United Kingdom Reverse Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

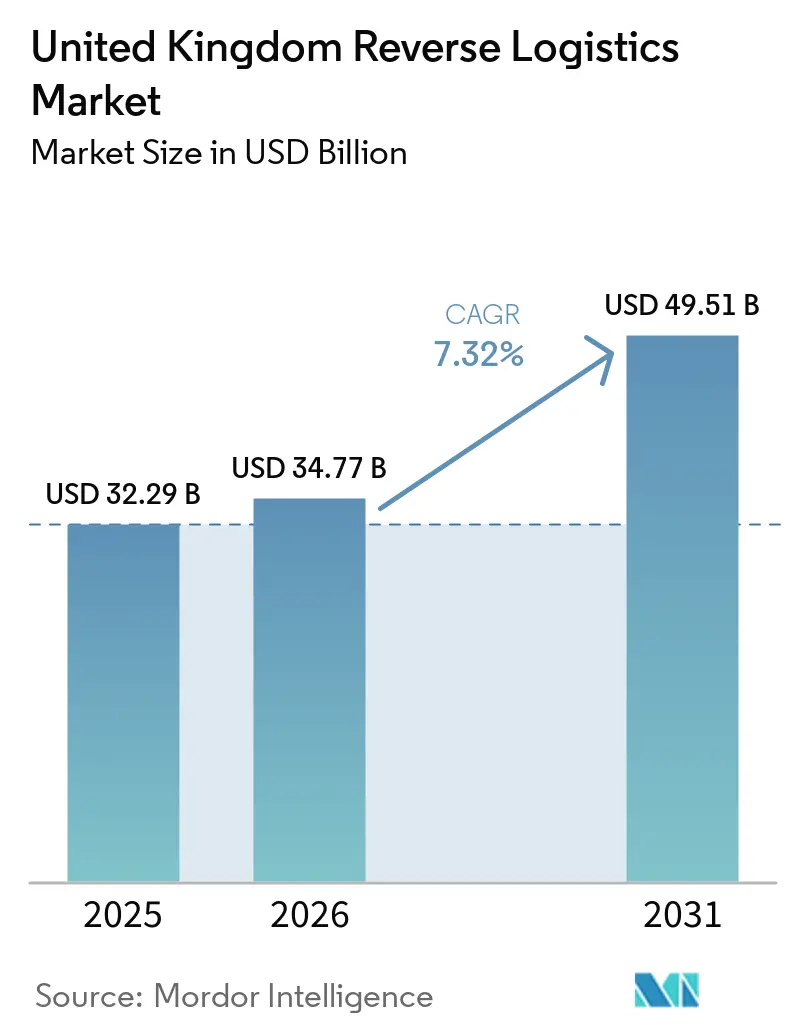

| Base Year Market Size (2025) | USD 32.29 Billion |

| Market Size (2026) | USD 34.77 Billion |

| Market Size (2031) | USD 49.51 Billion |

| Growth Rate (2026 - 2031) | 7.32% CAGR |

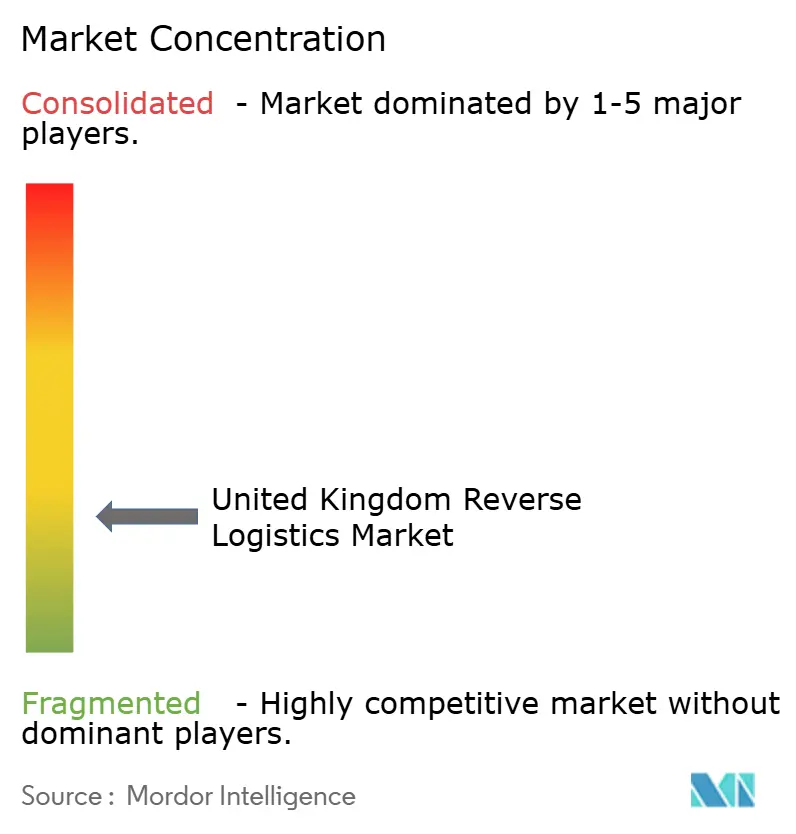

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Reverse Logistics Market Analysis by Mordor Intelligence

The United Kingdom reverse logistics market size was valued at USD 32.29 billion in 2025 and estimated to grow from USD 34.77 billion in 2026 to reach USD 49.51 billion by 2031, at a CAGR of 7.32% during the forecast period (2026 to 2031).

The United Kingdom reverse logistics market is being lifted by tighter recovery and recycling rules, as packaging EPR fees became enforceable in October 2025 and online marketplace obligations under the amended WEEE rules moved into force from August 2025, with financing obligations starting in January 2026. Competitive conditions are changing as large logistics groups add scale through acquisitions, most notably Evri with DHL eCommerce United Kingdom and DSV with Schenker, thereby raising network density and strengthening national coverage for outsourced returns programs. The United Kingdom reverse logistics market is also becoming easier to access for mid-sized retailers as shared-facility models and AI-enabled grading tools reduce the need for heavy in-house investment in returns infrastructure. The main limits remain high per-item handling costs, labor-intensive inspection work, inconsistent workflow standards, and increased exposure for operators who rely on cross-border return corridors or incomplete condition data at the point of return initiation.

Key Report Takeaways

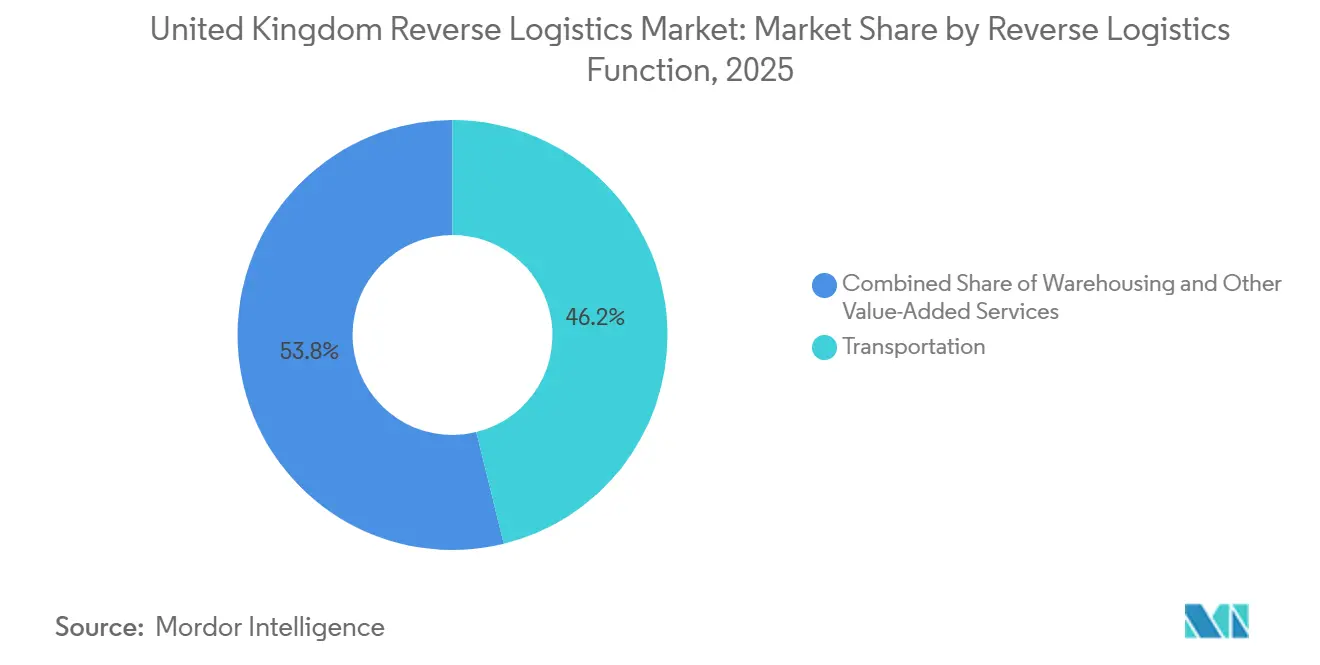

- By reverse logistics function, transportation accounted for 46.17% of the United Kingdom reverse logistics market size in 2025, while warehousing is forecast to expand at a 13.33% CAGR through 2031.

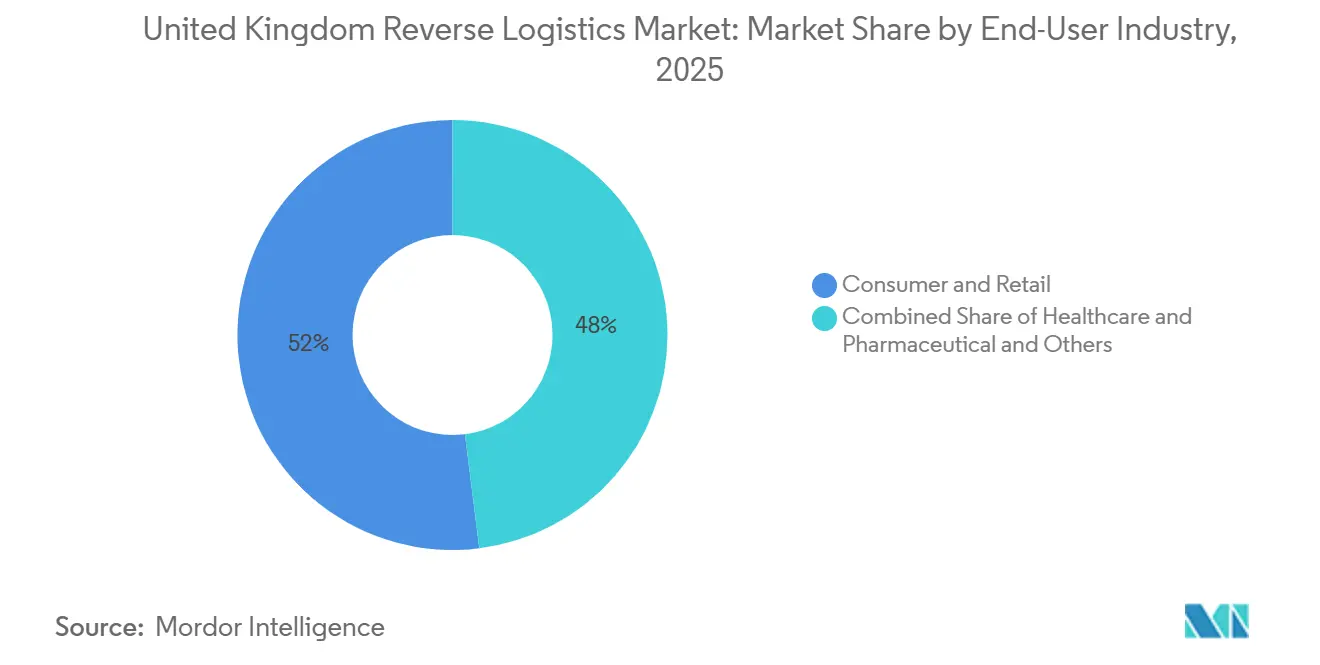

- By end-user industry, consumer and retail accounted for 51.98% of the United Kingdom reverse logistics market share in 2025, while healthcare and pharmaceuticals recorded the highest projected CAGR at 15.50% through 2031.

- By geography, England accounted for 74.28% of the United Kingdom reverse logistics market size in 2025, while Scotland is projected to grow at the fastest CAGR of 10.39% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Reverse Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-Commerce Return Volumes | +2.0% | England is dominant, with a growing impact across Scotland and Wales | Short term (≤ 2 years) |

| Retailer Push for Faster Refund Cycles | +1.1% | National, with the highest intensity in England’s dense retail corridors | Short term (≤ 2 years) |

| Regulation-Led Recovery, Repair, and Recycling Demand | +1.0% | National, strongest in England, Scotland, and Northern Ireland | Medium term (2-4 years) |

| Dense Urban Return Aggregation Networks in England | +0.8% | England-centric, with spillover to Scotland and Wales | Medium term (2-4 years) |

| Growth of Returnless Refund and Keep-It Decisioning | +0.6% | National, with early gains in the London and Manchester corridors | Short term (≤ 2 years) |

| AI-Driven Grading, Triage, and Recommerce Routing | +0.8% | National rollout, concentrated in England’s logistics hub network | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-Commerce Return Volumes

The United Kingdom reverse logistics market continues to benefit from elevated online return activity across apparel, footwear, and electronics. The United Kingdom e-commerce return rate remained near 17.5% through 2025, while fashion and footwear categories reached 30% to 40% during peak periods, keeping transport pickup and warehouse intake volumes structurally high. Returnuary 2026 alone generated GBP 1.6 billion (USD 2.14 billion) in returned goods, underscoring the continued concentration of seasonal demand in this country. A growing share of these returns comes from multi-item ordering behavior, meaning more products return in resale-ready condition and can be routed to quicker recovery channels rather than scrap or low-value clearance. That pattern supports greater spending on transport links, disposition tools, and returns platforms because each unit has stronger resale potential when the item is still new or lightly handled.

Retailer Push for Faster Refund Cycles

The United Kingdom reverse logistics market is also being shaped by retailer pressure to shorten the time between customer drop-off and refund confirmation. ASOS introduced a tiered return fee policy in January 2026, under which customers with a return rate above 70% face a GBP 4 (USD 5.35) charge unless they keep at least GBP 40 (USD 53) of goods, which shows how tightly retailers are now managing return economics[1]Source: ASOS, “ASOS Fair Use Policy,” ASOS Customer Care, asos.com. These fee changes do not remove the need to process returned items, because the product still has to move back through collection, inspection, and resale or disposal channels. Logistics providers are responding by pushing faster intake, sorting, and restocking workflows so that value is not lost while inventory sits idle. The result is a stronger demand for outsourced partners that can compress processing time from days to hours, especially in high-return categories such as fashion and consumer electronics.

Regulation-Led Recovery, Repair, and Recycling Demand

The United Kingdom reverse logistics market is gaining a more durable compliance base as recovery and recycling rules expand. The Waste Electrical and Electronic Equipment Amendment Regulations took effect on August 12, 2025. They reclassified online marketplace operators as producers of goods sold by non-United Kingdom suppliers through their platforms, thereby widening the pool of organizations that now need support for collection, treatment, recycling, and reporting. Financial obligations under that framework began in January 2026, which moved compliance from a future requirement to a current operating cost for affected platforms. Packaging EPR rules add a second layer, because disposal fees linked to recyclability create a direct incentive to document recovery outcomes and work with providers that can prove closed-loop handling. This pulls reverse logistics deeper into compliance planning and lifts demand from buyers who previously had little reason to outsource recovery operations.

Dense Urban Return Aggregation Networks in England

The United Kingdom reverse logistics market remains highly concentrated in England because dense urban collection networks make returns cheaper to aggregate and faster to move. InPost continued to expand its United Kingdom parcel locker footprint in 2025 and also began a nationwide Post Office trial, which widened access points for sending, receiving, and returning parcels outside standard store hours. Evri’s network also remained large, with around 17,000 ParcelShop and locker locations supporting national parcel access and return collection[2]Source: Evri, “Evri Delivers Record Year and Significant Investment in Customer Service,” Evri Press Release, evri.com. This density matters because the London, Birmingham, and Manchester corridor allows large volumes of returned items to be consolidated before they reach processing sites. The same network effect lowers pickup cost per item and helps explain why England keeps the largest share of the national total.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Per-Item Reverse Handling Costs | -0.9% | National, most acute in high-return fashion and electronics corridors in England | Short term (≤ 2 years) |

| Labor Intensity in Inspection and Sorting | -0.7% | National, with pressure concentrated at England’s major processing centers | Medium term (2-4 years) |

| Limited Standardization Across Returns Workflows | -0.5% | National, affecting multi-retailer and marketplace operators across all regions | Medium term (2-4 years) |

| Inconsistent Product Condition Data at Return Initiation | -0.4% | National, with particular impact on electronics and apparel routing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Per-Item Reverse Handling Costs

High per-item handling costs remain the clearest brake on the United Kingdom reverse logistics market. Every returned unit may require transport, intake, inspection, grading, repacking, and either restocking or disposal, making low-ticket goods hard to recover profitably. In high-return categories, reverse logistics spend can reach 7% of gross sales, which is enough to pressure margins for mid-tier online retailers. This is why some sellers use returnless refunds for items with low resale value, even when that means giving up product recovery entirely. The cost burden supports outsourcing in some cases, but it also limits how much retailers are willing to invest in premium returns handling for low-value goods.

Labor Intensity in Inspection and Sorting

The United Kingdom reverse logistics market still relies heavily on manual inspection, especially for damaged, multi-part, or higher-value products. Labor cost pressure in distribution centers has made that model harder to sustain since 2024, particularly during peak return periods when extra staffing is needed. Automation can reduce handling time, but the upfront cost remains high for smaller operators without the scale to justify full robotic or AI-enabled grading lines. GXO’s continued use of AI in reverse logistics shows the direction of travel, but it also highlights that advanced systems are still concentrated among larger providers[3]Source: GXO Logistics, “GXO Announces Completion of UK Regulatory Review of Wincanton Acquisition and Raises Full-Year 2025 Guidance,” GXO Investor Relations, investors.gxo.com. Until grading technology can handle a wider range of product conditions with less human oversight, labor will remain a structural cost headwind.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Reverse Logistics Function: Transportation Dominates, Warehousing Leads Growth

Transportation accounted for 46.17% of the United Kingdom reverse logistics market share in 2025, making it the largest function in the current structure of national returns activity. That leadership reflects the volume intensity of road-based collection between drop-off points, local aggregation nodes, and central returns sites. Evri’s national parcel access network and InPost’s ongoing rollout of parcel lockers and Post Office access points show why transport remains so central to the model, because every additional return touchpoint feeds collection density and line-haul demand. Transportation also absorbs a large share of operating costs because it has to connect dispersed consumers with processing hubs quickly enough to support refund expectations. The United Kingdom reverse logistics market stays road-led in this function because domestic parcel flows are dense and collection speed matters more than modal complexity for most returned goods.

Warehousing is the fastest-growing function, and the United Kingdom reverse logistics market for warehousing is projected to expand at a 13.33% CAGR through 2031. This growth is being driven by a shift from simple storage activities to multi-step returns processing within shared facilities. DHL Supply Chain’s Return Network, launched in October 2025, is built around 11 purpose-built facilities that process returns for multiple product types and customers within the same network, shortening the path from receipt to inspection and restocking. The function is gaining importance because retailers want co-located fulfillment and returns operations that can cut idle inventory time and lift recovery value. Other value-added services continue to gain ground in the mix as more returned goods are redirected to refurbishment, restocking, and recommerce channels rather than low-value disposal.

By End-user Industry: Consumer and Retail Anchors Volume, Healthcare Drives Growth

Consumer and retail accounted for 51.98% of the United Kingdom reverse logistics market size in 2025, reflecting the large share of fashion, footwear, and electronics returns in total national flows. The category remains dominant because those goods generate frequent returns and require rapid refund and disposition decisions to protect margin. Return fee adoption among major fashion brands rose sharply by January 2026, indicating the sector is trying to recover some of the cost burden rather than absorb it entirely. This does not reduce the need for physical processing, since the item still has to be collected, checked, and routed after the customer's decision is made. Home and decor, and FMCG remain smaller demand pools, but they bring their own handling pressures, as bulky items, fragile goods, and short-shelf-life products all require tighter operational control.

Healthcare and pharmaceutical is the fastest-growing end-user segments, and the United Kingdom reverse logistics market size for this segment is forecast to grow at a 15.50% CAGR through 2031. CEVA launched a dedicated maritime reverse logistics solution for used lithium-ion EV batteries in March 2026, using specially adapted containers on CMA CGM shipping lines, which points to a more structured battery return chain as EV volumes grow. The same segment is supported by remanufacturing economics, since remanufactured automotive components in the United Kingdom can sell at 40% to 60% of new-part prices while meeting the same performance standard, which keeps value recovery commercially attractive. This makes automotive growth less dependent on pure return volume and more tied to the rising value of repair, refurbishment, and regulated battery recovery.

Geography Analysis

England held 74.28% of the United Kingdom reverse logistics market share in 2025, indicating how strongly national activity is concentrated in the country’s main population and freight corridors. The region combines dense online demand, broad drop-off access, and the highest concentration of large processing facilities. Evri continued investing in capacity, including around GBP 57 million (USD 76 million) in its Barnsley Super Hub during the 2024 to 2025 period, which strengthened throughput for parcel-heavy flows. England also benefits from the closest alignment between high-street retail activity, parcel networks, and motorway freight routes, which lowers the collection cost per returned item. Those structural advantages make the region the anchor of the United Kingdom reverse logistics market and help explain why transport and warehousing providers continue to cluster capacity there.

Scotland is the fastest-growing geography in the United Kingdom reverse logistics market, with a forecast growth rate of 10.39% through 2031. Growth is being supported by circular economy planning and preparation for the Deposit Return Scheme, scheduled for October 2027 across England, Scotland, and Northern Ireland, with GBP 60 million (USD 80.80 million) in support funding confirmed for smaller retailers to install return points. Scotland is also benefiting from DSV’s post-acquisition network integration following the April 2025 Schenker deal, which supports broader contract logistics density across the United Kingsom[4]Source: DSV A/S, “DSV Completes the Acquisition of Schenker,” DSV Press Release, dsv.com. The region’s role is still smaller than England’s, but the pace of infrastructure and compliance-led demand expansion is stronger.

Wales and Northern Ireland together represent a smaller part of the national total, but both remain relevant to the broader United Kingdom reverse logistics market. Wales benefits from proximity to England’s Midlands logistics base, which lets operators serve cross-border retail flows without building fully separate infrastructure in every case. Northern Ireland faces an additional compliance layer for goods movement after Brexit, which increases documentation and classification requirements for some commercial return flows. Northern Ireland is also included in the Deposit Return Scheme planned for October 2027, which should support the establishment of new collection points and reverse handling needs as implementation approaches. Together, these regions remain smaller in scale, but both are tied closely to national policy shifts and network design decisions made elsewhere in the United Kingdom.

Competitive Landscape

The United Kingdom reverse logistics market shows low concentration. Large global groups such as DHL Supply Chain, GXO, DSV, CEVA Logistics, and Kuehne+Nagel compete on network reach, facility scale, and the ability to spread cost across many customers. One of the clearest strategic moves came from Evri and DHL eCommerce United Kingdom, whose deal won CMA approval in September 2025 and created a combined parcel and mail business with very large national volume capacity. Another major move came from DSV, which completed its Schenker acquisition in April 2025 and is integrating United Kingdom operations through 2026 to build stronger density across the Midlands and South East. These actions raise the scale threshold for competitors that want to win large outsourced returns contracts.

Technology and workflow design are now just as important as physical scale in the United Kingdom reverse logistics market. DHL’s Return Network gives retailers access to a ready-made multi-client returns platform, lowering the entry barrier for brands that do not want to invest in dedicated infrastructure. GXO’s use of AI in reverse logistics is another strong example, because it turns technology into a live operating tool for grading and routing rather than a simple positioning claim. CEVA has also moved into more specialized reverse flows through its EV battery return service, giving it a stronger position in the high-compliance, higher-value part of the chain. These moves show that the leading players are building advantage through targeted capability expansion as much as through size.

At the same time, the United Kingdom reverse logistics market still faces fragmentation pressure from specialist operators and narrower platform models. Mid-sized retailers now have greater access to shared processing, parcel locker networks, and outsourced returns tools than they did a few years ago, which limits any single provider's ability to dominate all client groups. InPost’s long-term United Kingdom investment plan and its Post Office locker trial show how out-of-home networks can expand access for both smaller merchants and large retailers. The market is therefore consolidating at the top while still leaving space for providers that solve a specific problem better than a full-service 3PL. That balance supports competition on service design, turnaround time, and recovery quality, not only on national asset ownership.

United Kingdom Reverse Logistics Industry Leaders

DHL Group

GXO Logistics, Inc.

Kuehne+Nagel International AG

CEVA Logistics (CMA CGM)

DSV A/S (incl. DB Schenker)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: CEVA Logistics launched a dedicated maritime reverse logistics solution for used lithium-ion EV batteries, operational on CMA CGM's shipping lines using 5 specifically adapted containers. The service transports used batteries from collection points to continental European recycling facilities, addressing a growing need in the United Kingdom's EV transition logistics chain.

- January 2026: DHL Group published data confirming the expansion of its DHL ReTurn Network to 11 strategically located multi-client reverse logistics facilities in North America following the January 2025 acquisition of Inmar Supply Chain Solutions, which added 14 return-processing centers. The North America model is being evaluated as a template for DHL Supply Chain's United Kingdom returns infrastructure strategy.

- September 2025: GXO and Greene King announced sustainability achievements from their long-standing United Kingdom partnership, with GXO's reverse logistics solutions eliminating over 160,000 waste collection journeys annually and recycling more than 9,000 tons of food waste and 4,000 tons of cardboard in 2024.

- May 2025: FedEx announced plans for 2 new state-of-the-art United Kingdom logistics hubs near its existing Marston Gate and Atherstone sites, consolidating from 5 road hubs to 2 purpose-built facilities, expected to be operational by 2029, each capable of sorting 32,000 packs per hour. In July 2025, FedEx opened a new 38,000 ft² facility in Manchester, followed by a 19,000 ft² dedicated freight handling facility at East Midlands Airport in September 2025.

United Kingdom Reverse Logistics Market Report Scope

| Transportation | Road |

| Air | |

| Other Modes | |

| Warehousing (Storage, Distribution, Consolidation) | |

| Other Value-added Services (Return Processing, Restocking, Refurbishment, Disposition) |

| Consumer and Retail |

| Home and Decor |

| Healthcare and Pharmaceuticals |

| FMCG |

| Other End Users |

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Reverse Logistics Function | Transportation | Road |

| Air | ||

| Other Modes | ||

| Warehousing (Storage, Distribution, Consolidation) | ||

| Other Value-added Services (Return Processing, Restocking, Refurbishment, Disposition) | ||

| By End-user Industry | Consumer and Retail | |

| Home and Decor | ||

| Healthcare and Pharmaceuticals | ||

| FMCG | ||

| Other End Users | ||

| By Geography | England | |

| Scotland | ||

| Wales | ||

| Northern Ireland |

Key Questions Answered in the Report

What is the forecast value of the United Kingdom reverse logistics market by 2031?

The United Kingdom reverse logistics market is forecast to reach USD 49.51 billion by 2031, rising from USD 34.77 billion in 2026 at a CAGR of 7.32%.

Which reverse logistics function leads in the United Kingdom right now?

Transportation is the largest function, with 46.17% share in 2025, because dense parcel collection and road-based returns movement still anchor the operating model.

Which end-user group generates the most returns activity in the United Kingdom?

Consumer and retail led the market with a 51.98% share in 2025, supported by strong returns in fashion, footwear, and electronics.

Which United Kingdom region is growing the fastest for reverse logistics activity?

Scotland is the fastest-growing geography, with a projected CAGR of 10.39% through 2031, driven by circular-economy investment and preparations for the Deposit Return Scheme.

Why are regulations becoming more important in United Kingdom returns operations?

WEEE obligations for online marketplaces and packaging EPR rules are making recovery, reporting, and recycling current compliance requirements, which is boosting demand for outsourced reverse logistics support.

How are major logistics companies changing competition in the United Kingdom?

Competition is shifting through scale deals and capability expansion, including the Evri and DHL eCommerce United Kingdom combination, DSV’s Schenker integration, and DHL’s multi-client ReTurn Network launch.

Page last updated on: