Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

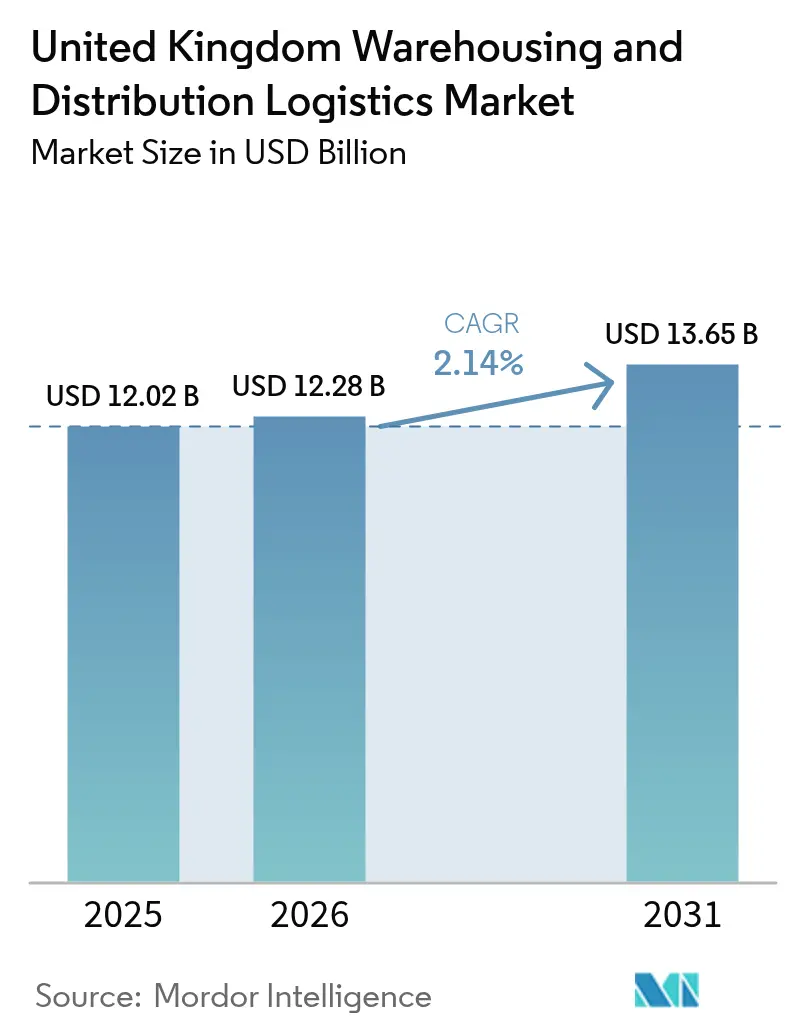

| Base Year Market Size (2025) | USD 12.02 Billion |

| Market Size (2026) | USD 12.28 Billion |

| Market Size (2031) | USD 13.65 Billion |

| Growth Rate (2026 - 2031) | 2.14% CAGR |

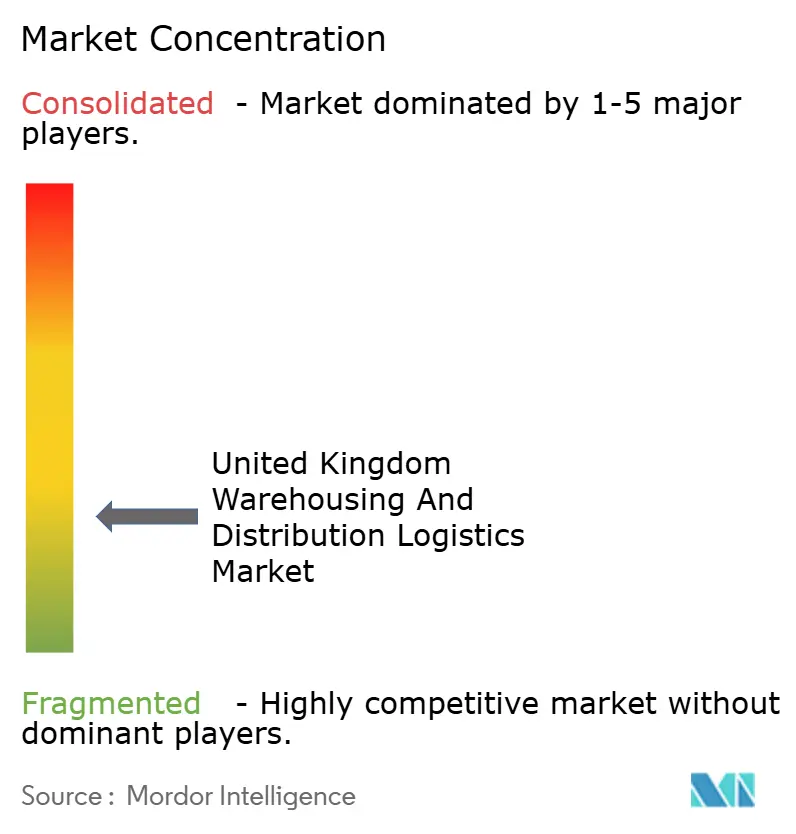

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Warehousing And Distribution Logistics Market Analysis by Mordor Intelligence

The United Kingdom Warehousing And Distribution Logistics Market size was valued at USD 12.02 billion in 2025 and estimated to grow from USD 12.28 billion in 2026 to reach USD 13.65 billion by 2031, at a CAGR of 2.14% during the forecast period (2026-2031).

Expanding e-commerce volumes, post-Brexit inventory realignments, and sustained investment in automation collectively underpin the market’s steady trajectory. Increasing demand for omnichannel fulfillment hubs near dense population centers, rising temperature-controlled storage requirements for grocery and pharmaceuticals, and government freeport incentives are reinforcing development pipelines. At the same time, land scarcity around major conurbations and labor shortages are exerting upward pressure on rents and wages, prompting faster adoption of robotics and energy-efficient designs. Consolidation among large operators allows scaling of capital-intensive technology, while mid-sized providers focus on niche services such as renewable-energy component storage to remain competitive within the United Kingdom warehousing & distribution logistics market.

Key Report Takeaways

- General Warehousing & Storage held 57.35% of the United Kingdom warehousing & distribution logistics market share in 2025, whereas Refrigerated Warehousing & Storage is advancing at a 5.22% CAGR through 2031.

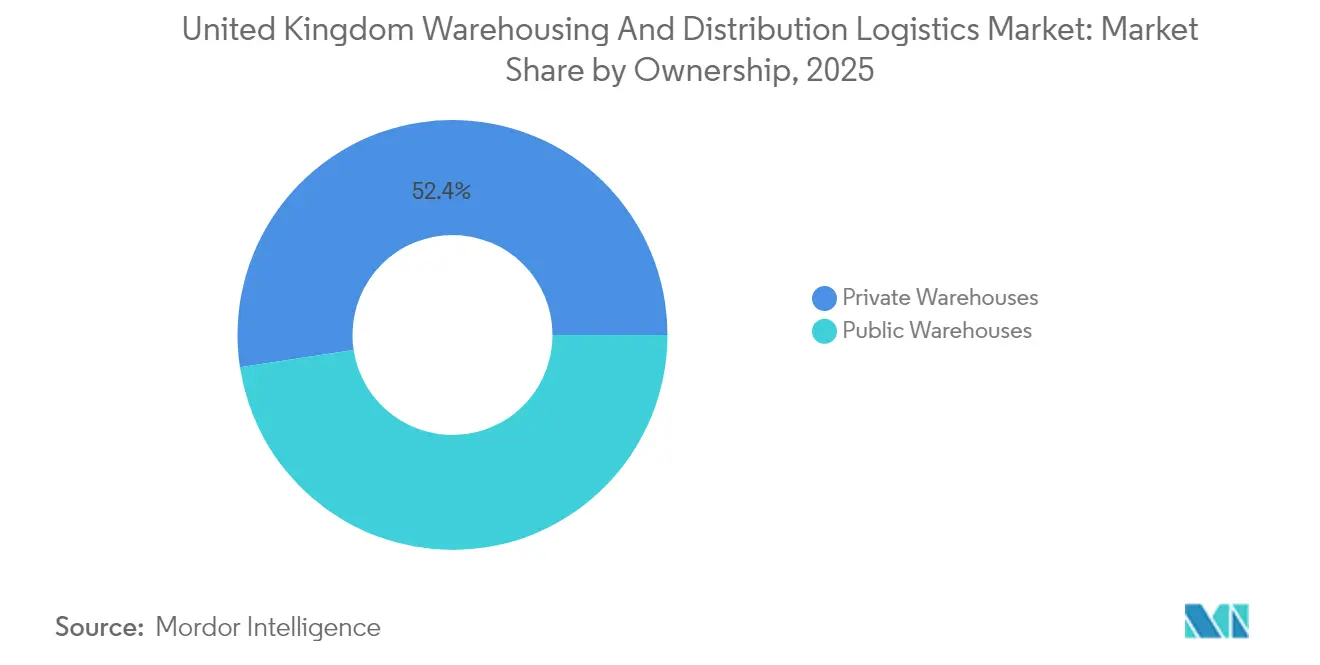

- Private Warehouses commanded 52.40% of the United Kingdom warehousing & distribution logistics market size in 2025 and will post the fastest 4.05% CAGR to 2031.

- By end-user industry, e-commerce & retail captured 23.60% revenue share in 2025, while pharma & healthcare will expand at a 4.84% CAGR during the same horizon.

- England led with 73.45% regional share in 2025; Scotland is poised for a 3.96% CAGR, the strongest within the geography segmentation.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Warehousing And Distribution Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce fulfillment space surge | +1.2% | England core, Scotland emerging | Medium term (2-4 years) |

| Cold-chain growth for grocery & pharma | +0.8% | National, London-Birmingham corridor | Long term (≥ 4 years) |

| Automation & robotics efficiency gains | +0.7% | England, Scotland industrial zones | Medium term (2-4 years) |

| Government freeport & industrial-park incentives | +0.5% | 12 designated freeport zones | Short term (≤ 2 years) |

| Re-/near-shoring of inventory post-Brexit | +0.6% | England ports, Scotland manufacturing | Long term (≥ 4 years) |

| ESG-driven brown-field redevelopment | +0.4% | Urban England, Wales industrial areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce Fulfillment Space Surge

Escalating online retail penetration has shifted network planning toward facilities located within 50 miles of the largest urban catchments. Operators prioritize multi-story hubs and micro-fulfillment annexes that compress last-mile delivery times while supporting returns processing. Amazon’s multi-year program of green-field and brown-field developments exemplifies the scale of investment, and large grocery chains now dedicate dedicated space to online picking alongside store replenishment. Extended Producer Responsibility rules for packaging, effective in 2025, add data compliance layers but simultaneously drive operational streamlining. Resulting capacity constraints in the Golden Triangle underpin premium rent growth and sustain double-digit pre-leasing rates across the United Kingdom warehousing and distribution logistics market[1]“Trade as a Driver of Innovation and Productivity,” Logistics UK, logistics.org.uk.

Cold-Chain Growth for Grocery and Pharma

Demand for temperature-controlled facilities now outpaces ambient capacity expansion as grocery home-delivery volumes converge with pharmaceutical buffer-stock strategies. Dual-use specifications capable of +4 °C chilled to -20 °C frozen enable operators to flex between sectors and smooth asset utilization. Strategic corridors linking London, Birmingham, and the eastern ports attract multi-tenant build-to-suit projects, while nationwide distribution requires satellite cross-dock nodes closer to consumers. Adoption of natural refrigerants aligns buildings with future sustainability regulation and generates operating-cost benefits once electricity-intensive systems are powered by on-site solar arrays. This specialist capability therefore commands a rental premium of 20-25% but continues to secure long-term commitments from brand-name occupiers, enhancing revenue visibility across the United Kingdom warehousing & distribution logistics market.

Automation and Robotics Efficiency Gains

Rising wage bills and the chronic 76% vacancy rate for warehouse operatives accelerate investment in goods-to-person robotics, autonomous mobile robots, and AI-enabled inventory orchestration. Ocado’s grid-based robotic system delivered over 30 million picks during 2024, demonstrating a pathway to 99.9% accuracy and sub-five-minute order cycles. Return on investment horizons have contracted to two-three years where throughput tops 150,000 picks per week, and early adopters report 25-50% productivity uplifts. As new facilities break ground, developers increasingly grade electrical capacity to support high-density automation from day one, embedding modular mezzanines and fiber backbones that future-proof buildings. These technology deployments are becoming a primary means of mitigating labor-market friction within the United Kingdom warehousing & distribution logistics market.

Government Freeport and Industrial-Park Incentives

Twelve freeports now offer streamlined customs processes, capital-allowance uplifts, and business-rate holidays, lowering entry thresholds for international traders. Forth Green Freeport couples renewable-energy benefits with automotive supply-chain clustering, reducing turnaround times for component flows into northern assembly plants. Complementary investment zones add research-and-development reliefs that attract value-added logistics operations such as light manufacturing and product customization. Although compliance procedures remain intricate, early participants unlock logistics cycle-time savings and total landed-cost efficiencies. The incentive framework effectively offsets short-term border frictions following Brexit and channels new FDI into the United Kingdom warehousing and distribution logistics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban land scarcity & rent inflation | -0.9% | London, Birmingham, Manchester cores | Short term (≤ 2 years) |

| Warehouse-labor shortages & wage spikes | -0.6% | National, acute in Southeast England | Medium term (2-4 years) |

| Grid-capacity limits for EV / automation | -0.4% | Industrial England, Scotland renewables | Medium term (2-4 years) |

| Planning-permission delays (NIMBY) | -0.3% | Urban England, suburban expansion zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urban Land Scarcity and Rent Inflation

Vacancy across prime logistics sub-markets remains below 2%, propelling rents upward by 8% annually as occupiers compete for scarce plots inside the M25 and along the M1 corridor. Developers increasingly pursue multi-story designs or repurpose obsolete big-box retail to unlock urban footprints. However, higher land outlays translate into elevated breakeven rent thresholds that smaller retailers struggle to absorb, driving polarization toward scale players. Local authorities attempt to balance employment opportunities against community concerns but retain stringent design codes to mitigate traffic and visual impact, slowing start-to-completion cycles within the United Kingdom warehousing and distribution logistics market.

Warehouse-Labor Shortages and Wage Spikes

Logistics UK surveys indicate that 76% of operators faced critical staffing gaps during 2024, even after median hourly wages rose 9% year on year. Housing affordability in the Southeast deepens recruitment difficulties, prompting employers to bus workers from peripheral towns or invest in on-site amenities. Skills shortages extend to maintenance engineers and data analysts needed for robotics upkeep and WMS optimization. Apprenticeship and reskilling programs are expanding but yield benefits only over multi-year horizons, placing near-term upward pressure on total cost to serve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Refrigerated Capacity Outpaces General Storage

Refrigerated Warehousing & Storage generated a 5.22% CAGR to 2031, comfortably ahead of the 2.14% overall growth registered by the United Kingdom warehousing & distribution logistics market size. Although General Warehousing & Storage retained 57.35% share in 2025, vacancy for high-spec cold units is virtually nonexistent, reflecting structural shifts in grocery home delivery and pharmaceutical integrity regulations. Capital intensity is higher refrigerated builds cost 40-60% more than ambient equivalents but operators pass through expenses via multi-year indexed contracts that insulate returns.

Energy-efficient chillers, IoT temperature monitoring, and modular racking improve space utilization and compliance, enabling providers to blend chilled and frozen zones on demand. Meanwhile, general warehousing leans on automation to defend margins, integrating shuttle systems and high-density pallets that reduce per-unit handling costs. Dual-certified facilities capable of toggling between cold and ambient regimes further blur segment boundaries, optimizing uptake across seasonal peaks within the United Kingdom warehousing & distribution logistics market.

By Ownership: Private Facilities Tighten Hold

Private Warehouses controlled 52.40% of the United Kingdom warehousing & distribution logistics market share in 2025 and are on course for a 4.05% CAGR, mirroring corporates’ desire for end-to-end visibility and integration. In-house management accelerates deployment of robotics and tailored WMS, supporting omnichannel flows and SKU proliferation. Public warehouses remain vital for SMEs and importers requiring flexible volume commitments, but commoditization places downward pressure on service margins.

M&A activity underscores the strategic value of private capacity; GXO’s USD 1.3 billion Wincanton transaction consolidates expertise across automotive, retail, and defense. Lease-purchase structuring, whereby occupiers take title at maturity, gains popularity as a hedge against long-term rent inflation. Conversely, REIT-owned public stock struggles to fund deep retrofits without extended lease terms, creating a bifurcated asset base inside the United Kingdom warehousing & distribution logistics market.

By End-User Industry: Healthcare Leads Premium Expansion

E-commerce & retail sustained 23.60% of 2025 demand, yet the pharma & healthcare vertical emerges as the fastest-growing at 4.84% CAGR, reflecting stricter Good Distribution Practice audits and nearshoring of vaccine and biologics manufacturing. Temperature and humidity monitoring are critical, pushing the adoption of validated digital twins and blockchain traceability. Food & beverage volumes remain high but margin pressure spurs co-location with grocery distribution to maximize cross-docking.

Automotive warehousing adapts to electric-vehicle component flows that require lithium-battery handling protocols and proximity to gigafactories. Manufacturing & engineering goods maintain steady requirements for heavy-lift capacity and secure yards. Growing renewable-energy investment adds demand for oversized turbine parts and grid-scale battery units, expanding the “Others” category. This diversification underpins stable baseline demand across the United Kingdom warehousing & distribution logistics market size.

Geography Analysis

England accounted for 73.45% of all occupied space in 2025, anchored by the “Golden Triangle” linking the M1, M6, and M42 that enables next-day delivery to 90% of UK households. Extended lead times for building permits and rail-freight network delays limit immediate capacity relief, so speculative projects secure pre-lets months before completion. London’s low vacancy pushes occupiers to Greater Essex and Kent, where supply pipelines are rising but compete with residential land uses. The cancellation of the northern HS2 leg in 2024 removed a catalyst for high-speed freight, raising concern about future inter-modal fluidity.

Scotland delivers the fastest 3.96% CAGR to 2031, stimulated by Forth Green Freeport incentives and abundant renewable-energy generation that lowers carbon intensity for cold-chain operators. Mossend International Railfreight Park enhances continental connectivity, reducing reliance on southern ports. Grant support for battery-storage and wind-turbine assembly drives specialized warehouse requirements that command premiums in the Central Belt. Wales concentrates activity around Milford Haven and Cardiff, where automotive and aerospace links draw inbound components and export flows, though labor supply remains tight.

Northern Ireland occupies a strategic interface between UK and EU regulatory zones, offering dual-market access that attracts value-added logistics services such as product customization and reverse logistics. However, customs protocols still create administrative overhead, dampening speculative development appetite. Cross-border projects with the Republic of Ireland share resources to mitigate scale limitations, gradually bolstering resilience across the wider United Kingdom warehousing & distribution logistics market.

Competitive Landscape

The market exhibits moderate concentration, signaling ample room for specialist and regional players. GXO’s absorption of Wincanton enriches its sector breadth and unlocks GBP 45 million (57.28 million) in annual synergies around automation procurement and network optimization. DHL, Kuehne + Nagel, and CEVA leverage global procurement strength to roll out standardized WMS platforms and sustainability features such as LED retrofits and electric shunter fleets.

Technology is the main competitive differentiator. Ocado licenses its proprietary robotic grid to third-party grocers as a service, while Amazon extends its European “multi-node” inventory algorithm to UK sellers, compressing delivery promise windows without ballooning stock levels. Mid-tier operators respond by partnering with software specialists to deploy plug-and-play autonomous mobile robots on a subscription basis. ESG credentials increasingly tip bidding contests; Prologis and SEGRO both market on-site solar generation and biodiversity offsets to secure blue-chip tenants.

Disruption risk persists as parcel networks integrate lockers and micro-depots that bypass central warehousing for fast-moving SKUs. At the same time, institutional investors pile into prime sheds seeking defensive yields, lifting acquisition multiples to record highs. This influx encourages sale-and-leaseback transactions that recycle capital back into automation, thereby reinforcing competitive moats across the United Kingdom warehousing & distribution logistics market[3]“Border Target Operating Model,” UK Government, gov.uk.

United Kingdom Warehousing And Distribution Logistics Industry Leaders

DHL Supply Chain

Kuehne + Nagel

GXO Logistics

CEVA Logistics

DSV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: DHL eCommerce UK merged with Evri, creating an extended parcel network capable of challenging national incumbents.

- April 2025: InPost completed the acquisition of Yodel, instantly becoming the country’s third-largest courier service.

- March 2025: Amazon unveiled a further GBP 8 billion (USD 10.18 billion) commitment to UK logistics and cloud facilities for the next five years.

- January 2025: The UK government enforced new Entry Summary data rules for inbound freight, elevating compliance demands for carriers.

United Kingdom Warehousing And Distribution Logistics Market Report Scope

Warehousing is one of the most important parts of this rapidly growing industry. It is mainly about storing goods that are going to be moved, either in or out.Distribution has to do with managing the flow of goods between where they are made and where they are used.The core objective of the warehouse and distribution logistics sector is to send the right product to the right destination on time, on budget, and with end-to-end visibility.

The UK warehousing and distribution logistics market is split up by end user, which includes manufacturing, consumer goods, food and beverage, retail, healthcare, and other end users. For all of the above segments, the report gives market size and forecasts in terms of value (in USD billion) for the UK warehousing and distribution logistics market.

By Warehouse Type (Value)

| General Warehousing and Storage |

| Refrigerated Warehousing and Storage |

By Ownership (Value)

| Private Warehouses |

| Public Warehouses |

By End-User Industry (Value)

| E-commerce and Retail |

| Food and Beverage |

| Pharma and Healthcare |

| Automotive |

| Manufacturing and Engineering Goods |

| Others |

By Region

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Warehouse Type (Value) | General Warehousing and Storage |

| Refrigerated Warehousing and Storage | |

| By Ownership (Value) | Private Warehouses |

| Public Warehouses | |

| By End-User Industry (Value) | E-commerce and Retail |

| Food and Beverage | |

| Pharma and Healthcare | |

| Automotive | |

| Manufacturing and Engineering Goods | |

| Others | |

| By Region | England |

| Scotland | |

| Wales | |

| Northern Ireland |

Key Questions Answered in the Report

How large is the United Kingdom warehousing & distribution logistics market in 2026?

The sector is valued at USD 12.28 billion in 2026, and it is forecast to grow at a 2.14% CAGR to 2031.

Which warehouse type is expanding fastest?

Refrigerated Warehousing and Storage is growing at 5.22% CAGR thanks to grocery home delivery and pharmaceutical demand.

Why are private warehouses gaining share?

Corporations seek tighter supply-chain control and faster automation rollouts, giving Private Warehouses 52.40% share in 2025 and a projected 4.05% CAGR.

Which region offers the highest growth potential?

Scotland leads with a 3.96% CAGR through 2031, supported by the Forth Green Freeport and renewable-energy investments.

What is the key technology trend shaping competitiveness?

Robotics and AI-driven automation deliver 25-50% productivity gains and are shortening return-on-investment periods to under three years.

How is sustainability influencing warehouse development?

Developers retrofit brown-field sites with rooftop solar, LED lighting, and low-carbon refrigerants to meet tenant ESG targets and secure long leases.

Page last updated on: