UEM In BFSI Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.39 Billion |

| Market Size (2031) | USD 4.47 Billion |

| Growth Rate (2026 - 2031) | 26.32% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UEM In BFSI Market Analysis by Mordor Intelligence

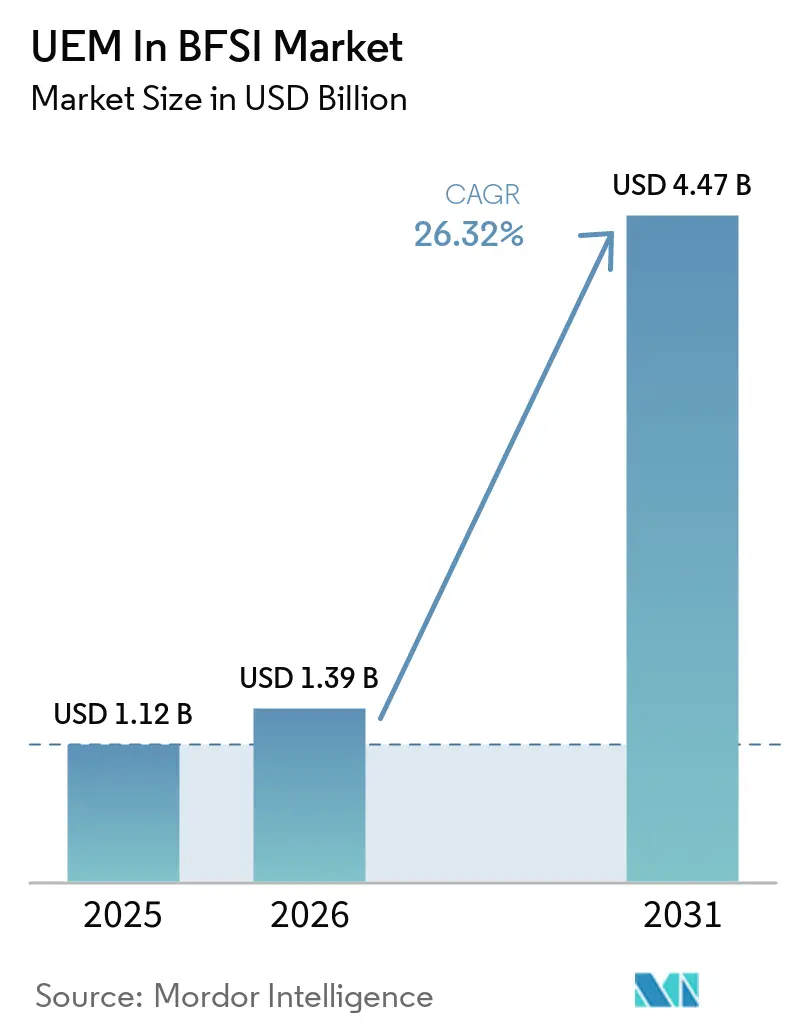

The UEM in BFSI market size was valued at USD 1.12 billion in 2025 and estimated to grow from USD 1.39 billion in 2026 to reach USD 4.47 billion by 2031, at a CAGR of 26.32% during the forecast period (2026-2031). The UEM in BFSI market is expanding as banks, insurers, and financial firms manage larger fleets of ATMs, payment kiosks, branch devices, trading workstations, remote laptops, and enrolled mobile devices across daily operations. DORA from January 2025 and PCI-DSS v4.0 compliance have turned endpoint governance into an auditable control, thereby shortening buying cycles and reducing purely discretionary spending. Hybrid work, BYOD policies, and zero-trust programs have pushed institutions to continuously verify device posture rather than rely on periodic checks. Cloud-native policy engines and AI-led automation are gaining traction because they support real-time enforcement, broader visibility, and tighter operating discipline across distributed device estates. Data residency rules, legacy integration costs, and vendor restructuring still limit choice, yet the UEM in BFSI market continues to open room for vendors that combine compliance depth, sovereign deployment options, and simpler commercial models.

Key Report Takeaways

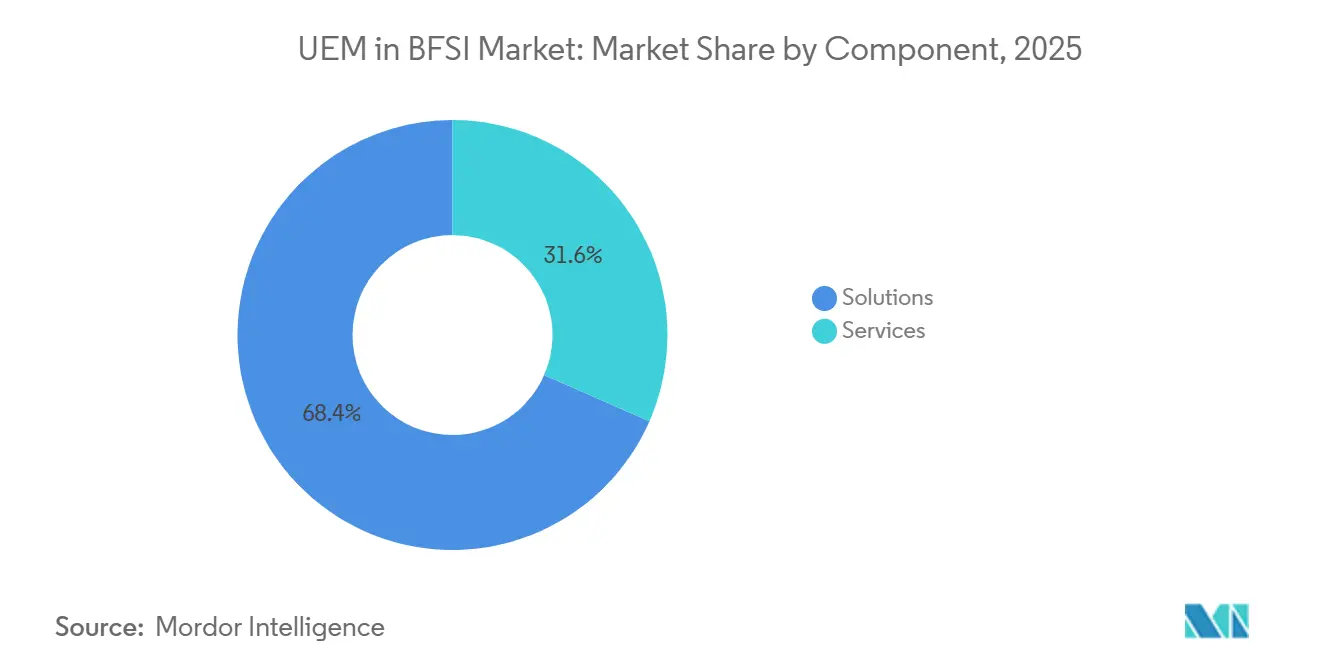

- By component, solutions accounted for 68.43% of UEM in BFSI Market share in 2025 and are projected to expand at a 27.45% CAGR through 2031.

- By deployment mode, cloud-based deployment accounted for 66.27% of revenue in 2025 and is projected to expand at a 27.59% CAGR through 2031.

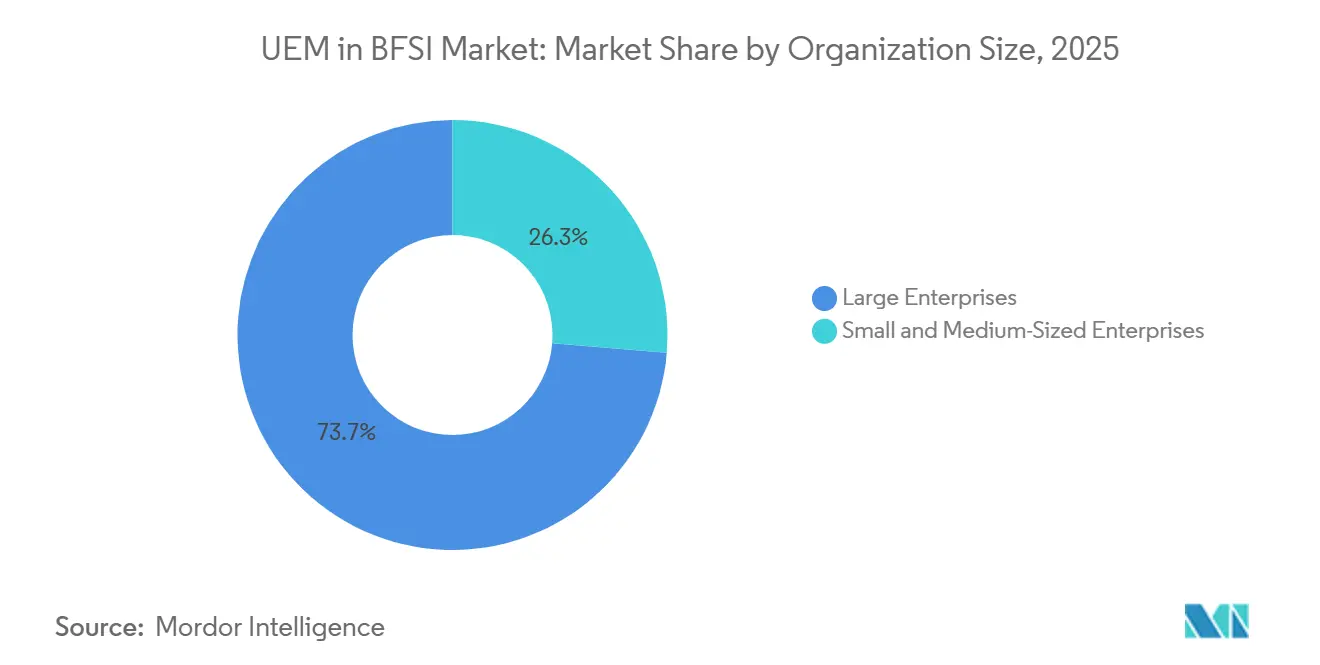

- By organization size, large enterprises accounted for 73.68% of UEM in BFSI Market share in 2025, while small and medium-sized enterprises are projected to grow at a 27.61% CAGR through 2031.

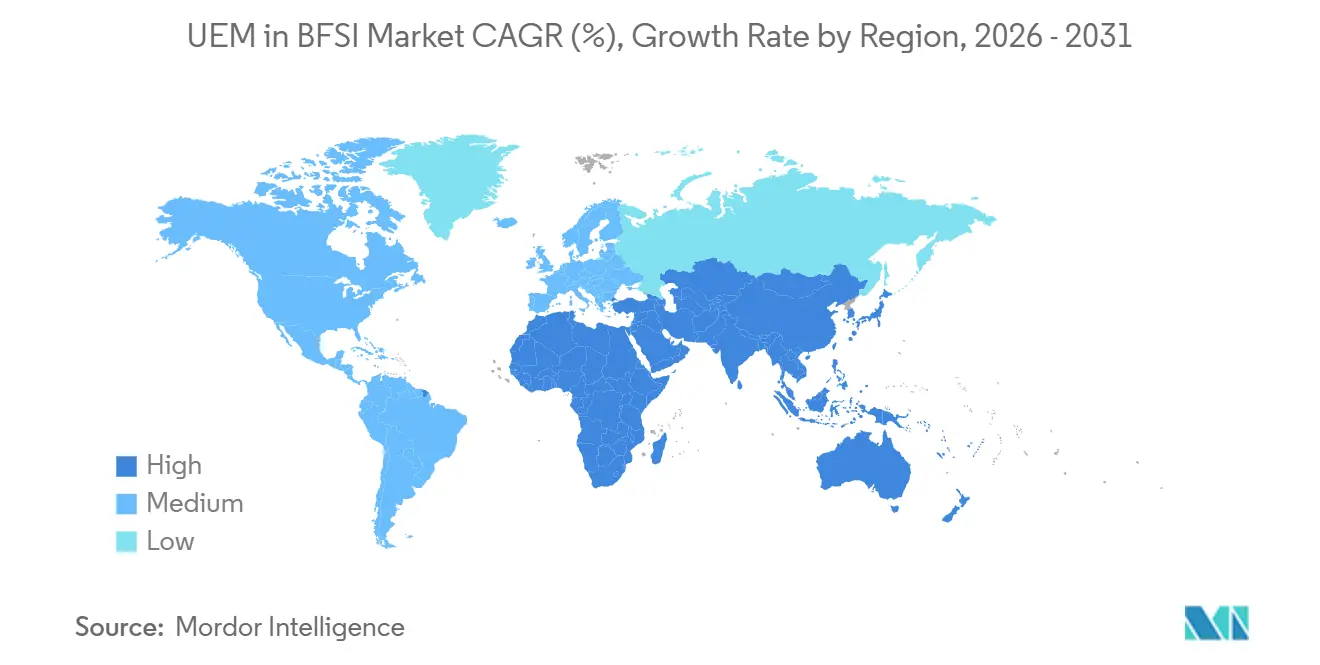

- By geography, North America held 36.14% of revenue in 2025, while Asia-Pacific is projected to grow at a 27.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global UEM In BFSI Market Trends and Insights

Driver Imapct Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid Work and BYOD Expansion in Banking Operations | +5.5% | Global, strongest pull in North America and Western Europe | Short term (≤ 2 years) |

| Zero Trust Rollouts Across Financial Institutions | +4.8% | Global, North America and EU core, spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Convergence of UEM with Identity and Access Controls | +4.2% | Global, early intensity in North America and Western Europe | Medium term (2-4 years) |

| AI-Driven Digital Employee Experience Optimization | +3.6% | North America, Western Europe, and advanced Asia-Pacific markets | Medium term (2-4 years) |

| Device-Level Carbon and Energy Reporting for ESG Commitments | +2.8% | EU core, spill-over to Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Growth in Frontline and Specialized Endpoint Fleets | +2.2% | Asia-Pacific core, South America, and Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hybrid Work and BYOD Expansion in Banking Operations

The UEM in BFSI market is seeing stronger demand because hybrid work has made personal-device governance a core security task for banks and insurers. Bank of America’s 2024 guidance states that institutions need clear rules on which devices can enter BYOD programs, along with endpoint security, VPN controls, and multifactor authentication to protect sensitive financial data.[1]Bank of America, “Cyber Security Journal, Securing Hybrid and Remote Workforces,” Bank of America, business.bofa.com That operating model increases the number of managed nodes because every approved laptop or mobile device that connects to core banking systems requires policy enforcement, lifecycle management, and secure access management. Shared and distributed branch devices add to the same workload because frontline worker deployments still require secure user separation and controlled sign-in behavior across common endpoints. Small Finance Bank’s rollout of ManageEngine Mobile Device Manager Plus across 25,000 devices shows how large financial institutions are already managing remote branches, shared devices, and BYOD endpoints through centralized policy frameworks. In practice, this makes endpoint posture a standing control in day-to-day banking operations, which is why the UEM in BFSI market keeps moving closer to mainstream security and compliance budgets.

Zero Trust Rollouts Across Financial Institutions

The UEM in BFSI market is also benefiting from zero trust programs that place device verification alongside identity, network, application, and data controls. The European Commission’s DORA technical standards require the secure management of portable and non-portable endpoint devices within the broader ICT risk framework, providing regulated institutions with a direct policy basis for stronger endpoint control. Research in the World Journal of Advanced Engineering Technology and Sciences describes endpoint protection, device attestation, and mobile device management as core enforcement tools within zero-trust environments for financial institutions. The EBA’s DORA preparation work also reinforces the need for financial entities to strengthen operational resilience and third-party ICT oversight, which supports more disciplined device governance across payment and transaction environments. As a result, the UEM in BFSI market is moving toward tools that combine policy depth, live posture monitoring, and faster response actions under regulated zero trust programs.

Convergence of UEM With Identity and Access Controls

The UEM in BFSI market is being shaped by tighter links between device governance and identity controls, as financial institutions try to reduce fragmented access policies across multiple systems. Research published in May 2026 found that 58% of financial sector respondents used 3 or more IAM solutions, while 51% identified rising IAM costs as their top challenge, indicating clear pressure for integration. The same direction emerged in March 2026, when Hexnode introduced a native identity provider within its UEM platform and tied zero-trust access to live device posture signals. This kind of architecture helps banks link every access decision to a device state record, making audit trails easier to assemble as control reviews become more detailed. It also increases the cost of delay because institutions that keep IAM and endpoint management in separate silos create more operational gaps across policy, logging, and remediation. This is why the UEM in BFSI market is giving more weight to platforms that present identity and device governance through one control layer instead of through disconnected point tools.

AI-Driven Digital Employee Experience Optimization

The UEM in BFSI market is widening beyond device administration because AI-led digital employee experience tools give operations teams earlier visibility into service issues and user disruption. Ivanti’s 2025 DEX report found that only 32% of organizations used UEM tools integrated with DEX capabilities, suggesting that most institutions still have room to add experience-level monitoring to their existing endpoint programs. That matters in financial services because endpoint telemetry can surface crash rates, login delays, and session failures before they widen into service-continuity events. A 2025 finance sector review also linked prolonged IT outages at major UK banking institutions to internal systems rather than cyberattacks, which keeps the focus on internal device and application stability as much as on perimeter defense. The same review cited savings from endpoint telemetry, including GBP 3.4 million (USD 4.35 million) in unused software licenses and GBP 7.5 million (USD 9.6 million) in avoided laptop refresh spending when replacement decisions were tied to actual performance data. Those use cases help explain why the UEM in BFSI market is starting to treat endpoint experience data as both an operating signal and a stronger piece of resilience evidence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Sovereignty and Privacy Compliance Constraints | -3.2% | EU core, secondary impact in Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| High Migration and Integration Cost of Legacy Estates | -2.8% | Global, highest in North America and Europe with established mainframe footprints | Long term (≥ 4 years) |

| Procurement Uncertainty Following Broadcom and VMware Ecosystem Changes | -2.1% | Global, highest in North America and Western Europe | Short term (≤ 2 years) |

| Shortage of UEM Automation and Scripting Skills | -1.6% | Global, most acute in emerging markets within Asia-Pacific, South America, and Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Sovereignty and Privacy Compliance Constraints

The UEM in BFSI market faces one of its clearest limits in data sovereignty because endpoint platforms now sit inside formal requirements on data location, encryption handling, and exit planning. IAPP’s 2025 review of GDPR and DORA integration shows that financial institutions must treat ICT contracts as compliance instruments, not as routine vendor paperwork, which narrows the field for cloud deployments. Ivanti’s April 2026 launch of a sovereign EU edition for Neurons for MDM, hosted on BSI-certified European infrastructure and aligned with the EU Cloud Sovereignty Framework, shows how directly vendors are responding to this pressure. France also added to the compliance load when ACPR endorsed the EBA/GL/2025/02 ICT risk management guidelines, effective May 20, 2025, which reinforced local expectations around controlled ICT governance. The practical effect is that vendor selection in the UEM in BFSI market is not only a product decision, because deployment location, data handling, and contractual structure now influence whether a platform can be approved at all. Similar patterns are spreading beyond Europe, keeping sovereign deployment and customer-managed data separation near the center of procurement reviews.

High Migration and Integration Cost of Legacy Estates

The UEM in BFSI market also slows when banks must modernize endpoint operations around long-standing legacy estates that already consume a large share of technology budgets. GFT Technologies stated in 2026 that 52% to 70% of IT budgets in financial institutions were spent maintaining legacy systems rather than improving them, leaving less room for parallel endpoint modernization programs. Even when funding is available, a move to unified endpoint management still requires policy redesign, device re-enrollment across multiple operating systems, and deeper integration with identity directories and security monitoring stacks. Talenbrium reported in 2025 that 55% of BFSI executives in the United States saw an urgent need for upskilling, indicating a labor and execution problem alongside the spending issue. Large rollouts such as AU Small Finance Bank’s 25,000-device implementation also show that distributed branch environments, remote users, and BYOD fleets add operational complexity even after the initial tool choice is made. This is why migration remains a real brake on the UEM in the BFSI market, especially for regional institutions that cannot absorb long implementation cycles without outside support.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platforms Anchor the BFSI Endpoint Control Plane

Solutions accounted for 68.43% of revenue in 2025, keeping software platforms at the center of the UEM in the BFSI market during the base year. Banks and insurers favored broader suites because security and compliance management, device management, and analytics tools are easier to manage when they sit within a single policy structure. That preference is tied to stronger documentation requirements under DORA and related financial controls, where institutions must demonstrate how device risk is identified, monitored, and addressed across the endpoint estate. Application management and content management also gained weight as BYOD programs required banks to separate business data from personal content without weakening oversight.

The services side of the UEM in BFSI market remained smaller, but it gained importance as institutions sought outside help with rollout design, IAM integration, and ongoing compliance validation. Managed services also meet the sector’s need for clearer third-party accountability, as DORA-related contracting emphasizes service continuity and documented control responsibilities. Ivanti’s 2025 DEX report found that only 24% of IT teams reported highly integrated DEX solutions within the broader UEM stack, suggesting a service opportunity in experience monitoring and tool integration. Over time, this leaves the UEM in BFSI industry with a component mix where platforms drive scale, while services support the harder work of integration, policy mapping, and audit readiness.

By Deployment Mode: Cloud Governance Becomes the New Operating Model

Cloud-based deployment is projected to expand at a 27.59% CAGR from 2026 to 2031, making it the fastest-growing deployment path in the UEM in BFSI market. Financial institutions are drawn to cloud control planes because they allow faster policy updates, broader visibility across remote devices, and more consistent compliance checks across widely distributed estates. That model aligns well with zero trust because device state can be validated in near real time instead of through slower synchronization cycles tied to local infrastructure. It also fits the growing need to link endpoint signals with access decisions as banks support more hybrid workers, contractors, and branch staff across multiple locations.

On-premise deployment still held an active role in the UEM in BFSI market because some institutions remain cautious about data location, sensitive workstation categories, and customer-controlled infrastructure boundaries. Hybrid deployment was therefore becoming a practical middle path, with cloud controls applied to standard and mobile fleets while more sensitive assets stayed under tighter local administration. Ivanti’s sovereign EU edition, hosted on BSI-certified infrastructure and aligned with the EU Cloud Sovereignty Framework, shows that vendor success increasingly depends on how well cloud delivery satisfies local compliance requirements. In effect, the UEM in BFSI industry is not moving toward one uniform deployment model, because control depth and jurisdictional rules still shape whether banks choose cloud, on-premise, or a blended design.

By Organization Size: Large Institutions Lead While Mid-Market Demand Rises

Large enterprises held 73.68% of revenue in 2025, which gave them the dominant position in the UEM in BFSI market share during the base year. Their lead came from the scale and variety of assets under management, including branch endpoints, ATM networks, remote advisor devices, shared frontline terminals, and employee-owned mobile devices. Microsoft’s current frontline worker guidance shows how shared device sign-in, user separation, and controlled access remain important for regulated operational settings with frequent shift changes and branch movement.[2]Microsoft, “Get Started with Frontline Worker Device Management, Microsoft Intune,” Microsoft Learn, learn.microsoft.com AU Small Finance Bank’s 25,000-device deployment also illustrates how large BFSI estates require automation, granular policy control, and centralized oversight across dispersed operating environments.

Small and medium-sized enterprises are projected to expand at a 27.61% CAGR from 2026 to 2031, making them the fastest-growing organization group in the UEM in BFSI market size outlook. This growth is tied to cloud-native pricing, easier setup models, and lower infrastructure demands, which reduce the entry barrier for regional lenders, credit unions, and fintech-licensed insurers. Vendors such as NinjaOne, Automox, and ManageEngine have widened their reach by emphasizing lighter deployment requirements and simpler administration for teams with fewer specialists. As this pattern continues, the UEM in BFSI market is likely to see faster adoption outside the largest banks, especially where regulators are extending endpoint governance expectations to institutions that historically operated with smaller formal control programs.

Geography Analysis

North America accounted for 36.14% of revenue in 2025, giving the region the largest position in the UEM BFSI market share during the base year. The region’s lead rests on a mature cybersecurity vendor base, high enterprise cloud use, and a regulatory setting that already pushes banks toward more formalized device governance. United States institutions have moved early on conditional-access endpoint programs, in which real-time device compliance is linked to access decisions rather than recorded as a separate audit record. Canada and Mexico added incremental demand as digital banking expanded and local oversight moved closer to stronger ICT governance expectations. The region still faces an execution gap, as Talenbrium reported in 2025 that 55% of United States BFSI executives identified urgent upskilling needs in modern endpoint platforms.

Europe remained the second-largest contributor to the UEM in BFSI market because GDPR and DORA have pushed endpoint oversight into a more formal board-level compliance discussion. Germany and France stood out as demanding markets where institutions must align technical controls with strict documentation and supervisory expectations. ACPR’s adoption of the EBA/GL/2025/02 ICT risk management guidelines from May 2025 added another layer of governance discipline for French institutions ACPR.[3]Autorité de Contrôle Prudentiel et de Résolution, “Mise en Conformité aux Orientations de l'Autorité Bancaire Européenne EBA/GL/2025/02,” Banque de France, acpr.banque-france.fr South America, the Middle East, and Africa remained earlier-stage regions, but open banking growth, SAMA-led cybersecurity requirements, and formalization of mobile money and distributed agent networks were steadily broadening the addressable device base.

Asia-Pacific is projected to grow at a 27.32% CAGR from 2026 to 2031, which makes it the fastest-growing regional block in the UEM in BFSI market size outlook. India is a major growth engine because digital banking expansion, payment bank activity, and stronger regulated IT risk expectations are increasing the number of managed endpoints across formal financial channels. China adds scale through broad fintech integration and strict data localization practices, which raise the value of centralized endpoint governance across large employee and branch networks. Japan and South Korea contribute through more structured cloud and security oversight across major banks and insurers. Southeast Asia strengthens the regional profile because mobile-first financial services models create growing volumes of customer-facing and employee-managed devices that require tighter policy control.

Competitive Landscape

The UEM in BFSI market reflects a moderately consolidated structure where Microsoft, IBM, and Ivanti, Inc. hold durable positions in large enterprise banking relationships built over several contract cycles. Microsoft remains especially well-positioned because many financial institutions already use Microsoft 365, Azure, and Entra services, making Intune a natural extension of their existing stack. The company’s current frontline worker device guidance also continues to support shared endpoint scenarios that matter in branch and service operations. That installed-base advantage still matters in the sector because regulated buyers often prefer extensions of tools they already know rather than a full reset of endpoint and identity controls. Even so, the UEM in the BFSI market is not closed to challengers, because buying teams are actively testing alternatives that promise simpler deployment, better automation, and stronger sovereign delivery options.

A second competitive theme in the UEM in the BFSI market is the rise of cloud-native challengers that are narrowing the gap with broader incumbents through speed and ease of use. NinjaOne’s June 2026 announcement of a USD 12.3 billion valuation and more than USD 600 million in annual recurring revenue signaled strong market confidence in a simpler single-platform operating model.[4]NinjaOne, “NinjaOne Reaches USD 12.3B Valuation as IT Operations Market Consolidates Around a Single Platform,” NinjaOne, ninjaone.com Ivanti’s April 2026 sovereign EU launch showed another path to differentiation, with certified regional hosting and compliance alignment aimed directly at regulated institutions managing localization risk. These moves show that the competitive discussion now reaches beyond standard device management features and into resilience evidence, deployment control, and policy automation depth.

A third theme is that the UEM in BFSI market is opening white space where device oversight intersects with operational resilience, ESG reporting, and AI-assisted administration. The EBA’s ESG risk guidelines, applicable from November 2026, support closer tracking of operational and reporting practices that can eventually widen the role of endpoint data in governance workflows. Ivanti’s Q2 2026 release added agentic AI and autonomous management features, which points to a race around remediation speed and management depth rather than simple endpoint coverage. For procurement teams, that means vendor choice is increasingly shaped by proof of compliance fit, audit support, and automation quality, not only by who can manage the broadest list of devices.

UEM In BFSI Industry Leaders

Microsoft Corporation

Broadcom Inc.

IBM Corporation

Ivanti, Inc.

Citrix Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: NinjaOne announced a USD 12.3 billion valuation following over USD 400 million in Series C extensions, with participation from Wellington Management, Sequoia Capital, ICONIQ, CapitalG, and Teachers' Venture Growth. The company surpassed USD 600 million in annual recurring revenue, achieving nearly 70% year-over-year growth, and was recognized as a Leader in the 2026 Gartner Magic Quadrant for Endpoint Management Tools.

- June 2026: Ivanti released its Q2 2026 product update for Ivanti Neurons for UEM, featuring agentic AI capabilities, autonomous endpoint management enhancements, AI Assist for identity governance, and new ARM architecture support, further embedding AI-driven automation into endpoint lifecycle operations.

- April 2026: Ivanti launched Ivanti Neurons for MDM - Sovereign Edition - EU, a cloud-based UEM solution hosted by BSI-certified European infrastructure provider sector27, meeting EU Cloud Sovereignty Framework criteria at SEAL-2 to SEAL-3.

- January 2025: MB Bank received ISO 14064-1 certification for its greenhouse gas inventory report built on the FPT VertZéro platform. The certification demonstrates early BFSI adoption of device-linked environmental reporting infrastructure, a precursor to UEM-integrated ESG compliance workflows.

Global UEM In BFSI Market Report Scope

The UEM in BFSI Market refers to the adoption and implementation of UEM solutions within the Banking, Financial Services, and Insurance (BFSI) sector. The scope of the report includes an analysis of market trends, growth drivers, challenges, and opportunities specific to the BFSI sector. It also examines the deployment of UEM solutions to manage and secure endpoints, streamline operations, and enhance customer experiences.

The UEM in BFSI Market Report is Segmented by Component (Solutions [Device Management, Application Management, Content Management, Security and Compliance Management, and Analytics and Automation], and Services), Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions | Device Management |

| Application Management | |

| Content Management | |

| Security and Compliance Management | |

| Analytics and Automation | |

| Services |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Nordics | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Component | Solutions | Device Management |

| Application Management | ||

| Content Management | ||

| Security and Compliance Management | ||

| Analytics and Automation | ||

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Nordics | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the UEM in BFSI market?

The UEM in BFSI market was valued at USD 1.12 billion in 2025, reached USD 1.39 billion in 2026, and is forecast to reach USD 4.47 billion by 2031 at a 26.32% CAGR.

Why are banks and insurers increasing endpoint management spending?

Demand is being driven by DORA, PCI-DSS compliance, hybrid work, BYOD expansion, and zero trust rollouts that require tighter control over laptops, mobile devices, branch systems, and other endpoints.

Which deployment model is gaining the most traction?

Cloud-based deployment is growing the fastest, with a projected 27.59% CAGR through 2031, because it supports real-time policy enforcement and wider visibility across distributed device estates.

Which buyer group contributes the most revenue?

Large enterprises led in 2025 with 73.68% of revenue, reflecting the complexity of global banking and insurance endpoint fleets across branches, ATMs, shared devices, and remote workers.

Which region is growing the fastest?

Asia-Pacific is expected to expand at a 27.32% CAGR through 2031, supported by digital banking growth in India, fintech integration in China, and mobile-first financial services models across Southeast Asia.

How are vendors trying to stand out in this space?

Vendors are competing through sovereign cloud options, stronger audit support, integrated identity controls, and AI-led automation that improves remediation speed and operational resilience.

Page last updated on: