Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

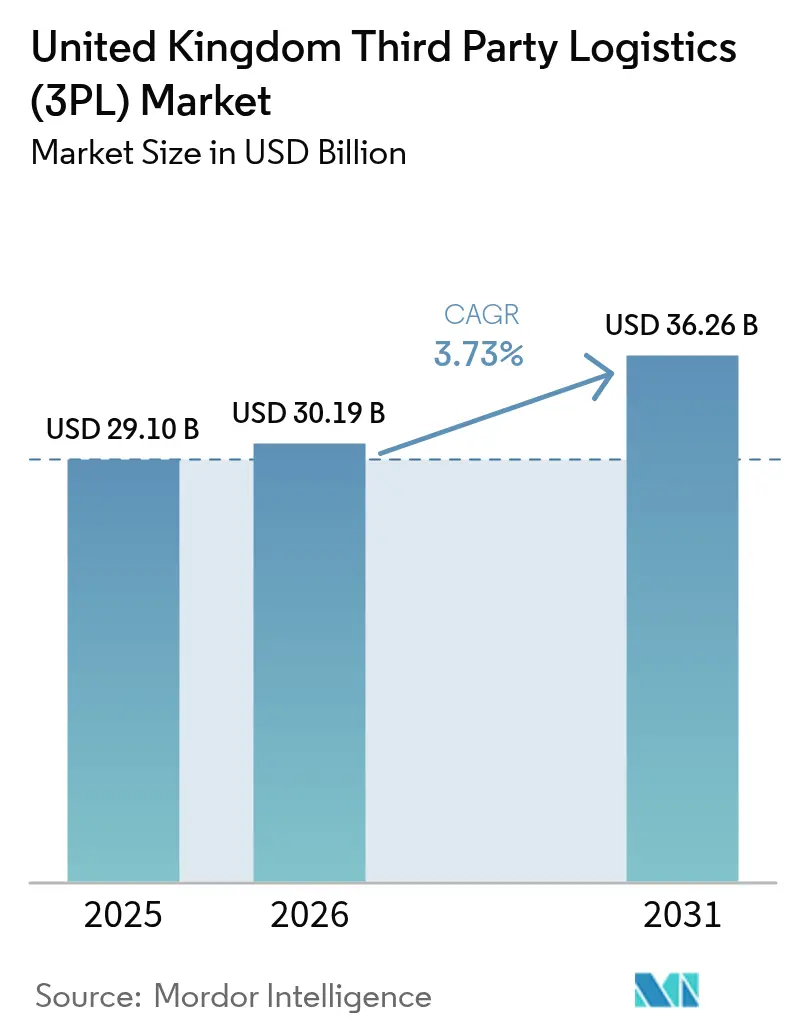

| Base Year Market Size (2025) | USD 29.10 Billion |

| Market Size (2026) | USD 30.19 Billion |

| Market Size (2031) | USD 36.26 Billion |

| Growth Rate (2026 - 2031) | 3.73% CAGR |

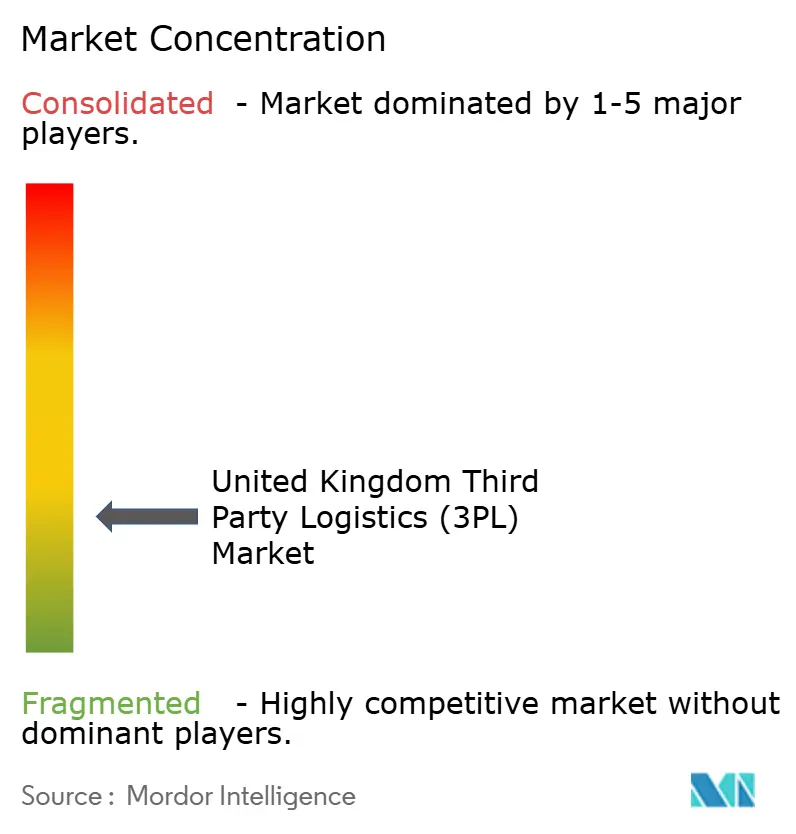

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Third Party Logistics (3PL) Market Analysis by Mordor Intelligence

The United Kingdom Third Party Logistics Market size is expected to grow from USD 29.10 billion in 2025 to USD 30.19 billion in 2026 and is forecast to reach USD 36.26 billion by 2031 at 3.73% CAGR over 2026-2031.

The market size trajectory reflects the sector’s gradual move from rapid expansion to steady maturation, shaped by Brexit-related customs friction, a deepening e-commerce culture, government decarbonization mandates, and persistent labor shortages. Businesses are migrating toward outsourced logistics partners because 3PLs can absorb regulatory shocks, aggregate technology investments, and deliver lower-carbon transport options at scale. Competitive intensity is rising as international players buy local specialists to secure port access and urban warehousing footprints, while domestic firms counter with automation and electric-fleet rollouts. Infrastructure upgrades across roads, rail, and truck stops provide new capacity yet also pressure operators to meet rising service expectations in direct-to-consumer fulfillment. Together, these forces underpin a market where resilience and flexibility determine long-term success.

Key Report Takeaways

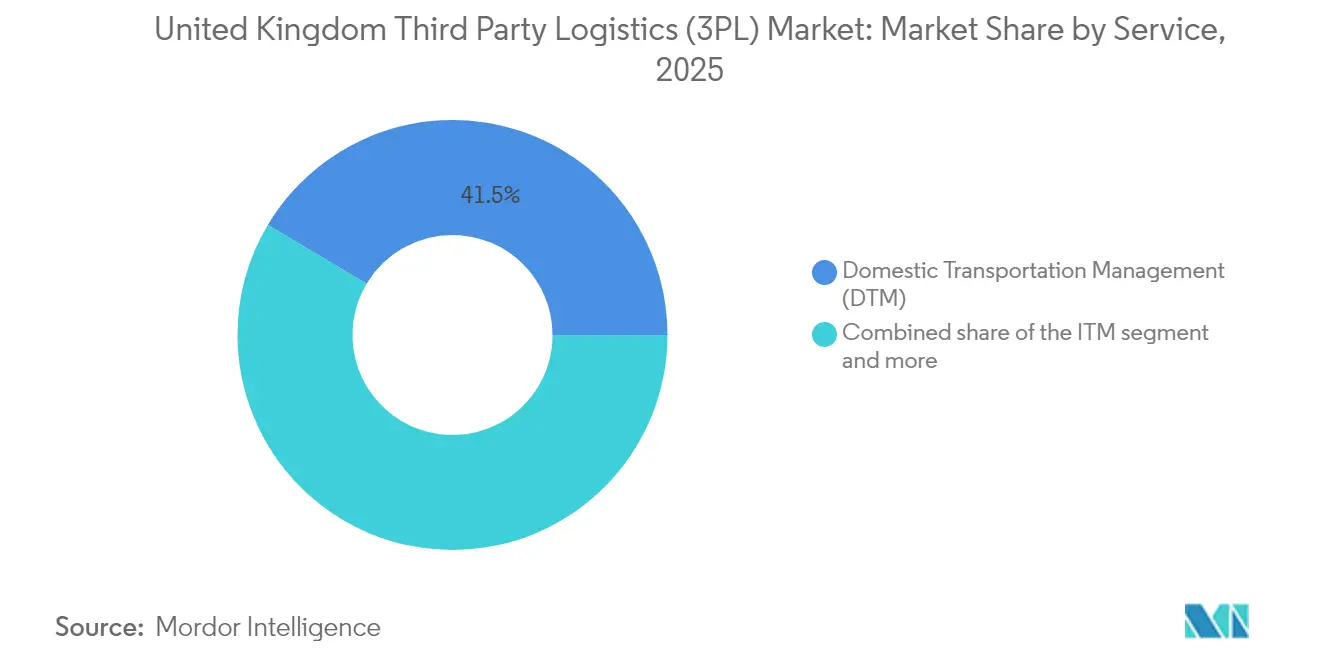

- By service, Domestic Transportation Management held 41.45% of the United Kingdom third-party logistics market share in 2025. At the same time, Value-Added Warehousing & Distribution is projected to post a 7.01% CAGR between 2026-2031, the fastest among service categories.

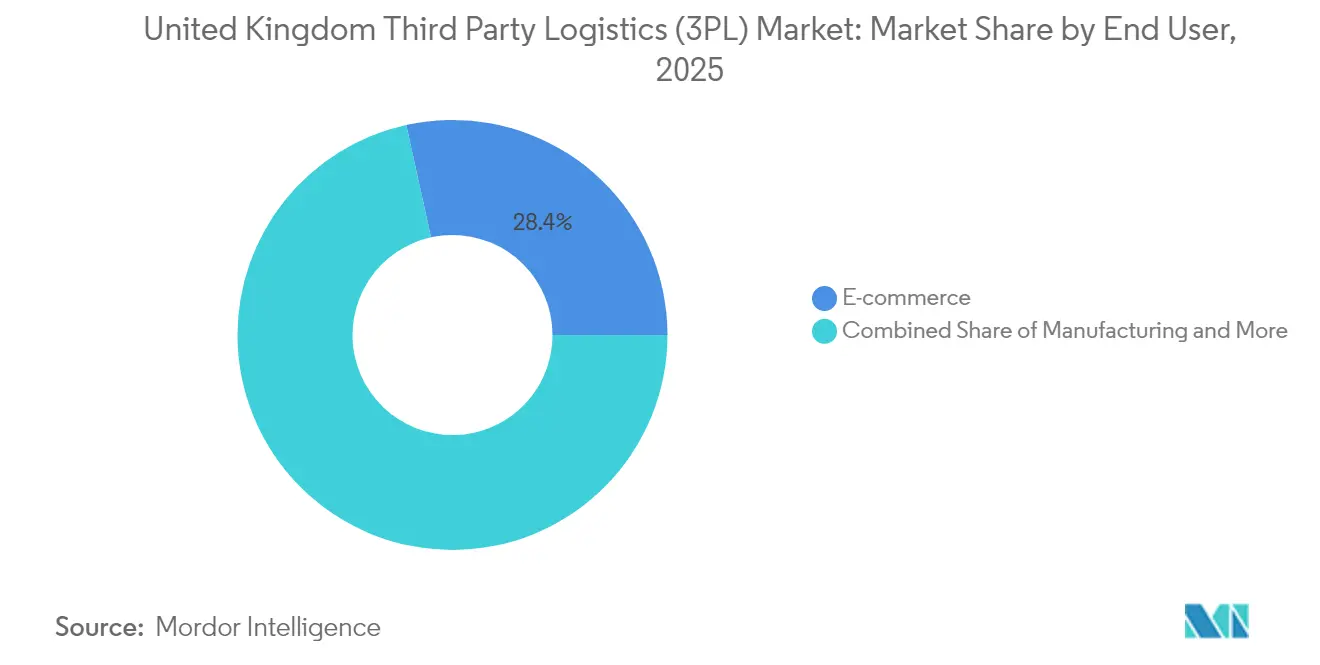

- By end user, E-commerce accounted for 28.45% of the United Kingdom third-party logistics market size in 2025 and is advancing at a 7.50% CAGR through 2031.

- By logistics model, Asset-Light operators captured 47.52% market share in 2025, while Hybrid models are on track for an 7.86% CAGR to 2031.

- By region, England dominated with a 68.90% share in 2025; Scotland is the fastest-growing geography at a 4.70% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Third Party Logistics (3PL) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive e-commerce parcel volumes | +1.2% | England dominant, Scotland emerging | Medium term (2-4 years) |

| Government decarbonization incentives | +0.8% | National, strongest in London and Manchester | Long term (≥ 4 years) |

| Warehouse automation & robotics adoption | +0.6% | England core, spill-over to Scotland | Medium term (2-4 years) |

| Post-Brexit near-shoring & customs 3PL need | +0.5% | England ports, Northern Ireland border | Short term (≤ 2 years) |

| Subscription D2C micro-fulfillment demand | +0.4% | England urban centers, Scotland cities | Medium term (2-4 years) |

| Product-security legislation | +0.3% | National, focus on England manufacturing clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive E-commerce Parcel Volumes

Online retail now represents 30% of all U.K. shopping. Rapid ordering frequencies compel 3PLs to enlarge urban micro-fulfillment footprints, evidenced by Amazon’s Project Juniper network that cuts delivery windows to hours. DPD Group UK has already completed more than 2,500 autonomous last-mile deliveries in Milton Keynes, proving robotics can meet commercial service-level agreements. London’s Portal Way hosts 260 dark kitchens that illustrate how quick-commerce models reshape warehousing demand. As retailers favor omnichannel fulfillment, operators that marry B2B distribution with direct-to-consumer parcel flows secure higher contract values and longer tenures.

Government Decarbonization Incentives for Freight

The government has earmarked USD 254 million for zero-emission HGV trials and set a 2040 deadline for phasing out new diesel trucks. Early movers gain bidding advantages; HIVED expanded its fully electric middle-mile fleet by ordering 11 Mercedes-Benz eActros units with 600 kWh batteries capable of 310-mile ranges[1]Alex Chisholm, “Future of Freight Plan,” Department for Transport, gov.uk. A further USD 20.96 million upgrade of 38 truck stops introduces high-capacity chargers and improved driver amenities, lowering range-anxiety barriers for electric haulage. Cold-chain transport emits 14.1 MtCO₂e annually, making temperature-controlled electrification a regulatory priority. ISO 14001 certification is becoming table stakes in public-sector tenders, thereby rewarding 3PLs that invest early in sustainable assets[2]Grant Shapps, “Transport Decarbonisation Plan,” Department for Transport, gov.uk.

Warehouse Automation & Robotics Adoption

More than 85% of U.K. warehouses are expected to deploy automation by 2030, while 79% of manufacturers plan generative-AI pilots in 2025. Wincanton’s VersaTile solution in Northampton lifts pick rates five times without sacrificing layout flexibility. Government AI grants average USD 48,000 per logistics project, and initiatives such as Robok’s SeeGul tracking platform receive funding to streamline yard operations. Culina Group invested USD 2.54 million in a chilled consolidation center that blends robotics with multi-temperature zones to cut waste and labor dependency. Automation helps 3PLs manage the 83% of retailers that expect order-volume growth while dealing with acute labor shortages[3]John Smith, “Wincanton PLC FY-2024 Results Presentation,” Wincanton Investor Relations, wincanton.co.uk.

Post-Brexit Near-Shoring & Customs-Integrated 3PL Demand

Fifty-eight percent of manufacturers now reshore segments of production, driving warehouse and domestic freight demand. The Border Target Operating Model adds health certificates for animal products, creating extra paperwork that favors 3PLs with in-house customs clearance. Wincanton licensed Zeus cargo-management technology to digitalize brokerage across modes. Average border delays of four to 55 hours cost shippers USD 596.9 million annually, accelerating migration to providers offering guaranteed transit slots. As the Single Trade Window becomes mandatory, specialized compliance talent becomes a gating factor, which entrenches established operators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Driver & warehouse-labor shortage | -0.7% | National; most acute in London and Manchester | Short term (≤ 2 years) |

| Brexit-related customs friction & paperwork | -0.4% | England ports; Northern Ireland border | Medium term (2-4 years) |

| HGV-charging & grid-capacity limits | -0.3% | National; dense corridors in England | Long term (≥ 4 years) |

| Logistics-property tax rise (post-2026) | -0.2% | Prime English sites and emerging Scottish hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Driver & Warehouse-Labor Shortage

The country is short 50,000 HGV drivers, with supply at 320,000 against demand for 370,000, limiting the expansion pace of the United Kingdom's third-party logistics market. The average driver age is 51, and 55% are within 50-65, signaling worsening attrition. Labor costs absorb more than 40% of 3PL operating spend and rose sharply after 19% of firms reported vacancies in early 2024. A USD 20.96 million fund to modernize 38 truck stops aims to improve job attractiveness, yet high housing costs in London and Manchester deter recruits. Warehouse labor gaps compound the issue as EU workers depart post-Brexit, pushing 3PLs toward robots and AI-driven slotting.

Brexit-Related Customs Friction & Paperwork

Additional border formalities cost government agencies USD 5.97 billion and firms USD 596.9 million each year. The final application of sanitary and phytosanitary checks has been delayed to July 2025, prolonging uncertainty that stalls big-ticket customs-infrastructure investments. Some EU haulers refuse U.K. lanes after 55-hour wait incidents, reducing cross-Channel capacity. Fragmented professional qualification rules complicate the hiring of customs brokers and aircraft engineers. Groupage loads face higher inspection rates, increasing operating risk for mixed-commodity consolidators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Warehousing Drives Future Growth

The United Kingdom's third-party logistics market size attributable to Domestic Transportation Management stood at 41.45% share in 2025, mirroring the island nation’s road-centric freight patterns. International Transportation Management remains critical for cross-border trade but wrestles with customs-driven volatility that depresses margins. Value-Added Warehousing & Distribution is accelerating at 7.01% CAGR as e-commerce clients outsource high-touch pick-pack, returns, and kitting tasks. Automated storage systems, climate-controlled chambers, and integrated customs areas turn warehouses into revenue-rich nodes rather than cost centers. Government road and rail upgrades worth USD 116.8 billion unlock intermodal plays, but the United Kingdom's third-party logistics market share for roads stays dominant through 2031 because urban consumption clusters hug motorway spines. Rail and short-sea players niche into renewable-energy projects requiring oversized-cargo moves, complementing rather than displacing trucking.

Growing enterprise reliance on warehousing has re-shaped contract structures. Clients demand variable-cost pricing tied to order lines, which suits the scalable nature of robotic picking. Cold-chain facilities earn premiums as climate-sensitive food and pharmaceutical flows expand. As automation compresses labor needs, operators redeploy headcount into value-added configuration and quality-check tasks. 3PLs that layer predictive analytics on inventory get preferred-supplier status, reinforcing consolidation trends.

By End User: Retail Dominance Accelerates

E-commerce contributed 28.45% to the United Kingdom third-party logistics market size in 2025 and is advancing at a 7.50% CAGR as online penetration deepens. Shoppers expect next-day or same-day drop windows, forcing retailers to rely on 3PLs with national node coverage and micro-fulfillment pods. Manufacturing volumes soften under Brexit-linked material delays, yet high-value assemblies shift back onshore, benefiting 3PLs offering kitting and final-stage sub-assembly. Energy & Utilities logistics rise on renewable component flow, notably tower sections and nacelles for offshore wind. Life Sciences stay resilient thanks to stringent temperature and chain-of-custody demands, spawning premium revenue per pallet.

Technology-electronics and automotive flows confront semiconductor and battery supply constraints. 3PLs with secured Asia-U.K. capacity and dangerous-goods accreditation enjoy a moat. Consumer goods remain staple cargo but grapple with promotional spikes that reward flexible 3PL labor and yard-management systems. Food & Beverage verticals navigate new import checks on animal and plant products; expert customs clearance, bonded storage, and sanitary unit loads distinguish capable providers.

By Logistics Model: Hybrid Approaches Gain Traction

Asset-light management contracts represented 47.52% of the United Kingdom third-party logistics market share in 2025 because shippers value variable cost structures. Hybrid models, blending owned fleets or sheds with brokered capacity, grow fastest at 7.86% CAGR as clients seek service security amid driver shortages and property scarcity. Asset-heavy providers bear rising real-estate taxes and decarbonization capex, yet still serve customers needing guaranteed peak-season capacity and specialized rigs. GXO’s USD 1.23 billion purchase of Wincanton marks a pivot toward scale synergies and integrated technology stacks. Meanwhile, digital freight platforms lower entry barriers for asset-light startups by aggregating small haulers.

Artificial-intelligence route optimizers boost asset-light velocity, allowing trucks to perform more drops per shift. Hybrids leverage shared electric-fleet hubs while bulking up control tower data. As battery truck availability improves, hybrids may reach cost parity with diesel fleets, extending their advantage over pure brokers.

Geography Analysis

England accounted for 68.90% of 2025 revenue within the United Kingdom third-party logistics market. Its dense consumer base, the ports of Felixstowe, Southampton, and London Gateway, and distribution clusters around the Midlands Triangle make it the default hub. Government transport funding of USD 116.8 billion across 50 projects, including the A66 Northern Trans-Pennine upgrade and Portishead rail reopening, enhances corridor speed. London wrestles with congestion and high land costs, yet leads in electric cargo-bike pilots and rooftop drone testbeds. Manchester and Birmingham consolidate inland container flows; tram extensions improve last-mile reach into city centers. The southeast manages Dover and Channel Tunnel freight despite 4-55-hour queue-time volatility.

Scotland is the fastest-growing slice at a 4.70% CAGR to 2031, fueled by USD 3.81 million rail-capacity upgrades at the Port of Grangemouth and offshore-wind turbine staging demand. Glasgow and Edinburgh anchor fulfillment for the Highlands and Islands, where rugged geography necessitates multimodal solutions. The region’s logistics renaissance aligns with national goals to double onshore wind by 2030, creating outsized heavy-lift and abnormal-load flows.

Wales provides strategic land bridges to Ireland; M4 corridor improvements reduce congestion and trim Cardiff-to-London haul times. Port of Holyhead leverages roll-on roll-off traffic for Irish trade. Northern Ireland operates under dual regulatory frameworks, raising customs complexity that entrenches incumbents familiar with both U.K. and EU rules. Renewable-energy components arrive through Belfast Harbor before distribution across the island, offering niche opportunities for specialized rigging and escort services.

Competitive Landscape

The United Kingdom's third-party logistics market is fragmented. GXO, MSC-Medlog, Kuehne+Nagel, DHL Supply Chain, and DPD Group collectively hold close to 50% of sector revenue. The GXO-Wincanton deal adds chemical, grocery, and defense accounts to GXO’s European network and enhances automation depth. MSC’s capture of Maritime Transport secures inland haulage for the group’s ocean-carrier volumes, tightening its port-to-door control. Kuehne+Nagel reported 15% revenue growth in Q1 2025 after directing AI-enabled optimization toward renewable-energy projects.

New entrants challenge incumbents on sustainability. HIVED positions its fully electric fleet as a turnkey zero-carbon service and plans megawatt chargers at hubs in London, the Midlands, and Manchester. Zendbox grew 300% in 2023 by pairing biodegradable packaging with same-day handover cut-offs for Shopify merchants. Technology adoption is the prime battleground; 85% of warehouses are forecast to automate by 2030, and 34% of logistics players invest in AI route selection. Compliance remains a moat: ISO 14001 and border-inspection certifications demand time and capital, limiting smaller challengers.

Incumbents diversify by sector specialization, moving into cold-chain automation, aerospace kitting, and customs-brokerage platforms to lock clients into broader service bundles. The U.K. Competition and Markets Authority’s Phase 2 review of the GXO-Wincanton tie-up illustrates regulator vigilance to ensure service choice. Nonetheless, rising capex for electric fleets, robotics, and property taxes favor scale players who amortize investments across multi-client campuses.

United Kingdom Third Party Logistics (3PL) Industry Leaders

DHL Supply Chain

Kuehne + Nagel

GXO Logistics

FedEx

UPS Supply Chain Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: HIVED ordered 11 Mercedes-Benz eActros trucks and confirmed megawatt charger installations at London, Midlands, and Manchester hubs, expanding the country’s first fully electric middle-mile network.

- September 2024: MSC subsidiary Medlog completed the purchase of Maritime Transport, the nation’s largest haulier, bolstering integrated port-to-door capacity.

- April 2024: GXO launched its USD 1.23 billion bid for Wincanton; a Phase 2 investigation opened in Jan 2025 to assess competitive impacts.

- March 2024: The government invested USD 20.96 million to upgrade 38 truck stops with secure parking, sanitation, and high-capacity EV chargers to ease driver shortages.

United Kingdom Third Party Logistics (3PL) Market Report Scope

Third-party logistics (3PL) services help organizations to focus on their core business and generate high revenue by reducing operating costs. These services also offer value addition to companies for the entire supply chain process, resulting in an efficient and effective supply chain. The main survival factors of the third-party logistic market include the cost-efficiency of services, company control, and technological advances. The United Kingdom Third Party Logistics (3PL) Market is segmented by Service (Domestic Transportation Management, International Transportation Management, and Value-added Warehousing and Distribution) and by End Users (Manufacturing and Automotive, Oil and Gas and Chemicals, Distributive Trade (Wholesale and Retail Trade including E-commerce), Pharmaceuticals and Healthcare, Construction, and Other End Users). The report offers the market sizes and forecasts for the United Kingdom Third Party Logistics (3PL) Market in value (USD) for all the above segments.

By Service

| Domestic Transportation Management (DTM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| International Transportation Management (ITM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| Value-Added Warehousing & Distribution (VAWD) |

By End User

| Automotive |

| Energy & Utilities |

| Manufacturing |

| Life Sciences & Healthcare |

| Technology & Electronics |

| E-commerce |

| Consumer Goods & FMCG |

| Food & Beverages |

| Others |

By Logistics Model

| Asset-Light (Management-Based) |

| Asset-Heavy (Own Fleet & Warehouses) |

| Hybrid |

By UK Region

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Service | Domestic Transportation Management (DTM) | Roadways |

| Railways | ||

| Airways | ||

| Waterways | ||

| International Transportation Management (ITM) | Roadways | |

| Railways | ||

| Airways | ||

| Waterways | ||

| Value-Added Warehousing & Distribution (VAWD) | ||

| By End User | Automotive | |

| Energy & Utilities | ||

| Manufacturing | ||

| Life Sciences & Healthcare | ||

| Technology & Electronics | ||

| E-commerce | ||

| Consumer Goods & FMCG | ||

| Food & Beverages | ||

| Others | ||

| By Logistics Model | Asset-Light (Management-Based) | |

| Asset-Heavy (Own Fleet & Warehouses) | ||

| Hybrid | ||

| By UK Region | England | |

| Scotland | ||

| Wales | ||

| Northern Ireland | ||

Key Questions Answered in the Report

What is the current value of the United Kingdom's third-party logistics market?

The market is worth USD 30.19 billion in 2026 and is projected to reach USD 36.26 billion by 2031.

Which service segment is expanding fastest within the U.K. 3PL?

Value-Added Warehousing & Distribution is growing at a 7.01% CAGR through 2031, driven by e-commerce fulfillment needs.

How big is the E-commerce share of the U.K. 3PL demand?

E-commerce accounts for 28.45% of sector revenue and posts the highest end-user CAGR at 7.50%.

Why are hybrid logistics models gaining traction?

Shippers want the flexibility of asset-light contracts but also guaranteed capacity, prompting an 7.86% CAGR for hybrid models through 2031.

Page last updated on: