Australia AI-Powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

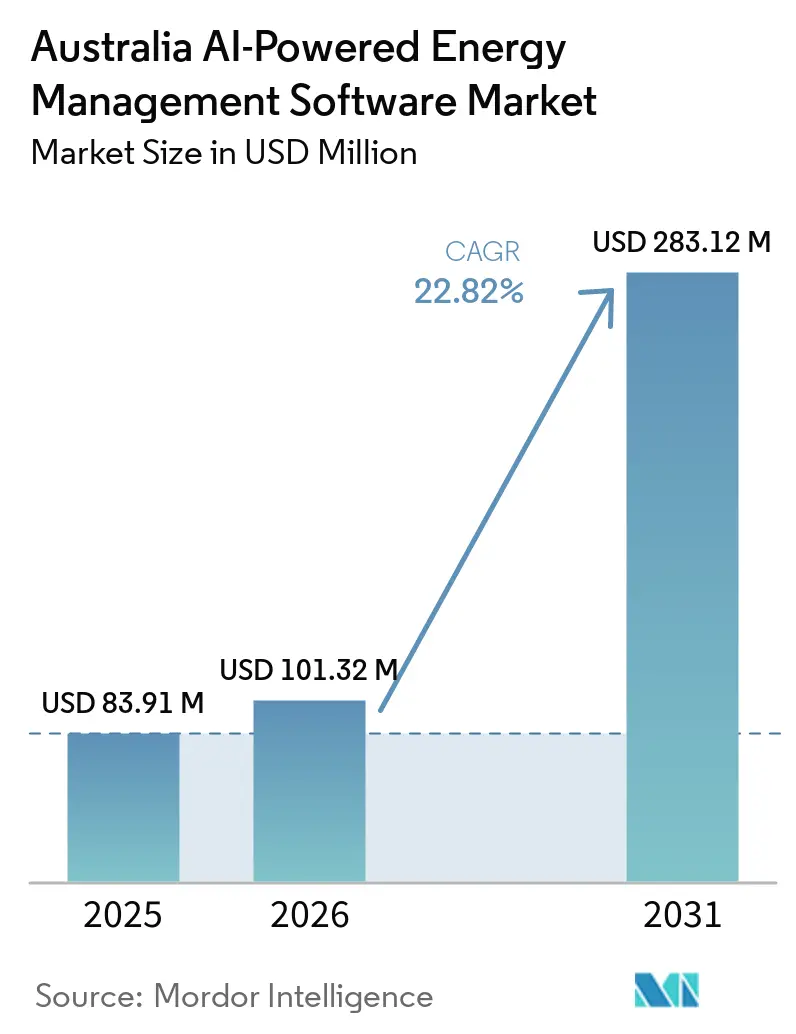

| Base Year Market Size (2025) | USD 83.91 Million |

| Market Size (2026) | USD 101.32 Million |

| Market Size (2031) | USD 283.12 Million |

| Growth Rate (2026 - 2031) | 22.82% CAGR |

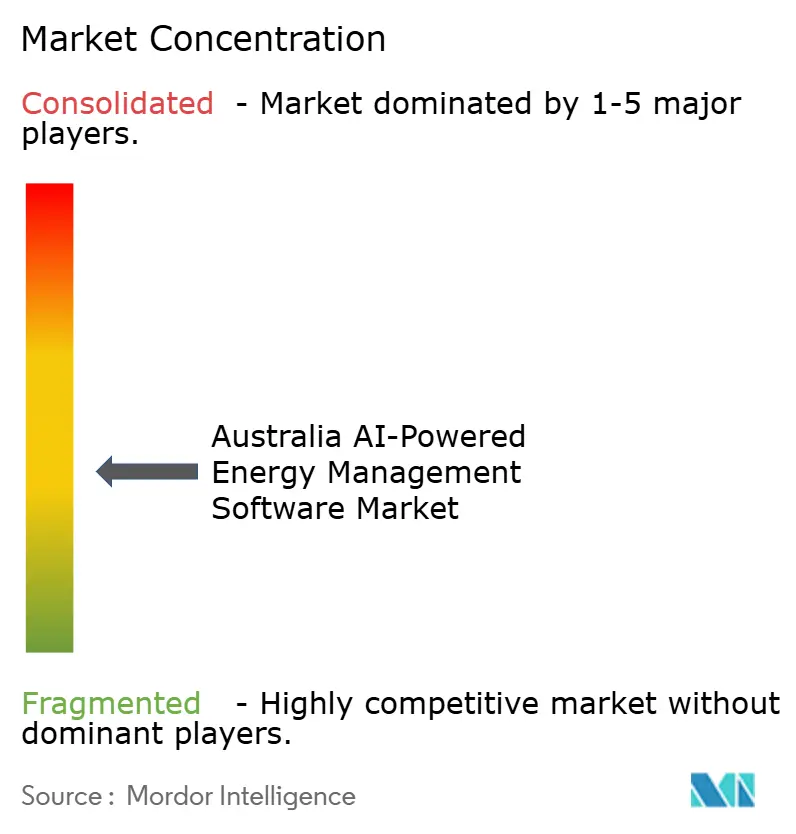

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia AI-Powered Energy Management Software Market Analysis by Mordor Intelligence

The Australia AI-powered energy management software market size is expected to grow from USD 83.91 million in 2025 to USD 101.32 million in 2026 and is forecast to reach USD 283.12 million by 2031 at 22.82% CAGR over 2026-2031. The Australia AI-powered energy management software market is expanding as distributed energy assets now operate at a scale that requires constant coordination across homes, commercial buildings, utilities, and industrial sites. Rooftop solar capacity moved past the country’s coal-fired fleet by the end of 2025, and battery adoption accelerated sharply after the Cheaper Home Batteries Program started in July 2025, which raised the need for software that can manage generation, storage, and load in real time. Electricity tariff volatility is also pushing buyers toward AI-led optimization, because five-minute market signals and higher exposure to peak pricing are making manual energy management less practical. Building energy rules, industrial emissions compliance, and network visibility needs are widening the buyer base, while hybrid deployment models are opening new room for vendors that can combine cloud analytics with site-level control. Competition now centers on platform depth, local grid integration, managed services capability, and the ability to serve both east coast NEM states and Western Australia’s separate market structure.

Key Report Takeaways

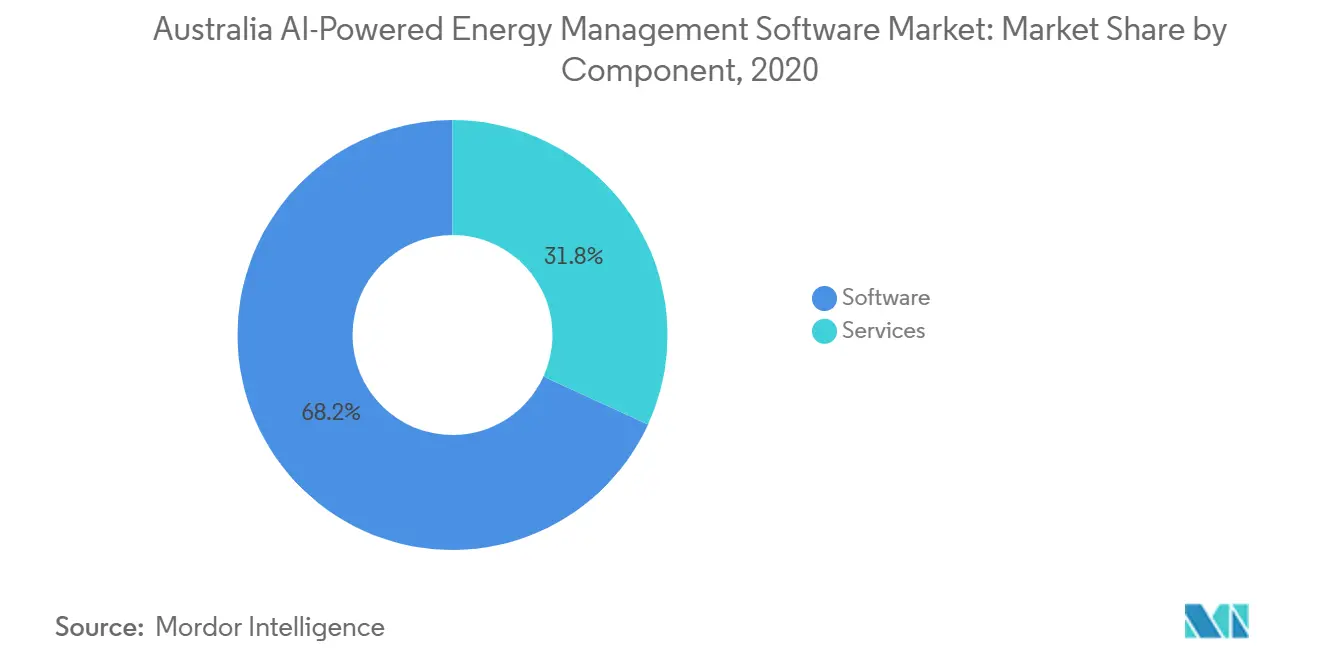

- By component, software held 68.17% share of the Australia AI-powered energy management software market in 2025, while services are projected to expand at a 23.91% CAGR through 2031.

- By deployment mode, cloud-based platforms accounted for 58.12% of the market share in 2025, while hybrid deployment is expected to record the fastest growth at 23.98% through 2031.

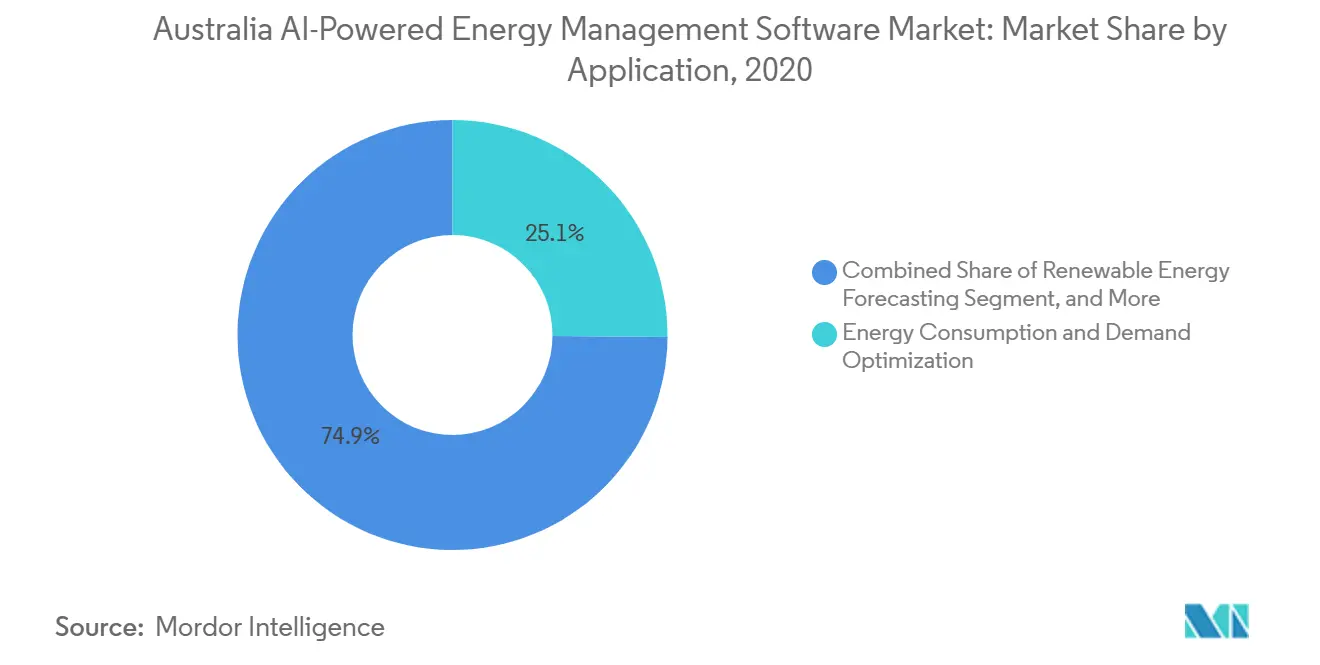

- By application, energy consumption and demand optimization accounted for 25.14% share of the Australia AI-powered energy management software market in 2025, while renewable energy forecasting and integration are projected to advance at a 24.12% CAGR through 2031.

- By end user, utilities held 32.18% share in 2025, while industrial facilities are expected to post the highest CAGR at 24.23% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia AI-Powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Rooftop Solar, Battery, and Flexible Load Orchestration Demand | +5.2% | National, with accelerated impact in NSW, QLD, SA, and VIC | Short term (≤ 2 years) |

| Rising Electricity Tariff Volatility and Peak Pricing Exposure | +4.1% | National, highest exposure in SA and NSW where spot price caps are steepest | Short term (≤ 2 years) |

| Mandated Energy Efficiency and Decarbonization Programs in Buildings and Industry | +3.8% | National, with early compliance gains in NSW, VIC, and ACT under CBD and NCC 2025 | Medium term (2-4 years) |

| Utility and Network Need for Behind-the-Meter Visibility | +3.2% | National in NEM states, with spillover to WA under SWIS reform | Medium term (2-4 years) |

| Edge-Aware AI for Site-Level Autonomy and Lower Latency Control | +2.3% | National, led by remote WA microgrids and SA high-DER distribution networks | Medium term (2-4 years) |

| Portfolio-Wide ESG Reporting and Measurement, Reporting, and Verification Automation | +2.2% | National, with early gains in large corporate portfolios in Sydney, Melbourne, and Brisbane | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Rooftop Solar, Battery, and Flexible Load Orchestration Demand

Australia’s distributed energy base has reached a point where coordination software has become part of everyday grid operations rather than an optional upgrade. Rooftop solar PV capacity passed 28.3GW by the end of 2025, and it supplied 14.2% of the country’s electricity generation in the second half of the year, up from 7.2% in 2020.[1]Clean Energy Council, “Rooftop Solar and Storage Report, July to December 2025,” Clean Energy Council, cleanenergycouncil.org.au Battery adoption also moved quickly, with 454,753 units installed cumulatively by the end of 2025, while battery discharge nearly tripled in the final quarter of 2025, easing evening wholesale price pressure. The July 2025 battery support program increased attachment rates and brought more storage systems into behind-the-meter settings that require fast decisions on charging, export, and self-consumption. That shift is strengthening the Australia AI-powered energy management software market because building operators, aggregators, and utilities now need a common software layer that can respond to real operating conditions instead of fixed schedules. The Australia AI-powered energy management software market is also benefiting from the fact that these assets now affect not only customer bills, but also local network stability and wholesale market behavior.

Rising Electricity Tariff Volatility and Peak Pricing Exposure

Electricity price volatility remains a clear reason for customers to invest in optimization software across the Australia AI-powered energy management software market. Australia’s authorized spot market price cap stood at AUD 18,600/MWh (USD 11,830/MWh) in 2025 and will rise to AUD 22,800/MWh (USD 14,455/MWh) from July 2026.[2]Australian Energy Regulator, “State of the Energy Market 2025,” Australian Energy Regulator, aer.gov.au The Australian Energy Regulator also reported that dispatch intervals with prices above AUD 300/MWh increased from 0.4% of all intervals in 2020 to 1.8% in 2024, which means exposure to price spikes has widened over time. South Australia showed how sharp that pressure can become when a January 2026 heatwave lifted the state’s quarterly average wholesale price from AUD 81/MWh (USD 51.52/MWh) to AUD 144/MWh (USD 91.58/MWh). The national smart meter rollout, which targets full penetration by 2030, will make five-minute time-of-use pricing more visible to a broader customer base and improve the payback case for AI-led load scheduling. As a result, the Australia AI-powered energy management software market is moving beyond large industrial accounts and gaining relevance with mid-sized commercial operators that now face more direct pricing signals.

Mandated Energy Efficiency and Decarbonization Programs in Buildings and Industry

Rules for buildings and industry are widening the addressable customer base for the Australia AI-powered energy management software market. NCC 2025 introduced binding energy monitoring requirements for commercial buildings larger than 500m², including time-of-use electricity and gas metering and EMIS functionality at 5-minute reporting intervals.[3]Australian Building Codes Board, “Part J9 Energy Monitoring and On-Site Distributed Energy Resources,” National Construction Code 2025, abcb.gov.au The Commercial Buildings Disclosure program also requires NABERS energy ratings for offices above 1,000 m² at sale or lease events, creating a direct need for continuous performance tracking rather than occasional reporting. Victoria’s all-electric building mandate will start in January 2027, and that is already shaping software buying decisions because operators will need better control over HVAC, batteries, and EV charging in fully electric properties. At the industrial level, the Safeguard Mechanism is turning energy optimization into a compliance issue, especially for large sites that cannot manage rising electricity costs and emissions duties separately. The Australia AI-powered energy management software market is therefore gaining support from regulations that affect both asset performance and reporting discipline throughout the full life of a building or industrial facility.

Utility And Network Need for Behind-The-Meter Visibility

Utilities and network operators are becoming more active buyers in the Australia AI-powered energy management software market because they need better visibility into assets that sit behind the customer meter. AEMO’s DER Data Exchange co-design process set out a standardized architecture for secure data sharing, aligned with ISO 27001 security standards and SOCI Act requirements.[4]Australian Energy Market Operator, “NEM Reform Program Industry Status Report, May 2026,” Australian Energy Market Operator, aemo.com.au The NEM Reform Program also moved forward in 2026 with new Battery Power Quality Data arrangements, which added new data-handling and integration work for utilities operating across NEM states. SwitchDin’s deployment with Endeavor Energy showed that utility-contracted platforms can manage export limits and renewable integration in real time at network scale, using IEEE 2030.5-based communications across a large grid monitoring base. That model changes the revenue profile of the Australia AI-powered energy management software market because utility contracts are usually larger and run longer than single-site building software deals. It also raises the value of vendors that can support both operational technology needs and regulatory interoperability within a single offering.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Building Management System Integration Complexity | -2.8% | National, concentrated in aging commercial building stock in Sydney CBD, Melbourne, and Brisbane | Medium term (2-4 years) |

| Cybersecurity and Data Governance Concerns for Cloud-Connected Platforms | -2.2% | National in NEM states and WA, with higher sensitivity among critical infrastructure operators | Short term (≤ 2 years) |

| Interoperability Gaps Across Inverters, Meters, HVAC, and Distributed Energy Resources | -1.8% | National, most acute in WA microgrids and multi-vendor industrial sites | Medium term (2-4 years) |

| Shortage of AI, Controls, and Energy Optimization Implementation Talent | -1.4% | National, concentrated in non-metropolitan markets with limited engineering labor pools | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy Building Management System Integration Complexity

Older building systems remain a practical barrier for the Australia AI-powered energy management software market, especially in commercial property portfolios with mixed equipment vintages. Many building management systems installed in the 2000s and early 2010s were not designed for open APIs, cloud-native data flows, or newer DER communication standards. That creates additional costs for middleware, metering upgrades, and partial hardware replacements before AI software can operate as intended. NCC 2025 is increasing this pressure because building owners who must meet new monitoring rules are finding that their current systems cannot always produce the required five-minute data without deeper reconfiguration. This issue matters most in the mid-market segment, where owners often lack internal technical teams and need vendors to manage both integration and compliance work together. The Australia AI-powered energy management software market therefore favors providers that already support the most common local BMS environments and can shorten retrofit timelines.

Cybersecurity and Data Governance Concerns for Cloud-Connected Platforms

Cybersecurity requirements are also slowing some purchases in the Australia AI-powered energy management software market, especially where utilities and critical infrastructure are involved. The amended SOCI framework imposes stricter risk management and reporting duties on operators of relevant electricity assets, and these obligations now shape software procurement much earlier in the sales process. AEMO’s Australian Energy Sector Cyber Security Framework gives utilities and their suppliers a recognized maturity benchmark linked to ISO 27001 and the NIST Cybersecurity Framework. The April 2026 independent review of the SOCI Act also pointed to virtual power plant aggregators and inverter manufacturers as areas where future tightening may occur, which suggests that compliance costs will rise further for cloud-connected platforms. Enterprise buyers now expect incident readiness, data governance controls, and compliance evidence up front, and that can extend sales cycles for vendors that do not have those elements in place.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Holds The Revenue Base While Services Gain Weight

Software accounted for 68.17% of revenue in 2025, which shows that the current value pool still sits mainly in the platform layer rather than in one-time deployment work. In the Australia AI-powered energy management software market, subscription and licensing revenue remains important because customers need continuous forecasting, dashboarding, reporting, and model updates after the first installation. This has helped software vendors maintain the revenue lead, especially when analytics, DER control, and demand optimization are delivered through recurring contracts. The Australia AI-powered energy management software industry also reflects a buyer preference for tools that can unify multiple energy assets into one operating view instead of relying on separate systems for each function. That structure supports a larger lifetime value per account even before services are added.

Services, however, are projected to grow at a 23.91% CAGR through 2031, indicating how much practical work still sits outside the core platform. Large customers often need help with integration, tuning, compliance reporting, alarm management, and user training, especially when assets come from several vendors or sites operate under different rules. Siemens’ cloud SCADA deployment for Global Power Generation Australia shows how major software rollouts can turn into multi-year support programs rather than short delivery projects. The Australia AI-powered energy management software market share held by software does not reduce the importance of services, because many buyers treat both as one operating package once the system moves into daily use. Over time, more vendors are likely to package software, optimization support, and reporting services together, making the line between component categories less visible to customers.

By Deployment Mode: Cloud Leads Today While Hybrid Fits Real-Time Control Needs

Cloud-based deployment accounted for 58.12% in 2025, confirming that low upfront costs and easy remote access continue to make SaaS the most practical entry point for many users. In the Australia AI-powered energy management software market, cloud delivery works well for analytics, portfolio dashboards, reporting, and fleet-level oversight across widely spread sites. It also meets the needs of commercial operators who want faster rollout and lower internal IT demands. On-premises deployment remains relevant for a smaller group of critical operators who place greater weight on data residency, network segregation, and direct control over system architecture. Those conditions keep on-premises options in play even as broader adoption stays cloud-led.

Hybrid deployment is expected to post the fastest CAGR at 23.98% through 2031, because it solves a practical problem that pure cloud models cannot always handle. Real-time battery dispatch, load control, and export management often require site-level response within seconds, while cloud systems are more useful for broader optimization and coordination. SwitchDin’s work with Endeavor Energy shows how edge-enabled devices and central analytics can work together in live network environments where export limits must be adjusted quickly. That combination is becoming more attractive in the Australia AI-powered energy management software industry as utilities, industrial operators, and advanced buildings all need both local autonomy and portfolio-level visibility. The Australia AI-powered energy management software market size tied to hybrid models should therefore continue to rise as more buyers shift from basic monitoring to active control.

By Application: Demand Optimization Stays Core While Forecasting Expands Fast

Energy consumption and demand optimization accounted for a 25.14% share in 2025, making it the most established application area in current deployments. This part of the Australia AI-powered energy management software market covers HVAC scheduling, load shifting, battery use, demand charge reduction, and basic operating efficiency across controllable assets. Buyers continue to prioritize these functions because the savings case is easier to understand and the operational benefits appear sooner than in newer applications. That is why demand optimization still anchors many first purchases, especially in buildings and industrial sites. It also gives vendors a starting point from which they can later sell forecasting, maintenance, and market participation tools.

Renewable energy forecasting and integration is projected to grow at a 24.12% CAGR through 2031, indicating that grid-facing use cases are accelerating. As rooftop solar, batteries, and distributed resources grow, operators need better short-interval forecasts and smoother coordination between site assets and network conditions. AEMO’s DER Data Exchange work and ongoing reform activity point to a system that is moving toward richer visibility and more structured data sharing across connected resources. That shift is giving the Australia AI-powered energy management software market new room in smart grid management, asset health, and pricing intelligence, even though those areas remain less mature than core optimization today. Over time, applications are likely to converge into broader platforms, meaning customers will buy fewer single-purpose tools and more integrated operating systems for energy assets.

By End User: Utilities Lead Current Demand While Industry Drives The Next Expansion

Utilities held the largest end-user share at 32.18% in 2025, which reflects the size and duration of software contracts linked to distribution networks, DER programs, and demand response. In the Australia AI-powered energy management software market, utility projects tend to involve larger contract values because one deployment can influence thousands of customers or a wide network area. They also require ongoing platform support, cybersecurity controls, and interoperability work, which support recurring revenue over the long term. Utility demand has been reinforced by the need for better behind-the-meter visibility and by reforms that increase the amount of data flowing into network operations. This keeps utilities at the center of the current market scale, even as other customer groups expand.

Industrial facilities are expected to grow at a 24.23% CAGR through 2031, making them the most important growth segment in the next phase. Rising electricity price exposure, tighter emissions rules, and more complex site energy systems are pushing industrial operators to treat optimization software as a control tool rather than only a reporting tool. Commercial buildings still offer strong volume potential, but older BMS environments can slow conversions in parts of that base. Residential buildings remain smaller by revenue, yet product launches aimed at households show how consumer-facing platforms are becoming more capable and more closely tied to batteries, EV charging, and flexible tariffs. The Australia AI-powered energy management software market share linked to utilities remains the largest today, but the fastest expansion is moving toward industrial users that need continuous control, compliance support, and asset coordination across multi-shift operations.

Geography Analysis

New South Wales remained the largest state opportunity in the Australia AI-powered energy management software market because it combines the country’s largest concentration of commercial buildings with the highest rooftop solar base at 8GW. Sydney’s office stock is deeply exposed to Commercial Buildings Disclosure and NABERS performance requirements, which keeps software demand tied not only to energy savings but also to leasing and valuation discipline. NSW also has active utility demand, and Enel X’s selection as the sole virtual power plant provider in the first firming tender under the state’s Electricity Infrastructure Roadmap showed that flexible demand solutions are being treated as a serious system resource. Queensland followed as the second-largest state opportunity because its 1.16 million rooftop solar installations and growing battery pipeline create a strong need for forecasting, dispatch, and control tools across utility territories.

South Australia carries more strategic weight than its population suggests because it has become a live testing ground for advanced DER management and flexible export architectures. That matters in the Australia AI-powered energy management software market because software proven in South Australia is often well placed to scale into other NEM states facing similar export and volatility issues. Price swings have also stayed pronounced there, and the January 2026 heatwave that lifted quarterly wholesale prices from AUD 81/MWh (USD 51.52/MWh) to AUD 144/MWh (USD 91.58/MWh) strengthened the case for automated demand response among commercial and industrial users. Victoria is moving into a stronger position as its January 2027 all-electric building rule approaches, pushing building owners to prepare for more integrated control of HVAC, storage, and EV charging. Hitachi’s March 2026 agreement with UTS and NTT DATA, aimed at localizing ESG data management and AI HVAC optimization for Australia, also showed that east coast commercial buildings remain a primary entry point for international vendors.

Western Australia stands apart because it operates under the South West Interconnected System rather than the NEM, which means vendors often need separate integrations and compliance pathways to compete nationally. That separate structure gives the Australia AI-powered energy management software market an unusual two-system character, where east coast rules do not automatically translate into Western Australian deployments. Horizon Power’s use of IEEE 2030.5-based DER management in remote communities supports the case for edge-aware control in places where geography and grid conditions make local autonomy more valuable. The Australian Capital Territory and Tasmania are smaller in commercial scale, yet they remain useful early-adopter locations because public-sector energy goals and high renewable penetration create good conditions for demonstration projects. These smaller markets do not define current revenue, but they can still shape product validation and reference wins for vendors looking to expand across the country.

Competitive Landscape

The Australia AI-powered energy management software market remains moderately fragmented, with global automation groups and local software specialists both holding meaningful positions across different customer sets. International players usually carry an advantage in large utility, industrial, and institutional deals because they can combine software with broader service networks, hardware links, and established system integration channels. Local firms, however, often hold greater credibility in grid-specific use cases because they built their products from the start around NEM dispatch timing, DER communications, and state-level operating realities. That split means competition is not based solely on brand scale, because local operating fit still matters in many buying decisions. It also helps explain why no single vendor is dominant across utilities, commercial buildings, industrial facilities, and residential use cases simultaneously.

Recent product moves show how leading companies are trying to widen their reach inside the Australia AI-powered energy management software market. Schneider Electric launched EcoStruxure Building Activate in Australia and New Zealand in July 2025 as an open SaaS platform aimed at small- and mid-sized buildings, signaling a direct push into the market segment where integration ease and subscription pricing matter most. ABB followed in March 2026 with Ability BuildingPro Suites, a cloud-based platform that brings together building automation, HVAC, energy management, IT, and IoT functions under a single layer, putting pressure on vendors that rely on narrower software offerings. Honeywell’s 25-year contract for the Melton Hospital in Victoria also showed how long-duration performance commitments can lock in a supplier for years in high-value institutional settings. These moves suggest that large vendors are not only selling software features but also trying to secure customer relationships through long-term service contracts and broader operational roles.

Local and regional specialists still have room to defend and expand their positions in the Australia AI-powered energy management software market, especially where network control, export management, and local interoperability are the main buying criteria. SwitchDin’s work with Endeavor Energy is a good example, demonstrating that Australian-built capabilities can support network-scale control while keeping local standards and live operating needs in mind. Enel X’s demand response virtual power plant rollout in New South Wales also highlighted how flexible capacity platforms are becoming part of state energy planning rather than a side offering. Hitachi’s collaboration model with UTS and NTT DATA pointed to another path: companies use local research partnerships to adapt global tools to Australian building conditions and reporting needs. The competitive field is therefore likely to remain mixed, with global firms strongest in broad portfolios and capital-intensive contracts, while local specialists retain an edge in software depth tied to domestic market design.

Australia AI-Powered Energy Management Software Industry Leaders

Schneider Electric SE

Siemens AG

Johnson Controls International plc

ABB Ltd

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Hitachi, Ltd., the University of Technology Sydney (UTS), and NTT DATA signed a Memorandum of Understanding (MoU) to expand green transformation (GX) business in Australia, using the UTS campus as a living lab. The partnership will localize Hitachi's EcoAssist-Enterprise ESG data management solution for NABERS compliance and integrate it with NTT DATA's HUCAST AI air conditioning optimization solution, which uses real-time weather and human traffic prediction for autonomous HVAC control.

- March 2026: ABB launched ABB Ability BuildingPro Suites at Light and Building 2026, a modular, cloud-based software platform that unifies building automation, HVAC, energy management, IT, and IoT systems under a single intelligence layer, supporting 40+ countries and targeting advanced analytics and portfolio-level optimization. The launch marks ABB's strategic shift toward a data-first digital building intelligence model.

- February 2026: UNSW Sydney's AI-enabled energy management system (EMS) living lab became operational at Dubbo Regional Council's facility in New South Wales, developed in collaboration with Sungrow Australia. The system targets Technology Readiness Level (TRL) 7-8 by end-2026, with planned future enhancements including EV integration and NEM trading capabilities.

- July 2025: Schneider Electric launched EcoStruxure Building Activate in Australia and New Zealand, an open, vendor-agnostic, cloud-based SaaS platform designed for small and mid-sized buildings, integrating HVAC, lighting, refrigeration, and energy management systems in a subscription model without large upfront capital requirements.

Australia AI-Powered Energy Management Software Market Report Scope

The Australia AI-Powered Energy Management Software market comprises platforms and services that leverage artificial intelligence to optimize energy consumption, improve asset performance, and enable smarter grid and distributed energy resource (DER) management. These solutions include predictive maintenance, renewable energy forecasting, demand-side optimization, and market intelligence for energy trading and pricing.

The Australia AI-Powered Energy Management Software market report is segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Smart Grid and Distributed Energy Resource (DER) Management, Renewable Energy Forecasting and Integration, and Energy Trading, Pricing and Market Intelligence), and End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential Buildings). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings |

Key Questions Answered in the Report

What is the size outlook for Australia AI-powered energy management software market through 2031?

The Australia AI-powered energy management software market stood at USD 83.91 million in 2025, reached USD 101.32 million in 2026, and is forecast to reach USD 283.12 million by 2031 at a CAGR of 22.82% over 2026-2031.

What is driving adoption of AI-based energy management software in Australia?

Growth is being supported by fast rooftop solar and battery adoption, higher tariff volatility, stricter building energy rules, industrial decarbonization needs, and rising utility demand for behind-the-meter visibility.

Which component generates the most revenue in Australia?

Software led the revenue mix with 68.17% share in 2025, which reflects the value of recurring subscriptions, analytics, reporting, and control functions across connected assets.

Which deployment model is growing the fastest?

Hybrid deployment is expected to grow the fastest at 23.98% through 2031 because many users now need both cloud-level analytics and site-level control for fast response.

Which application area is expanding the quickest?

Renewable energy forecasting and integration is projected to record the fastest growth at 24.12% through 2031 as distributed assets require more accurate coordination across the grid.

Which end-user group offers the strongest growth opportunity?

Industrial facilities are expected to post the highest CAGR at 24.23% through 2031 because they face rising electricity exposure, tighter emissions compliance, and more complex onsite energy systems.

Page last updated on: