart Meter and IoT Sensor Penetration Across Commercial Sites

Rapid meter and sensor adoption is expanding the database that building and facility software can use to learn normal operating patterns. In the North America AI-Powered Energy Management Software Market, this matters because better interval data helps platforms move from simple monitoring to active prediction and automated response. Commercial sites are also bringing HVAC controls, inverter feeds, and occupancy signals onto shared digital layers, which makes multi-site benchmarking more practical. That shift reduces the need for proprietary hardware in every location and improves the case for software-led rollouts across portfolios. Second-wave metering and sensor upgrades are also improving encryption, edge processing, and device reliability, which supports more secure analytics use in operating environments. As that installed base becomes more consistent, vendors in the North America AI-Powered Energy Management Software Market are better positioned to scale recurring software contracts across existing customer sites.

Rising Utility Tariffs and Demand Charges for Peak Load Customers

Rising electricity tariffs are turning energy optimization from a cost-control tool into a direct operating-margin tool for large facilities. Demand charges remain especially important because a short peak event can shape the full monthly bill for commercial and industrial users. Electricity demand in ERCOT grew by more than 9% year over year from October 2025 through March 2026, reflecting data center construction, industrial electrification, and growth in electric vehicle charging. That increase tightened grid conditions and strengthened the value of software that can shift load, automate response, and time battery dispatch more accurately. Facilities without these tools are facing not only higher bills but also greater exposure to short-term price swings as grid operators use more dynamic pricing structures. This is keeping the North America AI-Powered Energy Management Software Market closely tied to tariff pressure in high-load states.[1]Hitachi Energy, “The Hitachi Energy Grid Pulse, North American Load, Generation and Capacity Additions,” Hitachi Energy, hitachienergy.com

Portfolio Decarbonization Commitments from Enterprises and Campuses

Enterprise decarbonization programs are still supporting software demand even when broader capital spending is selective. 82% of companies maintained or accelerated their decarbonization timelines, and 60% began using AI for operational decarbonization in 2026. For the North America AI-Powered Energy Management Software Market, that means many buyers still need tools that can measure consumption, track scope 2 progress, and document results within formal reporting cycles. The same study found that fewer than 1% had reported measurable results, which shows that many organizations are still early in converting software pilots into verified outcomes. Mars said in 2026 that all of its United States operations were now powered by 100% renewable electricity, and that it planned USD 2 billion in United States manufacturing investment by the end of 2026. That kind of operating commitment keeps the North America AI-Powered Energy Management Software Market tied to measurable portfolio performance, not only to renewable power procurement.

Integration With Distributed Energy Resources and Battery Storage

Distributed energy growth is increasing the need for software that can coordinate more variable, distributed assets. Installed battery storage capacity in the United States reached nearly 50GW by March 2026, up from 31GW in March 2025, while solar, wind, and battery systems accounted for 85% of new United States capacity additions from October 2025 through March 2026. Each added battery system or solar installation creates another bidirectional point that older control layers were not built to manage in real time. In April 2026, it was noted that distributed energy resources can provide a scalable, lower-cost path to grid resilience, but only when the system can coordinate generation, storage, and flexible demand. That need is driving the expansion of orchestration engines that can make decisions across site loads, storage dispatch, and grid signals within a single platform. As a result, the North America AI-Powered Energy Management Software Market is gaining support from both utility programs and customer-owned energy assets.[2]The Pew Charitable Trusts, “Distributed Energy Can Unleash the Resilient, Affordable Grid of the Future,” The Pew Charitable Trusts, pew.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity with Legacy Building Management Systems | -2.0% | North America, with strongest relevance in older United States commercial buildings and Canadian mid-market sites | Medium term (2-4 years) |

| Cybersecurity And Data Governance Concerns for Connected Energy Data | -1.5% | United States regulated utilities and Canada | Medium term (2-4 years) |

| Long Enterprise Sales Cycles and Solution Validation Requirements | -1.0% | United States and Canada large enterprise segments | Long term (≥ 4 years) |

| Skilled Facility-Analytics Talent Shortage at Mid-Market End Users | -0.8% | North America mid-market commercial buildings and light industrial sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity with Legacy Building Management Systems

Legacy system complexity remains a major barrier because many buildings still operate with mixed protocols and older controllers. In the North America AI-Powered Energy Management Software Market, this slows deployment when building automation layers do not share a common data structure or an easy application interface. Many sites carry years of BACnet, Modbus, and proprietary controls that were installed in stages rather than designed as one connected architecture. That forces software vendors to spend more time on middleware, custom mapping, and validation before the first analytic model can deliver value. Mid-sized commercial properties are affected the most because they are large enough to justify software investment but often lack specialist integration and staff. This keeps deployment costs elevated and makes the North

Cybersecurity and Data Governance Concerns for Connected Energy Data

Cybersecurity is becoming a more visible buying factor as operating technology environments connect more assets and more external data streams. In 2025, it was reported that cyberattacks on energy utilities had tripled over the previous 4 years, underscoring how quickly digital exposure has grown. NERC finalized CIP-013-4 in April 2026, which added supply chain cyber security risk management requirements for bulk electric system cyber systems.[3]International Energy Agency, “Energy and AI, Executive Summary,” International Energy Agency, iea.org Those checks are lengthening validation and procurement timelines for utility buyers, especially when software touches operational environments or critical data paths. At the same time, AI can identify physical infrastructure incidents far faster than conventional methods, which means buyers also see AI as part of the defense response. This leaves the North America AI-Powered Energy Management Software Market in a position where stronger cybersecurity can initially slow sales but, over time, strengthen vendor credibility.[4]North American Electric Reliability Corporation, “CIP-013-4 Standard, Cyber Security Supply Chain Risk Management,” North American Electric Reliability Corporation, nerc.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Revenue Stayed Dominant While Services Continued To Deepen Customer Relationships

Software held 74.12% of the North America AI-Powered Energy Management Software market share in 2025, keeping vendor revenue centered on recurring subscriptions and licensing rather than hardware-led project margins. The North America AI-Powered Energy Management Software Market continues to favor software because customers typically want fast visibility, optimization logic, and reporting without adding significant new field hardware. That revenue profile also gives vendors more room to expand into analytics upgrades, dashboards, forecasting tools, and compliance modules over time. Eaton launched Brightlayer Energy in March 2026 for commercial buildings in healthcare, education, and retail, with functions for real-time analysis, forecasting, automated control, and distributed energy optimization. Product launches like this show how software vendors are tying energy optimization more closely to operational management and local compliance support

Services are smaller in absolute terms, but they are projected to grow at a 17.93% CAGR from 2026 to 2031, slightly ahead of the overall market pace. In the North America AI-Powered Energy Management Software Market, the customer base increasingly needs integration support, managed analytics, and model tuning after initial deployment. Many organizations lack sufficient internal energy analytics or data science staff to maintain complex in-house optimization tools. This is pushing providers to compete on service depth, onboarding quality, and ongoing performance support as much as on software features.

By Deployment Mode: Hybrid Models Balanced Cloud Scale With Operating Technology Control

Cloud-based deployment accounted for 63.14% of the market in 2025, reflecting the appeal of simpler rollout and lower infrastructure management for many building and enterprise users. The North America AI-Powered Energy Management Software Market has shifted toward the cloud because multi-site users often need centralized reporting and faster software updates across portfolios. Hybrid deployment is still the fastest-growing mode with an 18.02% CAGR from 2026 to 2031, because many regulated or sensitive environments want analytics scale without fully moving control-plane data outside the local security boundary. That makes hybrid architecture a practical fit for utilities and industrial operators that must keep tighter control over operational systems. It also helps vendors serve customers who want real-time edge decisions on-site while still using cloud layers for broader analytics and oversight.

NERC requirements reinforce the need for careful cyber design when software interfaces with the bulk electric system. AWS and Siemens Energy expanded their collaboration in April 2026 to support digital transformation and energy infrastructure solutions, reflecting how major technology providers are aligning cloud capabilities with the energy sector's operating needs. In the North America AI-Powered Energy Management Software Market, this supports the view that hybrid frameworks will remain central while utilities and large enterprises balance scale, latency, and compliance. Pure on-premises models will remain relevant in more stringent environments, but their relative growth is likely to lag that of more flexible architectures over the forecast period.

By Application: Demand Optimization Led Current Spending While Renewable Forecasting Expanded Fastest

Energy Consumption and Demand Optimization accounted for 28.17% of the North America AI-Powered Energy Management Software market in 2025, indicating that direct bill reduction remains the primary commercial entry point for many buyers. The North America AI-Powered Energy Management Software Market still depends on this application because customers can usually connect optimization tools to measurable load shifting, demand response, and avoided peak costs. Renewable Energy Forecasting and Integration is projected to grow at an 18.21% CAGR through 2031 as utilities and power producers work with a more variable generation mix. In 2026, researchers published findings that advanced deep learning methods can support 15-minute photovoltaic power forecasts across horizons ranging from 4 hours to 7 days. That kind of forecasting accuracy supports tighter scheduling, trading, and balancing decisions as renewable penetration rises.

In 2025, it was noted that AI-led optimization in buildings could deliver major electricity savings, supporting the staying power of demand optimization even in mature smart building environments. The North America AI-Powered Energy Management Software Market also includes asset performance, predictive maintenance, smart grid management, and energy trading tools that are gaining value as operating conditions become more dynamic. Forecasting and optimization are increasingly linked because buyers want a single platform that can read market signals, on-site generation, storage status, and load behavior together. That is pushing application demand beyond basic dashboards and toward decision engines that can act on variability rather than only report it.

By End User: Utilities Held The Largest Position While Industrial Facilities Showed The Fastest Expansion

Utilities captured 29.12% of the North America AI-Powered Energy Management Software market share in 2025, reflecting their role as large-scale users of demand response, DER coordination, and grid-facing analytics. The North America AI-Powered Energy Management Software Market continues to rely on utilities for scale because they can deploy platforms across large customer networks and grid programs. EnergyHub said its Edge DERMS platform managed more than 1.8 million distributed energy resources and over 2.5 GW of flexible capacity for over 120 utilities in 2026. That scale shows why utility contracts remain important for recurring revenue and ecosystem reach. Commercial buildings remained another important user group because owners and operators need lower occupancy-related energy costs and stronger reporting support for tenants and investors.

Industrial facilities are projected to grow at a 18.34% CAGR from 2026 to 2031, making them the fastest-growing end-user segment in the North America AI-Powered Energy Management Software Market. Their growth is being supported by the fact that energy is a direct production input, so efficiency gains flow quickly into plant economics. Large industrial sites also tend to face more volatile load profiles, higher exposure to peak demand charges, and stronger pressure to match production growth with emissions control. Residential uptake remains the smallest segment, but aggregation models are improving its path to scale, especially where demand response programs connect large numbers of homes into one coordinated resource.

Geography Analysis

The United States accounted for 66.18% of the North America AI-Powered Energy Management Software market size in 2025, making it the largest country market by a wide margin. The North America AI-Powered Energy Management Software Market is centered in the United States because the country combines the region's deepest software base with the largest data center buildout and the broadest utility modernization activity. In 2024, the United States accounted for 45% of global data center electricity consumption, which helps explain why demand for energy optimization software is rising quickly in data-intensive environments. United States electricity demand grew by 2% year over year from October 2025 through March 2026, while ERCOT load growth exceeded 9% in the same period. The same operating pressure is making AI-based demand flexibility more relevant as both a cost tool and an infrastructure support tool.

Canada held a smaller share of the North America AI-Powered Energy Management Software Market, but it remained important because of strong distributed energy and energy management program activity. Ontario IESO enrolled more than 100,000 homes within 6 months through its thermostat demand response program, creating Canada's largest residential virtual power plant in 2026. Bell Canada said in its 2025 sustainability data summary that it integrated its ISO 50001-certified Energy Management System into its ISO 14001 Environmental Management System, which shows how large Canadian enterprises are moving toward more unified governance structures. That shift favors software platforms that can connect operational efficiency with formal environmental management workflows.

Mexico is projected to grow at a 18.41% CAGR from 2026 to 2031, making it the fastest-growing geography in the North America AI-Powered Energy Management Software Market. Growth is being supported by nearshoring activity in northern manufacturing corridors, where new facilities are being built with more modern metering and control systems. Those projects are bringing stronger expectations for automated monitoring, demand control, and energy visibility from the start of plant design. Mexico also has a lower current base of AI software penetration in mid-sized industrial facilities, leaving more room for new adoption. As those sites scale production and face peak-demand pressure, software demand is likely to rise faster than in the region's more mature markets.

Competitive Landscape

The North America AI-Powered Energy Management Software Market remains moderately concentrated in large utility and enterprise accounts, where Schneider Electric, Siemens, Johnson Controls International, Honeywell International, and ABB benefit from broad installed bases and long customer relationships. At the same time, the market is more fragmented at the software layer, where specialist vendors can compete with faster model updates, narrower use cases, and more flexible integration approaches. This mix is creating a split market where incumbents hold trust, service reach, and integration capacity, while newer firms compete on speed and specialization. Johnson Controls acquired Nantum AI in April 2026 to add occupancy-driven airflow optimization, which had already shown more than 10% energy savings, and folded that capability into the OpenBlue ecosystem. That move shows how leading vendors are using acquisitions to close capability gaps more quickly than internal product development alone.

The market still has open space in mid-sized commercial buildings, where many properties are too complex for consumer tools but too constrained for large custom deployments. Eaton's March 2026 Brightlayer Energy launch targeted healthcare, education, and retail buildings with real-time analysis, forecasting, automated control, and support for distributed energy resources. That product direction shows how vendors are trying to simplify energy software for operators that want measurable savings without building large internal technical teams. Another open area remains industrial energy trading and market intelligence, where no single provider has yet established a clearly dominant position in the region.

Competitive differentiation is moving beyond dashboards and reporting toward automation, orchestration, and easier user interaction. Trane Technologies launched AI Control and ARIA in September 2025, with ARIA serving as a conversational AI agent for building management and AI Control targeting lower heating and cooling costs and carbon emissions. AWS and Siemens Energy also expanded their collaboration in April 2026, linking cloud capability more closely to digital transformation and energy infrastructure support. In the North America AI-Powered Energy Management Software Market, these moves suggest that buyers increasingly value platforms that combine energy logic, scalable deployment, and easier site-level action. The competitive balance is therefore shifting toward vendors that can integrate optimization, interoperability, and service execution into a single offer.

North America AI-Powered Energy Management Software Industry Leaders

Schneider Electric SE

Siemens AG

Johnson Controls International plc

Honeywell International Inc.

ABB Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: ABB and Samsung Electronics announced a new integration between ABB Ability Building Pro and Samsung SmartThings Pro. The partnership provides building operators with a unified view of lighting, climate, shading, and access-control systems alongside energy monitoring and presence detection data, directly addressing the multi-system visibility challenge central to commercial building energy management and expanding ABB's interoperability-led go-to-market strategy.

- May 2026: Schneider Electric completed phased delivery of over USD 290 million in AI infrastructure solutions, including Motivair liquid cooling technologies, at TeraWulf's Google-backed Lake Mariner campus in Barker, New York. Upon full buildout, the campus is projected to support up to 750 MW of power demand, reinforcing Schneider Electric's strategic positioning at the intersection of large-scale AI infrastructure and energy management.

- May 2026: Trane Technologies opened the BrainBox AI Trane Technologies AI Lab and showroom in Montreal, Canada. The facility serves as a dedicated development and scaling center for AI solutions targeting a 30% reduction in building energy waste, marking a key milestone in Trane Technologies' strategy to commercialize BrainBox AI-powered building optimization across its global HVAC customer base.

- April 2026: Johnson Controls International acquired Nantum AI, a New York-based company specializing in AI algorithms that deliver over 10% energy savings by optimizing building airflow in real time based on occupancy data. The acquisition strengthens the OpenBlue digital ecosystem and extends Johnson Controls' AI capability into complex facilities, including healthcare campuses and advanced manufacturing environments.

North America AI-Powered Energy Management Software Market Report Scope

The North America AI-Powered Energy Management Software market refers to platforms and services that leverage artificial intelligence to optimize energy consumption, improve asset performance, and enable smarter grid and distributed energy resource (DER) management. These solutions provide advanced capabilities, including predictive maintenance, renewable energy forecasting, carbon-aware demand optimization, and market intelligence for energy trading and pricing. By embedding AI-driven analytics into energy workflows, these platforms help utilities, industries, commercial facilities, and residential buildings reduce costs, enhance efficiency, comply with sustainability regulations, and accelerate the transition toward cleaner energy systems. The market’s primary objective is to enable data-driven decision-making, improve resilience, and support North America’s broader decarbonization and energy sustainability goals.

The North America AI-Powered Energy Management Software market report is segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Smart Grid and Distributed Energy Resource (DER) Management, Renewable Energy Forecasting and Integration, and Energy Trading, Pricing and Market Intelligence), End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential Buildings), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| United States |

| Canada |

| Mexico |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the size of the North America AI-Powered Energy Management Software Market?

The North America AI-Powered Energy Management Software Market was valued at USD 1.46 billion in 2025, reached USD 1.70 billion in 2026, and is forecast to reach USD 3.87 billion by 2031 at a 17.88% CAGR.

Which deployment model is growing fastest in North America AI-powered energy management software?

Hybrid deployment is the fastest-growing mode, with an 18.02% CAGR through 2031, as buyers balance cloud scale with local operating technology control needs.

Which application area is expanding the fastest across this space?

Renewable Energy Forecasting and Integration is the fastest-growing application, with an 18.21% CAGR through 2031, supported by rising solar, wind, and battery complexity.

Which end-user group is driving the fastest expansion?

Industrial facilities are growing the fastest, at an 18.34% CAGR, because energy costs directly affect production economics and peak demand exposure.

Which country leads adoption across North America?

The United States led the region with 66.18% share in 2025, supported by large data center demand, utility modernization, and a deep software vendor base.

Why are major vendors making acquisitions and new product launches in this space?

Vendors are trying to lock in recurring software and services revenue, improve automation, and strengthen cyber-ready and interoperable platforms, as shown by deals such as Johnson Controls and Nantum AI and launches such as Eaton Brightlayer Energy.

Page last updated on: