Healthcare EDI Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

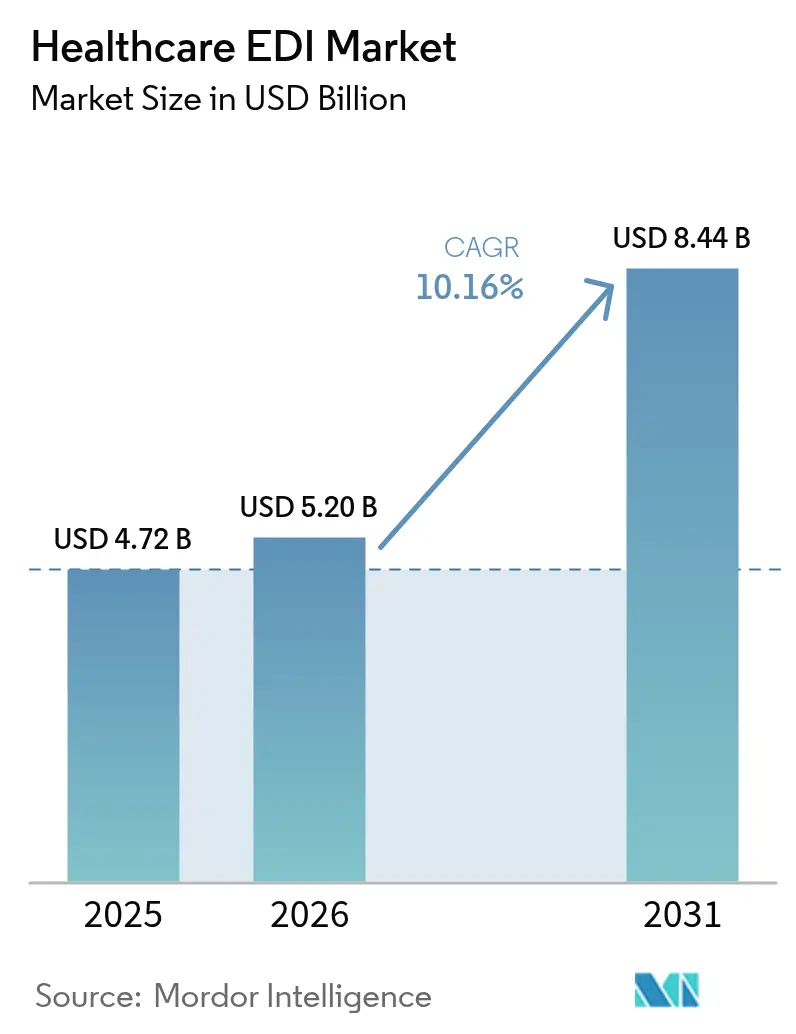

| Market Size (2026) | USD 5.2 Billion |

| Market Size (2031) | USD 8.44 Billion |

| Growth Rate (2026 - 2031) | 10.16% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare EDI Market Analysis by Mordor Intelligence

The Healthcare EDI market size is expected to grow from USD 4.72 billion in 2025 to USD 5.2 billion in 2026 and is forecast to reach USD 8.44 billion by 2031 at 10.16% CAGR over 2026-2031. Growing digitization, cost-containment mandates, and stringent data-exchange regulations are reinforcing adoption across payers, providers, and life-science firms. Widespread cloud migration lowers implementation friction, while the accelerating shift to value-based care creates fresh demand for real-time, multi-party data flows. Heightened cybersecurity awareness following the 2025 Change Healthcare breach further elevates investment in secure, auditable transaction platforms. Vendors that combine interoperability, advanced analytics, and robust compliance tooling are capturing new white-space opportunities as healthcare entities retire fragmented, manual workflows.

Key Report Takeaways

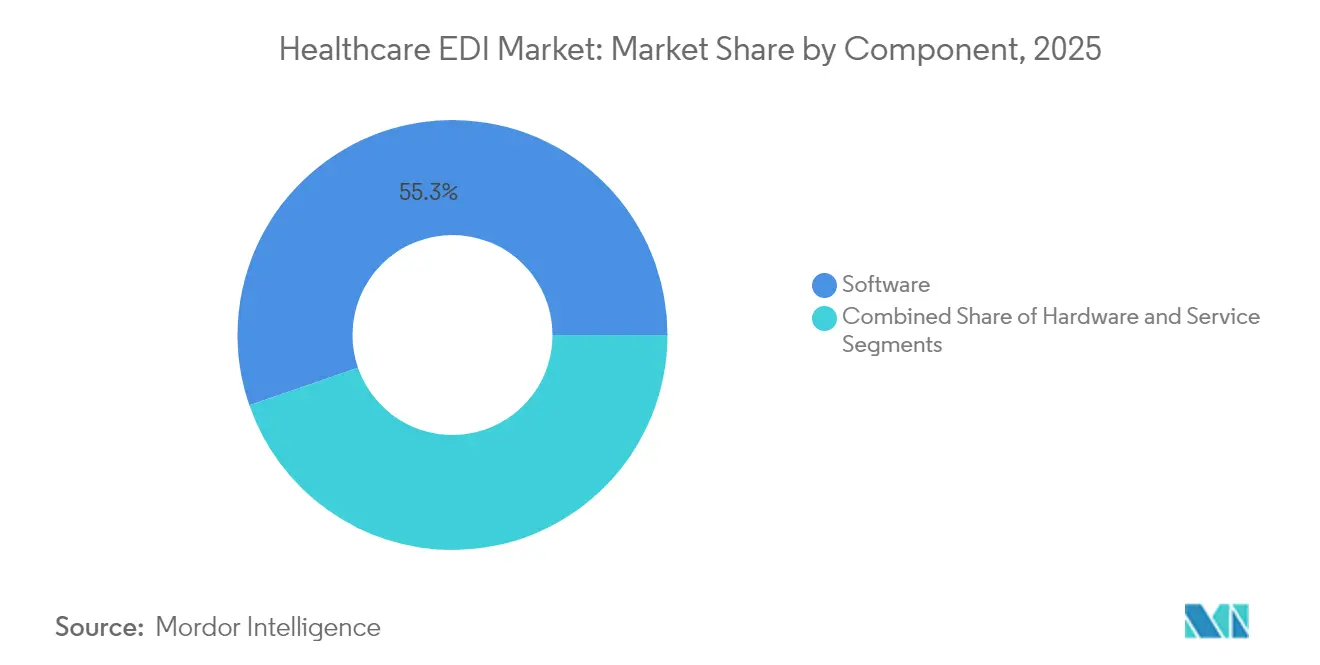

- By component, software retained 55.30% revenue share of the Healthcare EDI market in 2025; services are projected to rise at a 12.22% CAGR to 2031.

- By transaction type, claims management led with 47.60% of the Healthcare EDI market share in 2025, while supply-chain transactions are expected to expand at an 10.92% CAGR through 2031.

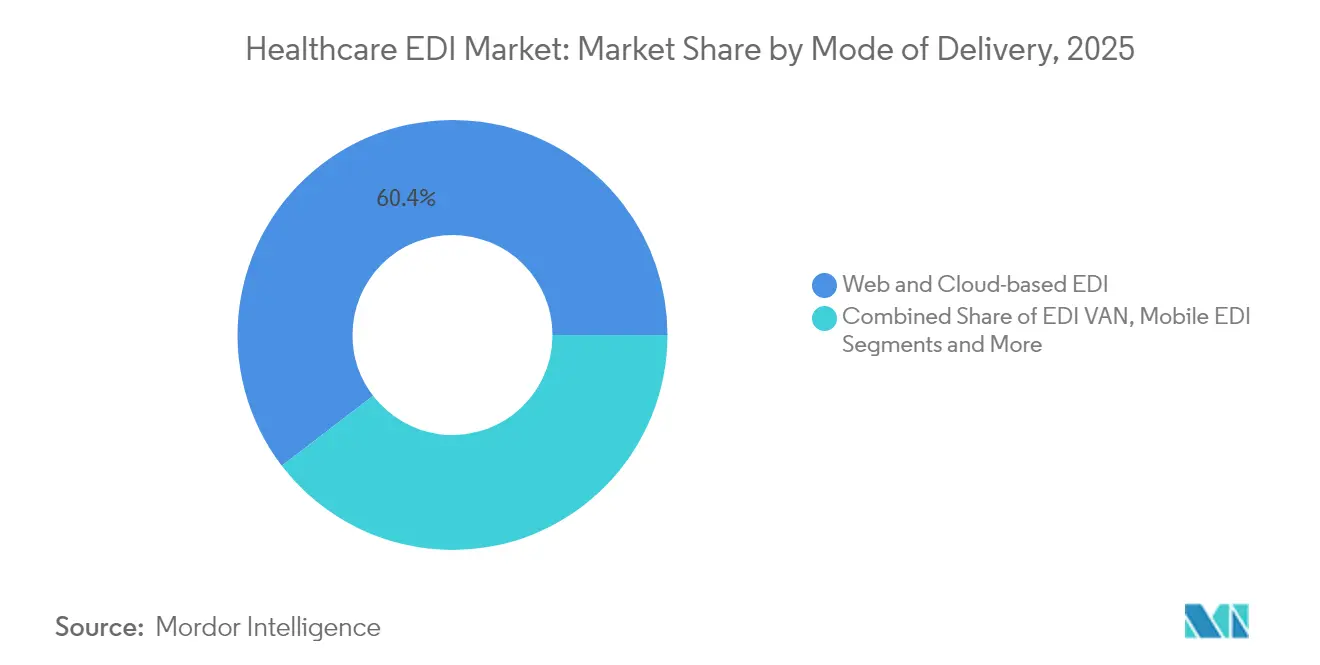

- By mode of delivery, cloud platforms commanded 60.40% share of the Healthcare EDI market size in 2025; mobile EDI is forecast to post a 16.98% CAGR between 2026-2031.

- By end user, providers accounted for 53.30% share of the Healthcare EDI market size in 2025, whereas payers are set to grow the fastest at 13.28% CAGR to 2031.

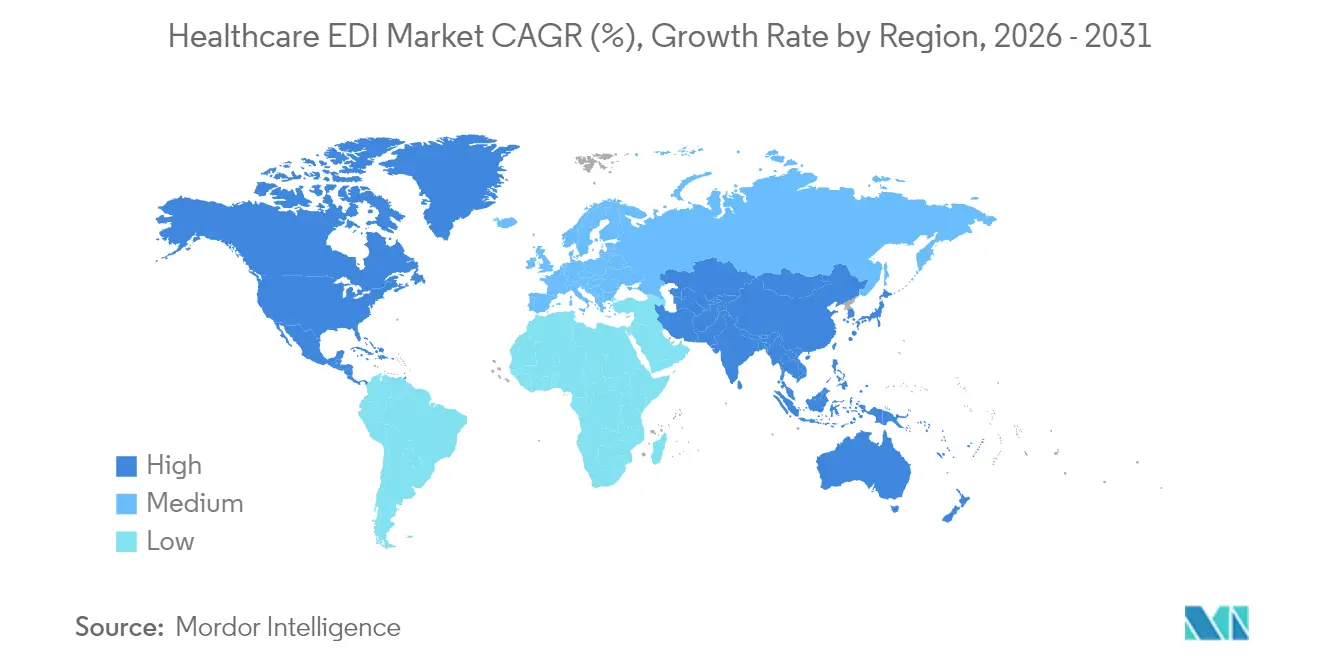

- By geography, North America dominated with 42.60% of the Healthcare EDI market in 2025; Asia-Pacific is poised for the highest regional CAGR of 11.74% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare EDI Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandated HIPAA and global regulatory push | +2.8% | North America, Europe, with growing influence in Asia-Pacific | Short term (≤ 2 years) |

| Rising healthcare cost-containment pressures | +2.1% | Global, with higher impact in mature markets | Medium term (2-4 years) |

| Cloud-enabled SaaS EDI adoption | +1.7% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Shift to value-based care revenue-cycle efficiency | +1.4% | North America, Europe, with gradual adoption in Asia-Pacific | Long term (≥ 4 years) |

| AI-driven auto-coding boosts EDI data integrity | +0.9% | North America, Europe, advanced Asian markets | Medium term (2-4 years) |

| Blockchain payer-provider pilots integrating EDI | +0.6% | North America, select European countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandated HIPAA and global regulatory push

HIPAA transactions remain obligatory in the United States, compelling providers and payers to exchange claims, remittances and eligibility data through standardized EDI formats. CMS deliberations on skipping directly to Version 8010 underscore the urgency of a modernized framework that removes legacy ambiguities[3]healthedge.com/resources/blog/regulatory-highlights-that-health-plans-should-know. Similar mandates in Europe and Asia are converging toward common syntaxes, compressing implementation timelines for multinationals and contributing roughly 2.8 percentage points to the Healthcare EDI market CAGR. Export-driven Asian health-tech vendors, particularly in South Korea and Taiwan, leverage this alignment to gain trading-partner acceptance in North America and the European Economic Area.

Rising healthcare cost-containment pressures

Healthcare organizations save an average of USD 2.7 per electronic transaction versus paper, trimming 82% of processing time. With reimbursement erosion squeezing margins, revenue-cycle managers increasingly view full-suite EDI as a non-negotiable operating requirement. Deployments that automate pre-authorization validation and auto-post remittance data deliver 15-30% cost reductions in administrative cost centers, reinforcing the Healthcare EDI market growth narrative.

Cloud-enabled SaaS EDI adoption

Eighty-seven percent of surveyed health enterprises now favor hybrid cloud. Pay-as-you-go subscription models eliminate large capital outlays, letting hospitals and ambulatory groups adopt the same compliance posture as large IDNs. Automated update cycles keep transaction sets aligned to regulatory changes without disruptive on-prem upgrades, adding 1.7 points to forecast expansion.

Shift to value-based care revenue-cycle efficiency

Bundled-payment contracts require data feeds that combine clinical and financial elements. Modern EDI platforms embed HL7 FHIR resource mapping next to X12 transactions, letting payers reconcile quality scores with financial withholds in a single pass. Early adopters report lower denial rates and faster settlement, securing a 1.4-point uplift to market momentum.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data security and privacy breaches | -1.2% | Global, with higher impact in North America and Europe | Medium term (2-4 years) |

| High implementation and integration cost | -0.9% | Global, with greater impact on emerging markets | Short term (≤ 2 years) |

| Skilled EDI workforce shortages | -0.7% | Global, particularly acute in rapidly growing markets | Medium term (2-4 years) |

| FHIR APIs eroding legacy EDI demand | -0.5% | North America, Europe, advanced Asian markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data security and privacy breaches

The February 2025 Change Healthcare ransomware attack disrupted claims nationwide and forced UnitedHealth Group to advance USD 6.5 billion in relief payments[1]UnitedHealth Group, “Information on the Change Healthcare Cyber Response,” unitedhealthgroup.com. Fallout heightened scrutiny of transaction routing and encryption layers, denting EDI rollout velocity among risk-averse providers and shaving 1.2% points from potential CAGR.

High implementation and integration cost

Complex environments comprising practice-management, EMR and legacy clearinghouse links can drive integration budgets 30-50% above plan. Rural hospitals operating on slim margins frequently defer upgrades, slowing near-term Healthcare EDI market adoption by 0.9 points.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Surge Amid Integration Complexity

Software remained the backbone of the Healthcare EDI market in 2025, generating 55.30% of total revenue as organizations standardized on cloud-ready clearinghouse engines. The services sub-segment, however, is expanding at a 12.22% CAGR through 2031, propelled by scarce in-house expertise and ever-evolving compliance mandates. Consultancies providing mapping, partner onboarding, and 24/7 transaction monitoring fill critical skill gaps for midsize systems pursuing aggressive digital agendas.

Growing reliance on managed services also reflects the rising sophistication of composite workflows that merge X12, HL7 FHIR, and proprietary APIs. Providers are turning to external specialists for data stewardship, exception handling, and continuous testing. The Healthcare EDI market size for service offerings is forecast to eclipse USD 3.25 billion by 2031, while the hardware footprint contracts as virtualized gateways replace rack-based modems.

By Transaction Type: Supply Chain Optimization Accelerates

Claims management held 47.60% revenue share of the Healthcare EDI market in 2025, underlining its centrality in cash-flow preservation. Nevertheless, supply-chain transactions are registering an 10.92% CAGR as health systems exploit EDI to rationalize inventory and tame rising device costs. Automated purchase orders, ASN feeds, and consignment stock alerts trim stock-outs and free working capital, positioning supply-chain EDI as a strategic lever for CFOs.

Interlacing IoT telemetry with EDI message sets offers real-time expiry tracking for temperature-sensitive biologics, reducing waste. This convergence is nudging procurement and biomedical engineering teams into joint governance councils, intensifying demand for integrated network-wide data visibility across the Healthcare EDI market.

By Mode of Delivery: Mobile EDI Disrupts Traditional Models

Cloud deployments captured a 60.40% share in 2025, affirming SaaS as the default onboarding route. Mobile EDI, though starting from a smaller base, is propelling segment growth at 16.98% CAGR. Physicians authorize claims corrections on smartphones while nurses query eligibility from bedside tablets. Flexible, native-app experiences remove the tether to on-prem terminals, aligning clinician workflow with modern mobility norms and reinforcing broader Healthcare EDI market expansion.

Hybrid delivery models now blend lightweight mobile interfaces with centralized cloud processing and established value-added networks for high-volume routing. Resulting architectures cut per-transaction costs yet uphold stringent HIPAA encryption thresholds.

By End User: Payers Accelerate Digital Transformation

Providers represented 53.30% revenue share of the Healthcare EDI market in 2025, relying on high-volume claim submission and remittance advice feeds. Payers, however, are projected to log a 13.28% CAGR as competitive pressures force automation of prior authorization, benefits coordination, and risk-score analytics. Next-generation payer hubs deploy configurable rules to pre-empt denials and feed value-based settlement engines.

Life-science manufacturers increasingly adopt EDI to synchronize production forecasts with distributor demand signals, enhancing lot traceability and shortening recall response windows. These dynamics expand the Healthcare EDI industry ecosystem into adjacent regulatory and pharmacovigilance arenas.

Geography Analysis

North America retained leadership with 42.60% of 2025 revenue, underpinned by HIPAA mandates and mature clearinghouse networks. Nearly all Medicare fee-for-service claims flow electronically, establishing a high baseline for the Healthcare EDI market. The Interoperability and Prior Authorization Final Rule intensifies digital requirements, nudging commercial payers toward automated exception handling and widening the addressable opportunity across smaller provider groups.

Asia-Pacific delivers the fastest growth at 11.74% CAGR, buoyed by rapid health-insurance expansion and extensive government cloud initiatives in China, India, and Indonesia. Mobile-first adoption allows clinics to bypass legacy modem infrastructure, accelerating penetration. Mandatory e-invoicing rules in economies such as South Korea cascade into accelerated healthcare data-exchange spending, lifting the regional Healthcare EDI market size toward USD 1.78 billion by 2031.

Europe showcases diverse adoption curves. Germany scales unified procurement exchanges within its DRG reimbursement framework, while the United Kingdom prioritizes cross-border EHR linkages that convert clinical events into billing-ready EDI stubs. Scandinavia benefits from nationwide electronic ID systems that streamline patient eligibility checks. Collectively, these initiatives maintain Europe’s role as the second-largest regional contributor to the Healthcare EDI market revenue.

Regulatory Landscape

In the United States, healthcare EDI is anchored to HIPAA Administrative Simplification standards and the operating rules maintained by CMS and HHS, including ASC X12 Version 5010 for core administrative transactions (such as claims and eligibility) and NCPDP D.0 for retail pharmacy drug claims. A major 2026 update is CMS-0053-F, finalized in the Federal Register and effective May 26, 2026, which establishes the first HIPAA-adopted standards for health care claims attachments using HL7 C-CDA and HL7 Attachments implementation guides. An industry compliance date is set for May 26, 2028.

Policy activity also continues to pull prior authorization deeper into standardized digital exchange. In April 2026, CMS released the Interoperability Standards and Prior Authorization for Drugs proposed rule, extending electronic prior authorization requirements for drugs and introducing API-related reporting expectations, which adds new compliance-driven work for payer and provider workflows. In parallel, the ONC/ASTP HTI rule series continues to evolve, with HTI-2 focusing on administrative updates and TEFCA-related alignment, reinforcing convergence of EDI transaction compliance with broader interoperability governance.

Value Chain Analysis

The healthcare EDI value chain begins with standards bodies and regulators that define transaction and interoperability requirements (for example, CMS and ONC/ASTP via HIPAA adopted standards, TEFCA alignment, and health IT certification rules). EDI platform vendors, clearinghouses, and value-added networks then convert these requirements into routing, mapping, validation, security, and audit capabilities, typically delivered as cloud software and managed services. Downstream participants include payers, providers, and life-sciences and supply-chain partners, such as manufacturers, distributors, and GPO-linked procurement ecosystems that exchange X12 and related messages for claims, eligibility, remittance, and supply-chain execution.

Implementation and operations are supported by systems integrators and specialized services providers that handle trading-partner onboarding, mapping updates, testing, and exception management, which becomes more prominent as organizations blend X12 with FHIR translation and attachment workflows. Regulatory milestones are reshaping workflow handoffs, including the March 2026 finalization of HIPAA-adopted electronic claims attachment standards and the October 2025 effective date of ONC/ASTP HTI-4, which includes certification criteria for electronic prior authorization and e-prescribing. Together, these dates increase demand for continuous compliance updates, automated testing, and stronger transaction validation across the chain, while new entrants target mapping and validation bottlenecks with AI-enabled automation platforms that shift operations from batch, legacy-heavy approaches toward more real-time, software-driven transaction governance.

Competitive Landscape

The competitive arena remains moderately consolidated. UnitedHealth Group’s 2022 purchase of Change Healthcare fused the largest clearinghouse with Optum’s analytics portfolio, giving the combined entity roughly three-quarters of first-pass claims-editing throughput. Edifecs counters through cloud-native EDI gateways that bundle AI-driven exception triage and blockchain-ready audit trails, while Experian Health leverages its credit-data roots to refine patient estimate workflows[2]Edifecs, “Edifecs Introduces Healthcare Interoperability Cloud,” edifecs.com.

Strategic alliances surface as a preferred scale pathway. Edifecs and HealthEdge integrate claims-adjudication engines with an eye on payer flexibilities. OpenText deepens reseller arrangements with major EMR platforms to embed secure messaging protocols. Start-ups focused on FHIR-over-EDI translation attract venture funding as interoperability rules converge.

Product roadmaps pivot hard toward cybersecurity, threat analytics, and zero-trust architectures. Vendors publicize SOC 2 Type II certifications and real-time anomaly detection modules, differentiators amplified by the Change Healthcare incident. Interoperability clouds that abstract transaction formats allow multinationals to harmonize claims flows across 20+ country codes without bespoke local stacks, shaping the next battleground in the Healthcare EDI market.

Healthcare EDI Industry Leaders

Change Healthcare

Optum Inc.

McKesson Corporation

Experian Health

Cognizant

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The move to HIPAA-adopted electronic claims attachments creates a modernization lane for EDI platforms that can operationalize attachment assembly, clinical-document packaging, and auditable exchange across payers, providers, and clearinghouses. With CMS-0053-F effective May 26, 2026 and compliance required by May 26, 2028, organizations that still rely on fax, portals, or manual document workflows need production-grade support for the adopted standards. This includes X12 transactions used in attachment workflows and HL7 C-CDA-based clinical content, which lifts demand for mapping services, partner onboarding, and attachment-focused validation tooling.

A second opportunity sits at the EDI-to-API convergence point for prior authorization and administrative exchange. CMS and ONC have proposed expanded electronic prior authorization requirements for drugs and additional interoperability and API expectations, while ONC Standards Bulletin 2026-1 (January 29, 2026) outlines updates to USCDI, including USCDI v7 work, alongside a standards lifecycle posture that includes proposed sunsets (for example, an ONC-proposed January 1, 2028 expiration date for certain currently adopted versions). These dated compliance roadmaps increase the value of cloud EDI platforms and managed services that bundle continuous standards updates, FHIR-to-X12 translation where required, and measurable transaction monitoring, particularly for payers and providers aiming to reduce administrative friction while meeting auditable exchange requirements.

Recent Industry Developments

- June 2026: CMS issued Transmittal R13816OTN detailing updates to the HIPAA EDI Front End, with implementation scheduled for October 5, 2026. The update cadence signals ongoing federal operational changes that clearinghouses and trading partners must absorb through testing, mapping maintenance, and release management.

- April 2026: One Call completed its acquisition of Data Dimensions, adding EDI and clearinghouse capabilities to its healthcare ecosystem infrastructure. The deal supports consolidation of transaction, documentation, and related administrative workflows under fewer platforms, tightening competitive pressure on standalone EDI service providers.

- December 2024: The Maryland Health Care Commission released a report on EDI adoption in healthcare and highlighted that most claims are submitted electronically under HIPAA standards, including very high Medicare electronic submission levels reported for 2023. The publication reinforced the maturity of claims EDI while underscoring remaining whitespace in areas where documentation and attachments still impede full electronic completion.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is sized as the revenues earned from healthcare-focused EDI software and services that enable standards-based electronic exchange of administrative and financial transactions between payers, providers, and related partners.

Scope exclusions: Supply-chain EDI and custom in-house integration tools that are not aligned to common healthcare EDI messaging standards are not counted.

Segmentation Overview

- By Component

- Software

- Hardware

- Services

- By Transaction Type

- Claims Management (837/835)

- Healthcare Supply-Chain (810/856)

- Others (Referral, Authorization, and more)

- By Mode of Delivery

- Web and Cloud-based EDI

- EDI VAN

- Mobile EDI

- Other Modes of Delivery

- By End User

- Healthcare Providers

- Medical Devices and Pharmaceutical Industry

- Payers

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Middle East and Africa

- GCC

- Israel

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia

- New Zealand

- Rest of Asia-Pacific

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the transaction and compliance backbone that drives EDI usage in healthcare, then linking that activity to spend. We review public healthcare administrative standards references and operating rules, and we also use payer and provider disclosures to understand adoption direction and budgeting priorities.

Source types used include, for example, US CMS publications and data releases, National Library of Medicine indexed research, HL7 and ASC X12 public documentation, OECD health statistics for cross-country context, and selected government health department releases where available. To anchor company level revenue context, we also use annual reports, investor presentations, reputable press, and a paid subscription focused on company financials and news, plus a paid patent database to track activity signals around EDI related workflows. These examples are not exhaustive, and many other public and paid sources were also reviewed to collect, validate, and clarify inputs.

Primary Interviews and Surveys

Primary work is used to convert adoption talk into practical sizing inputs, especially where pricing, contract structure, and delivery model mix varies by region. We speak with a balanced set of respondents across solution delivery, payer and provider operations, and implementation partners across APAC, EMEA, and the Americas. This helps confirm which transaction types are actually monetized and how renewal cycles influence run-rate revenue.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 14% | APAC: 42% |

| Mid tier: 46% | Functional/Unit leaders: 40% | EMEA: 36% |

| Smaller Players: 15% | Managers: 46% | Americas: 22% |

Market-Sizing & Forecasting

Sizing is built using both top-down and bottom-up checks, so the final number stays realistic even when public data varies across regions. On the top-down side, we use healthcare administrative digitization indicators and transaction standardization signals to reconstruct an addressable EDI spend pool, then translate it into market value using adoption and pricing assumptions by delivery model.

In the model, a few practical inputs do most of the work, such as the mix shift toward cloud subscriptions versus license and maintenance, the share of EDI traffic routed via clearinghouses versus direct links, typical implementation and managed services attach rates, and the pacing of regulatory and payer policy changes that move transaction volumes. Forecasts rely on scenario analysis supported by expert consensus on how quickly cloud migration and automation will change pricing per connection and services intensity over time. Bottom-up approximations are then used as guardrails, including sampled ASP-per-customer ranges applied to estimated active payer and provider counts, followed by channel checks on implementation throughput where data gaps exist.

Data Validation & Update Cycle

Model outputs are cross-checked against independent signals, and any sharp swings are investigated before numbers are finalized. When a variance shows up, assumptions are revisited in steps, starting with pricing logic, then delivery model mix, and then transaction intensity. If the gap is material, respondents are re-contacted.

Each report is refreshed annually, and interim updates are made when a major regulatory change, pricing reset, or macro event alters buying behavior. Before delivery, we run a final pass to reflect the latest public releases and ensure currency timing and inflation effects have been handled consistently across regions.

Mordor Intelligence's Global Healthcare Edi Market Market Size Compared With Other Published Estimates

It is normal to see different market sizes for healthcare EDI because studies do not always count the same revenue streams, and the timing of exchange rates and pricing updates can shift totals even when the overall narrative sounds similar. Differences also come from whether the analyst treats implementation services as one-time revenue or spreads them using contract duration assumptions.

In this report, the biggest gap drivers are usually whether supply-chain style EDI is mixed into healthcare administrative EDI, how cloud subscription ASP changes are carried forward year to year, and how often the model is refreshed when payers and providers re-price contracts. A refresh-led approach that re-tests FX timing and ASP movement using recent contract and adoption signals is what keeps the 2025 estimate aligned to the run-rate view used by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.72 B (2025) | |

| Industry Publisher A | USD 4.99 B (2025) | Uses a broader ecosystem view and tends to include adjacent end users beyond payer-provider administration, which can pull in extra services revenue and raise the 2025 total. |

| Industry Publisher B | USD 4.83 B (2024) | Anchors the base year at 2024 and carries forward a single growth path over a longer horizon, so currency timing and contract repricing effects are not re-checked as frequently when rolling into 2025. |

Across the three numbers, the spread mainly tracks scope boundaries and the timing mechanics behind price and currency conversion, rather than a disagreement that EDI demand is growing. By keeping the steps traceable to delivery model mix, ASP progression, and validation touchpoints, the resulting market size stays easier to reproduce and update when conditions change.

Key Questions Answered in the Report

What is driving the double-digit growth of the Healthcare EDI market?

Cost-containment mandates, HIPAA and global regulatory pressures, cloud affordability and the shift to value-based care collectively underpin the 10.16% CAGR forecast to 2031.

Which component segment is expanding the fastest?

EDI services, covering implementation, integration and managed operations, are growing at 12.22% CAGR as organizations outsource complex technical tasks.

How large is the North American Healthcare EDI market relative to other regions?

North America holds 42.60% of total 2025 revenue, more than double the share of any other region due to long-standing regulatory mandates and mature clearinghouse networks.

Which is the fastest growing region in Healthcare EDI Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Why are payers increasing their EDI investment?

Heightened competition and the need to cut administrative overhead are pushing payers toward automated claims adjudication and real-time prior authorization, fueling a 13.28% CAGR.

How is the Change Healthcare cyberattack influencing vendor selection criteria?

The February 2025 breach sharpened focus on encryption, zero-trust architectures and independent failover pathways, prompting buyers to prioritize vendors with demonstrable security certification.

What role will mobile EDI play by 2031?

Mobile usage is forecast to rise at 16.98% CAGR, enabling clinicians to execute eligibility checks and claims corrections at the point of care, further broadening EDI ubiquity across care settings.

Page last updated on: