Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 91.87 Billion |

| Market Size (2026) | USD 96.72 Billion |

| Market Size (2031) | USD 114.25 Billion |

| Growth Rate (2026 - 2031) | 3.39% CAGR |

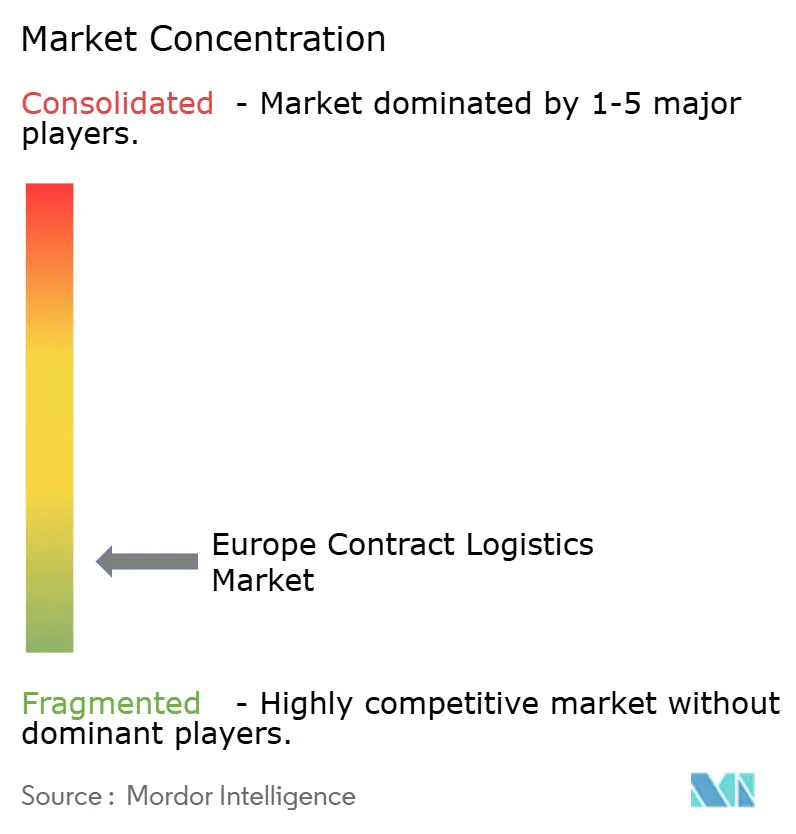

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Contract Logistics Market Analysis by Mordor Intelligence

The Europe Contract Logistics Market size is projected to be USD 91.87 billion in 2025, USD 96.72 billion in 2026, and reach USD 114.25 billion by 2031, growing at a CAGR of 3.39% from 2026 to 2031.

A measured growth outlook masks a pivot toward high-value verticals, the rapid rollout of automation, and selective network consolidation that targets density in strategic corridors. Leading providers are scaling robotics and digital control towers to compress cycle times, mitigate labor bottlenecks, and stabilize margins in a low-growth demand cycle. Contract models are also shifting as shippers seek flexibility to align with faster technology refreshes and tighter sustainability clauses. Country‑level divergence remains a defining feature as growth corridors in Central and Eastern Europe absorb nearshoring and e‑commerce flows while larger Western markets optimize footprints and quality of service.

Key Report Takeaways

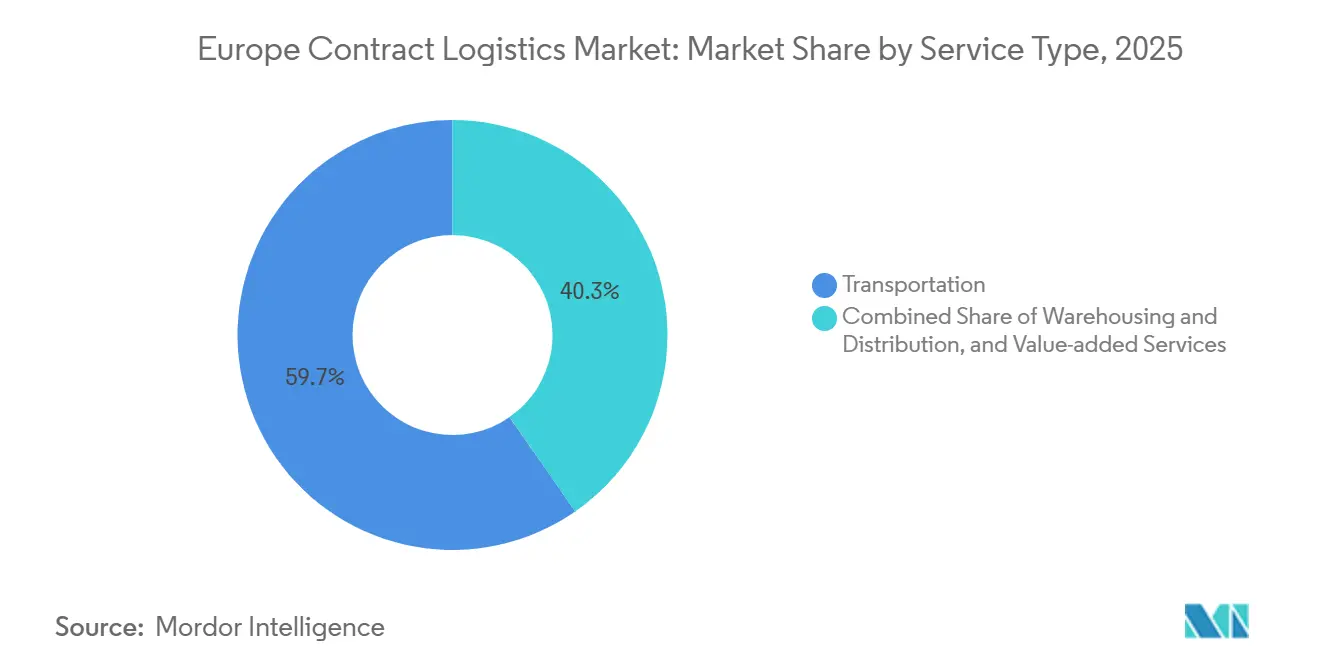

- By service type, transportation led with 59.67% market share of the Europe Contract Logistics Market size in 2025, while warehousing and distribution is forecast to expand at a 4.12% CAGR through 2031.

- By contract duration, long‑term agreements above three years held 54.12% market share in 2025, while 1‑3 year contracts are projected to grow at 3.89% through 2031.

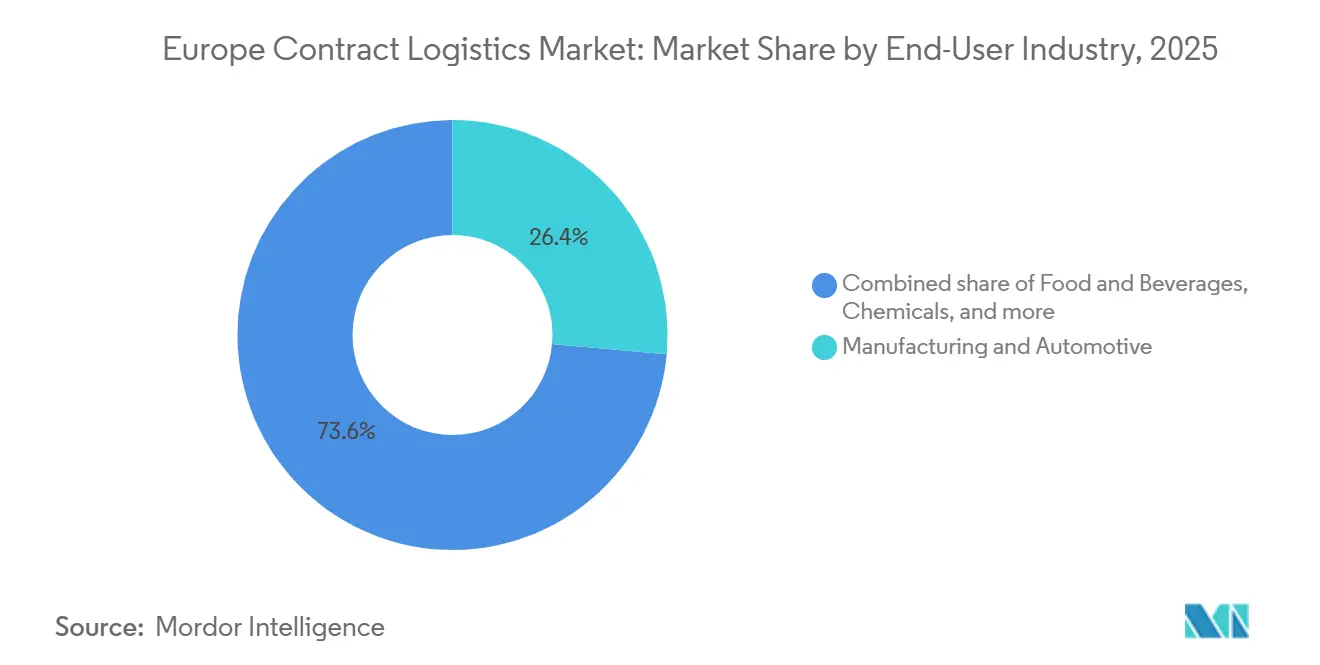

- By end‑user industry, manufacturing and automotive accounted for 26.43% of the Europe Contract Logistics Market share in 2025, while healthcare and pharmaceuticals are set to advance at a 4.35% CAGR through 2031.

- By geography, Germany held 23.23% in 2025, while Poland is expected to post the fastest growth at a 3.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Contract Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pan-European Warehouse Network Consolidation Strategies | +0.8% | Global, early gains in Germany, Netherlands, Poland, with spillover to CEE | Medium term (2-4 years) |

| AI-Driven Demand Forecasting Transforming Inventory Management | +0.7% | Global, with early adoption in UK, Nordics, Germany | Short term (≤ 2 years) |

| Growth of Circular Economy and Reverse Logistics Solutions | +0.6% | EU core markets including Netherlands, Germany, France, Belgium | Medium term (2-4 years) |

| Cross-Border E-Fulfilment Standardization Within the EU | +0.5% | EU‑27 with strongest impact in cross‑border corridors between Germany, Netherlands, Belgium | Short term (≤ 2 years) |

| Pharmaceutical Serialization and Compliance Logistics Expansion | +0.4% | Western Europe including Germany, Switzerland, France, Italy, UK | Medium term (2-4 years) |

| Integration of Contract Logistics with End-to-End 4PL Solutions | +0.4% | France, Benelux, Germany, UK | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Pan-European Warehouse Network Consolidation Strategies Drive Regional Hub Efficiency

Providers continue to consolidate multi‑country footprints into fewer hubs with cross‑docking and postponement capabilities to improve fixed‑cost absorption while protecting service levels. Recent investments anchor this approach in Central and Eastern Europe, including LX Pantos’ acquisition of a 109,000 square meter logistics center in Katowice to link Germany, Poland, and Ukraine through the A4 and A1 corridors for regional consolidation. The removal of the EUR 150 low‑value import duty exemption in July 2026 adds a powerful incentive to reposition inventory and customs expertise closer to demand centers inside the EU[1]European Commission, “E-commerce: 150 EUR Customs Duty Exemption Threshold to Be Removed as of 2026,” Taxation and Customs Union, taxation-customs.ec.europa.eu . Large‑scale M&A further concentrates network density and procurement leverage, exemplified by DSV’s acquisition of DB Schenker, which expands shared infrastructure and control tower reach. These moves set the foundation to absorb cross‑border flows at lower unit costs while maintaining speed to the consumer.

AI-Driven Demand Forecasting Transforms Inventory Positioning and Exception Handling

Digitalization stepped up in 2026 as operators shifted from pilots to scaled deployments across planning, inventory, and warehouse execution. DHL reports 8,200 digitalization projects with 92% of sites on its Accelerated Digitalization platform, which expands the data foundation for predictive demand planning and automated exception management. Providers are pairing advanced analytics with robotics to lift throughput, as seen in DHL’s rollout of 1,000-plus Stretch robots and GXO’s highly automated Levi’s site in Dorsten with high hourly unit processing. These integrated systems improve slotting precision, speed replenishment, and stabilize service levels in volatile cycles. The result is a more resilient operating model that reduces manual touchpoints and unlocks multi‑site optimization opportunities.

Growth of Circular Economy and Reverse Logistics Solutions Redefines Value Recovery

Circularity has moved from pilot to practice as retailers and logistics partners operate reverse flows to reclaim inventory value. Executive dialogues at the Reverse Logistics Summit in Amsterdam highlighted practical steps to reduce waste through refurbishment and re‑commerce pathways that cut costs and improve sustainability outcomes[2]National Retail Federation, “Solving Circularity: Highlights from NRF’s Reverse Logistics Summit in Amsterdam,” NRF, nrf.com . Contract logistics providers are adapting process designs to integrate returns triage, refurbishment, and quality assurance alongside forward fulfillment. Regulatory momentum inside the EU is reinforcing these models, and it is driving systems upgrades in traceability to meet producer responsibility commitments. These capabilities are becoming a commercial differentiator for tenders that reward measurable waste reduction and recovery rates.

Cross-Border E-Fulfilment Standardization Within the EU Simplifies Multi-Market Operations

Shippers continue to seek consistency in pricing, data standards, and returns flow across the EU to lower the soft costs of fragmentation. European institutions have advanced consumer product safety oversight in e‑commerce and reinforced the compliance burden on non‑EU imports, which raises the value of bonded facilities and customs brokerage inside the bloc. The July 2026 elimination of the low‑value duty exemption removes a longstanding distortion and is accelerating demand for scalable customs data management and IOSS‑aligned VAT processing. Standardized tracking and data exchange between national systems are also priorities for smoother cross‑border e‑fulfillment. Providers that unify customs, brokerage, and fulfillment under a single digital interface are positioned to capture cross‑market growth as compliance tightens.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Exposure in Long-Term Outsourcing Contracts | -0.5% | Global, with larger effects in Germany and France due to higher capex intensity | Long term (≥ 4 years) |

| Dependence on Volatile Retail and Automotive Demand Cycles | -0.6% | Germany, Italy, France, Hungary across the automotive belt | Medium term (2-4 years) |

| ESG Reporting Burden on Logistics Service Providers | -0.4% | EU‑27 and UK with CSRD and EU Taxonomy alignment needs | Short term (≤ 2 years) |

| Overcapacity Risks in Certain Western European Markets | -0.3% | Netherlands, Belgium, Germany’s industrial clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Exposure in Long-Term Outsourcing Contracts Constrains Provider Flexibility

Multi‑year agreements often require upfront investment in automation, fleet, and IT that can outlast a customer’s demand cycle or technology life. Leading players are committing significant capital to robotics and warehouse mechanization, which raises utilization risk if contract volumes change. DHL reported more than EUR 1 billion (USD 1.17 billion) in automation investments in recent years, and peers are scaling similar programs to defend service quality at lower unit cost. While these projects deliver productivity, they also bind providers to specific footprints and technology stacks, making contract exit or retooling more complex. The result is a higher hurdle rate for asset‑heavy bids and a premium on modular designs that can flex with customer needs.

Dependence on Volatile Retail and Automotive Demand Cycles Exposes Revenue Concentration Risk

Large shares of contract logistics activity still track consumer spending and automotive production, which both show sensitivity to macro cycles. Providers with deep exposure to automotive or discretionary retail can experience sharp swings in warehouse utilization and transport volumes. Europe’s largest forwarders and contract logistics firms described a challenging operating environment in 2025 with underutilization in some networks. These pressures force cost programs and footprint adjustments to stabilize earnings. Diversification into healthcare, technology hardware, and spare parts logistics can lower concentration risk when demand in cyclical verticals softens.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Retains Commanding Share as Warehousing Gains Automation Edge

Transportation captured 59.67% of the European contract logistics market in 2025, reflecting the centrality of linehaul and last mile across cross‑border corridors and national networks. This scale advantage remains critical as operators balance labor constraints and rising compliance costs in road operations. Air and sea continue to serve high‑value and long‑haul needs, with large forwarders highlighting volume gains in 2025 as they captured share on Asia to Europe routes and supported technology and perishables flows. Kuehne Nagel reported year‑on‑year increases in both air and sea volumes in the first half of 2025, underscoring the resilience of multimodal portfolios that complement inland transport. Network density and procurement reach also broadened after transformational M&A, as DSV integrated DB Schenker’s capabilities to strengthen capacity, access, and operational control across Europe.

Warehousing and distribution are growing faster than the European contract logistics market size at a 4.12% CAGR through 2031, powered by e‑commerce fulfillment, nearshoring, and the rapid deployment of robotics that raise throughput and stabilize service quality. DHL reports 8,200 digitalization projects with 92% of sites enabled, and it plans more than 1,000 Stretch robots across regions, all to compress dwell times and cut manual handling. GXO’s Dorsten facility for Levi’s processes over 10,000 units per hour and up to 155,000 units daily through a coordinated system of conveyors, mini‑loads, and automated packing, offering a reference architecture for high‑volume fashion fulfillment[3]GXO Logistics, “GXO Completes State-of-the-Art Warehouse in Germany with Levi’s,” GXO, gxo.com . These examples illustrate why warehousing is evolving from static storage to dynamic flow management centered on software and automation. The service type mix is therefore tilting toward facilities that combine valued services, rapid sortation, and integrated returns to meet omnichannel expectations at scale.

By Contract Duration: Long-Term Agreements Dominate Yet Flexible Tenures Capture Agility Premium

Contracts exceeding three years commanded 54.12% of arrangements in 2025, supported by co‑investment models in automation, cold chain, and specialized facilities that require multi‑year amortization. The European contract logistics market favors longer tenures in capital‑intensive verticals where network stability and quality certifications matter. Strategic anchor sites often sit near major production or consumption hubs to serve multi‑country flows under a unified control tower. Cost predictability and embedded productivity roadmaps are key benefits that allow both parties to plan upgrades with clear governance. Large operators publish standardized playbooks for automation and process excellence to deliver recurring gains over a multi‑year schedule.

Shorter 1‑3-year contracts are growing at a 3.89% rate to 2031, reflecting shippers’ need to recalibrate service levels, sustainability targets, and technology choices on a quicker cadence. Providers are responding with modular automation and flexible warehousing footprints that scale up or down without stranded capital. Notable long‑horizon partnerships are also being designed with annual refresh cycles that hardwire improvements while keeping the commercial framework stable. GXO’s 20‑year agreement for Levi’s Dorsten site shows how long‑term deals can still embed continuous innovation, quality, and sustainability milestones inside the governance model. This balance between multi‑year certainty and short‑cycle agility is shaping how bids are scoped and priced across European tenders.

By End-user Industry: Healthcare Emerges as Growth Leader While Automotive Navigates Structural Headwinds

Manufacturing and automotive held 26.43% of the European contract logistics market in 2025, supported by inbound‑to‑manufacturing flows, just‑in‑sequence delivery, and complex aftersales logistics. The industrial footprint across Germany, Central Europe, and the Iberian Peninsula sustains demand for synchronized warehousing and transport capacity. Yet production volatility and platform shifts in automotive create volume risk for providers concentrated in that vertical. Large network operators have outlined cost measures to protect earnings through softer periods and to reallocate resources to lanes with better visibility. These dynamics keep focus on productivity plays and multi‑vertical diversification to smooth revenue across cycles.

Healthcare and pharmaceuticals are the fastest‑growing end‑user group with a 4.35% CAGR through 2031, driven by stringent GDP standards and continued growth in temperature‑controlled therapies. Inspections reported in 2025 highlight recurring gaps in data integrity, facility access, and cold chain documentation, which are catalyzing upgrades to real‑time monitoring and segregated quarantine areas. These requirements elevate specialized nodes with validated temperature zones and trained personnel. Europe’s largest providers are expanding digital quality systems and standardized workflows to serve biopharma hubs efficiently on a large scale. As a result, the European contract logistics industry continues to see a tilt toward regulated segments where quality and compliance underpin growth.

Geography Analysis

Germany accounted for 23.23% of the European contract logistics market in 2025, reflecting its central position in EU transport corridors and its deep manufacturing base, while Poland is expected to post the fastest national growth at a 3.65% CAGR to 2031. Germany’s dense road and rail links support multi‑country distribution, and it is a focal point for automation and digital control tower investments by global leaders. The market is prioritizing network efficiency and service stabilization through scaled robotics, quality certifications, and shared service centers. Poland’s strength draws on pan‑European connectivity and cost‑effective operations that absorb nearshoring and cross‑border e‑commerce flows. LX Pantos’ Katowice campus acquisition underscores a broader shift to anchor capacity inside Central Europe in anticipation of tighter customs and VAT regimes.

The United Kingdom shows steady demand despite friction in EU trade flows, supported by strong grocery and omni‑channel fulfillment requirements. Providers are adding sites and headcounts to support large e‑commerce accounts and consumer brands, and they are building flexibility into multi‑year agreements with annual refresh cycles. France remains structurally important due to population density and well‑developed road and rail networks, and it is a base for several major operators that continue to invest in transport and distribution assets. Italy and Spain leverage port proximity and rising e‑commerce penetration to expand dedicated distribution centers and capacity for returns. Automation pilots in these markets evolve into scaled deployments as robotics partners and integrators expand footprints.

The Netherlands and Belgium function as critical Benelux gateways with Rotterdam and Antwerp enabling high‑velocity import and cross‑docking flows. Tight land supply has tempered take‑up in select submarkets, yet it is also supporting rental growth and incentivizing automation. Nordic markets post stable demand on the back of high digital adoption and consistent omni‑channel activity. Central and Eastern European markets beyond Poland, including the Czech Republic, Romania, and the Baltics, capture volume growth as production relocates and as corridor infrastructure improves. Across regions, tender documents increasingly request ISO 14001 certification and emissions calculations aligned to recognized standards, adding compliance value to integrated 4PL and data‑rich 3PL models.

Competitive Landscape

The European contract logistics market remains fragmented, with the top ten operators holding less than 20% combined share, which leaves room for both scale strategies and specialist niches. Leaders are using balance sheet strength to consolidate networks and standardize automation playbooks that compound cost advantages over time. At the same time, regional specialists continue to differentiate with sector expertise, agile footprints, and quality certifications in regulated verticals. Labor constraints remain a common threat, and the driver shortage reported by IRU adds urgency to automation, routing optimization, and alternative delivery models. The operating thesis across the region centers on density, digitalization, and vertical specialization.[4]International Road Transport Union, “Driver Shortage: Are Autonomous Vehicles the Solution,” IRU, iru.org

Scale moves are reshaping the leaderboard, most notably DSV’s acquisition of DB Schenker, which expands multi‑modal capacity and warehouse space across Europe and beyond. The integration is underway with synergy capture plans and a condensed timeline that reflects execution confidence. Providers are also strengthening automation pipelines, with DHL committing more than 1,000 Stretch robots on top of extensive digitization coverage across its sites. Balance sheet actions such as GXO’s USD 540 million bond raise in November 2025 support debt refinancing and fund growth at attractive capital costs. These actions sustain investment in technology and network densification through a lower‑growth environment.

Execution priorities emphasize operating leverage through standardized robotics, data‑driven planning, and shared services. Kuehne Nagel moved to lower structural costs and increased automation use in response to softer flows and margin pressure, while maintaining share gains in sea and air. Sector‑specific credentials continue to be a differentiator, such as GXO’s aerospace quality certification for its Dormagen site, which improves traceability and service levels for aircraft parts. Real estate actions also support footprint expansion in key corridors, as Rhenus doubled its space at a LEED Platinum site in Northern Italy to serve growing demand. Together, these measures point to a disciplined focus on productivity, quality, and corridor strength as sources of durable advantage.

Europe Contract Logistics Industry Leaders

Deutsche Post DHL Group

DSV

GXO Logistics

XPO Logistics

CEVA Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: LX Pantos acquired a large‑scale logistics center in Katowice, Poland, in partnership with KIND and the PIS No. 2 Fund for KRW 216 billion (USD 166.3 million), totaling 109,000 square meters across five buildings and positioned as a regional hub on the A4 and A1 corridors.

- April 2025: GXO’s multi‑user distribution center in Dormagen, Germany, received EN 9120 aerospace quality certification and supports over 9,000 aircraft parts with enhanced traceability and shorter delivery times.

- October 2025: Kuehne Nagel launched a cost‑reduction program targeting more than CHF 200 million per year, including process optimization and greater automation, to mitigate a challenging market backdrop.

- October 2025: DHL Group opened its Europe Innovation Center in Troisdorf near Bonn, a 5,360 square meter facility that showcases AI, robotics, IoT, and sustainability technologies and operates with zero greenhouse gas emissions.

Europe Contract Logistics Market Report Scope

Contract logistics refers to a long-term partnership that includes a variety of services, from the transportation of goods or replacement parts to the delivery of goods to the ultimate customer.

The report provides a complete background analysis of the European contract logistics market, including an assessment of the economy, a market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles are covered in the report. The report also covers the impact of COVID-19 on the market.

The report covers the European Logistic Companies, and it is segmented by End User (Industrial Machinery and Automotive, Food and Beverage, Construction, Chemicals, Other Consumer Goods, and Other End Users), and Country (Germany, the United Kingdom, the Netherlands, France, Italy, Spain, Poland, Belgium, Sweden, and Rest of Europe). The report offers the market size in value terms in USD for all the abovementioned segments.

By Service Type

| Transportation | Road |

| Rail | |

| Air | |

| Sea | |

| Warehousing & Distribution | |

| Value-added Services (Assembly, Labelling, Kitting) |

By Contract Duration

| 1-3 Years |

| Above 3 years |

By End-user Industry

| Manufacturing & Automotive |

| Food & Beverage |

| Retail & E-commerce |

| Healthcare & Pharmaceuticals |

| Chemicals |

| Other Industries |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Service Type | Transportation | Road |

| Rail | ||

| Air | ||

| Sea | ||

| Warehousing & Distribution | ||

| Value-added Services (Assembly, Labelling, Kitting) | ||

| By Contract Duration | 1-3 Years | |

| Above 3 years | ||

| By End-user Industry | Manufacturing & Automotive | |

| Food & Beverage | ||

| Retail & E-commerce | ||

| Healthcare & Pharmaceuticals | ||

| Chemicals | ||

| Other Industries | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe |

Key Questions Answered in the Report

What is the current size and growth outlook for the European contract logistics market?

The Europe contract logistics market size was USD 91.87 billion in 2025, and it is projected to reach USD 114.25 billion by 2031 at a 3.39% CAGR, after advancing to USD 96.72 billion in 2026.

Which service type leads and which grows fastest in Europe?

Transportation led with 59.67% share in 2025, while warehousing and distribution is forecast to grow at a 4.12% CAGR through 2031 as automation and e‑commerce fulfillment scale across the region.

Which country is the largest and which is the fastest growing in Europe?

Germany held 23.23% in 2025, and Poland is expected to post the fastest national CAGR at 3.65% to 2031 due to its corridor position and investment inflows.

What are the top technology priorities for providers in 2026?

Providers prioritize digital control towers, robotics, and automated exception handling as they scale programs such as DHL’s 1,000-plus Stretch robots and site‑wide digitization to stabilize service and costs.

How are compliance trends shaping European logistics contracts?

Shippers frequently request ISO 14001 certification and accredited emissions calculations, which elevate integrated 4PL and data‑rich 3PL models that automate Scope 3 reporting across networks.

What are the main labor constraints in European contract logistics?

A driver shortage limits capacity and raises operating complexity, with IRU highlighting the need for automation, routing optimization, and new talent pipelines to sustain service levels.

Page last updated on: