UEM In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.99 Billion |

| Market Size (2031) | USD 3.93 Billion |

| Growth Rate (2026 - 2031) | 31.75% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UEM In Healthcare Market Analysis by Mordor Intelligence

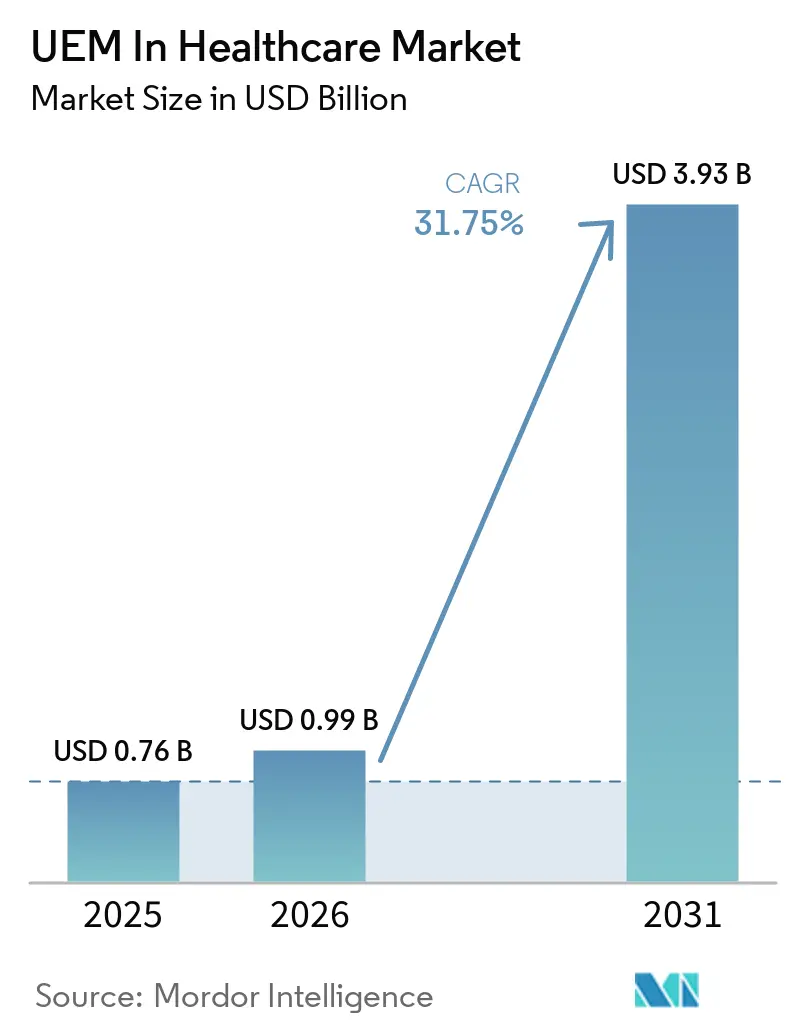

The UEM in Healthcare Market size was valued at USD 0.76 billion in 2025 and estimated to grow from USD 0.99 billion in 2026 to reach USD 3.93 billion by 2031, at a CAGR of 31.75% during the forecast period (2026-2031). The UEM in Healthcare Market is advancing as hospitals, clinics, and home care programs manage a wider mix of shared tablets, personal phones, infusion pumps, diagnostic terminals, and remote monitoring devices through a single control layer. Cybersecurity pressure is keeping endpoint governance high on healthcare IT budgets because breach costs remain severe and unresolved vulnerabilities persist in clinical environments for long periods. The UEM in Healthcare Market is also supported by tighter audit and security expectations, which are moving device control from a technical task to a broader governance issue across many health systems. Vendor strategy is now centered on cloud delivery, automation, and identity-aware policy controls because buyers want faster rollout and lower administrative burden across distributed care settings. Even so, legacy hospital systems and weak budgets at smaller providers still slow some projects, which keeps the UEM in Healthcare Market open to vendors that can simplify integration, pricing, and ongoing support.

Key Report Takeaways

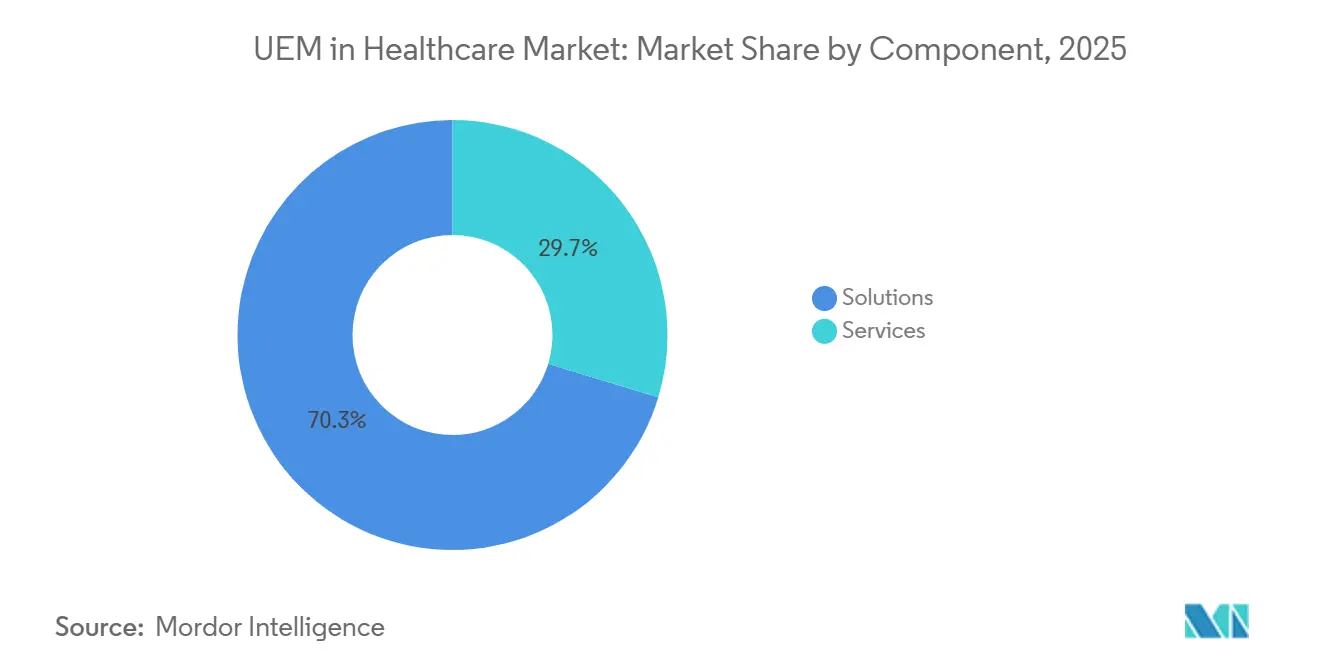

- By component, solutions accounted for 70.32% of UEM in Healthcare Market share in 2025 and are projected to expand at a 32.56% CAGR through 2031.

- By deployment mode, cloud-based deployment accounted for 67.54% of revenue in 2025 and is projected to expand at a 32.79% CAGR through 2031.

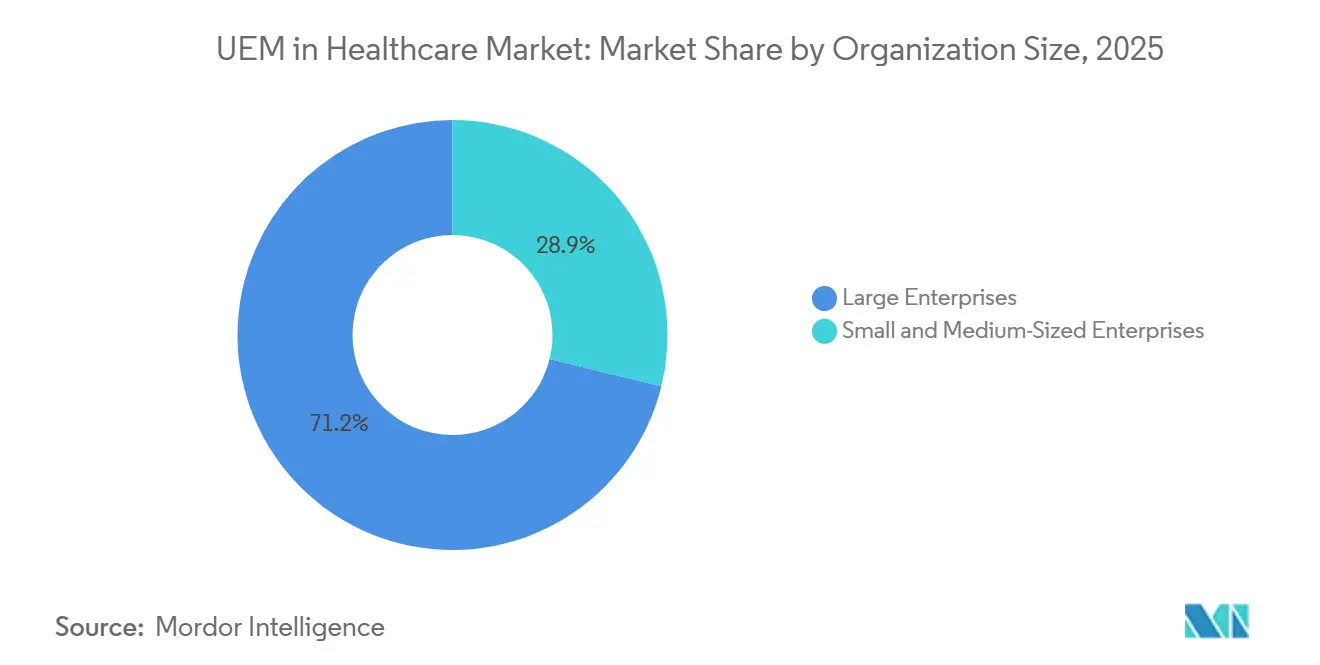

- By organization size, large enterprises accounted for 71.15% of revenue share in 2025, while Small and Medium-Sized Enterprises are projected to grow at a 32.41% CAGR through 2031.

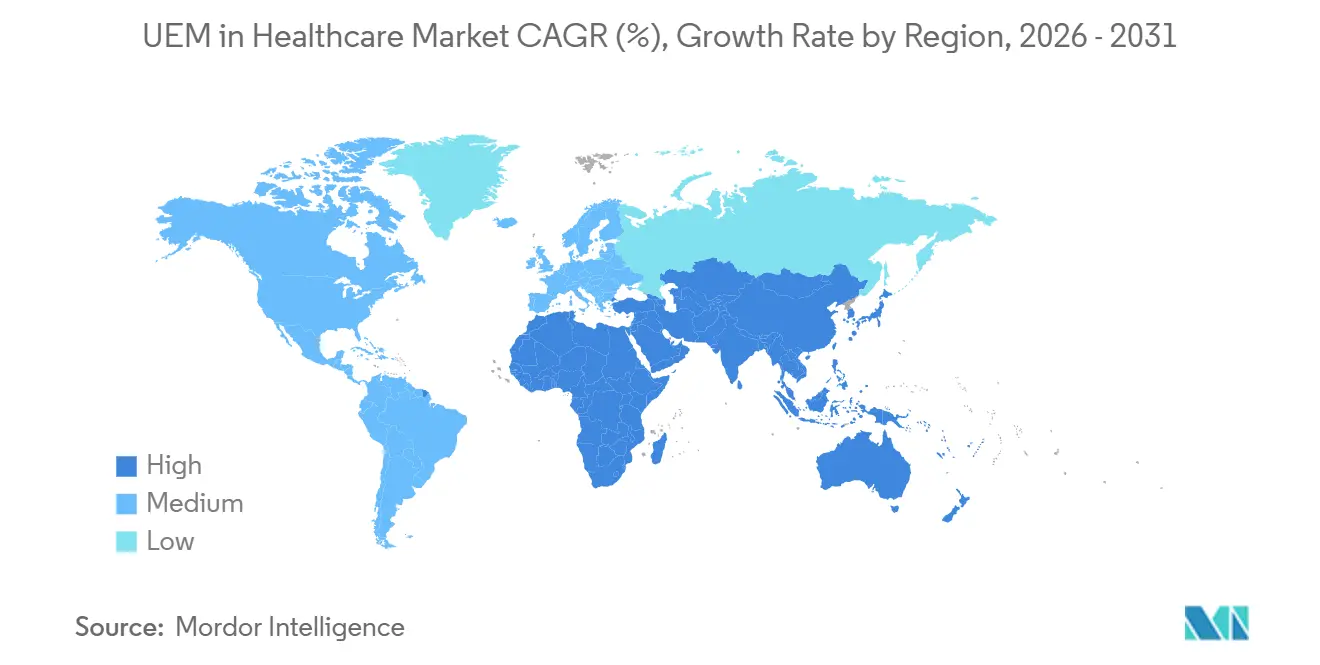

- By geography, North America held 41.38% revenue share in 2025, while Asia-Pacific is projected to expand at a 32.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global UEM In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Need for Centralized Endpoint Security Across Connected Care Environments | +8.2% | Global | Short term (≤ 2 years) |

| Expanding Bring Your Own Device Adoption in Clinical Workflows | +7.1% | North America and Asia-Pacific, with Europe, Middle East, and Africa spillover | Short term (≤ 2 years) |

| Increasing Compliance Pressure for Healthcare Data Protection and Auditability | +5.8% | North America (HIPAA), Europe (GDPR, NIS2), APAC (Japan, Australia) | Medium term (2-4 years) |

| Growth in Remote Care Delivery and Mobile Clinical Access | +4.6% | North America, Europe, APAC core | Short term (≤ 2 years) |

| Cross-Facility Identity and Session Mobility for Temporary Clinical Staff | +2.7% | North America, APAC | Medium term (2-4 years) |

| Rising Demand for Zero Trust Policy Enforcement on Shared Medical Devices | +2.3% | North America and APAC core, spillover to MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Need for Centralized Endpoint Security Across Connected Care Environments

The UEM in Healthcare Market is seeing strong demand because every unmanaged device can become an entry point into systems that hold sensitive patient and operational data. Verizon’s 2026 findings showed that vulnerability exploitation, phishing, and stolen credentials remained the leading healthcare access vectors, underscoring the need for patching, application control, and identity-enforced access in a single platform.[1]Verizon, “2026 Data Breach Investigations Report,” Verizon Communications Inc., textbookofdigitalhealth.com A 2026 review of the Stryker cyberattack found that attackers targeted identity and certificate management layers, the same control plane that advanced UEM platforms are built to govern. Netskope reported that regulated data accounted for 82% of data policy violations in healthcare cloud environments, indicating that endpoint risk often originates in cloud application behavior rather than at the network edge. That shift matters because hospitals can no longer separate device security from cloud access policy, session control, and device posture checks. As a result, the UEM in Healthcare Market is moving beyond device enrollment and into broader security orchestration across clinical workstations, mobile devices, and remote care endpoints.

Expanding Bring Your Own Device Adoption in Clinical Workflows

The UEM in Healthcare Market is also being driven by the widening gap between personal device use in hospitals and the formal controls needed to govern it. Imprivata’s July 2025 survey of 400 acute care leaders found that 81% of clinicians turned to personal devices when shared equipment was unavailable, and 79% admitted to sharing login credentials to gain access, which creates direct HIPAA exposure. A 2025 JMIR Human Factors study at a major public hospital in Victoria found a BYOD security maturity score of 2.04 out of 5, indicating that many large facilities still rely on ad hoc practices rather than formal endpoint governance. The same study identified UEM as the highest maturity level in the device security taxonomy, which makes the current gap easy for hospital leaders to frame and prioritize. That means healthcare buyers are not simply funding device access; they are funding a way to close known compliance and accountability gaps that already exist inside clinical workflows. The UEM in Healthcare Market is therefore benefiting from BYOD not as a convenience trend, but as a control problem that has become too visible to ignore.

Increasing Compliance Pressure for Healthcare Data Protection and Auditability

The UEM in Healthcare Market is gaining support from a regulatory environment that became materially stricter in 2025 and remains active in 2026. The U.S. Department of Health and Human Services published a proposed HIPAA Security Rule update in January 2025 that introduced mandatory requirements for multi-factor authentication, AES-256 encryption, biannual vulnerability scanning, and annual penetration testing, all of which closely align with the requirements that enterprise UEM platforms enforce or orchestrate. In Japan, the Ministry of Health, Labor and Welfare updated its FY2025 healthcare cybersecurity checklist and required hospitals to document the implementation of two-factor authentication or a defined path to compliance by fiscal year 2027. Germany’s NIS2 implementation, which came into force in December 2025, pushed hospitals classified as critical infrastructure to strengthen endpoint risk management, incident reporting, and governance documentation. Those obligations matter because they shift device control from a best-practice project into a documented compliance responsibility for hospital management. The UEM in Healthcare Market is therefore moving higher on procurement lists because legal and audit teams now have more direct influence over endpoint decisions.

Growth In Remote Care Delivery and Mobile Clinical Access

The UEM in Healthcare Market is also benefiting from the spread of remote care, mobile clinical access, and care delivery outside the traditional hospital perimeter. FAIR Health reported that telehealth utilization among commercially insured patients reached 15.2% of all medical claim lines in December 2025, indicating that remote care remained embedded in care delivery rather than fading after the pandemic. Every remote session initiated on a clinical device outside a facility boundary requires authentication, policy enforcement, and traceability that local tools cannot manage well at scale. Mobile Health Map reported in 2025 that more than 3,600 mobile clinics delivered over 10 million visits each year in the United States, which shows how quickly care delivery is expanding across distributed physical settings. That model multiplies device fleets that operate outside fixed IT perimeters, underscoring the need for a single administrative layer across tablets, phones, and shared workstations. The UEM in Healthcare Market is therefore supported by telehealth, mobile clinics, remote patient monitoring, and ambulatory expansion, as all 4 models depend on secure endpoint continuity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration of Complexity with Legacy Hospital Information Systems | -2.5% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Budget Constraints in Mid-Sized Care Providers and Public Health Networks | -1.6% | South America, Africa, smaller markets in Europe and APAC | Long term (≥ 4 years) |

| Clinical Workflow Friction from Overly Restrictive Device Policies | -1.0% | North America, Europe | Short term (≤ 2 years) |

| Limited Standardization Across Medical Device Operating Environments | -0.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity with Legacy Hospital Information Systems

Integration friction with older infrastructure remains the strongest technical restraint on the UEM in Healthcare Market. SOTI reported in June 2025 that 65% of healthcare organizations still used unintegrated, outdated systems for IoT and telehealth medical devices, while 59% reported downtime or technical issues due to legacy system conflicts. Many laboratory, imaging, and hospital information systems still run on operating system versions that either do not support modern UEM agents or create policy conflicts during rollout. Integration also becomes harder when hospitals rely on HL7 v2 interfaces, non-FHIR environments, or custom middleware layers, which can extend deployment from weeks to quarters. Those timelines compete with day-to-day clinical operations and delay projects for already stretched IT teams, even when demand remains strong. The UEM in Healthcare Market therefore faces a timing problem rather than a demand problem, since many organizations want the capability but struggle to fit it into legacy modernization schedules.

Budget Constraints in Mid-Sized Care Providers and Public Health Networks

The UEM in healthcare market also faces slower uptake in mid-sized hospitals, community facilities, and public health networks operating under persistent budget pressure. Subscription pricing can be difficult for providers that already manage narrow reimbursement margins and limited room for new software categories. The strain is sharper in lower-income settings across South America and Africa, where procurement processes, contract management capacity, and long-term software funding are often less mature. Cloud-native vendors are responding with tiered pricing and managed service delivery, but the sales cycle still runs longer for cost-sensitive buyers than for large integrated networks. This creates a split market in which growth concentrates in larger health systems, while smaller organizations continue to carry unmanaged endpoint risk. The UEM in healthcare market still has a large pool of unmet demand in this tier, but conversion depends on simpler pricing, channel support, and lower implementation burden.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Dominate as Platform Depth Widens

Solutions held 70.32% of the UEM in Healthcare Market share in 2025, and demand remained concentrated across device management, application management, content management, security and compliance management, and analytics and automation. Device management, security, and compliance management stayed the most established layers because hospitals still need encryption, remote wipe, access control, and audit support across shared clinical devices. Application management gained ground as providers tried to control which clinical apps reached endpoints, especially as AI-assisted diagnostics and third-party telehealth tools became more common. Content management also drew stronger interest from imaging-heavy specialties that needed governed distribution of radiology and pathology files across mixed device fleets. The UEM in Healthcare Market continued to favor broad platforms in this segment because buyers wanted fewer disconnected tools and clearer accountability for policy enforcement.

Analytics and automation remained the fastest-evolving areas within solutions, as health systems began using endpoint behavior data to detect anomalies, predict device issues, and automate remediation workflows. Ivanti expanded its platform in January 2026 with agentic AI capabilities aimed at automating endpoint discovery and remediation, which matched the staffing reality of hospital IT teams that manage large device fleets with limited headcount.[2]Ivanti, “Ivanti Launches Sovereign Cloud Solution to Support European Data Sovereignty and Compliance,” Ivanti, ivanti.com Services, which include deployment, managed support, and post-implementation optimization, accounted for the remaining share of the UEM in Healthcare Market and grew alongside rollout complexity in multi-facility environments. Managed service models gained traction inside the services layer because smaller provider teams often preferred outsourced governance over adding internal specialists. This mix shows that the UEM in Healthcare Market is rewarding vendors that can pair strong product depth with a delivery model that matches the operational limits of healthcare IT teams.

By Deployment Mode: Cloud Accelerates as Hybrid Gains Strategic Ground

Cloud-based deployment in the UEM in Healthcare Market size is projected to expand at a 32.79% CAGR from 2026 to 2031, which makes it the highest-velocity deployment model in the current mix. Cloud delivery fits healthcare’s need to govern devices across hospitals, ambulatory clinics, home health settings, and remote monitoring programs without adding large local infrastructure costs. It also aligns with zero-trust operating models because policy enforcement stays continuous even when staff, contractors, and devices move across facility boundaries. Microsoft widened the cloud adoption path in 2026 by bundling advanced Intune Suite capabilities into Microsoft 365 E3 and E5 subscriptions at no additional cost, lowering the entry barrier for existing healthcare customers already built on the Microsoft stack. The UEM in Healthcare Market is therefore seeing cloud adoption move from an option for large systems into a more practical standard for mid-sized organizations as well.

On-premise deployment kept a meaningful role in the UEM in Healthcare Market because some hospitals still manage classified research data, government-linked workloads, or sovereignty-sensitive telemetry that cannot move freely to the cloud. Hybrid deployment emerged as a practical middle route for integrated delivery networks that wanted cloud scalability for mobile endpoints and local control for fixed clinical workstations tied to EMR and PACS environments. Ivanti’s June 2026 launch of Neurons for MDM, Sovereign Edition, EU showed how vendors are trying to bridge compliance and cloud convenience through region-specific architectures operated through certified data centers. That move matters because architecture choice is no longer a simple cloud versus on-premise debate, it is now a governance design issue shaped by geography, data sensitivity, and legacy integration needs. The UEM in Healthcare Market is thus shifting toward architecture-agnostic platforms that can support mixed environments without forcing buyers into one operating model.

By Organization Size: SMEs Emerge as the New Growth Engine

Large enterprises accounted for 71.15% of the market share in 2025 because integrated health networks, academic medical centers, and major regional systems manage broad endpoint estates across many facilities. These organizations could justify full-featured platforms with advanced analytics, custom policies, and dedicated implementation teams because the operational load of unmanaged devices was already visible at scale. Imprivata’s 2025 shared mobile device study found that IT staff in larger institutions spent 32% of their time on device maintenance and 50% on device tracking and monitoring, underscoring how much labor can be absorbed by manual oversight in large hospital environments. Large providers also remained the main recipients of vendor integration support around Epic, Oracle Health, and Cerner environments, since those buyers shaped pricing, service design, and product roadmaps. The UEM in Healthcare Market therefore remained anchored by large enterprise spending even as growth momentum broadened.

Small and Medium-Sized Enterprises in the UEM in Healthcare Market size are projected to expand at a 32.41% CAGR from 2026 to 2031 as cloud-native pricing lowers the cost barrier for smaller providers entering formal endpoint management. Community hospitals, specialty clinics, imaging centers, and home health agencies are now joining the UEM in Healthcare Market because unmanaged endpoint fleets create both audit exposure and day-to-day operational drag. Hexnode’s May 2026 healthcare MSP guidance reflected a clear vendor view that SME buyers prefer managed, consumption-based delivery instead of direct software procurement with large internal setup demands. That behavior is changing roadmaps across the UEM in Healthcare Market, with more emphasis on quick onboarding, prebuilt compliance templates, and role-based policy libraries that smaller teams can activate without deep specialist expertise. The difference between enterprise and SME buying behavior is now shaping competition almost as much as the underlying security requirement itself.

Geography Analysis

North America accounted for 41.38% share of the UEM in Healthcare Market size in 2025, which kept the region in the lead on the back of strong HIPAA enforcement, dense health system networks, and high healthcare IT spending. The United States remained the main driver because the January 2025 proposed HIPAA Security Rule update specified technical controls, such as multi-factor authentication, AES-256 encryption, biannual vulnerability scanning, and annual penetration testing, that directly map to UEM capabilities.[3]U.S. Department of Health and Human Services, “Notice of Proposed Rulemaking: Modifications to the HIPAA Security Rule,” Federal Register, govinfo.gov Canada and Mexico remained meaningful secondary markets because unresolved endpoint governance gaps still sit alongside telehealth growth and older infrastructure. Microsoft and Jamf held visible positions across North American healthcare because many hospital buyers already used their broader enterprise environments and could extend device control from there. In 2026, Microsoft added Intune Suite value within existing Microsoft 365 subscriptions, widening cloud UEM access for mid-sized health systems that were previously less able to justify a separate premium platform.

Asia-Pacific in the UEM in Healthcare Market is projected to grow at a 32.83% CAGR from 2026 to 2031, making it the fastest-growing regional market in the current forecast period. Japan is a key driver because its FY2025 healthcare cybersecurity checklist set a documented path toward two-factor authentication compliance by fiscal year 2027, which creates a direct timetable for endpoint governance upgrades. South Korea is also strengthening the backdrop through government-led digital health infrastructure expansion that increases the number of connected endpoints in public hospital systems. India adds another growth layer because government digitization efforts under the Ayushman Bharat Digital Mission are bringing more clinical workflows and endpoint assets into managed digital environments. Australia reinforces the regional case because tighter data breach expectations and a 77% rate of unintegrated legacy systems in the 2025 SOTI survey combine compliance pressure with clear infrastructure gaps.

Europe remained structurally important in the UEM in Healthcare Market because Germany, the United Kingdom, France, and the Nordics combined regulatory pressure with mature hospital IT estates. Germany stood out after NIS2 came into force in December 2025, because hospitals classified as critical infrastructure now face stronger obligations around endpoint risk management, reporting, and executive oversight. Local providers such as Aagon GmbH and Baramundi Software show that region-specific compliance needs can still support specialized vendors even when global platforms remain active. The United Kingdom, the Middle East and Africa, and South America added supplementary growth, with the Middle East supported by hospital digitization programs in Saudi Arabia and the United Arab Emirates, and South America supported by rising compliance expectations in Brazil and the growth of private hospital networks in Chile, Argentina, and Colombia.

Competitive Landscape

The UEM in Healthcare Market remained moderately fragmented, with Microsoft, IBM, and Ivanti competing as platform-scale vendors pursued narrower positions across defined buyer groups. Competition in the UEM in Healthcare Market is shaped less by basic device control and more by how well a vendor connects endpoint management with identity, cloud security, analytics, and healthcare workflow needs. Microsoft’s position is strengthened by the wider Azure, Entra ID, and Microsoft 365 stack, which makes Intune a default evaluation option in hospitals that already run much of their productivity and identity environment on Microsoft tools.[4]Microsoft Corporation, “Faster, More Personalized Service Begins at the Frontline with Microsoft Intune,” Microsoft Security Blog, microsoft.com Jamf strengthened its healthcare relevance in April 2025 through the Identity Automation acquisition, which brought dynamic identity management into its Apple-focused platform and improved support for role changes, shift schedules, and location-based access in clinical settings. That move matters in the UEM in Healthcare Market because nursing, temporary staffing, and shared-device use all depend on fast role-appropriate access that changes during the workday.

Ivanti continued to compete in the UEM in Healthcare Market through a dual focus on automation and compliance fit. Its January 2026 Neurons expansion added agentic AI and broader asset visibility, which matched hospital demand for faster discovery and remediation without proportional staffing increases. Its June 2026 sovereign cloud launch for Europe showed an effort to capture regulated buyers that want cloud delivery without compromising regional governance expectations. These moves suggest that differentiation in the UEM in Healthcare Market is increasingly tied to how vendors reduce operational effort while still meeting strict audit needs. Smaller vendors kept pressuring the leaders in the UEM in Healthcare Market through vertical focus and faster product iteration.

Hexnode launched a native identity provider in 2026 that used device compliance signals for conditional access decisions, which simplified the link between identity and endpoint control for smaller healthcare teams. SOTI’s 2026.1 release added shared-device security and automation features that directly targeted frontline healthcare workflows where shift changes and device handoffs create daily friction. The Alliance for Smart Healthcare Excellence also announced the development of a Zero Trust Maturation Model for healthcare, which is likely to influence future buying criteria by giving health systems a more common framework for endpoint security progress. Broadcom’s VMware pricing changes also created an opening for alternative vendors because some enterprise healthcare buyers began reassessing cost and interoperability tradeoffs across their endpoint stack.

UEM In Healthcare Industry Leaders

Microsoft Corporation

IBM Corporation

Citrix Systems, Inc.

Ivanti, Inc.

Jamf Holding Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Hexnode published a healthcare MSP UEM framework guide detailing how managed service providers can structure healthcare endpoint management practices around compliance, security, and operational automation, supporting the growing MSP-delivered UEM channel in the SME healthcare segment.

- March 2026: The Health Information Sharing and Analysis Center, Health-ISAC, published best practices for configuring Microsoft Intune tenant administration to prevent unauthorized device wipes, addressing a governance gap that had caused operational disruptions in several U.S. health systems.

- October 2025: Francisco Partners announced a definitive agreement to acquire Jamf in an all-cash transaction valued at USD 2.2 billion, representing a USD 13.05 per share offer. The deal received unanimous board approval and reflected Jamf's strategic intent to use private-company flexibility to accelerate growth through innovation and acquisitions.

- July 2025: Imprivata released its 2025 State of Shared Mobile Devices in Healthcare Report, based on a survey of 400 leaders at acute care facilities across the United States, Canada, United Kingdom, and Australia, documenting that 92% of healthcare leaders consider mobile devices essential to care delivery and that shared-use device strategies save facilities an average of USD 1.1 million annually versus individual assignment or BYOD models.

Global UEM In Healthcare Market Report Scope

The UEM in Healthcare Market focuses on solutions that enable the centralized management of devices, applications, and data within healthcare organizations. The scope of the report includes analyzing the adoption of UEM solutions in healthcare settings and their impact on operational efficiency, regulatory compliance, and data security. It also examines market trends, growth drivers, challenges, and competitive dynamics within the forecast period.

The UEM in Healthcare Market Report is Segmented by Component (Solutions [Device Management, Application Management, Content Management, Security and Compliance Management, and Analytics and Automation], and Services), Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions | Device Management |

| Application Management | |

| Content Management | |

| Security and Compliance Management | |

| Analytics and Automation | |

| Services |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Nordics | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Component | Solutions | Device Management |

| Application Management | ||

| Content Management | ||

| Security and Compliance Management | ||

| Analytics and Automation | ||

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Nordics | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the UEM in Healthcare Market?

The UEM in Healthcare Market was valued at USD 0.76 billion in 2025, stands at USD 0.99 billion in 2026, and is forecast to reach USD 3.93 billion by 2031 at a 31.75% CAGR.

What is driving demand for endpoint management in healthcare settings?

The main drivers are rising cyber risk, growing BYOD use, stricter HIPAA and other compliance expectations, and the spread of remote and mobile care models that need centralized device control.

Which deployment model is expanding the fastest in healthcare endpoint management?

Cloud-based deployment is the fastest-growing model, with a projected 32.79% CAGR from 2026 to 2031, supported by easier scaling and lower infrastructure burden.

Which organization size segment is creating the next wave of growth?

Small and Medium-Sized Enterprises are projected to grow at a 32.41% CAGR through 2031 as cloud pricing and managed services make formal endpoint governance more practical for smaller providers.

Which region leads adoption and which region is growing the fastest?

North America led with a 41.38% share in 2025, while Asia-Pacific is projected to record the fastest growth at a 32.83% CAGR through 2031.

What is shaping vendor competition in this space?

Competition is centered on cloud delivery, identity integration, automation, compliance support, and healthcare workflow fit, with Microsoft, Ivanti, Jamf, SOTI, Hexnode, and IBM remaining key names.

Page last updated on: