Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

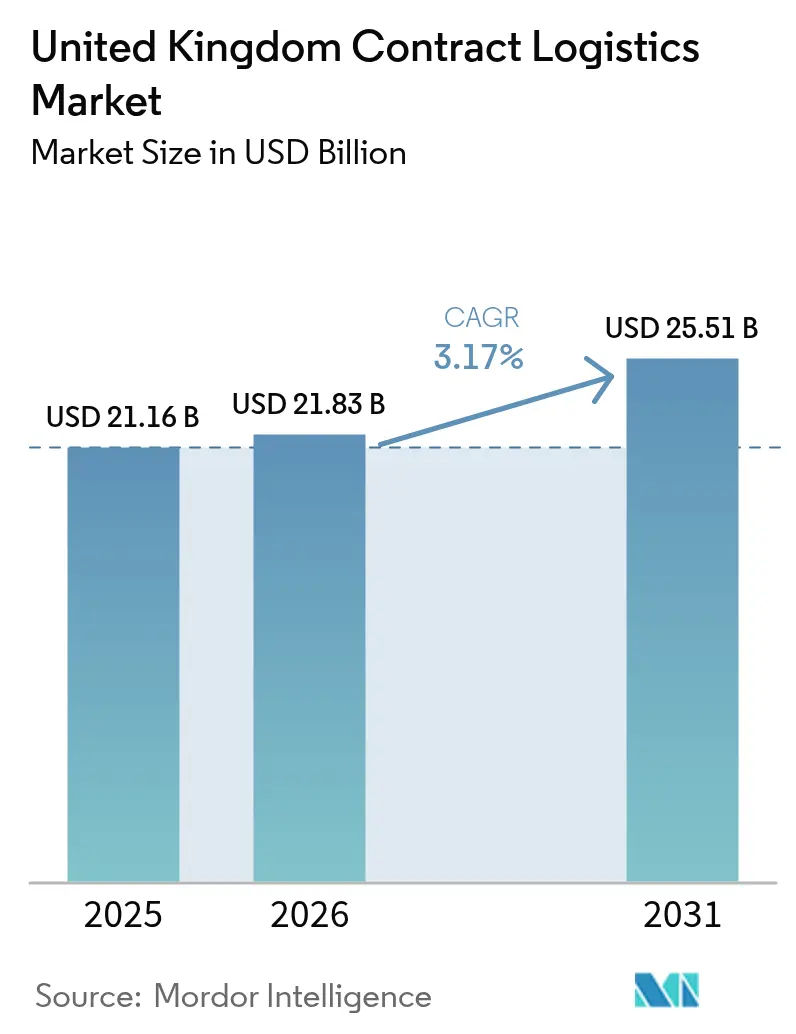

| Base Year Market Size (2025) | USD 21.16 Billion |

| Market Size (2026) | USD 21.83 Billion |

| Market Size (2031) | USD 25.51 Billion |

| Growth Rate (2026 - 2031) | 3.17% CAGR |

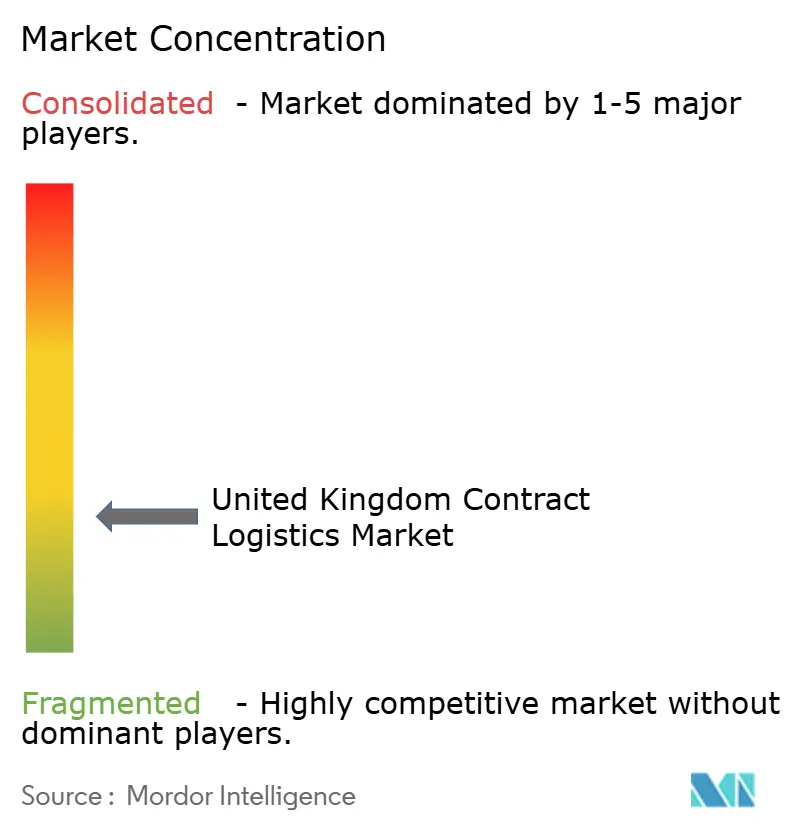

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Contract Logistics Market Analysis by Mordor Intelligence

The United Kingdom Contract Logistics Market size market size in 2026 is estimated at USD 21.83 billion, growing from 2025 value of USD 21.16 billion with 2031 projections showing USD 25.51 billion, growing at 3.17% CAGR over 2026-2031.

Persistent e-commerce demand, infrastructure modernization programs, and new customs requirements after Brexit underpin this growth trajectory. Transportation services retain a commanding position because retailers and manufacturers still rely on road and rail links even as deep-sea imports rise. Value-added services are expanding fastest as shippers outsource labeling, kitting, and near-production tasks to reduce cost and complexity. Extended contract durations gain favor because companies want stable partners able to navigate new border formalities and invest in automation. Regionally, England’s Golden Triangle benefits from major warehouse projects, while Scotland captures the strongest growth by aligning new rail investments with renewable energy supply chains. Consolidation among global integrators such as GXO, DSV, and DHL is changing competitive dynamics and accelerating technology adoption across operations.

Key Report Takeaways

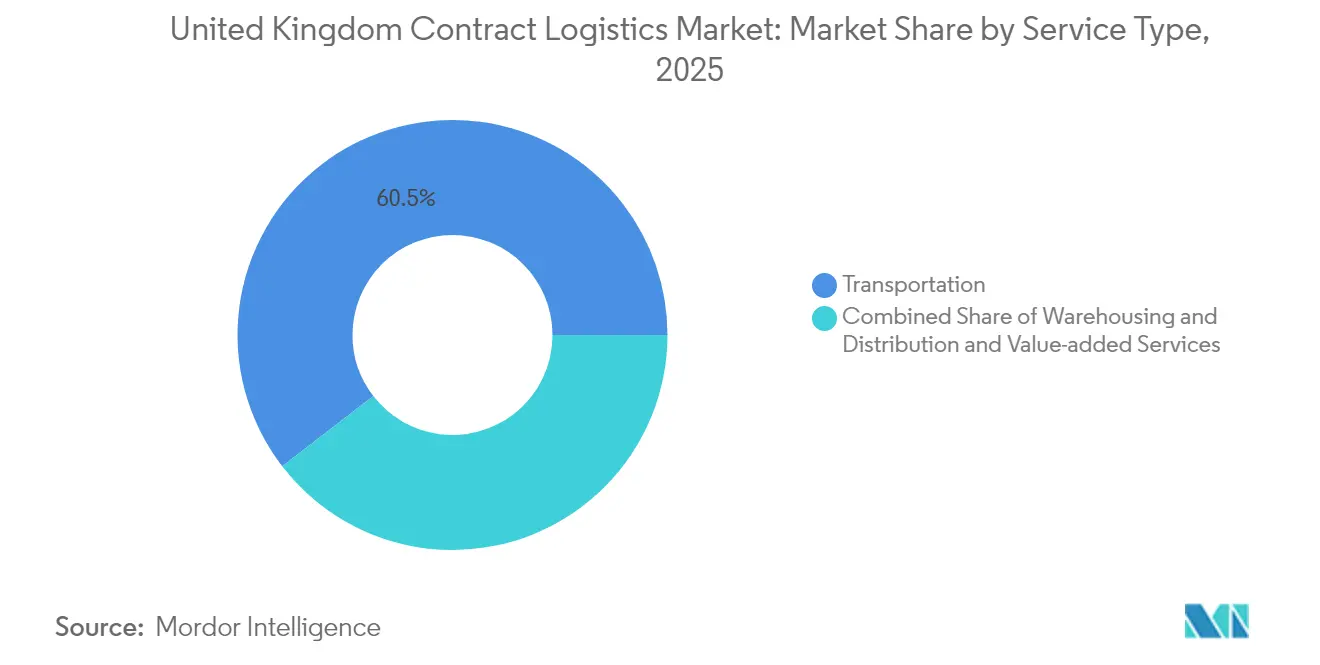

- By service type, transportation led with 60.45% of the United Kingdom contract logistics market share in 2025, while value-added services are advancing at a 3.28% CAGR through 2031.

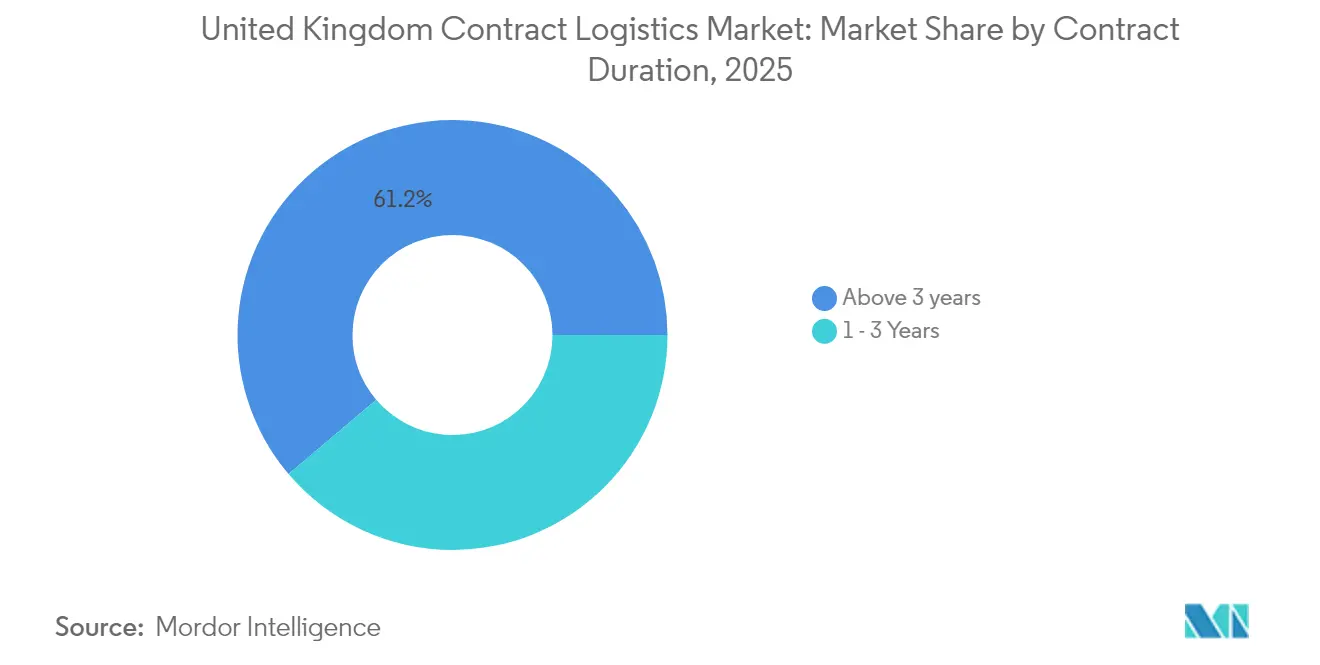

- By contract duration, agreements above three years commanded a 61.20% share of the United Kingdom contract logistics market size in 2025 and are projected to expand at a 3.82% CAGR between 2026 and 2031.

- By end-user industry, retail and e-commerce held 28.60% revenue share in 2025, whereas healthcare and pharmaceuticals are rising at a 4.15% CAGR to 2031.

- By region, England accounted for an 82.60% share of the United Kingdom contract logistics market size in 2025, while Scotland is set to grow at a 3.49% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Contract Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce parcel surge | +0.8% | England urban centers | Short term (≤ 2 years) |

| Warehouse automation and digital twins | +0.6% | England and Scotland manufacturing hubs | Medium term (2-4 years) |

| End-to-end supply-chain visibility demand | +0.5% | National, Brexit-driven urgency | Short term (≤ 2 years) |

| Post-Brexit customs brokerage integration | +0.4% | England ports and Northern Ireland border | Medium term (2-4 years) |

| Retailer micro-fulfilment outsourcing | +0.3% | London, Manchester, Birmingham metros | Long term (≥ 4 years) |

| Cold-chain expansion for pharma and food | +0.3% | National pharmaceutical clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce Parcel Surge Accelerates Fulfilment Infrastructure Demand

Online retail volumes have pushed parcel networks to add urban microhubs and larger automated fulfillment centers. Amazon’s announced USD 50 billion UK investment through 2027 funds four new regional facilities that shorten last-mile distances. Pilot microhubs in London removed up to 12 diesel vans per day and cut 4,186 kg CO₂ in nine months, proving both commercial and environmental value. Localized fulfillment spending could top USD 5.5 billion by 2030 as grocery and fashion chains outsource the task to 3PL specialists. Faster cycle times are becoming a decisive service benchmark, prompting contract logistics providers to expand same-day capabilities. As parcel density grows, the United Kingdom contract logistics market responds by optimizing urban routes and investing in electric delivery fleets to meet city emission rules.

Warehouse Automation Integration Transforms Operational Efficiency

Robotics, AI, and digital twins are now central to warehouse design. Ocado’s Luton site illustrates the shift, with robotic arms already handling 15% of items and targeting 70% within a few years. Government AI grants averaging USD 38,315 per logistics firm underscore national priorities for automation. Digital-twin platforms allow continuous monitoring of space utilization and process flows, cutting commissioning time for new facilities. Robotics-as-a-Service subscriptions lower upfront capital outlays, bringing advanced automation within reach of mid-sized operators. Predictive analytics improves labor scheduling, a critical advantage amid driver and picker shortages. These investments reinforce the value proposition of long-term contracts and push the United Kingdom contract logistics market toward data-driven service models.

Post-Brexit Customs Brokerage Integration Elevates Service Complexity

The rollout of the New Computerised Transit System Phase 5 in January 2025 replaced legacy paper processes with digital transit documentation, yet fallback paper Transit Accompanying Documents remain in force during system outages. Hybrid clearance models employing AI and blockchain have shown productivity gains of up to 20% when benchmarked at Multimodal 2024[1]EORI UK, “Multimodal 2024 highlights,” eori.uk. HMRC has expanded its compliance workforce, increasing audit frequency and raising the bar for service providers. The EU Carbon Border Adjustment Mechanism adds a tariff calculation layer for goods with embedded emissions, making specialized customs support essential. Contract logistics firms that integrate brokerage with transport and warehousing streamline compliance costs and strengthen retention, supporting above-market growth in the United Kingdom contract logistics market.

Cold-Chain Infrastructure Expansion Supports Pharmaceutical Growth

Government commitments of USD 1.3 billion to life-sciences commercialization and USD 2 billion to NHS supply upgrades boost demand for temperature-controlled storage and distribution[2]MHA, “2024 outlook for life sciences and pharmaceuticals,” mha.co.uk. Cold storage rents are rising, prompting speculative warehouse construction in major ports and biotech clusters. Americold and regional peers employ AI forecasting models such as SARIMA and Facebook Prophet to match capacity with vaccine and biologic pipeline schedules. Collaborative multi-tenant facilities reduce transport miles and energy usage, aligning with retailer sustainability goals. Workforce shortages remain a risk, but automation of pallet handling and remote monitoring mitigates some staffing constraints. These trends feed a 4.3% CAGR in pharmaceutical logistics, lifting the United Kingdom contract logistics market beyond traditional retail dependency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute driver and warehouse labor shortages | -0.4% | National logistics corridors | Short term (≤ 2 years) |

| Ageing road and rail infrastructure capacity | -0.3% | England corridors and Scotland rail network | Long term (≥ 4 years) |

| Urban congestion-charge escalation | -0.2% | London, Manchester, Birmingham | Medium term (2-4 years) |

| Rising ESG compliance cost burden | -0.2% | Manufacturing-intensive regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acute Driver and Warehouse Labor Shortages Constrain Operational Capacity

Heavy-goods-vehicle driver vacancies reached 19% in Q1 2024, driven by retirements and pay competition from other sectors. Brexit curtailed EU driver inflows while the pandemic prompted early retirements, cutting available skills just as parcel volumes surged. Grant Thornton notes additional headwinds, such as high fuel prices and inflation, that limit wage headroom[3]Grant Thornton, “Haulage sector faces significant headwinds,” grantthornton.co.uk. Logistics employs 8% of the national workforce, yet critical hands-on roles remain hard to fill despite apprenticeships and upskilling schemes. Automation eases some strain, but adoption takes time and capital. In the near term, limited labor availability caps throughput and increases operating costs in the United Kingdom contract logistics market.

Aging Infrastructure Capacity Limits Growth Potential

Royal Mail will end rail freight in October 2024, shifting 10,000 loads per year from rail to road and straining highway capacity. This decision conflicts with the Department for Transport's target of 75% rail freight growth by 2050. Scotland has earmarked USD 150 million for power upgrades on its rail network, but national road and rail maintenance backlogs remain large. Local authorities manage 40% of infrastructure funding, yet budget gaps and staffing shortages delay project delivery[4]Local Government Association, “Invest 2035,” local.gov.uk. Urban congestion charging adds complexity, raising last-mile costs for carriers in London and other major cities. Combined, these factors temper the growth rate of the United Kingdom contract logistics market over the long term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Dominance Faces Value-Added Upswing

Transportation services generated 60.45% of 2025 revenue, reflecting the enduring need for reliable multimodal links in the United Kingdom contract logistics market. Sea freight tonnage grew 4% to 60.7 million tons in 2024, boosted by deep-sea imports from China, while DP World’s USD 1.3 billion London Gateway expansion adds berth capacity and full-electric cranes. Road remains the backbone, yet urban emission rules and driver shortages push operators toward alternative fuels and route optimization platforms. Rail capacity suffers after Royal Mail’s withdrawal, adding pressure on highways and warehousing near ports.

Value-added services, though smaller, post a 3.28% CAGR as brands outsource packaging, kitting, and customization. GXO manages end-of-line assembly and cold-chain packing for grocery and e-commerce clients, illustrating how integrated solutions lighten shipper workloads. Robotics enables late-stage customization, meeting marketing needs without slowing throughput. As ESG reporting grows stricter, providers bundle packaging redesign with waste reduction analytics, offering differentiated value. This momentum positions value-added operations to capture incremental share in the United Kingdom contract logistics market over the forecast horizon.

By Contract Duration: Long-Term Partnerships Dominate Strategic Relationships

Contracts longer than three years held 61.20% of the United Kingdom contract logistics market share in 2025, affirming customer preference for stability in a volatile regulatory climate. Shippers seek partners capable of funding automation, customs technology, and ESG upgrades that require multi-year amortization. Recent mega-deals include Amazon’s USD 50 billion multi-year investment across four UK fulfillment centers, locking in contract volumes for chosen 3PLs.

Shorter contracts of one to three years maintain relevance for tactical projects but expand more slowly. Acquisition activity, such as GXO’s purchase of Wincanton, demonstrates how incumbents value embedded long-term contracts. With border processes still evolving, firms commit to extended deals to secure in-house expertise and avoid switching costs. Consequently, long-term arrangements underpin revenue visibility across the United Kingdom contract logistics market.

By End-User Industry: Retail Leadership Meets Healthcare Acceleration

Retail and e-commerce generated 28.60% of 2025 revenue thanks to high parcel volumes and fast replenishment cycles. Amazon, B&M, and DHL each announced significant distribution center investments, cementing retail’s primacy. Same-day delivery expectations spur micro-fulfilment build-outs near London and Manchester, increasing demand for inventory pooling and last-mile orchestration services.

Healthcare and pharmaceuticals register the fastest 4.15% CAGR, reflecting USD 2 billion NHS supply upgrades and robust life-sciences R&D funding. Advanced therapies require ultra-low-temperature handling, pressing 3PLs to expand validated cold-chain corridors. CEVA’s global finished-vehicle logistics pivot illustrates capability transfer from automotive to tightly controlled healthcare shipments. The growth of high-value, temperature-sensitive cargo offers margin upside and dilutes concentration risk for the United Kingdom contract logistics market.

Geography Analysis

England anchors the United Kingdom contract logistics market with an 82.60% revenue share in 2025, supported by the Golden Triangle’s central location and dense motorway web. DP World’s 598,000 sq ft Coventry warehouse automates pallet retrieval, while London Gateway’s new berth enhances deep-sea throughput. London pilots low-emission microhubs that completed 128,000 deliveries in nine months, validating sustainable urban models. Amazon’s forthcoming Hull and East Midlands sites widen regional employment and service coverage, reinforcing England’s primacy.

Scotland posts a 3.49% CAGR through 2031, the fastest among home nations, as the USD 150 million rail electrification program improves connectivity for renewable energy component shipping. Port upgrades support offshore wind turbine logistics, while Glasgow and Aberdeen labs drive pharmaceutical and biotech traffic. The confluence of green energy projects and manufacturing diversification boosts contract values and fuels infrastructure timber demand across distribution estates.

Competitive Landscape

The United Kingdom contract logistics market shows moderate concentration as global integrators consolidate local expertise. GXO’s USD 957 million acquisition of Wincanton expands sector coverage. DSV’s EUR 14.3 billion (USD 14.9 billion) purchase of Schenker creates a network spanning more than 90 countries. The CMA’s probe into a DHL-Evri parcel merger signals heightened regulatory vigilance over market dominance.

Strategic priorities center on automation, digital visibility, and specialized vertical solutions. CEVA repurposed its automotive competence to establish a finished-vehicle logistics division moving 4 million vehicles annually, illustrating vertical integration. ID Logistics’ entry via a Northampton facility demonstrates foreign appetite for UK consumer goods contracts.

Sustainability drives another layer of competition, with Hellmann adding a dedicated global sustainability division and DHL introducing low-carbon route planning tools. Emerging mid-tier disruptors harness robotics, micro-fulfilment, and data analytics to win urban retail contracts, challenging incumbents to remain agile. Taken together, these moves signal an environment of intensifying rivalry, service innovation, and ongoing consolidation in the United Kingdom contract logistics market.

United Kingdom Contract Logistics Industry Leaders

DHL Supply Chain

XPO Logistics

UPS SCS

GXO Logistics

CEVA Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: FedEx announced two new UK hubs near Kingsbury and Marston Gate, consolidating five road hubs into tech-enabled facilities for future growth.

- April 2025: DSV completed its EUR 14.3 billion (USD 14.9 billion) acquisition of DB Schenker, targeting DKK 9 billion (USD 1.3 billion) in annual savings by 2028.

- October 2024: Yusen Logistics chose Manhattan Active Warehouse Management for its 1.19 million sq ft Northampton center due online in Jan 2026.

- April 2024: GXO closed the USD 957 million Wincanton deal, adding sector expertise in aerospace, utilities, and healthcare.

United Kingdom Contract Logistics Market Report Scope

Contract logistics refers to a long-term collaboration for a wide plethora of services ranging from the conveyance of products or spare parts to the end customer delivery.

The UK contract logistics market is segmented by type (insourced and outsourced) and end-user (manufacturing and automotive, consumer goods and retail, pharmaceuticals and healthcare, hi-tech, and other end users).

The report offers the market size and forecasts in terms of value (USD) for all the above segments.

By Service Type

| Transportation | Road |

| Rail | |

| Air | |

| Sea | |

| Warehousing & Distribution | |

| Value-added Services (Assembly, Labelling, Kitting) |

By Contract Duration

| 1 – 3 Years |

| Above 3 years |

By End-user Industry

| Manufacturing & Automotive |

| Food & Beverage |

| Retail & E-commerce |

| Healthcare & Pharmaceuticals |

| Chemicals |

| Other Industries |

By Region

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Service Type | Transportation | Road |

| Rail | ||

| Air | ||

| Sea | ||

| Warehousing & Distribution | ||

| Value-added Services (Assembly, Labelling, Kitting) | ||

| By Contract Duration | 1 – 3 Years | |

| Above 3 years | ||

| By End-user Industry | Manufacturing & Automotive | |

| Food & Beverage | ||

| Retail & E-commerce | ||

| Healthcare & Pharmaceuticals | ||

| Chemicals | ||

| Other Industries | ||

| By Region | England | |

| Scotland | ||

| Wales | ||

| Northern Ireland |

Key Questions Answered in the Report

What is the current value of the United Kingdom contract logistics market?

The market is valued at USD 21.83 billion in 2026 and is on track to reach USD 25.51 billion by 2031.

Which service type contributes most to revenue?

Transportation services deliver 60.45% of sector revenue owing to sustained demand for multimodal goods movement.

Which segment is growing fastest?

Healthcare and pharmaceuticals are expanding at a 4.15% CAGR because of rising cold-chain and life-sciences investment.

Why are longer contract durations gaining popularity?

Shippers prefer multiyear agreements to secure customs expertise, automation investment, and ESG compliance support.

How is Brexit influencing the sector?

New customs rules have increased brokerage demand and pushed providers to integrate real-time visibility and compliance tools.

What infrastructure developments matter most for growth?

DP World’s London Gateway expansion, new Amazon fulfillment centers, and Scottish rail electrification collectively enhance national capacity.

Page last updated on: