UEM In Manufacturing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

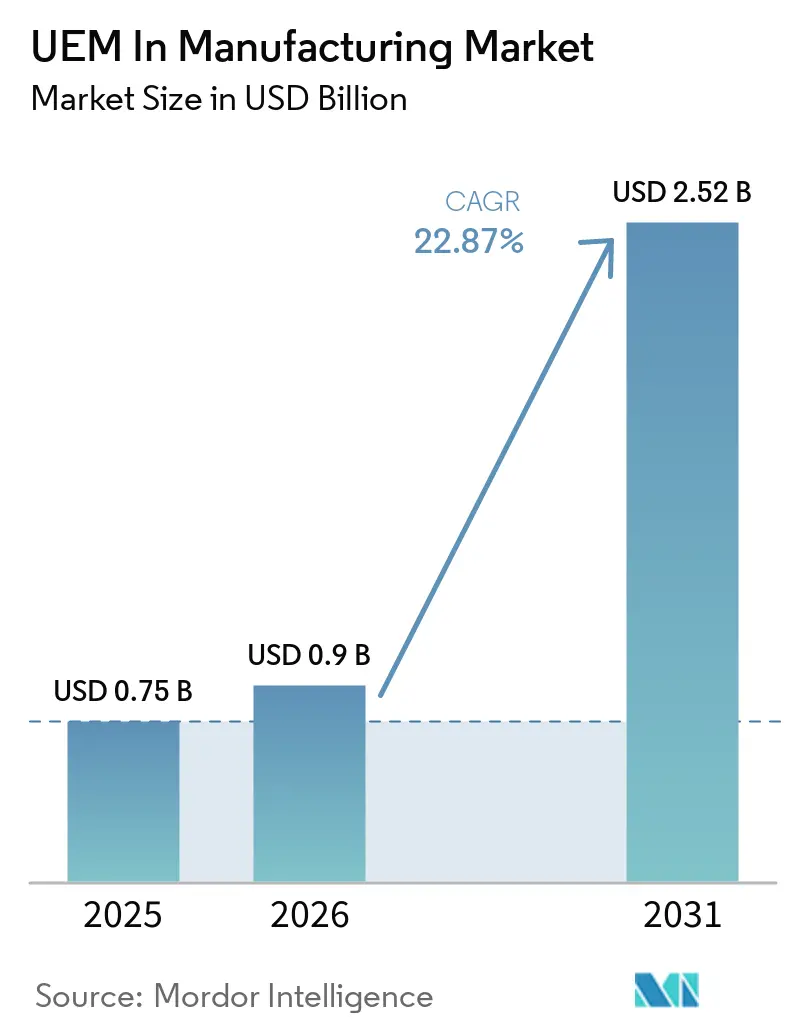

| Market Size (2026) | USD 0.9 Billion |

| Market Size (2031) | USD 2.52 Billion |

| Growth Rate (2026 - 2031) | 22.87% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UEM In Manufacturing Market Analysis by Mordor Intelligence

The UEM in manufacturing market size was valued at USD 0.75 billion in 2025 and estimated to grow from USD 0.90 billion in 2026 to reach USD 2.52 billion by 2031, at a CAGR of 22.87% during the forecast period (2026-2031). The UEM in manufacturing market is growing because factory operations now depend on a wider mix of endpoints, including rugged handhelds, shared tablets, industrial PCs, employee smartphones, and connected production equipment. Security pressure is also rising, pushing manufacturers to use a single control layer for visibility, policy enforcement, and audit readiness across IT and shop-floor devices. Cloud delivery is widening adoption because manufacturers can update policies across multiple facilities without plant-side upgrade work or frequent site visits. Smaller manufacturers are entering the UEM in manufacturing market faster as subscription pricing and easier setup reduce the barrier that once kept adoption concentrated in large enterprises. Competition in the UEM in manufacturing market is shifting toward ecosystem depth, rugged device support, and stronger links with OT, MES, and factory workflows rather than basic device control alone.

Key Report Takeaways

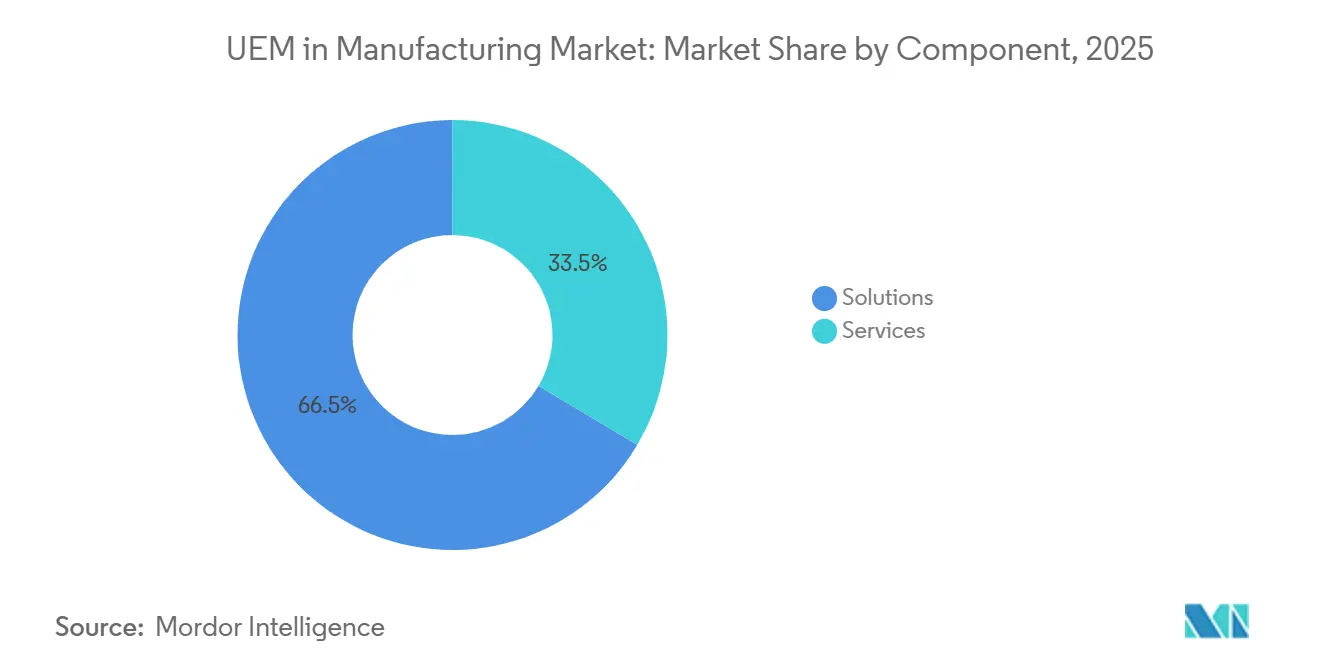

- By component, solutions accounted for 66.47% share of the UEM in manufacturing market in 2025 and are projected to expand at a 23.65% CAGR through 2031.

- By deployment mode, cloud-based deployment accounted for 61.59% of revenue in 2025 and is projected to expand at a 23.68% CAGR through 2031.

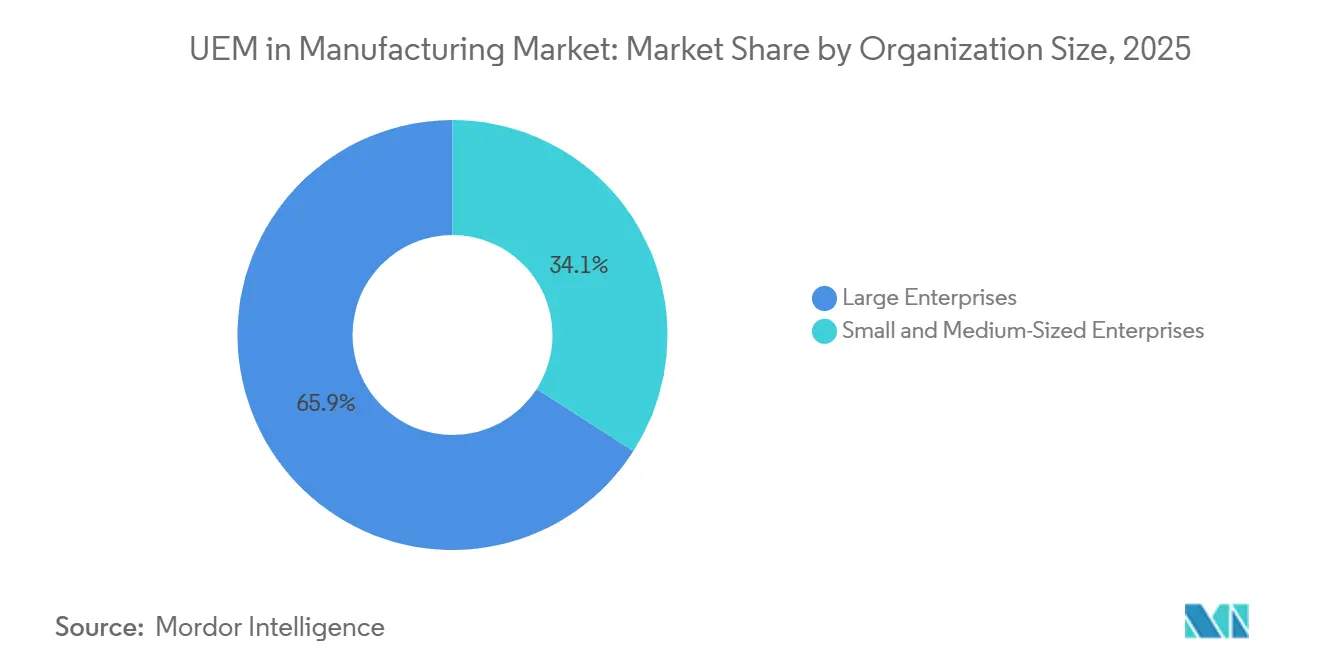

- By organization size, large enterprises held 65.93% share of the UEM in manufacturing market revenue in 2025, while small and medium-sized enterprises are projected to expand at a CAGR of 23.51% through 2031.

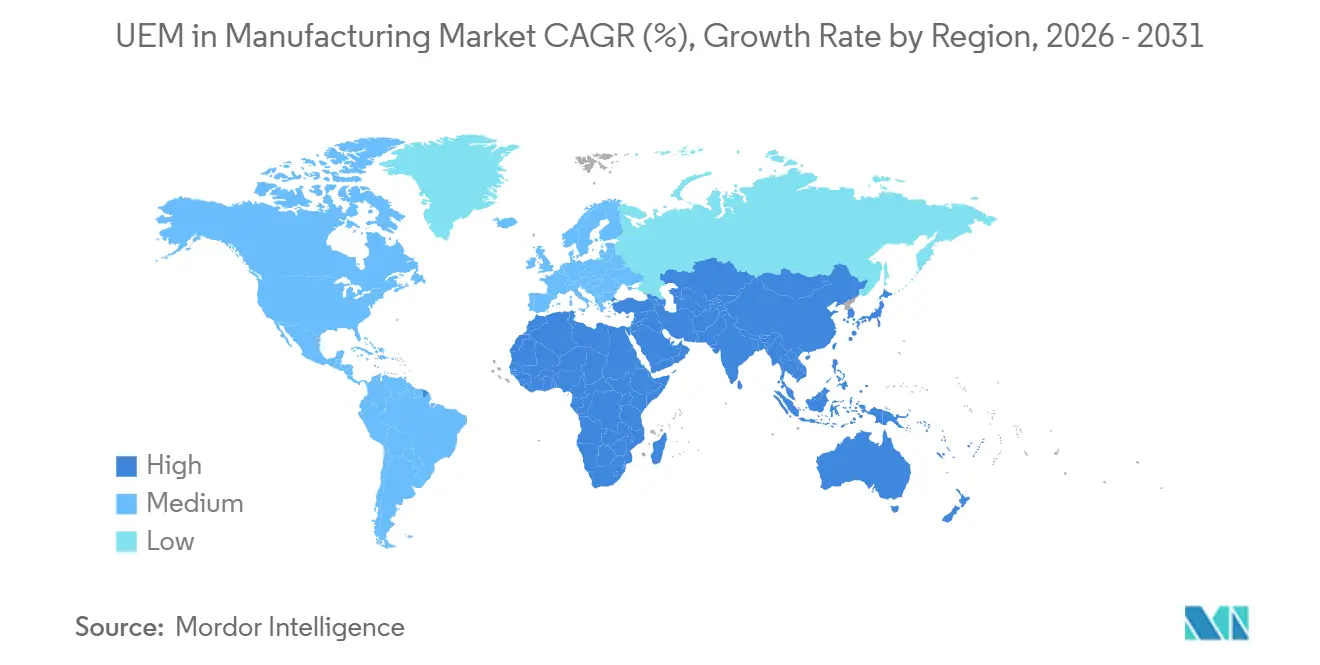

- By geography, Asia-Pacific accounted for 37.26% of revenue in 2025 and is projected to expand at a 23.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global UEM In Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising BYOD and Rugged Mobile Adoption in Factory Operations | +4.8% | Global, with peak intensity in Asia-Pacific and North America | Short term (≤ 2 years) |

| Security Standardization Across Heterogeneous Endpoints | +4.5% | Global, accelerated in EU and North America | Short term (≤ 2 years) |

| Remote Management Needs Across Distributed Plants | +4.0% | Global | Medium term (2-4 years) |

| Cloud Migration of Device Lifecycle Workflows | +3.5% | North America and Asia-Pacific core, spill-over to Europe | Medium term (2-4 years) |

| Multi-OS Endpoint Sprawl in Production Environments | +2.8% | Global | Medium term (2-4 years) |

| Compliance Pressure for Audit-Ready Endpoint Controls | +2.2% | EU and North America, expanding to Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising BYOD and Rugged Mobile Adoption in Factory Operations

The UEM in manufacturing market is benefiting from the way factory workers now use both personal smartphones and rugged handhelds on the same production floor. Rugged devices from vendors such as Zebra Technologies and Honeywell increasingly support Wi-Fi 6E, eSIM, and private 5G use cases, expanding device variety in manufacturing and logistics settings. This mixed-ownership model creates authentication, access, and data separation issues during shift handovers, especially when shared kiosks and Android devices are common. Microsoft updated frontline worker capabilities in April 2026 to support shared device mode and identity federation on Android Enterprise devices, directly addressing sign-in and sign-out gaps in multi-user factory environments. A further challenge is that hardened industrial handhelds often remain in use for 3 to 5 years, while consumer devices turn over much faster, so the UEM in the manufacturing market favors vendors that can govern both old and new device generations under a single policy model.

Security Standardization Across Heterogeneous Endpoints

The UEM in manufacturing market is also being driven by the need to secure diverse endpoint types with a single, consistent policy structure. Manufacturers operate Windows laptops, Android scanners, Linux industrial computers, and legacy controllers that cannot always accept standard agents without affecting deterministic processes. Forescout reported in June 2025 that 44% of industrial organizations said they had real-time cyber visibility, yet nearly 60% had low to no confidence in OT and IoT threat detection, which reflects the limits of siloed tools. The same operating reality creates long remediation cycles because patching production equipment often depends on maintenance windows and controlled downtime rather than standard IT timing. TeamViewer introduced its Agentless Access approach in April 2026 through a hardware gateway model, offering manufacturers a practical option for remote access and control of legacy OT endpoints without installing software directly on the devices. As IEC 62443 becomes more visible in procurement and security baselines, the UEM in manufacturing market is moving toward broader endpoint coverage that spans IT, OT, and IoT assets.

Remote Management Needs Across Distributed Plants

The UEM in manufacturing market is gaining support from manufacturers that now run wider plant networks but do not staff every site with dedicated IT teams. Rockwell Automation reported in 2026 that 96% of manufacturers have invested in or plan to invest in cybersecurity platforms over the next 5 years, indicating a broad need for remote control and governance at scale. This need is stronger in emerging manufacturing locations where plants often have limited on-site IT capacity and depend on zero-touch enrollment, remote provisioning, and automated policy enforcement. Microsoft highlighted maintenance window policies in June 2026 as a manufacturing-relevant capability because patching can be limited to planned downtime instead of active production hours. Remote governance also supports compliance checks against MES baselines, device lockdown outside approved plant zones, and wipe actions for unsupervised shared devices. In that setting, the UEM in manufacturing market is being justified less as an IT convenience and more as a direct support tool for uptime, continuity, and multi-site control.

Cloud Migration of Device Lifecycle Workflows

The UEM in manufacturing market is further supported by the move from plant-bound device management toward cloud-native and hybrid service models. Manufacturers that once resisted cloud deployment because of data sovereignty, connectivity, and integration concerns are changing their approach as vendors add sovereign instances, edge support, and offline synchronization. Omnissa completed its modern SaaS architecture rollout across shared SaaS customers by early 2025, improving scalability and resilience for enterprises managing larger, distributed fleets. Ivanti launched Neurons for MDM Sovereign Edition EU in 2026, which directly addressed regulated European use cases that require data residency, auditable controls, and NIS2-aligned reporting.[1]Ivanti, “Ivanti Enhances Autonomous Capabilities Across IT and Security Operations With AI-Driven Neurons Platform,” Ivanti, ivanti.com These changes matter because they separate platform modernization from hardware refresh timing, making the UEM in the manufacturing market easier to adopt across mixed factory estates. Hybrid models are also gaining traction because they keep latency-sensitive enrollment and configuration closer to the plant while moving analytics and multi-site reporting to the cloud.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity with Legacy OT and MES Environments | -2.2% | Global, most acute in Europe and North America with aged OT estates | Medium term (2-4 years) |

| Budget Friction in Mid-Market Manufacturing Plants | -1.5% | Global, most intense in South America, Africa, and Southeast Asia | Short term (≤ 2 years) |

| Endpoint Change-Management Resistance from Plant Operators | -0.9% | Global | Short term (≤ 2 years) |

| Limited IT Visibility into Shared Shop-Floor Devices | -0.7% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity with Legacy OT and MES Environments

The UEM in manufacturing market still faces resistance from the mismatch between modern endpoint platforms and long-life industrial systems. OT environments were built for stability and deterministic operation, while UEM tools were designed around frequent updates, dynamic policies, and broad agent coverage. Manufacturing plants also run proprietary and industrial protocols such as FL-net, OPC-UA, Modbus, and MQTT, which often require specialized connectors or translation layers to fit into a unified management plane. Palo Alto Networks reported in 2026 a 332% increase in unique internet-exposed OT devices and nearly 20 million OT-related services visible on the public internet, which shows how attempts to connect OT estates to cloud control layers can widen exposure if governance is weak. The same problem slows deployment because vendors often need to validate compatibility with each MES variant and the automation stack present at a site. As a result, the UEM in manufacturing market still depends heavily on vendors that can shorten rollout cycles through pre-built connectors, OT protocol support, and proven plant integration methods.

Budget Friction in Mid-Market Manufacturing Plants

The UEM in manufacturing market also faces a pricing and operating challenge in mid-sized plants that do not have enterprise-scale device counts or dedicated mobility teams. A licensing model that works well for a global OEM with tens of thousands of endpoints can be difficult for a supplier that manages only a few hundred rugged devices across 1 or 2 locations. The barrier is not limited to subscription fees, as many smaller plants hand UEM administration to OT-trained staff, which increases support and training costs after purchase. Vendors such as 42Gears and Miradore have tried to lower that burden through modular and usage-led pricing that lets manufacturers start with core controls and expand over time. Even so, many smaller buyers still need a clear link between platform costs and production outcomes, such as uptime, handover speed, and reduced dispatch requirements, before they commit. Until that link becomes more visible, the UEM in manufacturing market will continue to face slower adoption in price-sensitive manufacturing cohorts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Architecture Anchors Device Lifecycle Governance

Solutions held 66.47% of UEM in manufacturing market share in 2025, which showed that buyers preferred integrated platforms over stand-alone service engagements. Manufacturers increasingly chose one console for device management, application control, content delivery, security and compliance, and analytics-based automation. The strongest pull within the solutions layer came from device management and security, as well as compliance management, as manufacturers sought consistent configuration baselines across laptops, scanners, kiosks, printers, and RFID assets.

The solutions segment also expanded its scope in 2025 as vendors added broader IoT and remediation capabilities. Omnissa introduced Workspace ONE Vulnerability Defense in September 2025, linking AI-driven remediation with CrowdStrike Falcon Exposure Management to move the offering closer to proactive vulnerability management across physical and virtual endpoints.[2]Omnissa, “Omnissa Unveils Workspace ONE Vulnerability Defense to Transform Security Management Across All Endpoints and Applications,” Business Wire, businesswire.com Omnissa also standardized MQTT support for Zebra printers and rugged devices through Workspace ONE Intelligence, which showed that platform scope was moving beyond endpoint setup into factory IoT coordination. Services still mattered in the UEM in manufacturing industry because enterprise rollouts often needed integration, deployment, and change support across MES, ERP, and industrial middleware. That service role also raises switching costs, so vendors with certified regional integrators can hold accounts longer in the UEM in manufacturing market.

By Deployment Mode: Cloud-Native Architectures Accelerate Factory-Floor Governance

Cloud-based deployment accounted for 61.59% of the UEM in manufacturing market size in 2025, which reflected the appeal of subscription economics and remote policy delivery across plant networks. Manufacturers increasingly aligned endpoint governance with the wider move of ERP, MES, quality, and supply chain applications toward SaaS and hybrid operating models. That alignment made cloud UEM a practical control plane for environments where enterprise applications and factory data flows were already becoming more connected. Omnissa's shared SaaS modernization, planned for early 2025, will support this shift by improving platform resilience and scale for large, distributed device fleets.

On-premises deployment still held value in defense-linked production, regulated pharmaceutical sites, and facilities with strict sovereignty or air-gap rules. Hybrid deployment gained traction because manufacturers could keep latency-sensitive enrollment and configuration close to the factory edge while placing analytics and cross-site reporting in the cloud. Plants in Southeast Asia, South America, and sub-Saharan Africa also needed stronger offline synchronization and edge proxy support because internet reliability remained uneven across some production zones. Ivanti's 2026 sovereign cloud release showed where the next stage of the UEM in manufacturing industry may go, with regional instances designed for compliance, residency, and audit demands in regulated markets.

By Organization Size: SME Adoption Reshapes Market Boundaries

Large enterprises accounted for 65.93% of revenue in 2025, while the UEM in manufacturing market size for small and medium-sized enterprises is projected to expand at a CAGR of 23.51% between 2026 and 2031. This split shows that the current revenue base remained concentrated in larger manufacturers, even as the fastest adoption is moving toward smaller firms. Subscription pricing, vendor-managed infrastructure, and easier onboarding are widening access for smaller manufacturing businesses that once lacked the budget or staffing model for broad endpoint governance. The UEM in manufacturing market is also becoming more relevant to SMEs because supply chain customers increasingly expect endpoint controls, security hygiene, and audit readiness from tier-2 and tier-3 partners. In that setting, UEM adoption is shifting from an optional IT upgrade to a requirement tied to commercial eligibility.

India stands out as an important volume opportunity because its manufacturing base includes a large number of micro, small, and medium enterprises, creating a broad pool of cloud-first adoption candidates. These firms often carry less legacy device management baggage, so no-code and guided onboarding models can work well when internal IT capacity is limited. Large enterprises still shape the technical direction of the UEM in manufacturing market because they demand deeper links with identity, SIEM, MES, and security operations platforms. Their deployment choices often become the benchmark that smaller manufacturers later follow in simpler forms. This pattern keeps revenue anchored in enterprise accounts today, while the future expansion of the UEM in manufacturing market will increasingly come from smaller factories moving up the digital maturity curve.

Geography Analysis

Asia-Pacific accounted for 37.26% of the UEM in manufacturing market size in 2025, which made it the leading regional contributor. The region benefits from large-scale manufacturing activity across China, Japan, South Korea, India, and Southeast Asia, where connected devices are becoming more common in automotive, electronics, heavy industry, and export-oriented production. China remains central to regional demand because its smart manufacturing push and broad installed manufacturing base create large endpoint estates that need policy consistency across facilities. The UEM in the manufacturing market in Asia-Pacific also benefits from a mobile-first operating mindset in many enterprises, which fits cloud-first deployments and greenfield rollout models. India adds another strong demand layer, as its large MSME manufacturing base aligns well with lower-complexity, cloud-led onboarding models that do not require extensive legacy integration.

North America and Europe together represented a substantial share of the UEM in manufacturing market and remain the main centers of enterprise platform development. North America benefits from earlier cloud adoption, stronger alignment with zero-trust principles, and dense manufacturing activity in automotive, aerospace, defense electronics, and pharmaceuticals. Europe is moving under a clearer compliance cycle because the NIS2 Directive entered force in 2022 and active implementation and audit activity had already progressed by 2025 and 2026.[3]European Parliament and Council, “Directive (EU) 2022/2555 of the European Parliament and of the Council of 14 December 2022,” EUR-Lex, eur-lex.europa.eu That environment raises demand from manufacturers that need endpoint visibility, policy enforcement, and evidence-ready reporting across distributed operations. The UEM in manufacturing market in Europe is therefore being pushed not only by modernization goals, but also by regulatory accountability across industrial sectors.

South America, the Middle East, and Africa still contribute a smaller revenue base, but the UEM in manufacturing market has meaningful room to expand in these regions over the medium term. Brazil provides the clearest South American path because smart factory investment and wider MES use naturally increase the number of managed endpoints on plant networks. Saudi Arabia and the United Arab Emirates also present an attractive setup because new industrial projects can deploy cloud-native endpoint governance from the commissioning stage rather than retrofit old device estates later. Africa remains earlier in the curve because connectivity gaps and slower industrial digitalization still constrain broader rollout, although multinational manufacturers are already extending global endpoint policies into select local operations. As infrastructure and plant digitalization improve, the UEM in manufacturing market in these regions is likely to deepen from isolated deployments into more standardized multi-site programs.

Competitive Landscape

The UEM in manufacturing market remains moderately fragmented at the product level, although platform breadth is increasing as vendors combine device control with remediation, analytics, and security functions. Microsoft holds a strong enterprise position because Intune integrates naturally with Microsoft 365, Azure Active Directory, and Entra-based identity workflows, providing manufacturers with a familiar control plane across corporate, frontline, and shared devices. That bundled position matters in the UEM in manufacturing market because buyers often prefer to extend existing ecosystem contracts rather than add a separate platform with new licensing and integration work. Specialist vendors still defend meaningful ground by focusing on rugged fleets, frontline workflows, and hardware-certified support across factory environments. This is why competition in the UEM manufacturing market is moving away from feature checklists alone and toward proof of deployment in real production settings.

SOTI and 42Gears remain differentiated in the rugged and frontline part of the UEM in manufacturing market because they align closely with industrial device use cases. SOTI strengthened that position in August 2025 by partnering with Advantech so that SOTI MobiControl and SOTI XSight could sit within Advantech's industrial edge computing portfolio across Android, iOS, Windows, and Linux environments. Omnissa took a different path in September 2025 by introducing Workspace ONE Vulnerability Defense, which tied endpoint management more closely to vulnerability and exposure management. Those moves show that the UEM in manufacturing market is rewarding vendors that widen platform value without losing support for industrial operating needs.

A large white space remains around agentless OT governance, autonomous patching, and shared IT and OT policy enforcement inside the UEM in manufacturing market. TeamViewer addressed part of that gap in April 2026 when it launched a pre-configured Secure Access Gateway with Bechtle and Kontron for remote access to industrial OT systems without endpoint-side software installation.[4]TeamViewer, “Hannover Messe, TeamViewer Highlights Agentless Access and AI-Supported Maintenance for Industrial Operations,” TeamViewer, teamviewer.com Ivanti also advanced autonomous endpoint management in 2026 by adding Continuous Compliance features that allowed out-of-band patching for endpoints that missed scheduled maintenance windows. As buyers connect endpoint governance more closely with MES, ERP, and industrial middleware, the UEM in manufacturing market will favor vendors with stronger ecosystem certification and lower plant integration friction. That shift should keep large platform vendors and rugged-device specialists in direct competition, while smaller providers will need clearer niche strengths to protect share in the UEM in manufacturing market.

UEM In Manufacturing Industry Leaders

Microsoft Corporation

IBM Corporation

Ivanti, Inc.

SOTI Inc.

Jamf Holding Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: TeamViewer and Bechtle, in collaboration with Kontron, launched the Secure Access Gateway hardware solution at Hannover Messe 2026, pre-configured with Agentless Access technology to deliver plug-and-play zero-trust remote access and endpoint management for industrial OT systems, including legacy Windows XP-era controllers, without requiring software installation on the managed endpoint, targeting the IT and OT convergence gap in manufacturing environments.

- April 2026: Ivanti released its Q2 2026 product update, advancing Autonomous Endpoint Management with Continuous Compliance for patch management, enabling automatic out-of-band patch deployment to endpoints that missed scheduled maintenance windows, and introduced the EU Sovereign Cloud edition of Neurons for MDM, purpose-built for regulated European manufacturers requiring verifiable data residency and NIS2-aligned audit controls.

- September 2025: Omnissa unveiled Workspace ONE Vulnerability Defense at Omnissa ONE 2025 in Las Vegas, combining AI-driven remediation with CrowdStrike Falcon Exposure Management to unify vulnerability management, unified endpoint management, and digital employee experience on a single platform, with limited availability launched in late 2025 and agentic AI-powered automation planned for subsequent releases.

- August 2025: SOTI announced a strategic partnership with Advantech, a global IoT intelligent systems provider, to integrate SOTI MobiControl and SOTI XSight into Advantech's industrial edge computing solution portfolio, enabling scalable mobility management across Android, iOS, Windows, and Linux platforms for manufacturing, smart logistics, and industrial automation deployments.

Global UEM In Manufacturing Market Report Scope

The UEM in Manufacturing Market focuses on solutions that enable the centralized management of devices, applications, and data within manufacturing environments. The scope of the report includes analyzing the adoption of UEM solutions across various manufacturing industries, assessing their impact on operational efficiency, and identifying key trends, drivers, and challenges shaping the market. The study covers the market dynamics, competitive landscape, and technological advancements influencing UEM implementation in manufacturing.

The UEM in Manufacturing Market Report is Segmented by Component (Solutions [Device Management, Application Management, Content Management, Security and Compliance Management, and Analytics and Automation], and Services), Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions | Device Management |

| Application Management | |

| Content Management | |

| Security and Compliance Management | |

| Analytics and Automation | |

| Services |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Nordics | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Component | Solutions | Device Management |

| Application Management | ||

| Content Management | ||

| Security and Compliance Management | ||

| Analytics and Automation | ||

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Nordics | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and future value of UEM in manufacturing?

The UEM in manufacturing market was valued at USD 0.75 billion in 2025, rose to USD 0.90 billion in 2026, and is forecast to reach USD 2.52 billion by 2031 at a CAGR of 22.87%.

Why are manufacturers investing more in unified endpoint management?

The main reasons are rising endpoint diversity, stronger cybersecurity pressure, remote plant support needs, and the need to keep IT, OT, and shared devices under one policy framework.

Which deployment model leads to adoption across factories?

Cloud-based deployment led with 61.59% of revenue in 2025 because it supports subscription pricing, remote updates, and easier multi-site management.

Which company size is creating the fastest growth opportunity?

Small and medium-sized enterprises are expected to post the fastest expansion, with a projected CAGR of 23.51% from 2026 to 2031.

Which region currently leads demand?

Asia-Pacific led in 2025 with 37.26% of revenue, supported by large manufacturing bases, mobile-first enterprise setups, and growing smart factory activity.

What makes competition difficult for new vendors?

Vendors need more than device control. They need strong rugged-device support, OT and MES integration, compliance features, and proven performance in real plant environments.

Page last updated on: